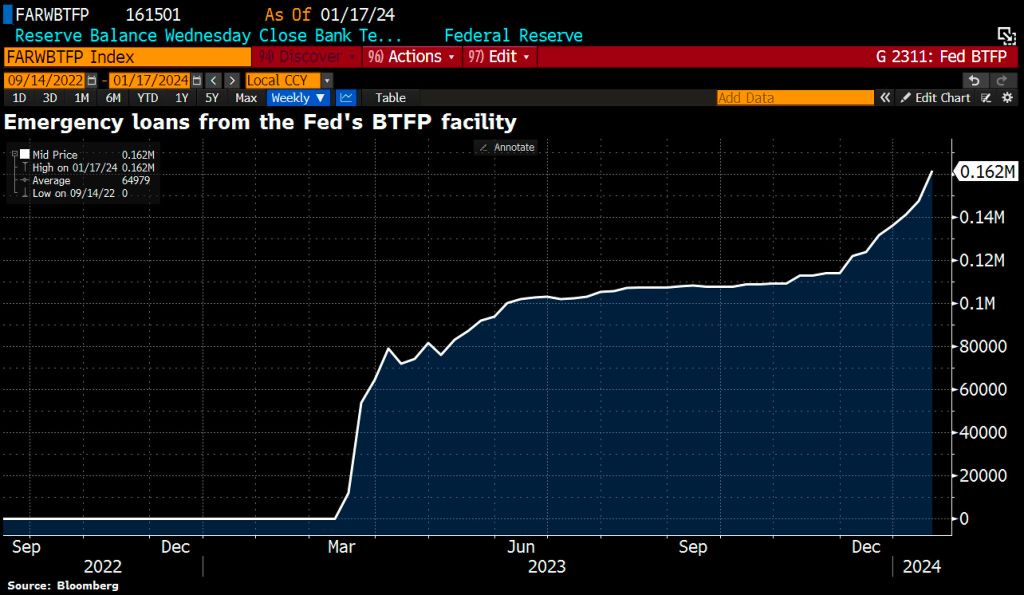

Remember the massive bank bailout of “subprime” mortgage securities back that resulted in the Dodd-Frank banking legislation of 2010? Yes know, where they promised NO MORE BANK BAILOUTS EVER??? Particularly if Disease X is unleashed and we start shutting down economies and schools again. Will we see ANOTHER bank bailout??

Cantor Fitzgerald CEO Howard Lutnick spoke with Fox Business host Maria Bartiromo on the sidelines at the World Economic Forum in Davos, Switzerland, last week. He offered a bleak outlook on the commercial real estate sector, warning a “very ugly” two years is ahead.

“Coming due in the next two and a half years at these higher rates – you’re not going to get proceeds, meaning when you have a $120 million loan on a building, and someone says I’ll give you 90 million at a much higher rate – than it throws the keys back to the lenders – and there’s going to be a lot of them that are going to get wiped out,” Lutnick told Bartiromo.

“I think $700 billion could default … The lenders are going to have to do things with them. They’re going to be selling. It’s going to be a generational change in real estate coming at the end of 2024 and all of 2025. We will be talking about real estate being just a massive change,” Lutnick said.

He warned: “I think it’s going to be a very, very ugly market in owning real estate over the next, you know, 18 months, two years.”

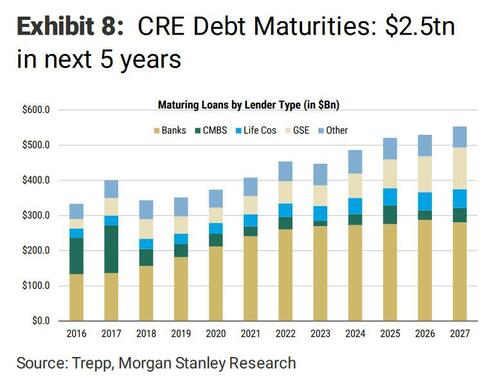

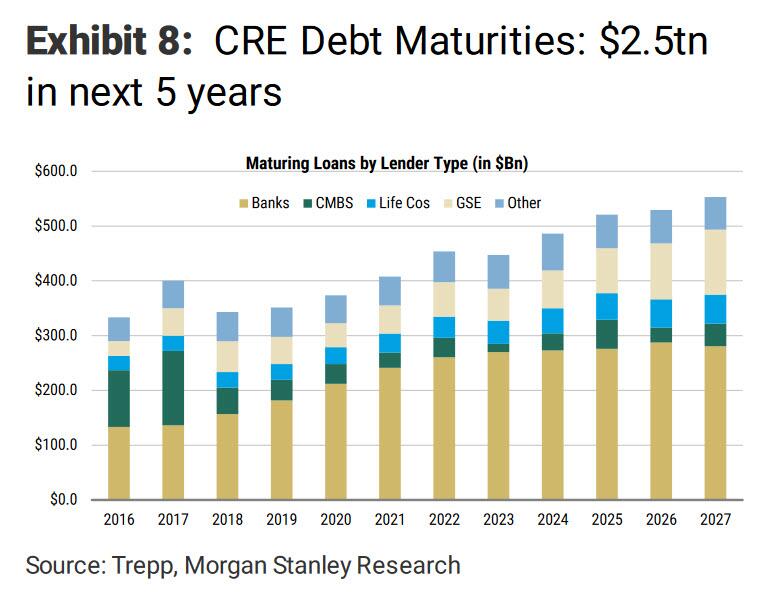

Lutnick noted that loan sales are set to become a major business opportunity with the upcoming maturity of CRE mortgages. He highlighted that an estimated trillion dollars of CRE debt is coming due over the next 2.5 years.

Shortly after the regional bank implosion in March 2023, Morgan Stanley penned a note to clients about a $2.5 trillion wall of CRE debt coming due over five years.

A recent survey of Terminal users by Bloomberg’s Markets Live found most respondents believe the office tower market needs a deeper correction before a rebound materializes.

Lutnick pointed out, “Real estate equity, REITS, are going to be in trouble … a lot of them are going to be wiped out, so many defaults, I think.”

Bloomberg office REITs have been plunging since early 2022 when the Federal Reserve embarked on the most aggressive interest rate hiking cycle in a generation to tame inflation.

“Commercial real estate is experiencing a meaningful repricing as cap rates correlate to long-term to interest rates,” Morgan Stanley told clients in a recent report, adding, “Patience is required while refinancing to higher debt costs gradually triggers valuation adjustments.”

Lutnick’s not the only one with a dismal outlook on CRE.

In a recent interview, Scott Rechler, Chairman and CEO of RXR Realty, told Goldman’s Allison Nathan that the CRE downturn is still in the early innings.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.