Isn’t it wonderful to be 81 years old like Biden and a have a credit card with seemingly no credit limit? And partner with other octogenarians like Pelosi and McConnell to bankrupt the US? Free-spending US Senate Demagogue Democrat Chuck Schumer is only 73. But all these elderly politicians are heaping debt on to backs of younger Americans.

The “surprise” Q4 GDP report showed GDP rising by $182.6 billion. Unfortunately, Biden had to borrow $834 billion to get $182.6 in GDP.

Graphically, we can Biden’s folly where Q4 public debt grew almost 5 times faster than real GDP.

Remember the massive bank bailout of “subprime” mortgage securities back that resulted in the Dodd-Frank banking legislation of 2010? Yes know, where they promised NO MORE BANK BAILOUTS EVER??? Particularly if Disease X is unleashed and we start shutting down economies and schools again. Will we see ANOTHER bank bailout??

Cantor Fitzgerald CEO Howard Lutnick spoke with Fox Business host Maria Bartiromo on the sidelines at the World Economic Forum in Davos, Switzerland, last week. He offered a bleak outlook on the commercial real estate sector, warning a “very ugly” two years is ahead.

“Coming due in the next two and a half years at these higher rates – you’re not going to get proceeds, meaning when you have a $120 million loan on a building, and someone says I’ll give you 90 million at a much higher rate – than it throws the keys back to the lenders – and there’s going to be a lot of them that are going to get wiped out,” Lutnick told Bartiromo.

“I think $700 billion could default … The lenders are going to have to do things with them. They’re going to be selling. It’s going to be a generational change in real estate coming at the end of 2024 and all of 2025. We will be talking about real estate being just a massive change,” Lutnick said.

He warned: “I think it’s going to be a very, very ugly market in owning real estate over the next, you know, 18 months, two years.”

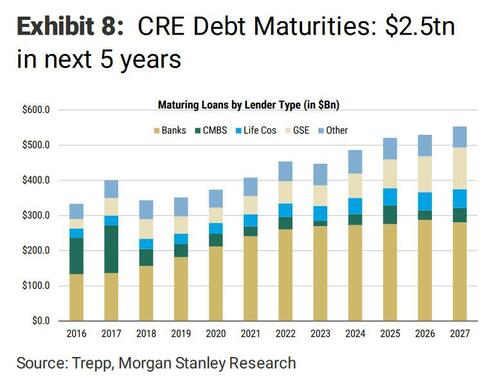

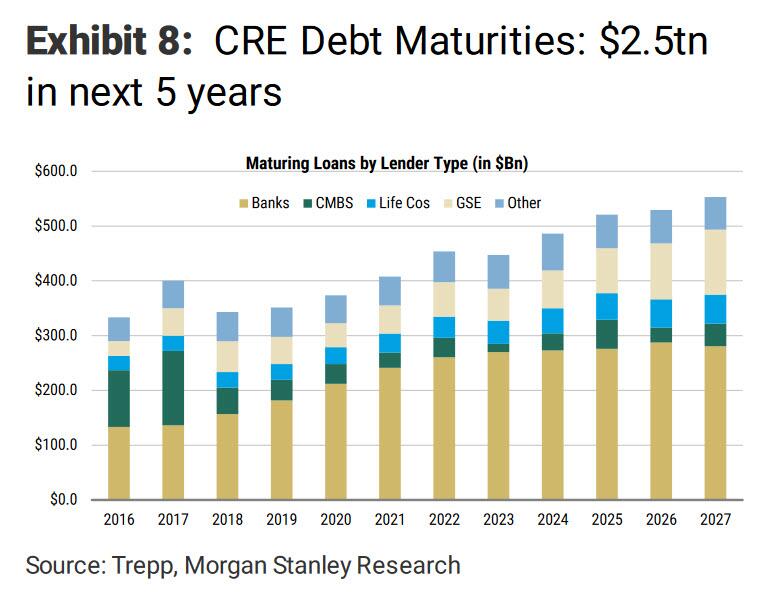

Lutnick noted that loan sales are set to become a major business opportunity with the upcoming maturity of CRE mortgages. He highlighted that an estimated trillion dollars of CRE debt is coming due over the next 2.5 years.

Shortly after the regional bank implosion in March 2023, Morgan Stanley penned a note to clients about a $2.5 trillion wall of CRE debt coming due over five years.

A recent survey of Terminal users by Bloomberg’s Markets Live found most respondents believe the office tower market needs a deeper correction before a rebound materializes.

Lutnick pointed out, “Real estate equity, REITS, are going to be in trouble … a lot of them are going to be wiped out, so many defaults, I think.”

Bloomberg office REITs have been plunging since early 2022 when the Federal Reserve embarked on the most aggressive interest rate hiking cycle in a generation to tame inflation.

“Commercial real estate is experiencing a meaningful repricing as cap rates correlate to long-term to interest rates,” Morgan Stanley told clients in a recent report, adding, “Patience is required while refinancing to higher debt costs gradually triggers valuation adjustments.”

Lutnick’s not the only one with a dismal outlook on CRE.

In a recent interview, Scott Rechler, Chairman and CEO of RXR Realty, told Goldman’s Allison Nathan that the CRE downturn is still in the early innings.

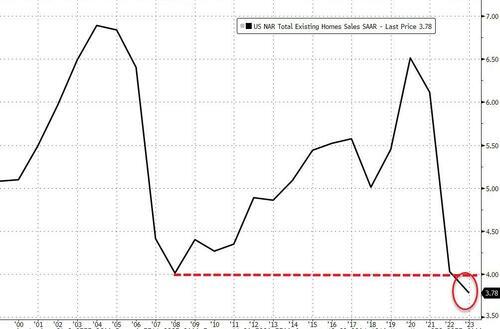

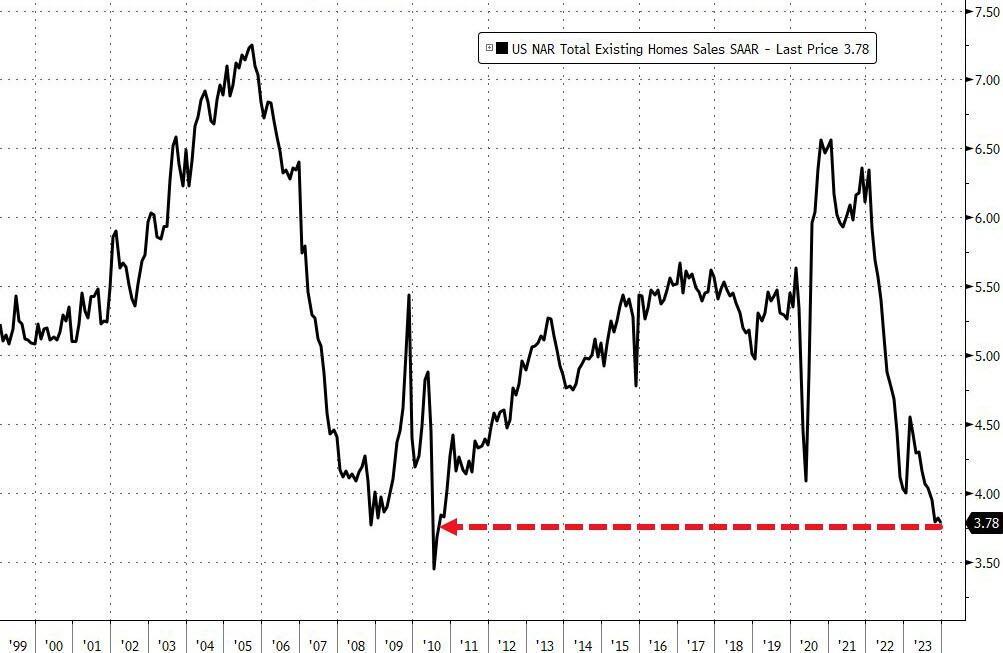

Existing Home Sales fell 1.0% MoM in December, worse than the +0.3% expected, leaving sales down

Source: Bloomberg

Total Existing Home Sales in December 2023 were 3.78mm – the lowest SAAR since 2010…

Source: Bloomberg

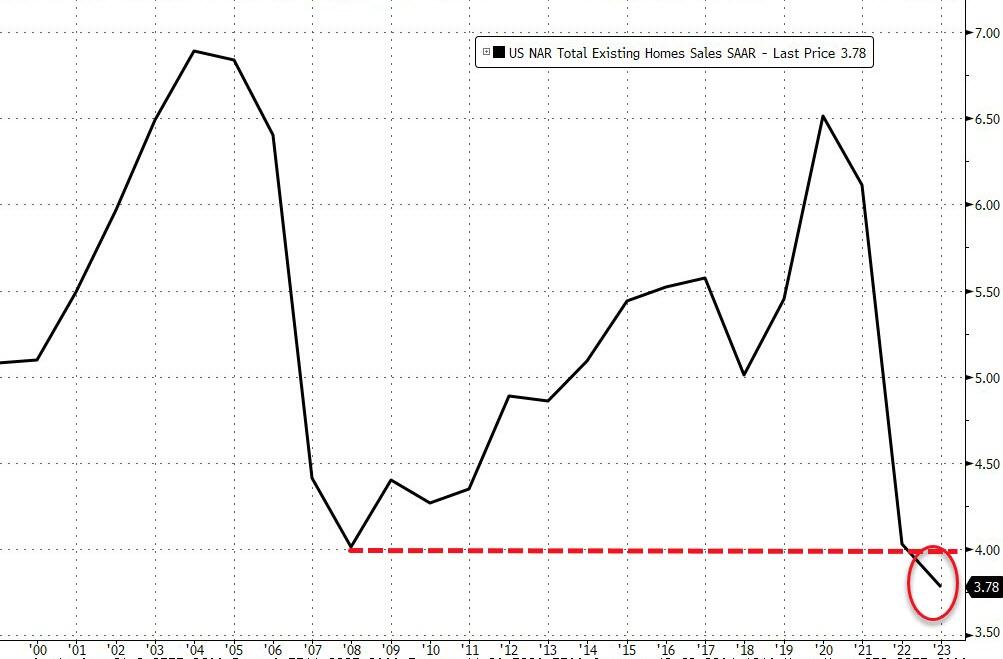

But, on an annual basis, this is the worst year on record (back to at least 1995)..

