The next Federal Reserve Open Market Committee (FOMC) meeting in on Wednesday, November 2nd. Let’s see what The Fed does with its BIG GREEN BAG … OF MONEY.

As I set here on Sunday morning waiting to see how the Cleveland Browns will lose to cross-state rival Cincinnati Bengals, I see that both the US Treasury 10yr-2yr and 10yr-3mo yield curves are inverted (below zero).

Core inflation (CPI less food and energy) YoY (blue line) was only 1.3% in February 2021 shortly after Biden was sworn-in as President and is now 6.6% in September 2022. That is over a 400% increase in core inflation!

We have this tantalizing headline on Bloomberg:

Goldman Sachs Now Sees Fed Rates Peaking at 5% in March By Simon Kennedy(Bloomberg) —

Goldman Sachs Group Inc. economists said they now expect the US Federal Reserve to raise interest rates to 5%, higher than previously predicted.

The central bank will lift its benchmark rate to a range of 4.75% to 5% in March, 25 basis points more than earlier expected, economists led by Jan Hatzius wrote in an Oct. 29 research report.

The route to the new peak includes increases of 75 basis points this week, 50 basis points in December and 25 basis points in February and March, they said.

The economists cited three reasons for expecting the Fed to hike beyond February: “uncomfortably high” inflation, the need to cool the economy as fiscal tightening ends and price-adjusted incomes climb, and to avoid a premature easing of financial conditions.

Well, not exactly earth-shattering. Fed Funds Futures data point to a peak of near 5% (4.905%) for the May 2023 FOMC meeting, so Goldman Sachs is calling for an earliest peak at the March 2023 FOMC meeting,

Regardless of what Goldman Sachs thinks, Fed officials are expecting a peak in 2023 followed by a decline to 2.5%.

Brainard and Bostic are the only “doves.” Which is silly because Chicago’s Evans is a perma-dove. Let’s see how the Dots Plot changes at the November 2nd meeting.

America’s distressed debt pile is biggest since September 2020.

As The Federal Reserve continues to withdraw its massive Covid-related monetary stimulus, US mortgage applications continue to fall to the lowest level since 1997.

Mortgage applications decreased 1.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending October 21, 2022.

The Refinance Index increased 0.1 percent from the previous week and was 86 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 2 percent from one week earlier. The unadjusted Purchase Index decreased 3 percent compared with the previous week and was 42 percent lower than the same week one year ago.

Under Biden, we have seen (orange line) a significant decline in mortgage purchase applications (peak 2021 to this week). Mortgage rates are the highest since 2001 (wait for it!)

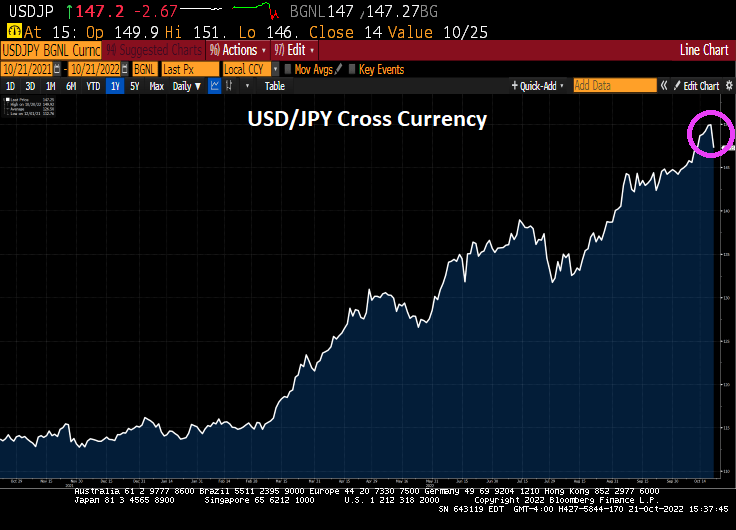

Wall Street saw another day of stunning reversals, with stocks rallying after a Treasury selloff sputtered. The yen jumped as Japan intervened again to prop up the currency.

After many twists and turns, the S&P 500 pushed solidly into the green and headed for its best week since June as 10-year yields fell from the highest since 2007.

Probably because The Fed is likely to pivot with impending recession. The Dow is up 774 points this Friday. And today was a huge option expiration day!!

And the 10-year Treasury yield fell -2.2 basis points.

Here is the result of Japan’s intervention.

But today’s numbers were largely monthly stock index option expiration.

Why did it fall upon Powell to be the wielder of the Fed tightening scimitar? Why didn’t Yellen? Because “Good Girls Don’t.” But Powell did.

Have a nice weekend. I will be rooting for Ohio State to annihilate the Iowa Hawkeyes at noon on Saturday.

