Big bubbles! US home pricest hit an all-time high as The Fed keeps its foot on the monetary gas pedal following the Covid economic shutdown in 2020.

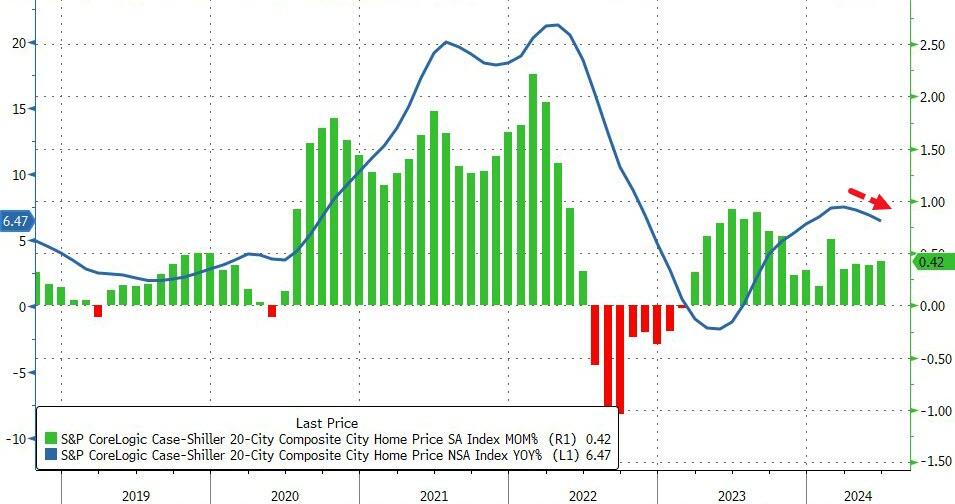

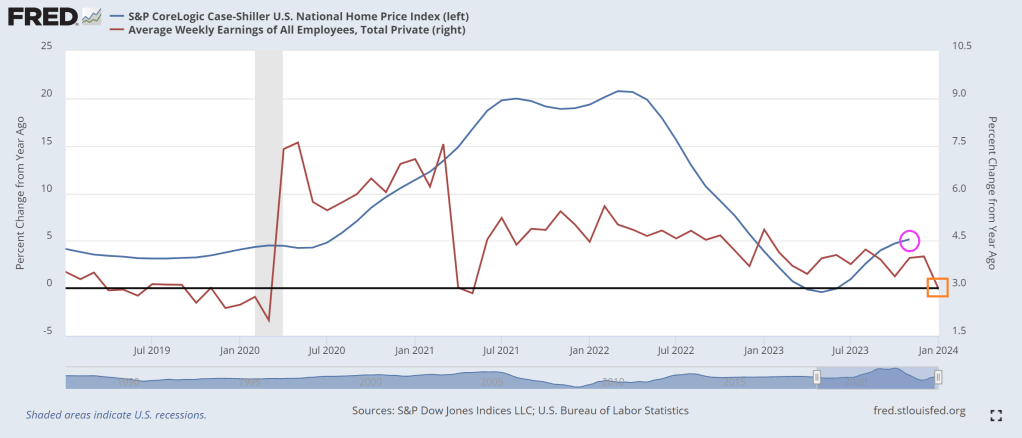

Home prices in America’s 20 largest cities rose for the 16th straight month in June (according to the latest data from S&P CoreLogic – Case Shiller – data today), up 0.42% MoM (hotter than expected and accelerating from May). On a YoY basis, prices rose 6.47%, but notably that is the third straight monthly slowdown in the pace of price appreciation…

Source: Bloomberg

Overall, US home prices reached a new record high in June (as median new home prices continued to tread water)…

Source: Bloomberg

Home prices continue to track Fed Reserves closely, but a turning point may come soon…

Source: Bloomberg

Given the smoothing and heavy lag in the Case-Shiller data, it’s hard to find a causal relationship between prices and mortgage rates…

Source: Bloomberg

But, with prices reaccelerating and mortgage rates already back below 7.00% – in anticipation of The Fed – WTF does Powell think is going to happen when he actually starts cutting with prices at these record highs.

The Freddie Mac HP index shows the variation in home price growth. New Jersey coastal towns of Atlantic City and Ocean City grew at 10% YoY while Lake Charles LA declined by -2% YoY.

The US is already at $35+ trillion with unfunded liabilties totalling $218+ trillion. Of course, the Biden Administration is attempting to cut Medicare for seniors and raise the price while handing out unlimited benefits to illegal immigrants.

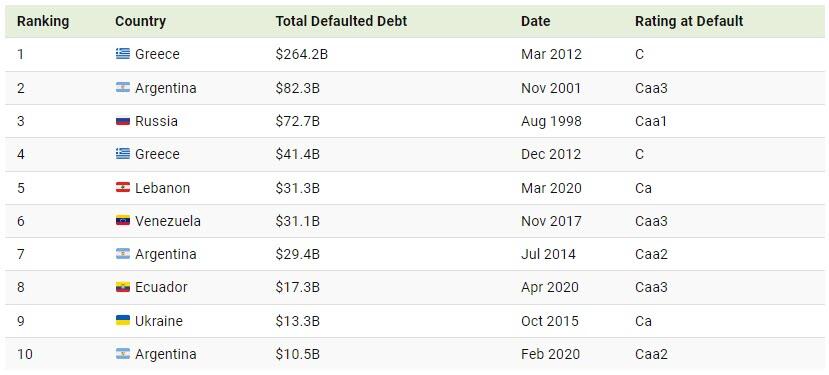

.Given the financial burden of war, the country suspended interest payments on international debt over the last two years, which was set to expire on August 1, 2024.

Without this new debt restructuring, this default would have ranked among the 10 largest in recent history. The last time Ukraine defaulted on its debt was in 2015, after Russia’s invasion of Crimea.

Below, we show the biggest sovereign debt defaults between 1983 and 2022:

Greece’s $264.2 billion default in 2012 stands as the largest overall, unfolding when the country was mired in recession for the fifth consecutive year.

The country defaulted again just nine months later, making it the fourth-largest ever. Leading up to the crash, Greece ran significant deficits despite being one of the fastest-growing countries in Europe. Furthermore, in 2009, the newly elected prime minister revealed that the country was $410 billion in debt—substantially more than previous estimates.

With the second-highest default recorded, Argentina failed to repay interest on $82.3 billion in foreign debt in 2001. Like Greece, it is a repeat offender, defaulting numerous times since independence in 1816. Today, Argentina is the largest debtor to the International Monetary Fund, despite being Latin America’s third-largest economy.

Following next in line is Russia’s 1998 default on $72.7 billion in loans, coinciding with a currency crisis that erased more than two-thirds of the ruble’s value in a matter of weeks. That year, several other countries including Venezuela, Pakistan, and Ukraine defaulted on their debts after the Asian Financial Crisis of 1997 spurred instability in global financial markets.

Just as 1998 saw a wave of defaults, 2020 was a year marked by major debt upheavals. Due to the pandemic and collapsing oil prices, it was a record year for sovereign defaults, reaching seven in total. Among these, Lebanon, Ecuador, and Argentina saw the largest defaults amid deepening fiscal pressures.

Harris is just another free-spending politician who will eventually lead the US into default. But at least Harris/Walz exude joy.

At least Harris/Walz haven’t adopted (stolen) the phrase “Work makes one free”.

