I love how The Federal Reserve talking heads, the media, economists like Paul Krugman, all refer to inflation as “transitory” and excessive liquidity as “temporary.”

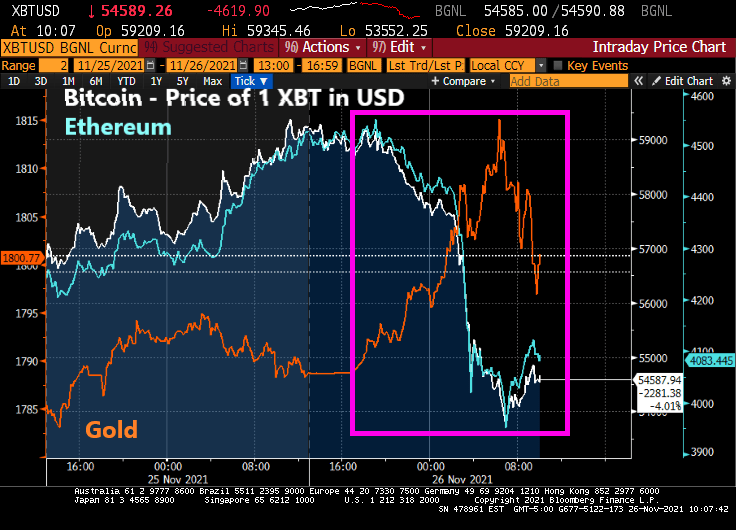

Let’s look at a variety of alternative investments to the S&P 500, GameStop, Bitcoin, Ethereum and Gold after The Federal Reserve’s and Federal government massive (over)reaction to COVID in early 2020. Gold is the first asset to surge after M2 Money surged, but has declined since. Game Stop had a big surge (likely due to positive vibes on Reddit), but has been volatile and generally falling since “The Surge.” Bitcoin had a delayed surge as did Ethereum. Despite fear about government regulation, Ethereum in particular remains elevated.

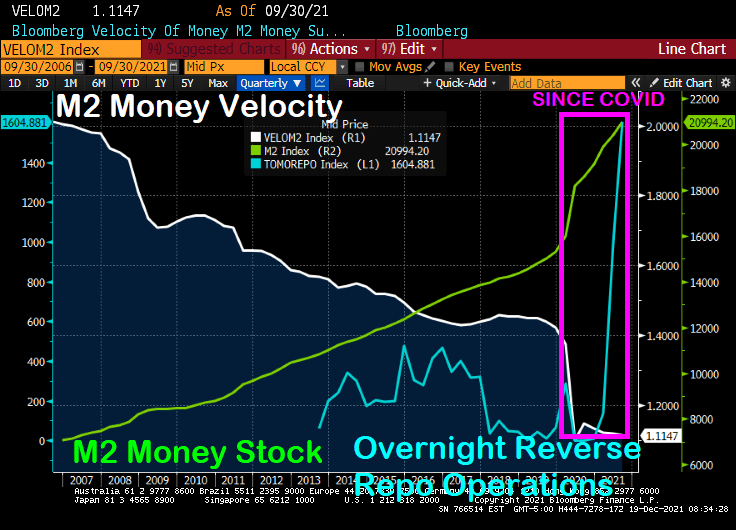

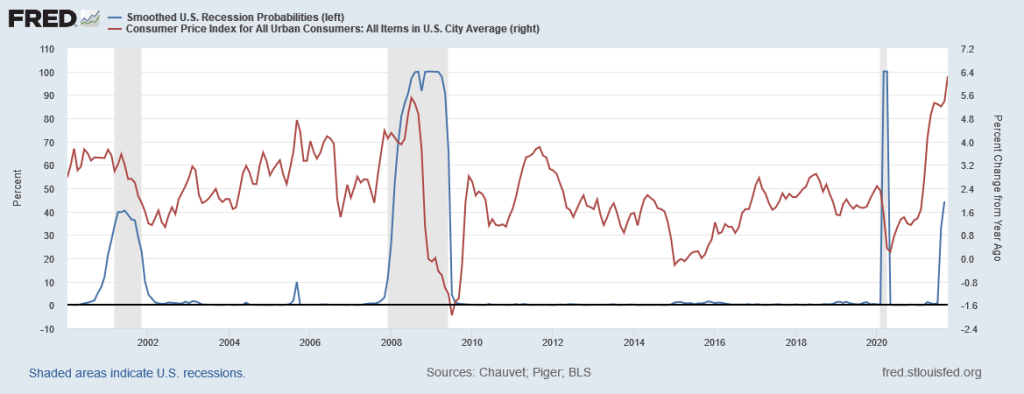

The “temporary” stimulus has resulted in the lowest M2 Money velocity in history. And we will have to see if the “temporary” excess liquidity in the financial system is truly temporary.

