The Federal Reserve forecast for the US economy is a dismal 0.50% YoY. Do I detect a trend?

The FOMC forecast for 2023 and 2024. Core PCE YoY (inflation) is forecast to drop to 3.50%, still considerably higher than The Fed’s target rate of inflation of 2%. And unemployment is forecast to be 4.60%.

To cope with Bidenflation, US personal savings rate as of October is -67.9% YoY. The “good” news is that rents YoY are crashing. But food prices under Inflation Joe remain very high. But most everything is slowing down, not due to Biden’s policies, but a global and US economic slowdown.

With a big slowdown coming our way, you can understand why The Fed’s December Dot Plot is showing declining Fed Funds Target rate starts declining in 2024.

Even US mortgage rates are headed down.

Speaking of going down, cryptos are down across the board with Cardano leading the decline at -6.91%.

Years ago, Brent Ambrose, Michael Lacour-Little and I wrote a paper on the US 30-year jumbo mortgage spread over conforming 30-year mortgage rates entitled “The effect of conforming loan status on mortgage yield spreads: a loan level analysis.” But that paper was written before Covid and the dramatic distortion caused in mortgage markets by The Federal Reserve’s massive increase in money.

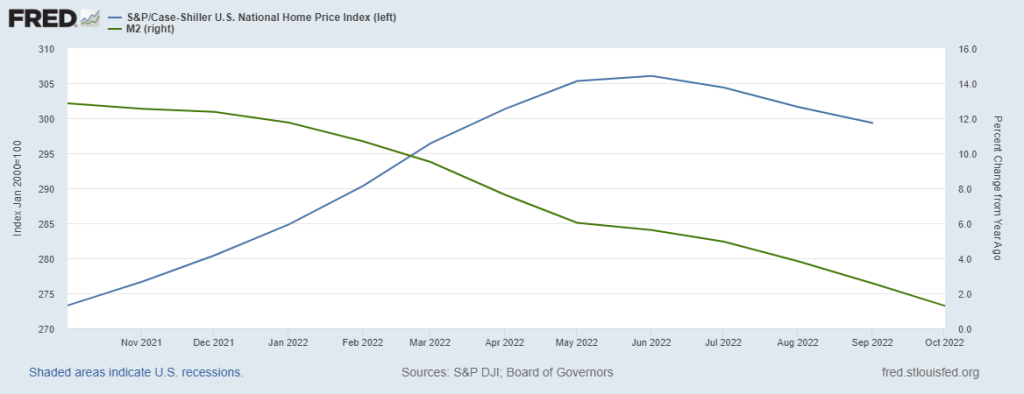

Here is the spread between Bankrate’s 30-year mortgage rate and their 30-year JUMBO mortgage. Notice that between 2007 and early 2020, the median “jumbo spread” was 49 basis points. But after Covid and The Fed’s counterattack (by printing M2 Money), the median Jumbo spread from 4/1/2020 to today is only 1 basis point.

In the following chart, you can see the jumbo mortgage rate (yellow) against the conforming mortgage rate (white) and there is almost always a spread between the two UNTIL 2020 where we saw M2 Money growth (green line) spike and The Fed increased their purchases of Agency MBS (purple line). Since Covid and The Fed’s massive reaction, the jumbo rate and conforming rate are virtually the same. In fact, the latest jumbo spread is 1 basis point over the conforming rate.

Why is this happening? One explanation is that demand from the investors who ultimately buy jumbo mortgages. The strong demand by investors appears to have driven down the yields on jumbos relative to conventional loans, especially as the use and accessibility to jumbos has grown.

A second explanation is that Loan Level Price Adjustments that were added to conforming loans post-financial crisis never went away (until just recently on selected loans). This makes jumbos and conforming loans very close in yield.

So, when will the mortgage market return to normal and jumbo mortgages go back to the normal 50 basis point spread? We may see normalization if The Fed speeds up its withdrawal from markets. Also, getting rid of Loan Level Price Adjustments would help normalized the mortgage market.

