The University of Michigan’s consumer sentiment index for housing for October just fell to its lowest level since 1992 as The Fed counterattacks against Bidenflation, causing mortgage interest rates to rise.

Of course, despite slowing home price growth, expensive home prices are really hurting along with expensive rents. But how sustainable are high home prices when REAL average hourly earnings growth is negative??

As the Biden Administration touts “affordable housing,” we are seeing the 30-year mortgage rate rise above 7% as The Federal Reserve fights inflation … caused by the Biden Administration. Meanwhile, US home prices are falling.

The Biden Administration launched a war on domestic energy production, resulting in crude oil prices rising 74% under Biden and regular gasoline prices rising 62.4%.

As Biden pleaded with OPEC to increase oil production, he was embarrassingly rejected. Hence, West Texas Crude Oil prices have begun to rise again along with gasoline prices (pink box).

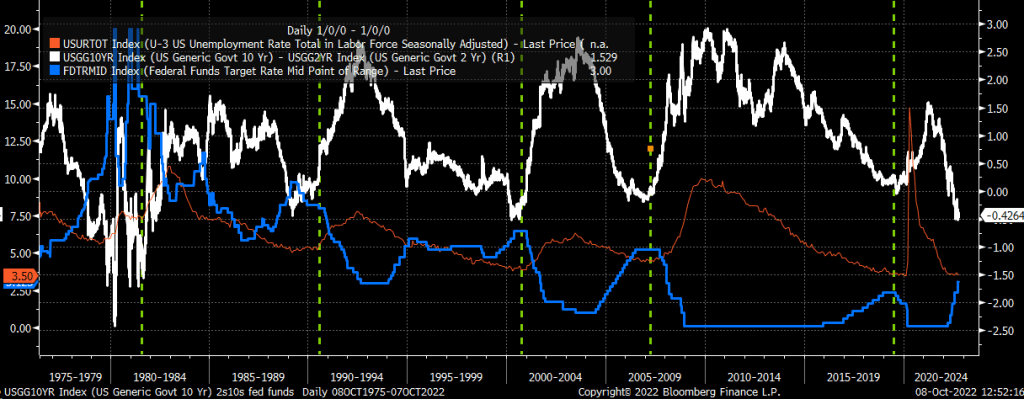

How about unemployment and the 10yr-2yr yield curve?

In addition to creating the highest inflation rate in 40 years, we are now seeing the highest mortgage rate in 16 years. I feel like we are all on a chain gang.

(Bloomberg) — US mortgage rates jumped to a 16-year high of 6.75%, marking the seventh-straight weekly increase and spurring the worst slump in home loan applications since the depths of the pandemic.

In fact, mortgage application just fell to the lowest level since May 1997.

The contract rate on a 30-year fixed mortgage rose nearly a quarter percentage point in the last week of September, according to Mortgage Bankers Association data released Wednesday. The steady string of increases in mortgage rates resulted in a more than 14% slump last week in applications to purchase or refinance a home.

Over the past seven weeks, mortgage rates have soared 1.30 percentage points, the largest surge over a comparable period since 2003 and illustrating the abrupt upswing in borrowing costs as the Federal Reserve intensifies its inflation fight.

The effective 30-year fixed rate, which includes the effects of compounding, topped 7% in the period ended Sept. 30, also the highest since 2006.

The Refinance Index decreased 18 percent from the previous week and was 86 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 13 percent from one week earlier. The unadjusted Purchase Index decreased 13 percent compared with the previous week and was 37 percent lower than the same week one year ago.

Here is today’s table of MBA mortgage applications and its ugly.

Unfortunately for the US chain gang, gasoline prices are rising again as the US drains its petroleum reserve. Because, that’s the way … uh-huh … they like.

US mortgage applications dropped to the lowest level since 1997. I wonder if President Biden will invite boring crooner James Taylor back to the White House to sing about the collapsing mortgage market? Perhaps he can sing “Shower The People” and change the lyrics to “Shower ON The People.”

Mortgage applications decreased 1.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending September 9, 2022. This week’s results include an adjustment for the observance of Labor Day. The Refinance Index decreased 4 percent from the previous week and was 83 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 0.2 percent from one week earlier. The unadjusted Purchase Index decreased 12 percent compared with the previous week and was 29 percent lower than the same week one year ago.

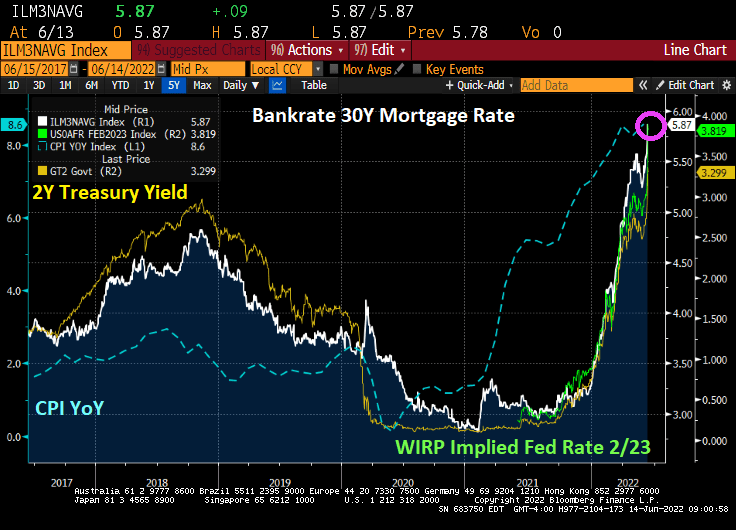

The Bankrate 30-year mortgage rate is now at the highest level since 2008 at the advent of Fed’s QE.

