While the Nestea plunge was meant to be refreshing, the housing starts plunge is not refreshing at all. Just another warning about the shortcomings of Bidenomics.

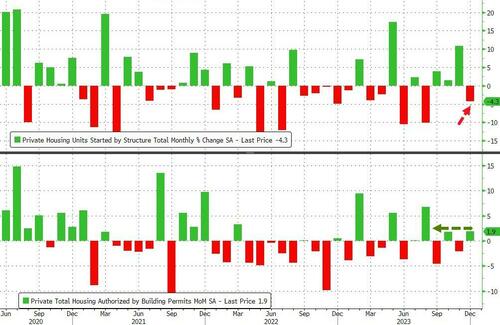

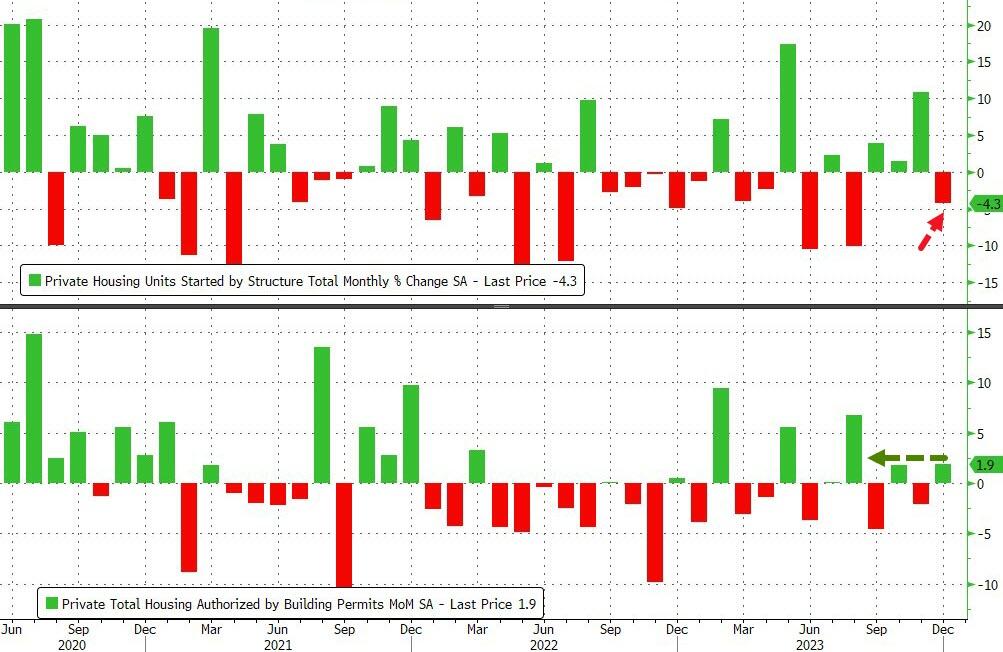

Analysts were right in direction but wrong in magnitude – too bearish. Housing starts declined 4.3% MoM (vs -8.7% MoM exp and +10.8% MoM in November, a big downward revision from the initial +14.8% MoM). Building permits also rose more than expected (+1.9% MoM vs +0.6% exp but saw November’s 2.5% MoM decline upwardly revised to -2.1% MoM…

Source: Bloomberg

On a SAAR basis, Housing Starts and Building Permits are higher YoY

Source: Bloomberg

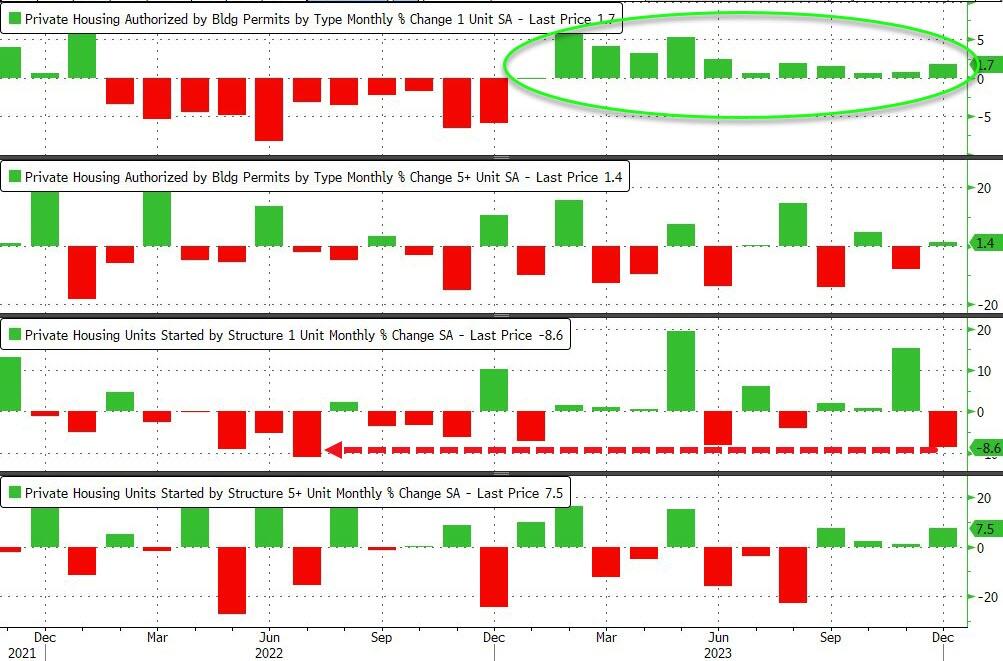

Under the hood, single-family permits rose for the 12th month in a row (i.e. every month in 2023) but single-family home starts plunged 8.6% MoM after surging 15.4% MoM in November… that is the biggest monthly decline since July 2022…

Source: Bloomberg

Perhaps the optimism among homebuilders about future sales is a little overdone given their actions?

Source: Bloomberg

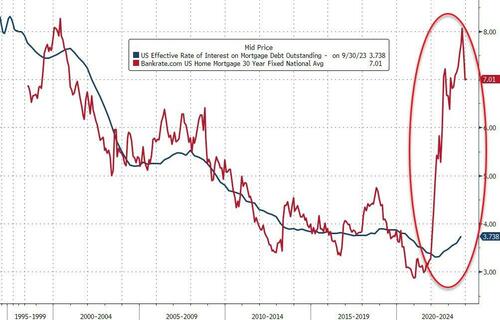

And why would starts be down so much if rates are tumbling?

Source: Bloomberg

Still along way to go for mortgages to be affordable…

Source: Bloomberg

Will less supply of new homes do anything to help the Shelter component of CPI (hint – no!).