Source: Bloomberg

“The latest month’s sales look to be the bottom before inevitably turning higher in the new year,” said NAR Chief Economist Lawrence Yun. “Mortgage rates are meaningfully lower compared to just two months ago, and more inventory is expected to appear on the market in upcoming months.”

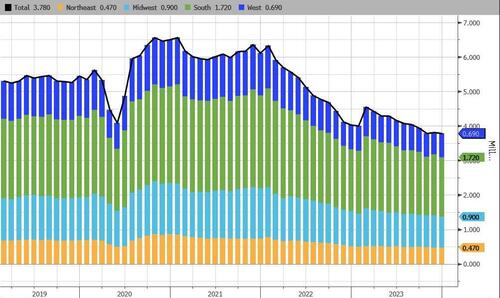

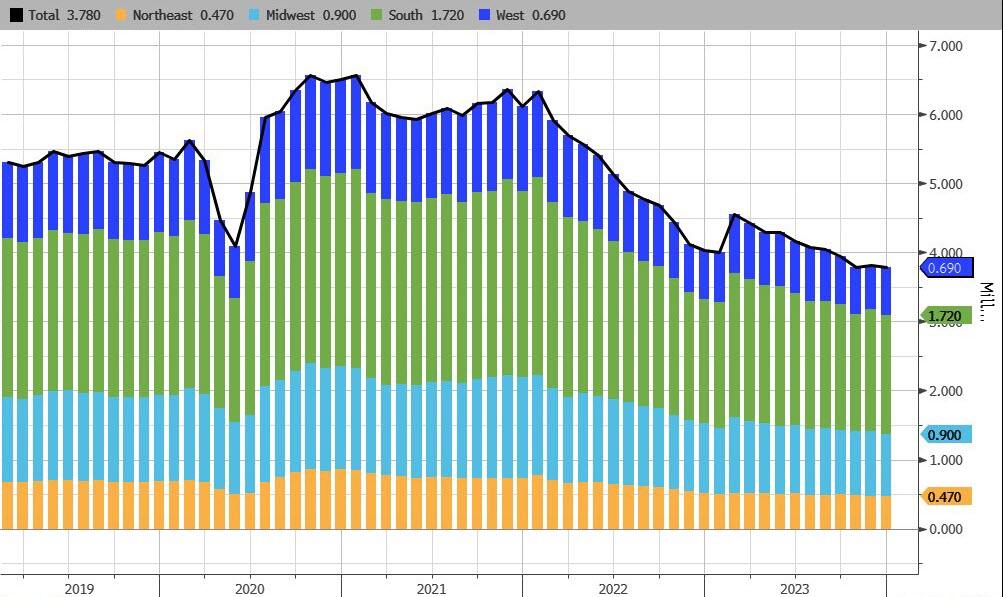

Existing Home Sales were flat in the Northeast, lower in the MidWest and the South, and up marginally in the West (driven by single-family-home sales as condo sales declined)…

Source: Bloomberg

Last month, the number of previously owned homes for sale dropped to 1 million, the lowest since March.

At the current sales pace, selling all the properties on the market would take 3.2 months.

Realtors see anything below five months of supply as indicative of a tight resale market.

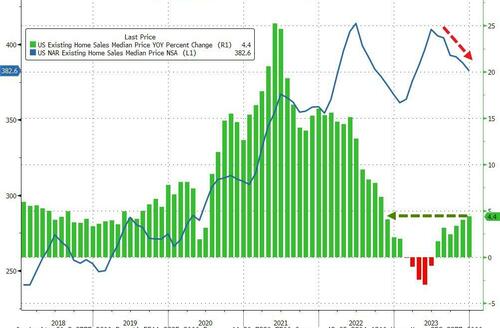

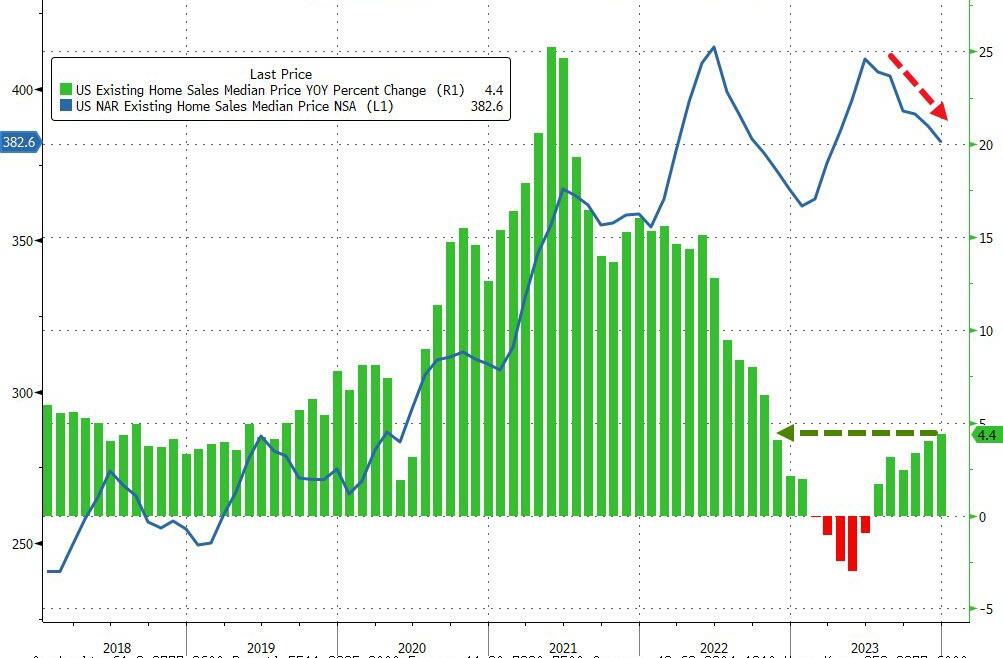

That lack of inventory is helping to keep prices elevated.

The median selling price climbed 4.4% to $382,600 in December from a year ago, reflecting increases in all four regions. Prices hit a record of $389,800 in 2023.

Source: Bloomberg

But, with mortgage rates having tumbled (and given the lagged responses), are sales about to start rising again?

Source: Bloomberg

So The Fed managed to kill sales, collapse inventories, send home prices higher, destroying affordability… and now what is going to happen?

The yield on the 10-year Treasury note was recently up 4 basis points at 4.108% after briefly getting to 4.117%, the highest since Dec. 13. The 2-year Treasury yield rose by around 11 basis points to trade at 4.335%.

December’s retail sales data indicated strong consumer demand at the holidays. Retail sales increased 0.6% for the month, above economists’ estimates of 0.4%, as compiled by Dow Jones. Excluding autos, sales rose 0.4%, which also topped a 0.2% estimate.

On Tuesday, yields jumped after comments from Federal Reserve Governor Christopher Waller, who suggested that while the central bank will likely cut rates this year, it may take its time.

At the World Economic Forum in Davos, more European Central Bank members indicated that markets were getting ahead of themselves on rate cut projections.

The president of the Dutch central bank, Klaas Knot, told CNBC Wednesday that the euro zone’s central bank looked at overall financial conditions, and that “the more easing the market has already done for us, the less likely we will cut rates.” Knot was referring to the fact that higher stock and bond prices in the fourth quarter of last year acted as the equivalent of easier interest rate policy, while lower prices act as the equivalent of tighter policy.

Rising interest rates are going to bite a big chunk out of The Fed’s massive ass (I mean balance sheet). Of course, The Fed sends the bill to Treasury. Gee, no wonder Biden/Yellen want so much money!

There is something wrong with letting aging politicians like Biden (81), Grassley (90), Pelosi (83), etc. borrow vast sums of money to spend when they will likely not be around for another 10 years.

You may remember that the Biden administration expected a significant deficit reduction from its tax increases and the expected benefits of its Inflation Reduction Act.

