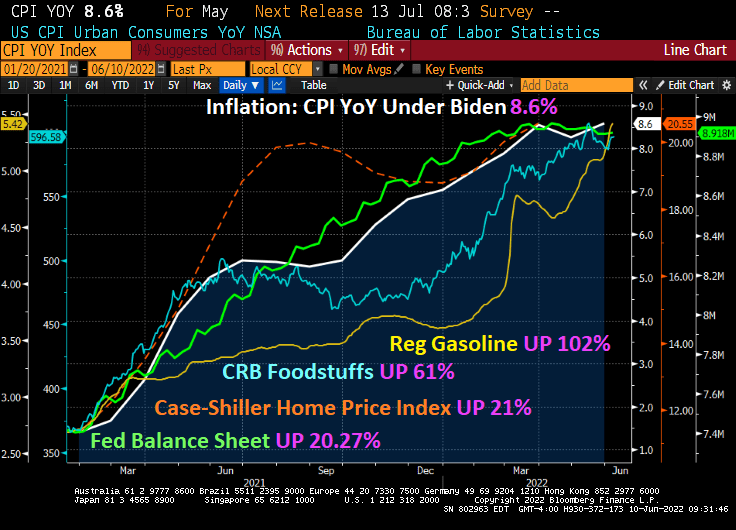

Inflation, the bane of the middle class and working families, just rose to 8.6%.

Core inflation, that excludes energy and food, actually declined slightly to 6% from 6.2% in April. But since most families are concerned with gas prices and food, (not to mention home prices growing at 21.17% YoY), core inflation really underestimates the suffering.

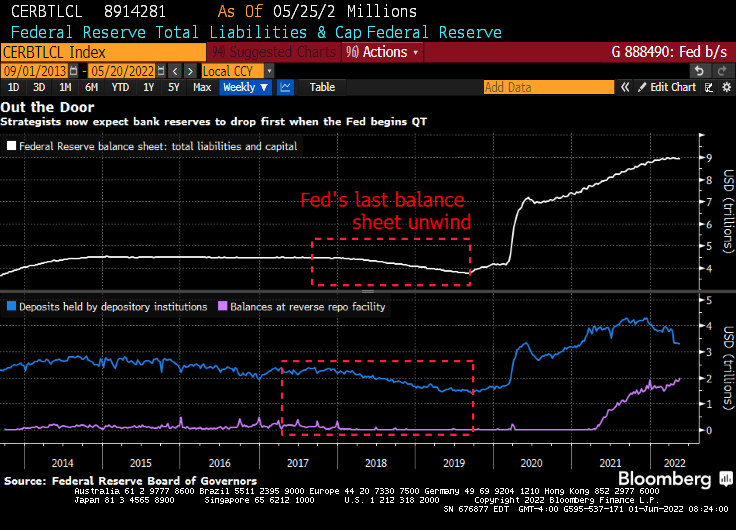

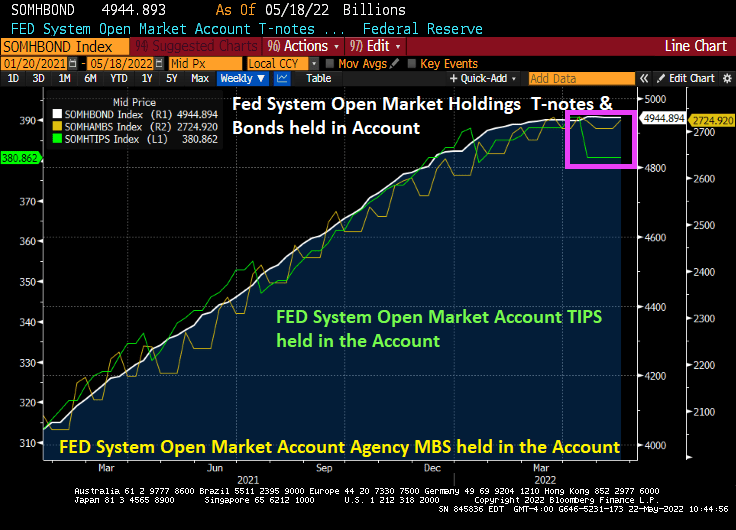

Under Biden’s leadership in cooperation with eternal Fed stimulus (until now), inflation started at 1.4% YoY and has increased to 8.6% YoY. The Fed’s balance sheet has increased by 20.27% (more monetary Stimulypto!), Case-Shiller home prices started at 10.44% YoY and has now doubled to 20.55% YoY. Regular gasoline started at $2.57 and is now at $5.42, up 102%. Food is up 61%.

