(Bloomberg) — To understand the highest mortgage rates in two decades, look to the intricacies of the market for bonds backed by home loans.

So says Guillermo Roditi Dominguez, managing director at New River Investments LLC. On the latest episode of the Odd Lots podcast, he describes how the surging cost of home loans can be traced to changes in the market for mortgage-backed securities, or MBS. The average rate on a 30-year fixed mortgage jumped above 7%, according to data released on Wednesday. That’s the highest since 2001.

Of course, mortgage rates are supposed to rise as the Federal Reserve hikes benchmark interest rates. That’s how tighter monetary policy works — by making the cost of credit more expensive. But the average borrowing cost on a 30-year fixed-rate mortgage now far exceeds the yield on equivalent US Treasuries, with the difference between the two at the highest level on record.

At issue is the changing nature of the market for mortgage bonds, and who’s buying them. Once the center of the housing bubble that burst in 2008, the vast majority of mortgage-backed securities come with guarantees from the US housing agencies, meaning investors aren’t necessarily worried about people paying back their loans. Yet their exposure to movements in US interest rates (known as “duration”) means they can still carry significant risks for investors.

“It’s not because people are afraid house prices are going to go down,” Dominguez says. “Mortgage-backed securities went from being effectively short-lived assets because we went through a pretty epic refinancing boom in 2020 and 2021, to all of a sudden rates going up very, very, very quickly — faster than anybody expected.”

Most buyers of MBS — which range from big banks to bond funds and the Fed itself — understand there’s a risk of early repayment. People might refinance their home loans during periods of low interest rates, or simply move and sell their house. Dominguez estimates that some 17% of home-loan balances were extinguished in 2019, compared to 36% in 2020 and 2021 as the Fed pushed interest rates to historic lows.

Mortgage refi activity exploded in early 2020, when rates were cut to basically zero.

In times of low rates, MBS investors who get their loan principal paid back early have to reinvest that money at potentially lower yields. But the transition from low rates to higher ones means that suddenly investors are left with longer-term assets, as borrowers hold onto the lower mortgage rates they locked-in previously. In times of higher interest rates, early repayments disappear and investors don’t have as much money to invest at higher yields. That means many buyers are shying away from the mortgage market, which Dominguez describes as “broken,” even as spreads go higher. Adding to the pressure on mortgage rates is the fact that the Federal Reserve is now reducing its balance sheet after buying the debt as part of its emergency monetary easing.

“A mortgage-backed security is essentially similar to a covered call in equity terms,” Dominguez says. “And that means that you have all of the downside and, you know, very, very little of the upside and you trade that in for a little bit of extra coupon. And when rates were going down, everybody was upset about it because Treasury bonds were going up in price. People were making money there. If you held MBS, you got your money back and then when you went to buy new bonds, you bought them at a lower yield. And right now what we’re seeing is all of a sudden bond prices are going down, yields are going up and you’re not getting any cash flows so you don’t get to reinvest that money.”

But mortgage purchase and refi applications are showing a strongly negative trend as The Fed tightens.

US Q3 GDP numbers are out and they are … meh. Only Biden and Karine Jean-Pierre would cheer about 1.8% real GDP growth. At least real GDP growth wasn’t negative!

Real GDP rose 2.6% after -0.6% in Q2 and 1.8% YoY. But the most interesting data bit is the GDP Price Index. It fell to 4.1% in Q3 down from a whopping 9.0% in Q2.

But wait! Also declining at a stall speed is M2 Money.

And brace yourself for a cold winter. Heating oil is UP 162% under Biden.

As the midterm elections get close, the news for Americans gets worse.

On the housing/mortgage front, Bankrate’s 30-year mortgage rate (yellow line) just hit 7.20%, the highest since 2000. Also, the US Treasury 10yr-3mo yield curve (white line) inverted, historically a precursor to recession, before barely climbing back above 0%.

Meanwhile, M2 Money growth has collapsed to the lowest level since 2010.

US GDP numbers are due out at 8:30AM EST for Q3. The numbers are expected to show slow growth (around 2.4%) with rapid inflation (5.3%). While the GDP numbers are better than Q2’s numbers, they are still pretty lousy.

One reason is diesel fuel prices are up 102% under Biden’s Reign of Error. While inventory of diesel fuel down -37%. Meanwhile core inflation is up from a measly 1.3% to a whopping 6.6% at the latest inflation report.

Introducing Biden’s Thanksgiving dinner … in a can to cope with rising prices.

Just kidding. This is too clever for the clueless Biden Administration. But Karine Jean-Pierre might get as confused as Joe Biden and repeat it as one of the ways that The Biden Administration is helping consumers.

As I told my Chicago, Ohio State and George Mason University finance and real estate students, repeatedly, “Watch out when The Fed begins to tighten monetary policy. It will be a bloodbath for taxpayers.”

Well, here we are. I argue that Biden’ green energy knucklehead policies are driving inflation, or it could be the insane level of Federal spending that Obama economist Larry Summers warned us about, or rising wages (in part due to Federal spending) is to thank for inflation. Or all of the above.

