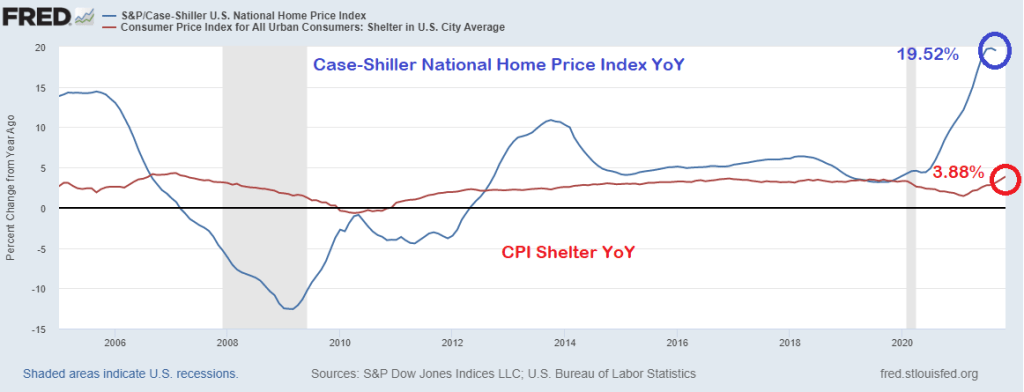

But that 6.9% YoY is very misleading because of the strange way the Bureau of Labor Statistics measures the largest asset in most households’ expenditures: housing.

The BLS measures inflation in housing using the Shelter measurement. Which was only 3.88% YoY. The problem is that the Case-Shiller National Home Price Index was 19.52% in its last reading. That is quite a discrepancy.

So, if we substitute the Case-Shiller National home price index for the CPI Shelter, we get an inflation rate of greater than 11%.

