Mortgage applications increased 27.9 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending January 13, 2023. But mortgage applications are 60% lower than the same week last year.

The Refinance Index increased 34 percent from the previous week and was 81 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 25 percent from one week earlier. The unadjusted Purchase Index increased 32 percent compared with the previous week and was 35 percent lower than the same week one year ago.

Here are the stats.

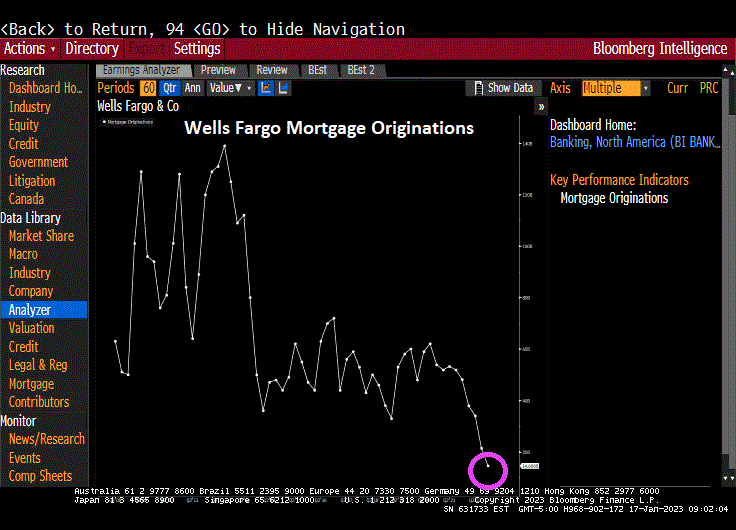

One lender in particular, Wells Fargo, smells blood in the economic waters, and has cut back mortgage originations.

Just remember, mortgage applications generally rise in the first part of the year until May, then start slowing until the last week of the year. This is called seasonality. But despite the fast growth this year, purchase applications are still down -35% compared to last year at this time.

The Empire Strikes Out! No, not Klaus Schwab and the World Economic Forum, but the New York State Manufacturing index. For January, the index fell to -32.9.

Then we have Wells Fargo and their crashing mortgage originiations.

One of the big problems with Federal goverment and Federal Reserve monetary stimulus is … it wears out. Just look at M2 Money growth.

US existing homes sales fell -7.70% in November to 4.09 million units SAAR. And since the same month last year, existing home sales are down -35.4% YoY.

Existing home sales were the lowest in November since 2010.

The good news? The median price of existing homes fell to 3.21% YoY. The bad news? The ark is really bad pointing to a bad December. Inventory for sale (orange line) remains below pre-Covid shutdown levels.

Years ago, Brent Ambrose, Michael Lacour-Little and I wrote a paper on the US 30-year jumbo mortgage spread over conforming 30-year mortgage rates entitled “The effect of conforming loan status on mortgage yield spreads: a loan level analysis.” But that paper was written before Covid and the dramatic distortion caused in mortgage markets by The Federal Reserve’s massive increase in money.

Here is the spread between Bankrate’s 30-year mortgage rate and their 30-year JUMBO mortgage. Notice that between 2007 and early 2020, the median “jumbo spread” was 49 basis points. But after Covid and The Fed’s counterattack (by printing M2 Money), the median Jumbo spread from 4/1/2020 to today is only 1 basis point.

In the following chart, you can see the jumbo mortgage rate (yellow) against the conforming mortgage rate (white) and there is almost always a spread between the two UNTIL 2020 where we saw M2 Money growth (green line) spike and The Fed increased their purchases of Agency MBS (purple line). Since Covid and The Fed’s massive reaction, the jumbo rate and conforming rate are virtually the same. In fact, the latest jumbo spread is 1 basis point over the conforming rate.

Why is this happening? One explanation is that demand from the investors who ultimately buy jumbo mortgages. The strong demand by investors appears to have driven down the yields on jumbos relative to conventional loans, especially as the use and accessibility to jumbos has grown.