What Americans got was a massive deficit and persistent inflation.

According to Moody’s chief economist, Mark Zandi, the entire disinflation process seen in the past years comes from exogenous factors such as “fading fallout from the global pandemic on global supply chains and labor markets, and the Russian War in Ukraine and the impact on oil, food, and other commodity prices.” The complete disinflation trend follows the slump in money supply (M2), but the Consumer Price Index (CPI) should have fallen faster if deficit spending, which means more consumption of newly created currency, would have been under control. December was disappointing and higher than it should have been.

The United States annual CPI (+3.4%) came above estimates, proving that the recent bounce in money supply and rising deficit spending continue to erode the purchasing power of the currency and that the base effect generated too much optimism in the past two prints. Most prices rose in December, and only four items fell. In fact, despite a large decline in energy prices, annual services (+5.3%), shelter (+6.2%), and transportation services (+9.7%) continue to show the extent of the inflation problem.

The massive deficit means more taxes, more inflation, and lower growth in the future.

The Congressional Budget Office (CBO) expects an unsustainable path that still leaves a 5.0% deficit by 2027, growing every year to reach a massive 10.0% of GDP in 2053 due to a much faster growth in spending than in revenues. The enormous increase in debt will also lead to extremely poor growth, with real GDP rising much slower throughout the 2023–2053 period than it has, on average, “over the past 30 years.”

Deficits are not a tool for growth; they are tools for stagnation.

Deficits mean that the currency’s purchasing power will continue to vanish with money printing and that the real disposable income of Americans will be demolished with a combination of higher taxes and a weaker real value of their wages and deposit savings.

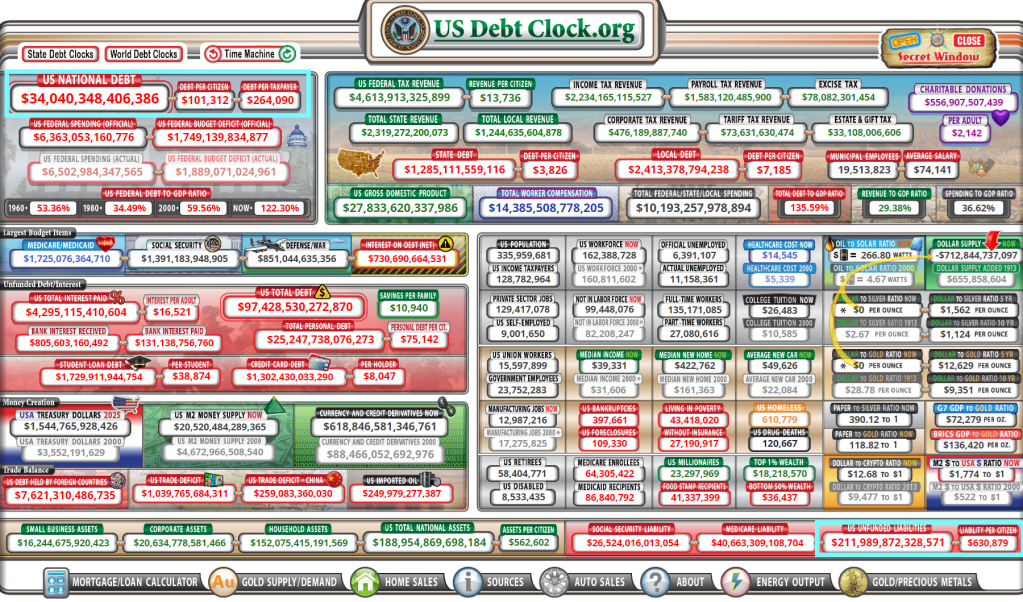

We must remember that, in Biden’s administration’s own estimates, the accumulated deficit will reach $14 trillion in the period to 2032.

Yes, the US has $34 trillion in national debt and $212 trillion in promises made to keep the 99% quiet while the 1% gut the economy for their own wealth. Think Biden, Clintons, and various Congress Critters who suddenly become millionaires.

The Debt Star was born under Obama and weaponized under Biden/Pelosi/Schumer.

Yes, national debt rose under Trump too. Bear in mind that spending originates in The House and Trump was saddled with warhawks like RINO Paul Ryan and insider trading expert and warhawk Nancy Pelosi.

Did you see the recent government propaganda from the U.S. Bureau of Labor Statistics?

Not the latest faulty claim that consumer prices increased at an annual rate of just 3.4 percent in December. But rather the claim that 216,000 jobs were added in December.

Upon release, and right on cue, Treasury Secretary Janet Yellen declared that the U.S. economy had achieved a soft landing. She also said that her “hope is that it will continue.”

What Yellen neglected to mention was that October employment was revised down by 45,000 jobs and November was revised down by 26,000 jobs. That’s 71,000 jobs the government recently reported which didn’t exist.

How many of the 216,000 jobs reported for December will wind up being pure fantasy?

Yellen also didn’t mention that 52,000 of the reported jobs are in government, 59,000 are in health care and social assistance, and 22,000 are in food services.

These aren’t the kind of jobs that create and spread new wealth and abundance to the economy.

In addition, there are 4.2 million workers that are employed part time for economic reasons.

This represents individuals who prefer full-time employment but are working part-time because their hours have been cut or they cannot find full-time work.

There are also 8.5 million multiple job holders. These are people who work more than one job because a single job doesn’t pay the bills.

Yellen, obviously, isn’t interested in these pesky details. What she is interested in is that when the data is massaged and contrived, and then summed up, the government can report an unemployment rate of 3.7 percent.

Hence, she can point to this number and crow about how through her expert navigation skills she has piloted a soft landing.

What’s really going on?

Here we’ll offer an anecdote followed by some thoughts…

Burning Ambition

Your editor’s son, a junior in high school, works at a pizza joint in the mall. There he makes and sells pizzas to hungry customers for $12.50 per hour – pre-tax. The minimum wage in Tennessee is $7.25 per hour.

Of note, he’s the only highschooler working there. His coworkers are all well into their dirty-30s. Some have kids. Some have multiple jobs. We haven’t asked any of them. But we suppose none would claim to be living the dream.

Reviews on Google are unflattering. They warn of pizzas and customer service that are of dubious quality. They tell a story of a shortage of good help. Here are several recent examples:

“Walked up to ask when they open. Some jerk behind the counter with a ponytail and big ear piercings goes, ‘Lights out not open!’ With a ton of attitude. We said, ‘You don’t have to be rude, we just wanted to know what time you opened.’ And his response was, ‘Welcome to the mall.’ What an absolute jerk. Don’t go here!”

“Ever had stale crackers with cheap ketchup and paper-thin burnt pepperoni on top of a thin layer of what was once cheap cheese before? If you’re on a quest to find the worst pizza in Knoxville, then come to the west town mall.”

“Got a slice of cheese pizza, sat down and the bottom of it was burnt. I tried to go get a different slice and he told me that all the other pizzas would be like that too and that it was normal for them to serve burnt pizza. He was a bit sarcastic about the situation.”

There are over one hundred reviews posted which share various tales of customer dissatisfaction. You’ve likely had similar experiences at your own local establishments. Burning pizzas and serving them with heapings of attitude is normal these days. Though having a burning ambition is rare.

What’s the point…

Cherry Picking Data Durations

These low-level service jobs, filled by people with low-level skill sets, are the jobs that Yellen is so excited about.

Absolutely, these jobs are important.

If they didn’t exist there would be no option to get cheap mall pizza while simultaneously getting insulted.

Life would be less abundant.

Nonetheless, these are not the type of jobs that drive the economy forward.

They certainly don’t offer opportunities for American workers to get ahead.

They don’t provide the cutting-edge skills, or the higher wages needed to propel the American economy above its foreign competitors.

One of Yellen’s key talking points is that wage growth is outpacing inflation. She can even point to the December jobs report for justification.

Based on the government propaganda, hourly earnings rose 4.1 percent in the year through December while consumer price inflation, as measured by the consumer price index (CPI), came in at 3.4 percent for the year. Here’s Yellen:

“Wage increases are running over price increases now. American workers are getting ahead and the progress for the middle-income families is very noticeable.”

Cherry picking data durations to support a false narrative is a longstanding tactic of big government statists. The reality is that on Yellen’s watch American workers have steadily fallen behind.

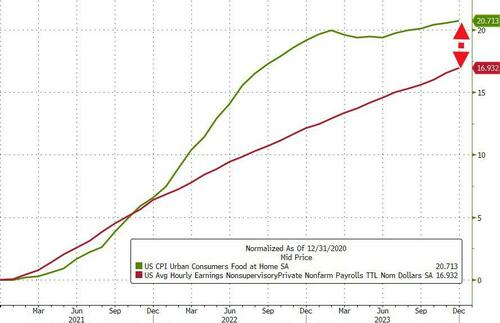

When you zoom out to show from December 2020 to the present, average hourly wages and CPI tell a much different story.

