REAL average hourly earnings growth remain in the toilet at -3.06% YoY.

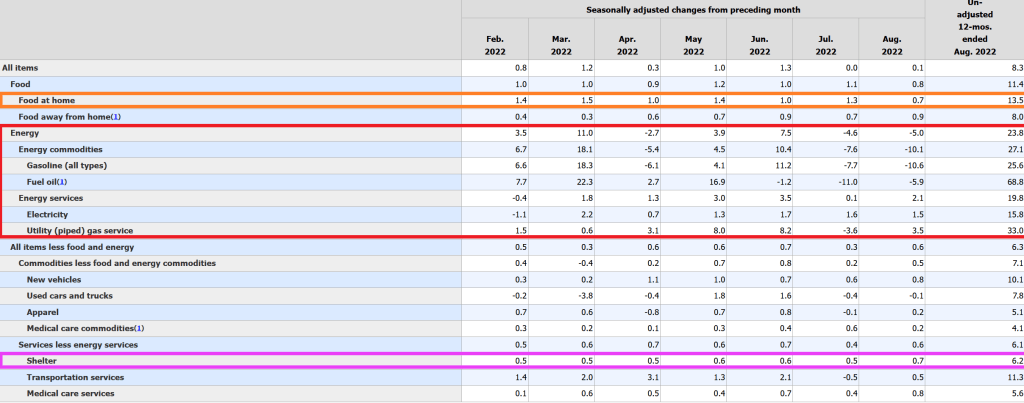

Fuel oil used to heat homes rose 68.8% YoY. Food at home rose 13.5% YoY while rent (shelter) rose “only” 6.2% YoY. Wow, renters are REALLY getting the short-end of the stick from The Fed and the Biden Administration!!

New vehicles are UP 10.1% YoY. Good luck buying those “cheap” electric cars that Mayor Pete Buttigieg trumpets! And wait for the bill when the battery needs to be replaced!!!

Joe Biden is the king of malaprops. But his press secretary is just as bad as her boss. Recently, she said that under Biden, there were 10,000 million jobs created. Better known as 10 BILLION jobs created. Not bad, considering that the total population of the US is 333 million. THAT is a hot labor market! /sarc

But seriously, the US U-3 unemployment rate is 3.7% in August, the lowest since Donald Trump was President and BEFORE the Covid outbreak. The Covid economic shutdown saw a surge in the unemployment rate to 14.7% in April 2020 that begat a huge spike in M2 Money growth (22% YoY in May 2022 (green line). Only now is M2 Money growth returning to Trump-era growth rates.

But as The Federal Reserve removes its hefty monetary stimulus, it is unlikely that the unemployment rate will remain low.

In defense of Biden’s press secretary, the US economy saw 10.247 million jobs added under Biden (although while technically correct, even MSNBC wouldn’t give Biden credit for job creation in his first several months as President. Check that. They probably would.

April 2020 saw a decline in US jobs of -20.493 million jobs thanks to the Covid economic shutdowns. BUT with the M2 Money surge, we saw +12.1 million jobs added between May and November 2020 under Trump. Then the US elected China Joe (or Beijing Biden) as President.

The economic shutdowns due to Covid were an economic disaster for millions. But the surge in M2 Money (supporting the various Federal spending programs and inflation) explains the surge in jobs added, not economic wizardry of Biden.

For some reason, Biden and his press secretary failed to mention that inflation is so bad that REAL average hourly earnings YoY are declining at a 3% pace.

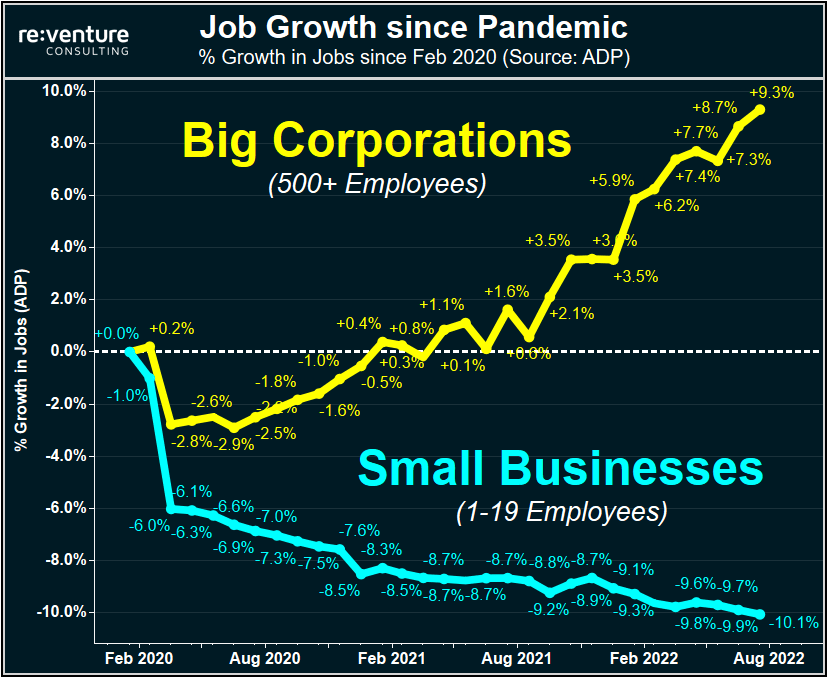

And not surprisingly, job growth has accrued to big corporations and not small businesses.