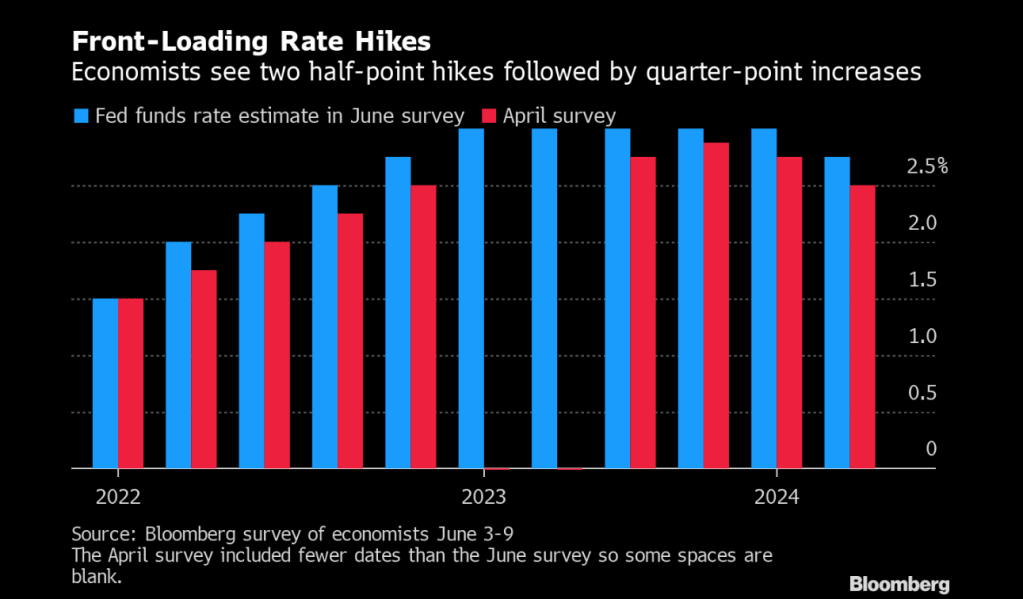

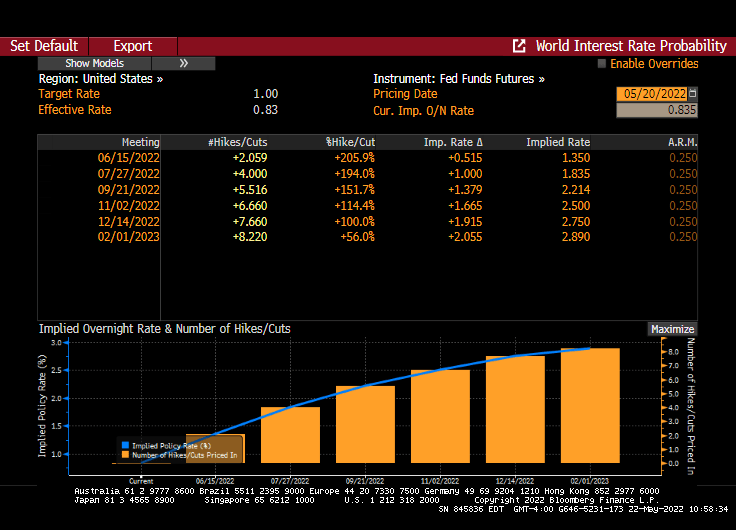

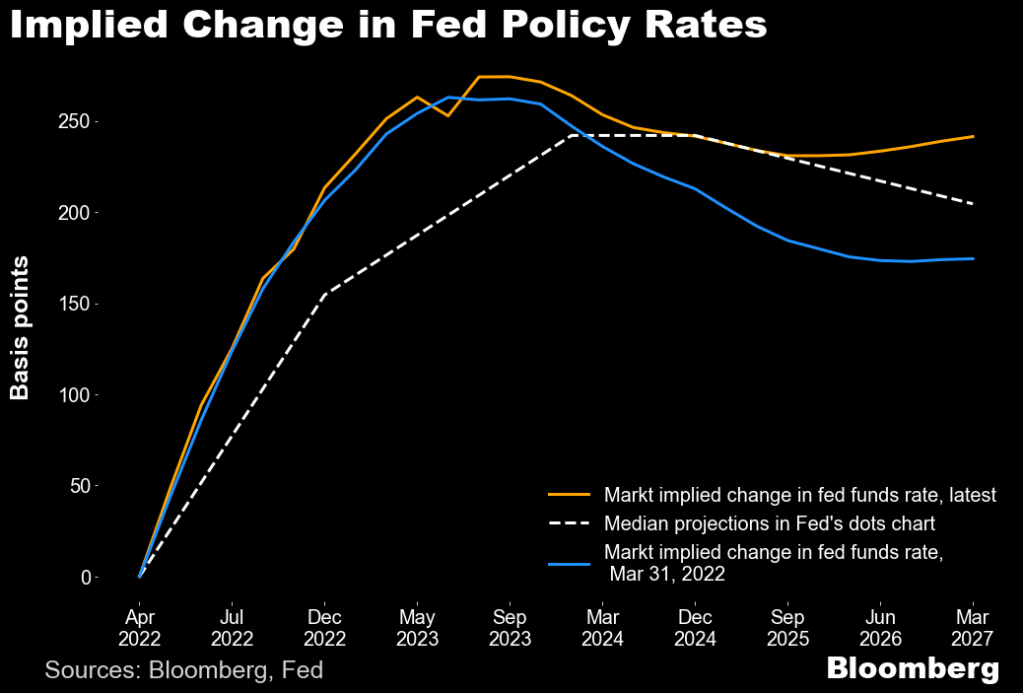