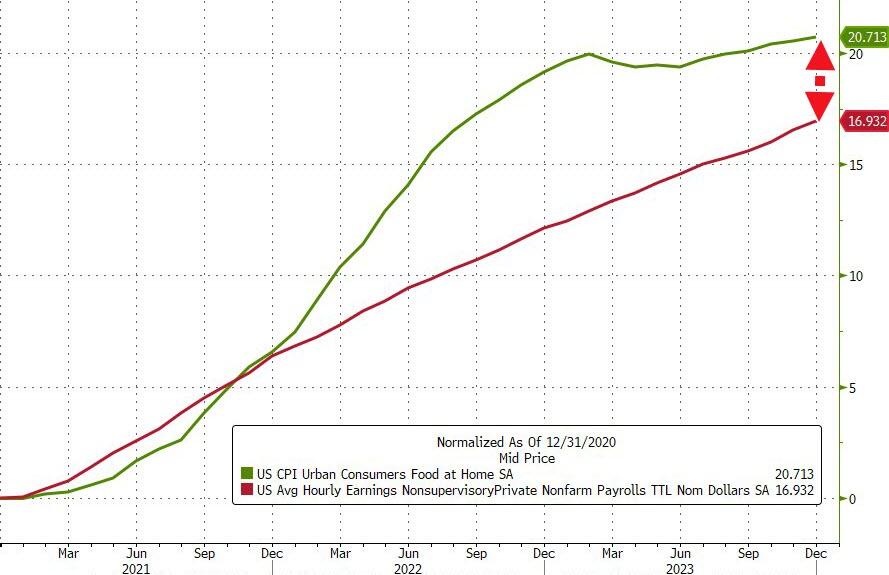

As David Stockman, the former Director of the Office of Management and Budget recently detailed, “the cost of living has risen 25 percent more than the average hourly wage.”

In other words, American workers have taken a significant pay cut over the last three years.

Yellen’s Bald-Faced Lies

If you didn’t know, Yellen has held various positions with the Federal Reserve and later the Treasury over the last 30 years. She’s participated in and advanced an era of unprecedented economic activism.

Moreover, Yellen and her colleagues at the Fed have their fingerprints all over the wage debasement that has taken place over the last several years.

As Stockman elaborated:

“A few years ago when the shortest inflation ruler available—the core PCE deflator—was running significantly below the Fed’s sacred 2.00% target, the Eccles Building was all for a catch-up of the level. The Fed even announced a policy of targeting inflation to average 2.0% over time, which ukase did not include, conveniently, the exact span of time to be measured.

“‘The Federal Reserve now intends to implement a strategy called flexible average inflation targeting (FAIT). Under this new strategy, the Federal Reserve will seek inflation that averages 2% over a time frame that is not formally defined. This means that after long periods of low inflation, the Federal Reserve will not enact tighter monetary policy to prevent rates higher than 2%. One benefit of this flexible strategy to managing the mandate of price stability is that it will impose fewer restrictions on the mandate of full employment.’

“Wouldn’t you know it? The Fed switched to ‘averaging’ in August 2020—just months before inflation went soaring to levels not seen since the 1970s.”

The gap between reality – consumer price increases vs wage increases – and what government bureaucrats want you to believe to be true takes frequent bald-faced lies to fill.

Yellen, for her part, excels at selectively using contrived data to make assertions that are visibly false.

We don’t know if she believes the propaganda she spews or if her intent is to deceive people. Regardless, the whole act is exceedingly wearisome.

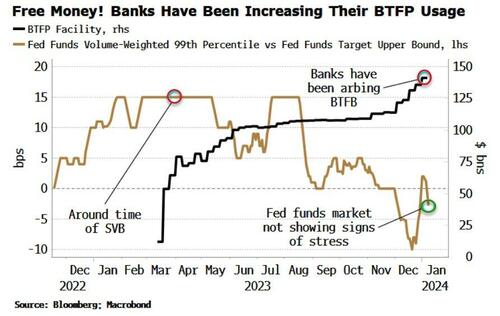

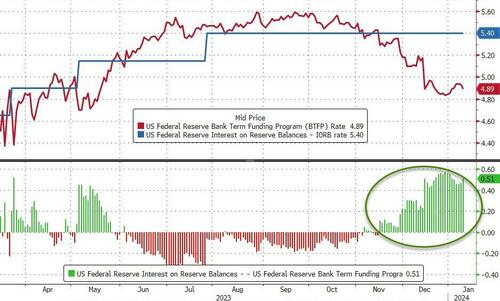

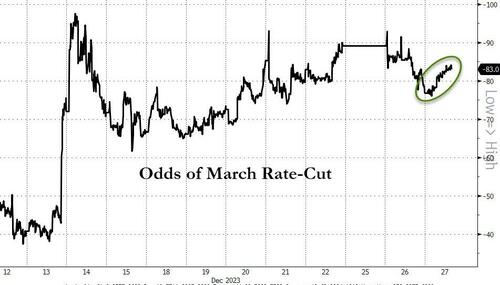

Here we sit with core inflation rate BELOW the current Fed Funds Target Rate (upper bound). So is it time to start withdrawing its more than ample monetary stimulus. Like the Bank Term Funding Program.

The Federal Reserve is likely to retire the Bank Term Funding Program in March. This would entail an additional ongoing headwind for reserves, and thus liquidity, through 2024. At the margin, this adds weight to the case for the Fed cutting interest rates sooner in the year.

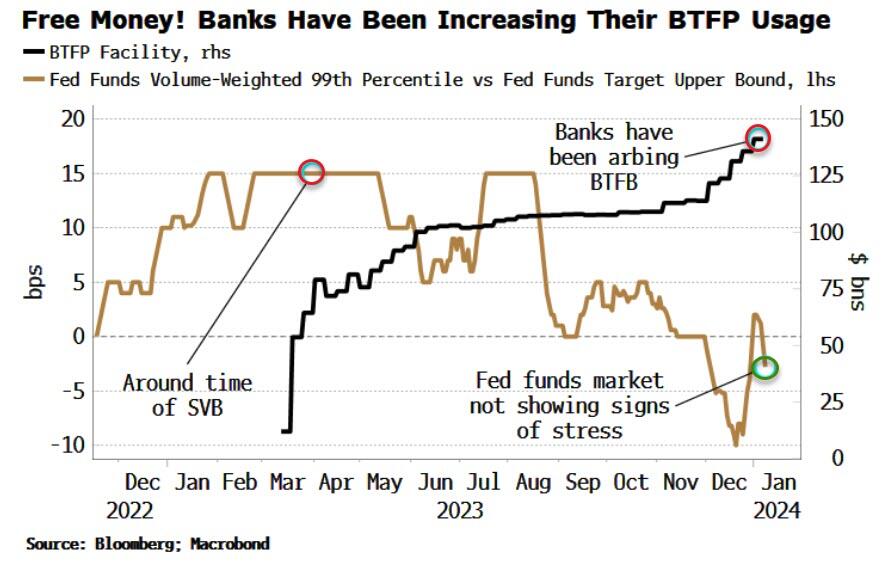

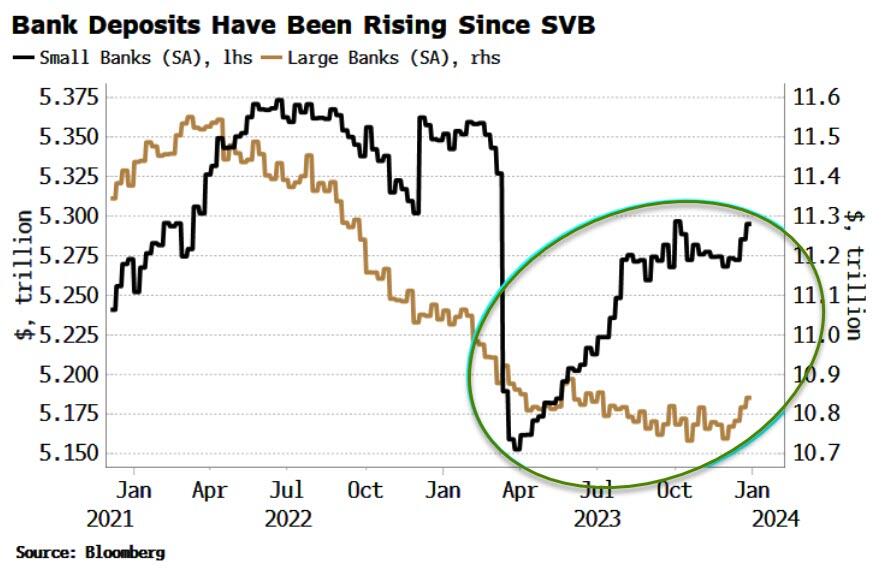

The BTFP was created in the wake of the SVB crisis to help struggling banks get access to liquidity when bond prices were dropping. However, its use in recent months has jumped to over $140 billion. That is not, however, a sign of banking stress.

The chart below shows the usage of the BTFP along with the rate paid at the 99th percentile in the fed funds market relative to the upper bound of the range for fed funds.

As can be seen, this is under zero, i.e. banks are not having to pay up to get liquidity.

