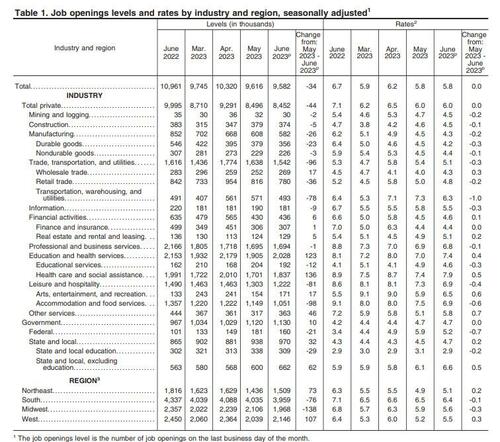

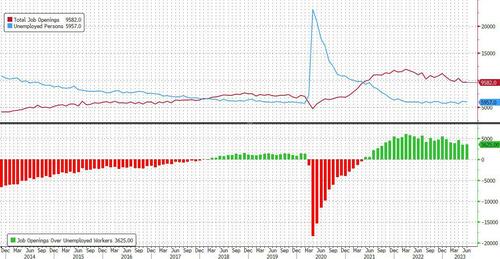

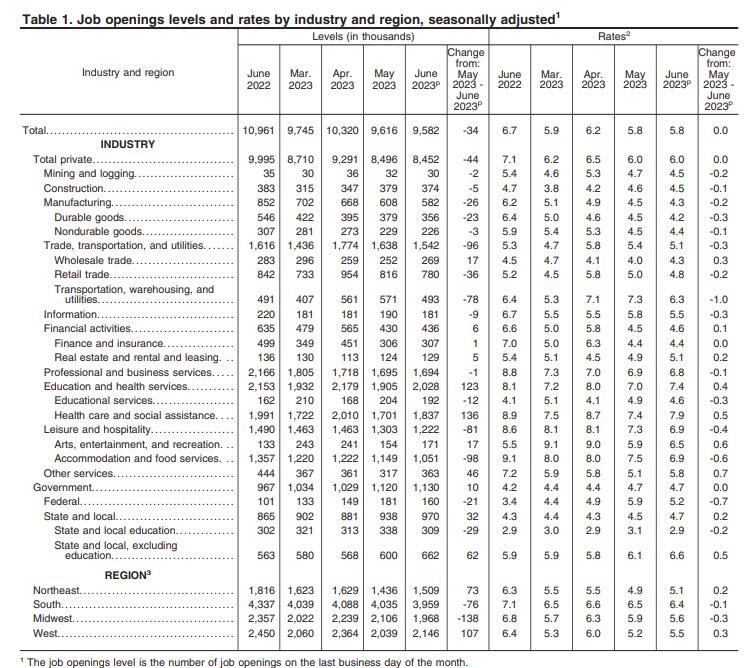

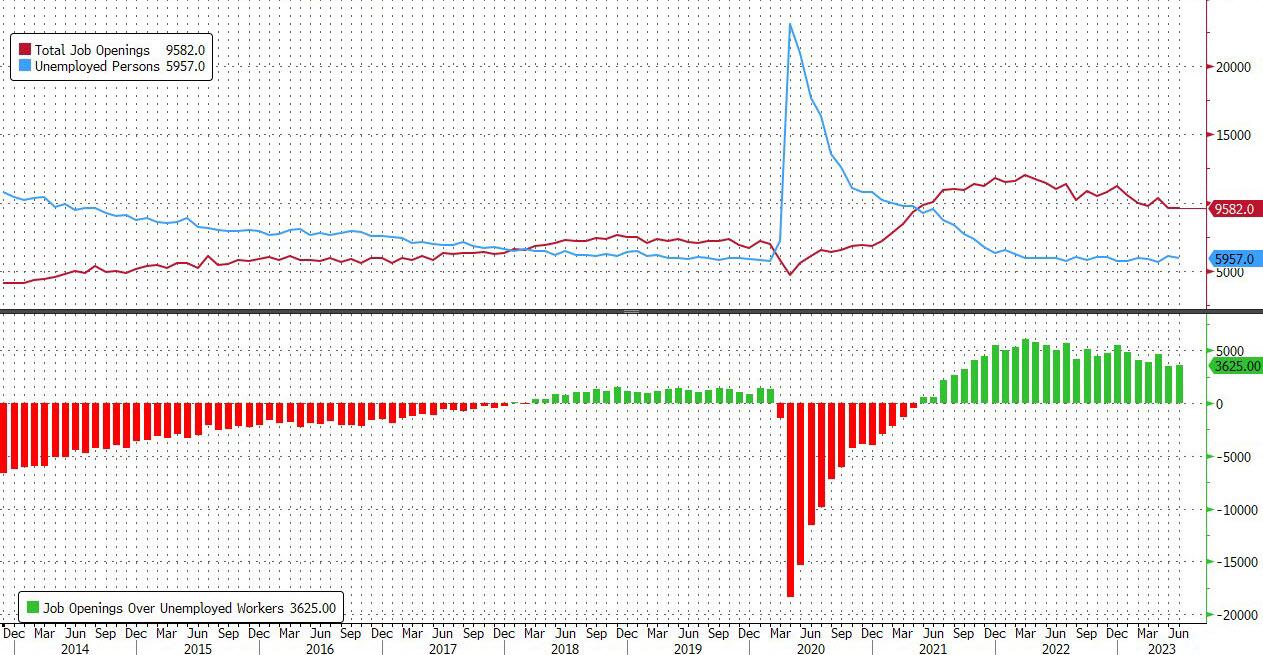

The number was about 1.4 million below the 11 million from a year ago and below the consensus estimate of 9.6 million, a rare miss in a series which has been best known for decisively beating Wall Street’s expectations.

