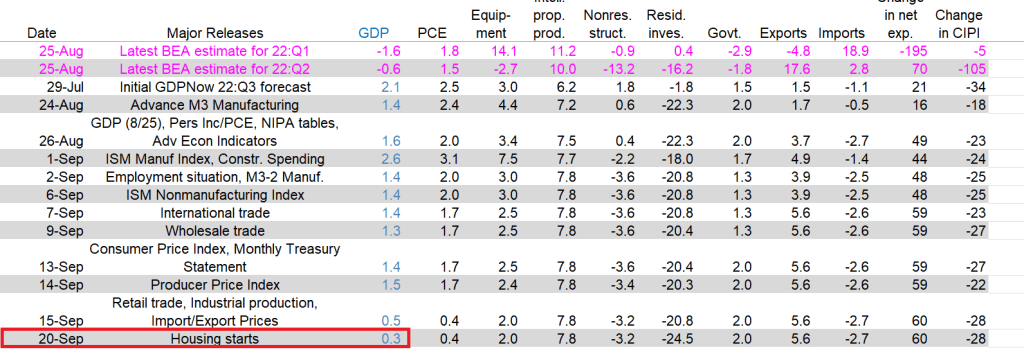

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the third quarter of 2022 is 0.3 percent on September 20, down from 0.5 percent on September 15. After this morning’s housing starts report from the US Census Bureau, the nowcast of third-quarter residential investment growth decreased from -20.8 percent to -24.5 percent.

The culprit? US Housing starts!

We knew from this morning that housing starts declined -0.01% YoY as The Fed’s Stimulypto wears off.

It was not immediately clear why buyers had submitted requests for capacity when Russia has given no indication since it shut the line that it would restart any time soon.

Russia, which had supplied about 40% of the European Union’s gas before the Ukraine conflict, has said it closed the pipeline because Western sanctions hindered operations. European politicians say that is a pretext and accuse Moscow of using energy as a weapon.

But German inflation, using CPI, is only 7.9%. Something has to give!

On the western front (US), the US Treasury 10yr yield is up +10.2 bps. And sovereign yields in Europe are all above 10 bps.

Even Obama’s economic advisor, Larry Summers, is wondering why Biden won’t allow pipelines to be build to reduce energy prices and reduce inflation.

Having said that, US mortgage rates are now the highest since 2008 and continue to rise with the expectation of more Fed rate hikes this year. Even core inflation is on the rise motivating The Fed to do more tightening since they aren’t receiving any help from Biden on energy or Congress in terms of massive spending of our money.

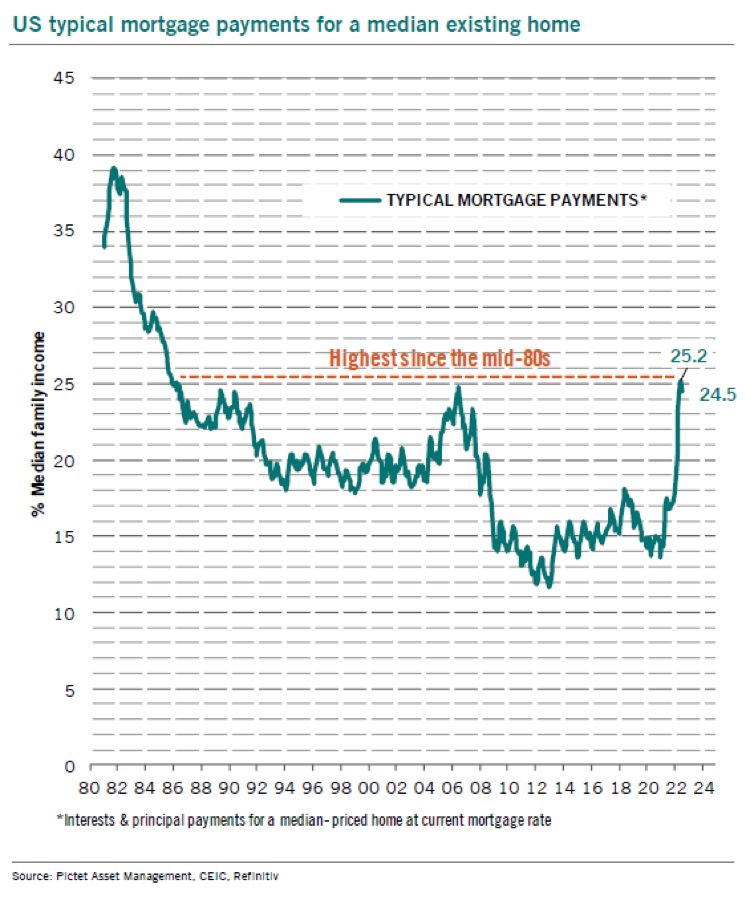

Mortgage payments for a median existing home in the US is back to the mid-1980s.

Data from Fed Funds futures implies that The Fed will raise their target rate to 4.50% by March 2023, then slowly lower rates.

Futures are down with the prospect of a 75 basis point bump in rates tomorrow. The Dow Jone Mini is down -167 points.