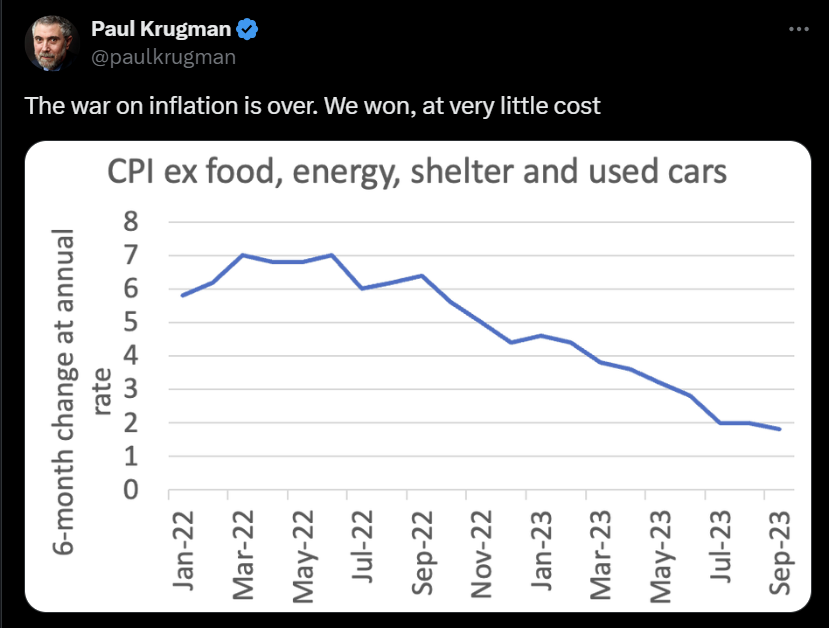

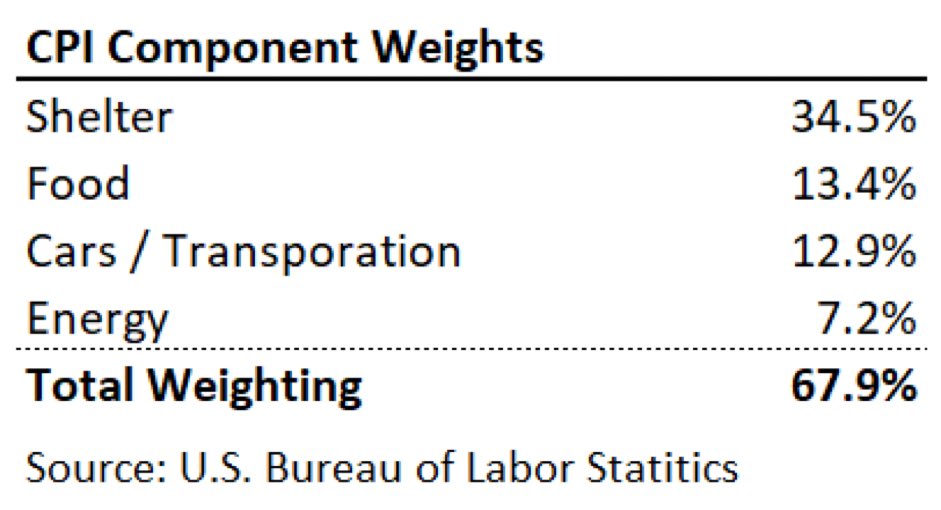

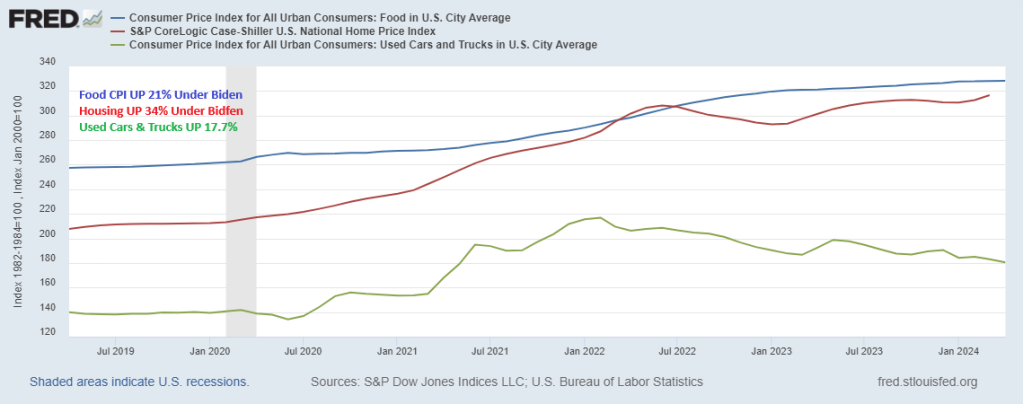

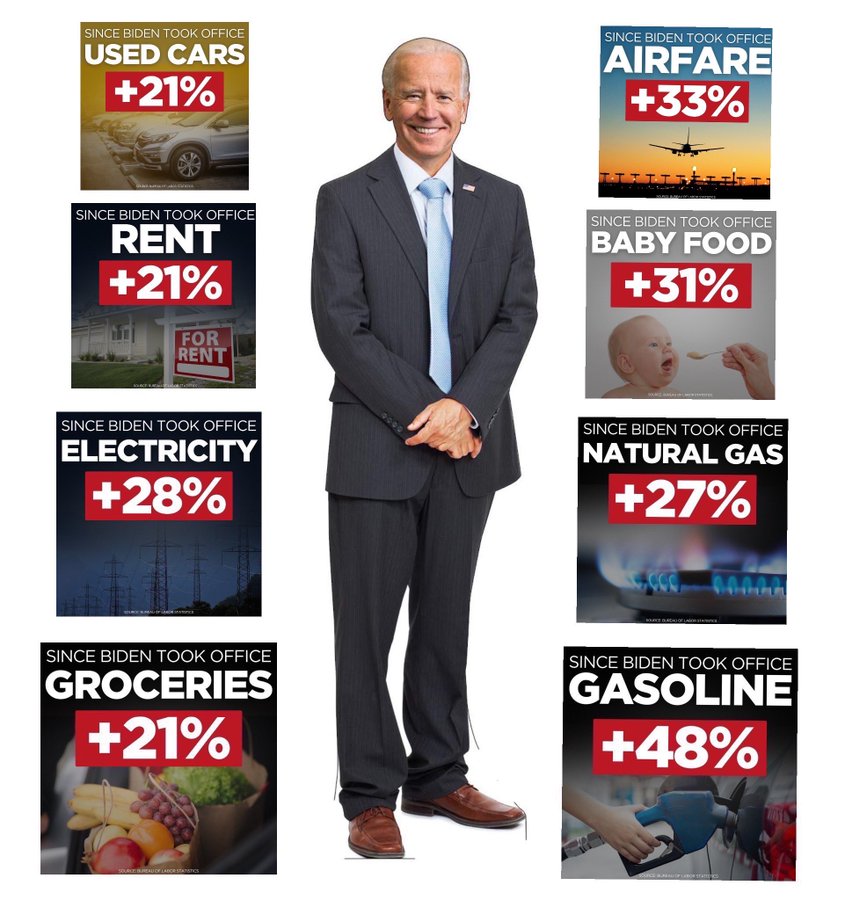

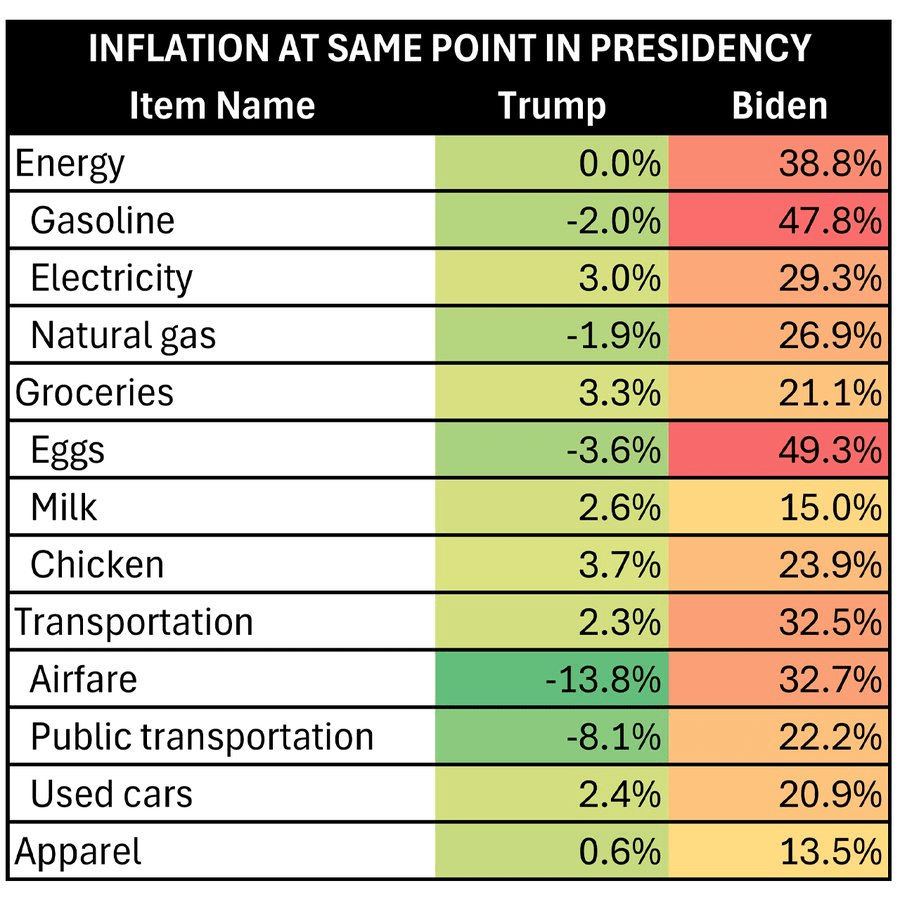

Back in 2023, Socialist Paul Krugman declared that “the war on inflation is over!!! “We” won, at very little cost.” I love when elitists claim “We won!” since clearly 99% of Americans lost since food, housing and car prices up are double digits under Biden.

The problem is that food, energy, shelter, and used cars/trucks are a huge part of Americans consumption basket.

Under Biden, food CPI is up 23%. Home prices are up 34% and used cars/truck prices are up 17.7%.

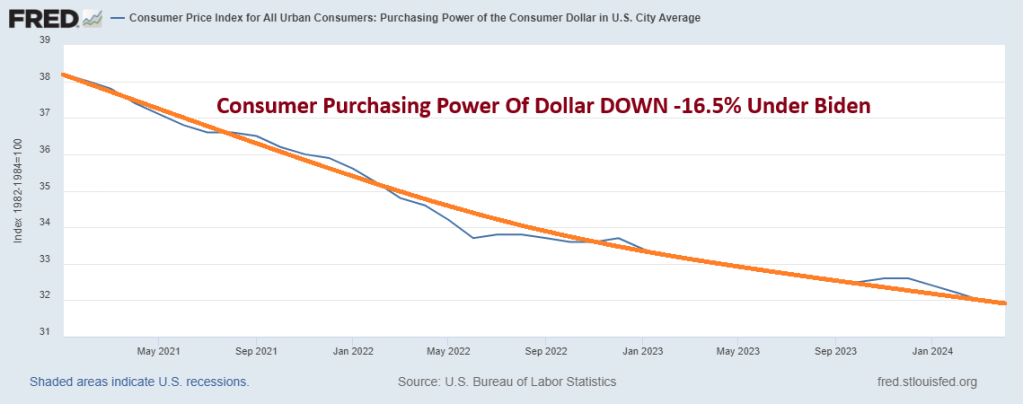

A note to Paul Krugman, YOU may have won, but the rest of Americans lost. Consumer purchasing power of the US Dollar is DOWN 16.5% Under Biden.

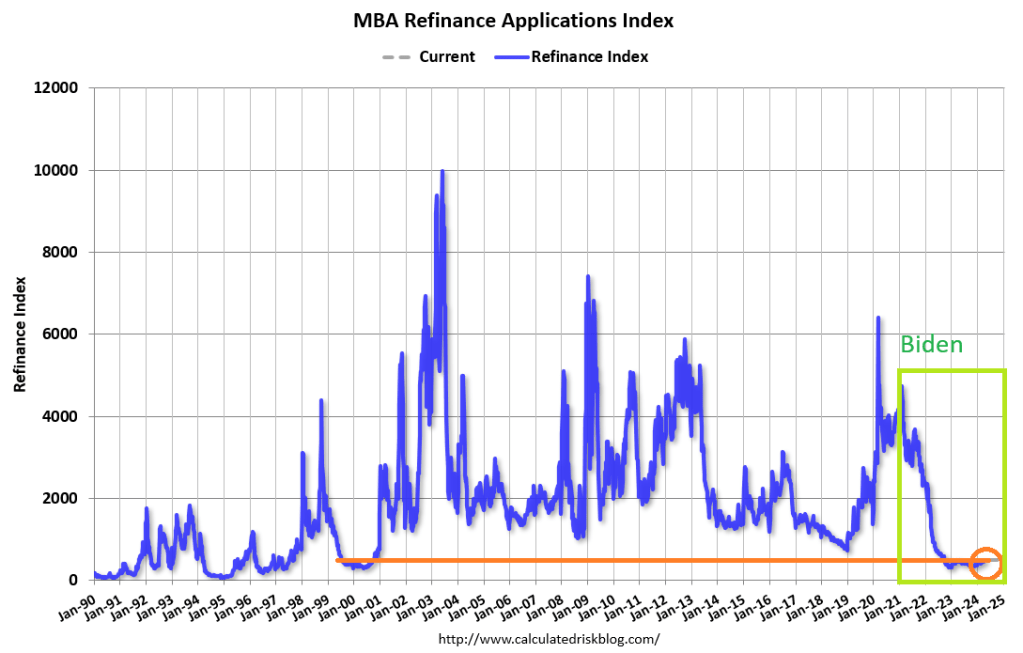

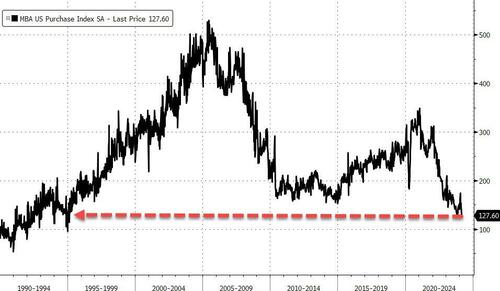

Mortgage applications increased 3.3 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending April 12, 2024.

