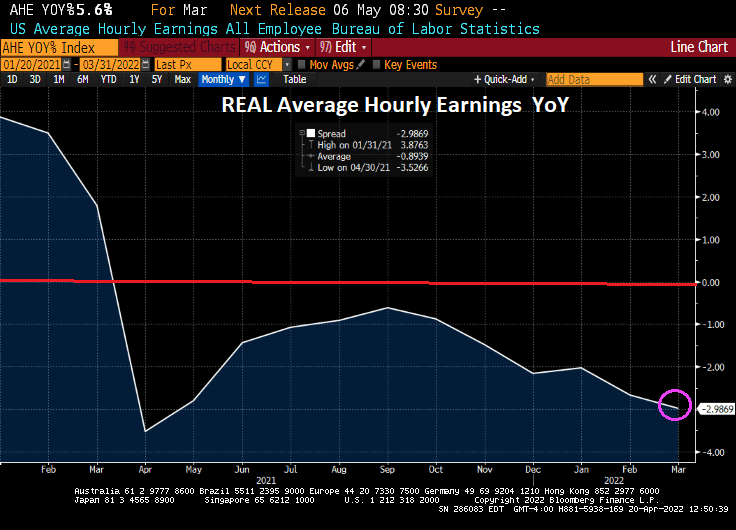

US President Biden went green and signed executive orders on his first day to limit oil and natural gas exploration of Federal lands and offshore (also, killed the Keystone Pipeline), helping to drive up energy prices and food prices. These orders begat inflation (also caused by the massive Covid relief by the Federal government). The highest inflation in 40 years begat The Federal Reserve signalling a tightening of Fed monetary policy … to fight the problem caused by The Fed in the first place … too much monetary stimulus for too long. Fiscal and monetary fanaticism and ignorance is forever busy and needs feeding

There was an interesting article on MarketWatch entitled “Bond rout exposes Social Security’s insanity.” The headline was “Every dollar of yours that’s invested in the Social Security trust fund is invested in low-yielding government bonds.”

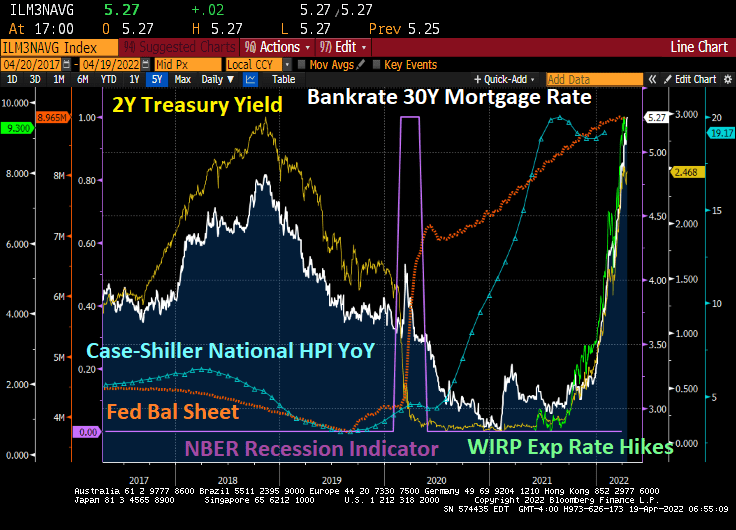

Yes, another disastrous consequence of The Fed’s lax monetary policy since 2008, helping to push Treasury yields extremely low. And REAL Treasury yields into negative territory.

