We got trouble in Potomac City! No, I’m not talking about the numerous Top Secret documents that Biden carelessly left in his garage in Delaware and the UPenn Biden Center. And they found more over the weekend. I’m talking about the US Treasury 10Y-2Y yield curve being inverted for 135 straight days. And thanks to inflation, REAL wage growth has been negative for 21 straight months.

All this is happening while M2 Money growth (green line) stalls to 0% YoY.

Swaps 5Y are rising as The Fed withdraws monetary stimulus.

The 2020 Covid outbreak and the resulting government shutdowns and school closures begat a Washington DC spending spree and Federal Reserve monetary stimulus barrage unlike anything other time in history. Congress and Administrations love to spend other people’s money, but as Rahm Emanuel once said “You never let a serious crisis go to waste. And what I mean by that it’s an opportunity to do things you think you could not do before” And wow, did they ever binge spend and expand the M2 Money supply. I call it “The Great Dislocation” of the economy and we never recovered from it.

But after the massive spending splurges and Fed monetary stimultypto, The Fed finally started withdrawing “the punch bowl” to combat inflation. M2 Money growth year-over-year (YoY) is now 0%. And with inflation, US average weekly earnings growth YoY turned negativc and has been negative for 21 straight months.

After the spending explosion under Pelosi/Schumer and Powell’s monetary, M2 Money velocity (GDP/M2 Money) crashed to it lowest level in history. So now we have depressed money velocity and no M2 money growth. And the US still has 21 straight months of negative weekly earnings growth.

But former Fed Chair and current Secretary of Treasury Janet Yellen is pleased that inflation is FINALLY slowing which Yellen attributes to relaxing supply chains. Or is it declining M2 Money growth, Janet?

Now that the Federal government’s spending spree and The Fed’s monetary stimulypto dislocated the US economy, we are headed for a recession with no ammunition left in The Fed’s arsenal.

After all. The Federal Reserve has been destroying consumer purchasing power since 1913. And we may be at the end of The Fed’s monetary rope.

Even worse, we have Joe Biden as President, who curiously has been found to have classified documents in his possession from when he was Vice President, at least, at two locations (his Wilmington DL home that his son Hunter had access to and the now infamous Penn Biden Center in Washington DC). Even worse, Biden seems to be talking to dead world leaders like Germany’s Schmidt and France’s Mitterand.

Knowing Biden’s penchant for blatant lying and carelessness, I wouldn’t be surprised if this is a stack of classified documents on the table during his meeting with Treasury Secretary Janet Yellen.

Let’s hope Biden isn’t saying that he is talking to late Robert Kennedy, the former US Attorney General.

Its that time again when Congress does its Kabuki Theater drama about raising the US debt limit. Of course, everyone in Congress and the Biden Administration want to spend trillions of dollars so they will hike the debt limit.

With the US government facing the danger of a payments default later this year, Congress has a variety of paths to avert economic disaster and boost the debt ceiling.

All of them would likely involve going right up to the market-rattling brink, according to current and former lawmakers and aides.

The timeline kicks off within weeks, when Treasury Secretary Janet Yellen is expected to advise that the government will deploy extraordinary accounting measures to avoid running out of cash. Those steps are forecast to be exhausted after July.

Republicans now in control of the House are demanding deep spending cuts as the price for an increase in the ceiling, while President Joe Biden and congressional Democrats reject such an outcome.

Nothing has been the same since the financial crisis of 2008 and the ascension of all-time big spender Nancy Pelosi as House Speaker. Budget deficits have never been the same. The last budget surplus was under House Speaker Newt Gingrich. But since the financial crisis of 2008, Federal spending seems to have increased its trajectory.

Note that mandatory spending (Medicare, Social Security, etc) is growing like a wild fire while discretionary spending is seemingly flat. So, it mandatory spending that Congress will pretend to cut.

Yes, it is Medicare for our aging population that has blown out of control.

Then we have defense spending. The Ukraine spending should come from this pot, but forces decisions to make between Ukraine and taking care of our Navy (to compete with the growing Chinese navy).

Of course, as The Fed fights inflation, we are seeing the COST of Federal debt soaring since Covid.

Yes, Congress NEEDS to cut back the spending, particularly on Social Security and Medicare (not to mention Ukraine spending), but it is all Kabuki theater. Queue the screams of “Republicans will take away …”.

I wish everyone in Congress were like Kentucky U.S. Senator Rand Paul, not the other spendaholic Kentucky Senator.

The Federal Reserve will be the backstop of the Treasury market this year to alleviate dysfunction resulting from its increasing size and the retreat of regular buyers.