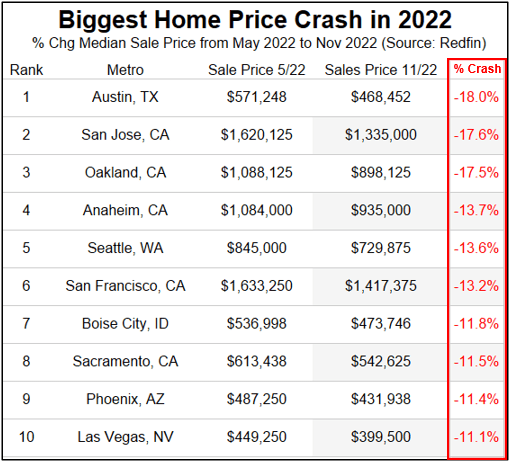

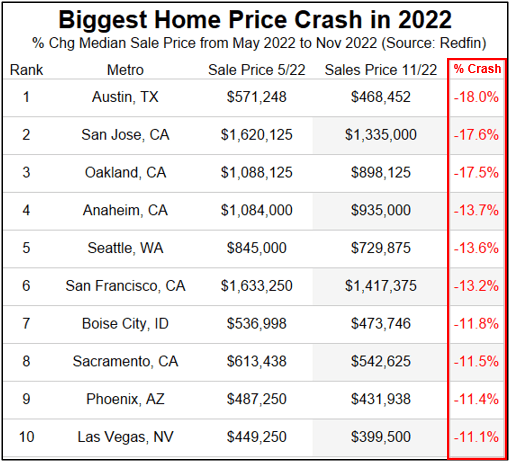

But things are getting stressed in jumboland (California) where home prices are crashing in 5 of the top 8 metro areas.

Harry Houdini couldn’t have created a more tantalizing mystery … and one I wish would go away.

Apparently, despite the denials from the Biden Administration, someone at Bureau of Labor Statistics or someone in Congress or the Federal Reserve or the Biden Admininstration itself likely tipped the wink on the soft CPI report on Tuesday.

Treasuries were well on the front-foot in the lead up to the below-estimate November CPO print, as a surge of buying took place seconds before the official 8:30 am New York release time. Over a 60 second period before the data, 13,518 March 10-year futures traded as the contract moved from 114-04+ up to 114-22. Gains were then extended up to 115-11 session highs once the data was released.

On the equity side, stock futures suddenly spiked more than 1%. Trading in Treasury futures surged, pushing benchmark yields lower by about 4 basis points. Those are major moves in such a short period of time — bigger than full-session swings on some days. And they should get scrutinized by regulators, long-time market observers say, even if a leak is only one of several possible explanations for why traders suddenly started buying right before the report was published.

Remember that current Treasury Secretary Janet Yellen was accused of leaking information to a NY hedge fund ahead of the Fed Open Market Committee meeting? And then we have the Wolf of Wall Street.

I wonder if the REAL Wolf of Wall Street did this?

Fun week ahead. US inflation numbers are out on Tuesday (forecast? CPI YoY = 7.3%, Core CPI YoY = 6.1%) and The Federal Reserve’s Open Market Committee (FOMC) rate decision is on Wendesday.

So, where are we sitting on Monday?

First, the US Treasury 10Y-2Y yield curve has been inverted (a precursor to recession) for 116 straight days). Second, the likelihood of recession in 2023 is 100%. Third, with the forecast of core inflation at a still numbing 6.1%, The Fed seems dead set on raising their target rate by 50 basis points to 4.50% on Wednesday.

dddd

So, as The Fed debates recession versus fighting inflation (partly caused by The Fed), we have Kevin Malone from The Office debating Angela versus double-fudge brownies:

This will be the last time (Fed rate hikes) as the US economy is forecast to either go into a recession in 2023 or slow down to an anemic 1.20% Real GDP YoY. Even the Fed is forecasting 3.10% core inflation in 2023, still higher than their target rate of 2%.

