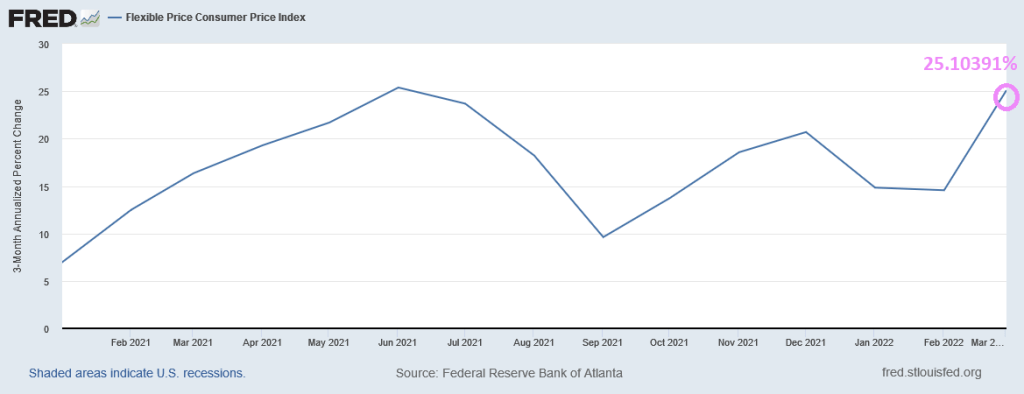

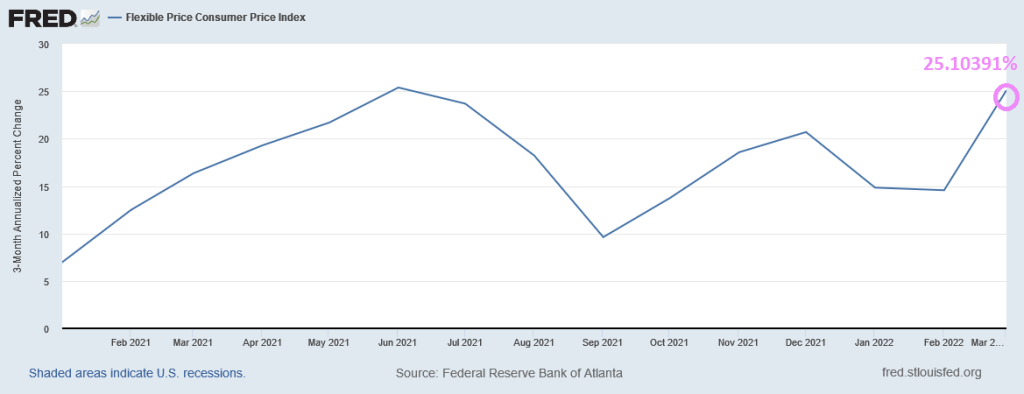

While headline inflation is growing at 8.6% YoY in March, flexible price inflation grew at a terrifying 25% YoY rate.