According to the BLS, the largest increases in job openings was in health care and social assistance (+136,000) and in state and local government, excluding education (+62,000). Job openings decreased in transportation, warehousing, and utilities (-78,000), state and local government education (-29,000), and federal government (-21,000)

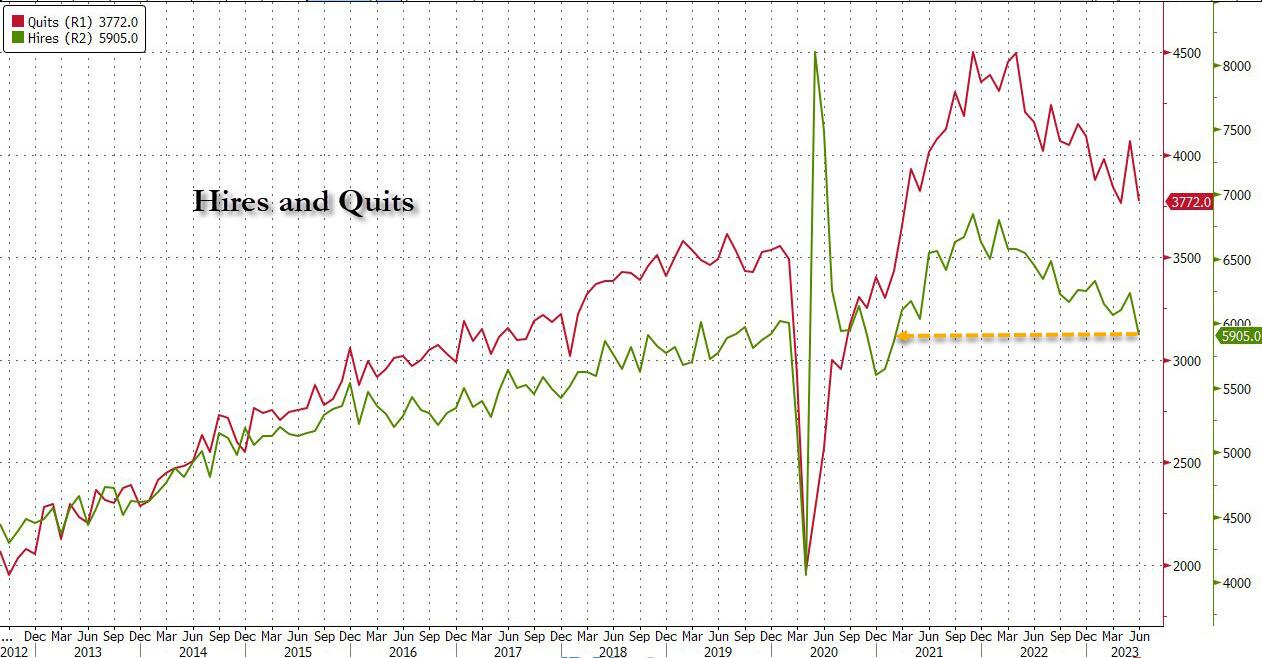

The slide in the number of job openings meant that after rising to the highest since January 2023 in April, in June the number of job openings was just 3.7625 million more than the number of unemployed workers, the lowest since Sept 2021.

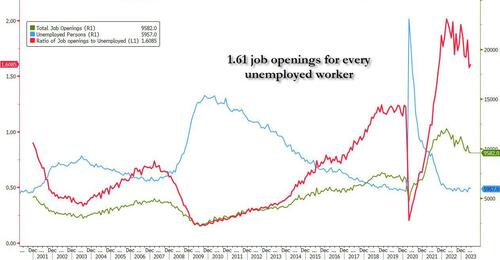

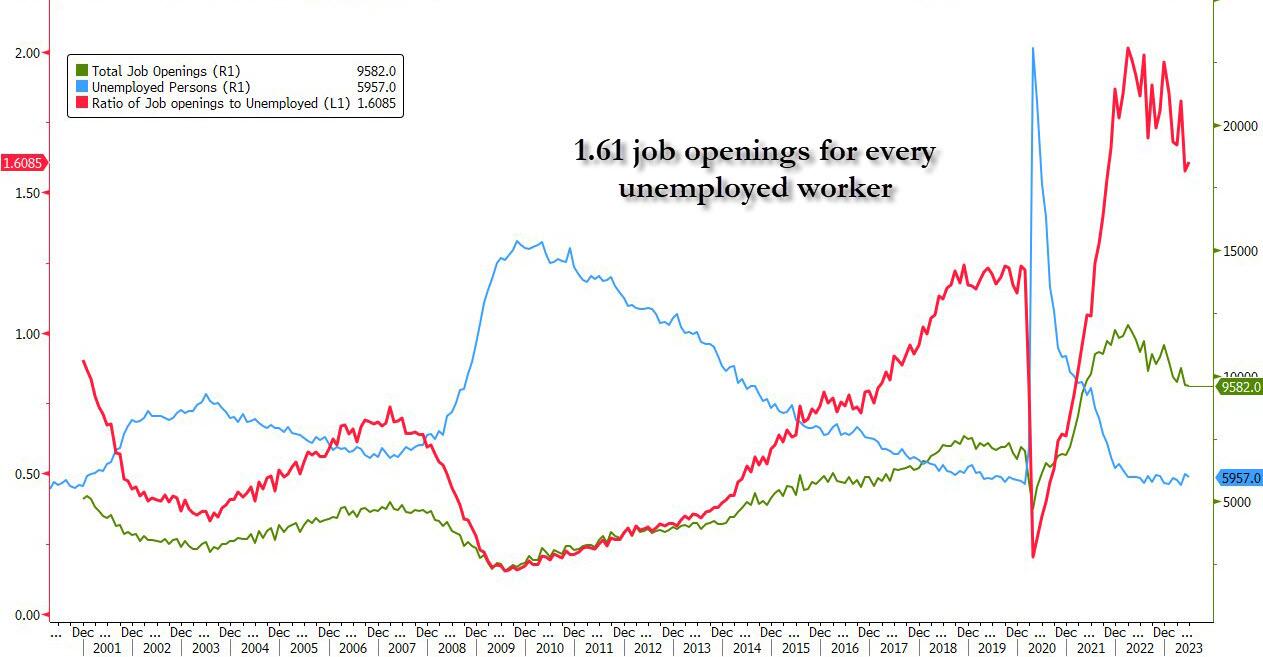

Said otherwise, after rising to 1.82 openings for every worker in April, in June the number dropped to just 1.61, which would have been the lowest level since Oct 2021 if it weren’t for last month’s sharp downward revision.