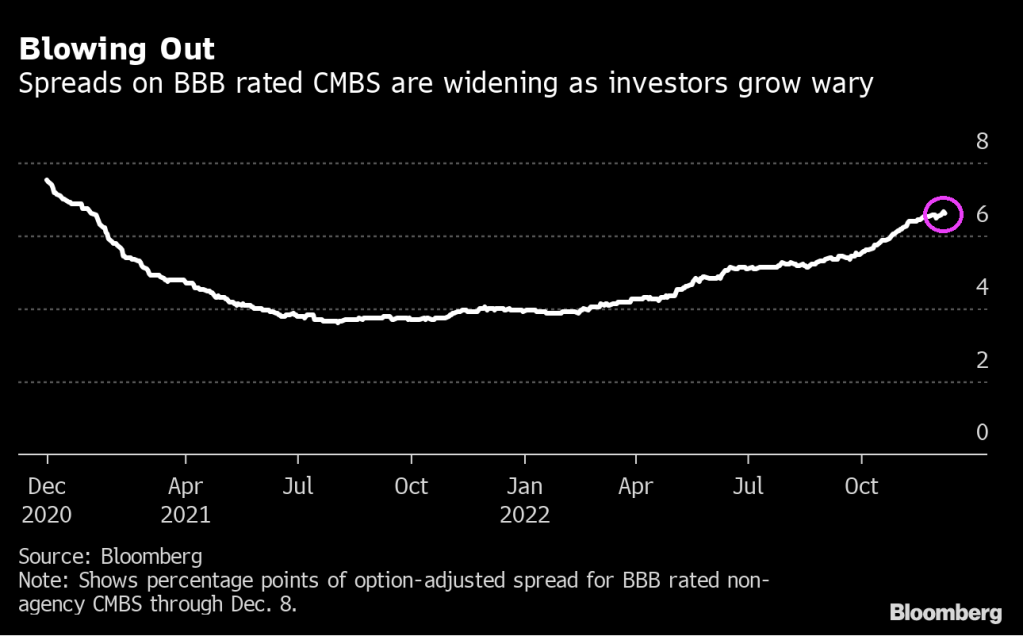

One of the sectors that is suffering is commercial real estate.

Commercial mortgage bonds could get clobbered in the coming months, and investors are backing away from the securities.

Some $34 billion of the bonds come due in 2023, and refinancing property loans is difficult now. Property prices could fall 10% to 15% next year, according to JPMorgan Chase & Co. strategists. And some types of properties seem particularly vulnerable as, for example, city workers are slow to come back to their offices full time.

That may be why spreads on BBB commercial mortgage bonds have widened by about 2.7 percentage points this year through Thursday to around 6.6%, for the securities without government backing. They are now at their widest since January 2021. They’ve been getting hit particularly hard in the last few months, even as risk premiums on investment-grade and high-yield corporates have been shrinking on hopes the Federal Reserve will scale back its tightening campaign.

“For CMBS investors, there’s lots of uncertainty, especially around whether maturing loans are going to get refinanced or not, and if not, what the resolution will be,” said David Goodson, head of securitized credit at Voya Investment Management, in an interview. “Layering in risk from lower office utilization makes the assessment even tougher.”

The trouble that the bonds face won’t necessarily translate to a surge in defaults in the near term, which is part of why betting against them is so difficult. When property owners can’t refinance mortgages that have been bundled into bonds, noteholders have a difficult choice to make. They can seize the buildings and liquidate them, or they can extend the debt and accept repayment later. They usually go for the second option.

Extending maturities allows bondholders to kick the can down the road and potentially recover more later, said Stav Gaon, head of securitized products research at Academy Securities. The question is whether properties have permanently lost value as, for example, people reorder their lives after the pandemic, or whether declines may be more temporary because of higher rates.

“Foreclosing on a loan, rather than granting an extension, can be really messy — that’s a lesson that was learned during the great financial crisis,” said Gaon. “The lenders also recognize that today’s higher interest rates are a very sudden development that many high-quality borrowers need time to adjust to.”

Some investors that are still buying are focusing on higher-quality borrowers and properties, that are likelier to withstand any downturn in real estate prices without having to seek extensions on loans.

“We think trophy properties will fare better due to better access to the debt markets, lower potential property declines, and a continued tenant flight to quality,” said Zach Winters, senior credit analyst at USAA Investments.