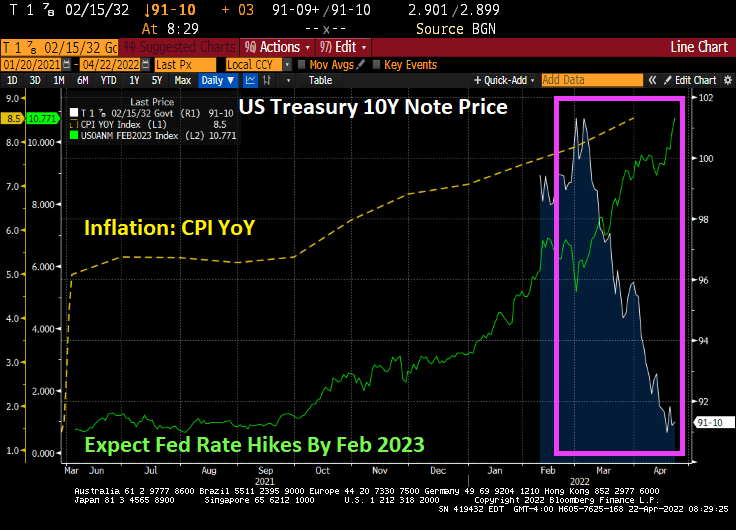

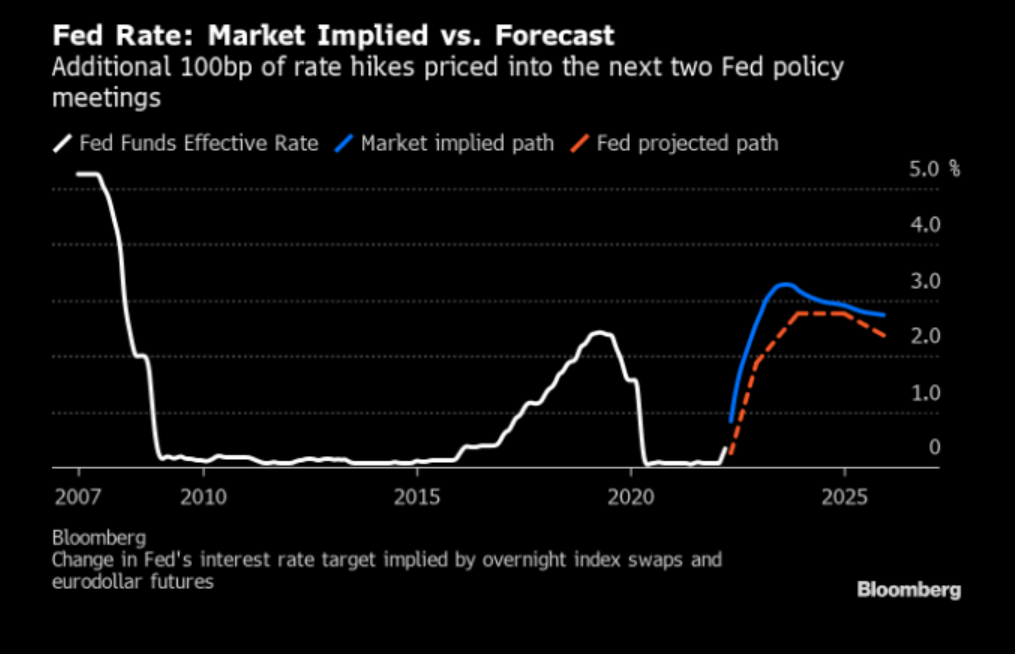

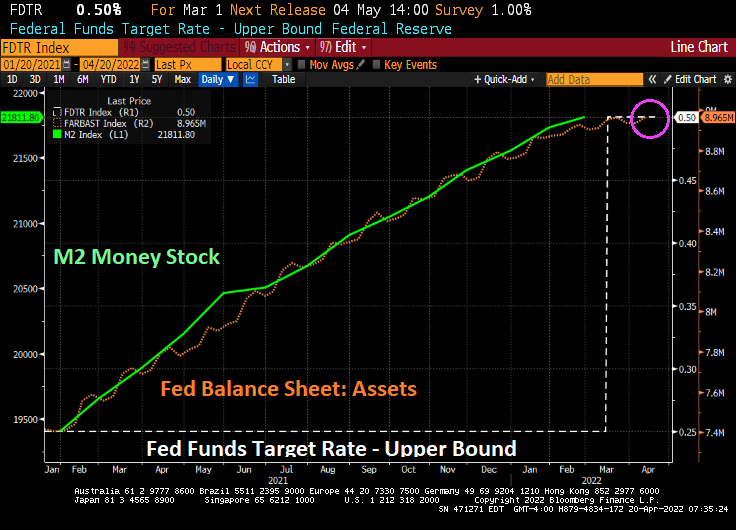

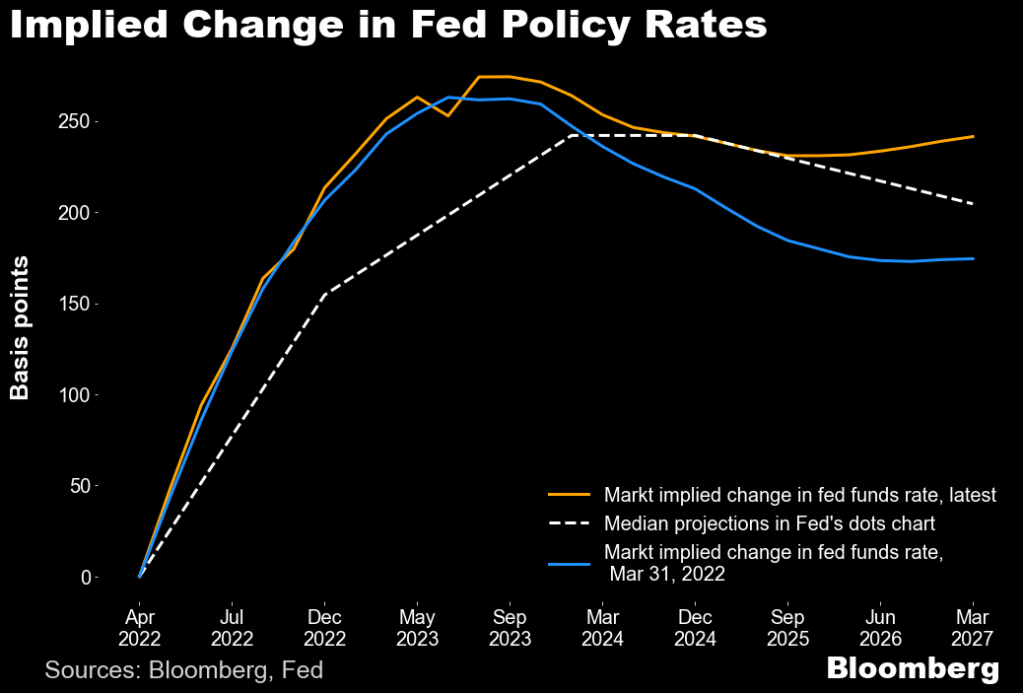

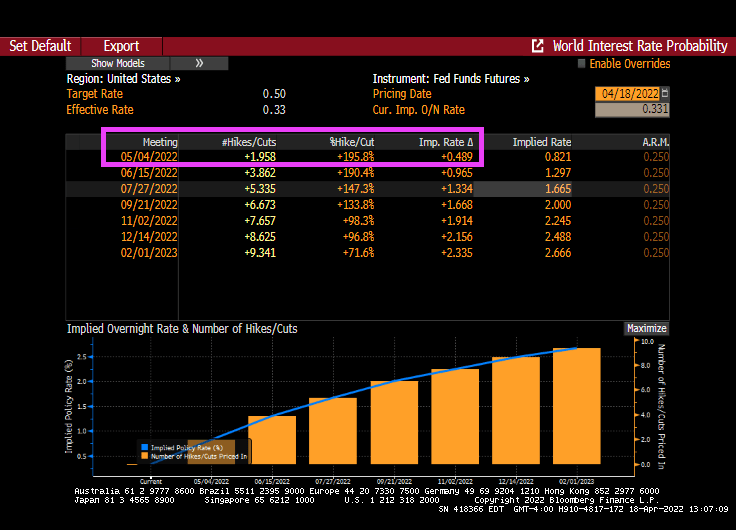

But here we sit today with The Fed threatening to trim their balance sheet and raise rates … to combat the inflation they helped create in the first place. Now we have the 10-year Treasury Note price falling like a paralyzed falcon with expected hate hikes going above rate hikes by February 2023 (based on Fed Funds Futures prices).