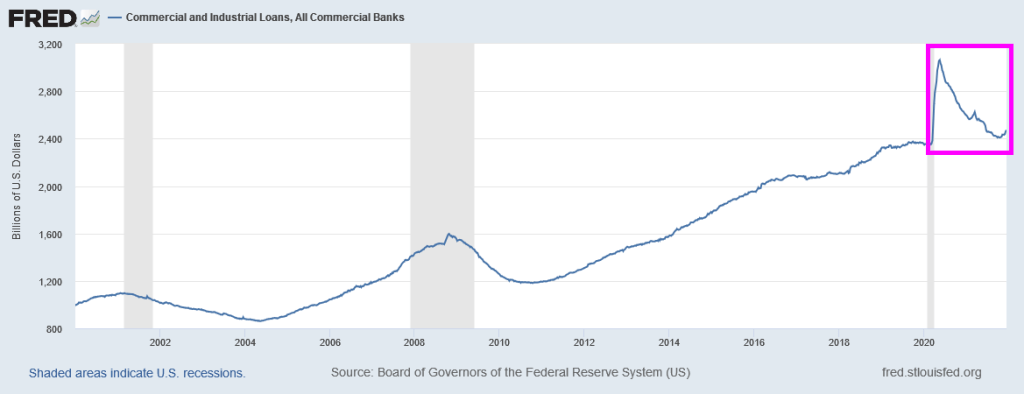

Here is a chart to show the “Stimulytpo” effect on commercial and industrial loans which surged (including PPP loans) but have simmered down to pre-COVID levels.

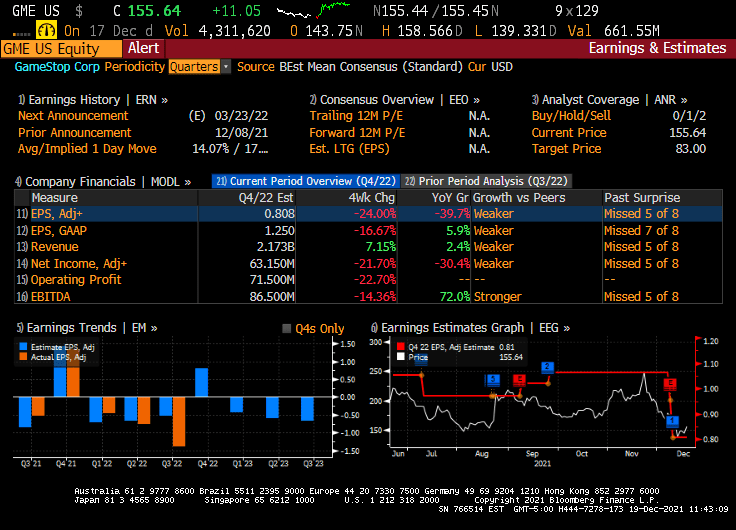

The earnings for GameStop were terrible (down 39.7% YoY). But at least Christmas season is upon us and maybe GameStop will surge with a good retail spending season.

But what happens to markets if the Federal government “stimulypto” is removed? If it ever is.

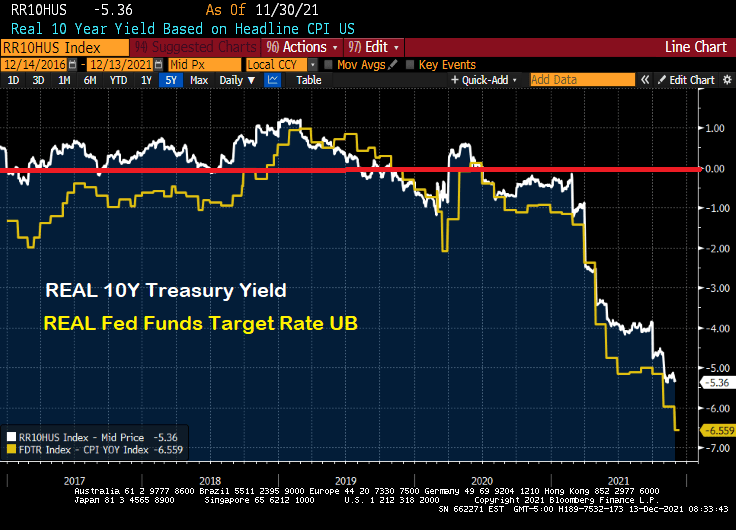

Inflation-adjusted return of Treasuries fell to lowest since the 1980s. For bond investors, this is their version of Kevin’s Famous Chili from The Office! Or The Fed’s Famous Chili!