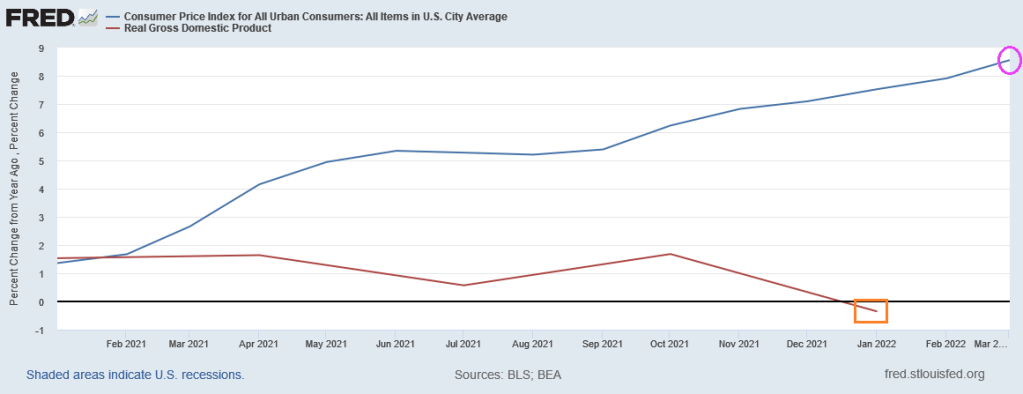

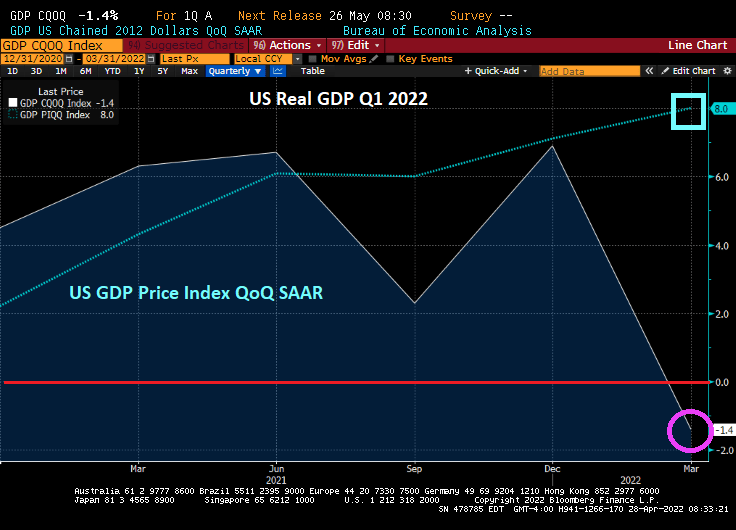

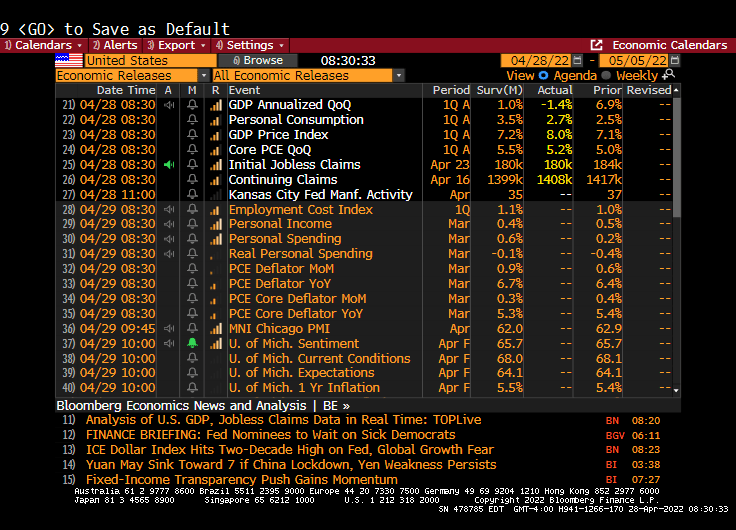

Even with headline inflation of “only” 8.56% YoY, today’s Q1 real GDP growth checked in at -1.4% QoQ. Clearly, Bidenflation isn’t help the economy or anyone else.

Diesel prices have skyrocketed under Biden.

Instead of Shoeless Joe, we have Clueless Joe as President.

I hope America’s foreign policy wizards (Biden, Harris and Blinken) weren’t relying on the Russian Ruble staying pulverized, because the Ruble (relative to King Dollar) has regained all its losses.

On the other hand, the Japanese Yen and Chinese Yuan have crashed harder than Biden’s popularity.

Actually, The Atlanta Fed’s flexible price inflation rate is 25%, up from 3.90% Pre-Joe.

Perhaps Biden, Harris and Blinken think Putin is a pasta sauce.

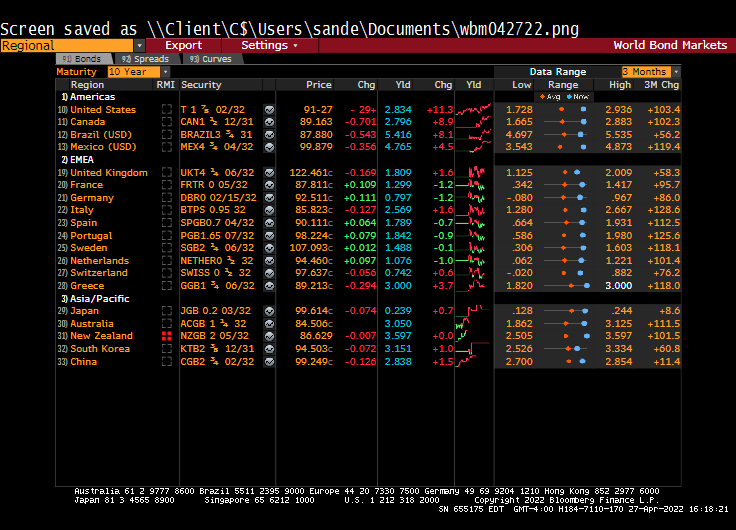

Particularly if you are a pension fund and hold US Treasuries and Agency Mortgage Backed Securities.