That’s the view of Credit Suisse Group AG analyst Zoltan Pozsar, who in a note to clients Friday predicted the Fed will restart asset purchases during the summer of 2023.

In Pozsar’s analysis, relative-value funds won’t buy Treasuries unless they cheapen a lot relative to overnight index swaps, and banks with sagging reserves are more likely to tap the funding markets than to buy Treasuries. FX-hedged buyers have been “priced out,” and geopolitical events have reduced large reserve managers’ appetite for US debt, he said.

Flagging demand from marginal buyers will depress demand for Treasury auctions, sparking selloffs in equities, credit and emerging markets, according to Pozsar.

“This is a ‘checkmate-like’ situation,” he wrote. “The Fed won’t be a pivot and the terminal rate may have to go higher still, neither of which augurs well for either risk assets or Treasuries.”

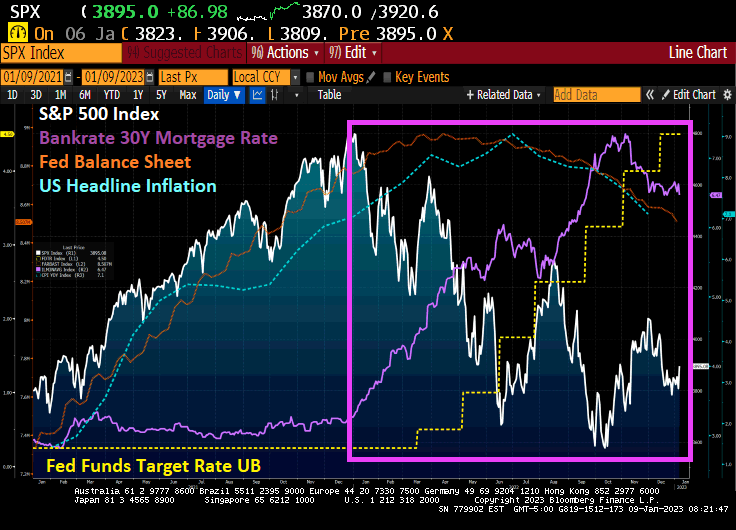

As The Fed started to raise rates (yellow line) to fight inflation (blue dashed line), the S&P 500 index started to fall. Note that The Fed’s balance sheet (purple line) is mirroring the inflation rate.

Fed Funds Futures point to Zoltan’s reversal in June 2023.

Will The Fed pivot? Zoltan says yes, the talking Fed heads say no.

US headline inflation began to soar as soon as Joe Biden became President. A combination of massive stimulus spending related to the Covid economic shutdown and his war on fossil fuels, driving up gasoline and diesel fuel prices. In other words, headline inflation rose from 1.4% Year-over-year (YoY) at the end of December 2020 to 9.1% YoY in June 2021. It has now simmered down to 7.1% YoY as The Fed continues to remove monetary stimulus.

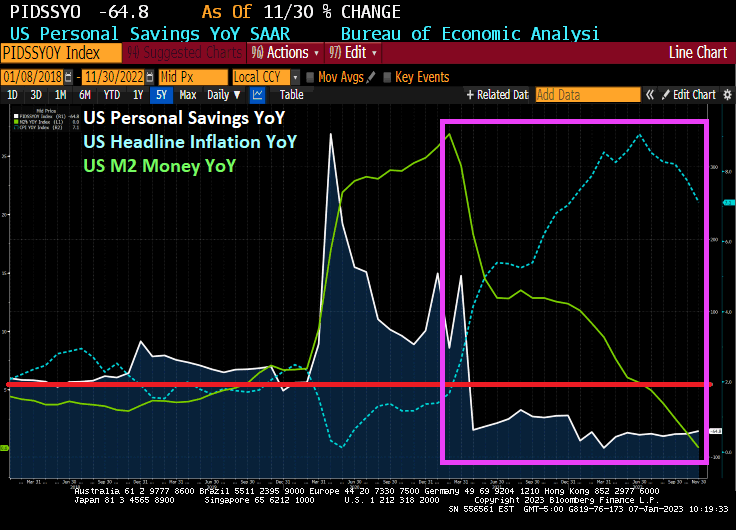

How have consumers coped with inflation caused by massive Federal spending and Biden’s anti-fossil fuel policies? In November, personal savings dropped -64.8% YoY. This marks 20 straight months of declining personal savings.

US M2 Money growth YoY is now … 0%. That is the lowest in US history.

