Fannie Mae’s Home Purchase Sentiment index has declined from 81.7 shortly after Biden was sworn-in as President to a meager 62.8 in July 2022.

Of course, mortgage rates have risen quite rapidly and home price growth remains elevated as The Fed still has not trimmed its balance sheet as promised.

While President Biden is technically correct (CPI didn’t increase from June to July), he left out that headline inflation was still painful at 8.5% YoY and core inflation was 5.9% YoY. He also left out that CORE inflation rose 0.3% in July. And he left out that REAL earnings growth was still negative.

The midterm elections are approaching fast and, of course, Biden and his crew have to put the best face of his and the Democrats accomplishments. But seriously Joe, REAL weekly earnings growth is negative meaning that inflation is crushing wage growth. Meanwhile, CPI rent is skyrocketing and was 5.8% YoY in July.

As we know, the CPI measure of rent is terrible and does not reflect the actual rise in rents. Zillow’s Rent index YoY is slowing, but remains at 14.75% YoY, far higher than the CPI rent measure of 5.8%.

So, the Federal Government and Federal Reserve keeps pumping trillions into the economy, so it is not surprising that we have rampant inflation crushing renters.

The US July inflation report remains hot, hot, hot! While mortgage purchase and refinancing applications are not, not, not.

The US consumer price index rose 8.5% in July. And real average weekly growth remains burned by horrid inflation, at -3.6% YoY.

Source of inflation?

Headline inflation above estimates in 14 of last 16 months.

Data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending August 5, 2022 revealed that … the Refinance Index increased 4 percent from the previous week and was 82 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 19 percent lower than the same week one year ago.

The US Treasury 10Y-2Y yield curve descended further into inversion, signaling impending recession.

The US unemployment rate (U-3) tends to be the lowest when the 10Y-2Y yield curve inverts, then explodes when recession strikes.

The spread between the Bankrate 30-year mortgage rate and the Bankrate 5/1 ARM rate widened to 139 basis points.

This is happening as The Fed is expected to keep raising their target rate (yellow line) and the US Senate passed its massive “inflation reduction” boondoggle that is expected to NOT reduce inflation, but raise taxes on the middle class and low-wage workers.

The US housing market is simply unaffordable for millions of Americans. To illustrate the problem, here is a chart of the Case-Shiller National home price index less CPI YoY graphed against Average Hourly Wages less CPI YoY.

The gap between the REAL national home price index YoY and REAL US average hourly earnings YoY is near the largest since 1988. Inflation is making matters far worse since REAL average hourly earnings growth continues to decline.

The only thing positive to say is that REAL home price growth YoY is lower now than at the peak of the 2005 home price bubble that burst catastrophically.

Another “positive” is that the REAL 30-year mortgage rate has fallen to -3.23%. At the peak of the house price bubble in June 2005, the REAL 30-year mortgage rate was +2.58%. THAT is one big difference between the pre-2008 recession and today’s impending recession.

Here is your weekend update on Treasury and Mortgage markets.

The current US Treasury 10Y-2Y yield curve just slipped further into reversion at -40.299 basis points, screaming impending recession. Oddly, The Federal Reserve has been leaving its balance sheet of Agency Mortgage-backed Securities (MBS) in tact (green line).

On the mortgage front, Bankrate’s 30-year mortgage rate index rose to 5.60% while the affordability-friendly 5/1 Adjustable Rate Mortgage (ARM) rate rose to 4.21%.

Currently, a 5/1 ARM borrower can save 139 basis points over the traditional 30-year mortgage rate.

Today’s jobs report was … strange. While the US economy added more jobs than expected, we also saw labor force participation contract and real wage growth decline again.

The reaction in the bond market? US Treasury 10-year yields exploded by +14 basis points. As I used to tell my fixed-income students, any basis point jump or decline of 10 basis points or more is a BIG DEAL.