Regardless of the cause, the bond market is enduring its worst selloff in a generation, triggered by high inflation and the aggressive interest-rate hikes that central banks are implementing. Falling bond prices, in turn, mean paper losses on the massive holdings that the Fed and others accumulated during their rescue efforts in recent years.

Rate hikes also involve central banks paying out more interest on the reserves that commercial banks park with them. That’s tipped the Fed into operating losses, creating a hole that may ultimately require the Treasury Department to fill via debt sales. The UK Treasury is already preparing to make up a loss at the Bank of England.

The Reserve balance has crashed into negative territory.

And Fed losses are skyrocketing.

Agency MBS prices are up today, but are down since August 2022. But risk measures duration and convexity are zooming upwards.

Alarm! US home prices are decelerating as inflation rages and The Fed tightens.

Home price growth in the US slowed the most on record as a doubling of borrowing costs (thanks to the US Federal Reserve) has sapped demand.

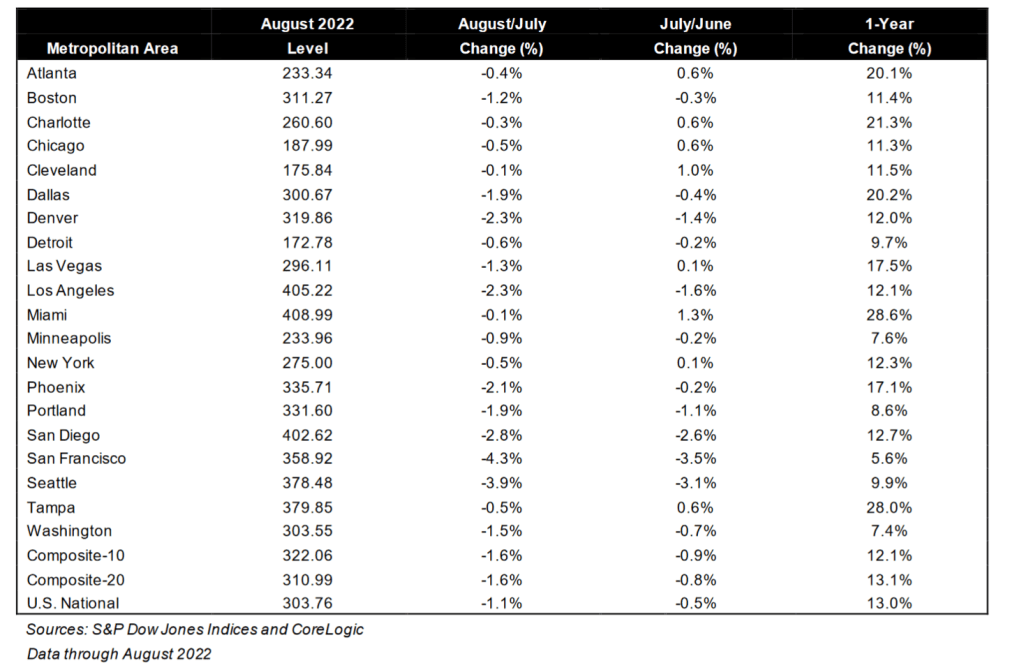

A national measure of prices increased 13% in August from a year earlier, but is down from 20.79% in March, the S&P CoreLogic Case-Shiller index showed Tuesday. That’s the biggest deceleration in the index’s history.

The housing market has started to slump as the Federal Reserve hikes interest rates to curb the hottest inflation in decades. Even with the deceleration, prices remain high compared to last year. Coupled with mortgage rates that are edging closer to 7%, many would-be buyers have been shut out, while some sellers have retreated.

While 13% growth sounds good, it is not good for renters looking to buy a home.

According to S&P/CoreLogic/Case-Shiller, Southern (red) cities Atlanta, Charlotte, Dallas, Miami and Tampa all still grew at over 20% YoY. Other cities like blue cities Detroit, Minneapolis, Portland, San Francisco, Seattle and Washington DC are grew at UNDER 10% YoY.

On related news, I always said in my classes that +/- 10 basis point in the US Treasury yield is a big deal. This morning, the US Treasury 10-year yield is DOWN -16.1 bps. In fact, the 10-year yields are down across the board globally.

The Federal Reserve’s DOTS PLOT shows where each Fed official’s projection for the central bank’s key short-term interest rate is headed. As of the September 21, 2022 Fed Open Market Committee (FOMC) meeting, the prediction of future Fed target rates is decidedly DOWNWARD SLOPING.

The Fed hawks, those that want to tighten monetary policy, are Bowman, Waller, Kashkari, Mester and George. The Fed doves (or those who are neutral) are Biden recent appointees Barr, Cook, Jefferson, Logan, Collins. Note that Brainard and Bostic are the only technical doves.

I call the hawks at The Fed “The Blackhawks” since their mission of fighting inflation may lead to a recession. And Bowman, Mester and George are Lady Blackhawks.