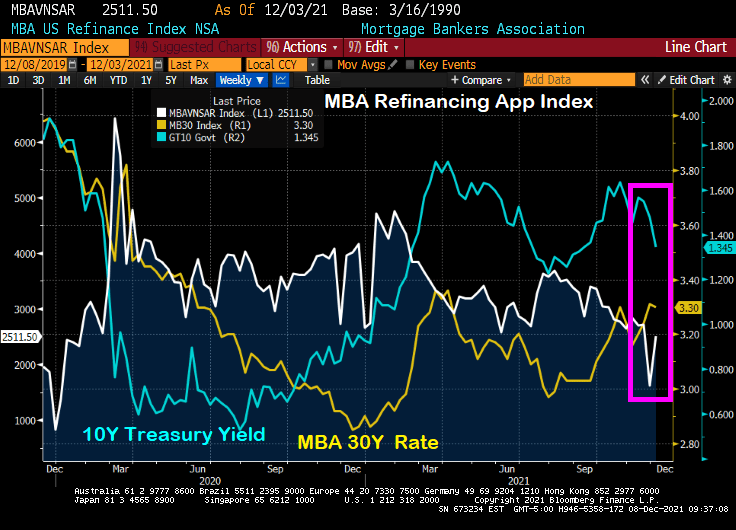

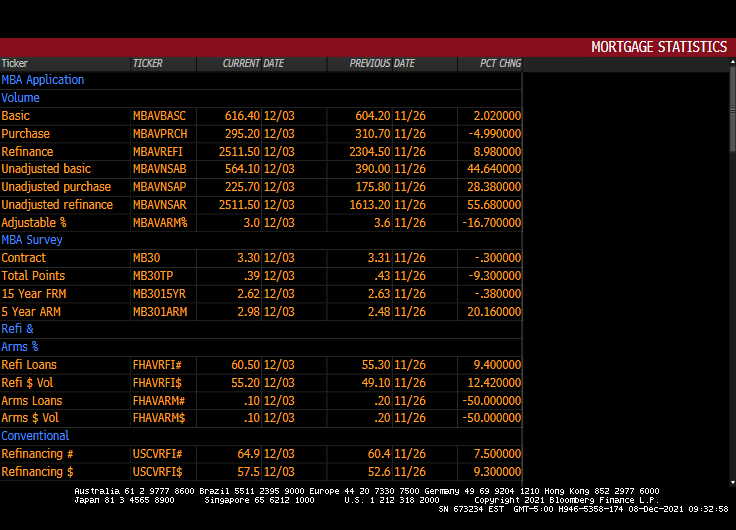

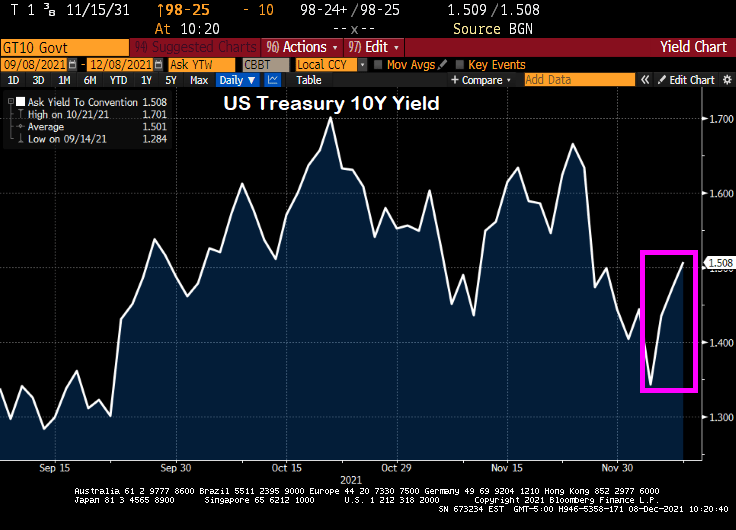

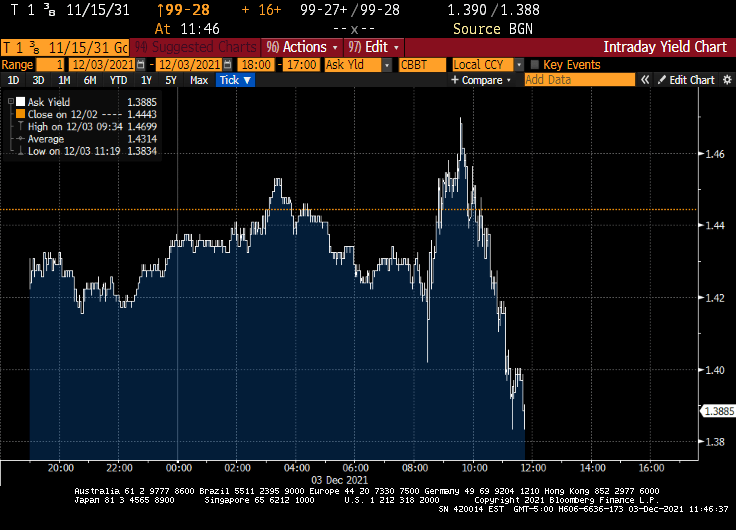

Despite the “Talk, Talk” from The Federal Reserve about balance sheet taper and rate “normalization,” we actually saw the 10-year Treasury yield fall from 1.6651% on 11/23/2021 to 1.343 on 12/3/2021. While the 30-year mortgage rate only fell from 3.31% to 3.3%, it is the SIGNAL that The Fed is sending that people should refinance their mortgages ASAP.

You can see the rise in mortgage refinancing applications of 56% week-over-week (WoW) (white line) with the drop in the 10-year Treasury yield (blue line) despite the relatively small drop in the Mortgage Bankers Association (MBA) tiny drop in their 30-year mortgage rate index.