The Market Composite Index, a measure of mortgage loan application volume, increased 3.3 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 4 percent compared with the previous week. The seasonally adjusted Purchase Index increased 5 percent from one week earlier. The unadjusted Purchase Index increased 6 percent compared with the previous week and was 10 percent lower than the same week one year ago.

The Refinance Index increased 0.5 percent from the previous week and was 11 percent higher than the same week one year ago.

Bidenomics, a massive subsidy to the political donor class, but heartless towards the middle class.

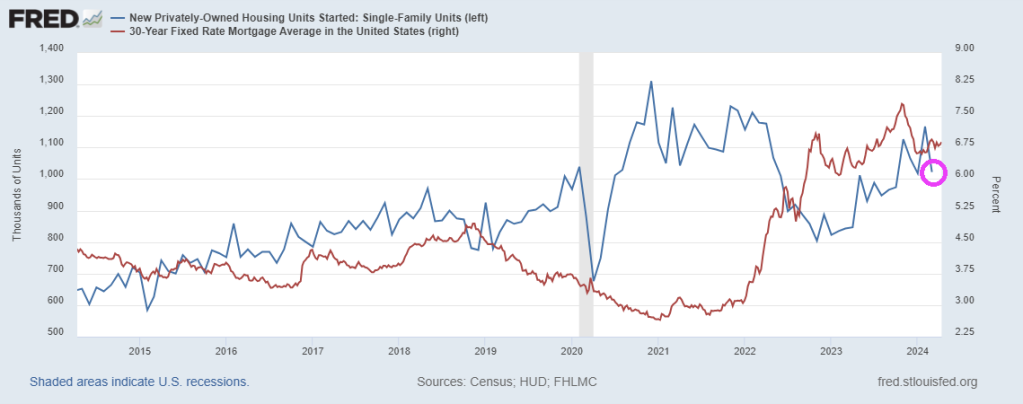