Today is all quiet of the financial market front since the US stock

Today is all quiet of the financial market front since the US stock and bond markets are closed. But as the new year starts, we have to ask the following question: is the US already in a recession?

A simple measure of IMPENDING recession is the US yield curve which is currently inverted. Typically, a recession occurs within months of the yield curve inverting. But if we look at real GDP growth, the Atlanta Fed GDP tracker is at 3.7%, so no recession there (two consecutive quarters of negative GDP growth is often used as a measure of recession).

But another indicator of “all is not well” is the CBOE Put/Call Ratio. Typically, the Put/Call Ratio spikes during a recession. But on December 28, 2022, the Put/Call Ratio spiked to its highest level since 1996. Although it has calmed down to 0.84 on December 30, 2022. Suffice it to say that there is enormous uncertainty in markets.

Covid begat massive Fed monetary stimulus and an excuse for the Federal government to go on a series of spending sprees (Covid “relief”, Instrastructure, Inflation Reduction, and now the $1.7 Trillion pork-laden Omnibus bill). Now that historic big spender Nancy Pelosi (CA-D) is no longer Speaker, will her successor have such a voracious spending appetite? The US economy is still benefitting from Covid-related stimulus which also helped generate 40-year highs in inflation.

Thanks to inflation, US workers have had 20 consecutive months of negative wage growth. But as M2 Money growth slows to a halt, so will real average hourly earnings.

The traditional measures of recession (unemployment and Real GDP growth) are NOT pointing to recession, but 20 straight months of negative wage growth points to bad news for workers. Throw in an inverted yield curve and massive volatility in the CBOE Put-Call Ratio and we have a party … that I don’t want to attend.

A simple measure of IMPENDING recession is the US yield curve which is currently inverted. Typically, a recession occurs within months of the yield curve inverting. But if we look at real GDP growth, the Atlanta Fed GDP tracker is at 3.7%, so no recession there (two consecutive quarters of negative GDP growth is often used as a measure of recession).

But another indicator of “all is not well” is the CBOE Put/Call Ratio. Typically, the Put/Call Ratio spikes during a recession. But on December 28, 2022, the Put/Call Ratio spiked to its highest level since 1996. Although it has calmed down to 0.84 on December 30, 2022. Suffice it to say that there is enormous uncertainty in markets.

Covid begat massive Fed monetary stimulus and an excuse for the Federal government to go on a series of spending sprees (Covid “relief”, Instrastructure, Inflation Reduction, and now the $1.7 Trillion pork-laden Omnibus bill). Now that historic big spender Nancy Pelosi (CA-D) is no longer Speaker, will her successor have such a voracious spending appetite? The US economy is still benefitting from Covid-related stimulus which also helped generate 40-year highs in inflation.

Thanks to inflation, US workers have had 20 consecutive months of negative wage growth. But as M2 Money growth slows to a halt, so will real average hourly earnings.

The traditional measures of recession (unemployment and Real GDP growth) are NOT pointing to recession, but 20 straight months of negative wage growth points to bad news for workers. Throw in an inverted yield curve and massive volatility in the CBOE Put-Call Ratio and we have a party … that I don’t want to attend.

US existing home sales in November collapsed by -38.6% YoY as M2 Money growth runs out of gas.

The above chart is similar to yesterday’s “Ski Slope” chart of US home prices YoY.

Unfortunately, pending home sales YoY are the worst in recorded history.

What will President Biden do about this dire situation? Our “Vacationer in Chief” is off on yet another vacation to St. Croix in the US Virgin Islands, so probably nothing. Now that Biden is sunbathing, what will his Treasury Secretary Janet Yellen do?

A classic good news, bad news story. The good news? US new home sales rose 5.8% in November, better that the expected -5.1%, The bad news? On a year-over-year basis, US new home sales FELL

Sales of new US homes unexpectedly rose in November, suggesting some stabilization in demand as mortgage rates eased late in the month from their highs.

Purchases of new single-family homes increased 5.8% to an annualized 640,000 pace last month after rising in October, government data showed Friday.

A mid-month retreat in 30-year mortgage rates back below 7% along with an increase in builder incentives may have helped support demand. Still, the sales data are volatile from month to month. With home prices remaining elevated and the Federal Reserve poised to raise interest rates further, headwinds for the housing market will persist into 2023.

The increase in sales last month was concentrated in the West and Midwest.

The report, produced by the Census Bureau and the Department of Housing and Urban Development, showed the median sales price of a new home was up 9.5% from a year earlier to $471,200.

There were 461,000 new homes for sale as of the end of last month, though the grand majority remain under construction or not yet started. The number of homes sold in November and awaiting the start of construction — a measure of backlogs — rose to the highest since the beginning of the year.