A second explanation is that Loan Level Price Adjustments that were added to conforming loans post-financial crisis never went away (until just recently on selected loans). This makes jumbos and conforming loans very close in yield.

So, when will the mortgage market return to normal and jumbo mortgages go back to the normal 50 basis point spread? We may see normalization if The Fed speeds up its withdrawal from markets. Also, getting rid of Loan Level Price Adjustments would help normalized the mortgage market.

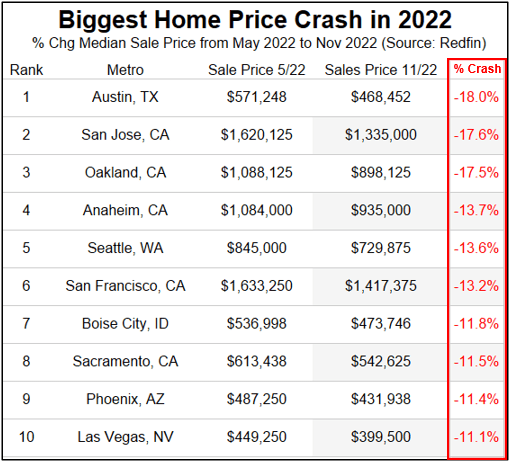

But things are getting stressed in jumboland (California) where home prices are crashing in 5 of the top 8 metro areas.

Harry Houdini couldn’t have created a more tantalizing mystery … and one I wish would go away.

Mortgage applications increased 3.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending December 9, 2022.

The Refinance Index increased 3 percent from the previous week and was 85 percent lower than the same week one year ago. The unadjusted Purchase Index decreased 1 percent compared with the previous week and was 38 percent lower than the same week one year ago.

You can see the impact of seasonalilty on mortgage purchase applications (white line). They peaked in the week of May 6, 2022 and have been generally declining since. While refi applications (orange line) increased over the past week, they have been pummelled by The Fed tightening.

It is quiet today as investors wait for The Fed to announce a 50 basis point rate increase. Fed Funds Futures point to almost another 100 basis point hike by May 5, 2023, then a slow decline in The Fed Funds target rate (upper bound).

And here is Sam Bankman-Fried and his high-powered legal defense.

US mortgage rates fell for a fourth week in a row, the longest such stretch of declines since May 2019.

The contract rate on a 30-year fixed mortgage eased 8 basis points to 6.41% in the week ended Dec. 2, still the lowest since mid-September, according to Mortgage Bankers Association data released Wednesday.

Rates have retreated for the past month as the Federal Reserve has signaled it will soon slow down the pace of interest-rate hikes, likely at next week’s policy meeting.

Even so, MBA’s mortgage purchase index fell 3%, the first drop in five weeks, underscoring how demand remains fickle and driving a decline in the overall measure of mortgage applications. On the other hand, refinancing activity rose last week, but remains near the lowest level in two decades.

Here is a chart of mortgage applications from the Mortgage Bankers Association showing the decline in US mortgage rates, and increases in mortgage purchases and refi applications. The Refinance Index increased 5 percent from the previous week and was 86 percent lower than the same week one year ago. The unadjusted Purchase Index increased 31 percent compared with the previous week and was 40 percent lower than the same week one year ago.

The MBA survey, which has been conducted weekly since 1990, uses responses from mortgage bankers, commercial banks and thrifts. The data cover more than 75% of all retail residential mortgage applications in the US.

US mortgage rates fell last week by the most since the end of July, slipping below 7% and helping generate a bounce in purchase applications that otherwise remain depressed, but only in the Seasonally Adjusted data. The NON-Seasonally Adjusted data show a hefty decline.

The contract rate on a 30-year fixed mortgage decreased 24 basis points to 6.9% in the week ended Nov. 11, according to Mortgage Bankers Association data released Wednesday. The group’s index of applications to buy a home rose 4.4% — the most since June — but is still near the weakest level since 2015.

But the bounce was in Seasonally Adjusted data only. The NON-seasonally adjusted data remained depressed.