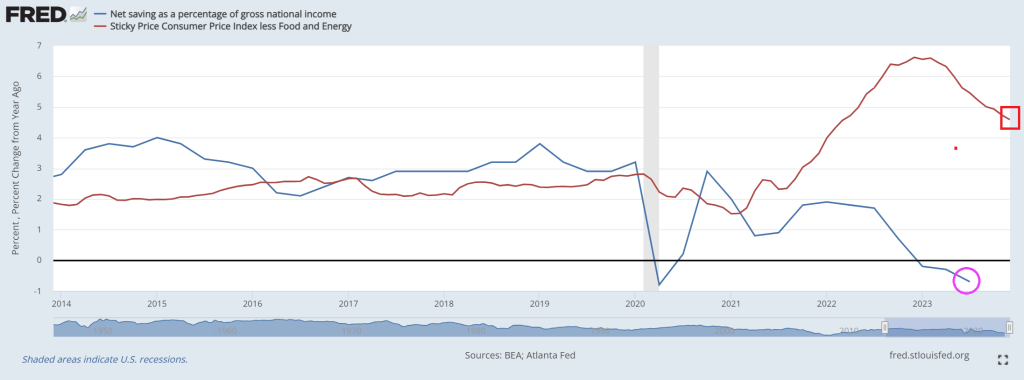

President Biden still shuffles around mumbling about Maga Republicans and defending democracy (while gettig his DOJ and affiliates to prosecute his leading Presidential opponent) even though …. consumers continue to struggle. While Biden is in wonderland, American consumers are in hell.

Savings as a percentage of GDP is actually NEGATIVE as sticky price inflation remains above 4%.

Any good news? At least the US Treasury yield curve (10Y-5Y) is normalizing.

How true!

Speaking of Biden, is this photo real? With AI, I wonder.

The yield on the 10-year Treasury note was recently up 4 basis points at 4.108% after briefly getting to 4.117%, the highest since Dec. 13. The 2-year Treasury yield rose by around 11 basis points to trade at 4.335%.

December’s retail sales data indicated strong consumer demand at the holidays. Retail sales increased 0.6% for the month, above economists’ estimates of 0.4%, as compiled by Dow Jones. Excluding autos, sales rose 0.4%, which also topped a 0.2% estimate.

On Tuesday, yields jumped after comments from Federal Reserve Governor Christopher Waller, who suggested that while the central bank will likely cut rates this year, it may take its time.

At the World Economic Forum in Davos, more European Central Bank members indicated that markets were getting ahead of themselves on rate cut projections.

The president of the Dutch central bank, Klaas Knot, told CNBC Wednesday that the euro zone’s central bank looked at overall financial conditions, and that “the more easing the market has already done for us, the less likely we will cut rates.” Knot was referring to the fact that higher stock and bond prices in the fourth quarter of last year acted as the equivalent of easier interest rate policy, while lower prices act as the equivalent of tighter policy.

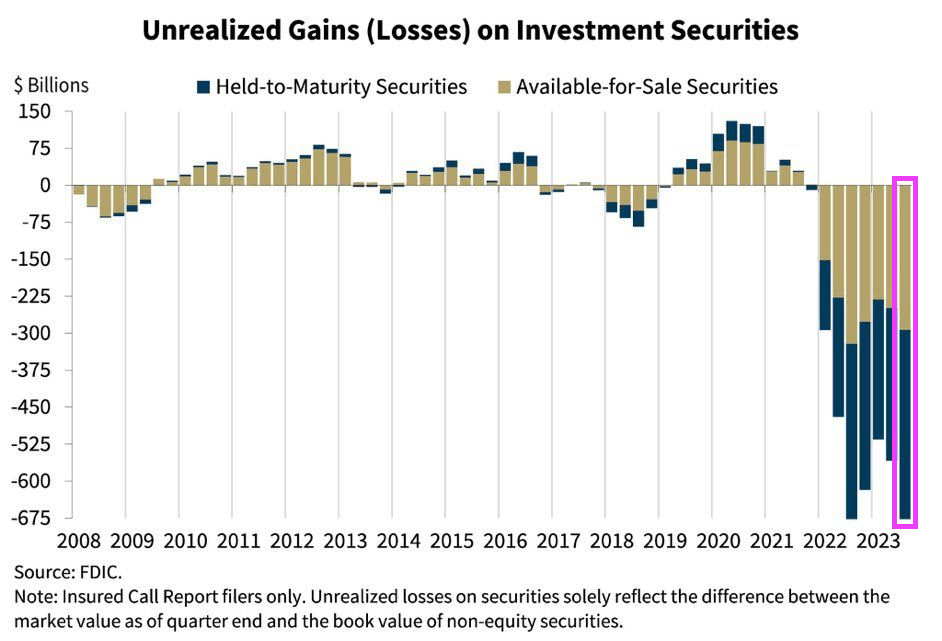

Rising interest rates are going to bite a big chunk out of The Fed’s massive ass (I mean balance sheet). Of course, The Fed sends the bill to Treasury. Gee, no wonder Biden/Yellen want so much money!

There is something wrong with letting aging politicians like Biden (81), Grassley (90), Pelosi (83), etc. borrow vast sums of money to spend when they will likely not be around for another 10 years.

You may remember that the Biden administration expected a significant deficit reduction from its tax increases and the expected benefits of its Inflation Reduction Act.

What Americans got was a massive deficit and persistent inflation.

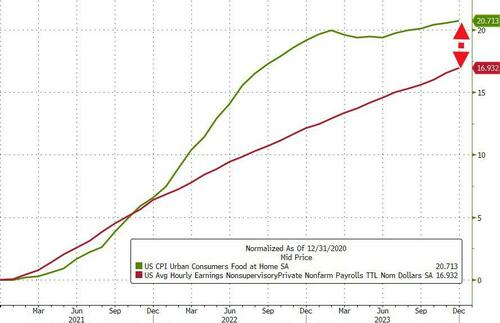

According to Moody’s chief economist, Mark Zandi, the entire disinflation process seen in the past years comes from exogenous factors such as “fading fallout from the global pandemic on global supply chains and labor markets, and the Russian War in Ukraine and the impact on oil, food, and other commodity prices.” The complete disinflation trend follows the slump in money supply (M2), but the Consumer Price Index (CPI) should have fallen faster if deficit spending, which means more consumption of newly created currency, would have been under control. December was disappointing and higher than it should have been.

The United States annual CPI (+3.4%) came above estimates, proving that the recent bounce in money supply and rising deficit spending continue to erode the purchasing power of the currency and that the base effect generated too much optimism in the past two prints. Most prices rose in December, and only four items fell. In fact, despite a large decline in energy prices, annual services (+5.3%), shelter (+6.2%), and transportation services (+9.7%) continue to show the extent of the inflation problem.

The massive deficit means more taxes, more inflation, and lower growth in the future.

The Congressional Budget Office (CBO) expects an unsustainable path that still leaves a 5.0% deficit by 2027, growing every year to reach a massive 10.0% of GDP in 2053 due to a much faster growth in spending than in revenues. The enormous increase in debt will also lead to extremely poor growth, with real GDP rising much slower throughout the 2023–2053 period than it has, on average, “over the past 30 years.”

