- New CEO Koerner sought to reassure employees in Friday memo

- Shares fall to a fresh record low, gauge of credit risk rises

It is like the Lehman Brothers debacle in 2008 all over again.

(Bloomberg) — Credit Suisse Group AG was plunged into fresh market turmoil after Chief Executive Officer Ulrich Koerner’s attempts to reassure employees and investors backfired, adding to uncertainty surrounding the bank.

The stock, which had already more than halved this year before Monday’s sell-off, fell as much as 12% in Zurich trading to a record low that values the firm at less than $10 billion. That was accompanied by a spike in the cost to insure the bank’s debt against default, which jumped to its highest ever.

Koerner, for the second time in as many weeks, had sought to calm employees and the markets with a memo late Friday stressing the bank’s liquidity and capital strength. Instead, it focused attention on the dramatic recent moves in the firm’s stock price and credit spreads, and investors rushed for the exit when trading reopened after the weekend.

One notable difference between 2008 and today is that Credit Suisse’s equity was flying high in June 2007 then crashed a the global banking crisis went into full motion. We then saw Credit Suisse’s credit default swaps soar in early 2009. But today Credit Suisse’s equity is a pale imitation of its former self, but its credit default swap is now higher than it was at its peak in early 2009.

Credit Suisse is now trading lower than its European rival Deutsche Bank (aka, The Teutonic Titanic).