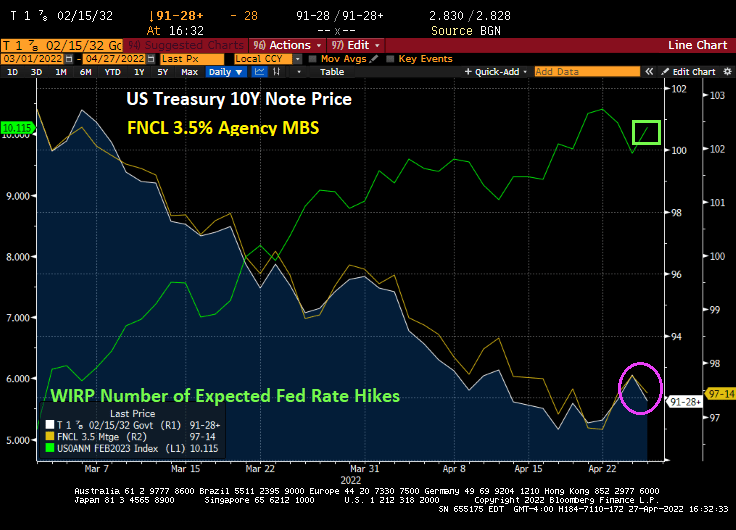

The bad news is that the 10-year US Treasury Note declined in price, sending the yield up over 10 bps today.

As The Fed is projected to raise its target rate over 10 times by February 2023, 10-year Treasury Note prices and agency MBS 3.5% prices continue to decline.

Heartaches in heartaches. US GDP growth for Q2 has stumbled to 0.446% as The Fed is launching quantitative tightening (QT) to fight the inflation that they caused in the first place.

According to the Atlanta Fed’s GDPNow real-time GDP tracker, US GDP growth has stumbled to a meager 0.446%. Despite the massive stimulus from The Federal Reserve and Washington DC’s massive fiscal stimulus.

Here is Dvorak’s New World Symphony, an appropriate piece the global turmoil that has taken place after Russia’s invasion of Ukraine.

Here is the ratio of the S&P 500 index against the Bloomberg Commodity Price Index. This ratio is plotted against The Federal Reserve’s balance sheet of assets. Notice the decline in the Commodity Ratio in 2022, even ahead of the Russian invasion of Ukraine.

Global currencies, on the other hand, have been really crushed since the Russian invasion of Ukraine. The Japanese Yen, China’s Renminbi and Europe’s Euro relative to the US Dollar are falling due to a variety of reasons. Covid lockdown in China, Japan’s insistence on monetary easing while other Central Banks are tightening and the Euro with Russia threatening nuclear war.

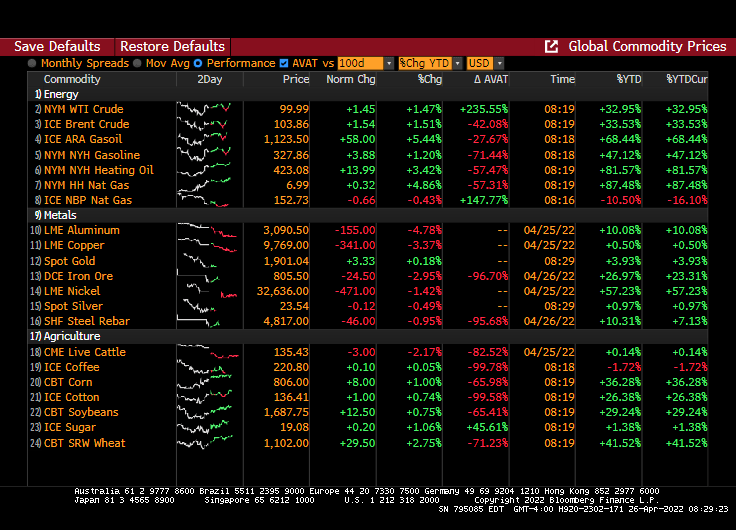

WTI Crude is back to $100 a barrel. Critical metals are down today related to a slowing global economy and wheat is up 2.75%.