(Bloomberg) — Treasury investors are losing more money than they have in four decades, once inflation is taken into account. And if markets are right, they’re unlikely to come out ahead for years.

The federal government’s debt has already lost about 2% outright over the past year as the Federal Reserve started removing pandemic-era stimulus from the economy and inched closer toward raising interest rates. But on top of that, the consumer price index has surged 6.8%, putting investors even deeper in the hole.

Taken together, that’s resulting in the worst real returns — or those adjusted for inflation — since the early 1980s, when then Fed Chair Paul Volcker was in the midst of fighting a wage-price spiral. What’s more, the dynamic isn’t expected to change: The bond market is projecting that 10-year Treasury yields will hold below the inflation rate for the next decade, meaning any investment income will be more than wiped out by the rising cost of living.

If we look at the REAL 10-year Treasury yield and REAL Fed Funds Target Rate, they are both negative.

Let’s see if Powell spills his famous chili on Wednesday at 2:00PM EST. The Fed keeps saying they are serious about controlling inflation, just like Kevin Malone.

China cut the amount of cash most banks must hold in reserve, acting to counter the economic slowdown in a move that puts the central bank on a different policy path than many of its peers.

The People’s Bank of China will reduce the reserve requirement ratio by 0.5 percentage point for most banks on Dec. 15, releasing 1.2 trillion yuan (US$188 billion) of liquidity, according to a statement published Monday.

The reduction was signaled by Premier Li Keqiang last week when he said that authorities would cut the RRR at an appropriate time to help smaller companies, and is the second reduction this year.

The decision comes after recent data showed the economy and industry stabilizing, although Beijing’s tightening curbs on the property market have led to a slump in construction and worsened a liquidity crisis at developer China Evergrande Group and other real estate firms.

Evergrande’s ADR is collapsing (now 5.975) along with Evergrande debt falling to 23.12 (versus 100 par).

China’s credit impulse has nosedived (see pink box) as the PBOC drops bank reserve ratios to lowest level since 2007 in an effort to float the boat. Will the PBOC drop in reserve ratios stem the tide? Or is it peasant magic?

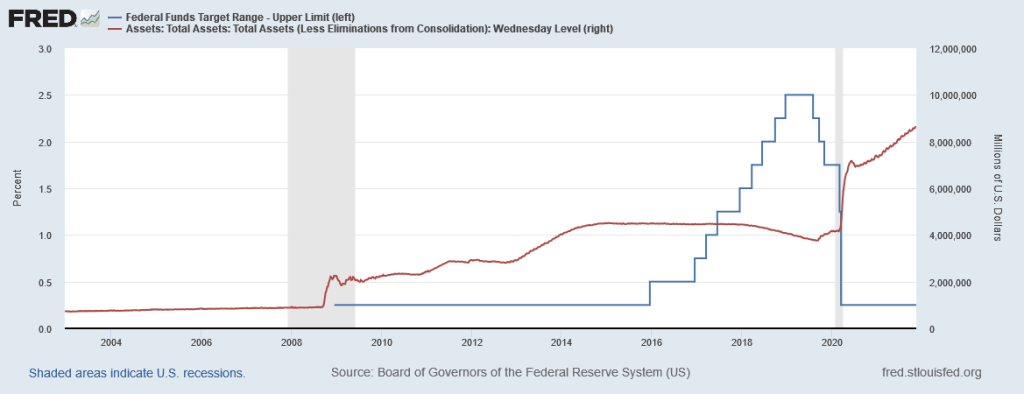

As The Federal Reserve tries to drain-off the extraordinary growth in its balance sheet since COVID without raising its target rate (good luck with that!), it is time to appraise where we are sitting. First, liquidity.

(Bloomberg) Buying and selling large quantities of U.S. government debt without substantially moving the market is about the hardest it’s been since the pandemic sent markets reeling in March 2020. Volatility has jumped, failed trades have increased — and Wall Street analysts warn that the Federal Reserve’s exit from bond-buying is set to make matters worse.

When markets seized up last year, liquidity in most Treasuries vanished, forcing the Fed to embark on massive asset purchases and other measures to avert a full meltdown. Now, the U.S. central bank is scaling back that buying, which has targeted the least-liquid Treasuries, and is poised to quicken the wind-down. At the same time, new government borrowing is ebbing, with the combination setting the stage for more fireworks.