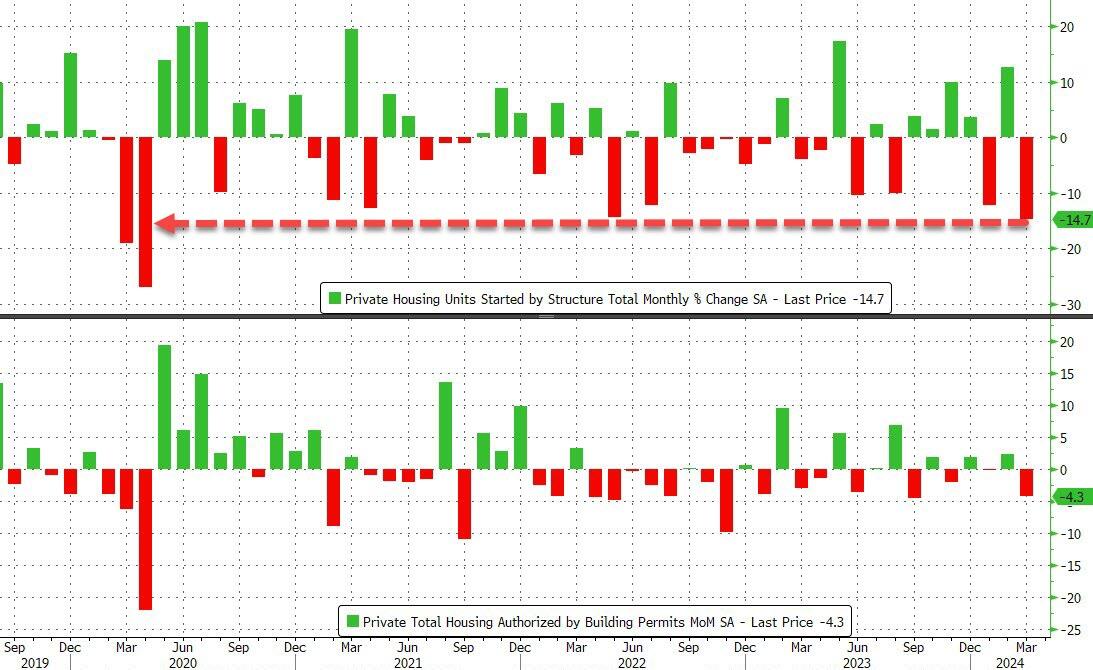

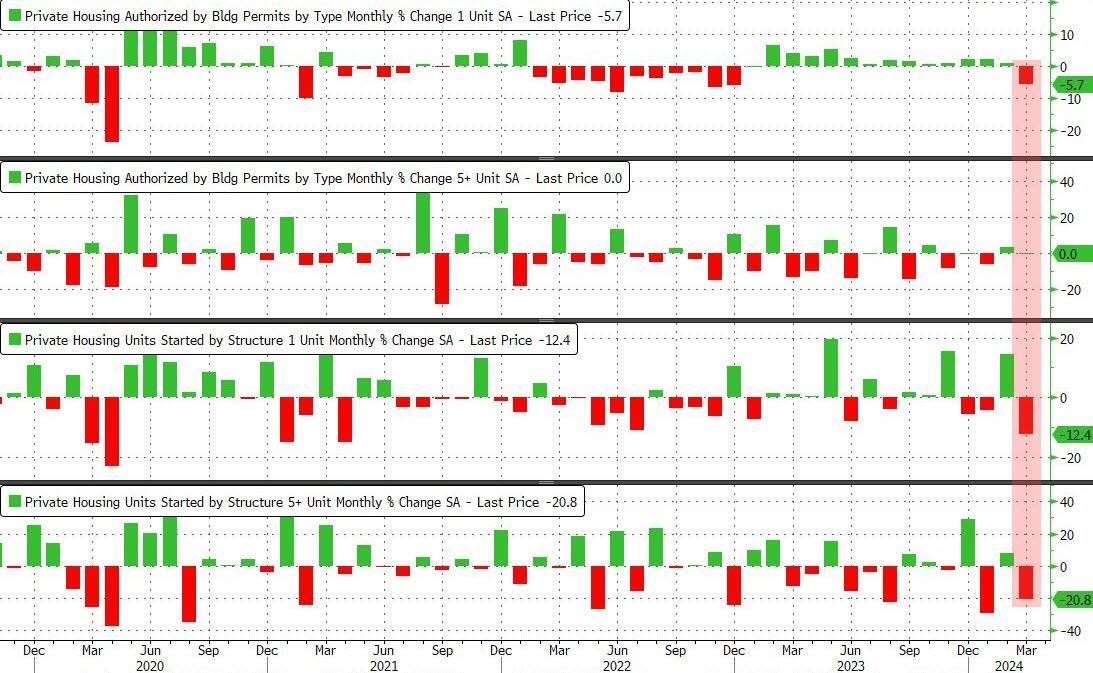

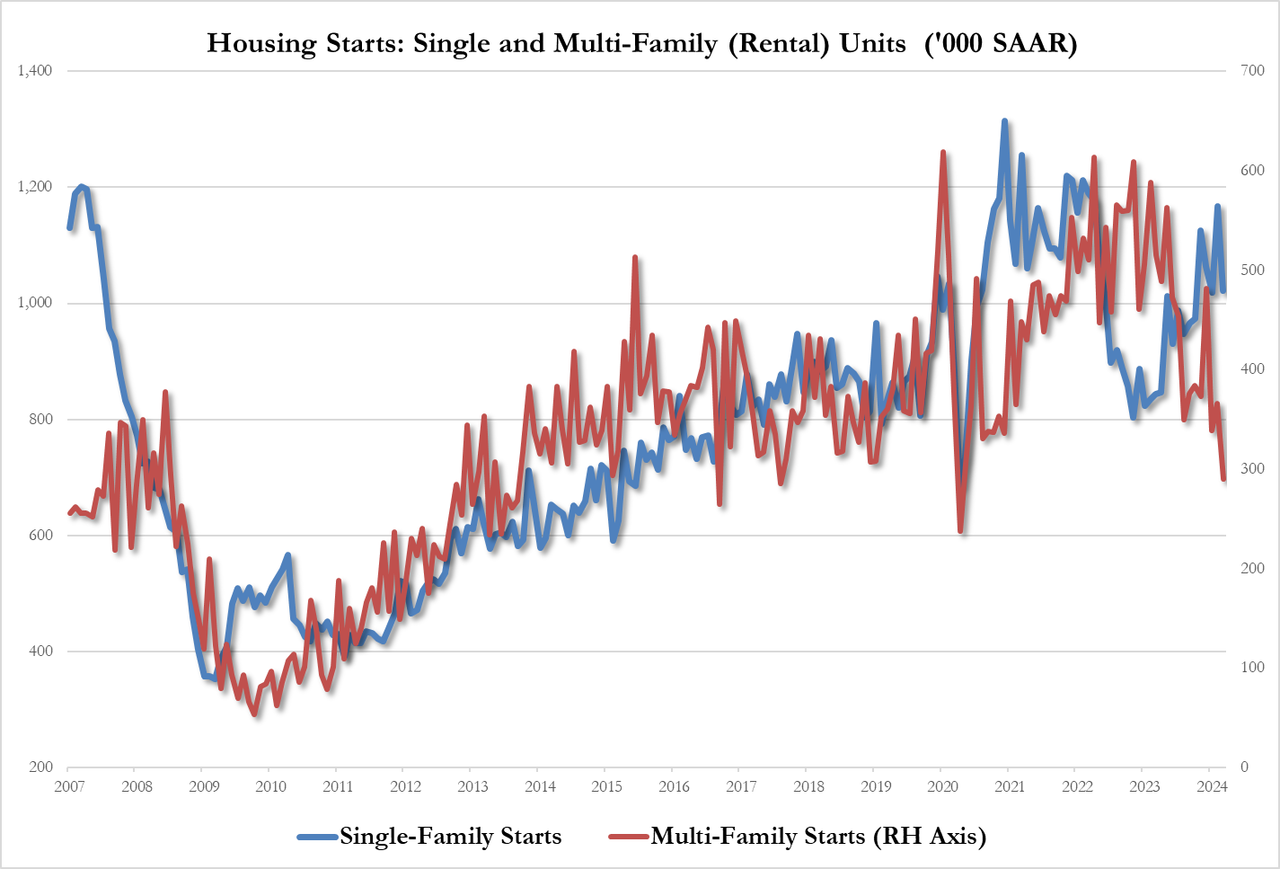

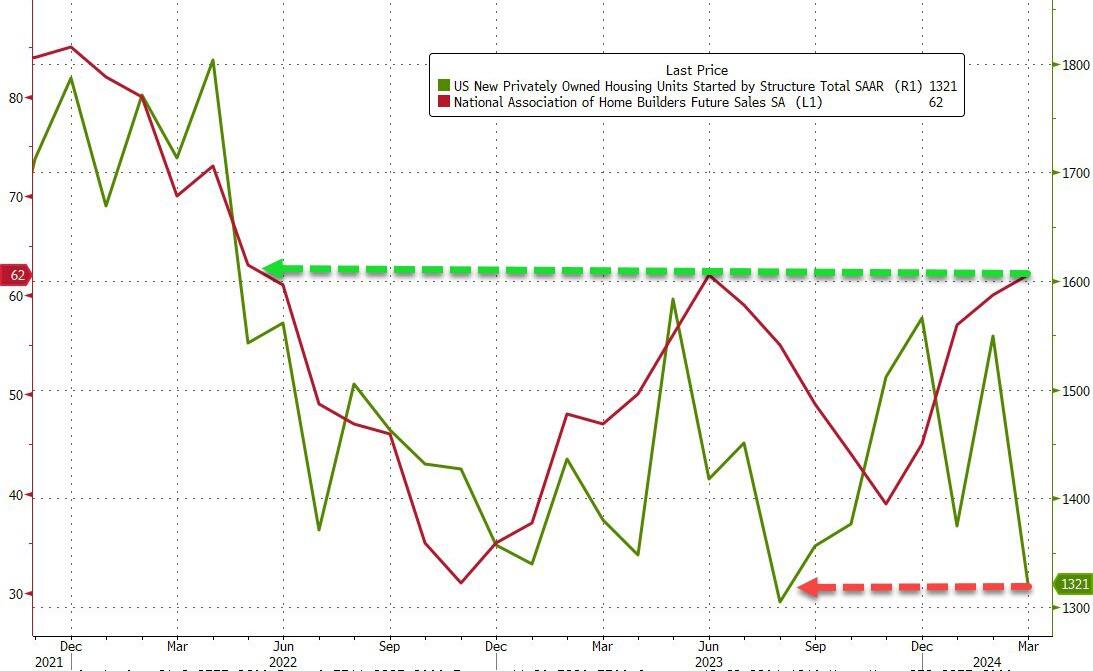

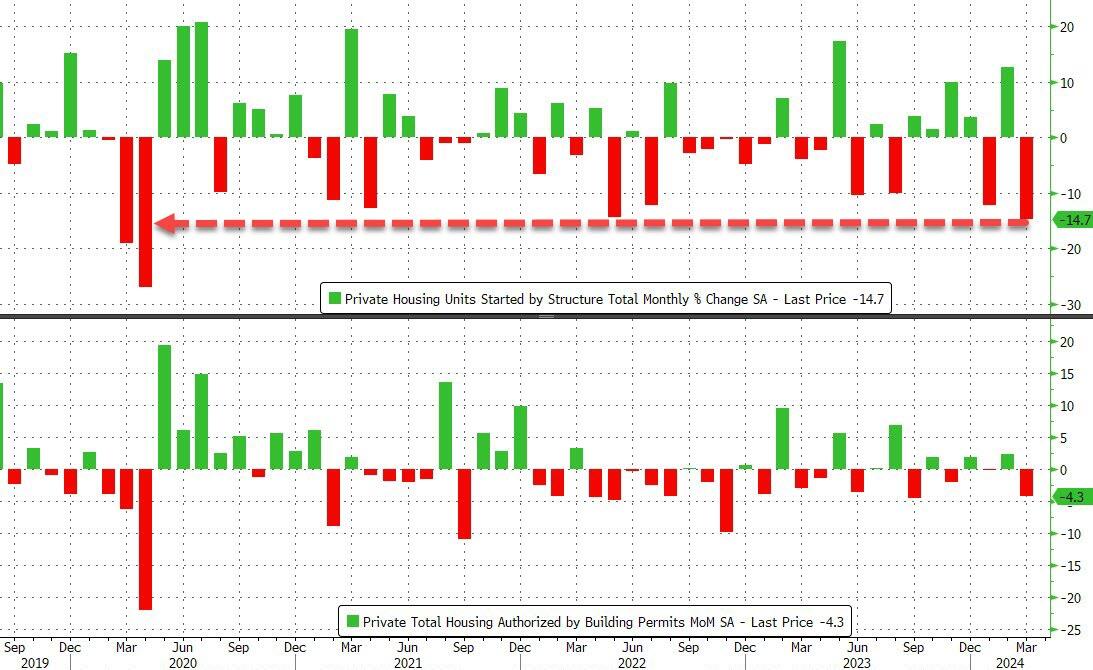

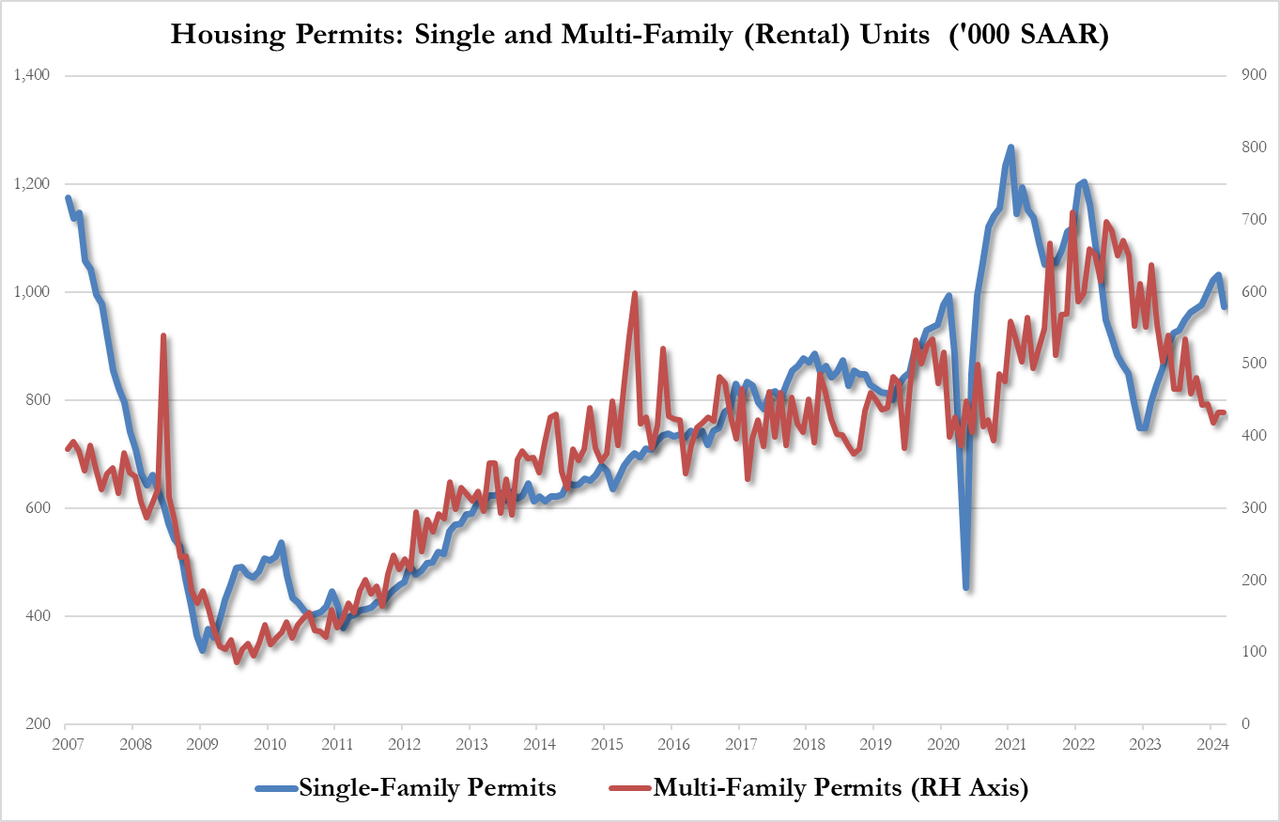

Come feel the noise! After steady growth in 1-unit housing starts under Trump, housing starts have been eratic under Biden despite the foreign invasion force of millions … of low wage workers.

For context, this is the largest MoM drop in housing starts since the COVID lockdowns…

Source: Bloomberg

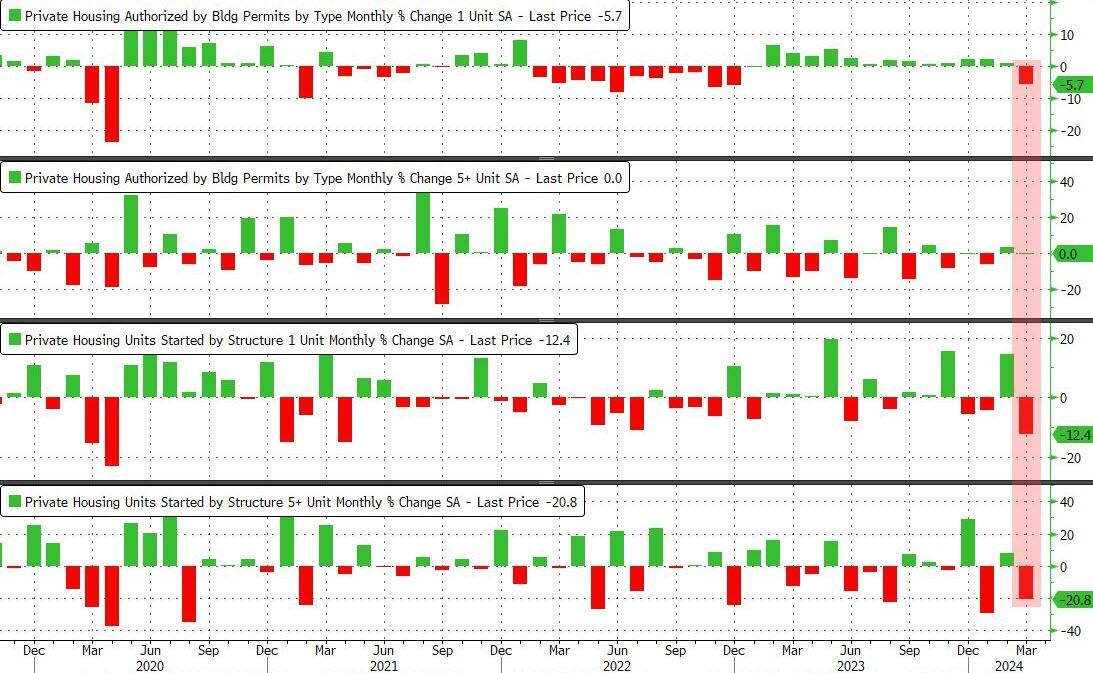

It was a bloodbath across the board with Rental Unit Starts plummeting 20.8% MoM…