Mortgage applications decreased -10.0 percent SA from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending November 11, 2022. This week’s results include an adjustment for the observance of Veterans Day.

The Refinance Index decreased -11.44% percent from the previous week and was 88 percent lower than the same week one year ago.The unadjusted Purchase Index decreased -10 percent compared with the previous week and was 46 percent lower than the same week one year ago.

Mortgage purchase applications will continue to fall in NSA terms since it is the Winter and home buying season won’t really start until January. Refinancing applications actually dropped -11.44% even with the drop in mortgage rates.

The data. As my former students know, I like the “raw” data, better known as NON-seasonally adjusted (NSA) data and avoid seasonally-adjusted data (SA) since it hides what is going on.

And on The Fed Futures Front, The Federal Reserve is still looking a hiking their target rate from 4% to just under 5%.

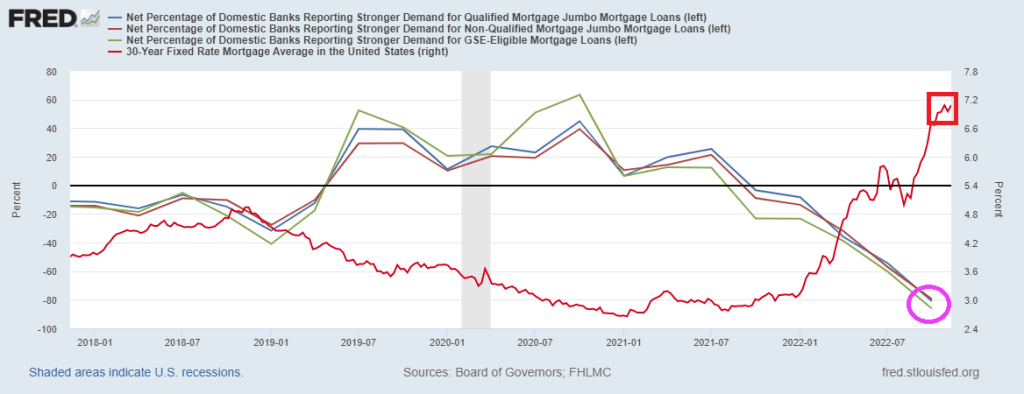

The Net Percentage of Domestic Banks Reporting Stronger Demand for Mortgage Loans is sinking faster than Joe Biden’s oratory skills as The Fed tightens their monetary belts.

And today, the University of Michigan (BOOO!!) consumer survey for housing buying conditions fell to the lowest level in recorded history.

Given the latest inflation numbers (improving from disastrous, 8.2% YoY to really horrible, 7.70% YoY), and unemployment rate rising from 3.5% to 3.7%, we now see that Taylor Rule estimate for Fed Funds is now … 13.85%. The US is currently at 4.00%. THAT is a big gap!

Yes, The Fed will not be able to fill the gap between the Taylor Rule and the current Fed Funds Target Rate, without incredible damage being done.

Unfortunately, this is an ACTIVE FAILURE for The Fed which has left monetary stimulus too high for too long since late 2008.

On a personal note, I am glad the midterm elections are over. We saw John Fetterman arguing until he was blue in the face that he loved fracking and will continue to let Pennsylvania frack. Then PA governor-elect Josh Shapiro came out yesterday and said that PA will end all fracking. And we are to believe that Lt Gov Fetterman did not talk with PA Attorney General Shapiro about fracking? To quote Joe Biden, “C’mon man!”

US mortgage applications declined for the sixth consecutive week despite a slight drop in rates.

Mortgage applications decreased 0.5 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending October 28, 2022. This week’s results include revised data to reflect an update to last week’s survey results.

The Refinance Index increased 0.2 percent from the previous week and was 85 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 41 percent lower than the same week one year ago.

This morning’s WIRP (Fed Funds Futures data) is pointing to a 75 basis point increase from The FED FOMC (open market committee) at 2pm EST, rising to over 5% by the May 2023 meeting before declining again.

You must be logged in to post a comment.