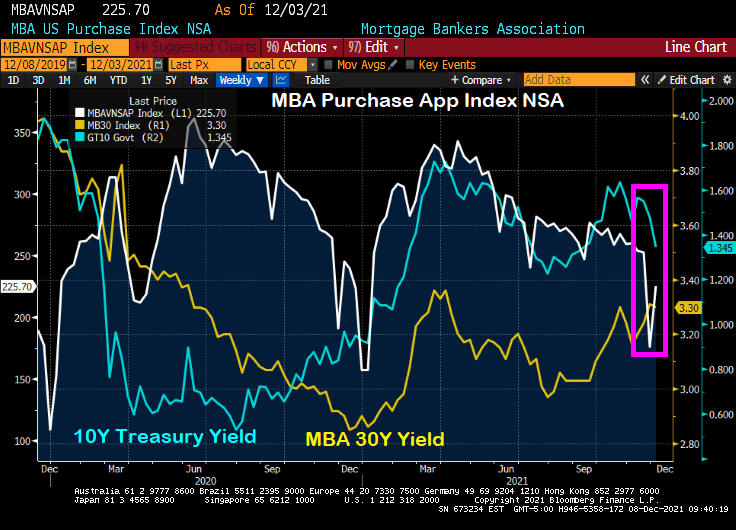

Ditto for the MBA mortgage purchase application index. The drop in the US Treasury yield (blue line) resulted in a 28% WoW increase in mortgage purchase applications.

Here is the table of MBA data for the week of 12/03.

Please note that the 10-year Treasury yield have jumped since 12/03 indicating that mortgage application activity for the week of 12/10 will be lower.

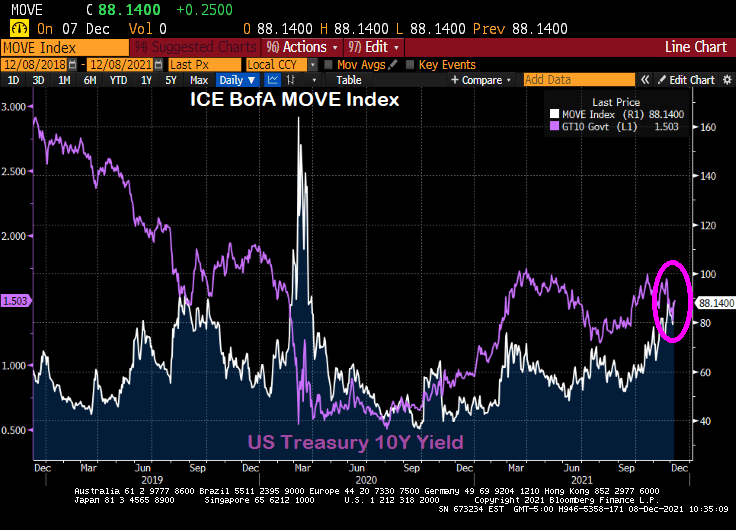

Here is the MOVE bond volatility index and the US Treasury 10-yield chart. Can you spot the COVID outbreak??

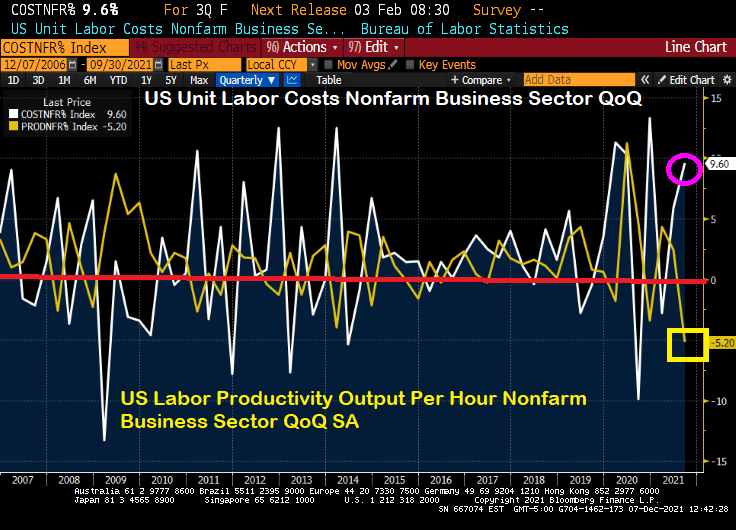

If this what the Biden Administration had in mind? Soaring labor costs at the same time that labor productivity is falling to its lowest level since 1960?