The US housing market is facing stress thanks to The Federal Reserve’s “war on inflation.” As The Fed starts trimming its excess ballast and M2 Money growth YoY slows to the lowest since Pre-Covid, we are seeing housing markets like San Francisco beginning to experience declines in home prices.

According to Redfin, Oakland California is leading the nation in terms of declining sales prices at -15.1% over a 3 month period. Followed by Silicon Valley and San Jose at -12.7%. San Francisco is in third place at -11.2% (I will ignore Lake Havasu AZ since it is teeny but does have one of the London Bridges) and Austin TX is in 5th place at -9.7%.

The monetary noose tightens on the housing and mortgage markets.

Mortgage applications decreased 0.8 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending September 2, 2022. They are now the lowest since 1999.

The Refinance Index decreased 1 percent from the previous week and was 83 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index decreased 3 percent compared with the previous week and was23 percent lower than the same week one year ago.

At least the percentage of adjustable rate mortgages (ARMs) remained the same at 8.5%.

For the sake of the housing and mortgage market, somebody stop Powell and The Gang from tightening!

Thanks to Federal Reserve increases in their target rate, the 30-year mortgage rate has risen above 6%.

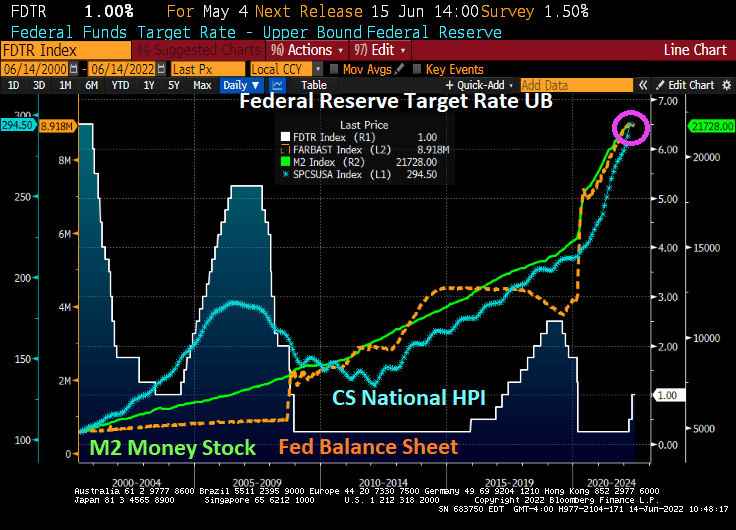

What drives me crazy about The Fed is their failure to removed monetary stimulus following the financial crisis of 2008 when they dropped their target rate to 25 basis points (0.25%) and began assets purchases (orange line). The Fed raises their target rate only once during Obama’s Presidency but then raised rates 8 times after Trump was elected President.

Now we are seeing The Fed NOT shrinking their balance sheet in a meaningful way. However M2 Money growth YoY (green line) has slowed to 5.2%.

While it is a good thing that The Fed is FINALLY reducing some of the monetary stimulus in place since 2008, the bad thing is that mortgage rates are rising rapidly.

The Fed’s quantheads are predicted to resume easing in March 2023.

The US housing market is sensitive to Fed “catch-up” monetary tightening. For example, the NAHB’s traffic of prospective homebuyers declined rather dramatically in August as The Fed tightened rates and the 30yr mortgage rate rose. That is what I call a “Nestea Plunge.”

How are mortgage rates impacted by Fed monetary policy? While The Fed began really “sloshing” markets with excess stimulus (QE in late 2008), the latest round of QE (or asset purchases) came with the US Covid shutdowns (what genius thought of that??) and that stimulus has NOT been withdrawn yet. Only the Fed Funds Target rate has tightened.

The 30yr mortgage rate rose with Fed rate tightening, but the Fed’s System Open Market Holdings (SOMH) of Treasury Notes and Treasury Bonds has come down a bit. But not the pare-down The Fed has hinted at. The 30yr mortgage rate is cooling as the prospect of future Fed rate hikes declines.

As of this morning, The Fed Funds Futures market points to rates rising until March 2023 … then easing again.

One reason The Fed has been slow to sell assets off its balance sheet is that a large chunk of T-Notes and T-Bonds are maturing shortly. It will be a matter of whether The Fed reinvests the proceeds or lets the balance sheet wind-down.

The US economy is slowing as inflation ravages consumers. US Regular Gasoline prices, for example, are up 104% under President Biden which helps to slow the economy.