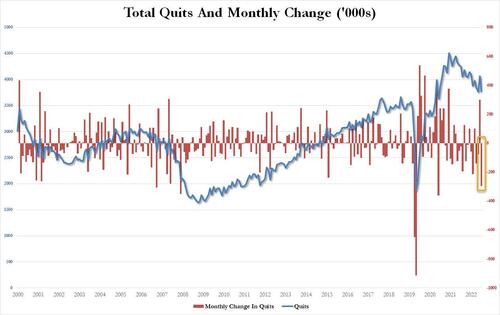

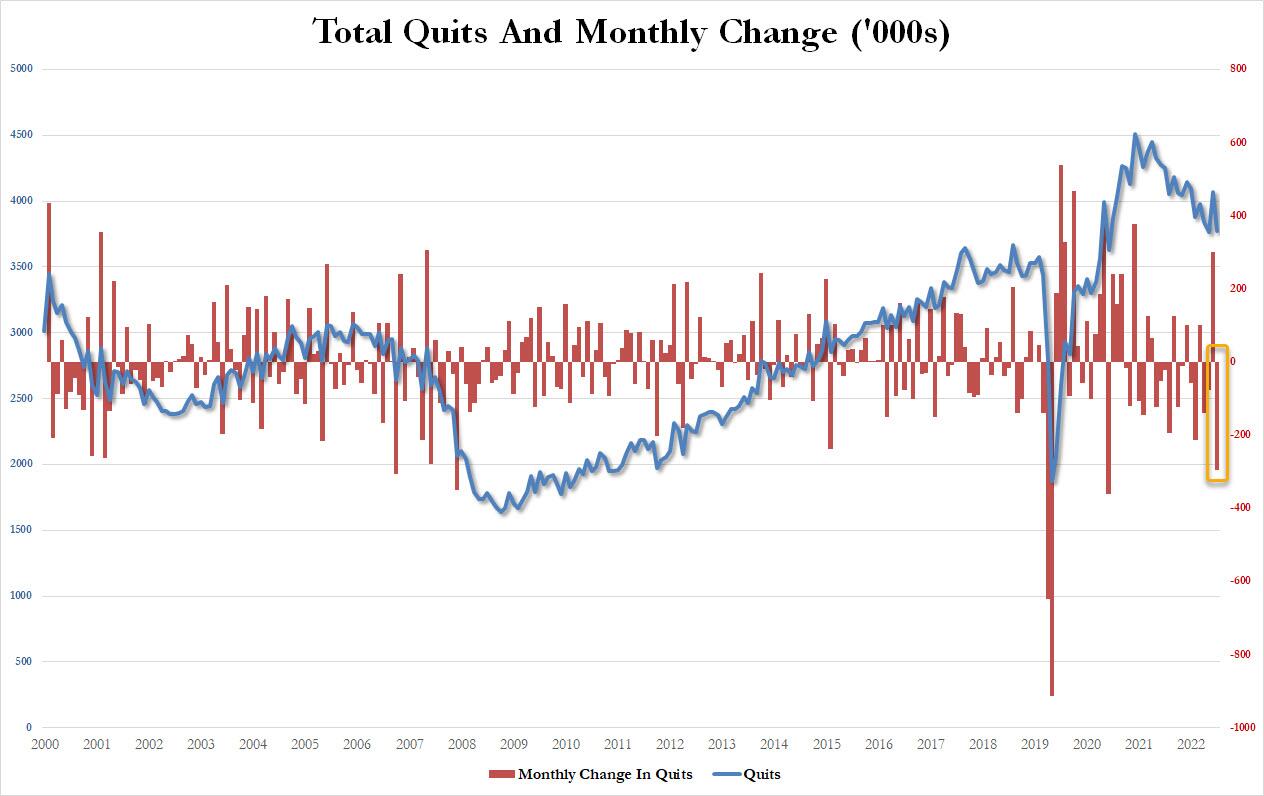

Yet even as the number of job openings dropped only modestly from the (sharply) downward revised print for May (because under Biden, no number is ever revised stronger), conflicting data remained and in June, the number of people quitting their jobs – an indicator traditionally associated with labor market strength as it shows workers are confident they can find a better wage elsewhere – unexpectedly tumbled by 295K to just 3.772MM, the biggest monthly drop since May 2021.

According to the BLS, the number of quits decreased in several industries, with the largest decreases in retail trade (-95,000), health care and social assistance (-75,000), and construction (-51,000). The number of quits increased in arts, entertainment, and recreation (+20,000).