Could it be that US Dollar hegemony is nearly over and commodity-backed currencies are the way of the future?

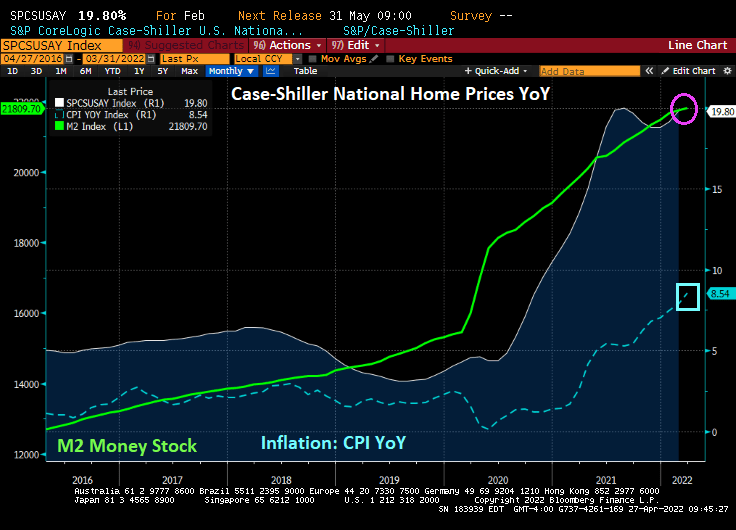

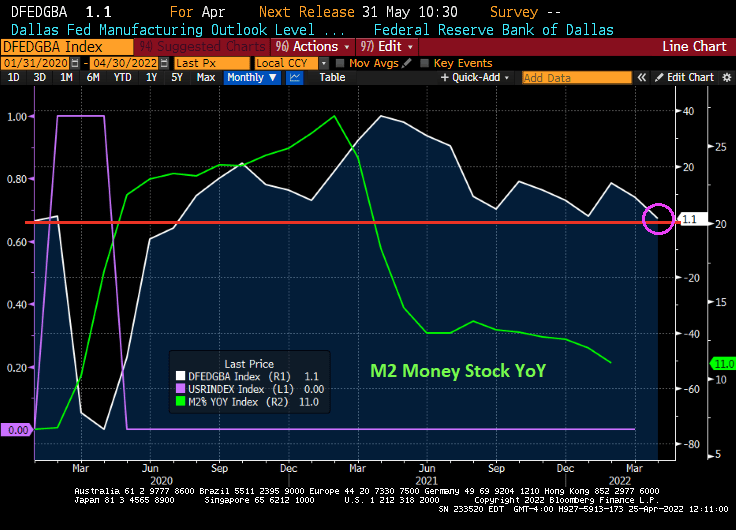

M2 Money stock YoY skyrocketed during the Covid mini-recession, peaking at 21% during February of 2021. The Dallas Fed manufacturing outlook grew to 38.1 in March 2021.

However, as M2 Money growth has slowed 11%, the Dallas Fed manufacturing outlook has plunged to near zero.

Its Saturday and I am dreading markets opening on Monday. But here is where we sit today.