Deficits are not a tool for growth; they are tools for stagnation.

Deficits mean that the currency’s purchasing power will continue to vanish with money printing and that the real disposable income of Americans will be demolished with a combination of higher taxes and a weaker real value of their wages and deposit savings.

We must remember that, in Biden’s administration’s own estimates, the accumulated deficit will reach $14 trillion in the period to 2032.

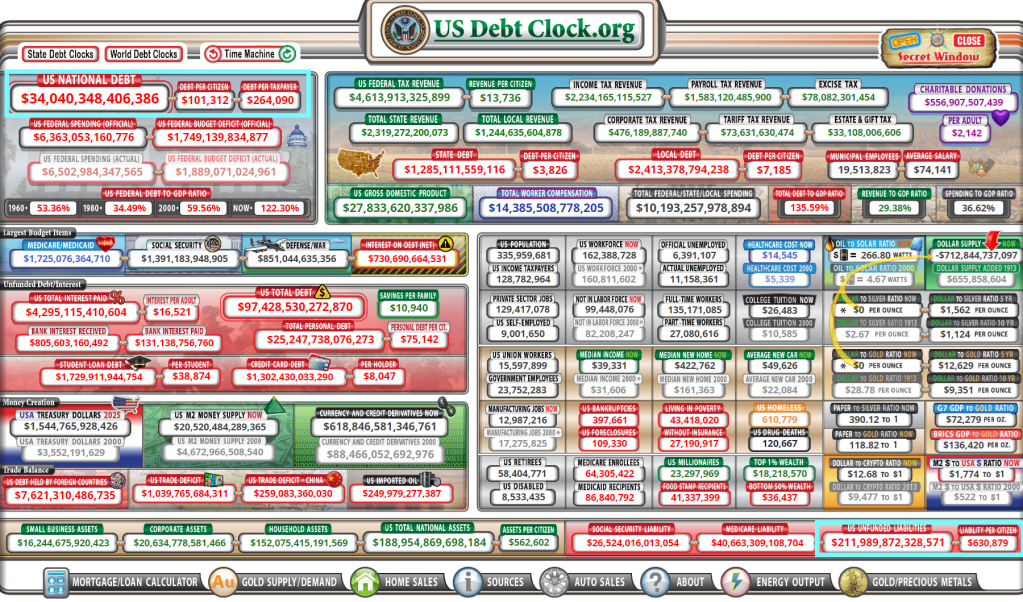

Yes, the US has $34 trillion in national debt and $212 trillion in promises made to keep the 99% quiet while the 1% gut the economy for their own wealth. Think Biden, Clintons, and various Congress Critters who suddenly become millionaires.

The Debt Star was born under Obama and weaponized under Biden/Pelosi/Schumer.

Yes, national debt rose under Trump too. Bear in mind that spending originates in The House and Trump was saddled with warhawks like RINO Paul Ryan and insider trading expert and warhawk Nancy Pelosi.