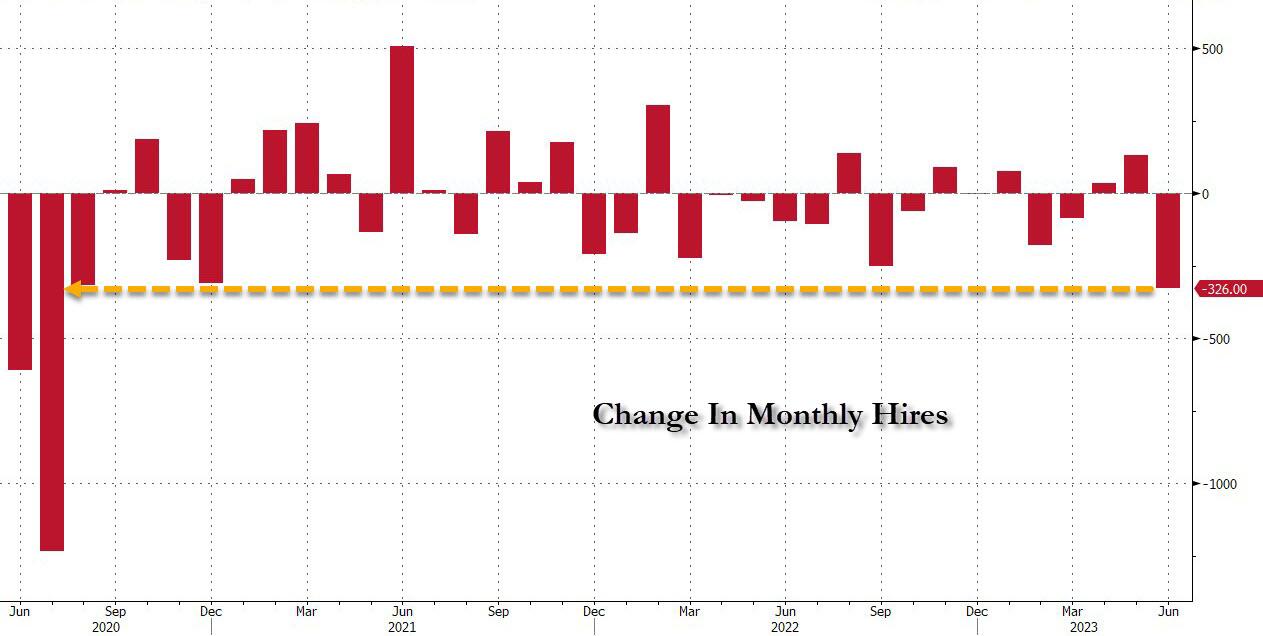

And just in case some still believe Biden’s strong jobs lie, the number of hires also tumbled in June, crashing by 326K – the biggest monthly drop since July 2020…

… to 5.905MM, the lowest since February 2021.

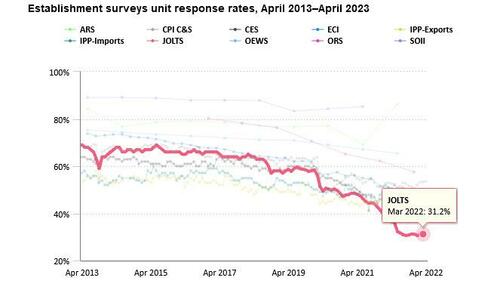

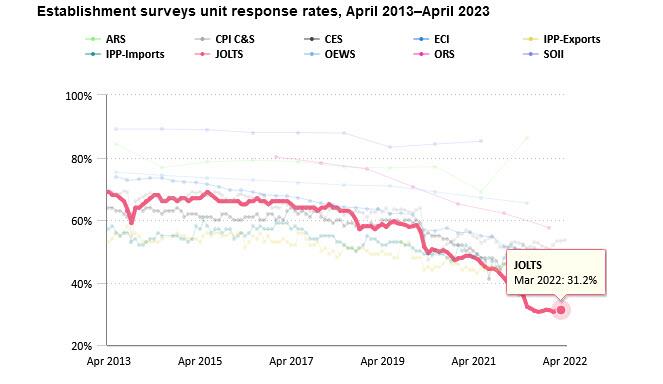

Of course, as we have explained on multiple occasions previously, none of the above data actually matters or is credible for the simple reason that the response rate of the JOLTS survey is stuck at a record low 31.2%. Which means that only those who actually have job openings to report do so, while two-thirds of employers are either non-responsive or their mail is quietly lost in the mail.

Joe Biden said that Republicans will impeach him in the House of Representatives since inflation is coming down. Huh? No Joe, it is because your are the most corrupt President in history, a compulsive liar and your economic policies are pure World Economic Forum mandates (open borders, Central Bank Digital currency, green energy, etc). Biden started off his Presidency by declaring war on fossil fuels that helped drive prices through the roof. And the middle class are paying the price.

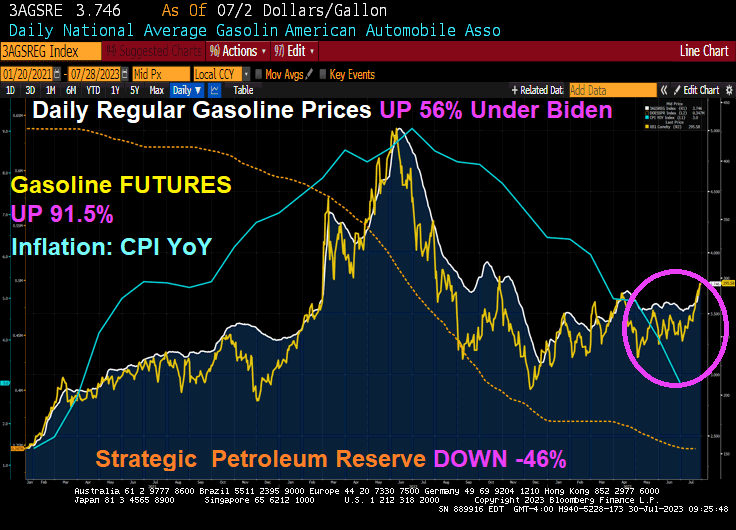

But as inflation cools (blue line) thanks in part to Biden draining the Strategic Petroleum Reserve (orange line), Biden can gloat. But remember, gasoline prices remain 56% higher under Biden’s Reign of Error. Even worse, gasoline FUTURES are up 91.5% under Biden. Yikes!

But look at how gasoline prices and gasoline futures have risen in July (pink circle). The last inflation report showed that inflation has declined to 3% (still higher than The Fed’s 2% target), gasoline prices are up almost 5% since July 19, 2023.

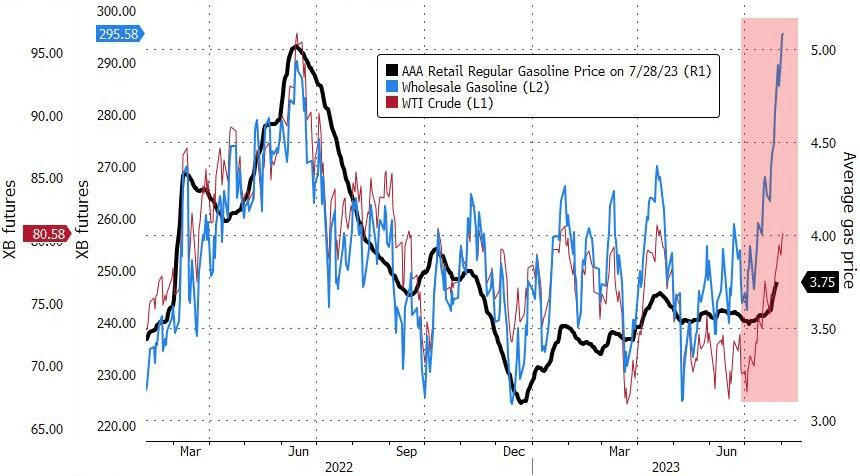

Gasoline, meanwhile, started the year at less than $2.50 per gallon. This week, gasoline topped $2.90 per gallon and may yet reach $3.