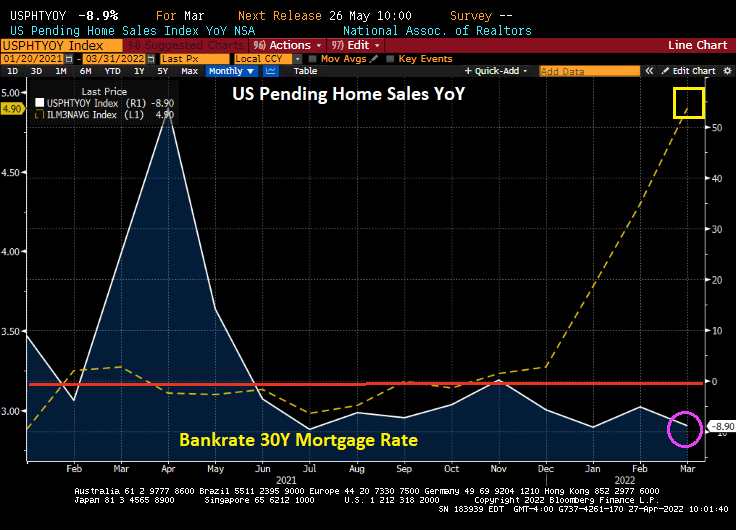

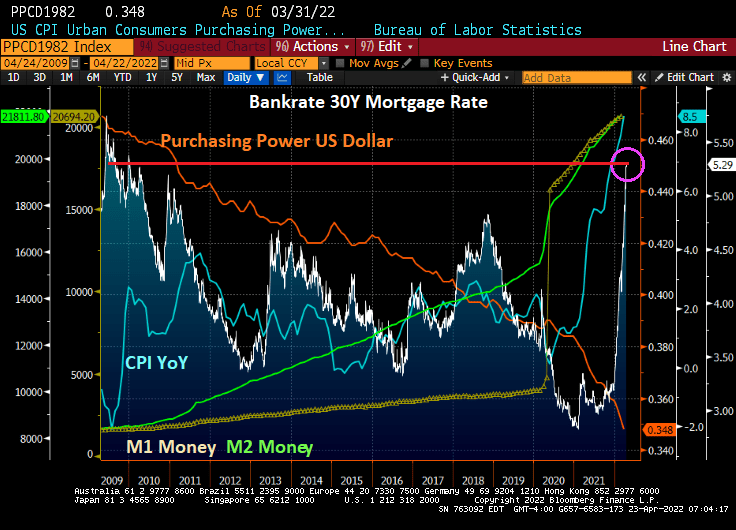

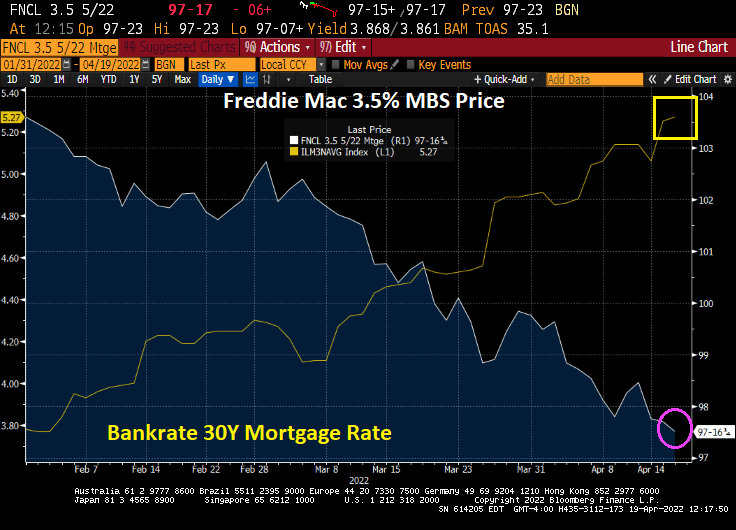

The 30-year mortgage rate has soared to 5.29%, the highest level since 2009 at the beginning of Obama’s Presidency. Since 2009, we have seen the purchasing power of the US Dollar decline further (orange line) while inflation (blue line) has soared. M1 (yellow) and M2 (green) has been growing since the financial crisis, but really took-off with the Covid outbreak in 2020 and The Fed’s massive overreaction coupled with Federal government stimulus.

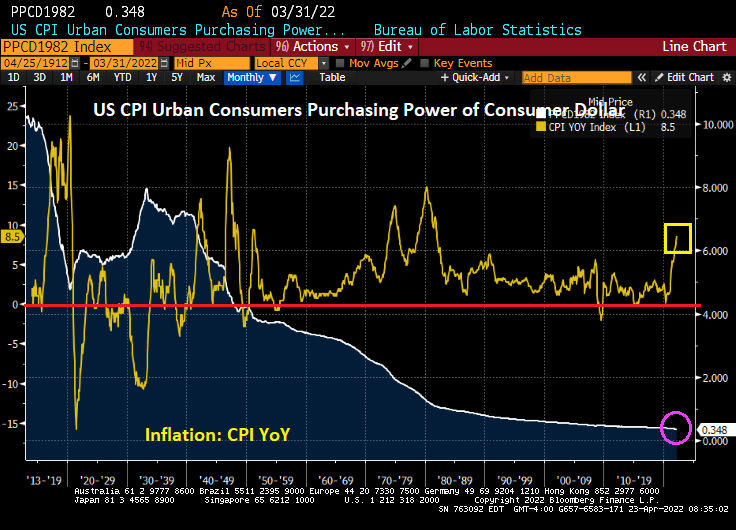

Since the creation of The Federal Reserve System under President Woodrow Wilson, the purchasing power of the US Dollar has collapsed so much that $10 in 1913 in worth 34.8 cents today. But notice that since 1949, the CPI YoY has rarely been negative meaning that prices are pretty much only going up.