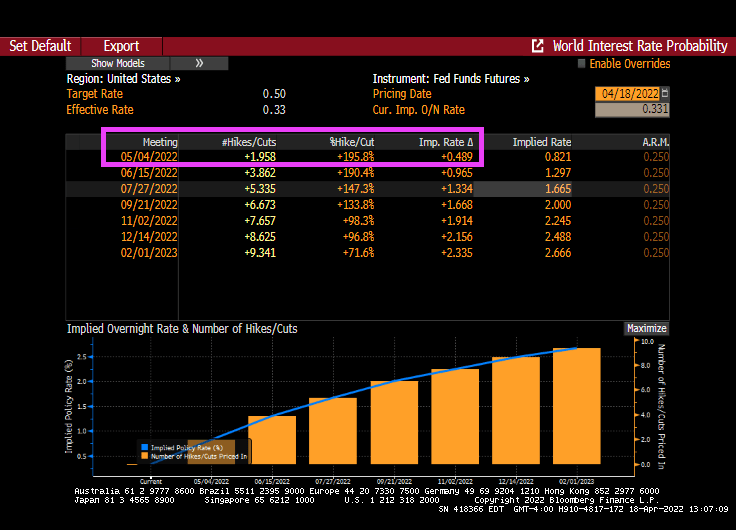

The Fed is expecting two half-point hikes followed by quarter-point increases.

