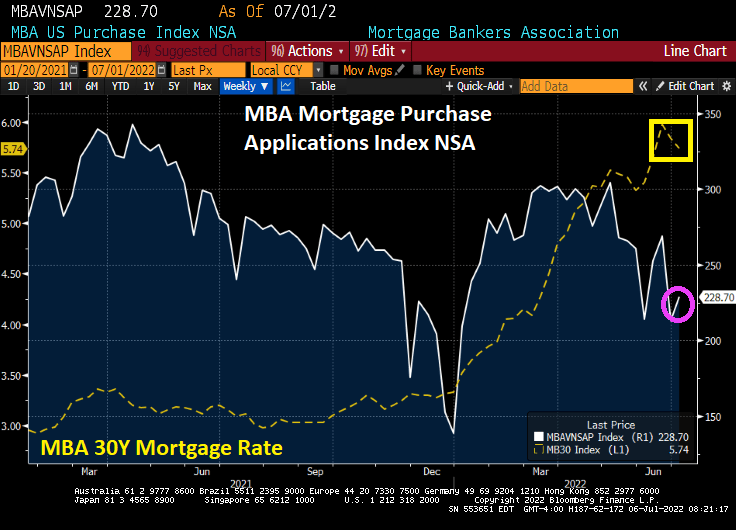

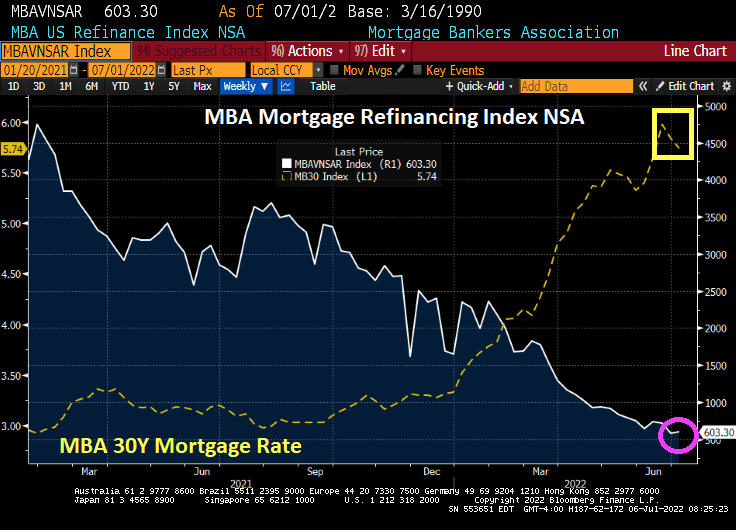

As The Fed takes away the massive monetary punch bowl, mortgage rates have risen to the highest since November 2008. And with the withdrawal of monetary stimulus (raising Fed Target Rate), mortgage purchase applications have declined.

Here is a photo of The Federal Reserve fighting the housing and mortgage market.

The monetary noose tightens on the housing and mortgage markets.

Mortgage applications decreased 0.8 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending September 2, 2022. They are now the lowest since 1999.

The Refinance Index decreased 1 percent from the previous week and was 83 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index decreased 3 percent compared with the previous week and was23 percent lower than the same week one year ago.

At least the percentage of adjustable rate mortgages (ARMs) remained the same at 8.5%.

For the sake of the housing and mortgage market, somebody stop Powell and The Gang from tightening!

Thanks to Federal Reserve increases in their target rate, the 30-year mortgage rate has risen above 6%.

What drives me crazy about The Fed is their failure to removed monetary stimulus following the financial crisis of 2008 when they dropped their target rate to 25 basis points (0.25%) and began assets purchases (orange line). The Fed raises their target rate only once during Obama’s Presidency but then raised rates 8 times after Trump was elected President.

Now we are seeing The Fed NOT shrinking their balance sheet in a meaningful way. However M2 Money growth YoY (green line) has slowed to 5.2%.

While it is a good thing that The Fed is FINALLY reducing some of the monetary stimulus in place since 2008, the bad thing is that mortgage rates are rising rapidly.

The Fed’s quantheads are predicted to resume easing in March 2023.

Mortgage application volume dropped and remained at a multi-decade low last week(back to 1997), led by an 8 percent decline in refinance applications, which now make up only 30 percent of all applications. Purchase applications have declined in eight of the last nine weeks, as demand continues to shrink due to higher rates and a weaker economic outlook.

Mortgage applications decreased 3.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending August 26, 2022.

The unadjusted Purchase Index decreased 4 percent compared with the previous week and was23 percent lower than the same week one year ago.

The Refinance Index decreased 8 percent from the previous week and was 83 percent lower than the same week one year ago.