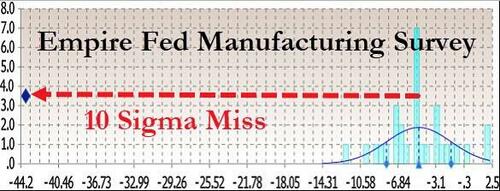

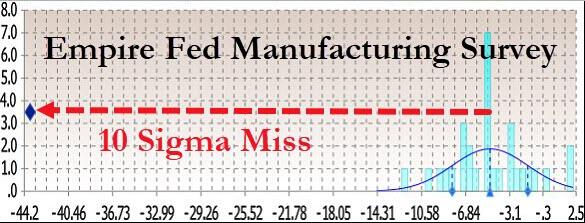

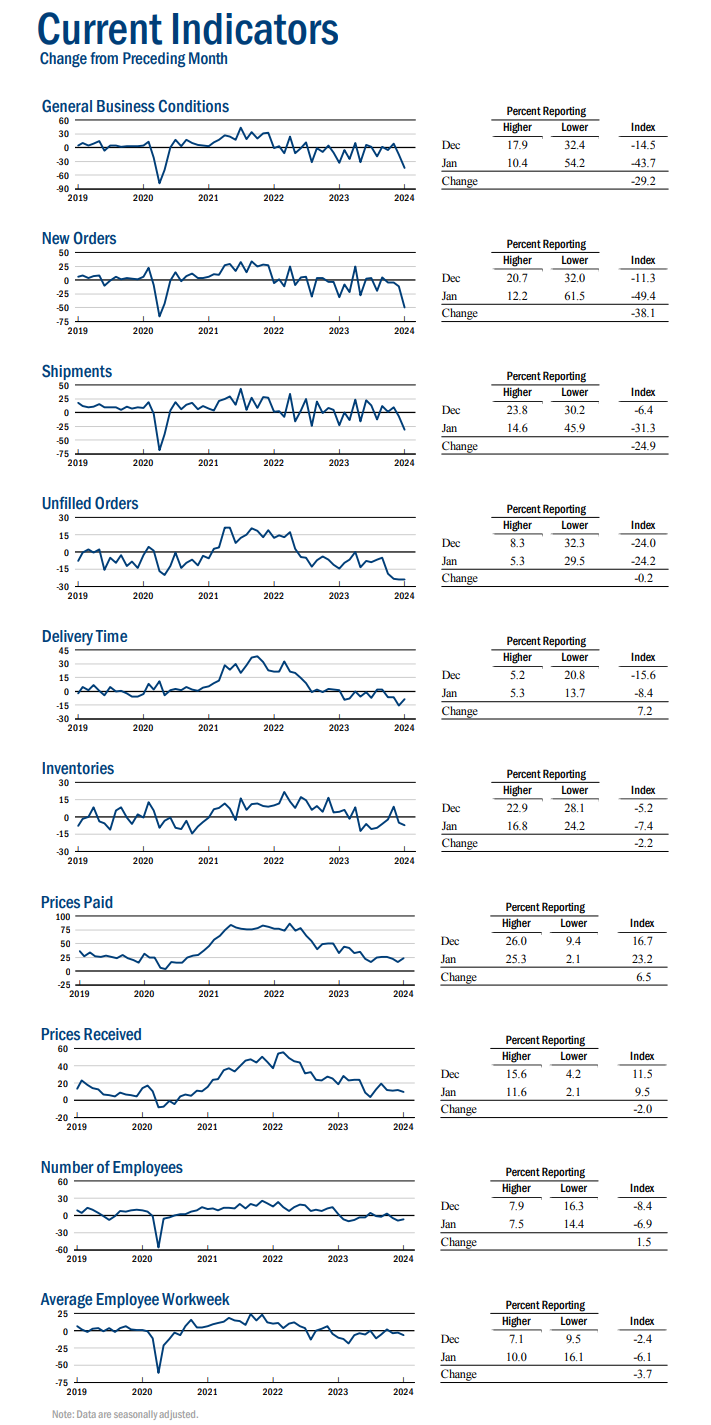

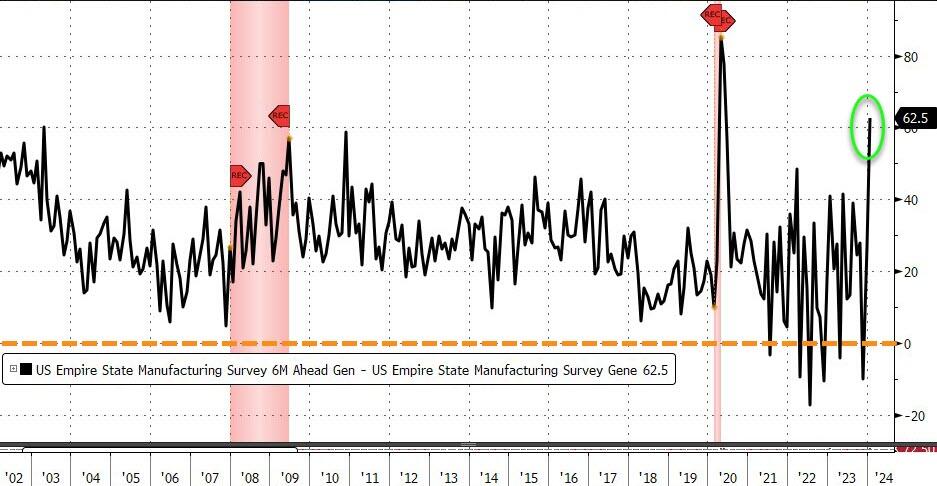

The -43.7 print was a stunning 10 standard deviations below expectations of a bounce to -5.0…

Source: Bloomberg

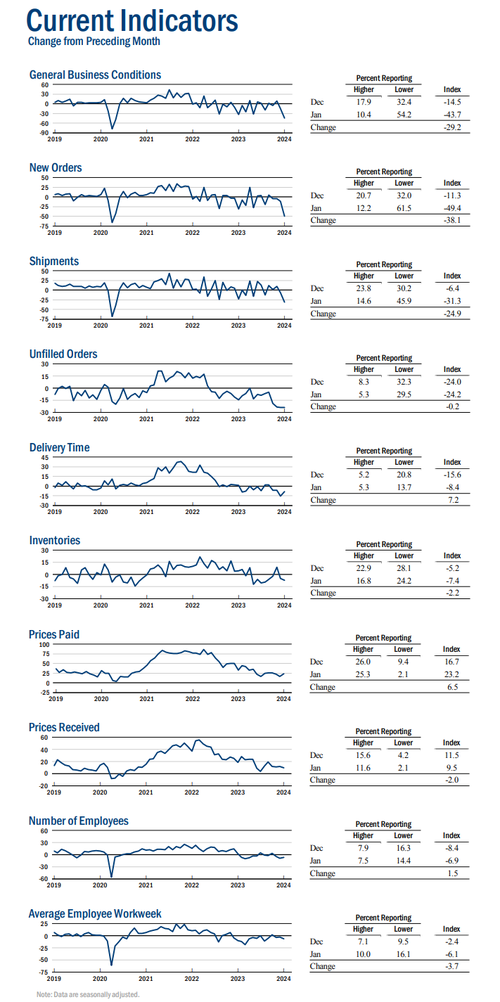

Under the hood, it was a bloodbath. New orders slumped more than 38 points to minus 49.4, the weakest since April 2020, while shipments dropped by the most since August. Worse still, the index of prices paid for materials increased to a three-month high.

But hope remains high as the six-month outlook for overall activity improved to a three-month high, suggesting manufacturing will stabilize at a weak level. The measure of the outlook for capital expenditures increased to the highest since April 2023, suggesting a pickup in investment.

However, the spread between current reality and a hopeful future is at near record highs (record Ex-COVID-lockdowns)…

Housing is simply unaffordable under Bidenomics, a strange brew of big corporate green subsidies, political handouts (any wonder why Biden is forgiving student loans in an election year?) and bad Fed policy errors.

But young Americans don’t always have a sugar daddy like Hunter Biden has who are willing to pay for rent for political parasites like those in Washington DC.

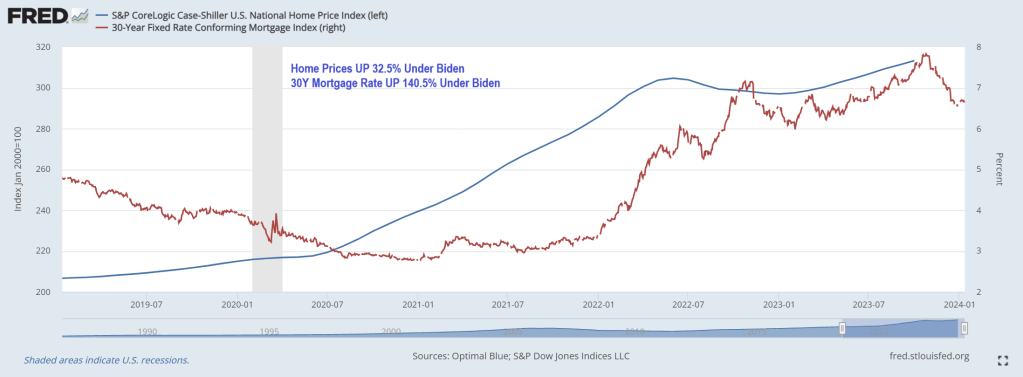

Young adults used to dream of moving out of their parents’ homes and into their own apartments, but living alone has become a luxury not everyone can afford. Not surprising, since home prices under Biden have risen 32.5% while 30-year mortgage rates are up a staggering 140.5% under Clueless Joe.

But in growth terms (year-over-year), White House Propagandists Karine Jean Pierre and John Kirby will no doubt focus on the cooling of housing prices and mortgage rates … although both are reaccelerating.

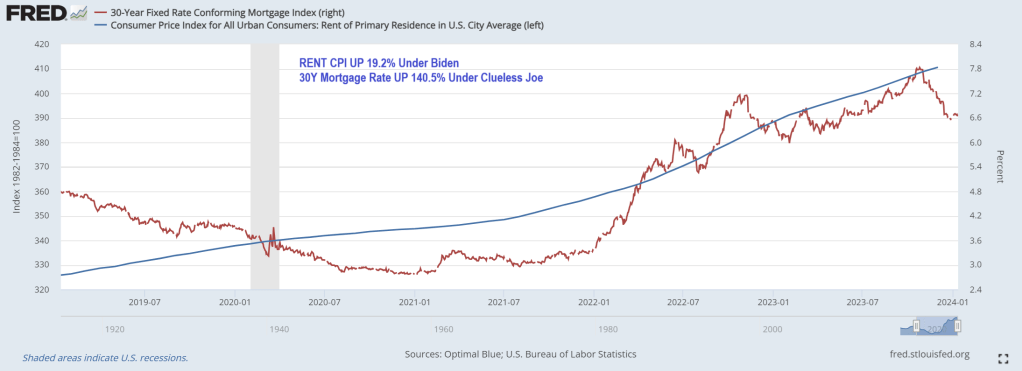

Rent CPI is up 19.2% under Clueless Joe.