This is in stark contrast to last March at the time of SVB’s fall when some banks were having to pay 15 bps above the fed funds upper bound for liquidity.

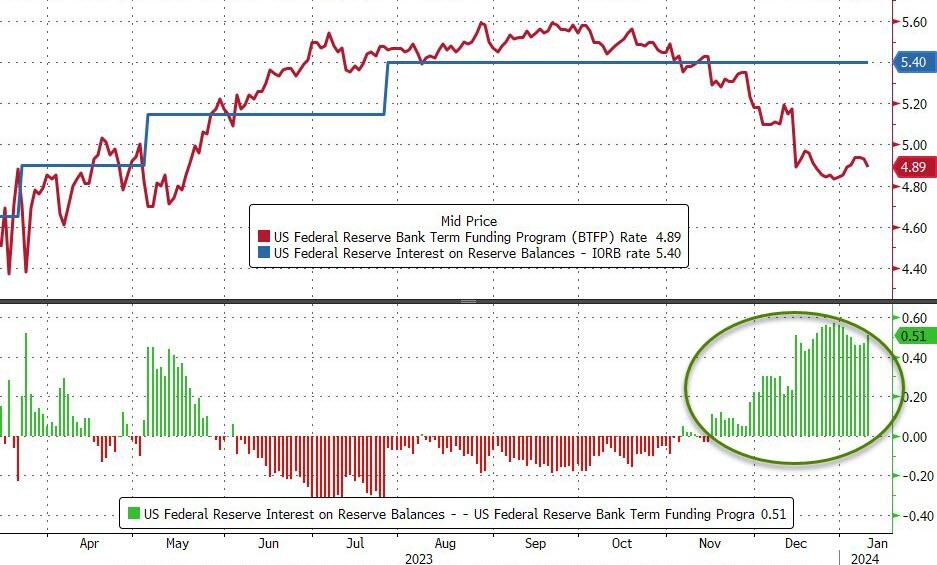

This time the rise in BTFP usage is good old-fashioned arbitrage. After the Fed’s pivot, term rates have come down relative to the policy rate. The cost to use the BTFP is 1y OIS + 10 bps, which is ~4.90%. Banks can post USTs at par as collateral, borrow at this rate, then deposit the funds back at the Fed at the IORB rate (interest on reserve balances), i.e. 5.40%, for a juicy risk-free profit.

This is not good optics, so it is unlikely the program will be renewed when it is due to expire on March 11. Michael Barr, the Fed’s vice chair for supervision, hinted as much on Tuesday when he emphasized the BTFP is an “emergency program.”

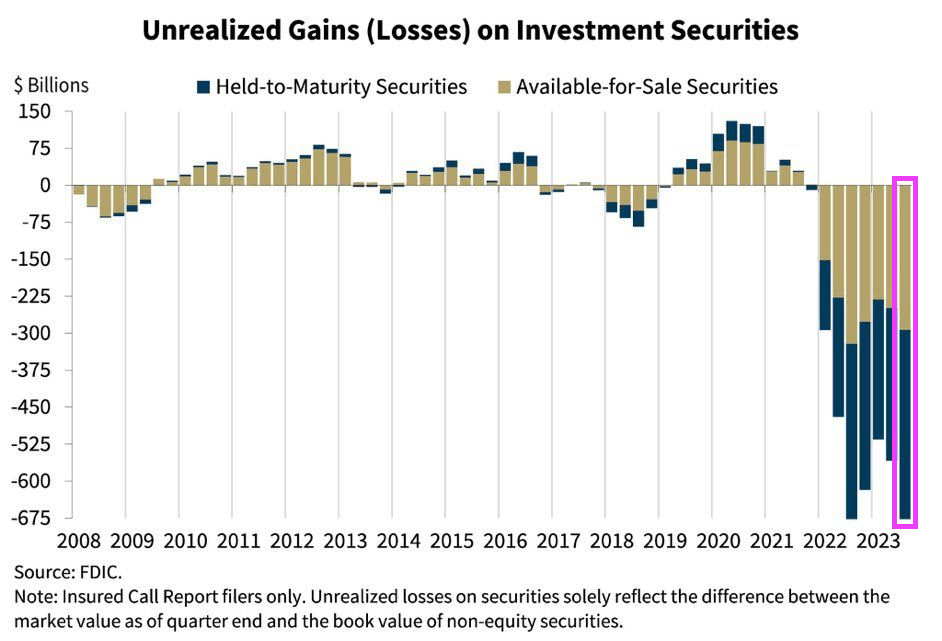

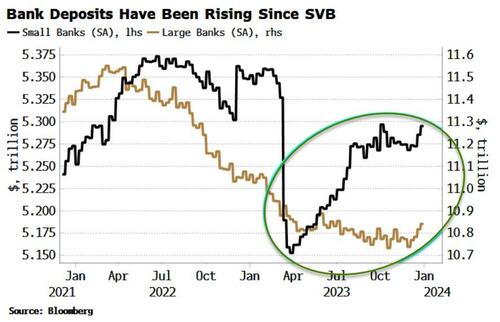

And it seems clear the emergency is over. Deposits of small banks (for whom the program was aimed at) have been rising since their drop after SVB’s collapse (both on a seasonally and non-seasonally adjusted basis). That, along with the quiescent fed funds market, suggests banks are not facing stress. Furthermore, the Fed’s pivot has also increased collateral values, making banks’ hold-to-maturity portfolios less underwater.

The BTFP’s expiry would mean another ongoing drain on reserves as the loans expire over the year.

With the Fed now seemingly focused on liquidity in this new paradigm, this adds to reasons why the central bank may cut earlier in the year.

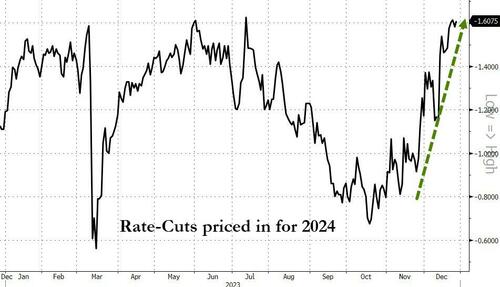

The market is currently pricing 17 bps of cuts for the March 20 meeting, so that’s not an attractive risk-reward, but at under ~7 bps or so that proposition changes – more so if the BTFP is no more.

Meanwhile, the futures market is forecasting rate cuts of over 200 basis points!

The Federal Reserve is a private enterprise that works with The Federal government like in the film “Prometheus” or “Chariots of the Clods.”