Over the past year, the dollar has been on a tear: The U.S. Dollar Index, which measures the dollar’s strength against a basket of foreign currencies, is up 18%. And up 25.2% under 80-year old US President Joe Biden (well, he will be 80 in November).

For tourists, a strong dollar is great news. It means you get more for your money abroad.

But for investors, a beefed-up buck is decidedly bad news.

When the dollar strengthens, that means foreign revenues are going to translate into fewer dollars. Those earnings are going to come in lower and any overseas investment you own is going to hurt you in a rising dollar environment.

Diesel, the lifeline of the shipping industry, is UP 100% under Biden (that is, diesel prices have doubled) while the inventory of diesel fuel has declined by -37.5% under Biden.

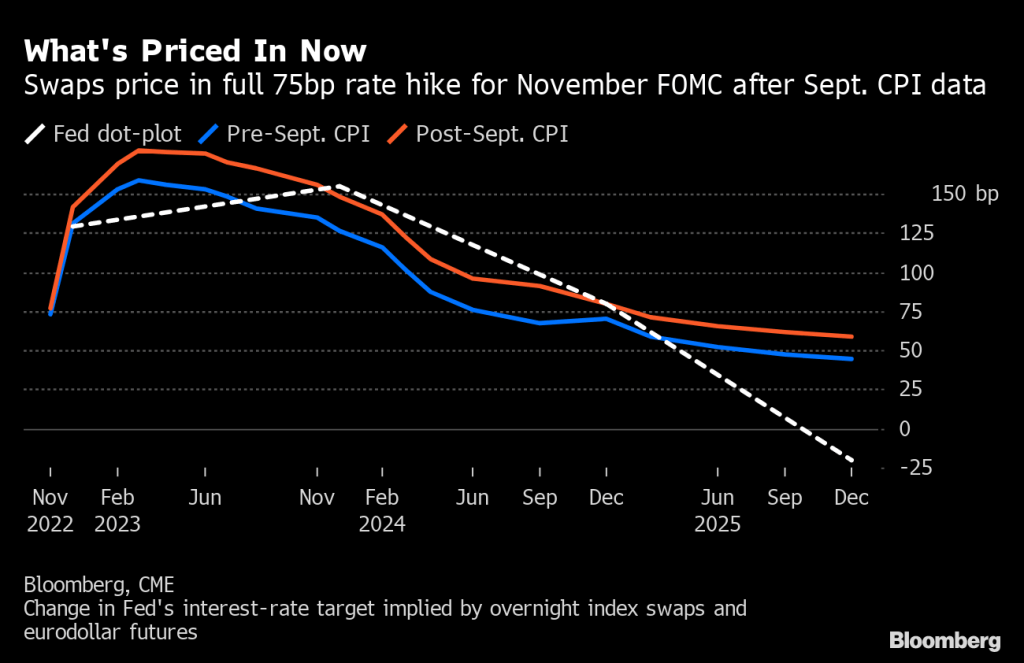

* Fed Swaps Lean Toward Back-to-Back Three-Quarter-Point Hikes * Hotter-than-expected September inflation data spark shift

(Bloomberg) — The market for wagers on the Federal Reserve’s policy rate is leaning toward pricing back-to-back 75 basis point rate hikes in the next two central bank meetings after consumer prices rose more than forecast in September.

The rate on the November overnight index swap contract rose to 3.86%, more than 75 basis points above the current effective fed funds rate, while the one referring to December climbed to 4.50%. A total of 142 basis points of rate hikes are now priced in for the next two policy meetings, just short of consecutive three-quarter-point hikes.

Prior to the inflation data, OIS markets were leaning toward the central bank cooling the pace of tightening to a 50 basis point move in December. At Wednesday’s close, swaps priced in around 130 basis points of hikes over the remaining of the year, which is equivalent to 55 basis points for December.

The market also priced in a higher eventual peak for the policy rate, with the March 2023 contract touching 4.864%.

The CPI data was “clearly a shock for the markets and the markets are off because of it,” Seth Carpenter, chief global economist at Morgan Stanley said on Bloomberg television. “There is persistence, particularly in the services side of inflation.”

Excluding food and energy, the Consumer Price Index increased 6.6% from a year ago, the highest level since 1982, Labor Department data showed Thursday. From a month earlier, the core CPI climbed 0.6% for a second straight month.

The Fed has raised its policy rate five times since March, most recently to a range of 3%-3.25% in September, after dropping the lower bound to 0% two years earlier at the onset of the pandemic.

The Fed Funds Futures data is pointing further Fed rate hikes with a turnaround in March 2023.

And with that awful inflation report and the likely Fed counterattack, the two year US Treasury yield has risen to 4.4361%, the highest since The Great Recession and banking crisis.

Fed Fireball! Comin’ at ya!!

Biden and Powell should appear on Saturday Night Live as the joint Debbie Downer. Or Democrat Downer.

You must be logged in to post a comment.