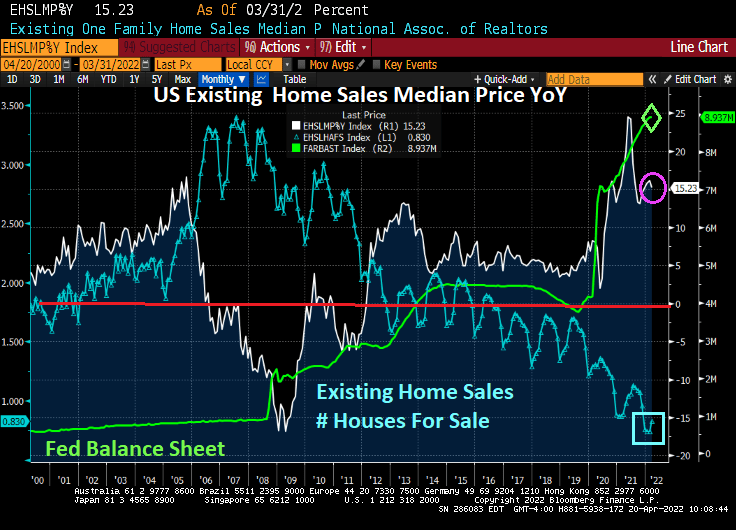

Most pension funds also invest heaving in US Treasuries, along with agency Mortgage-backed Securities (AgencyMBS).

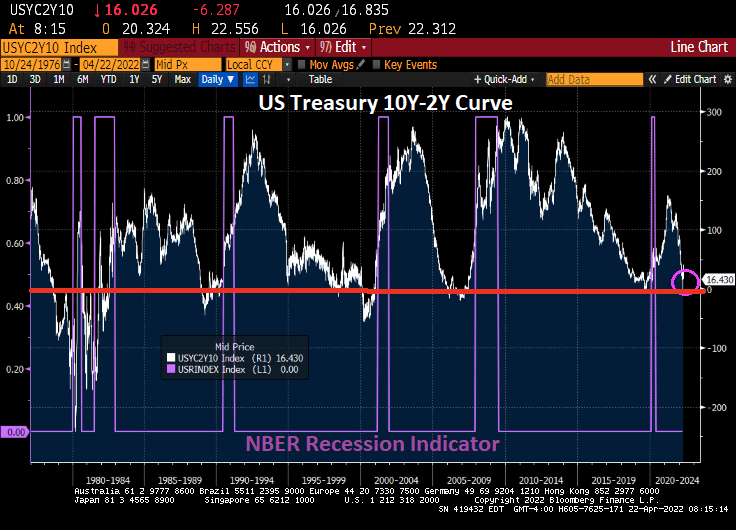

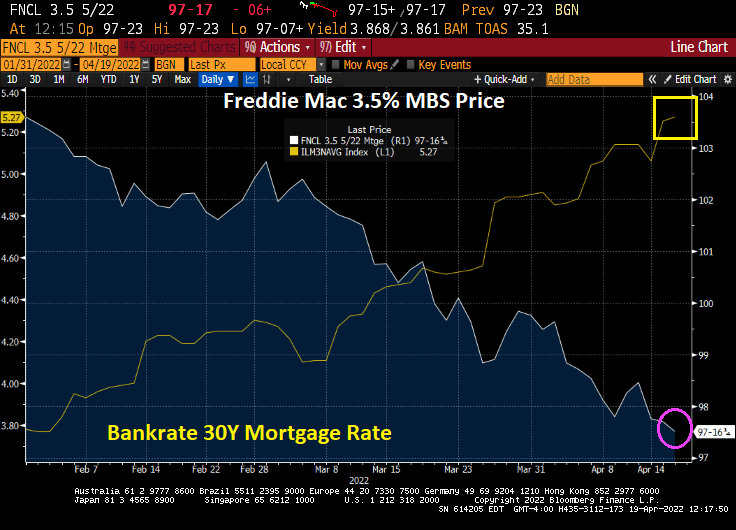

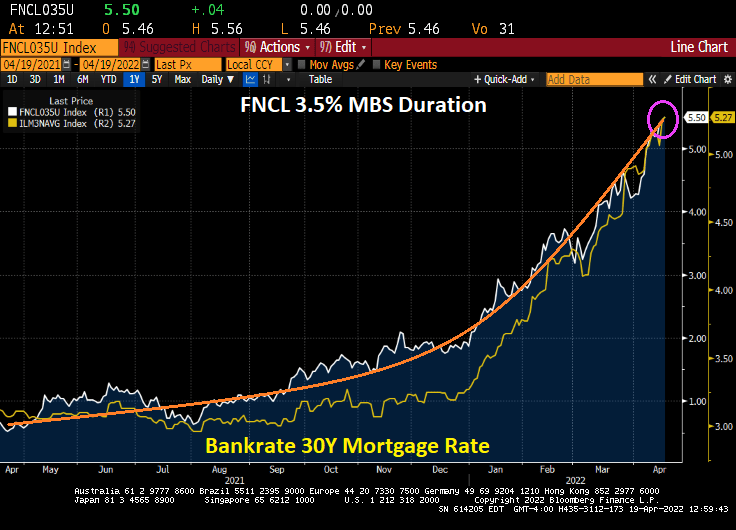

Plus we have the Treasury curve slipping into darkness.