Powell and the Gang’s monetary approach doesn’t seem to be working for the labor market …

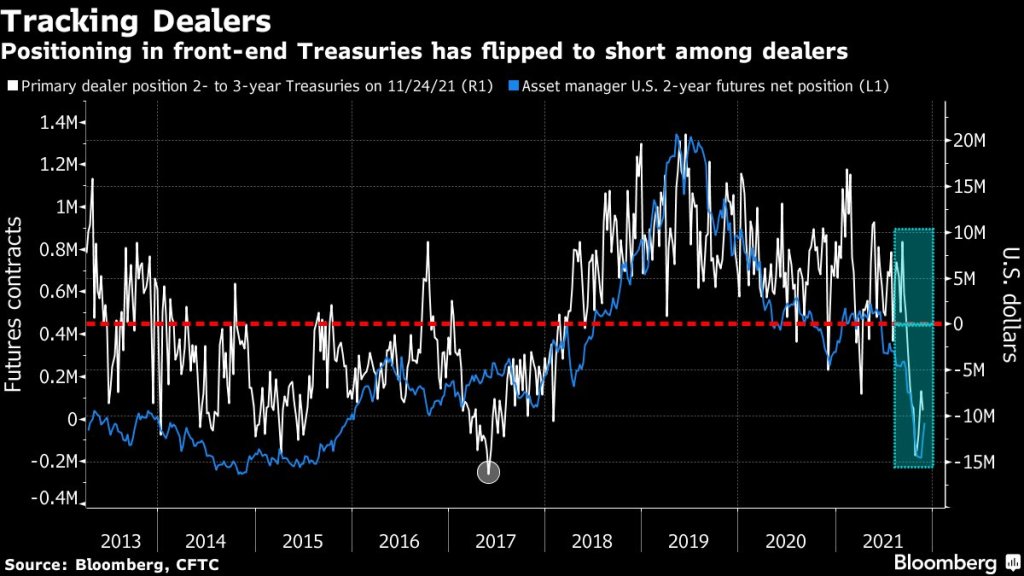

(Bloomberg) — The recent drop in primary-dealer holdings of front-end Treasuries is another warning of potential market dislocation heading into the year-end liquidity vacuum.

As of Nov. 24, primary dealers — which are mostly the large banks — were on the whole betting against two- to three-year Treasuries rather than buying. They had net short positions of just over $9 million, near the most bearish levels since 2017, signaling a pullback by buyers that provide crucial liquidity for older Treasury issues.

The positioning in the front-end of the curve “suggest less demand from the dealer community to fund off-the-run long positions,” Barclays strategists Anshul Pradhan and Andres Mok say in a Dec. 3 note. Off-the-run Treasuries are notes and bonds created in past years and traded less frequently than the newest issues; they’re the biggest part of the market and make up most of the Federal Reserve’s daily asset purchases, which are being scaled back.

Short positioning increased on a relative basis as a result, “which may also have crowded demand to borrow particular issues over others,” the analysts wrote.

Those forces together could contribute to an increase in market dislocations.