OK, liquidity isn’t as bad as COVID and March 2020, but it is near the highest level since March 2020. The question is … will the numerous asset bubbles around the globe burstLet’s look at the ongoing saga of Chinese conglomerate Evergrande (mainly known as a large real estate developer). Their 8.25% bond has plunged to $23.481 on speculation of a catastrophic default on their bond payments. Then we have Invesco’s Golden Dragon China ETF (measuring a diversified market cap of US-listed companies headquartered or incorporated in China & derive a majority of their revenues from the People’s Republic of China). This ETF has crashed and burned back to pre-COVID (and Stimulytpo) levels.

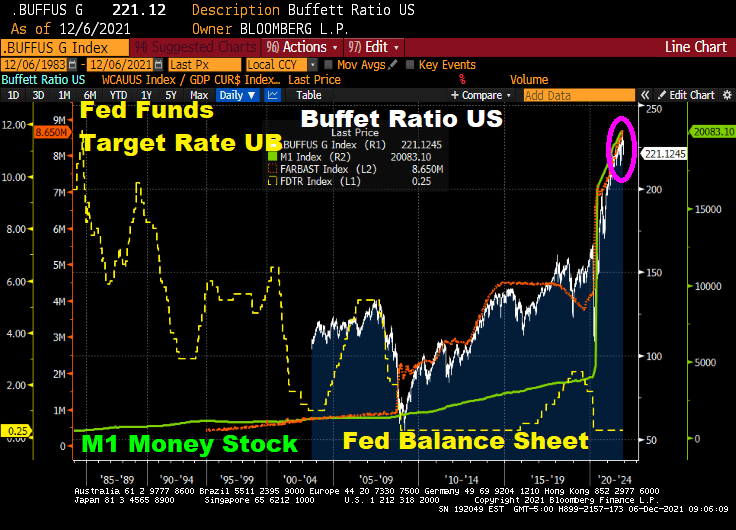

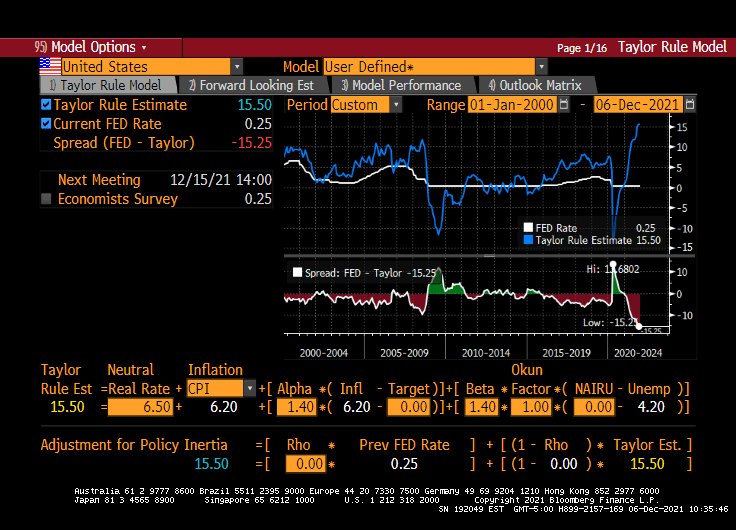

Speaking of cracks, how will the Buffett Ratio US react to a reduction in The Fed’s balance sheet (orange line) and M1 and M2 Money stock? Given that the Fed Funds target rate is WAY below where it should be (according to the Taylor Rule).

As I mentioned yesterday, the Shiller CAPE ratio is at its highest level since the Dot.com debacle of 2000. How will the Shiller CAPE ratio react to The Fed’s tapering?

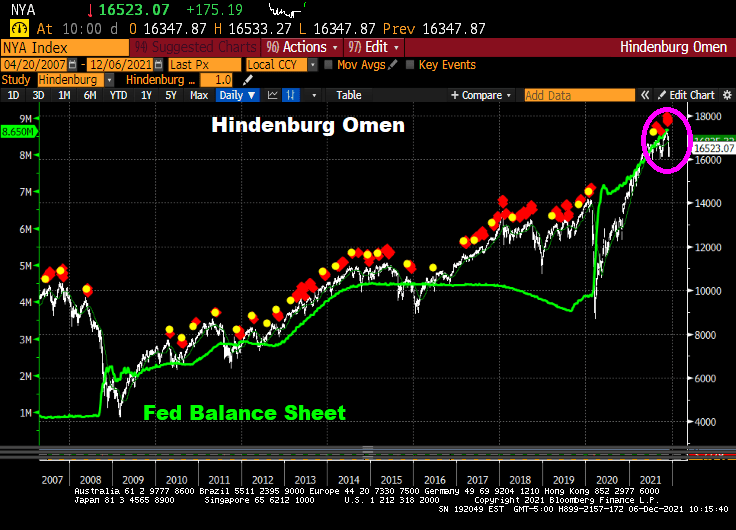

Even the Hinderburg Omen is flashing red … again.