Just wait for The Federal Reserve to start unwinding its enormous balance sheet!

The US July inflation report remains hot, hot, hot! While mortgage purchase and refinancing applications are not, not, not.

The US consumer price index rose 8.5% in July. And real average weekly growth remains burned by horrid inflation, at -3.6% YoY.

Source of inflation?

Headline inflation above estimates in 14 of last 16 months.

Data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending August 5, 2022 revealed that … the Refinance Index increased 4 percent from the previous week and was 82 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 19 percent lower than the same week one year ago.

Here is your weekend update on Treasury and Mortgage markets.

The current US Treasury 10Y-2Y yield curve just slipped further into reversion at -40.299 basis points, screaming impending recession. Oddly, The Federal Reserve has been leaving its balance sheet of Agency Mortgage-backed Securities (MBS) in tact (green line).

On the mortgage front, Bankrate’s 30-year mortgage rate index rose to 5.60% while the affordability-friendly 5/1 Adjustable Rate Mortgage (ARM) rate rose to 4.21%.

Currently, a 5/1 ARM borrower can save 139 basis points over the traditional 30-year mortgage rate.

Mortgage applications declined for the third week in a row, reaching the lowest level since 2000.

Mortgage applications decreased 6.3 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending July 15, 2022.

The Refinance Index decreased 4 percent from the previous week and was 80 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 7 percent from one week earlier. The unadjusted Purchase Index increased 16 percent compared with the previous week and was 19 percent lower than the same week one year ago.

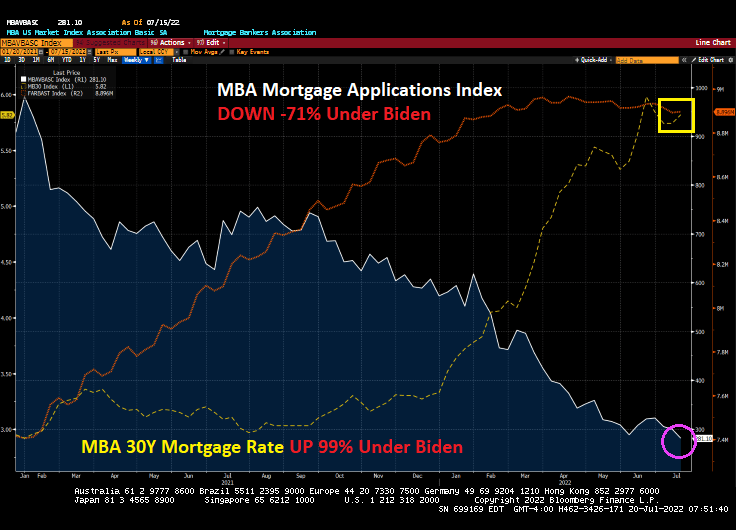

Heartache #1: Mortgage rates have risen 99% under Biden.

Heartache #2: Mortgage application have fallen -71% under Biden.

As The Federal Reserve continues to fight inflation caused by 1) excessive stimulus by The Federal Reserve and Federal government surrounding Covid and 2) Biden’s energy policies, we are seeing the mortgage market as collateral damage.

Housing in the US is simply unaffordable for the middle class and low-wage workers. Combine rising food costs and gasoline/heating costs, and we have an economic disaster on our hands.

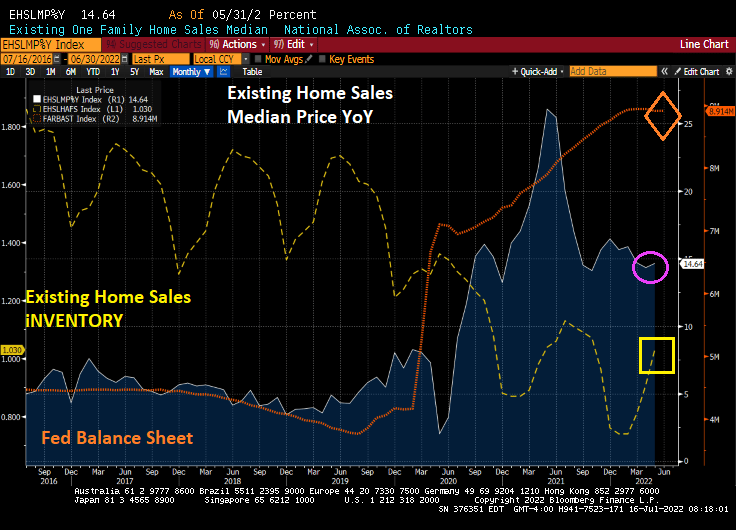

US existing home sales for June will be released on Wednesday. But can The Fed kill-off home price inflation?