But for all the cheerleading, new home sales were DOWN -15.3% on a year-over-year basis. The ninth straight month of negative new home sales growth.

At least the median price of new home sales was down -2.79% from October to November.

Do I detect a trend in the US Leading Economic Indicator data?

The Conference Board’s US Leading Economic Indicator was released this morning and it wasn’t pleasant. The US Leading Index was down -1% MoM in November.

On a year-over-year basis, it is down -4.5% YoY as The Fed withdraws its massive monetary stimulus.

The good news … for military contractors … is that Biden and Congress have given Ukraine’s Zelenskyy ANOTHER $47 BILLION.

The highest interest rates in 15 years are delaying home dreams, putting business plans on ice and forcing many Americans to agree to loan terms that would have been unimaginable just nine months ago. Biden’s anti-fossil fuel policies are helping drive up prices and The Federal Reserve is hiking rates to cool it off.

Most of all, the surge in borrowing costs is punishing the cash-poor. And it’s about to get worse as the Federal Reserve carries on with its anti-inflation campaign and keeps hiking rates next year.

As the Fed’s most aggressive interest-rate hike cycle in a generation filters through the US economy, the gap is widening between the haves and the have-nots. Even without a recession, households and businesses are feeling the financial pain.

Here’s a look at pockets of the economy that are bearing the brunt of the impact.

Housing in Holding Pattern

Manda Waits from Suwanee, Georgia, feels lucky that she and her husband bought their townhouse near Atlanta a year ago with a 3% loan — less than half of where mortgage rates are now.

To trim expenses amid soaring consumer prices, the couple recently bought a freezer and stocked it with a quarter cow and half a pig sourced from an agricultural school. But they shelved their plan to upgrade to a single-family home for the time being.

“We would like to buy some land to build on, but these rates aren’t making it attractive, so we are in a holding pattern,” said Waits, who receives disability benefits.

Even in the once red-hot market of Tampa, Florida, a few people showing up at an open house is now considered a good day. “People are just waiting on the sidelines,” said Rae Anna Conforti, a realtor with Re/Max Alliance Group.

As mortgage rates hit their highest levels since 2001 this year, real estate agents suddenly found themselves hunting for clients again — if not losing their jobs. Thousands of mortgage employees have already been laid off at lenders including Wells Fargo & Co. and JPMorgan Chase & Co.

The higher rates, coupled with a surge in home values during the pandemic, pushed the monthly mortgage payment on a median-priced house to more than $2,000, up from about $1,100 just before Covid-19 hit.