WTI Crude Oil futures have broken through the $80 barrier … again. Heating oil futures are up 1.43% today with WTI Crude futures up 0.61%.

So as energy prices keep rising (and Biden’s EPA keeps issuing green energy edicts and fails to recognize that our power grid can’t support all the electric cars and trucks envisioned by the Obama/Biden green dreamers). As such, energy prices will keep rising and with it … inflation.

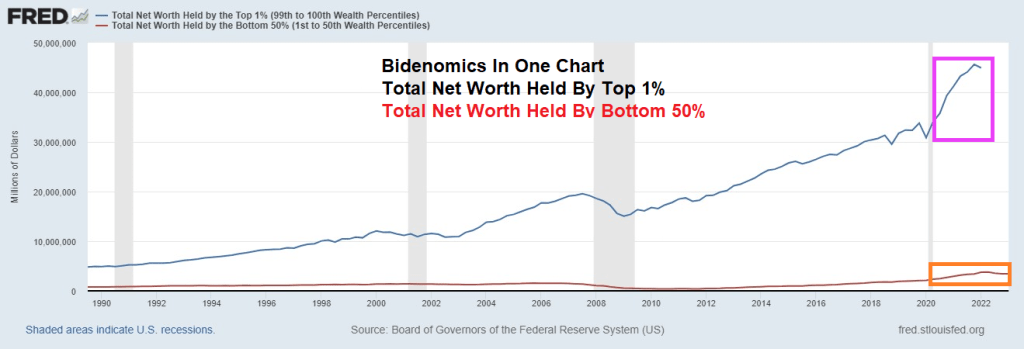

Commercial real estate (CRE), particularly office space, reminds me of the Arthur Brown tune “Fire!” except that Jerome Powell of The Federal Reserve is the God of Hellfire! While fighting inflation caused by … The Federal Reserve and insane Federal spending (aka, Bidenomics). Call this the Over, Under, Sideways Down economy. The top 1% are doing quite well, while the lower 50% of net worth households are struggling.

The Q1 2023 NCREIF Office property (value) index shows declining office value since Q2 2022 as The Fed began raising its target rate to combat inflation.

From Trepp, we have this shocking table showing the decline the average total value loss over the span of around a decade. The oldest buildings experienced the largest reduction in value of 60%, and the newest experienced the least (but quite substantial) reduction of 52%. Although the newest buildings performed the best relatively, their 52% value reduction is easily the most concerning, and displays truly how much distress is present in the office sector. This group has the highest percentage of Class A buildings, but its reduction value over the past decade is still approximately on par with buildings constructed over half a century prior. With north of $150 billion in securitized maturities beyond 2023, these trends set a gloomy tone for their future and the performance of office properties as a whole.

Then we have this alarming headline from Trepp: “Commercial Mortgage Sector Faces Another Wall of Maturities as $2.75 Trillion Rolls by 2027.” An estimated $528.7 billion of commercial mortgages mature this year, according to Trepp data, which projects that next year, maturities will increase to $532.8 billion. The projections are based on data for the first quarter compiled using the Federal Reserve’s flow of funds and made various assumptions regarding loan terms for each of the major lender categories. The data would indicate that the market is facing a wall, if not a mountain of maturities that would make the 2015-2017 wall of maturities look almost inconsequential. During that period, roughly $1.1 trillion of loans were scheduled to come due. But attention was focused on the CMBS market, as more than $335 billion of loans were set to mature during the period.

Well, REAL gross domestic income fell -0.8% YoY in Q1 2023 as M2 Money growth crashes. Not a good sign for the US economy or commercial real estate.

Of course, office properties are suffering from almost out-of-control crime in major American cities and the desire of workers to work from home rather than commute to work in cubicles.

But never fear! We have massively corrupt and compulsive liar Joe Biden as President!! He is the President of The 1%! Not the other 99%.

Bidenomics, massive spending on green energy mandates while curbing fossil fuel consumption, has been a true wonder for the top 1% of net worth (let’s call them The Elites). And Bidenomics, like Obamanomics, relied on super generous Federal Reserve money printing.

The result? Total Net Worth held by the top 1% has grown rapidly since the Covid outbreak and Fed monetary expansion (plus Congress going wild spending). The bottom 50%? They improved in terms of net worth

So, The Elites (top 1%) want The Fed to keep on printing money, since their net worth soars.

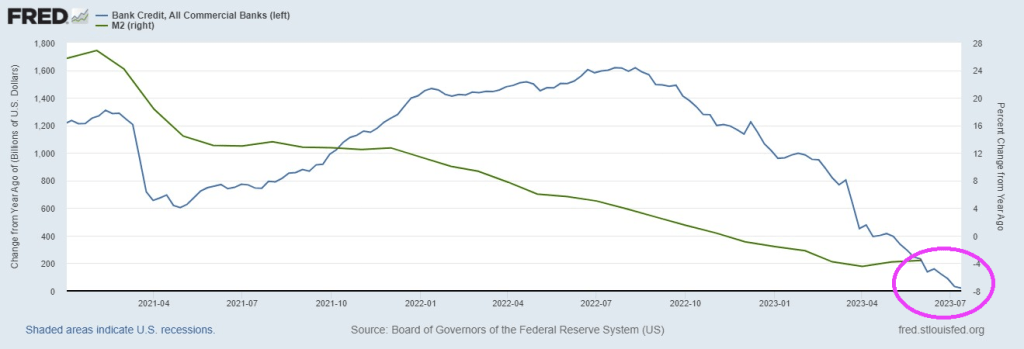

Meanwhile, US bank credit is crashing as The Fed slows M2 Money growth.