The Federal Reserve is facing an interesting problem. On the one hand, they vow to fight inflation by raising their target rate. At the same time, the probability of a recession in one year has grown to 50%.

Bankrate’s 30yr mortgage rate rose 31 basis points over the past week as 1) inflation probability increased and 2) Fed Funds Futures point to an O/N rate of 3.523% by the December FOMC meeting (up from 2.50% today). Growing recession probability typically results in Fed intervention and a lowering of rates while growing inflation typically results in Fed tightening. What’s The Fed to do??

Fed Funds Futures point to The Fed raising their target rate to 3.660 by March 2023, then loosening again.

Will The Fed consider that Public Debt grew from $7.84 trillion at the peak of the previous housing bubble in June 2005 to a whopping $30.7 trillion in August 2022? That is a 290% growth in Federal government debt since June 2005. With The Fed fighting inflation, the 2yr Treasury yield is smoking, making it more expensive to fund Federal government operations.

Real estate investment trusts (REITs) are an interesting asset class, allowing investors to purchase shares in large-ticket assets like multi-family properties or shopping centers. But given the changing landscape due to online shopping (aka, the Amazon effect), Covid economic shutdowns, etc., REITs should be having a hard time. But aren’t. How come?

Covid economic shutdowns definitely took its toll on retail shopping centers, as an example. And you can see the plunge in the NAREIT All equity index in early 2020. But the NAREIT All-equity index rallied … until The Federal Reserve started tightening their loose monetary policy. Note that as the implied O/N rate rose (orange line), REIT shares declined.

But as the WIRP implied O/N rate settled (pink box), the NAREIT index began to climb again. It is clear that REITs, like other equities, benefit from Fed easing. But how long will The Fed continue tightening?

As of this morning, The Federal Reserve is anticipated to raise their O/N rate to 3.738% by March 22, 2023. Then begin lowering their target rate … again.

Sadly, REITs, like other equity investments such as the S&P 500 index, are sensitive to The Fed’s easing/tightening. Look for REITs to struggle as The Fed tightens, then rally as The Fed eases again.

Here is the (in)famous Hindenburg Omen. Notice how the Hindenburg Omen alarm bells (yellow and red dots) have been silenced by The Fed. But as The Fed tightens (at least until March ’22), we may see the Hindenburg Omen flashing again. Call it the Powellburg Omen.

The NCREIF property index had a decline in the Covid-outbreak era (early 2020) and you can see a slight slowdown in the NCREIF index as The Fed started tightening to fight inflation.

Today’s US industrial production and capacity utilization numbers showed a nice “steady as she goes” slow decline from previous months, though still positive at 3.90% YoY.

And it is difficult to argue that the US is in a recession when capacity utilization is at 80.27%.

Notice that industrial production growth falls below 0% during a recession and capacity utilization slumps. We are NOT there … yet.

However, M2 Money growth is shrinking awfully fast.

While the US is technically in default (two consecutive quarters of negative GDP growth), it doesn’t FEEL like a recession with 3.90% YoY industrial production growth and capacity utilization above 80%. During the Covid recession in early 2020, industrial production growth YoY had declined to -17.65% and capacity utilization shrank to 64.53%.

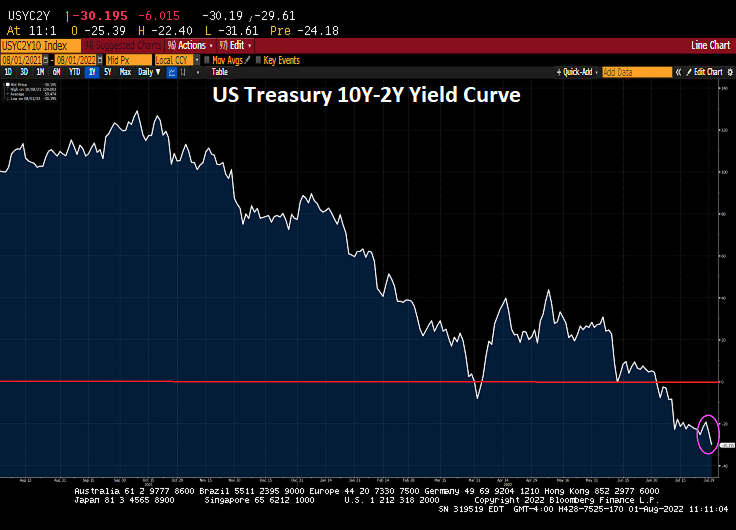

Speaking of a recession SIGNAL, the 10Y-2Y Treasury yield curve is SCREAMING impending recession.