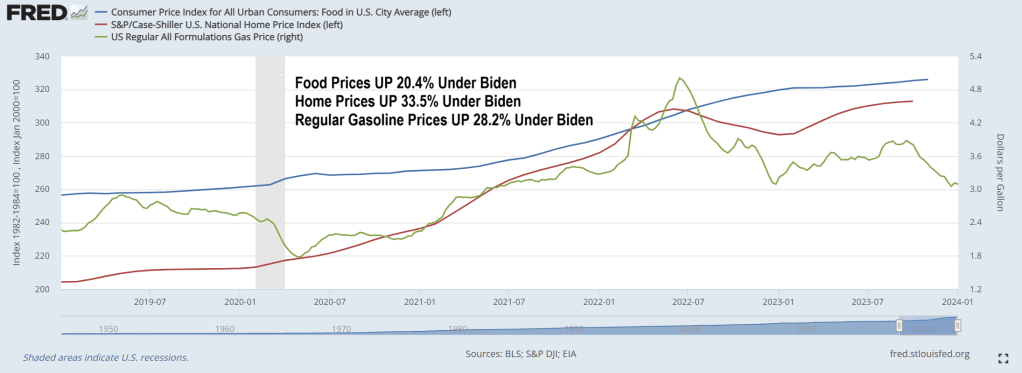

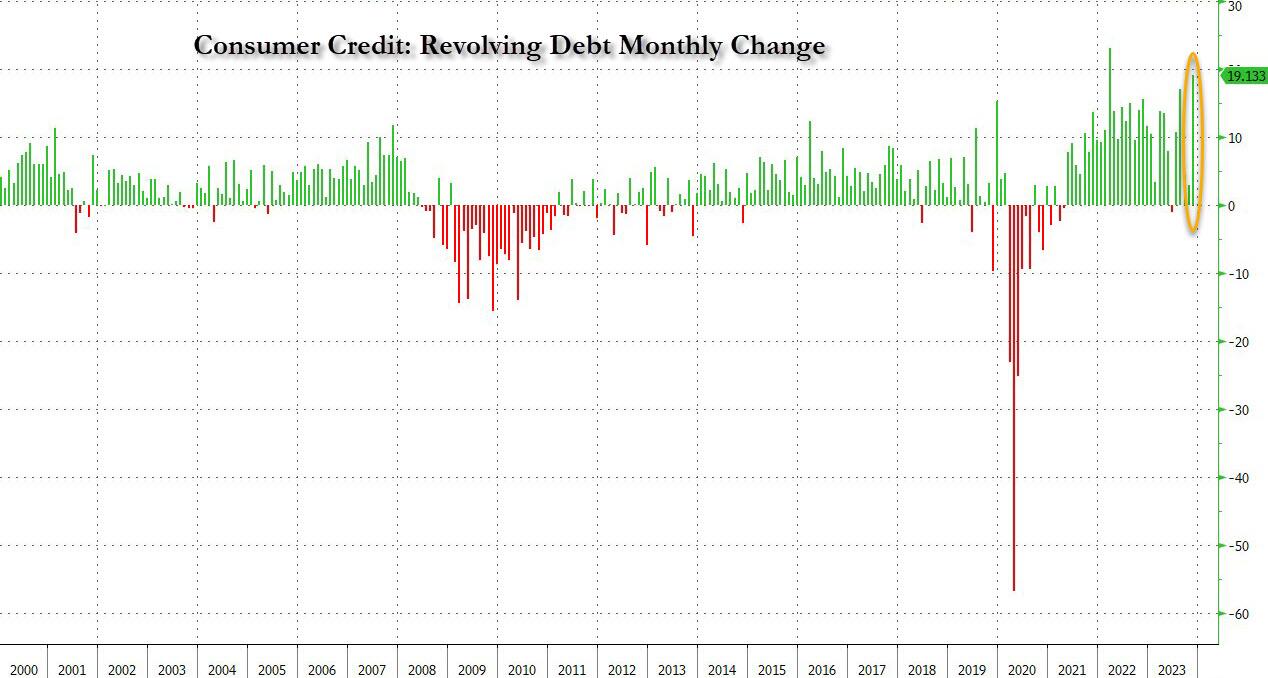

Bidenomics has taken the US economy to the underworld. Where households have to run up credit cards to ridiculous levels to cope with inflation under Bidenomics. Under Bidenomics, food prices are up 20.4%, home prices are up 33.5% and regular gasoline prices are up 28.2%. Whip out those credit cards!!!!!

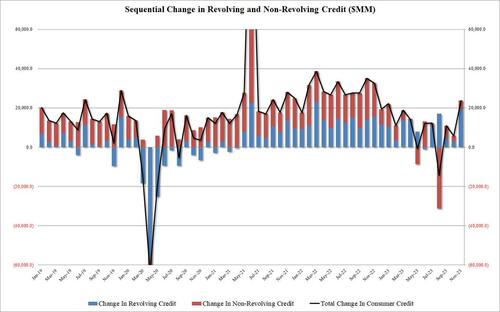

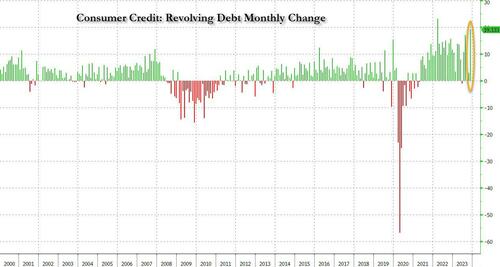

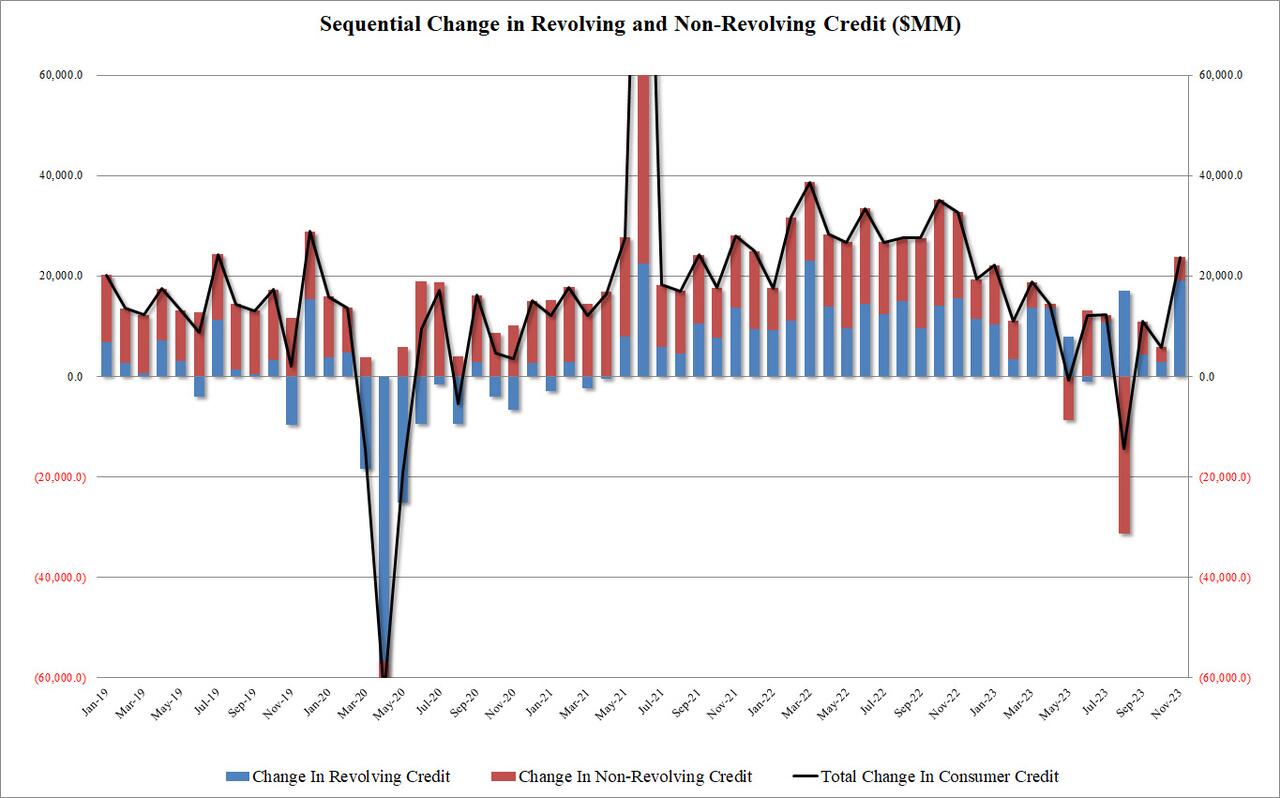

According to the latest monthly consumer credit report from the Fed, in November, consumer credit exploded higher by $24.75BN, blowing away expectations of a “modest” $9BN increase after the surprisingly subdued $5.8BN (upward revised from $.5.1BN) in October and the $4.3BN average of the past 6 months. This was the biggest monthly increase since last November, and was the first $20BN+ print since Jan 2023.