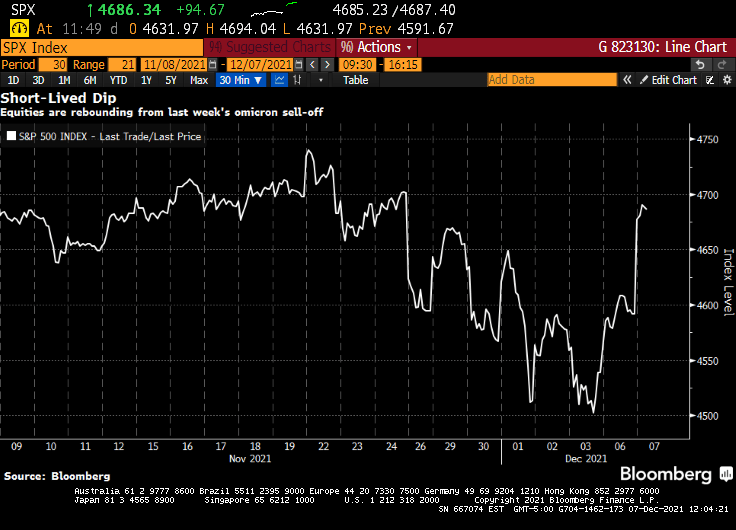

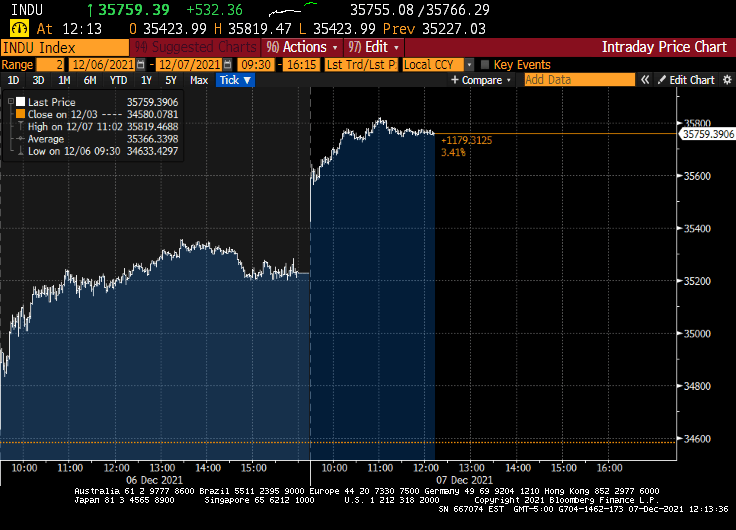

Jerome Powell’s hawkish pivot shocked financial markets. A week later, stocks are higher. The S&P 500 staged its biggest rally since March to wipe out losses from the past week. The speculative fringe that was a smoldering wreck Friday was soaring Tuesday. An index of meme stocks rallied more than 4%, while one composed of airlines added 1.6%. A gauge of newly public companies advanced more than 4%, SPACs jumped more than 2% and even cryptocurrencies rallied, with Bitcoin powering back above $51,000.

It’s a stunning about-face for risk assets that went into a tail spin after the Federal Reserve chair suggested he favored accelerating the removal of monetary support. What follows are takes from market-watchers on why the market is looking past the Fed’s potential change in policy.

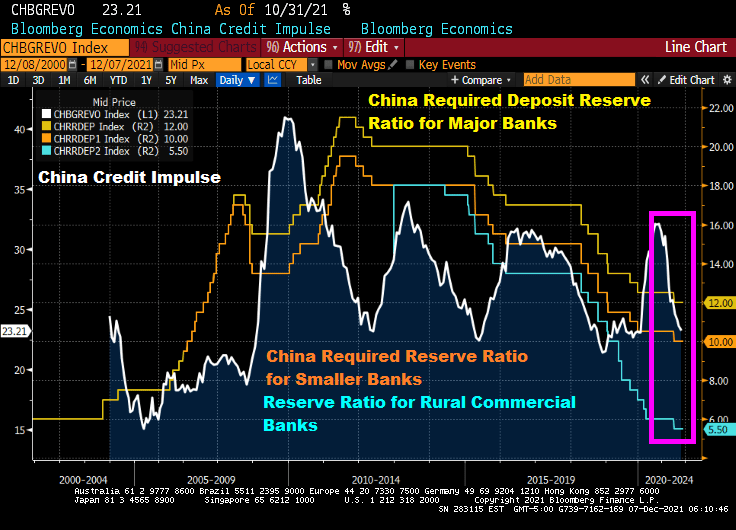

China cut the amount of cash most banks must hold in reserve, acting to counter the economic slowdown in a move that puts the central bank on a different policy path than many of its peers.