How does this impact younger Americans? According to a recent study by Intuit Credit Karma, 31% of Gen Zers are living with their parents because they can’t afford to rent or buy their own place. Overall, 11% of American adults still live at home with their parents.

“The current housing market has many Americans making adjustments to their living situations, including relocating to less-expensive cities and even moving back in with their families,” said Courtney Alev, a consumer financial advocate at Intuit Credit Karma.

Even young adults who live alone are reconsidering their living arrangements because costs are too high.

About a quarter (27%) of Gen Zers reported that they could no longer afford rent and 25% said they’ll have to move back in with family to make ends meet.

Millennials are in the same boat: 30% say rent is unaffordable, and 25% are thinking about moving back in with their parents.

The research is consistent with a 2021 study conducted by the U.S. Census Bureau, which showed that one in three adults ages 18 to 34 live with their parents.

In a 2022 study, Pew Research also found that the percentage of Americans living with their parents has increased steadily since 2000. Pew calls these living arrangements “multigenerational households,” and said young adults ages 25 to 29 are most likely to cohabit with their parents.

Different studies, but all tell the same story: Finances are the top reason young adults are still living with family.

Housing and rental costs rise

It’s hardly surprising that young adults are struggling to make ends meet. Housing costs and living expenses have skyrocketed since the pandemic, and younger generations have faced the most financial hardship.

As Creditnews Research reports, Millennials and Gen Zers have been locked out of homeownership due to rising home prices, elevated interest rates, and stagnant real wages (adjusted for inflation).

For example, in 2023, Millennials accounted for only 28% of homebuyers despite being in their prime home-buying age. Gen Zers barely made a dent in the housing market, accounting for a paltry 4% of all buyers.

According to Fed data, average home prices were $431,000 as of the third quarter of 2023.

The rental market isn’t much better. Although rent costs have declined for three straight months, landlords are still asking for $1,964 per month on average, per Redfin data. Average rents were below $1,650 at the start of Covid.

But the problem of surging rents goes back much longer than that. According to a report from Moody’s Analytics, rent prices grew 135% between 1999 and 2022, while average incomes for all age groups were up 77% over the same period.

In terms of earning potential, younger generations are at the lower end of the totem pole, so they’re more likely to be affected by rising rent prices.

Where’s the “strong economy” everyone always talks about?

While the U.S. economy has steered clear of recession and unemployment remains near historic lows, Americans are still struggling to afford basic expenses. This is especially true for younger generations.

A 2023 study conducted by Deloitte found that more than half of Millennials and Gen Zers were living paycheck to paycheck. Perhaps shockingly, 37% of Millennials and 46% of Gen Z reported taking another part-time or full-time job just to afford their bills.

Working longer hours and barely scraping by is one of the main reasons why younger adults feel they’re worse off financially than their parents were at their age.

An August 2023 study conducted by The Harris Poll found that 74% of Millennials and 65% of Gen Zers believe they are starting further behind financially than previous generations.

“They’re telling us they can’t buy into that American dream the way that their parents and grandparents thought about it—because it’s not attainable,” said The Harris Poll CEO John Gerzema.

Remember, Clueless Joe Biden is in charge!(or Obama, take your pick).

For visitors, Universal Studios Florida offers a chance to visit a fantastical land full of wizards, Minions and various characters from NBC Universal’s many film and television properties. But for the roughly 28,000 men and women who work at the 840-acre theme park and resort complex in Orlando, the troubles of the real world — like the rising cost of housing — are not far away.

Central Florida has seen some of the nation’s fastest pandemic-era rent increases, thanks to a confluence of job growth, migration and housing underproduction that has put a strain on residents. The average tenant in the region saw their monthly rent jump by $600 between early 2020 and early 2023. According to the National Low Income Housing Coalition, the Orlando-Kissimmee-Sanford metro area has one of the worst affordable housing shortages in the US, with only 15 available units for every 100 extremely low-income renter households.

The dire need for workforce housing is behind the entertainment conglomerate’s latest project in Central Florida: a 1,000-unit mixed-use development, set to open in 2026, that promises to give tenants who work in the service industry a short commute to the constellation of tourist attractions and hotels nearby. To launch the project, Universal donated 20 acres of land adjacent to the Orange County convention center. Called Catchlight Crossings and built in partnership with local developer Wendover Housing Partners, the project broke ground in November.

Universal’s nearby rival is also wading into affordable housing. In 2022, Walt Disney Co.announced plans to donate 80 acres for a proposed 1,450-unit affordable development a few miles to the southwest. Also set to open in 2026, the project would be built near Flamingo Crossings Village, a campus for participants in Disney’s college internship program that also leases units to some Disney World cast members. (Oh great, brainwashing by woke Disney types).

As housing costs in Central Florida have soared, the theme park giants have faced criticism for underpaying workers. In June, Universal raised its minimum wage by $2 to $17 an hour, while Disney, which employs 82,00 people in Florida, agreed to bump its starting hourly rate to $18 in 2024. Still, both lag behind the $18.85 that the Massachusetts Institute of Technology’s Living Wage Calculator estimates would be needed to support an adult with no children in Orange County.

Visitors throng Disney’s Magic Kingdom in Orlando.Photographer: David Ryder/Bloomberg

Even smaller theme parks in more affordable areas have become homebuilders in an effort to ease the housing crunch. In May, Indiana’s Holiday World opened a $7 million development called Compass Commons, which is meant to provide seasonal housing for up to 136 employees. It will replace a proposed theme park attraction that was set to open last summer.

Such partnerships between entertainment industry employers, developers and local government represent the latest spin on a solution for the ongoing scarcity of apartments for lower-income households. Catchlight Crossings is part of Universal’s Housing to Tomorrow initiative, which was inspired by the Orange County mayor’s Housing for All Task Force. The company represents almost 10% of the tax base of Orange County, which includes Orlando.

“What could we do that would be more than just the typical corporate response?” said John Sprouls, executive vice president and chief administrative officer at Universal Parks and Resorts. “If you’re going to provide affordable housing, providing affordable housing where the jobs are sure makes a lot of sense.”

The Truly Missing Middle

Workforce housing is a much-needed housing type without a precise definition. Unlike affordable housing, which must meet stringent rental rates matched to specific income levels to qualify for government support and subsidies — typically 40% of units need to be priced to support those households who make 60% of the area median income — workforce housing stands as more of a catch-all term. Some define it as housing that serves those making between 80% and 120% of median area income. Often, the term is used to invoke housing for teachers, first responders and other public servants who have been increasingly priced out of expensive metros.