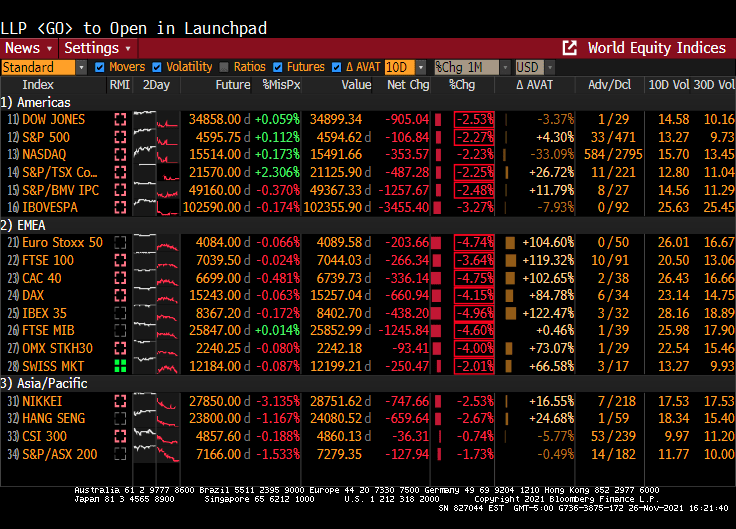

Now, the Dow is up 600 points today, primarily on the news that the Omicron Variant is about as harmful as the common cold.

A major shift is underway at the Federal Reserve to begin to remove the central bank’s massive pandemic easing policies, and could see it hike rates sooner than is priced in by markets.

Comments by Fed officials suggest the central bank is likely to decide to double the pace of its taper to $30 billion a month at its December meeting next week. Initial discussions could also begin as soon as the December meeting about when to raise interest rates and by how much next year with Fed officials set to submit a fresh round of economic forecasts and projections for the fed funds rate.

There is no consensus yet on when to begin hikes, but it’s clear that the faster taper is designed to give the Fed flexibility to raise rates as soon as the spring. The markets do not appear to expect the first rate hike until the summer of 2022.

Uh-huh. Let’s see what happens when and if The Fed starts to taper. Is economic growth so strong that it can continue without Federal Stiumulypto? THAT is the right question.

Look at the above charts and tell me if The Fed will actually raise their target rate more than twice. Despite the Taylor Rule suggest a target rate of 15.50% to cool inflation.

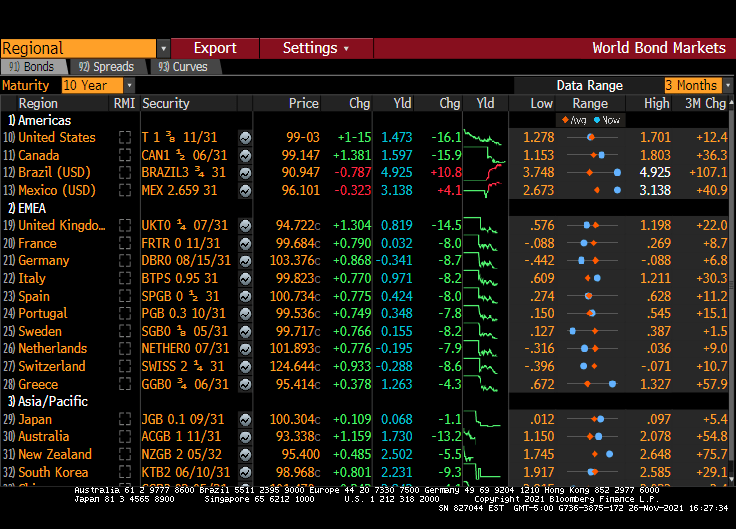

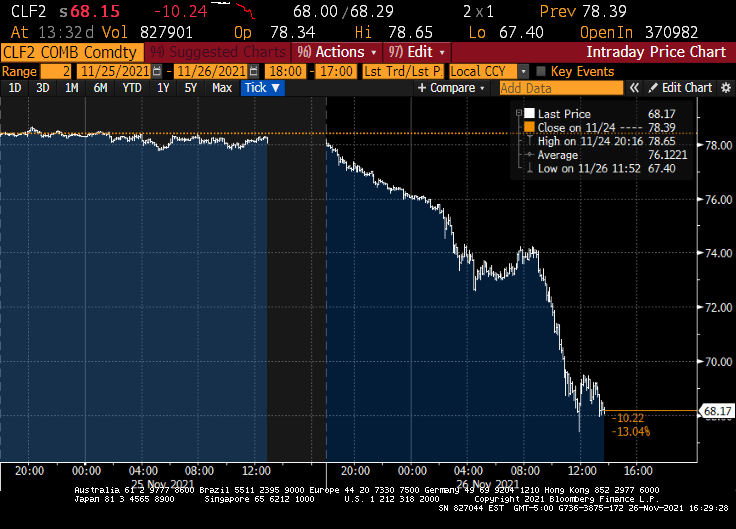

It has been a grim Friday. The Dow fell 900 points, 10Y Treasury yields fell 16.1 basis points and West Texas Crude fell to $68.17.