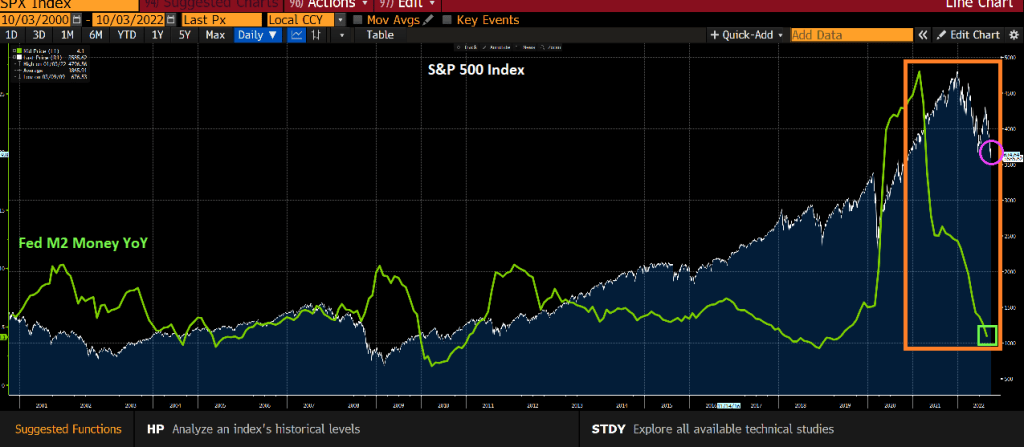

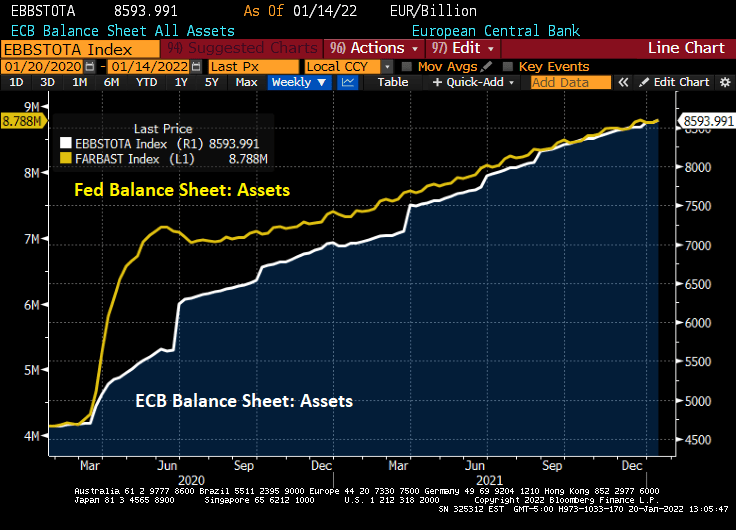

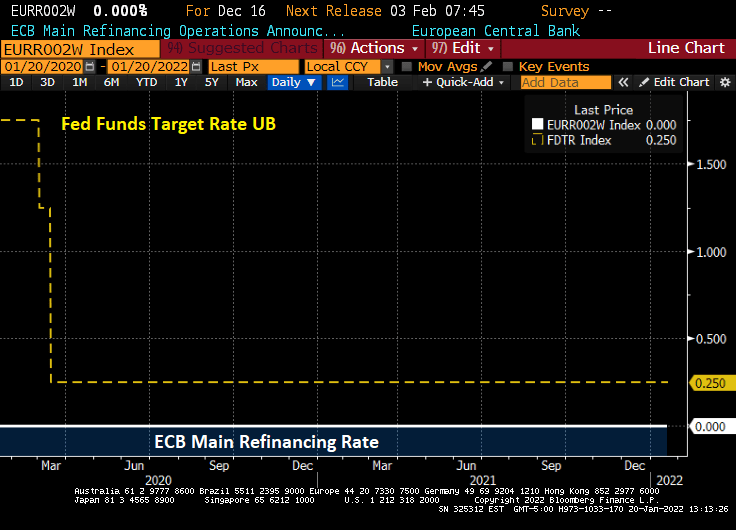

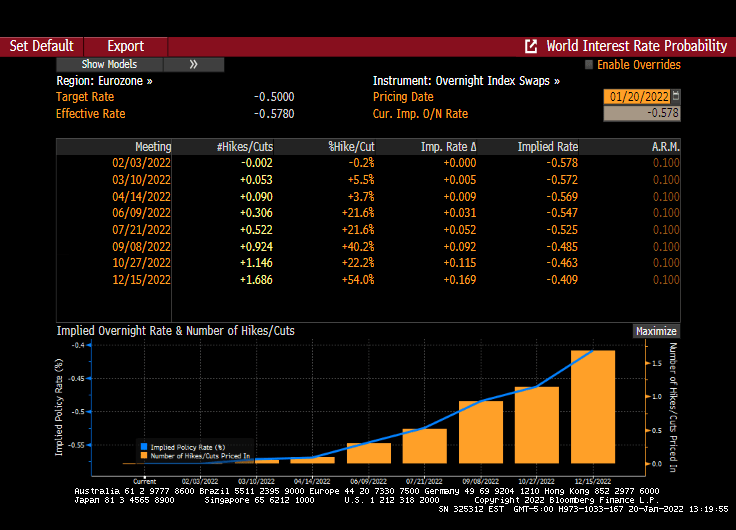

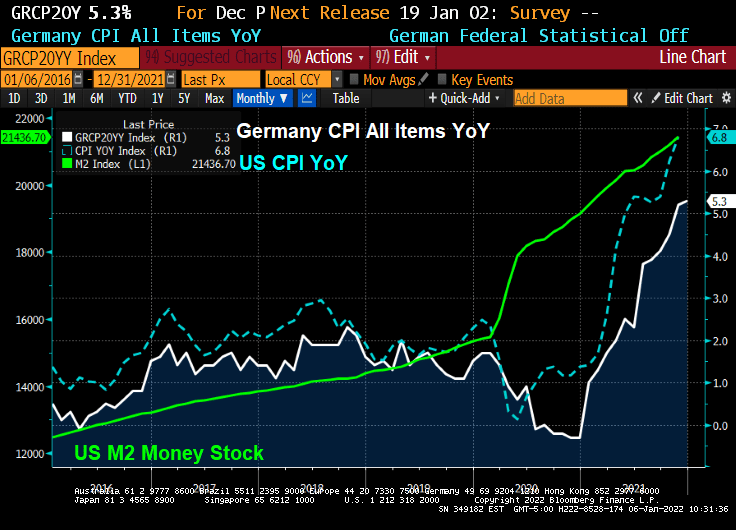

Yes, this brings back sickening memories of the 2008-2009 global financial crisis. Let’s see how The Federal Reserve, ECB and Bank of Switzerland handle this debacle, particularly with M2 Money growth so low.

It appears that we are in another Lehman debacle. Or should I say “Lemur Bros.”

You must be logged in to post a comment.