Over the last decade, and through the recent pandemic-era surge in apartment construction, developers have largely ignored the lower end of the market, focusing instead on Class A apartments. Beginning in 2013, half or more of units delivered each year were considered high-end or luxury, according to statistics from the National Multifamily Housing Council. Only since the middle of 2022 has that shifted towards Class B, or more affordable units.

Seeking lower production costs and rents, a handful of big developers have created new sub-brands of apartments designed to appeal to less-monied tenants. Grubb Properties launched a series of “car-light” developments called Link, which emphasize accessibility to major urban employers, while Greystar’s Modern Living Solutions concept offers modular multifamily buildings that are assembled on site from factory-built elements in an effort to trim construction costs.

To promote more construction of this type of housing, a bipartisan coalition of federal lawmakers recently introduced the Workforce Housing Tax Credit Act. Like the low-income housing tax credit, the proposed legislation would provide tax credit to investors who build affordable apartments. The bill’s sponsors, including Oregon Senator Ron Wyden, say the credit would finance approximately 344,000 affordable rental homes. It’s been a pet issue for Wyden in particular; 70% of Oregon school districts have built or rented housing to provide support for their teachers.

Nationwide, the US is short approximately 2.2 million workforce units, according to a 2022 Fannie Mae study. Central Florida’s service-based economy has left it with one of the highest levels of need, Wendover founder and Chief Executive Officer Jonathan Wolf said. There are roughly 100,000 people living within a five-mile radius of Catchlight Crossings who would income-qualify for the development.

Besides pools for residents, the proposed Universal development will include such amenities as a preschool and adult education center.Credit: Wendover Housing Partners

Rents at the Universal-led project will range from $400 to $2,200, depending on income qualifications (the average two-bedroom unit in the area rents for just shy of $1,900 a month). The development will also contain medical offices, retail, community space including pools and fitness centers, bike and walking paths and a tuition-free Bezos Academy preschool and adult education center. A transit center will connect residents to buses, ride-hailing services and company shuttles; a stop on the proposed Sunshine Corridor, a new east-west rail line that’s designed to help tourism workers get around, may take shape nearby.

“You’re not creating an economic ghetto,” Wolf said. “You’re creating a lifestyle enhancement for so many people, giving folks the ability for mobility.”

The theme park giant owns a few thousand acres in the area, so this was a relatively small donation, according to Sprouls. It also comes during a time of booming profits: Central Florida’s tourism industry generated a record $87.6 billion in economic impact in 2022. And since Universal transferred the land via a 501c3 charity with deed restrictions, the donation can lower development costs and help ensure long-term affordability; lots of affordable housing tends to revert back to market-rate pricing after a set term.

Employer-sponsored projects like Catchlight Crossings can’t mandate that only their employees can be tenants — that would violate fair housing rules. But for a customer-facing company like Universal, working to close the region’s housing gap can pay direct benefits, Sprouls said. When employees can’t find housing nearby and need to drive hours to get to work, it impacts not just their performance, but the guest experiences that drive satisfaction and repeat visits.

Park guests arrive at the Universal Studios theme park in Orlando in 2020.Photographer: Zack Wittman/Bloomberg

“It helps us to be able to recruit because people are able to have jobs here,” Sprouls said. “Salaries go into making you an attractive employer in the area, but you also need to make this an attractive place to live.”

Corporate Housing’s Mixed Record

Still, it remains to be seen if privately financed efforts like the Universal and Disney investments can have a significant impact on the lives of local renters. Other industries, most notably tech, have poured hundreds of millions of dollars and even billions into financing the construction of workforce housing near their headquarters. Amazon.com Inc., Google and Meta Platforms Inc. have all done variations of this kind of development, with mixed results. Many such efforts took off after severe backlash to the impact tech jobs had on local housing markets, and most were in the forms of loans, financing and leases, which can be helpful but not exactly game-changing. Recent swings in interest rates and increases in housing costs, not to mention struggles in the tech industry, have curtailed many of these programs.

“There was a lot of energy, and then there wasn’t,” Alex Schafran, a visiting scholar at San Jose State University’s Institute for Metropolitan Studies and a former consultant for Facebook’s housing initiative, told the Guardian. “The balloon didn’t pop overnight, but now there’s very little air in it.”

And the support of powerful local employers can’t inoculate these projects from community pushback. At a town meeting for the Disney project in September, residents raised a host of familiar objections about traffic congestion, school crowding and site location. When it comes to building multifamily developments, even Goofy has to contend with NIMBYs.

Wendover’s Wolf argues that while the financing part is critical, it may not be enough. His firm has been very involved in pushing for more government support for the affordable housing projects they specialize in. Associate Ryan von Weller, for example, was among the local developers who consulted with Florida lawmakers on a state bill, Live Local, which directed more than $700 million into supporting affordable housing. (Sprouls said Universal won’t see any tax benefits from their land donation.) But Wolf believes the area’s big corporate employers need to play a bigger role in solving this crisis.

“We need your involvement in it in a very direct way to work alongside us, to make this a success,” he said. “It’s not just a simple check and walk away. We need the land. We need cooperation.”

Here is the REAL problem with the lack of housing stock. Growth of new housing units has slowed to negative speeds as mortgage rates soared, but aren’t growing again with declining mortgage rates which remain relatively high. Add in the 11 million or so illegal immigrants crossing the border and we have a major problem.

Did you see the recent government propaganda from the U.S. Bureau of Labor Statistics?

Not the latest faulty claim that consumer prices increased at an annual rate of just 3.4 percent in December. But rather the claim that 216,000 jobs were added in December.

Upon release, and right on cue, Treasury Secretary Janet Yellen declared that the U.S. economy had achieved a soft landing. She also said that her “hope is that it will continue.”

What Yellen neglected to mention was that October employment was revised down by 45,000 jobs and November was revised down by 26,000 jobs. That’s 71,000 jobs the government recently reported which didn’t exist.

How many of the 216,000 jobs reported for December will wind up being pure fantasy?

Yellen also didn’t mention that 52,000 of the reported jobs are in government, 59,000 are in health care and social assistance, and 22,000 are in food services.

These aren’t the kind of jobs that create and spread new wealth and abundance to the economy.

In addition, there are 4.2 million workers that are employed part time for economic reasons.

This represents individuals who prefer full-time employment but are working part-time because their hours have been cut or they cannot find full-time work.

There are also 8.5 million multiple job holders. These are people who work more than one job because a single job doesn’t pay the bills.

Yellen, obviously, isn’t interested in these pesky details. What she is interested in is that when the data is massaged and contrived, and then summed up, the government can report an unemployment rate of 3.7 percent.

Hence, she can point to this number and crow about how through her expert navigation skills she has piloted a soft landing.

What’s really going on?