A preliminary analysis of existing home sales for June is for a seasonally adjusted annual rate of 5.1 million, down 5.4% from May and down 14.2% from last June. As The Fed cranks up its target rate (green line) and eventually shrinking its balance sheet, we will see further shrinking of existing home sales this summer.

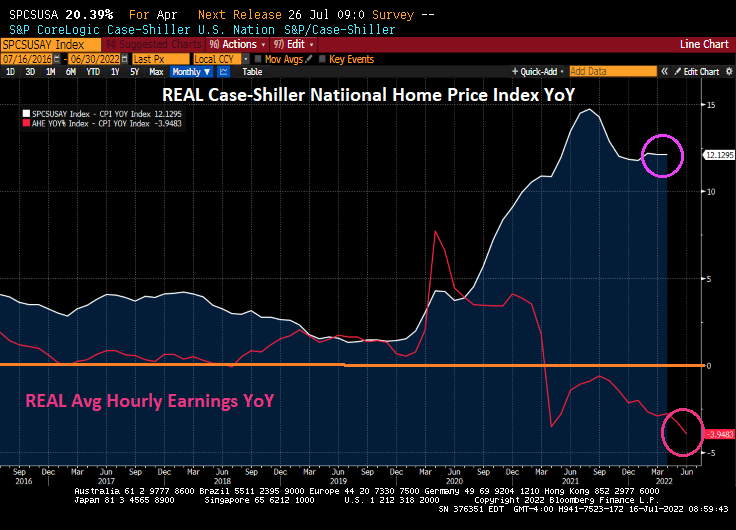

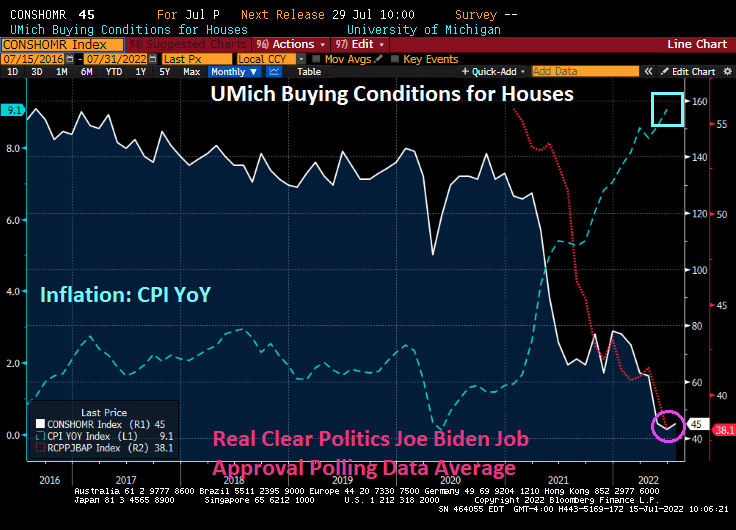

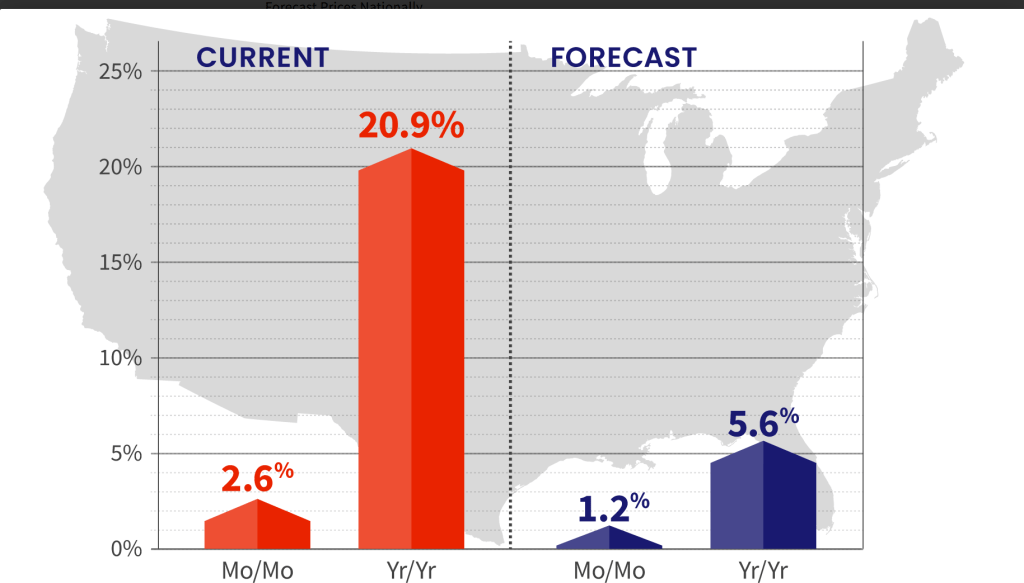

But home price inflation remains high (Case-Shiller National home price index at 21.23% YoY, Zillow’s rent index at 14.75% YoY) while the Consumer Price Index YoY is at 40-year high of 9.1% YoY. In other words, home price inflation is 233% of the stated inflation rate from Uncle Sam.