He acknowledges that this strategy isn’t always popular now, even if it turns out to make sense.

“When we go out and bid on a bond tied to a trophy office building now, usually the number of buyers is significantly less than before,” Winters said.

After the Pandemic

The market for commercial mortgage bonds without government backing was about $670 billion as of the end of 2021, and although the securities soared in the second half of 2020 as the Fed opened the money spigots, they’re facing more difficulty now. With office occupancy still below 50% in many cities as more people work from home, corporate buildings may see their values drop. Retail space is similarly under pressure as consumers have grown used to buying more online. And while travel volume is rising, many hotels are struggling to reach 2019 levels for room charges.

A survey of institutional real estate market professionals in November found that firms expect office values to fall about 10% next year, and overall commercial property declines of 5%, according to the Pension Real Estate Association.

The $34 billion of bonds due next year includes mostly fixed-rate CMBS bonds sold without government backing. It’s a steep increase from the $24.4 billion of such bonds maturing this year, according to Academy Securities.

There’s another $103 billion of a type of CMBS known as single-asset single-borrower bonds maturing next year, according to Academy — although most of that debt pile has a built-in contractual ability to extend loans, meaning they’ll be able to seek extensions more easily.

Next year won’t be the first time that CMBS bondholders and servicers have faced tough choices about whether to allow en masse extensions to the underlying borrowers. After the 2008 financial crisis, commercial property values plummeted and many lenders chose to give owners of those properties more time to pay back their loans. As a result they ended up getting more money back than if they’d immediately foreclosed on the loans and liquidated the properties, said Jeff Berenbaum, head of CMBS and agency CMBS strategy at Citigroup.

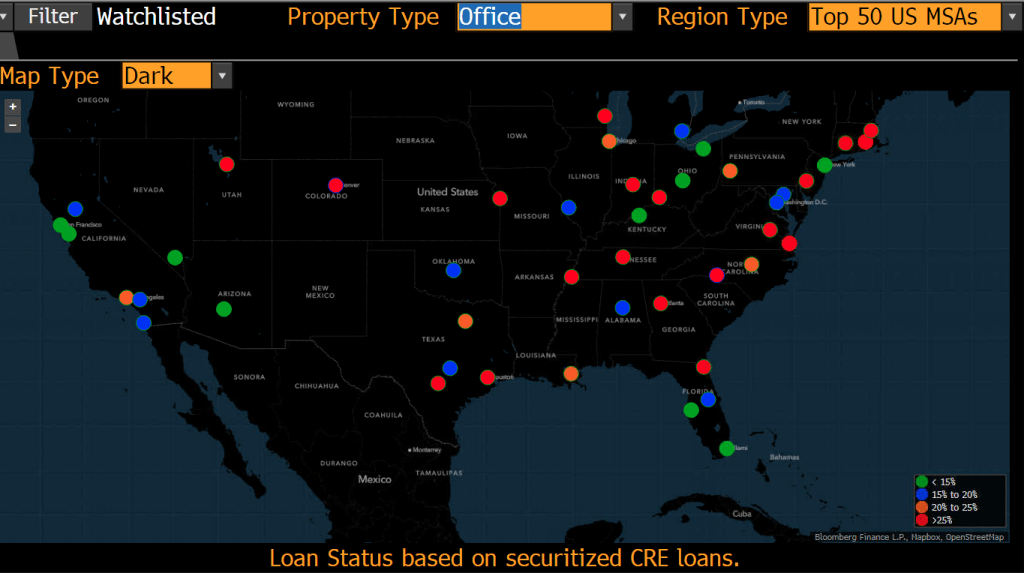

In terms of watchlisted CMBS loans, currently most of the USA is in the green (good) except for San Francisco, New Orleans, Memphis and Chicago all have elevated commercial loans on the watchlist (loans being watched for going late and into default). Puerto Rico is also in the red (>25%) watchlisted commercial loans, so I expect AOC to be asking for a bailout.

On the office property front, we can see red (>25% of commercial loans watchlisted) pretty much across the board.