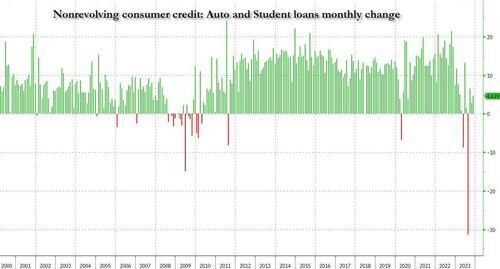

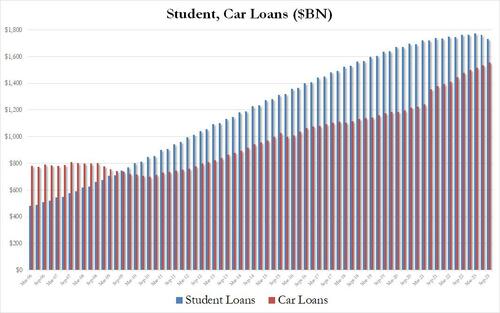

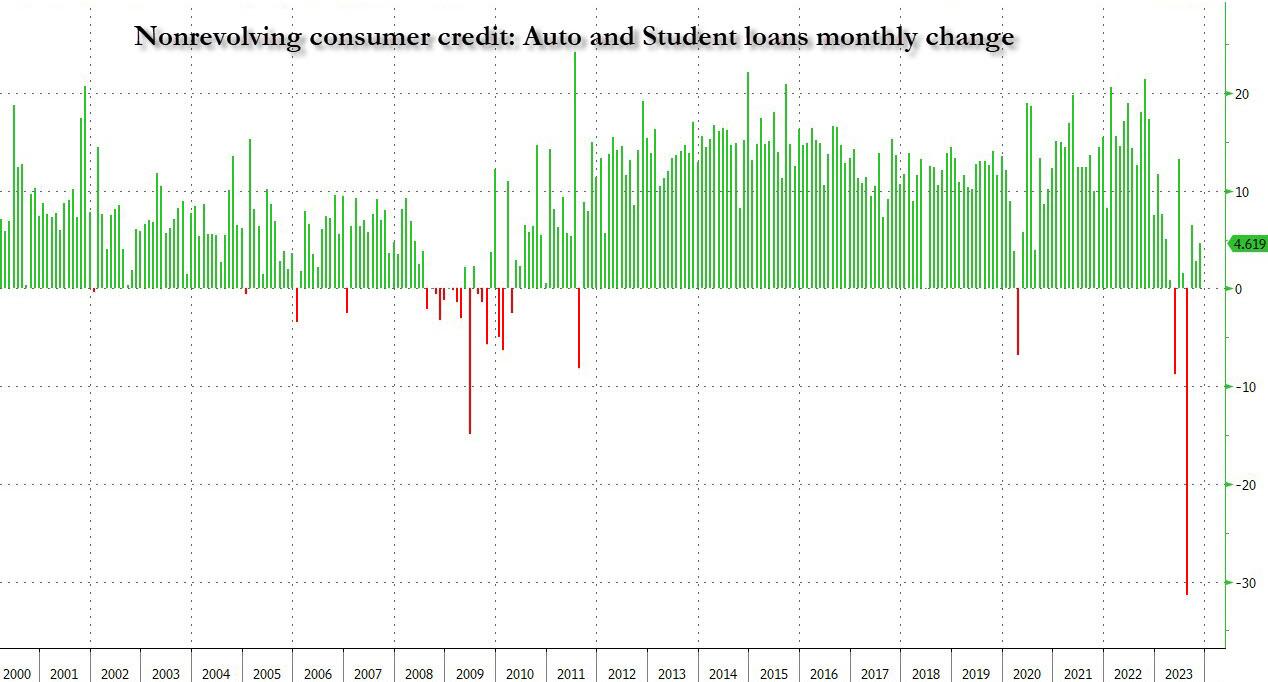

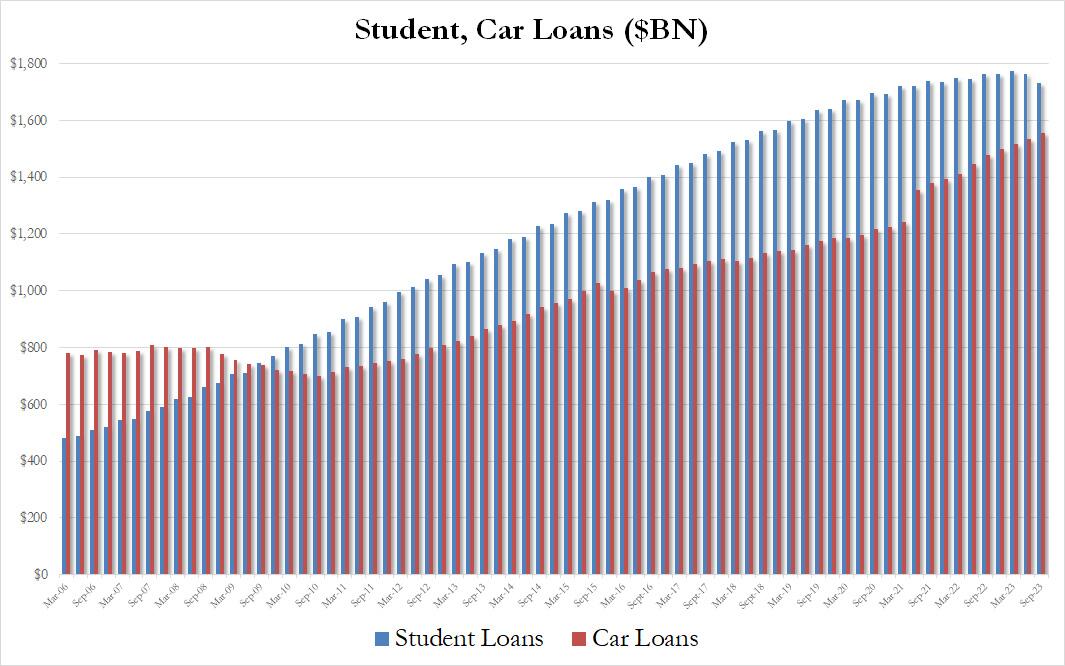

When looking into the details we find something remarkable: while non-revolving credit rose a modest $4.6BN…

… in keeping with the subdued increase in recent months as rates on auto loans make them prohibitive for most consumers while student loans are actually shrinking for the 2nd quarter in a row…

… what was the big shock in today’s data was the blowout surge in revolving credit, which in November exploded by a whopping $19.133BN, a record surge from the $2.9BN in October, and the second biggest monthly increase in credit card debt on record!

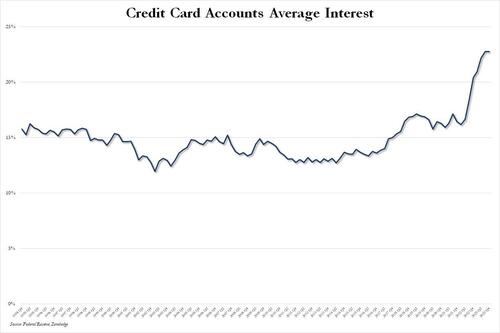

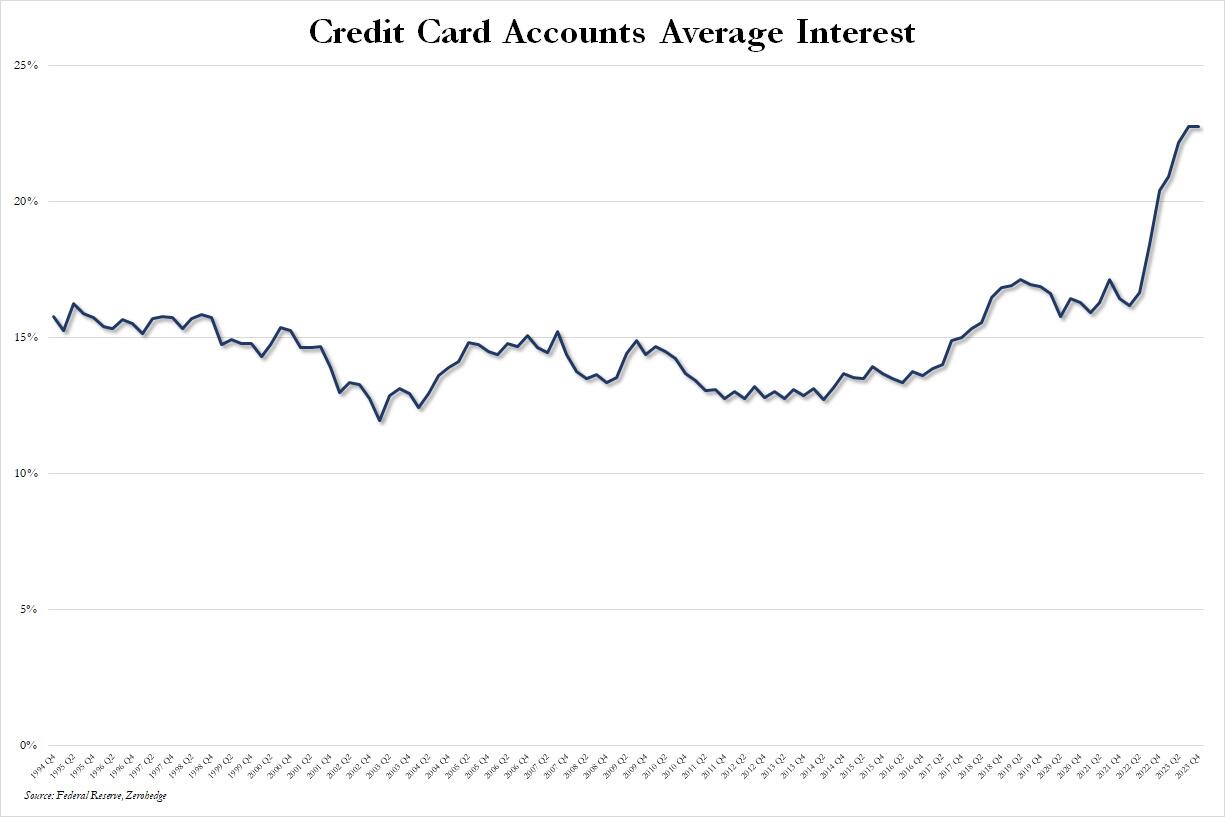

This, despite the average interest rate on credit card accounts in Q4 flat at a record high 22.75% for the second quarter in a row.