The People’s Bank of China will reduce the reserve requirement ratio by 0.5 percentage point for most banks on Dec. 15, releasing 1.2 trillion yuan (US$188 billion) of liquidity, according to a statement published Monday.

The reduction was signaled by Premier Li Keqiang last week when he said that authorities would cut the RRR at an appropriate time to help smaller companies, and is the second reduction this year.

The decision comes after recent data showed the economy and industry stabilizing, although Beijing’s tightening curbs on the property market have led to a slump in construction and worsened a liquidity crisis at developer China Evergrande Group and other real estate firms.

Evergrande’s ADR is collapsing (now 5.975) along with Evergrande debt falling to 23.12 (versus 100 par).

China’s credit impulse has nosedived (see pink box) as the PBOC drops bank reserve ratios to lowest level since 2007 in an effort to float the boat. Will the PBOC drop in reserve ratios stem the tide? Or is it peasant magic?

Russia and Brazil are tightening along with Mexico, Colombia, Peru, Argentina and Chile. Add Pakistan, The Czech Republic and Poland to the list of tighteners.

The looseners? The US, of course, with Canada, Australia, China, India, Western Europe, Turkey and Nigeria. New Zealand is the quickest loosener.

This looks very cold war-like. But a monetary cold war.

Let’s see if The Fed becomes a tightener rather than a loosener.

Treasury Secretary Janet Yellen said yesterday that “It’s Fed’s Job to Avoid Any Wage-Price Spiral.” Well, The Fed is helping to avoid a wage increase in real terms, since the November jobs report revealed that REAL US Average Hourly Earnings growth YoY fell to -1.378%. In other words, inflation is greater than hourly earnings.

And in other jobs related news, nonfarm payrolls rose by only 210k versus expectations of 550k jobs to be added. Even NOMINAL hourly earnings growth (4.8% YoY) was less than expected (5.0%).

Labor force participation rose a bit to 61.8%, still well below the pre-COVID levels of 63.4% in January 2020.

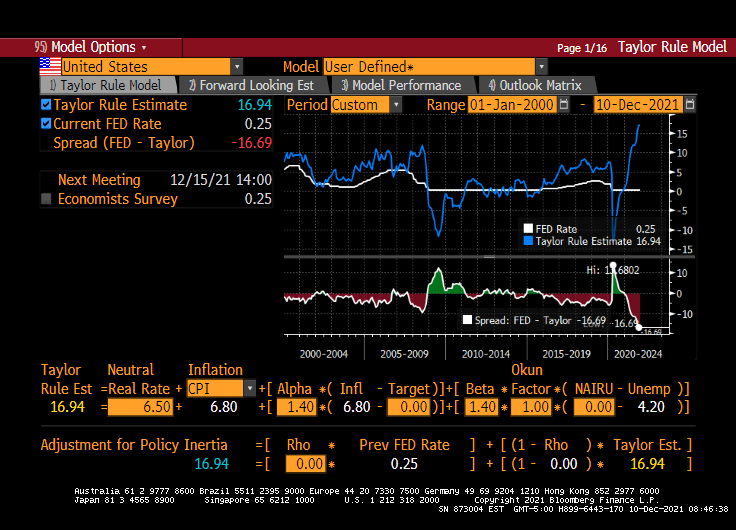

The U-3 unemployment fell to 7.8%. Still higher than the pre-COVID rate of 7.0% in February 2020, but getting close! As for what this means for The Fed, the new target rate implied by the Taylor Rule is 15.50%.

After this lousy jobs report, 10-year Treasury yields dropped … like Biden’s approval ratings.