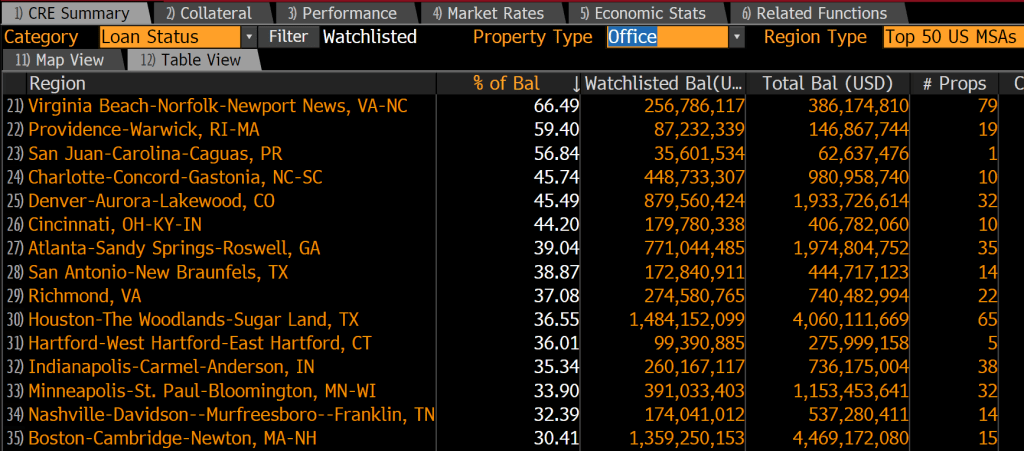

The leading metro area in terms of watchlisted office property loans is … Virginia Beach-Norfolk-Newport News VA-NC at 66.49% (that is pretty bad). Providence RI is second and San Juan Puerto Rico is third followed by Charlotte NC in fourth place. The only Ohio city in top 15 is Cincinnati, home of Skyline Chili and Montgomery Inn.

While most are calling for more rate hikes in 2023, I predicted that December’s likely 50 basis point hike with be the last one for a while as the US economy grinds to a halt. Or it’s all over now for Fed rate hikes.

While The Fed predicts slow growth, markets are pointing to recession. The Fed is out of touch with reality. As is the US Secretarty of Treasury, “Too low for too long” Janet Yellen.

US producer prices rose in November by more than forecast, driven by services and underscoring the stickiness of inflationary pressures that supports Federal Reserve interest-rate increases into 2023.

The producer price index for final demand climbed 0.3% for a third month and was up 7.4% from a year earlier, Labor Department data showed Friday. The monthly gains for October and September were revised higher.

At the same time, the annual increase was the smallest in 18 months, extending a months-long easing and suggesting the central bank still has scope to pause its rate hikes next year as expected. Cooler demand at home and abroad has taken some stress off supply chains.

The data come just days before the release of the closely watched consumer price index, which is forecast to show inflation, while much too high, continues to decelerate.

While PPI is declining, it is still far above The Fed’s inflation rate of 2% (red line).

Watch out for energy prices when the sleeping giant (China) opens up again and demand for energy skyrockets. Meanwhile, Clueless Joe is merrily draining the US Strategic Petroleun Reserve.

Lastly, congratulations to former Cleveland Brown QB Baker Mayfield for winning with the LA Rams against the Las Vegas Raiders with a stunning 99 yard drive for a TD at the end of the game.

Always behind the curve, US Senators (Warren, Marshall, Kennedy) want to get to the bottom of Silvergate’s decline and its relationship with Sam Bankman-Fried and FTX. This reminds me of the 2008 financial crisis when The Federal Reserve claimed they never saw it coming. Despite the data.

But back to crypto bank Silvergate.

Crypto bank Silvergate Capital Corp. was asked by three US Senators to release all records about transfers of funds for the collapsed FTX empire of Sam Bankman-Fried.

“Your bank’s involvement in the transfer of FTX customer funds to Alameda reveals what appears to be an egregious failure of your bank’s responsibility to monitor for and report suspicious financial activity carried out by its clients,” Senators Elizabeth Warren, Roger Marshall and John Kennedy wrote in a letter released Tuesday. “The public is owed a full accounting of the financial activities that may have led to the loss of billions in customer assets, and any role that Silvergate may have played in these losses.”