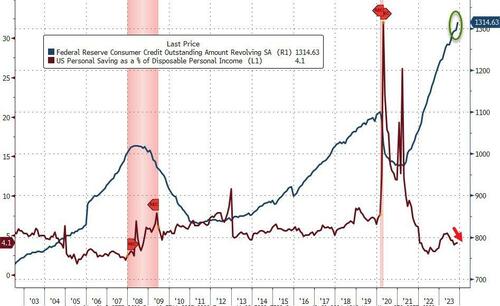

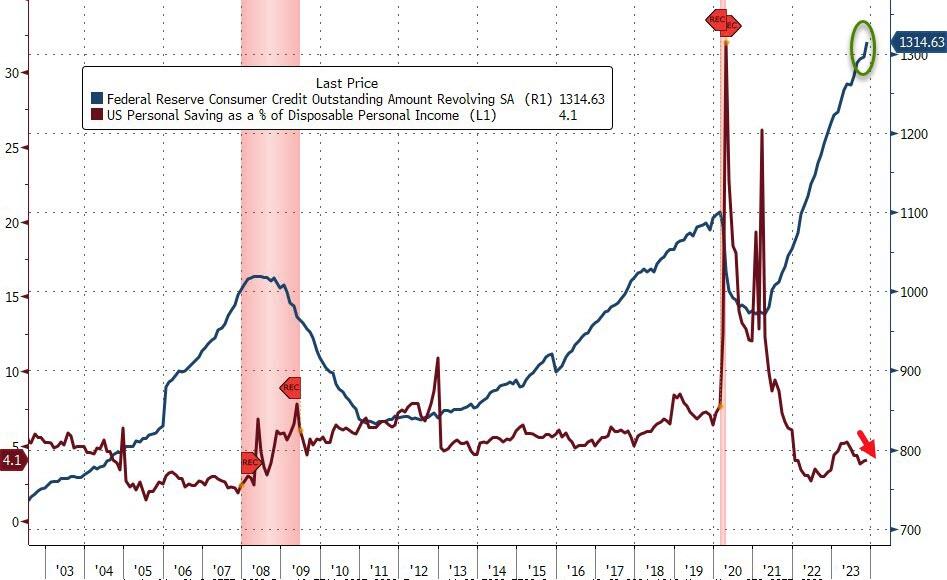

What is especially surprising about this conirmation that the bulk of holiday spending was on credit is that it takes place after several months of relative return to normaly, when consumers appeared increasingly reluctant to max out their credit cards due to record high rates, and at a time when the personal savings rate in the US has collapsed back near multi-decade lows in recent months.

Well, it now appears that Americans have once again done what they do so well: follow in the footsteps of their government and throw all caution to the wind, charging everything they can (and whatever they can’t put on installment plans which also hit a record late last year) including groceries, on their credit card, and praying for the best… or not even bothering to worry about what comes next.

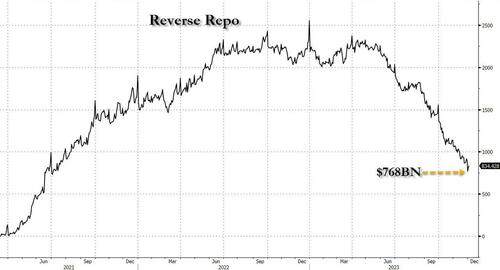

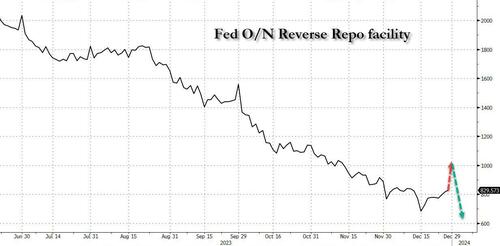

We didn’t have long to wait because just a few days later, on December 1 (just after the customary month-end window dressing period) when reverse repo tumbled to a fresh multi-year low of $765 billion…

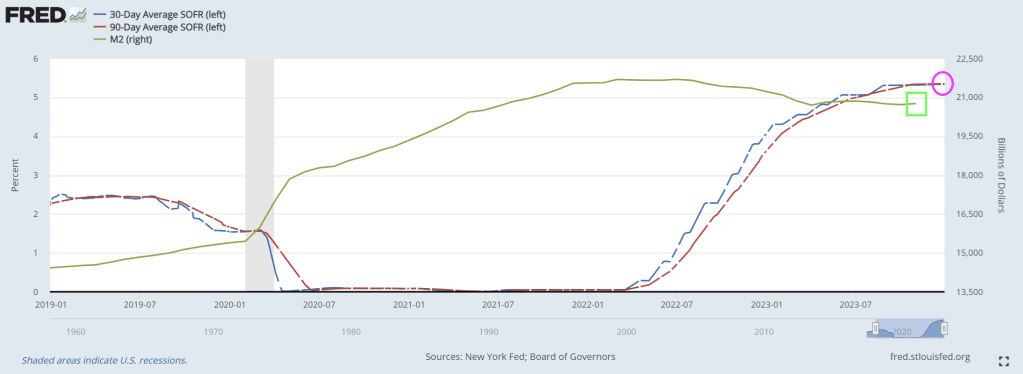

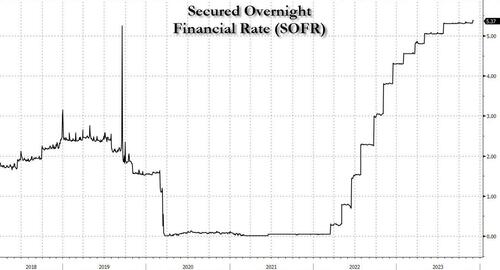

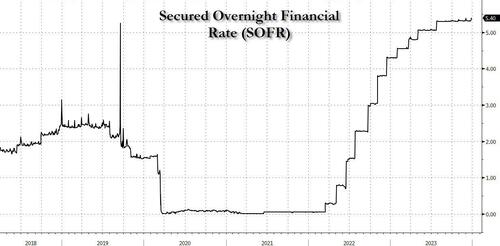

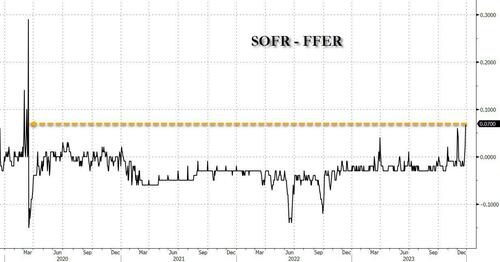

… things indeed broke as we explained in “Sudden Spike In SOFR Hints At Mounting Reserve Shortage, Early Restart Of QE” (in which we correctly previewed the coming Fed pivot at a time when most were still dead certain that Powell would only care about inflation for months to come): that’s when the the all-important SOFR rate (i.e., the new Libor) unexpectedly jumped 6bps to 5.39%, the highest on record…

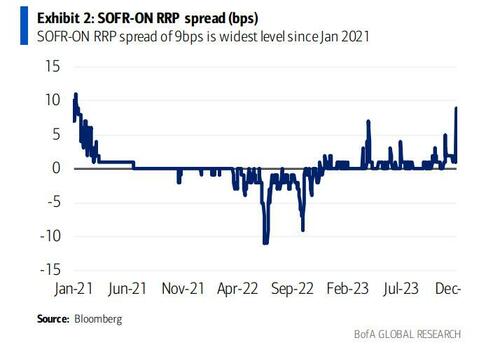

… also resulting in the largest SOFR spike vs ON RRP since Jan ’21, which hit 6bps.

The spike caught almost everyone by surprise, even such Fed-watching luminaries as BofA’s Marc Cabana because it was with “no new UST settlements, lower repo volumes, and lower sponsored bi-lateral volumes.” More ominously, and confirming our take from three weeks ago, Cabana warned at the time (full note here) that “the move is consistent with the slow theme of less cash & more collateral in the system” – i.e., growing reserve scarcity – and “may have been exacerbated by elevated dealer inventories, bi-lateral borrowing need, and limited excess cash to backstop repo. If funding pressure persists, it risks Fed re-assessment of ample banking system reserves & potential early end to QT.”

Then, the mini liquidity crisis disappeared almost as fast as it emerged, as SOFR rates eased off and the SOFR-Fed Funds spread normalized once GSE cash entered the market as it does every month….

… until today when not only did SOFR hit a new record high, ironically at a time when the market is pricing in more than 6 rate cuts in 2024…

… but the spread between the SOFR and the effective Fed Funds rate just spiked to the highest level since the March 2020 repo crisis…

.. with a similar move also observed in the spread between SOFR rate and the O/N Reverse Repo which similarly blew out to the widest since the start of 2021.

While there was no specific catalyst behind the sudden spike, two factors are the likely culprits: the year-end liquidity crunch, and the recent sharp increase in the Fed’s reverse repo facility, which has increased from a multi-year low of $683 billion on Dec 15 to yesterday’s $830 billion, and which STIR strategists expect will shoot up above $1 trillion in today’s final for 2023 reverse repo operation as a whopping $300+ billion in short-term liquidity in pulled from markets in just days.

That’s the bad news.

The good news is that come 2024 in a few hours, and specifically the first day of trading on Jan 2, we expect the reverse repo facility to plummet back to $700 billion once the year-end window dressing is over (especially with total US debt rising above $34 trillion to start the year), and floods the system with fresh liquidity which will stabilize the monetary plumbing at least until reverse repo dips below that key level of $700 billion at which point we expect the SOFR spikes to become a daily occurrence, and one which the Fed will no longer be able to ignore.

Indeed, one can already see traces of this in the repo market, where the rate on overnight GC repo first surged to 5.625% at the open on the final trading day of December before dropping to 5.45%, according to ICAP. It has since climbed back to 5.50%. But that’s still lower than where repo rates for Dec. 29 were trading during the prior session, as markets now start frontrunning the coming reverse repo liquidity flood.

Of course, once reverse repo eventually tumbles to $0 some time in March, all bets are off and the narrative shift to the next QE will begin.

“Say, can I sniff you if you take Trump off of Maine’s Presidential ballot??”

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.