Bitcoin tumbled 20% from record highs notched earlier this month as a new variant of the coronavirus spurred traders to dump risk assets across the globe.

The world’s largest cryptocurrency fell as much as 8.9% to $53,624 on Friday during London trading hours. Ethereum, the second-largest digital currency, dropped more than 12%, while the wider Bloomberg Galaxy Crypto Index declined as much as 7.5%. On the other hand, gold rose as cryptos fell, then retreated as cryptos rebounded.

A new variant identified in southern Africa spurred liquidations across markets, with European stocks falling the most since July and emerging markets also slumping.

The Dow is down around 900 points … and look at Europe!

The 10-year Treasury yield is down 16.1 basis points. Most of Europe is down around 8-9 basis points while the UK is down 14.5 BPS.

And West Texas Intermediate crude futures are down to 68.17 from 78.39. No Jen Paski, this isn’t due to Cousin Eddie (Biden) releasing the Strategic Petroleum Reserve (SPR).

Maybe it was all the tryptophan released by eating turkey.

Its Thanksgiving in the USA! Confession: I don’t like turkey. Prime rib with horseradish sauce? You bet!!

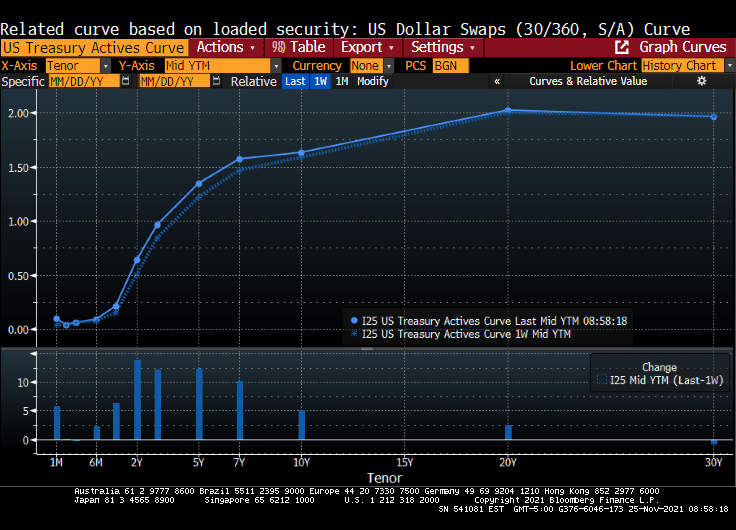

Anyway, Treasuries ended mixed Wednesday with the yield curve sharply flatter after a raft of U.S. economic data and minutes of the November FOMC meeting bolstered expectations for an earlier start to Fed rate increases. Two- and 5-year yields reached YTD highs, and 5s30s spread reached narrowest since March 2020.

Over the past week, the Treasury actives curve rose 13.85 basis points at the 2 year tenor.

Yields ended richer by ~6bp across long-end of the curve, while front-end cheapened almost 3bp; 2s10s flattened more than 5bp, 5s30s more than 6bp; 10-year yields shed ~3bp to ~1.635% Release of Nov. 2-3 FOMC meeting minutes drew minimal market reaction, as flatter curve held its shape.

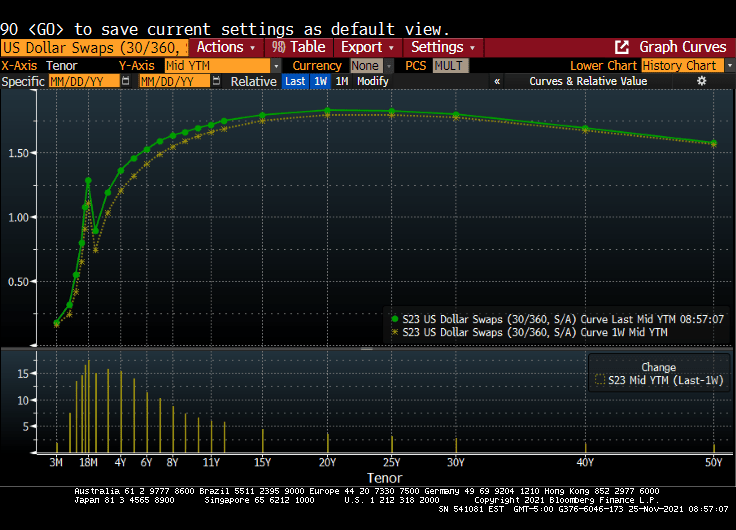

The US Dollar Swaps curve rose from the previous week as well.