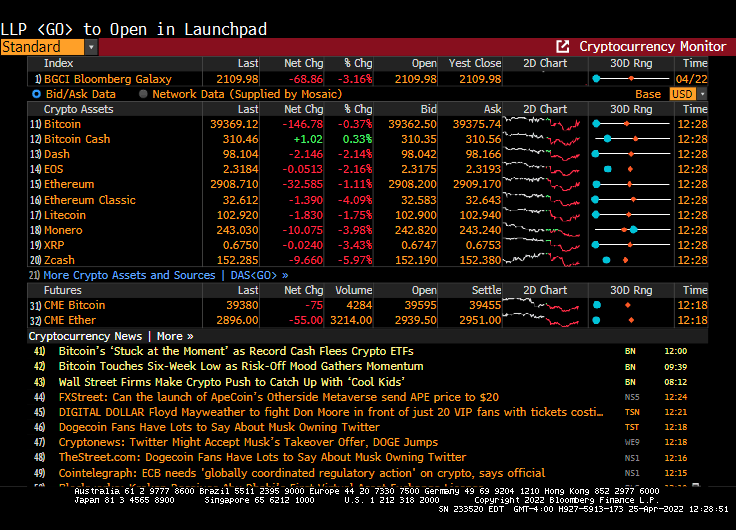

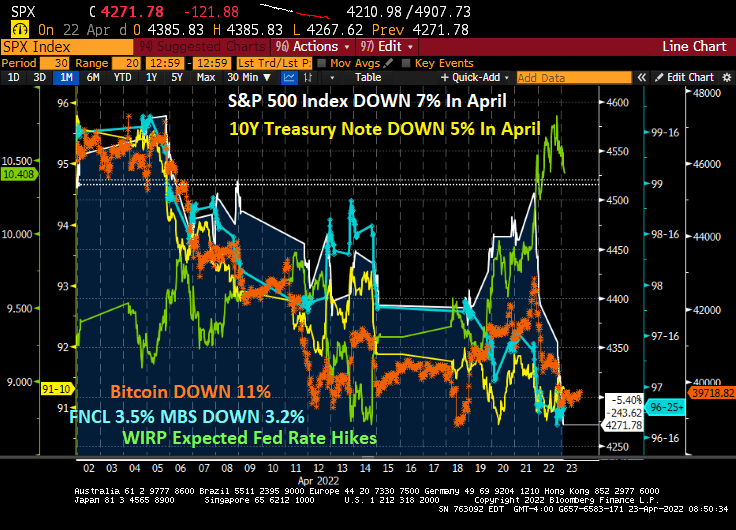

Instead of April showers bring May flowers, it is April expected Fed rate hikes (now 10.408 rate hikes by February 2023) bringing declining assets prices. In April so far, the S&P 500 index is DOWN 7%, the 10-year Treasury Note price is DOWN 5%, Bitcoin is DOWN 11%, the 3.5 coupon agency MBS price is down 3.2%.

We are seeing increased volatility in both the equity and bond markets.

Well, Powell and The Fed are hurling fireballs at mortgage rates and asset prices in April.

People Get Ready! For The Federal Reserve to actually withdraw its massive stimulus.

I generally discuss that negative impact of rising mortgage rates on the housing market, but today I am focusing on the decline in agency mortgage-backed security prices due to rising mortgage rates.

Here is the uniform MBS price for a 3.5% coupon security. It is falling like a rock with anticipated Fed monetary tightening.