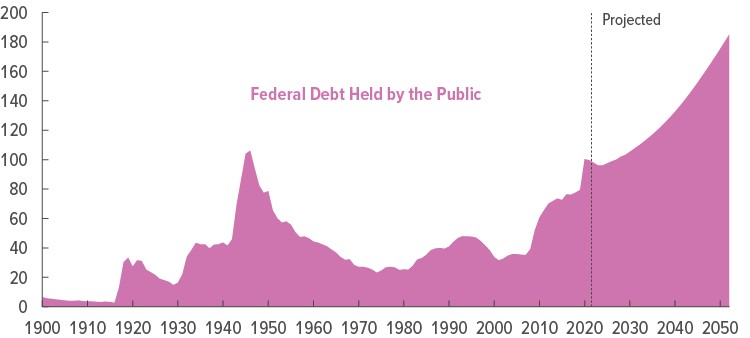

The Federal Reserve’s Open Market Committee (FOMC) will announce their latest round of rate increases on Wednesday, September 21st, at 2pm EST. Will the members of the FOMC discuss the fact that the US debt load is now at a whopping 123% of GDP?? Or will the FOMC only discuss inflation in its deliberations?

The Fed is expected to raise the upper-bound of their target rate to 3.25%, a 75 basis point increase in a futile attempt to cool inflation. Yet the rampant spending by Biden, Pelosi and Schumer (3 of the 4 Horsemen of the Economic Apocalypse) has raised the Federal Debt to GDP ratio to 123%. Even more disturbing, M2 Money Velocity (GDP/M2 Money) is near the all-time low. Meaning that rampant Federal spending is doing little to increase GDP.

Raging US inflation is resulting in Federal Reserve monetary tightening, causing the 30-year US mortgage rate to hit it highest level since November 2008 (the beginning of Fed Quantitative Easing). Bankrate’s 30-year mortgage rate just hit 6.28%, the highest rate in 14 years.

The Biden Administration will be remembered for crippling inflation, the highest in 40 years AND the highest mortgage rate in 14 years.

And with Fed chatter about hiking rates, Dr T (me) predicts pain for the mortgage market.

According to the Committee for a Responsible Budget (what a misnomer for insane-spending Congress and the Biden Administration), the Biden Administration has just approved $4.8 TRILLION in new Federal borrowing, leading to an increase in the budget deficit of another $4.8 TRILLION.

With a Democrat majority in The House, and VP Harris with the tie-breaker in the Senate, it is hardly surprising that Democrats have gone on a legendary spending spree which has helped drive inflation to 40 year highs.

Particularly since Fed monetary policy and “green” spending has resulted in a seismic shift in wealth towards the 1% under Obama and Biden.

The Federal government reaction to the Covid outbreak in early 2020 included massive monetary stimulus, Federal government spendathons and Biden’s green energy policies have resulted in a sizzling 8.5% inflation rate (update on Monday morning).

The problem is that The Federal Reserve is far behind the inflation curve with their target rate at only 2.5%. And The Fed’s balance sheet remains near $9 TRILLION in assets held.

In Euroland, we are seeing a similar problem (Frankfurt, we have a problem!). The Eurozone inflation rate is at 9.1% while their version of The Fed Funds Target rate is only 0.75%, a large catch-up gap.

If we look at the Taylor Rule for the US using headline inflation, we see that The Fed needs to raise their target rate to … 21.72% to crush inflation.

In Euroland, the problem is similar. At 9.10% inflation, the ECB will have to raise their version of The Fed’s target rate to 16.80% to combat inflation. As if that will happen in either the US or Euroland.

On a different note, is it my imagination or does US Democrat Senate candidate from Pennsylvania John Fetterman look like the alien from the flick “Battleship”?

As The Fed takes away the massive monetary punch bowl, mortgage rates have risen to the highest since November 2008. And with the withdrawal of monetary stimulus (raising Fed Target Rate), mortgage purchase applications have declined.

Here is a photo of The Federal Reserve fighting the housing and mortgage market.

(Bloomberg)Investors who might be looking for the world’s biggest bond market to rally back soon from its worst losses in decades appear doomed to disappointment.

The US employment report on Friday illustrated the momentum of the economy in face of the Federal Reserve’s escalating effort to cool it down, with businesses rapidly adding jobs, pay rising and more Americans entering the workforce. While Treasury yields slipped as the figures showed a slight easing of wage pressures and an uptick in the jobless rate, the overall picture reinforced speculation the Fed is poised to keep raising interest rates — and hold them there — until the inflation surge recedes.

Swaps traders are pricing in a slightly better-than-even chance that the central bank will continue lifting its benchmark rate by three-quarters of a percentage point on Sept. 21 and tighten policy until it hits about 3.8%. That suggests more downside potential for bond prices because the 10-year Treasury yield has topped out at or above the Fed’s peak rate during previous monetary-policy tightening cycles. That yield is at about 3.19% now.

Then we have Bankrate’s 30-year mortgage rate soaring on Fed intervention expectations.

Inflation? US inflation is near its highest in 40 years and the USDollar Plain Vanilla Swap was at 0.50 when Biden first took office as President and is now 3.371 (quite an increase!).

Here is an interesting chart of FNCL 2% Agency MBS.

Thanks to Federal Reserve increases in their target rate, the 30-year mortgage rate has risen above 6%.

What drives me crazy about The Fed is their failure to removed monetary stimulus following the financial crisis of 2008 when they dropped their target rate to 25 basis points (0.25%) and began assets purchases (orange line). The Fed raises their target rate only once during Obama’s Presidency but then raised rates 8 times after Trump was elected President.

Now we are seeing The Fed NOT shrinking their balance sheet in a meaningful way. However M2 Money growth YoY (green line) has slowed to 5.2%.

While it is a good thing that The Fed is FINALLY reducing some of the monetary stimulus in place since 2008, the bad thing is that mortgage rates are rising rapidly.

The Fed’s quantheads are predicted to resume easing in March 2023.

You must be logged in to post a comment.