Source: Bloomberg

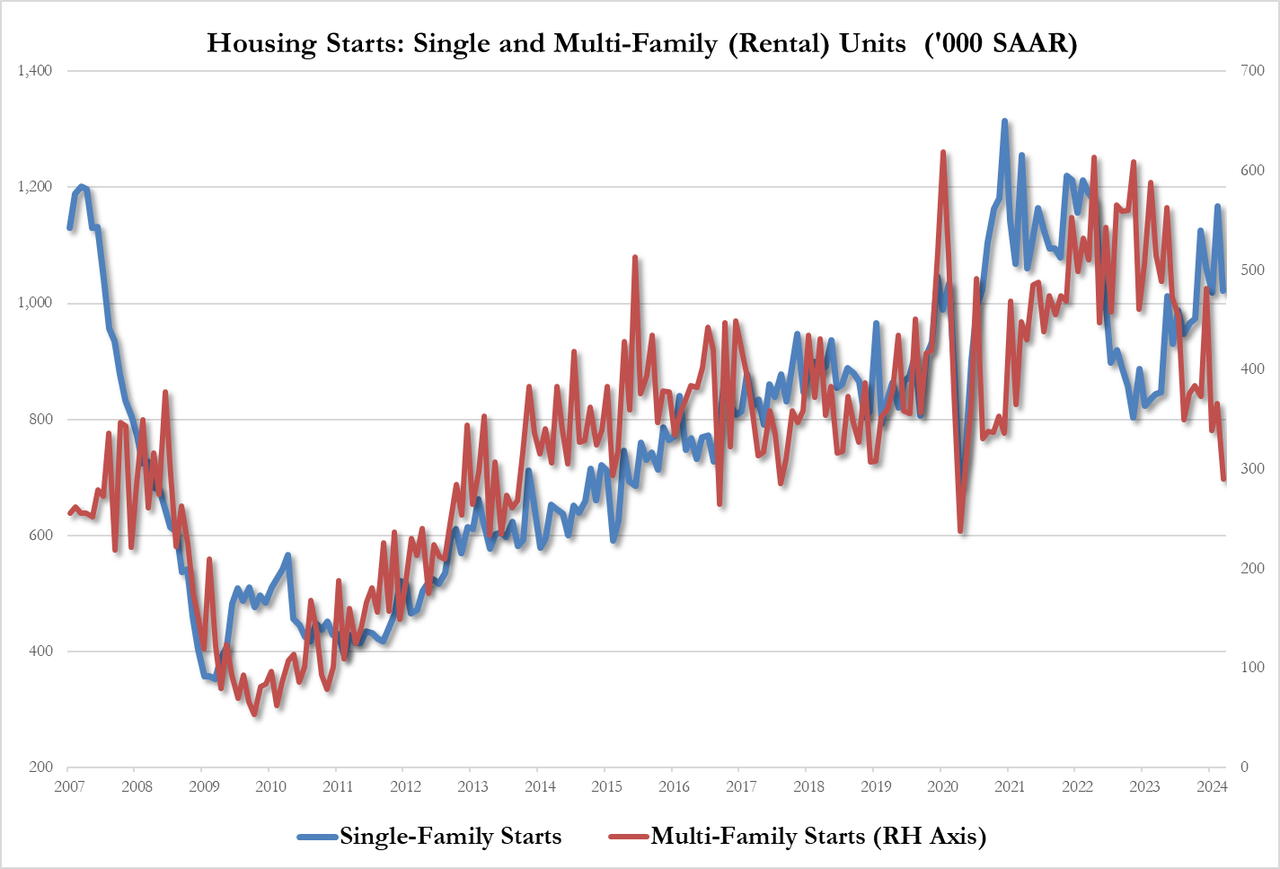

That pushed total multi-family starts SAAR down to its lowest since COVID lockdowns…

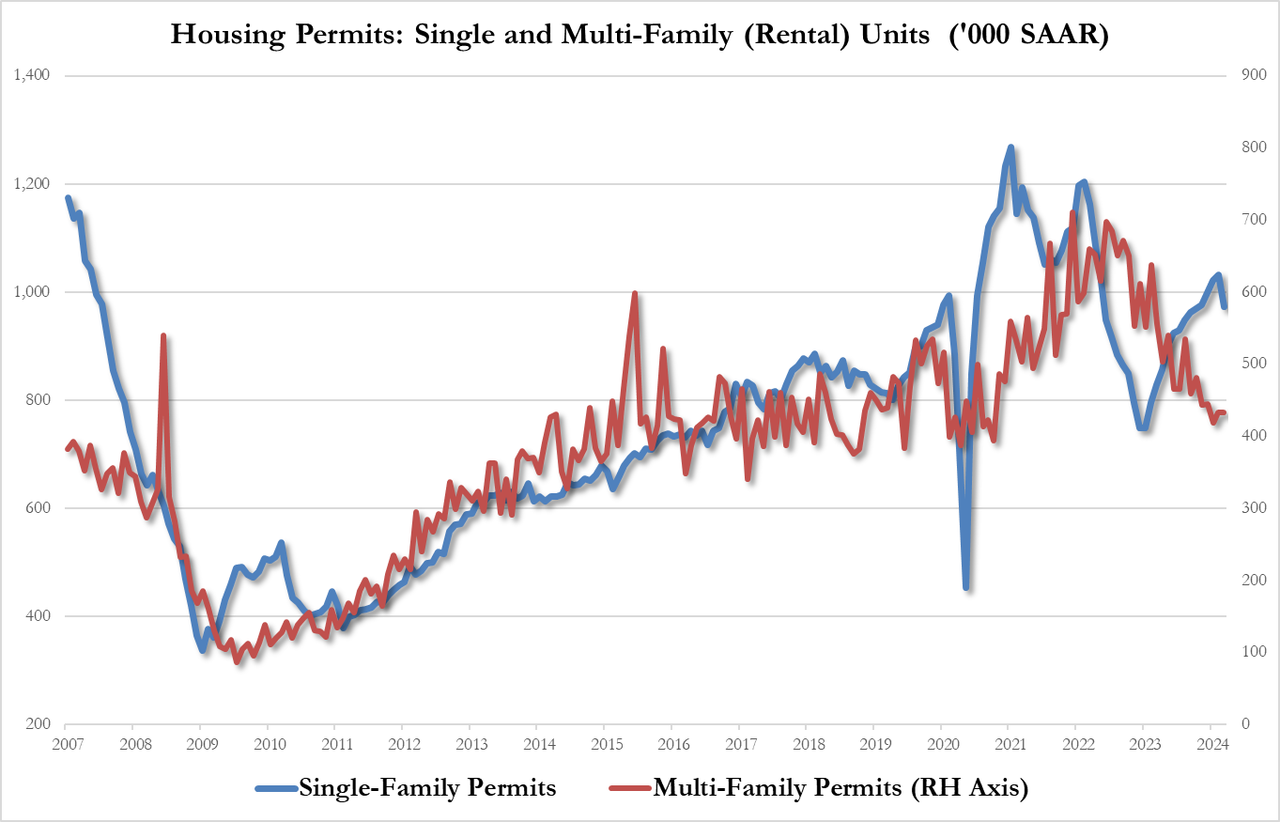

The plunge in permits was less dramatic and driven completely by single-family permits down 5.7% to 973K SAAR, from 1.032MM, this is the lowest since October. Multi-family permits flat at 433K

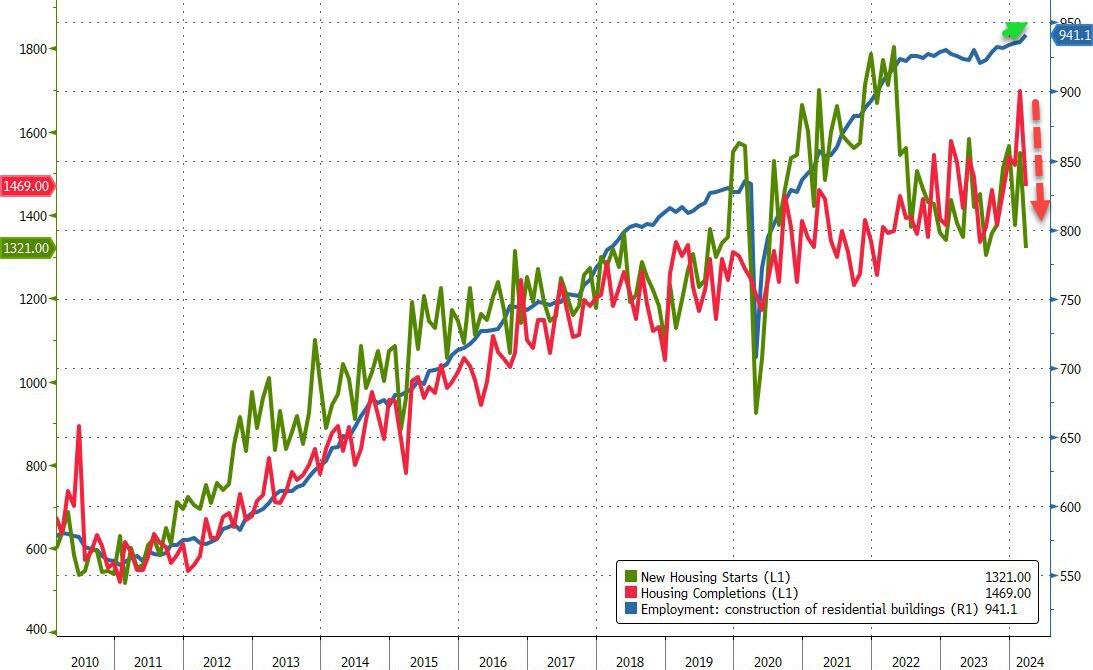

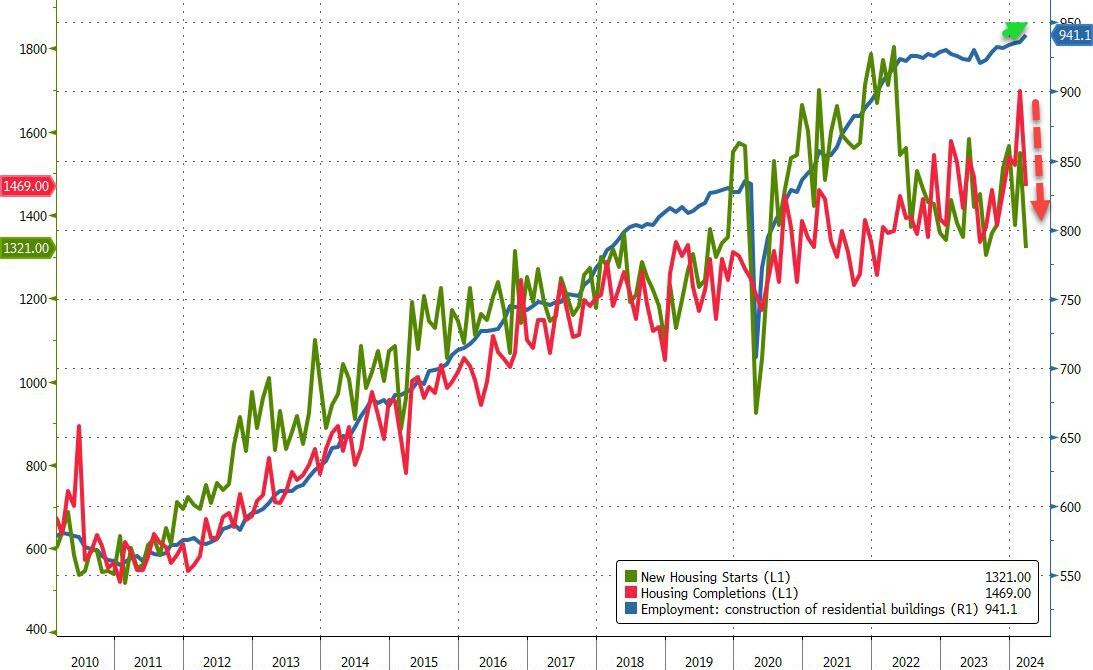

Intriguingly, while starts and completions plunged in March, the BLS believes that construction jobs surged to a new record high…