The 2020 Covid outbreak led to a massive (and generally awful) reaction. There were economic shutdowns that caused extensive damage (particularly to small firms), but it was the massive overreaction by The Federal government in terms of Covid relief and The Federal Reserve’s expansion of the money supply that caused considerable damage.

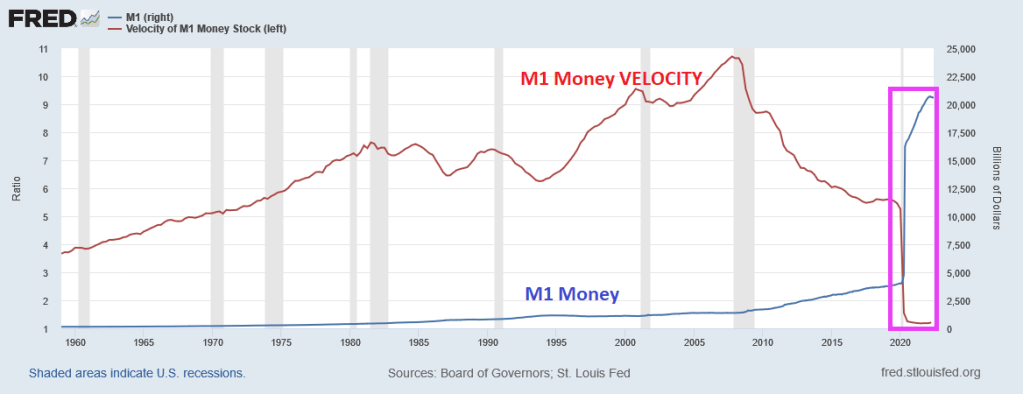

One truly horrific chart is that of M1 Money and M1 Money Velocity (M1/GDP). M1 Money surged with Covid driving M1 Money Velocity down to levels never seem before.

The broader measure of money, M2, isn’t as dramatic, but we also see that M2 Money VELOCITY has plunged to levels never seen before.

What does low money velocity indicate? Simply put, The Fed is printing trillions of dollars, but GDP isn’t moving much. But that won’t stop Congress from spending (and using The Fed to buy its debt).

So, here we sit. This morning, the US Treasury yield curve (10Y-2Y) remains inverted. This AM, the curve inverted another -.591 basis points to -42.725, a sign of impending recession.

Yes, we are living through Jay Powell’s famous chili episode where money velocity is near historic lows and we have an inverted yield curve.

BTW, congratulations to Will Zalatoris (aka, Happy Gilmore’s caddy) for his first PGA Tour victory at the FedEx St. Jude Championship!

Federal Reserve Bank of St. Louis President James Bullard said he favors a strategy of “front-loading” big interest-rate hikes, and repeated he wants to end the year at 3.75% to 4% to counter the hottest inflation in four decades.

“We still have some ways to go here to get to restrictive monetary policy,” Bullard said in a CNBC interview Tuesday.

“I’ve argued now with the hotter inflation numbers in the spring, we should get to 3.75% to 4% this year. Exactly whether you want to do that at a particular meeting or some other meeting is a great question. I’ve liked front-loading. I think it enhances our inflation-fighting credentials.”

Federal Reserve presidents including Bullard speaking this week emphasized that inflation at a 40-year high has yet to slow, and pushed back against the perception the central bank was pivoting to a less aggressive phase of tightening monetary policy. Fed Chair Jerome Powell last week cited Federal Open Market Committee forecasts that the Fed would raise rates to 3.4% at the end of the year and 3.8% in 2023.

Bullard wants to raise rates to boost Fed credibility?? When flexible price inflation is at 20.13% and The Fed is awfully slow to shrink their balance sheet??? What credibility is he talking about????

We are seeing a slowing of the US economy. For example, the JOLTs (job openings) numbers are out for June and they are down -5.5% from May. And from April to May, JOLTs declined -3.2% MoM. That is a clear slowing trend.

And on the housing front, the CoreLogic HPI Forecast indicates that home prices will increase on a month-over-month basis by 0.6% from June 2022 to July 2022 and on a year-over-year basis by 4.3% from June 2022 to June 2023. But rose +18.3% YoY in June. Also a clear cooling trend.