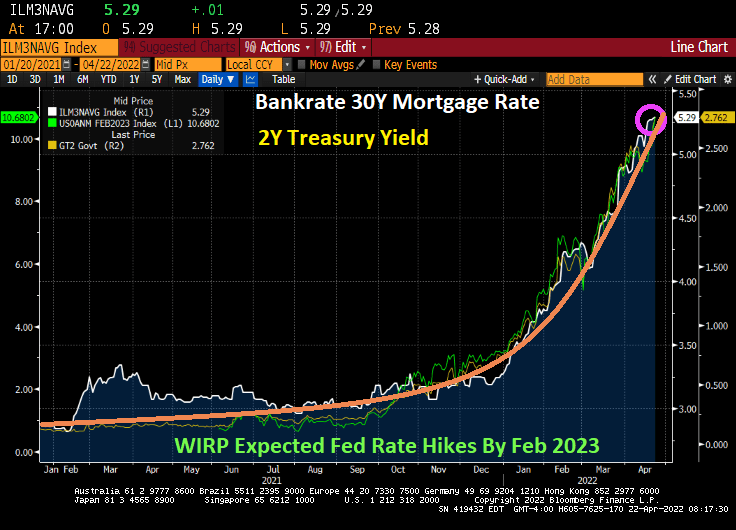

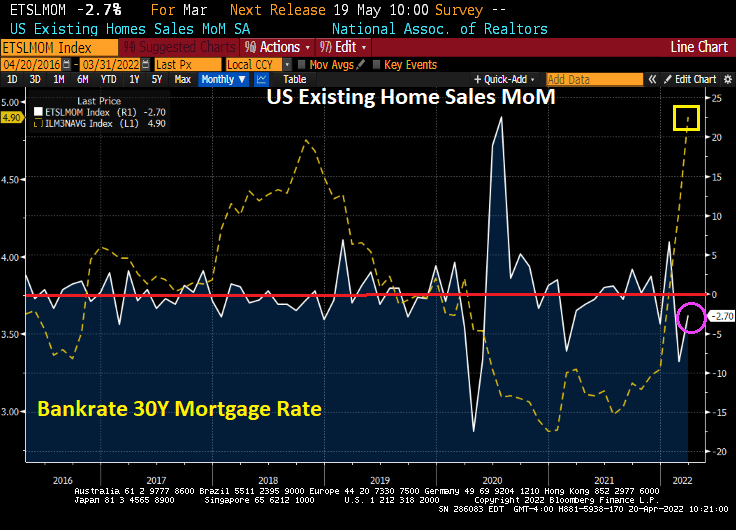

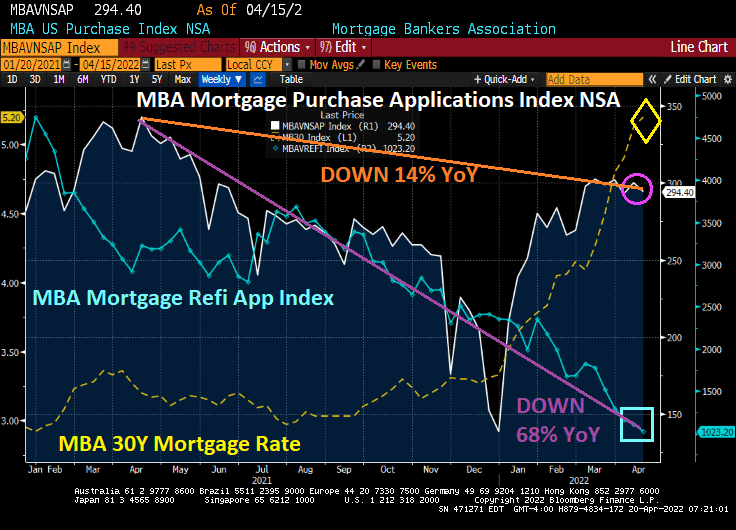

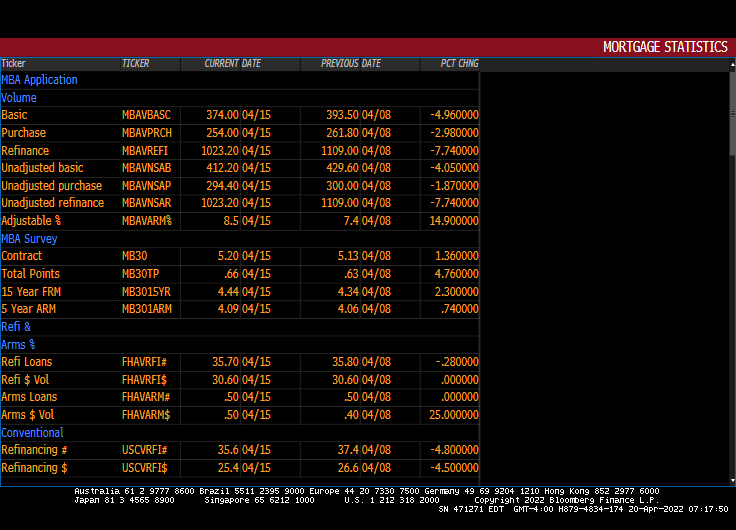

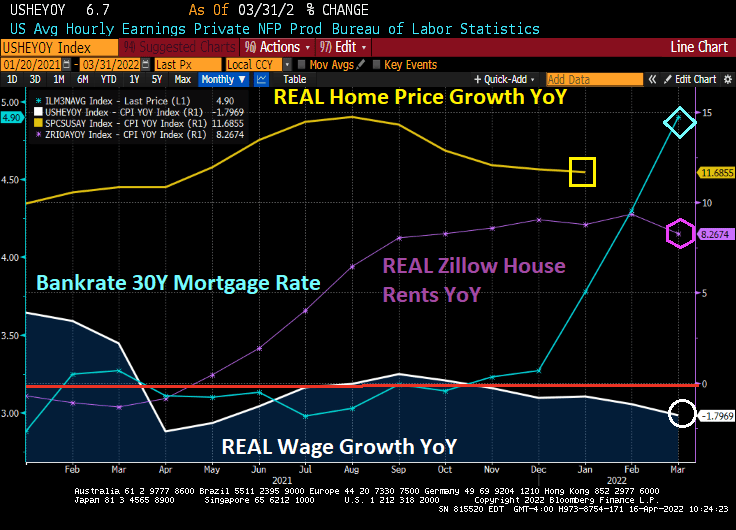

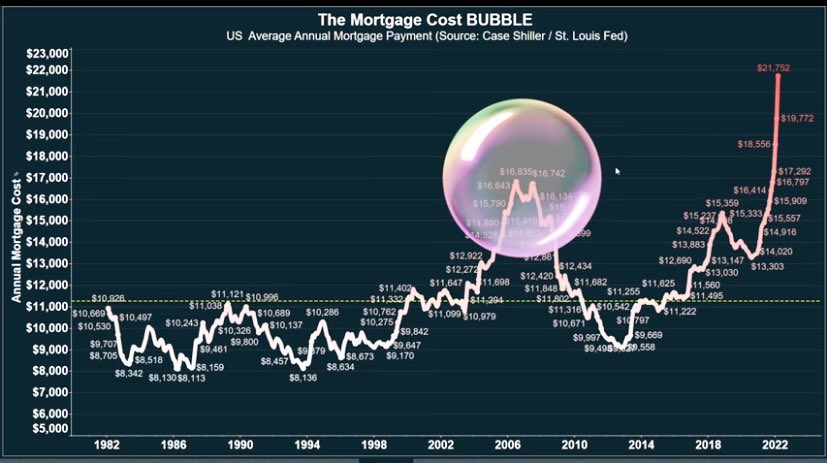

Speaking of “Slipping Into Darkness,” mortgage rates are soaring.

Meanwhile, Biden, Fed economists and Congress are merrily partying at some DC nightclub.

What is hip? NOT Biden, Pelosi, Schumer or Powell.

You must be logged in to post a comment.