Things are getting interesting in DC, to say the least. The US is 100% likely to face a recession in the next 12 months while The Federal Reserve is on its crusade to fight inflation caused by … The Federal Reserve, Biden’s green energy shenanigans and massive, irresponsible Federal spending that even Former Obama economist Lawrence Summers warned would cause inflation. So what will The Fed do? Lower rates and expand their assets purchases to fight the impending recession OR keep tightening to fight Bidenflation? But where we are now is that the fixed-income market could be in big, big trouble.

For months, traders, academics, and other analysts have fretted that the $23.7 trillion Treasuries market might be the source of the next financial crisis. Then last week, U.S. Treasury Secretary Janet Yellen acknowledged concerns about a potential breakdown in the trading of government debt and expressed worry about “a loss of adequate liquidity in the market.” Now, strategists at BofA Securities have identified a list of reasons why U.S. government bonds are exposed to the risk of “large scale forced selling or an external surprise” at a time when the bond market is in need of a reliable group of big buyers.

“We believe the UST market is fragile and potentially one shock away from functioning challenges” arising from either “large scale forced selling or an external surprise,” said BofA strategists Mark Cabana, Ralph Axel and Adarsh Sinha. “A UST breakdown is not our base case, but it is a building tail risk.”

In a note released Thursday, they said “we are unsure where this forced selling might come from,” though they have some ideas. The analysts said they see risks that could arise from mutual-fund outflows, the unwinding of positions held by hedge funds, and the deleveraging of risk-parity strategies that were put in place to help investors diversify risk across assets.

In addition, the events which could surprise bond investors include acute year-end funding stresses; a Democratic sweep of the midterm elections, which is not currently a consensus expectation; and even a shift in the Bank of Japan’s yield curve control policy, according to the BofA strategists.

The BOJ’s yield curve control policy, aimed at keeping the 10-year yield on the country’s government bonds at around zero, is being pushed to a breaking point.

Well. Bidenflation certainly isn’t helping, but Statist Economist and Cheerleader Janet Yellen can’t bring herself to blame green energy policies, rampant Federal spending or irresponsible Federal Reserve policies for the crisis.

You will note the differences between today and the financial crisis of 2008-2009. The financial crisis gave us a massive surge in government securities liquidity thanks to then Fed Chair Ben Bernanke imitating Japan’s Central Bank and buying US government securities. Fast forward to today and the liquidity index hasn’t budged much since 2010 (except for a little blip around the Covid Fed intervention of early 2020), but we are now seeing near 40-year highs in inflation and a barely declining Fed balance sheet. And M2 Money YoY (mostly commercial bank deposits) are crashing.

I am guessing that The Fed will pivot given that stock futures are way up for Monday. The Dow Jones mini is up 770 points and the S&P 500 mini is up 88.75 points.

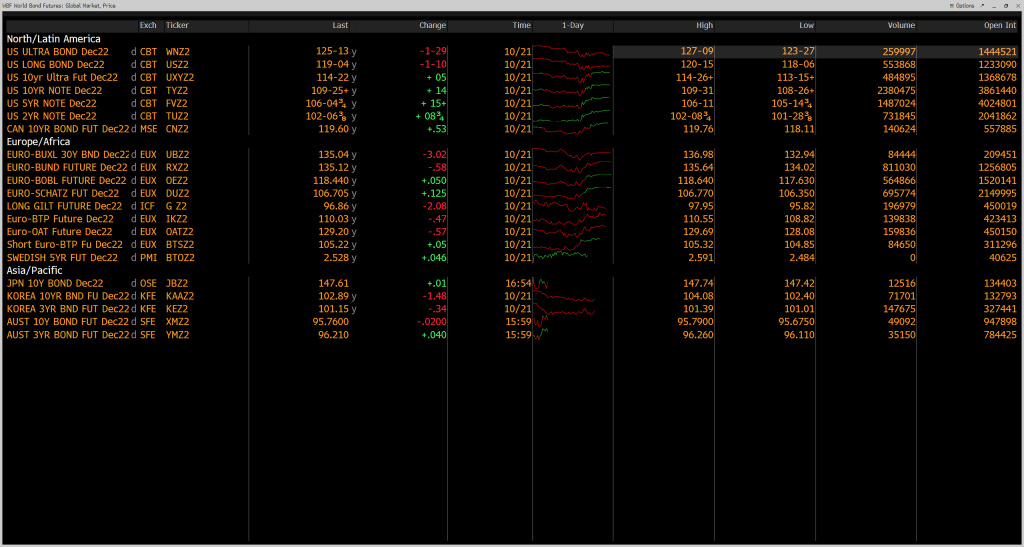

Bond market futures (specifically the US Ultra Bond) is down for Monday, meaning yields will be climbing.

I remember giving a speech at The Brookings Institute in Washington DC. Talk about stranger in a strange land. One person who I was debating got frustrated and said “You are such a … Republican!!!” As if that was the worst slur he could throw at me.

You must be logged in to post a comment.