Here we’ll offer an anecdote followed by some thoughts…

Burning Ambition

Your editor’s son, a junior in high school, works at a pizza joint in the mall. There he makes and sells pizzas to hungry customers for $12.50 per hour – pre-tax. The minimum wage in Tennessee is $7.25 per hour.

Of note, he’s the only highschooler working there. His coworkers are all well into their dirty-30s. Some have kids. Some have multiple jobs. We haven’t asked any of them. But we suppose none would claim to be living the dream.

Reviews on Google are unflattering. They warn of pizzas and customer service that are of dubious quality. They tell a story of a shortage of good help. Here are several recent examples:

“Walked up to ask when they open. Some jerk behind the counter with a ponytail and big ear piercings goes, ‘Lights out not open!’ With a ton of attitude. We said, ‘You don’t have to be rude, we just wanted to know what time you opened.’ And his response was, ‘Welcome to the mall.’ What an absolute jerk. Don’t go here!”

“Ever had stale crackers with cheap ketchup and paper-thin burnt pepperoni on top of a thin layer of what was once cheap cheese before? If you’re on a quest to find the worst pizza in Knoxville, then come to the west town mall.”

“Got a slice of cheese pizza, sat down and the bottom of it was burnt. I tried to go get a different slice and he told me that all the other pizzas would be like that too and that it was normal for them to serve burnt pizza. He was a bit sarcastic about the situation.”

There are over one hundred reviews posted which share various tales of customer dissatisfaction. You’ve likely had similar experiences at your own local establishments. Burning pizzas and serving them with heapings of attitude is normal these days. Though having a burning ambition is rare.

What’s the point…

Cherry Picking Data Durations

These low-level service jobs, filled by people with low-level skill sets, are the jobs that Yellen is so excited about.

Absolutely, these jobs are important.

If they didn’t exist there would be no option to get cheap mall pizza while simultaneously getting insulted.

Life would be less abundant.

Nonetheless, these are not the type of jobs that drive the economy forward.

They certainly don’t offer opportunities for American workers to get ahead.

They don’t provide the cutting-edge skills, or the higher wages needed to propel the American economy above its foreign competitors.

One of Yellen’s key talking points is that wage growth is outpacing inflation. She can even point to the December jobs report for justification.

Based on the government propaganda, hourly earnings rose 4.1 percent in the year through December while consumer price inflation, as measured by the consumer price index (CPI), came in at 3.4 percent for the year. Here’s Yellen:

“Wage increases are running over price increases now. American workers are getting ahead and the progress for the middle-income families is very noticeable.”

Cherry picking data durations to support a false narrative is a longstanding tactic of big government statists. The reality is that on Yellen’s watch American workers have steadily fallen behind.

When you zoom out to show from December 2020 to the present, average hourly wages and CPI tell a much different story.

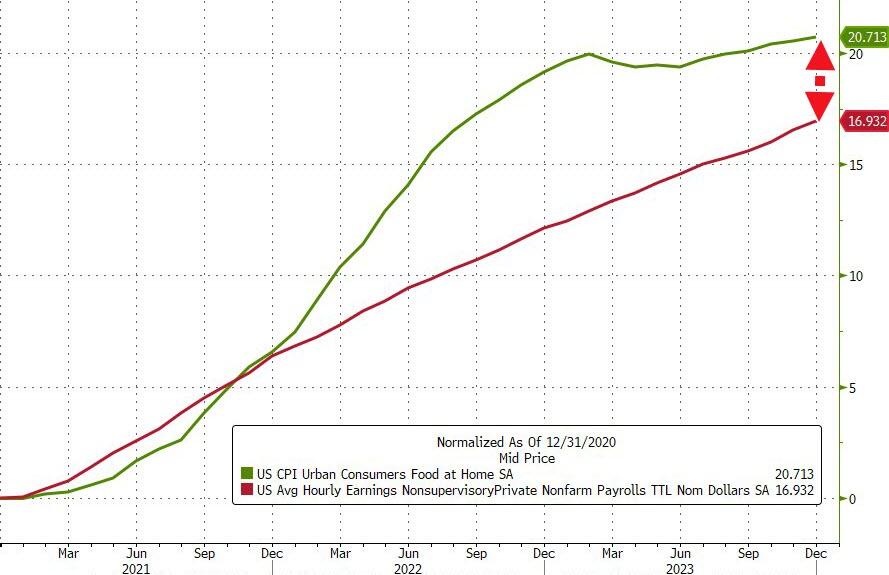

As David Stockman, the former Director of the Office of Management and Budget recently detailed, “the cost of living has risen 25 percent more than the average hourly wage.”

In other words, American workers have taken a significant pay cut over the last three years.

Yellen’s Bald-Faced Lies

If you didn’t know, Yellen has held various positions with the Federal Reserve and later the Treasury over the last 30 years. She’s participated in and advanced an era of unprecedented economic activism.

Moreover, Yellen and her colleagues at the Fed have their fingerprints all over the wage debasement that has taken place over the last several years.

As Stockman elaborated:

“A few years ago when the shortest inflation ruler available—the core PCE deflator—was running significantly below the Fed’s sacred 2.00% target, the Eccles Building was all for a catch-up of the level. The Fed even announced a policy of targeting inflation to average 2.0% over time, which ukase did not include, conveniently, the exact span of time to be measured.

“‘The Federal Reserve now intends to implement a strategy called flexible average inflation targeting (FAIT). Under this new strategy, the Federal Reserve will seek inflation that averages 2% over a time frame that is not formally defined. This means that after long periods of low inflation, the Federal Reserve will not enact tighter monetary policy to prevent rates higher than 2%. One benefit of this flexible strategy to managing the mandate of price stability is that it will impose fewer restrictions on the mandate of full employment.’

“Wouldn’t you know it? The Fed switched to ‘averaging’ in August 2020—just months before inflation went soaring to levels not seen since the 1970s.”

The gap between reality – consumer price increases vs wage increases – and what government bureaucrats want you to believe to be true takes frequent bald-faced lies to fill.

Yellen, for her part, excels at selectively using contrived data to make assertions that are visibly false.

We don’t know if she believes the propaganda she spews or if her intent is to deceive people. Regardless, the whole act is exceedingly wearisome.

The Federal Reserve has tightened their monetary manipulations to combat inflation caused by loose monetary policy and excessive spending by Biden and Congress.