May’s existing home sales report was … sobering. There is still historically low levels of available inventory and median sales price of existing home sales was 14.64% YoY. Of course, the alternative to ownership is renting which is growing at 14.75% YoY. Simply unaffordable.

The gap between REAL home price growth (12.13% YoY) and REAL average hourly earnings (-3.95% YoY).

Consumer sentiment for housing is near the lowest level since 1982.

The Fed seems determined to remove the punch bowl in its efforts to crush inflation. But will The Fed’s efforts also crush the housing and mortgage market?

US inflation is the highest in 40 years, yet inflation may be slowing as 1) The Fed cranks up interest rates and 2) the global economy is slowing.

US inflation data in the coming week may stiffen the resolve of Federal Reserve policy makers to proceed with another big boost in interest rates later this month.

The closely watched consumer price index probably rose nearly 9% in June from a year earlier, a fresh four-decade high. Compared with May, the CPI is seen rising 1.1%, marking the third month in four with an increase of at least 1%.

While persistently high and broad-based inflation is seen persuading Fed officials to raise their benchmark rate 75 basis points for a second consecutive meeting on July 27, recession concerns are mounting. There are signs, though, that price pressures at the producer level are stabilizing as commodities costs — including energy — retreat.

But the expectations of inflation, as measured by The Fed’s 5-year forward breakeven inflation rate, just crashed to 1.8437%.

The breakeven inflation rate is a market-based measure of expected inflation. It is the difference between the yield of a nominal bond and an inflation-linked bond of the same maturity.

The USD Inflation Swap Forward 5Y5Y is also falling like a rock as The Fed hikes their target rate (green line).

Could it be that inflation is cooling with Fed rate hikes (but not the shrinking of their $8 trillion balance sheet)?

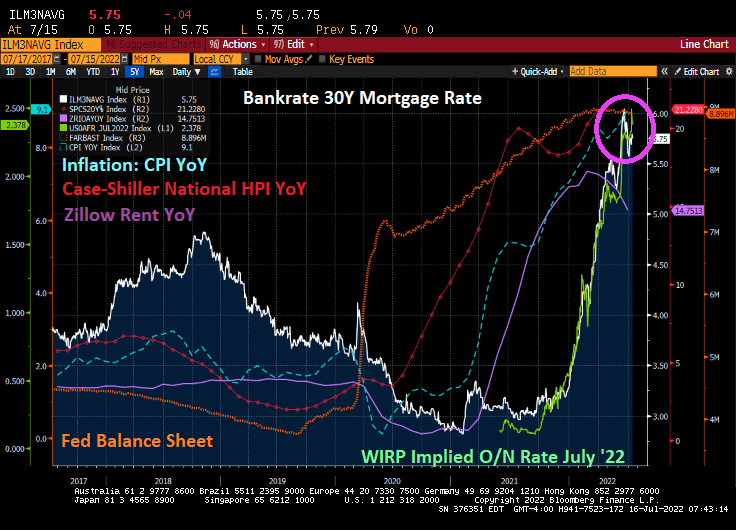

Currently, Fed Funds Futures are pointing to a Fed target rate of 3.552% by February 2023. And with that, Bankrate’s 30-year mortgage rate rose to 5.75%. Once again, like velociraptors from Jurassic Park, The Fed’s balance sheet is still out in force.

Fed Chair Jerome Powell and Atlanta Fed President Raphael Bostic are keeping The Fed’s balance sheet at near $9 trillion as they hunt assets to inflate.

Well, this is one way to get inflation under control … crash the economy. And inflation fears growing, we are seeing mortgage rates declining and mortgage applications increasing.

Mortgage applications decreased 5.4 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending July 1, 2022. This week’s results include a holiday adjustment to account for early closings the Friday before Independence Day.

The seasonally adjusted Purchase Index decreased 4 percent from one week earlier. The unadjusted Purchase Index increased 7 percent compared with the previous week and was 17 percent lower than the same week one year ago.

The Refinance Index decreased 8 percent from the previous week and was 78 percent lower than the same week one year ago.

You must be logged in to post a comment.