Not only is credit growth grinding to a halt, but unrealized losses on bank investment securities continues to worsen.

If you didn’t see this, then check out House testimony of extraterrestrial visitations to Earth. This has been happening since the 1950s (allegedly), so why NOW is there sudden interest in aliens? Deflection away from the horrible scandal of Biden taking money from foreign actors? Likely answer? Biden and Mayorkas will send Treasury Secretary Janet Yellen to negotiate with alien invaders giving them anmesty, free school, free food, free healthcare and directions on how to register to vote. And giving aliens preferential trade status. All for “10% for The Big Guy!”

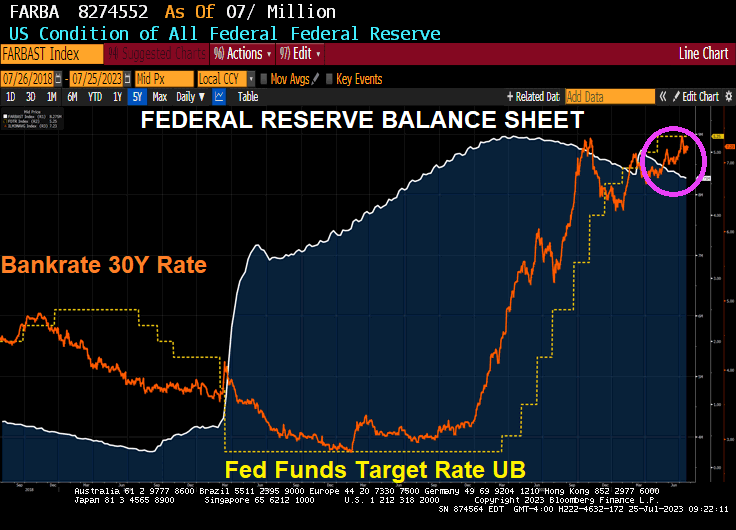

Both The Federal government and Federal Reserve went wild with stimulus surrounding the Covid economic shutdown in 2020. The excessive reaction function is still working its way through the economy and we finally got Q2 Real GDP QoQ of 2.4%! But seriously, is that all we got from an increase in public debt of 39% since January 2020, and M2 Money increased 36%. And, of course, The Federal Reserve double their balance sheet from 2020 to today … and are slow walking its removal. So, with Biden’s insane green spending and Powell’s monetary stimulytpo, all we got was 2.1% Real GDP growth YoY??

And US public debt to GDP is now over 120%, thanks in part to Federal spending and Fed monetary stimulus related to the Covid economic shutdowns.

New home sales in June fell -2.5% from May to June to 697k units sold. But on a year-over-year (YoY) basis, new home sales are up 23.8%. Thanks largely to The Federal Reserve slow walking the shrinking of their massive balance sheet.

Too much monetary stimulus and The Fed’s failure to remove the Covid stimulus is now hitting new home sales.

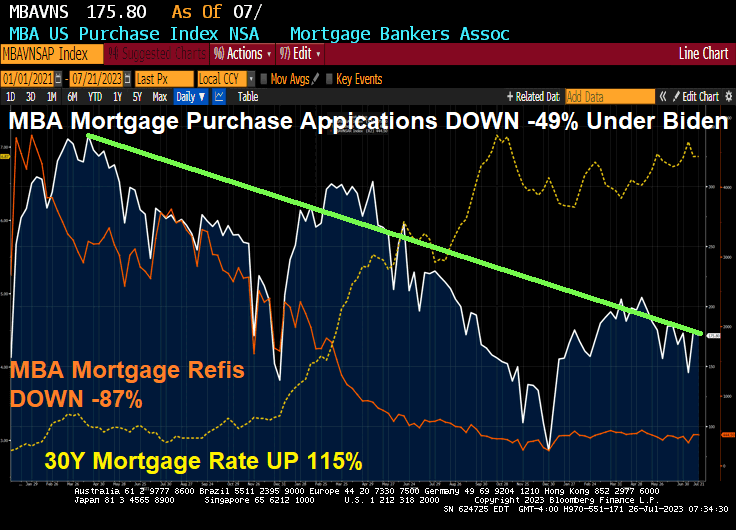

Mortgage applications decreased 1.8 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending July 21, 2023.

The Market Composite Index, a measure of mortgage loan application volume, decreased 1.8 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index 1.5 percent compared with the previous week. The Refinance Index decreased 0.4 percent from the previous week and was 30 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 3 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 23 percent lower than the same week one year ago.

Since April 2021, purchase mortgage demand is down -49%, refi mortgage demand is down -87% as mortgage rates are up 115%.

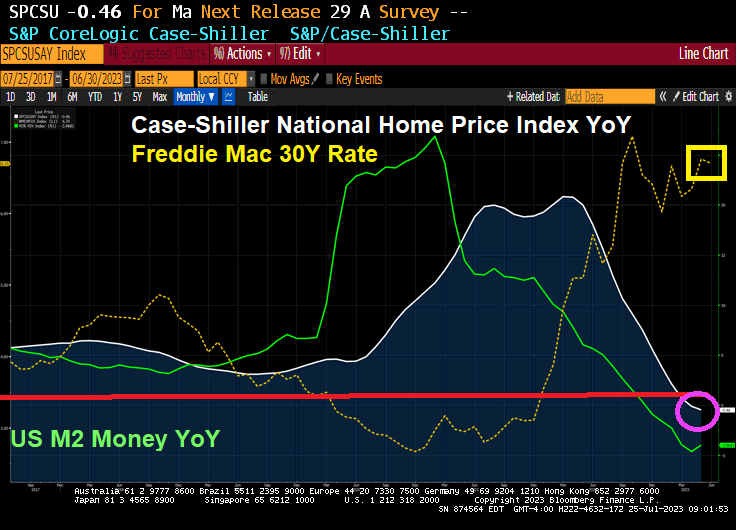

The Case-Shiller home price numbers are out for May. The national home price index is down -0.46% YoY as The Fed slows M2 Money growth into negative growth territory. No doubt Biden (and Karine Jean-Pierre) will take credit for slowing home price growth, although The Federal Reserve slowing monetary stimulus is mostly responsible.