Source: Bloomberg

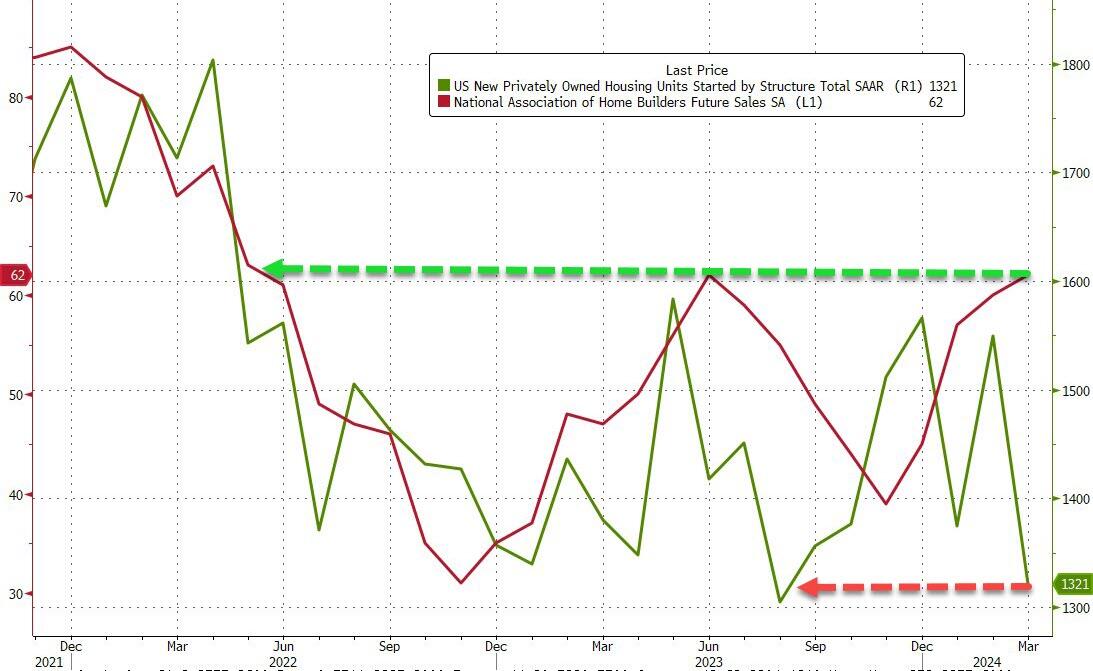

Finally, just what will homebuilders do now that expectations for 2024 rate-cuts have collapsed?

Source: Bloomberg

One thing is for sure – do not trust what homebuilders ‘say’ (as NAHB confidence jumped to its highest since May 2022 at the same time as housing starts crashed)…

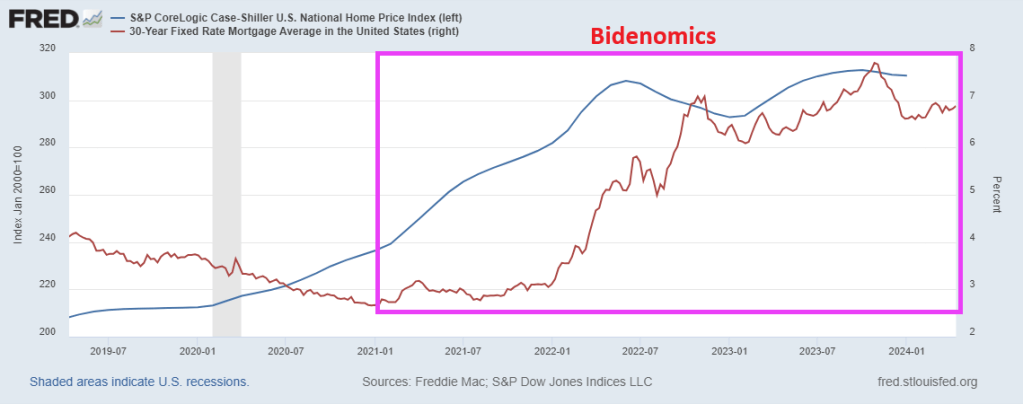

One reason that America’s youth is disgusted with Bidenomics is skyrocketing prices, particulalry housing. (simply unaffordable). Thanks to awful economic policies, home prices are up 32.5% under Biden and 30-year mortgage rates are up a whopping 160%! Good luck buying a home with a part-time job.

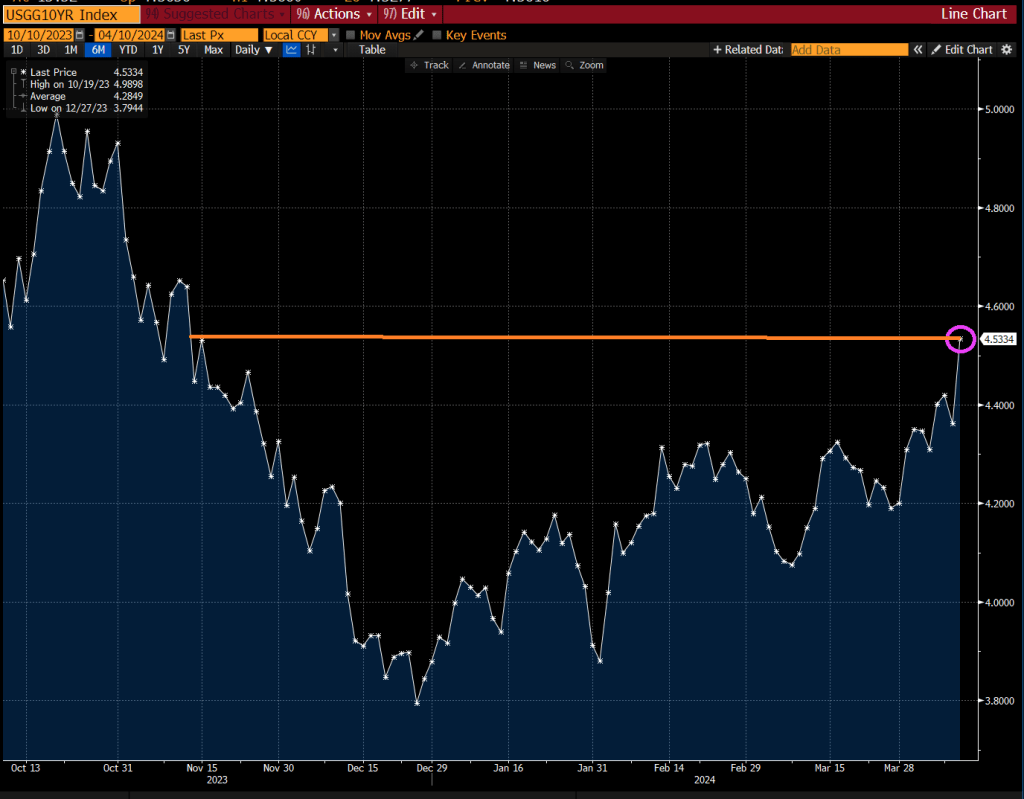

The bad news is that the 10-year Treasury yield rose to 4.53%, the highest since November 2023. This means that mortgage rates will rise even further.

Yes, rising rates AND home prices are daunting to part-time job holders.

Funky cold Joe Biden is his reaction to inflation caused by his outragous spending. His legion of sycophants are now saying inflation is a good thing or don’t notice it. But Biden will never stop spending .