Shares of the La Jolla, California-based bank fell as much as 8%. The slide extends Silvergate’s losses on the year to more than 84% and has it trading at a fresh 52-week low. Not surprisingly, Silvergates’ stock price is closely linked to cryptocurrency Bitcoin.

The letter cite concerns about the banking services that Silvergate provided to both FTX as well as Bankman-Fried’s trading firm, Alameda Research. It says the arrangement between FTX and Alameda depended on Silvergate’s depository services and puts the bank “at the center of the improper transmission of FTX customer funds.”

“Silvergate’s failure to take adequate notice of this scheme suggests that it may have failed to implement or maintain an effective anti-money laundering program, as required under the Bank Secrecy Act,” the Senators said.

Perhaps Silvergate should be renamed Silverfish. But seriously, no US Senator or DC regulator saw the following chart?? Bitcoin and other cryptos have been clobbered in 2022 as The Fed tightens monetary policy to combat inflation.

Here is our regulator, SEC’s Gary Genslar, keeping an eye on cryto exchanges like FTX.

Maybe US Senators and DC regulators thought Silvergate is a silverfish.

The start of a new week and the US Treasury 10-year yield is up 10 basis points, always a noteworthy change. And with it, the 30-year mortgage rate should climb.

Since Biden/Pelosi/Schumer are in a lame duck session with Republicans taking the House in January, let’s see if Republicans can halt the insanity in Washington DC.

Be that as it may, Fed Funds Futures are pointing at a 50 basis point rate hike at the December 14th FOMC meeting.

Seriously, how is The Federal Reserve going to cope with $204 TRILLION … and growing Federal debt AND unfunded liabilities?

We are truly living in Strange Days under Joe Biden. And with Elon Musk’s release of Twitter’s suppression of the Hunter Biden laptop scandal, they call Joe Biden the Sleaze.

As The Federal Reserve tries to crush Bidenflation, we are seeing Fed Remittances to the US Treasury soaring (white line). At the same time, we see the Biden Administration draining the Strategic Petroleum Reserve (orange dashed line). And as The Fed tightens, M2 Money growth crashes (green line).

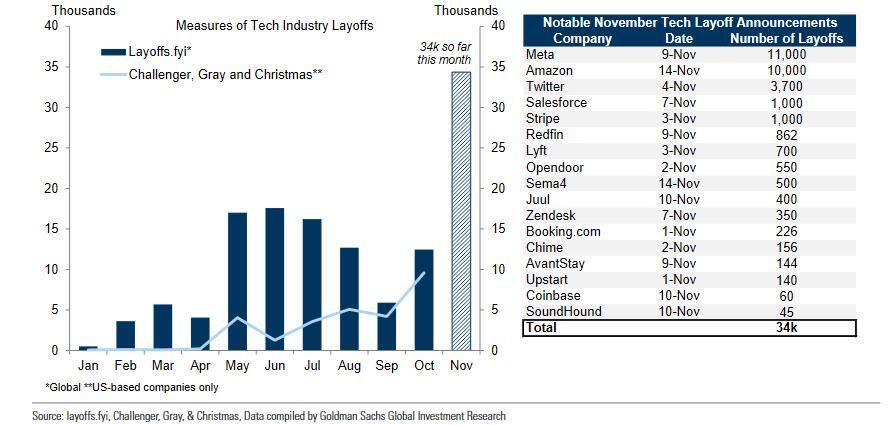

And with tech layoffs, I predict that 2023 job growth will be pretty bad.

As I have discussed before, I am a fan of ADP’s job reports and not a fan of the BLS NFP reports. As M2 Money growth slows, we can see declining ADP jobs added (yellow line), but BLS’s NFP report shows huge spikes.

Lastly, we have Sam Bankman-Fried and FTX. SBF should be in custody for being involved in one of the biggest fraud cases in history, but like Hunter Biden, is roaming free and trying to raise MORE funds. Why are these lapses in justice occuring with “10% for The Big Guy” Biden?

You must be logged in to post a comment.