The Fed is still slow walking shrinking its enormous balance sheet. Although The Fed is cranking up their target rate.

The Taylor Rule suggests a 10.42 target rate to cool inflation. They are only half way there!!!

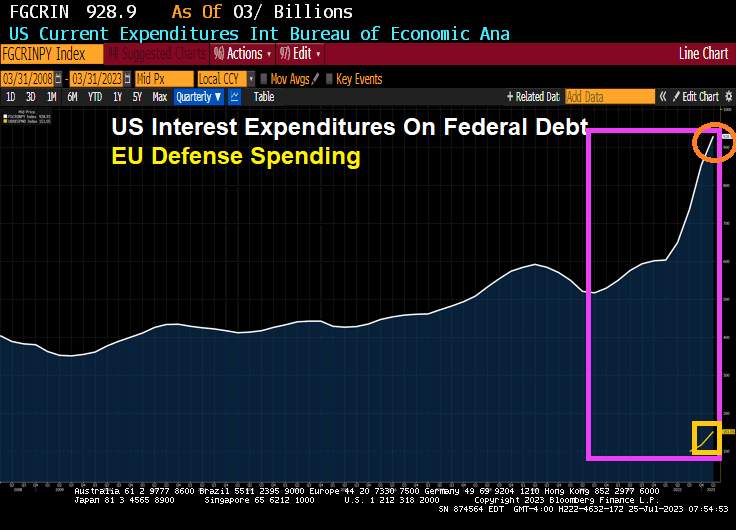

How badly has Bidenomics and generally Federal spending has crippled the US? An example. The interest on US Federal debt is approaching $1 TRILLION (and Biden/Democrats REFUSE to cut any spending, not that Republicans are much better). To show up how messed up this is, the EU’s defense budget (remember Ukraine?) is far smaller that the US interest payments on their debt. That is, US interest payments alone on the massive Federal debt of over $32 trillion is over 6 times larger than the entire defense budget for the European Union!

How this all works, considering the nation’s technically insolvent, is quite miraculous. But it works, nonetheless. Again and again, the Treasury borrows money. And Washington spends it.

Yellen likely knows that full faith and credit is too good to be true. The U.S. government’s gross fiscal mismanagement should call the veracity of its notes into question. But why focus on it when there’s an abundance to be acquired from weekly Treasury bill auctions?

On a recent trip to China, Yellen was spotted by a local food blogger consuming a plate of magic mushrooms. An aide to Yellen later confirmed that she did, indeed, order them. The restaurant’s “staff said she loved [the] mushrooms very much. It was an extremely magical day.”

We don’t know what their acute effects on Yellen were, while she was in Beijing. But the mushrooms appear to be contributing to her chronic hallucinations about the U.S. economy’s current health. This week, for example, while attending the G20 meeting in India, Yellen remarked:

“For the United States, growth has slowed, but our labor market continues to be quite strong. I don’t expect a recession. The most recent inflation data were quite encouraging.”

These, no doubt, are the fantasies of a person under the influence of mind-altering chemicals. Either that, or her mind has turned soft over decades of working as a professional economist for the Federal Reserve and the Treasury.

Tempered Perspective

The unemployment rate reported by the Bureau of Labor Statistics (BLS) is, in fact, just 3.6 percent. Yellen can celebrate the data point. But the quality of the jobs being created is not the type that will drive economic growth.

Higher-paying technology and finance jobs are being purged. While leisure, hospitality, and government are the sectors contributing to employment growth. These jobs may be important. Still, they will not create new wealth or help America compete with its global rivals.

Yellen, while under the influence, also remarked that she doesn’t expect a recession. Maybe this is why you should expect one.

Her predictive acumen has missed the target in the past. If you recall, in 2017 she said she did not believe another financial crisis would happen in our lifetime. Since then, we’ve had one financial crisis after another, including the most recent bank failures this spring.

Just this week, Bank of America reported its bond losses in the second quarter increased $7 billion to nearly $106 billion. And Starwood Capital Group just defaulted on a $215.5 million mortgage on an Atlanta office tower. Probably nothing to worry about, right?

In addition, this week Taiwan Semiconductor Manufacturing Company (TSMC), the mega chip maker, reported its first profit drop in 4 years. Revenue slipped 10 percent from a year ago. What’s more, net income fell 23.3 percent. Wasn’t AI supposed to drive silicon wafer production to commanding heights?

With respect to what Yellen called ‘encouraging inflation data’. While under the influence, she was likely referring to the recent CPI report from the BLS, which showed that in June, consumer prices increased at an annualized rate of 3 percent. This is still 50 percent higher than the Fed’s arbitrary inflation target.

Moreover, the energy commodities component showed a 16.7 percent price decline over the last year. This has coincided with President Biden draining the Strategic Petroleum Reserve to a 40-year low. Without these short-sighted actions, the current inflation data would be much less encouraging.

Structural Crisis

In short, the U.S. economy’s prospects do not quite align with Yellen’s positive outlook. And if you look out further than just the current data reports, you’ll be greeted with a structural crisis of significant consequence.

In fact, simple arithmetic quickly reveals the precarious predicament the 118th Congress is putting the American people in.

The Treasury Department, the agency Yellen oversees, recently reported that for the first 9 months of the 2023 fiscal year, the federal government ran a budget deficit of nearly $1.4 trillion. That’s a 170 percent increase from the same period last year.

The big surprise, however, was that interest on Treasury debt securities for the first 9 months of FY2023 topped $652 billion. A 25 percent increase for this period a year ago.

Rapid and repeated interest rate hikes by the Fed to contain the raging price inflation of its own making, has blown out the interest owed on Treasury debt. Anyone with half an inkling knew this was coming from miles away.

The growth of federal debt has been out of control for decades. But the rate of debt growth in the 21st century has rapidly accelerated.

The solution that’s commonly offered by the politicians for getting a handle on Washington’s debt problem is for the economy to somehow grow its way out. Countless policies over the years have generally involved borrowing money from the future and spending it today.

Yet economic growth never manages to outpace the debt increases. Instead, the debt piles up higher and higher with each passing year. The simple fact is you can’t grow your way out of debt when the debt’s increasing faster than gross domestic product (GDP).