Minutes said participants considered elevated inflation as likely transitory, “but judged that inflation pressures could take longer to subside than they had previously assessed”

Earlier, front-end and belly sold off after a heavy slate of U.S. economic data including the lowest initial jobless claims tally since 1969

Also during U.S. morning, Fed’s Daly said she would support accelerated tapering of asset purchases, which added to pressure across front-end Treasuries

Subsequently, eurodollars traded heavy over the session as rate-hike premium continued to ramp up in 2022 and 2023; overnight index swaps showed 30% chance of a March hike, while around three hikes — or 75bp — were priced in by the end of next year

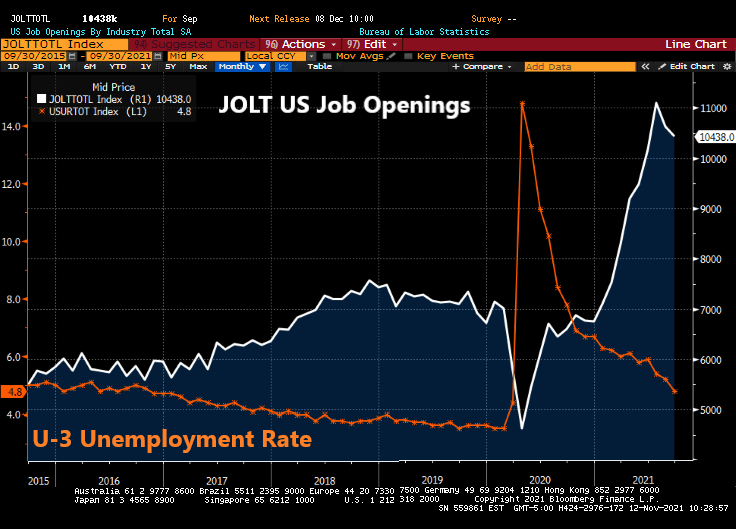

The Federal Reserve continues to JOLT markets with excessive monetary stimulus despite numerous reasons why they should back off.

For example, today’s JOLT report (US job openings) revealed that 10.4 million jobs were open in September. This is the fourth consecutive month of 1 million plus job openings, yet The Fed refuses to raise their target rate.