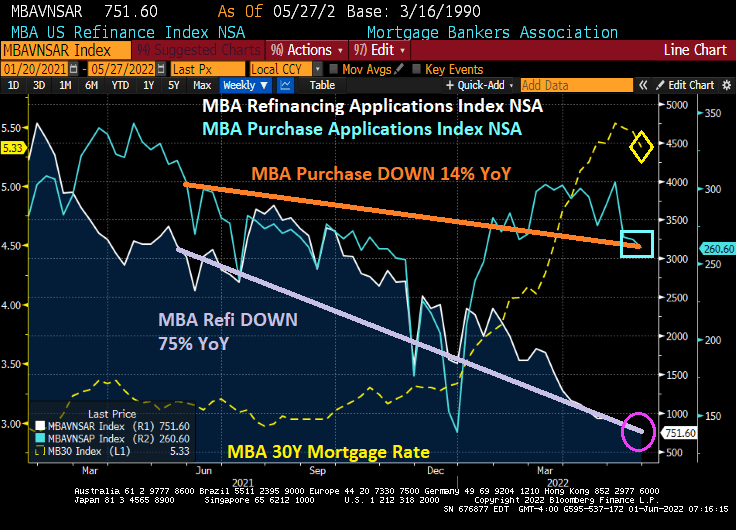

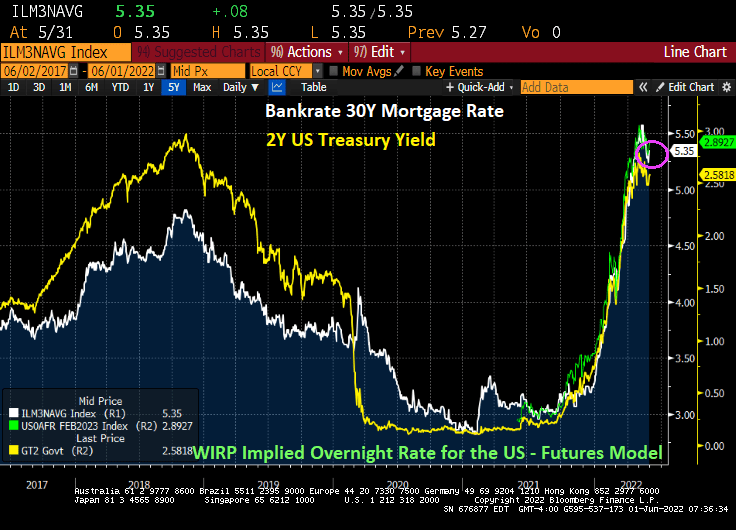

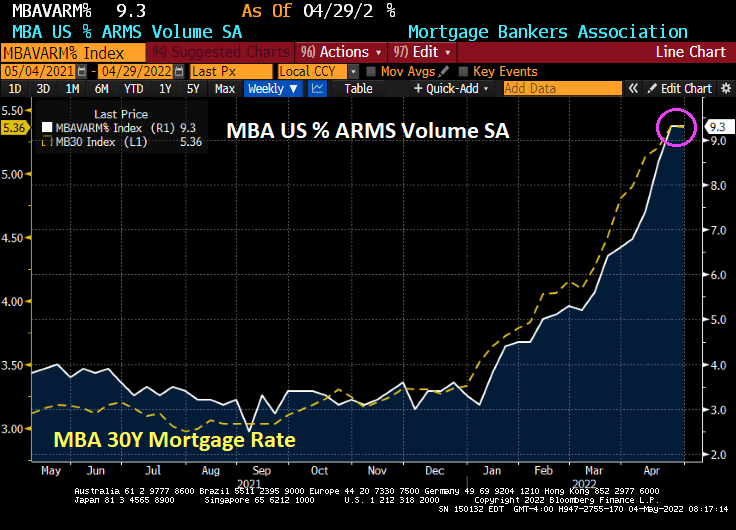

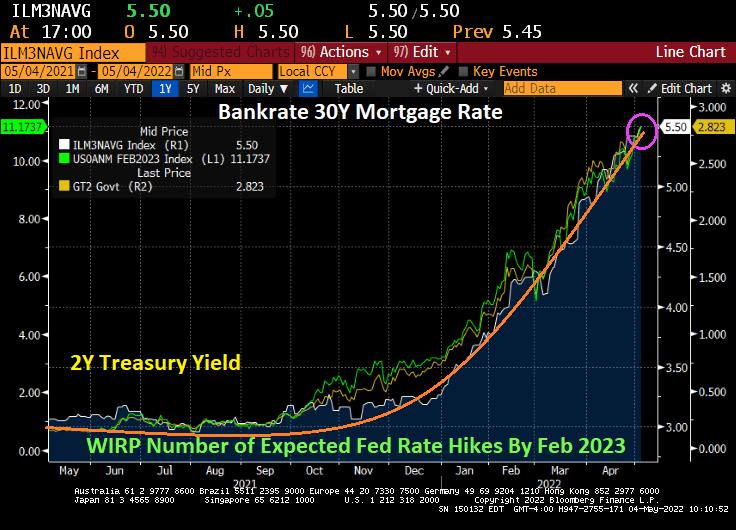

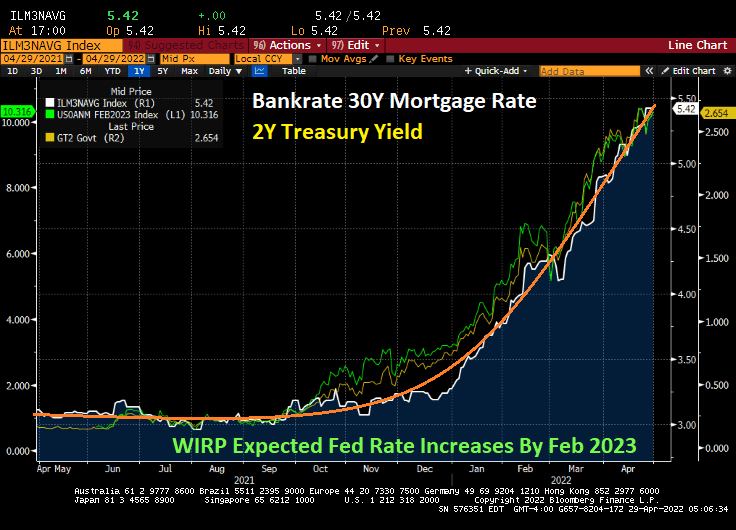

And mortgage rates keep rising as The Fed fights the inflation fire.