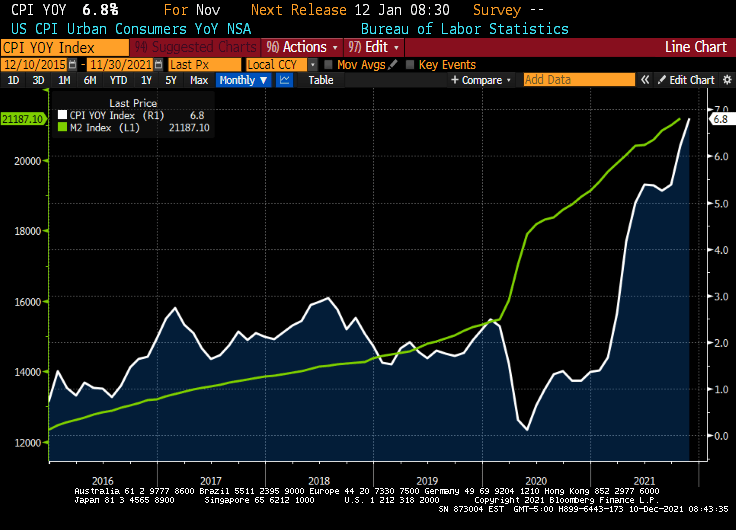

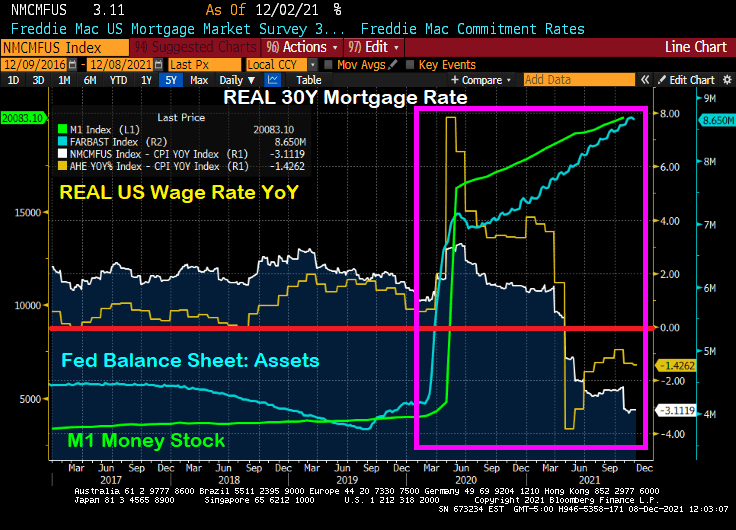

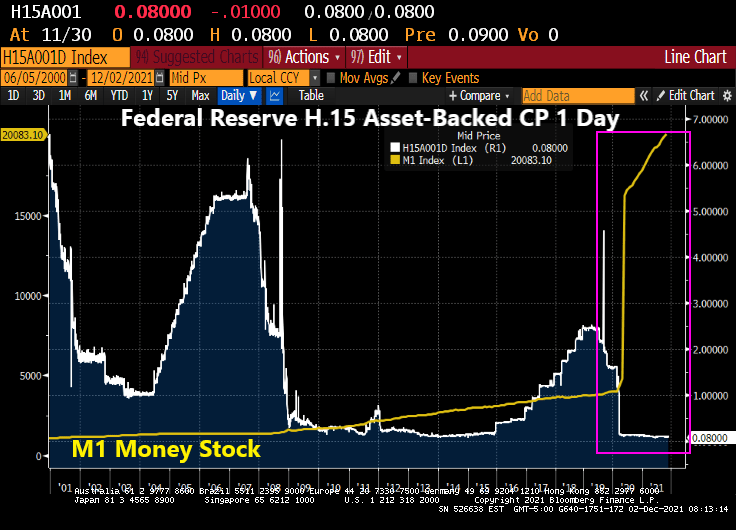

The Dream Team (Fed Chair Jay Powell and Treasury Secretary Janet Yellen) just can’t believe that inflation struck even after M1 Money Stock increased by 369% from March 2020 to today while interest rates remained near zero.