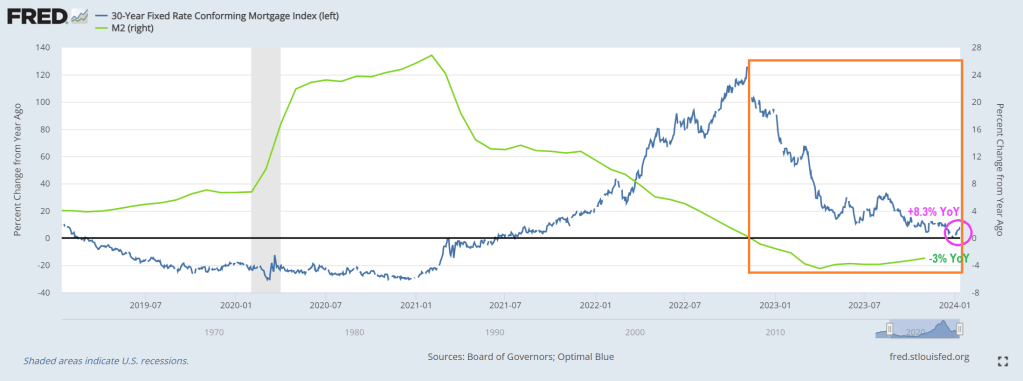

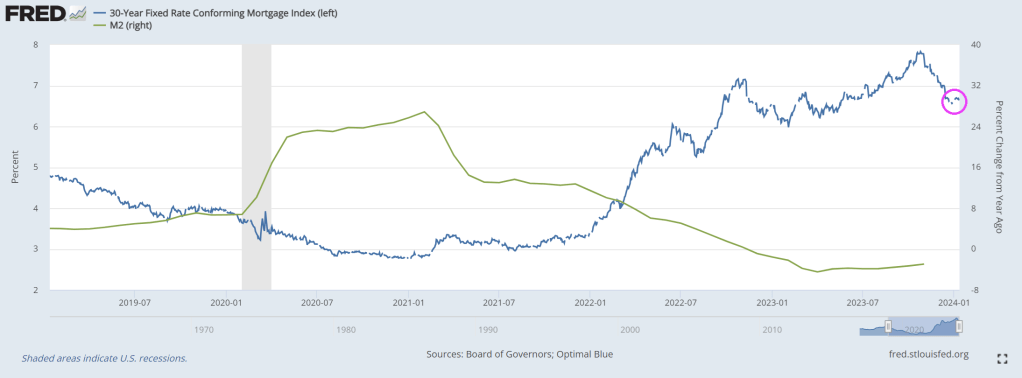

The result? US conforming 30-year mortgage rates are up 8.3% since last year and up a whopping 141% since the beginning of 2021 (the year Biden was selected to be President).

Check out mortgage rate GROWTH (blue line) as M2 Money growth *green line) went negative (orange box).

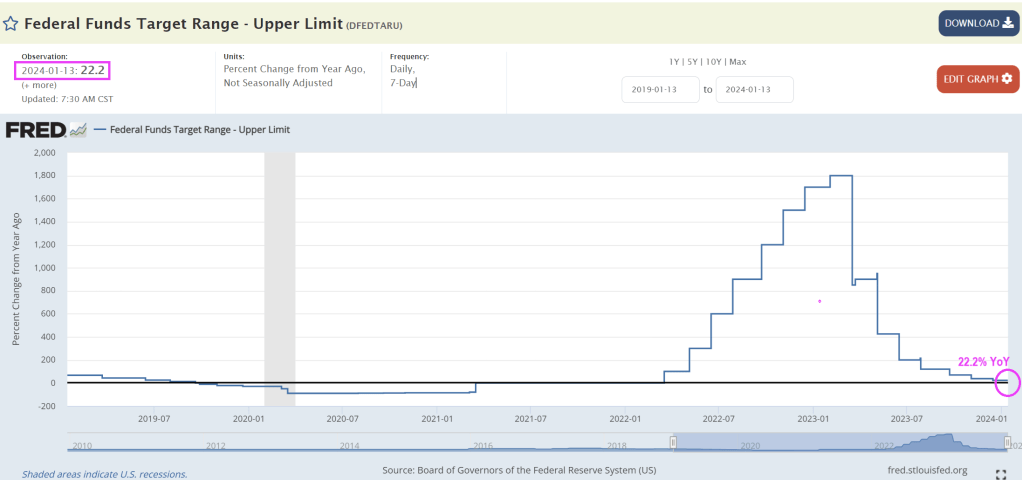

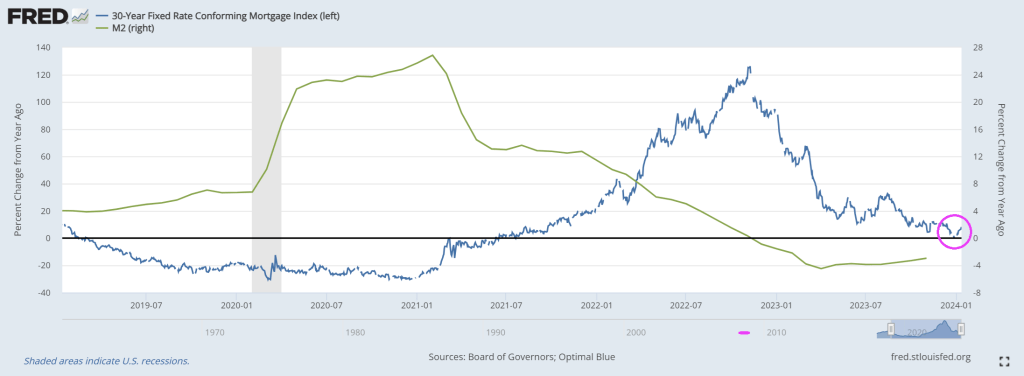

This graph corresponds nicely with this chart of YoY changes in The Fed Funds rate. Which is still rising at a rate of 22.2% year-over-year (YoY).

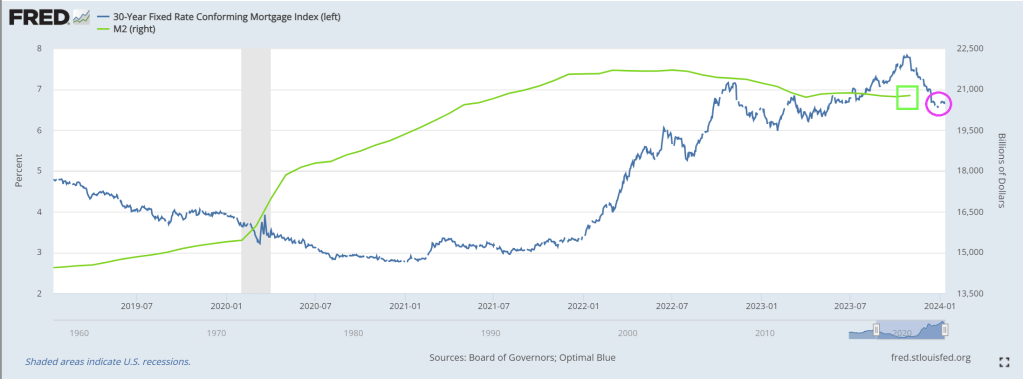

The 30-year mortgage rate had been falling after peaking in August 2023 after peaking at 7.299%. The latest reading on January 11, 2024 was 6.662%.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.