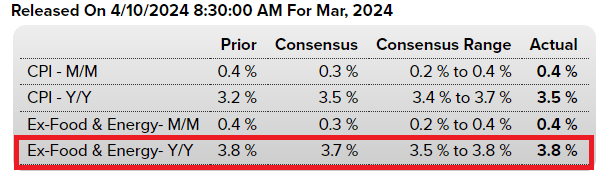

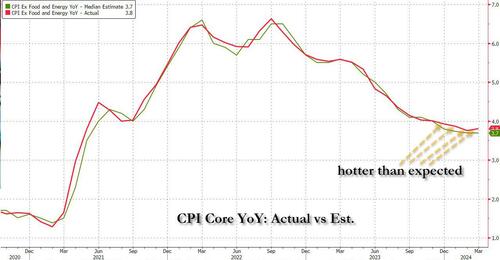

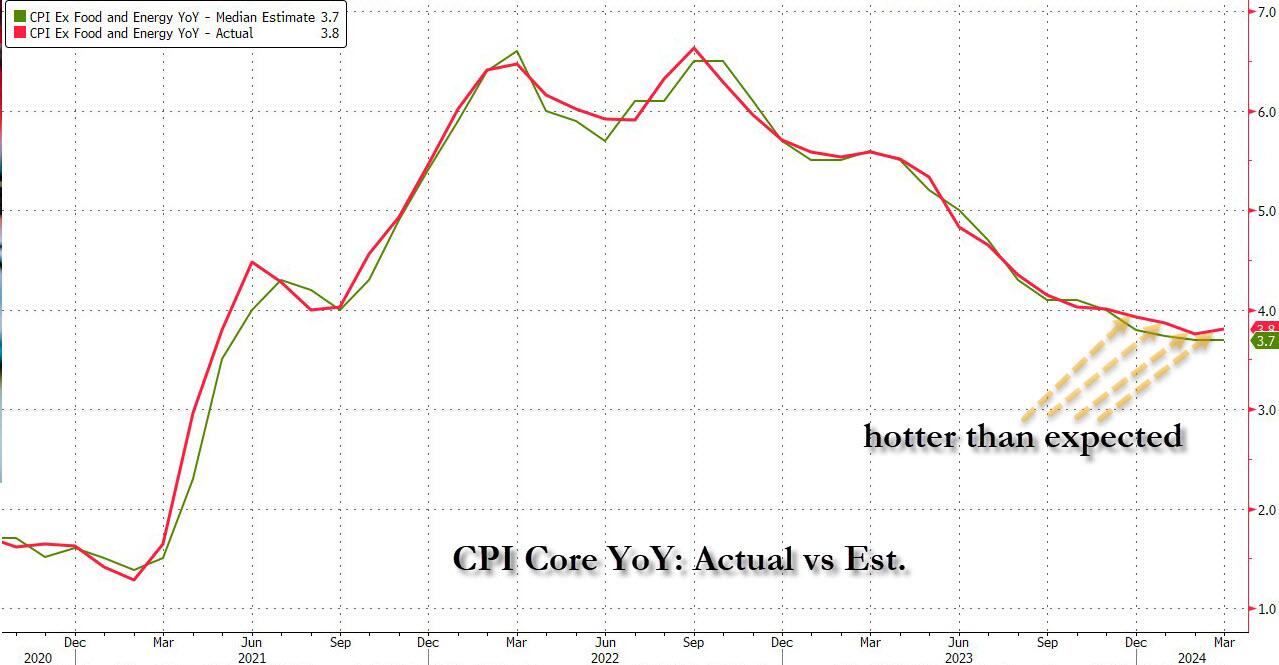

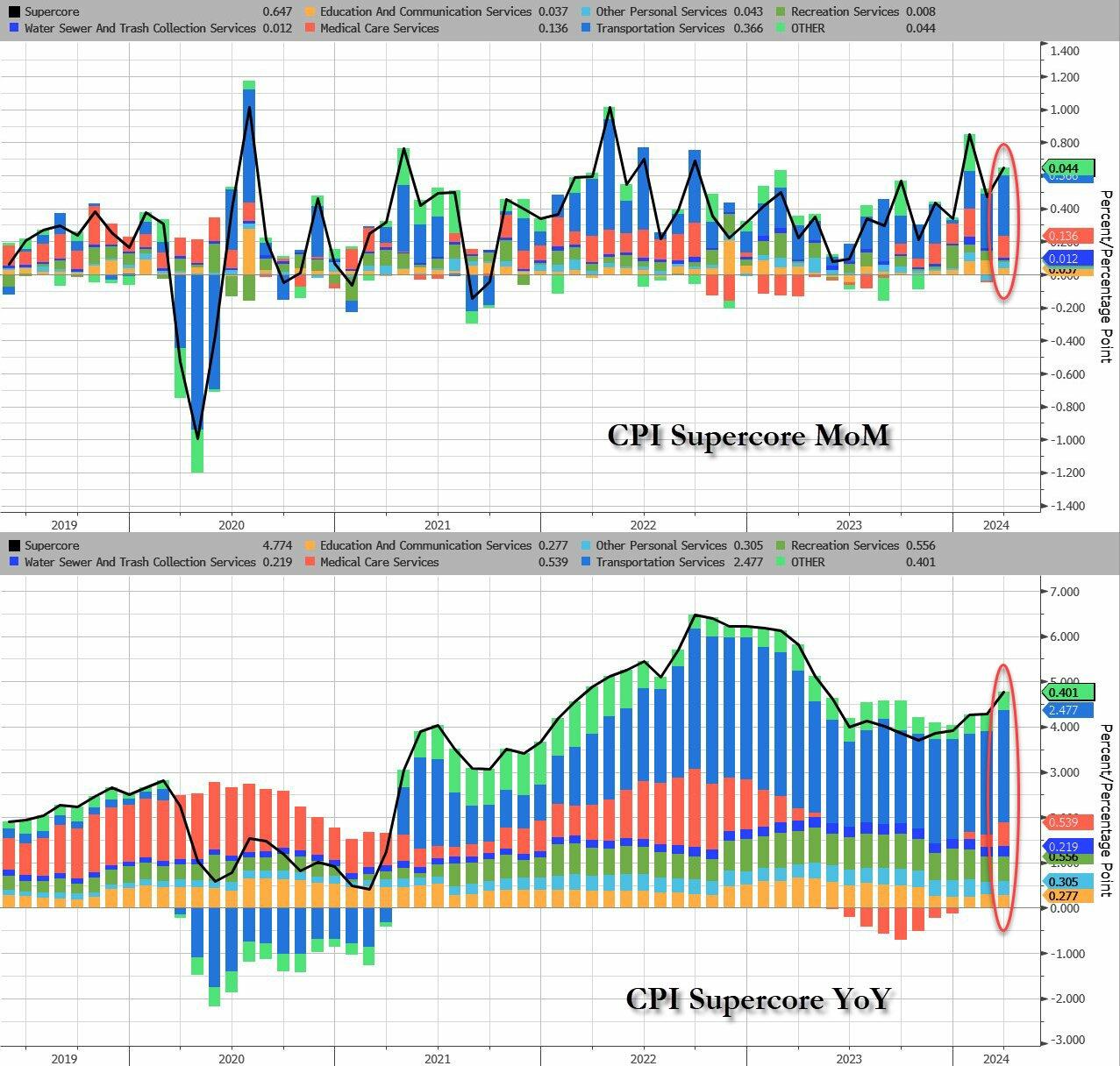

Coming into today’s CPI number, which followed three previous red-hot inflation prints, we said that it’s time for a “miss” (the first of 2024) not because the data demands it – on the contrary, prices continue to rise at a frightening pace – but because a dovish CPI print today would be the last opportunity for the Fed to set a timetable for a rate cut calendar ahead of November’s election.

Well, you can wave goodbye to all that, because we just got the 4th consecutive “inflation beat” in a row…

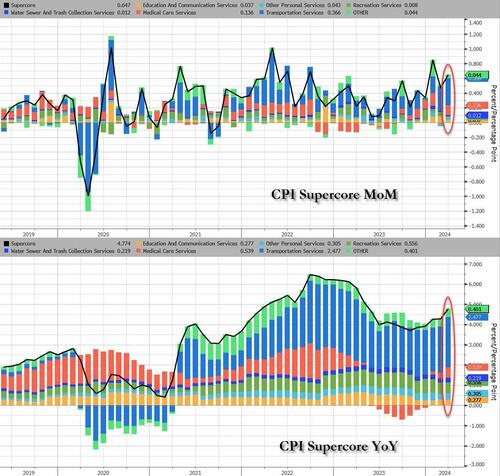

… with supercore inflation coming in blazing hot…

… thanks to a boiling inflation print which saw every single CPI metric coming in hotter than expected – was a shock, not because it reflected reality, but because it effectively sealed Biden’s fate because as Bloomberg’s Chris Antsey writes, “obviously, this is very bad news for Joe Biden… we’re approaching the point where high inflation is bound to still be in voters’ minds when they head to the polls, regardless of how the price figures come in over summer.”Easy financial conditions continue to provide a significant tailwind to growth and inflation. As a result, the Fed is not done fighting inflation and rates will stay higher for longer.”

It’s about to get even worse: recall today we have a $39 billion 10-year auction which is already being dubbed “sloppy” and a definitive break of 4.5% could easily extend if underwriting dealers are left holding the bag. As it stands, the 10yr has popped above the 4.5% parapet. Ian Lyngen at BMO Capital Markets says:“We expect the setup to the auction will break 4.50% in 10-year yields with ease.”

Obviously, this is very bad news for Joe Biden. It’s still only April, and we’ll have another half-a-year’s worth of inflation reports before the election. But we’re approaching the point where high inflation is bound to still be in voters’ minds when they head to the polls, regardless of how the price figures come in over summer.

Joe Biden continues to act like a gangsta giving away student loan forgiveness despite being told no by the US Supreme Court. As I said, Funky Cold Joe Biden. But Biden’s gangstaism favors the top 0.5% of net worth people, not the masses.

As Biden gropes for more voters, claiming he was raised in Puerto Rican, Greek, Black, and every other race on the planet, he probably sings “Ride The White Horse” to The Presidency. Reminiscint of Hillary Clinton claiming she kept a packet of hot sauce in her purse when talking to a black commentator.

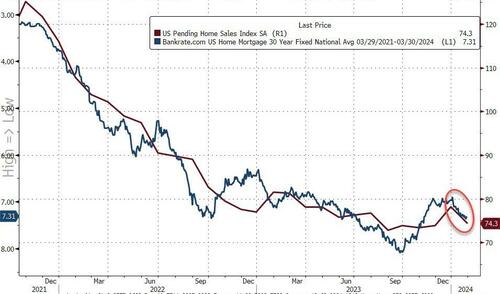

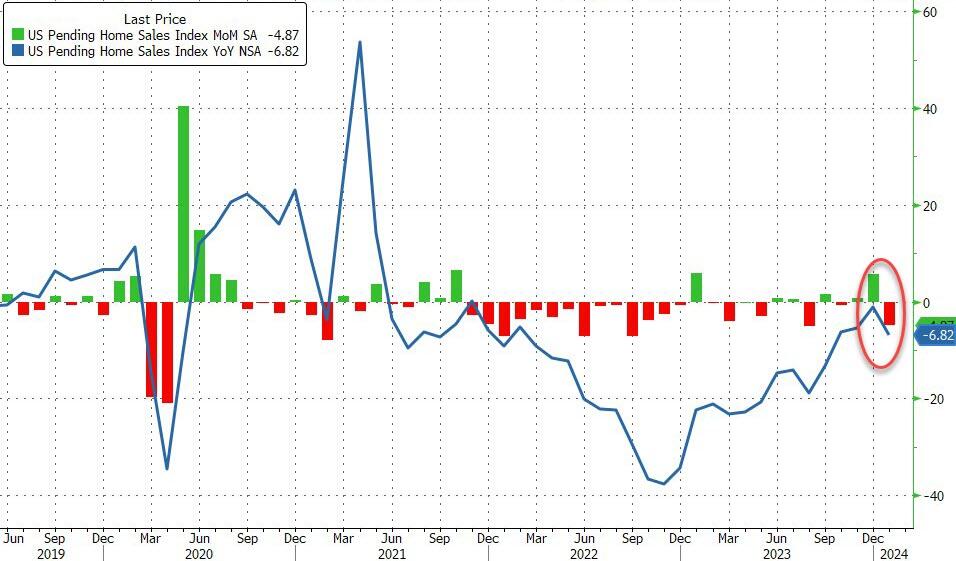

Pending home sales puked in January, tumbling 4.9% MoM (vs +1.5% MoM exp). This was made worse by a large downward revision for December (from +8.3% MoM to +5.7% MoM)…

Source: Bloomberg

That was the biggest MoM decline since August and dragged the YoY sales decline to -6.82%, tumbling back near record lows…

Source: Bloomberg

Realtors gonna realtor…

“This combination of economic conditions is favorable for home buying,” Lawrence Yun, NAR’s chief economist, said in a statement.

“However, consumers are showing extra sensitivity to changes in mortgage rates in the current cycle, and that’s impacting home sales.”

WTF are you talking about Larry?