For example, in 2000 the federal debt was about $5.6 trillion, and U.S. GDP was about $10 trillion. Today, the federal debt is over $32.5 trillion, and GDP is about $26.5 trillion. In just 23 years the federal debt has increased by over 480 percent while GDP has increased just 165 percent.

How Washington Ruined America’s Future

Recently, the Peter G. Peterson Foundation attempted to characterize the $32 trillion federal debt. The number is so large it is difficult to comprehend. Here is some of what the foundation came up with:

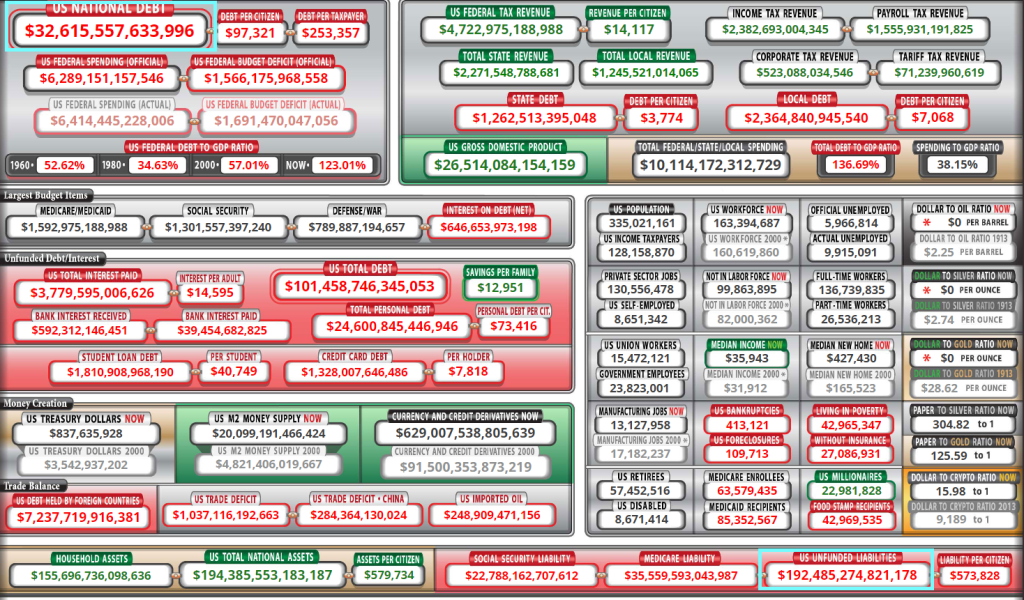

The $32 trillion debt is more than the combined values of the economies of China, Japan, Germany, and the United Kingdom. It represents $244,000 per household or $96,000 per person in America. And if every household contributed $1,000 per month towards paying down the national debt it would take over 20 years.

Without question, Washington has run up an impossible tab. Yet, what does it have to show for all this recklessness?

America’s cities are decaying from the inside out. The infrastructure is crumbling. The country has been involved in one overseas quagmire after another. And the populace is struggling with gender identification pronouns.

The political will to stop this massive debt pileup has been nonexistent. Democrats and Republicans have both spent like drunken sailors. There’s been no tradeoffs or compromises to cut spending. There’s been zero effort to balance the budget. And now it’s too late.

As mentioned above, interest on Treasury debt securities for the first 9 months of FY2023 topped $652 billion – a 25 percent increase from a year ago. But this is just the beginning.

As interest rates continue to rise, the annual interest on Treasury debt will soon pass $1 trillion. That would put this line item at par with outlays for Social Security, the U.S. government’s largest expenditure.

This would also put spending on interest payments above the combined spending of research and development, infrastructure, and education.

Consequently, by repeatedly borrowing and spending money, piling up massive debt, and then being forced to jack up interest rates, Washington has ruined America’s future.

Yippee! Look Ma, no hands! The face of America decline: Former Fed Chair Janet “Too Low For Too Long” Yellen who is now our woefully inept Treasury Secretary. You know, the Treasury Secretary who bowed three times to a Chinese Communist Party leader.

A reminder of the pickle that our politicians have put us in. US Federal debt is at $32.62 TRILLION … and UNFUNDED LIABILITIES (Social Security, Medicare, Medicaid, etc) are at $192.5 TRILLION!!! Yes, the US economy is broken beyond hope of repair, yet dunce voters keep reelecting imbeciles like Joe Biden, Chuck Schumer, John McConnell, etc.

Starwood Capital Group’s Barry Sternlicht recently told Bloomberg’s David Rubenstein about the ongoing crisis in the commercial real estate sector, equating it to a severe “Category 5 hurricane“. He cautioned, “It’s sort of a blackout hovering over the entire industry until we get some relief or some understanding of what the Fed’s going to do over the longer term.”

Currently, the biggest problem in the CRE space is sliding office and retail demand in downtown areas. Couple that with high-interest rates, and there’s a disaster lurking for building owners. According to Morgan Stanley, the elephant in the room is a massive debt maturity wall of CRE loans that totals $500 billion in 2024 and $2.5 trillion over the next five years.

Senior markets editor for Bloomberg, Michael Regan, chatted with John Fish, who is head of the construction firm Suffolk, chair of the Real Estate Roundtable think tank and former chairman of the board of the Federal Reserve Bank of Boston, in the What Goes Up podcast to discuss the biggest problems in the CRE market.

Fish warned that “capital markets nationally have frozen” and “nobody understands value.” He said, “We can’t evaluate price discovery because very few assets have traded during this period of time. Nobody understands where the bottom is.”

For a sense of recent price discovery trends, we were the first to point out to readers of a wicked firesale of office towers in the downtown area of Baltimore City:

As for the overall CRE industry, Goldman Sachs chief credit strategist Lotfi Karoui recently told clients, “The most accurate portrayal of current market conditions with Green Street indicating a 25% year-over-year drop in office property values.”

Sooooo, Powell and The Fed will likely raise rates this week. And maybe a few more times over the next few months. And The Fed remains defiant about taking away the Covid monetary stimulus.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.