And its “Escape From Blue States” (perhaps a new Kurt Russell movie), with home prices rising fastest in red states (primarily The South). And contiguous migration from California to Nevada and Arizona.

The Fed Funds Futures market is pricing in rate hikes until the March 2023 FOMC meetings. After all, Prince Imhotep (aka, Minneapolis Fed’s Neel Kashkari) is screaming for more rate hikes to fight inflation … caused by 1) loose monetary policies since late 2008 and 2) insane Federal government spending.

Let’s see if “Mr. Freeze” (aka, Jerome Powell) relents on Fed rate increases before the March 2023 FOMC meeting.

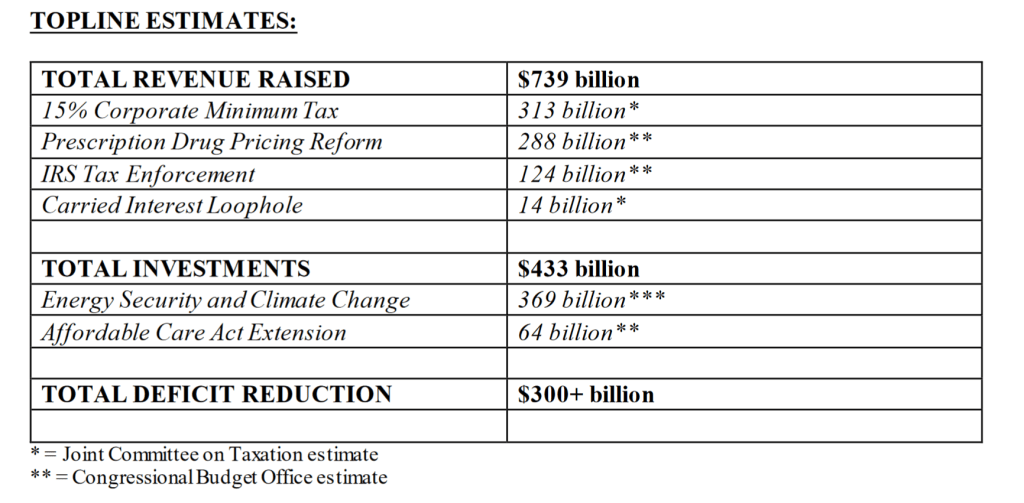

The spendiholics in Washington DC (aka, Biden and Congress) have passed yet another inflationary legislation, this time the sadly misnamed “The Inflation Reduction Act” since it will likely lead to a furthering recession of the US economy. Well, that is one way to reduce inflation: cause a recession and job loss.

An analysis by the National Association of Manufacturers says the tax in 2023 alone will reduce real GDP by $68.5 billion and cut labor income by $17.1 billion. One well-known economic truth is that corporations don’t really pay taxes (they pass on taxes to consumers in the form of higher prices). They are essentially tax collectors, as the corporate tax rate ultimately falls on some combination of workers, shareholders and customers. Raise the corporate tax rate, and you’re cutting wages and salaries for workers.

“Americans are already experiencing the consequences of Democrats’ reckless economic policies. The mislabeled ‘Inflation Reduction Act’ will do nothing to bring the economy out of stagnation and recession, but it will raise billions of dollars in taxes on Americans making less than $400,000,” said Sen. Mike Crapo, an Idaho Republican who sits on the Senate Finance Committee as a ranking member, and who requested the analysis.

“The more this bill is analyzed by impartial experts, the more we can see Democrats are trying to sell the American people a bill of goods,” Crapo added.

According to Schumer and Manchin, “The Inflation Reduction Act of 2022 will make a historic down payment on deficit reduction to fight inflation, invest in domestic (green) energy production and manufacturing, and reduce carbon emissions by roughly 40 percent by 2030. The bill will also finally allow Medicare to negotiate for prescription drug prices and extend the expanded Affordable Care Act program for three years, through 2025.”

No wonder House Speaker Nancy Pelosi took her extensive entourage on a paid vacation to Singapore, Malaysia and perhaps Taiwan. Its called “Getting out of Dodge.” If Pelosi believed in this legislation, she could have “saved the environment” by simply doing a Zoom call. Then again, Biden’s Climate Envoy, John Kerry, still travels the globe trying to sell green energy and carbon reductions in his private carbon-spewing jet. But I forget, Biden, Pelosi, Schumer and Kerry are our elites who deserve platinum treatment, not lowly serfs like 99% of the US population.

So, here we go loop-de-loop. Politicians want to spend money on their friends and donors and then raise taxes on the rest of us.

On the recession front, the 10Y-2Y US Treasury yield curve just flattened another -6.015 basis points to an inverted -30.195 basis points.

You must be logged in to post a comment.