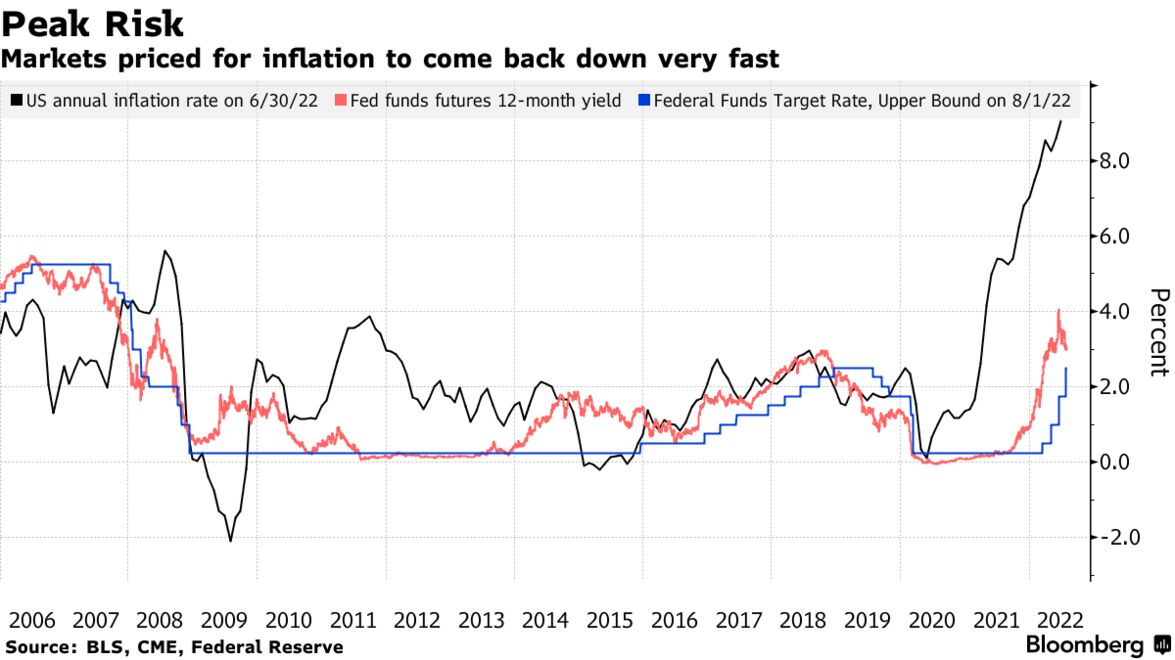

The implied target rate for The Fed (based on Fed Funds Futures) is now lower for the Jan 1, 2024 FOMC meeting (3.025%) than it is for the Sept 21, 2022 FOMC meeting (3.034%).

Mortgage rates? They will go up as The Fed removes its Brawndo, the economy mutilator.

The media is thrilled with today’s jobs report showing a sizzling 528k jobs added to the US economy. And with that, the media is cheering that recession fears are shrinking.

But hold on a second.

First, while 528k jobs were added in July (great news!), REAL average hourly earnings growth YoY fell to -3.8173. Why? Because the rate of inflation is greater than nominal average hourly earnings YoY of 5.2%. That is BAD.

This charts shows that inflation-adjusted (or real) wage growth is the worst in recorded history.

And the “sizzling” jobs report isn’t feeling any love in the bond market where the US Treasury yield curve (10Y-2Y) deepened its inversion to -37.593 basis points, a drop of -1.331 BPS. Note that the 10Y-2Y curve falls below 0% just prior to every recession.

Labor force participation actually fell to 62.1% from 62.2% in June.

I am assuming that The Fed will misread the jobs report and argue for LESS COWBELL.

The US economy may need to undergo a deeper and longer recession than investors currently anticipate before inflation can be brought under control, according to Zoltan Pozsar of Credit Suisse Group AG.

Markets expect the surge in consumer prices will soon peak and central banks will become less hawkish, but there’s a high risk that global cost pressures will remain elevated, Pozsar, global head of short-term interest-rate strategy at Credit Suisse in New York, wrote in a client note.

The world is being wracked by an economic war that’s undermining the deflationary relationships that have prevailed in recent decades where Russia and China supplied cheap goods and services to more developed nations such as the US and those in Europe, he said.

“War is inflationary,” Pozsar wrote. “Think of the economic war as a fight between the consumer-driven West, where the level of demand has been maximized, and the production-driven East, where the level of supply has been maximized to serve the needs of the West.” That pattern held “until East-West relations soured, and supply snapped back,” he said.

The result is that inflation is now a structural problem, rather than a cyclical one. Supply disruptions have arisen from the changes in Russia and China, along with tighter labor markets due to immigration restrictions and a reduction in mobility caused by the coronavirus pandemic, Pozsar said.

There’s now a risk the Federal Reserve under Chair Jerome Powell has to raise interest rates to 5% or 6% and keep them there to create a substantial and sustained reduction of aggregate demand to match the tighter supply profile, he said.

‘More Misguided’

Connect the dots on the biggest economic issues.Connect the dots on the biggest economic issues.Connect the dots on the biggest economic issues.

Dive into the risks driving markets, spending and saving with The Everything Risk by Ed Harrison.Dive into the risks driving markets, spending and saving with The Everything Risk by Ed Harrison.Dive into the risks driving markets, spending and saving with The Everything Risk by Ed Harrison.

Sign up to this newsletter

Pozsar’s warning that inflation will stay elevated puts him at odds with the Treasury market, which rallied last month as investors switched their focus to recession risks from inflation concern. While an economic slowdown typically weighs on consumer prices, the latest annual US inflation reading of 9.1% for June remains far above the Fed’s 2% goal, although the price surge is forecast to slow for the first time in three months to 8.8% in July according to a Bloomberg poll of economists.

The bond market is more misguided now than at any other time this year as traders wager the US central bank will start cutting rates in early 2023, Bloomberg Economics’ chief US economist Anna Wong and her colleagues said this week. Money markets are wagering on almost one percentage point of hikes by year-end followed by a quarter-point cut by June.

“Interest rates may be kept high for a while to ensure that rate cuts won’t cause an economic rebound (an ‘L’ and not a ‘V’), which might trigger a renewed bout of inflation,” Pozsar wrote in his note. “The risks are such that Powell will try his very best to curb inflation, even at the cost of a ‘depression’ and not getting reappointed.”

Speaking of “recession,” the US Treasury 10Y-2Y yield curve has inverted even further to -31.69 BPS.

You must be logged in to post a comment.