From The Hill: Federal Reserve Chairman Jerome Powell and Treasury Secretary Janet Yellen on Wednesday said they underestimated how quickly the U.S. economy would rebound from the COVID-19 recession and strain supply chains.

During a Wednesday hearing before the House Financial Services Committee, the top two U.S. economic policymakers acknowledged that high inflation has risen higher and lingered much longer than they expected.

“We understood demand would be strong,” Powell said. “We didn’t understand [the] significant problems of the supply side.”

Both Yellen and Powell said substantial fiscal and monetary stimulus played a role in stoking the higher demand that fueled inflation, but they called it a challenging side-effect of an otherwise fast recovery.

Seriously? The Fed and the Federal government dumped trillions of dollars into an economic system and didn’t think there would be negative consequences??

Look at the surge in M1 Money Stock at the same time asset-backed commercial paper rates are 0.08%. That is, about 1/3rd The Fed Funds Target rate (upper bound). None of this concerned The Dream Team?

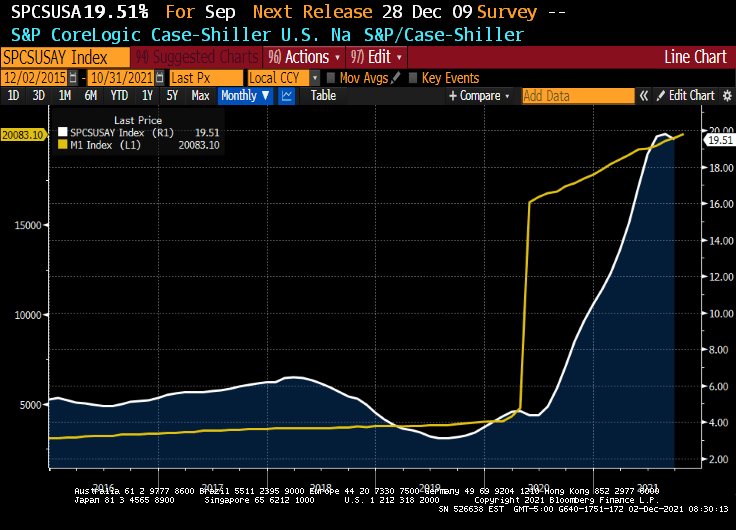

An example of what The Dream Team didn’t see happening was the explosion of home prices. Home price growth was about 4% YoY prior to COVID, and is now 19.51% YoY.

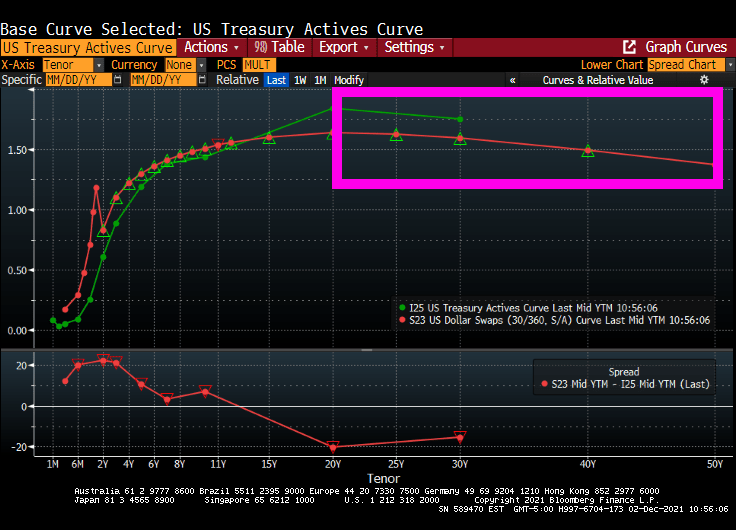

Now we have the US Treasury Actives curve inverting like the US Dollar Swaps curve after 20 years.

You must be logged in to post a comment.