US personal consumption expenditures fell to +0.2% MoM in May as “inflation” or real personal consumption expenditures PRICES rose +6.3% YoY as The Fed’s balance sheet (aka, Master Blaster!) remains.

As I mentioned above, US regular gasoline prices are UP 103% under President Biden, diesel prices (the cost of shipping goods to markets like … food is up 119% under Biden while CRB foodstuffs is up 55% under China Joe.

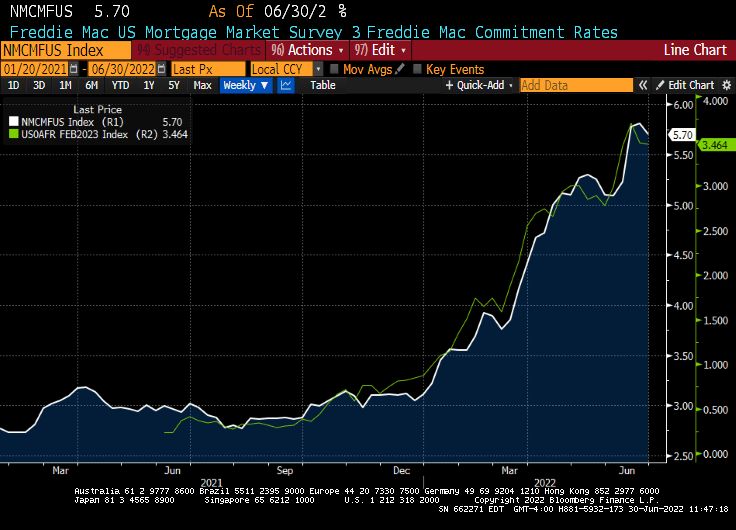

Now we have mortgage rates in the US falling for the first time in four weeks. The average for a 30-year loan was 5.7%, down from 5.81% last week, Freddie Mac said in a statement Thursday.

This year’s Fourth of July celebration is going to cost 18% more than last year’s celebration.

Lastly, the Atlanta Fed GDPNow real time tracker for Q2 is showing … -1% GDP “growth.”

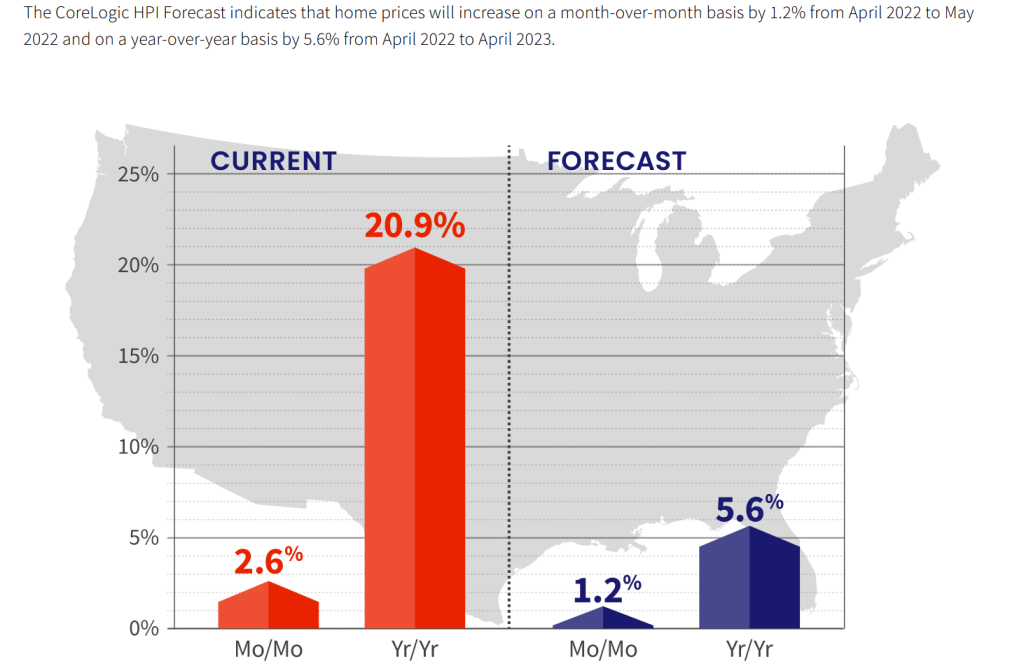

US home prices are still skyrocketing as The Federal Reserve kept its massive foot on the monetary accelerator pedal.

CoreLogic’s home price index grew at a 20.9% YoY pace in April, but is expected to slow to 5.6% YoY in late 2022.

Remember peeps, The Fed still have its staggering monetary stimulypto in place.

The Fed is signaling its withdrawal of stimulus, causing mortgage rates to soar.

Given the slowdown of the US and global economy, we shall see if The Fed keeps to its tightening plans. As of today, the market is expecting The Fed to raise its target rate from 1% to 3.819% by February 2023. That is a 291% increase in The Fed’s target rate.ng

The Fed trying to tame inflation (caused by The Fed and Biden’s energy policies and Congressional spending) is like Curly trying to eat oyster stew.

You must be logged in to post a comment.