Here is a video of Milton Friedman speaking on inflation.

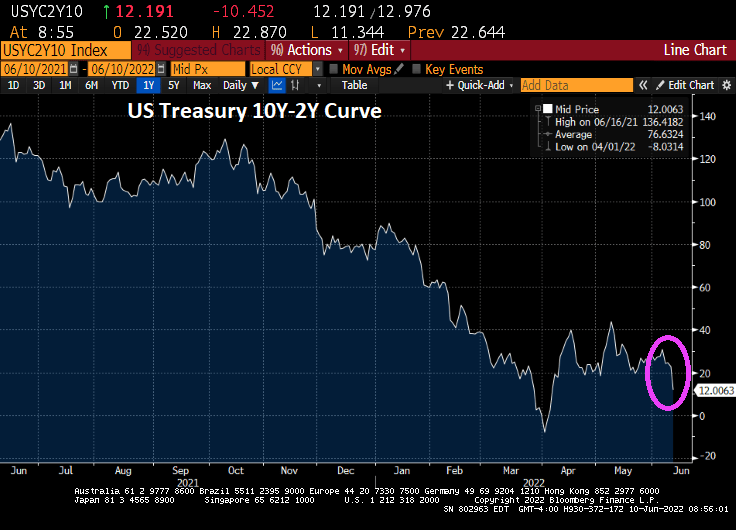

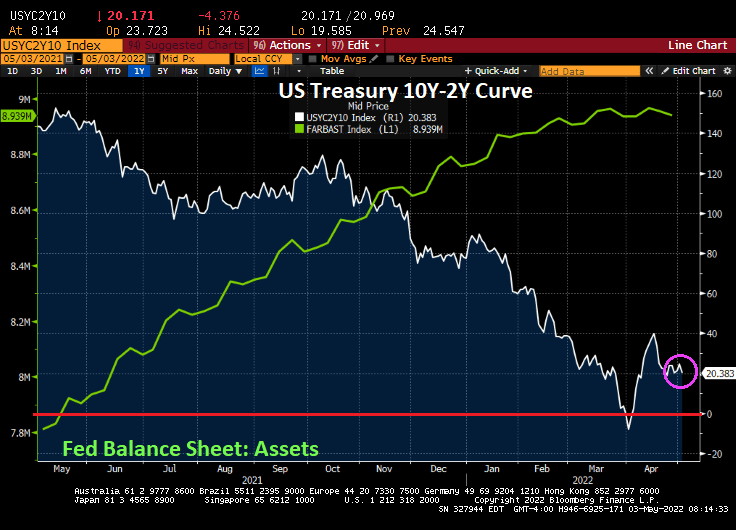

On the hotter than expected inflation news, the US Treasury 10Y-2Y curve flattened to 12 bps.

You must be logged in to post a comment.