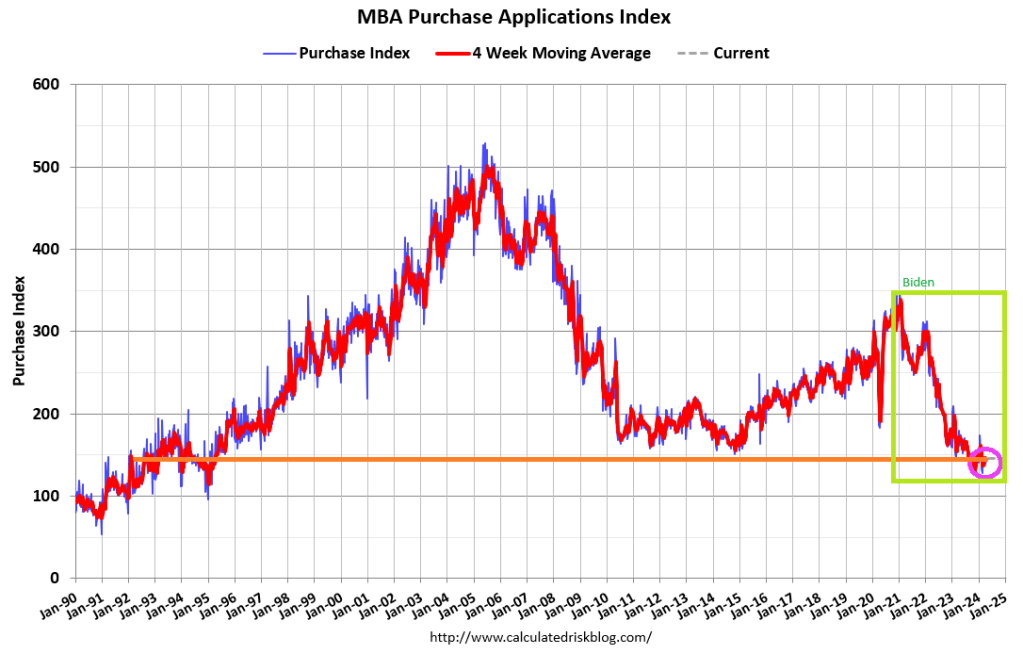

Earlier this week, a gauge of US mortgage applications for home purchases fell for a fifth week, nearing its lowest level since 1995.

Who could have seen that coming? As rates surged once again…

Source: Bloomberg

The pending-home sales report is a leading indicator of existing-home sales given houses typically go under contract a month or two before they’re sold.

The index of contract signings decreased 7.3% in the South, the nation’s biggest housing market.

Pending sales also fell 7.6% in the Midwest, but climbed 0.8% in the Northeast and 0.5% in the West.

“Southern states and those in the Rocky Mountain time zone experienced faster job growth compared to the rest of the country,” Yun said.

“As a result, long-term housing demand is increasing more significantly in these regions. However, the timing and number of purchases will largely depend on the prevailing mortgage rates and inventory availability.”

Overall sales are expected to increase 13% this year, according to NAR’s economic outlook, but as the chart above shows, unless rates start tumbling soon, that ain’t gonna happen.

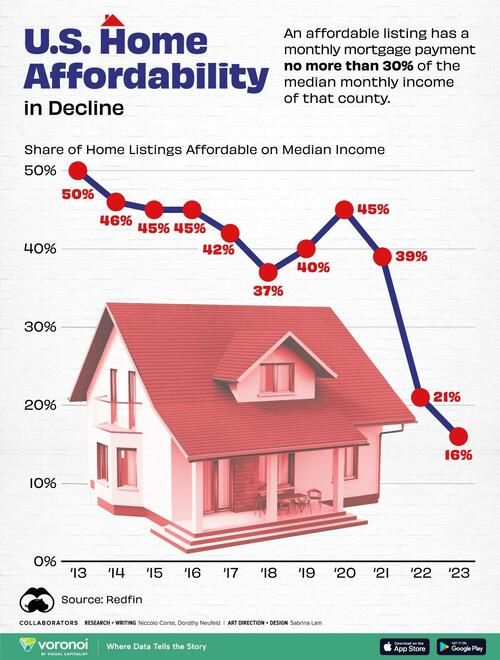

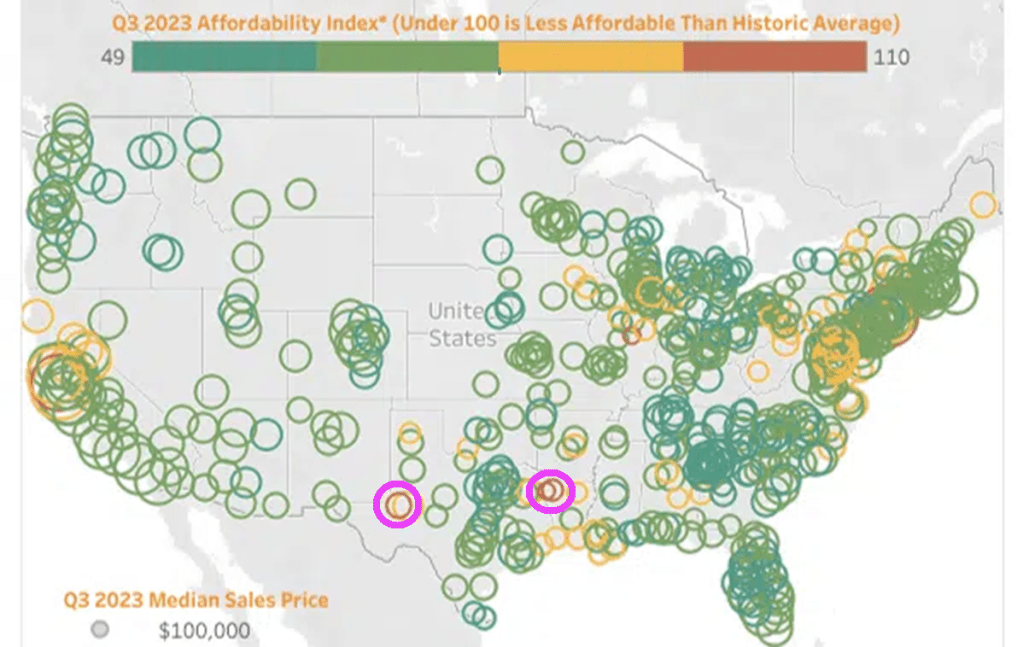

Although the Attom data is from Q3 2023, not much has changed. Under Biden (and his HUD Secretary Marcia Fudge, Fed Chair Jay Powell, and Treasury Secretary Janet Yellen), I did manage to find TWO AFFORDABLE areas to live: Shreveport Louisiana and Midland/Odessa Texas. The housing market remains unaffordable for millions of Americans.

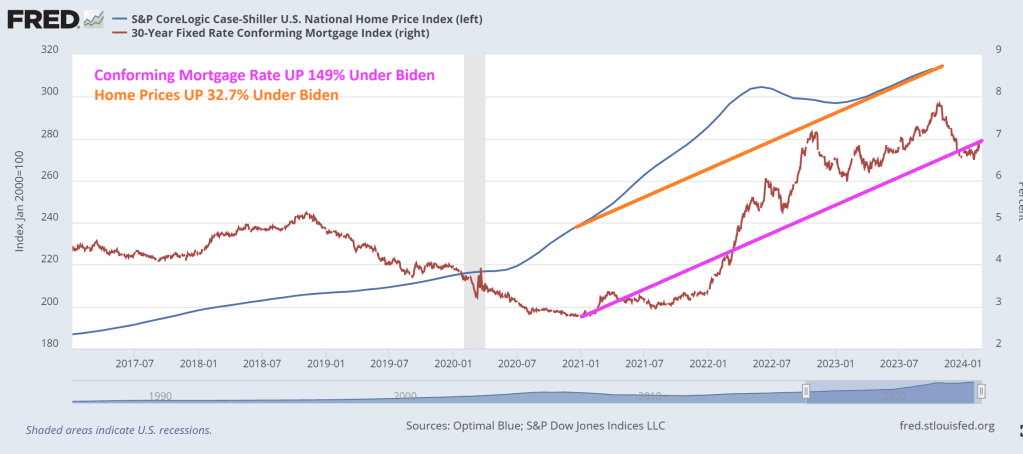

I am not surprised given that the Case-Shiller National home price index has risen by 32.7% under Biden while mortgage rates are up … 149%.

Robin Hood is a legendary heroic outlaw originally depicted in English folklore and subsequently featured in literature, theatre, and cinema. Traditionally depicted dressed in Lincoln green, he is said to have stolen from the rich to give to the poor. Politicians have created the new “Forgotten Man” by Amity Shlaes.

However, politicians like Joe Biden, Chuck Schumer, Mitch McConnell are “reverse Robin Hoods” dressed in business suits (although Jamie Raskin D-MD is often seen wearing a bandana and John Fetterman D-PA is often seen in a hoodie and shorts). They instead enact policies that steal from the middle class and give to themselves and the donor class. How do you think that politicians like the Bidens, Obama, Clintons and AOC go in broke and emerge as multi-millionaires?

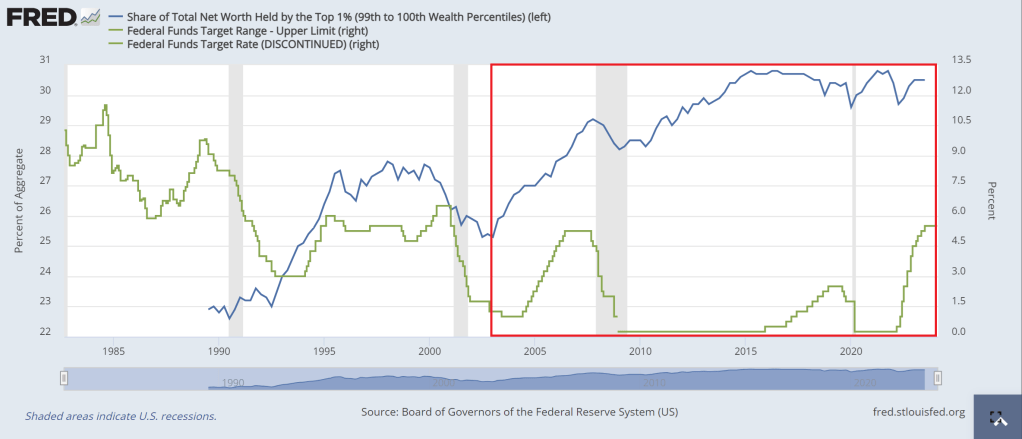

Part of the problem with the reverse Robin Hood model is the Federal Reserve itself. They helped punish the 99% with inflation due to excessive money printing. The share of total net worth held by the top 1% has exploded since The Fed’s rate cuts following the 2001 recession. The Fed has never lowered rates since to levels we saw prior to the 2001 recession, although The Fed is getting close.

Then we have the green energy hysteria (which like pornography excites the brain and distorts logical thinking). Wealthy donors have received a massive windfall (along with China) from Biden/Congress’s green energy spending (scam). The middle class and low-wage workers are now playing higher utility bills (sacrificial lambs on the altar of global warming … or cooling) along with seeing gasoline and diesel prices far higher than before Biden was elected. Gasoline prices are up 46.25% under Biden and diesel prices are up 55.6%.

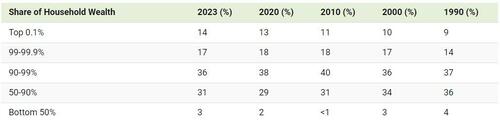

I like this chart of the distribution of household wealth by income group. The top 1% (the elite Pelosi class, are getting wealthier and wealthier. The 90-99% group are doing well, but not as well as the top 1%. The bottom 50% (who the Washington DC elite class seems to have forgotten about)

Here is a table of the same data.

Then we have the exploding mortgage rates under Biden. Rates are up over 155% under Old Grandad Joe Biden. Another shot through the heart of the middle class. And Washington DC is to blame.

Speaking of Washington DC millionaire elites, I want to share this picture with you. Hillary Clinton is NOT Robin Hood but an example of a REVERSE Robin Hood.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.