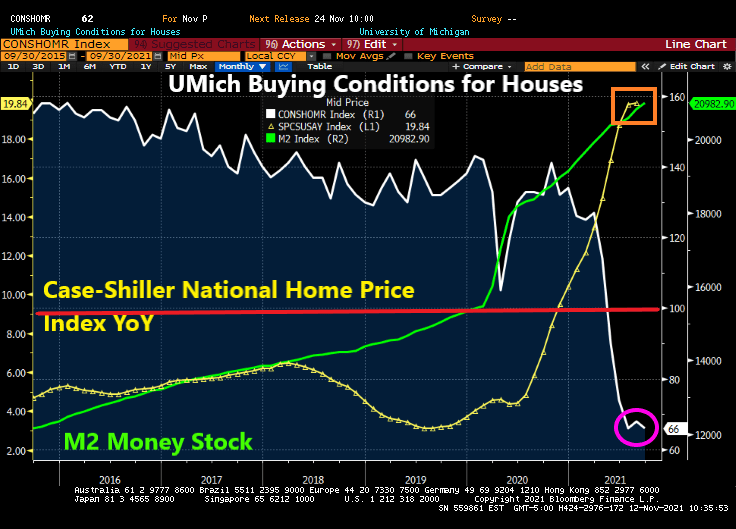

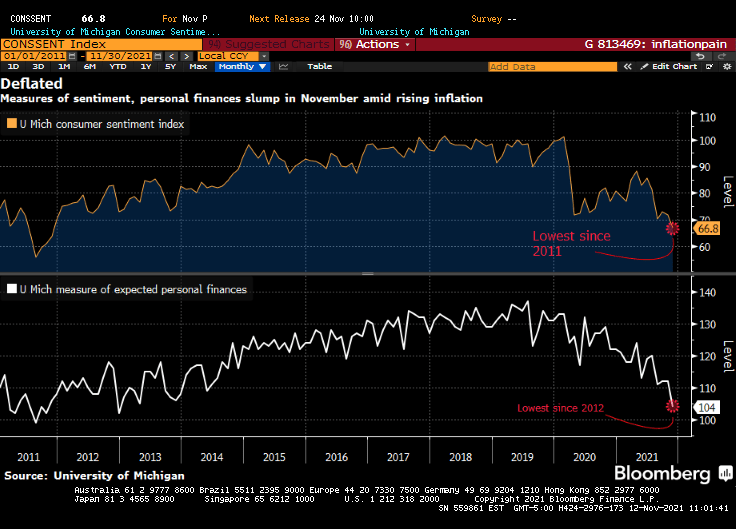

At the same time, the University of Michigan survey revealed that buying conditions for houses dropped to 66 (baseline of 100). To show how bad this is, buying conditions for houses was at 144 this time last year.

UPDATE: UMich revised their number downward to 62, the lowest since 1981.

In The Fed’s mind, they are still chasing at least 3.5% unemployment, the lowest rate under President Trump prior to COVID. But with perpetual million plus job openings GOING UNFILLED, trying to get to pre-COVID unemployment rate of 3.5% is a fool’s errand.

Of course, with The Fed helping to pump up house prices to largely unaffordable levels, it makes sense that enthusiasm for buying expensive homes has crashed.

Meanwhile, The Fed continues to JOLT the economy with excess stimulus.

Overall inflation fears are leading to lowest consumer confidence since 2011.

Now that President Biden is interviewing Lael Brainard for Federal Reserve Chair, I am really getting a peaceless, uneasy feeling that The Fed will NEVER raise rates and inflation will be perpetual. To whit, …

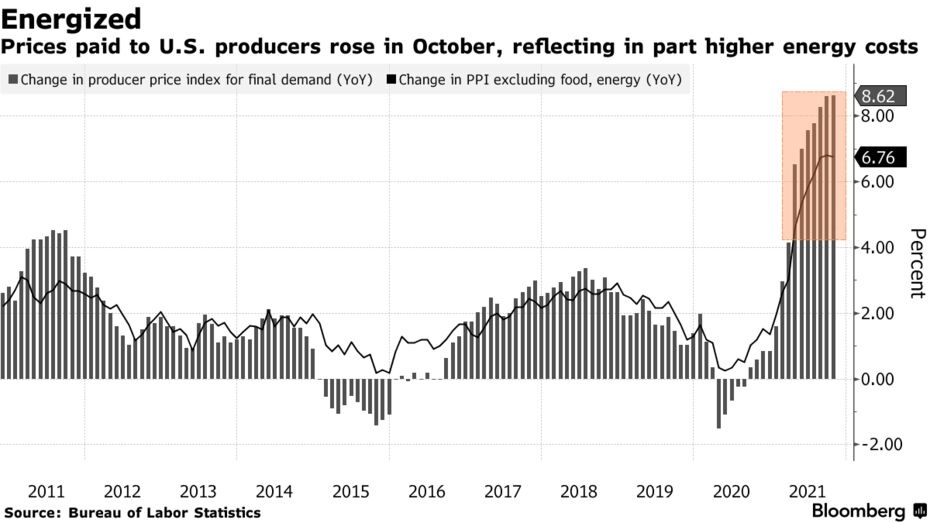

Prices paid to U.S. producers accelerated in October, largely due to higher goods costs, fueling concerns about the persistence of inflationary pressures in the economy.

The producer price index for final demand increased 0.6% from the prior month and 8.6% from a year earlier, matching forecasts, Labor Department data showed Tuesday. The annual advance was the largest in figures back to 2010.

Excluding the volatile food and energy components, the so-called core PPI rose 0.4% and was up 6.8% from a year ago.

More than 60% of the headline increase was due to goods, which jumped 1.2%. Higher energy costs, including that for gasoline, drove the gain. The cost of services rose a more moderate 0.2% for a second month, reflecting a further pullback in the cost of securities brokerages and investment advice.

The report underscores how transportation bottlenecks, materials shortages and increasing labor costs have sent prices soaring across the economy in recent months. Trucking freight costs jumped a record 2.5% from September.

Inflation is a tax created by printing too much money and stupid Federal economic policies (or follicies).

Lael Brainard? Discussing the chairmanship with Brainard could signify that the Biden team is weighing how a break with Powell might help advance their goals for the central bank. Brainard and Powell work closely together on multiple issues and are viewed as holding similar views on monetary policy, but she’s favored a tougher stance on big banks.

Remember, The Federal Reserve is a privately-owned entity independent of The Federal Government. A Brainard appointment would make The Fed the financing arm of the Democrat Party.

You must be logged in to post a comment.