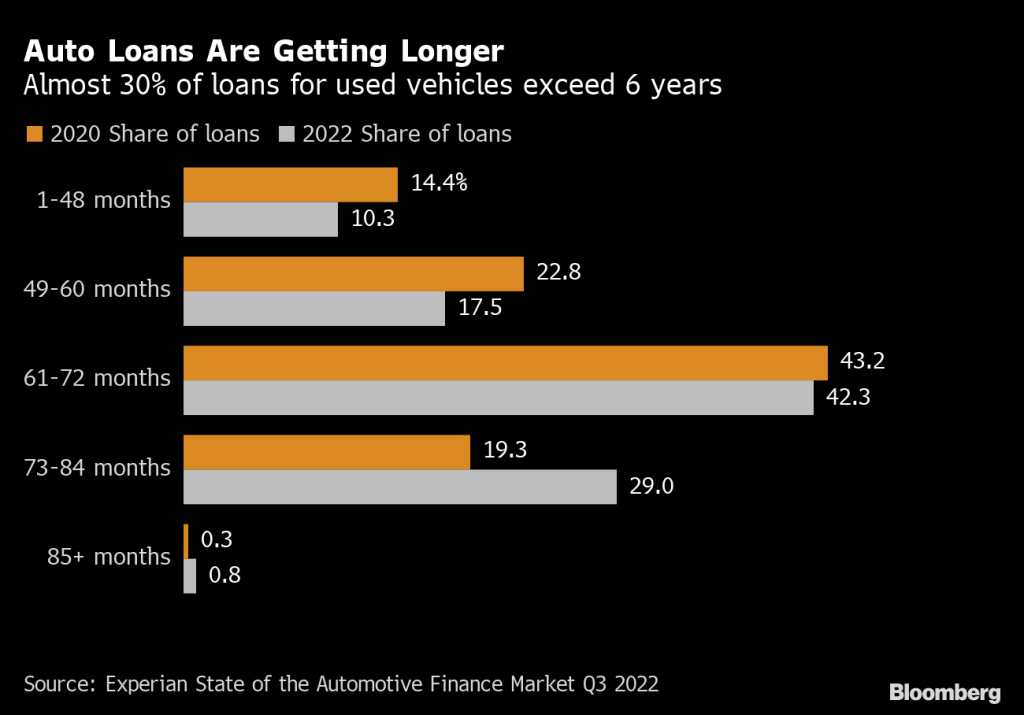

‘Vicious Circle’ The widening gap between the cash-rich and the cash-strapped is playing out at car dealerships across the nation. The former are paying more upfront, while the latter are stuck with high-rate auto loans that will leave them underwater — or forced to settle for cheaper and less reliable vehicles.

Almost one in three car buyers are now taking out six- to seven-year loans on used vehicles to help lower monthly payments.

When consumers are locked for so long, the outstanding balance quickly exceeds a used car’s value, said Oren Weintraub, whose California-based service helps consumers negotiate better prices with dealers for a fee. When they buy their next car, that balance will get tacked onto to the new loan.

“It’s a vicious cycle,” he said.

Matt Tambornini was hoping to take out a car loan to build his credit history. The 22-year-old, who lives near Knoxville, Tennessee, with his parents, figured he’d be in a position to buy a house when mortgage rates eventually come down.

His plan stumbled when a local car dealership offered a 23% loan rate and a 60-month term, a deal that would’ve had him paying thousands more than he wanted. He bought the car anyway, quickly got buyer’s remorse and returned it for a refund.

For now, he’s driving a 15-year-old pick-up he bought with cash.

“It seems like everything is just unaffordable,” Tambornini said.

Soaring Credit Debt Interest rates on credit cards that averaged 16.3% at the beginning of the year have climbed to just over 19%, according to Bankrate.com, the highest level in data going back to 1985.

That’s a massive increase especially for lower-income consumers, who may be making the minimum payment and carrying a balance for 20 years, said Scott Sanborn, chief executive officer of LendingClub Corp.

“I don’t think consumers have fully internalized yet how much their cost of living has actually increased,” Sanborn said.

The surge in APRs to historical highs isn’t affecting consumers the same way. It makes no difference to those who pay off their balances monthly — many don’t even notice the rate increases — but it’s hitting those who are falling behind.

Mike Lauretti, 24, has about $12,000 in debt on four cards, as well as car, student and private debt. The high school social worker, who lives near Hartford, Connecticut, is working on paying off the card with the smallest amount first before moving to the next — known as the snowball method. He also took an extra job as a coach of the girls basketball team to supplement his income.

“I am using the snowball method to pay off the cards first and then it’ll eventually lead to me paying the private loan,” the largest, he said.

American consumers will end the year with about $110 billion more in credit-card debt than they started with, which would be close to an annual record, according to WalletHub, an online personal finance data firm. The reality may hit next year, when many economists predict the US will enter a recession. Household debt delinquencies are still well below their end of 2019 levels, but they’re picking up.

“We expect delinquencies to continue to increase, with new credit-card and auto delinquencies reaching pre-pandemic levels in the first half of next year,” Moody’s Investors Service said in a report.

Small Businesses

In Dayton, Ohio, Clara Osterhage would love to add to her 82 Great Clips hair salons and she knows people who are looking to sell.

“But I can’t put myself in a place to buy them, because the interest rates on any money that we would borrow would be astronomical,” she said.

Matt Haller, chief executive of the International Franchise Association, said high loan rates will keep smaller buyers of franchises out of the market, while bigger companies with more access to capital consolidate.

Meantime, some would-be buyers are demanding that sellers help finance the deal, said Dustin Zeher of Horizon Business Brokers in Virginia.

“We’re talking about 50% to 80% of the transaction, because they are cognizant and aware of the rising interest rates and how that has effectively reduced their buying power and has increased the cost of the transaction,” Zeher said.

Greg Vojnovic, owner of a small fast-food chain in the Youngstown, Ohio area, said the debt service — or debt payments — on his Small Business Administration loan has risen by $70,000 annually, and he expects it to climb at least another $15,000 as the Fed continues to raise rates. He’ll have to cut two part-time corporate-office positions to lower costs.

“If bacon goes up, people understand if you raise prices,” said Vojnovic, owner of the Hot Dog Shoppe. “If chicken goes up, people understand that. If debt service goes up, you just kind of have to eat that.”

Here is Joe Biden, shooting the hopes of millions of Americans in the tuchus.

You must be logged in to post a comment.