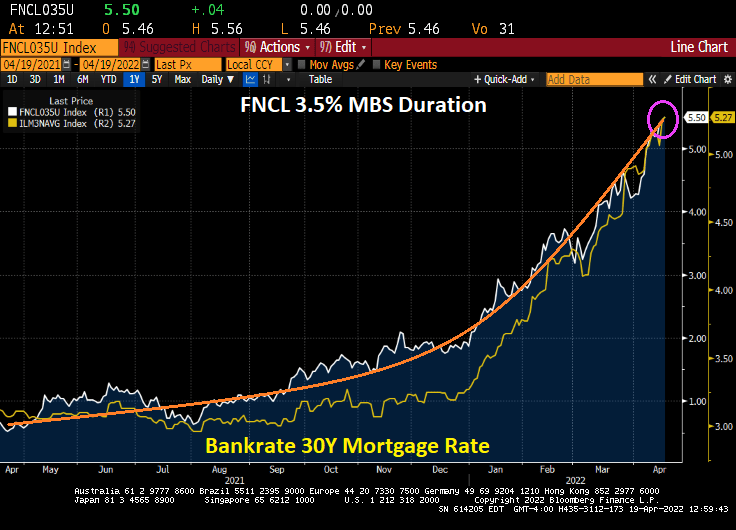

And duration risk is going to the moon! (That is, accelerating rapidly).

FNCL 3.5 coupon MBS has a WAC of 4.206 and a WAM (or WARM) of 359. Not to mention a factor 0.997.

At least energy prices are cooling thanks to China grinding to a halt with the latest Covid epidemic.

I wish The Fed would back off its allegedly ambitious tightening and soothe me.

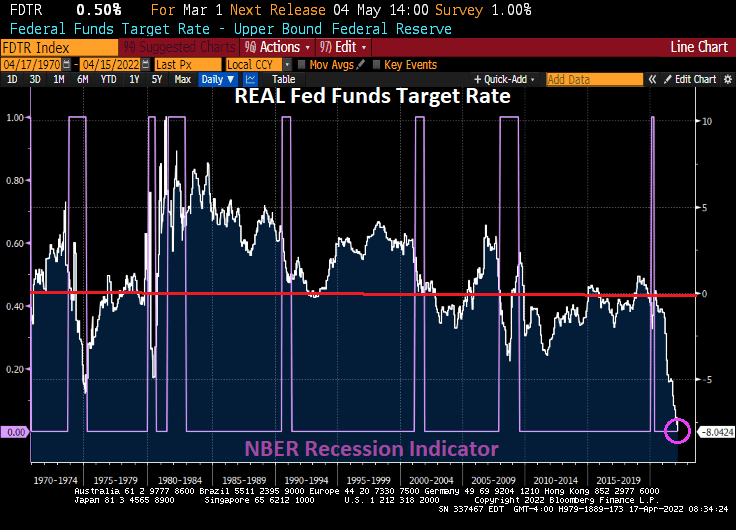

As inflation crushes the middle class and low wage workers, we see that the REAL Fed Funds Target Rate (based on headline inflation) is the lowest in history. Notice that the REAL Fed Funds Target Rate tends to hit its lowest negative reading DURING recessions, although The Fed has had a poor track record since the Dot.com bubble burst and the 2001 recession meaning that the REAL Fed Funds Target rate has been in negative territory (that is, the rate of inflation has exceeded The Fed Funds Target Rate for much of the post-2000 era).

The “good” news? Inflation caused by The Fed’s negative interest rate policy (NIRP?) has actually led to REAL home price growth to slow 11.6855% YoY, lower than the peak of the 2005-2007 house price bubble.

With The Fed’s OVERSTIMULATION of markets with historically low REAL Fed Funds Target Rate, we can see that the US unemployment rate is overheated (that is, below the Congressional Budget Office (CBO) Short-term Natural Rate of Unemployment. Yes, it appears that Slow Walking Fed Chair Jay Powell should be raising The Fed’s target rate AND removing (at least) the Covid monetary stimulus.

Inflation Joe is a career politician, so it is not surprising that he is trying to blame Russia for the horrid inflation in the US. However, inflation grew from 1.4% when Biden took office to 7.9% when Russia invaded Ukraine. The latest inflation report was 8.5%, so Russia is only partly to blame for rising prices since February 24, 2022. The rest is due to Inflation Joe, Slow Walking Jay and Congress.

Again, Congress helped drive prices through the roof by massive Federal spending (aka, Covid stimulus “relief”). Hence, the Four Horsemen of the Inflation Apocalypse is appropriate. And now Biden is once again pitching massive government spending (Build Inflation Back Better?).

You must be logged in to post a comment.