The Federal Reserve isn’t soothing me with their rate hikes.

As The Fed has been raising their target rate and beginning to shrink their balance sheet, we are seeing Q3 Real GDP slipping further down the rabbit hole to -1.5%.

The culprit? Friday’s retail trade, import/export prices and industrial production.

Time for some tequila to soothe me, since The Fed or the Biden Administration won’t help.

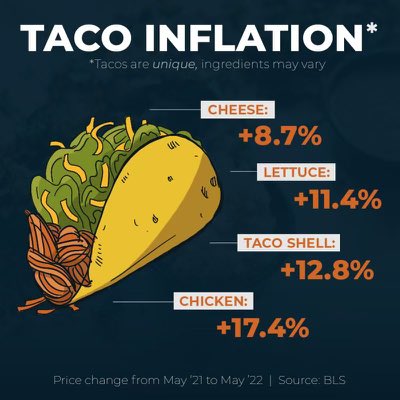

Housing in the US is simply unaffordable for the middle class and low-wage workers. Combine rising food costs and gasoline/heating costs, and we have an economic disaster on our hands.

US existing home sales for June will be released on Wednesday. But can The Fed kill-off home price inflation?

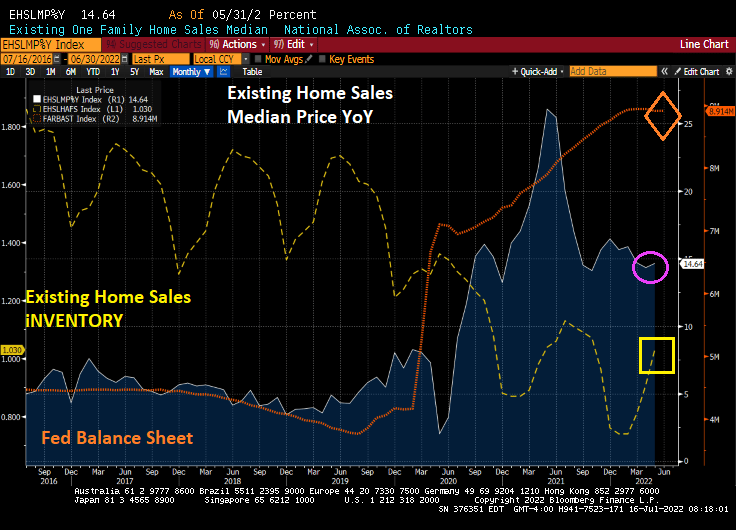

A preliminary analysis of existing home sales for June is for a seasonally adjusted annual rate of 5.1 million, down 5.4% from May and down 14.2% from last June. As The Fed cranks up its target rate (green line) and eventually shrinking its balance sheet, we will see further shrinking of existing home sales this summer.

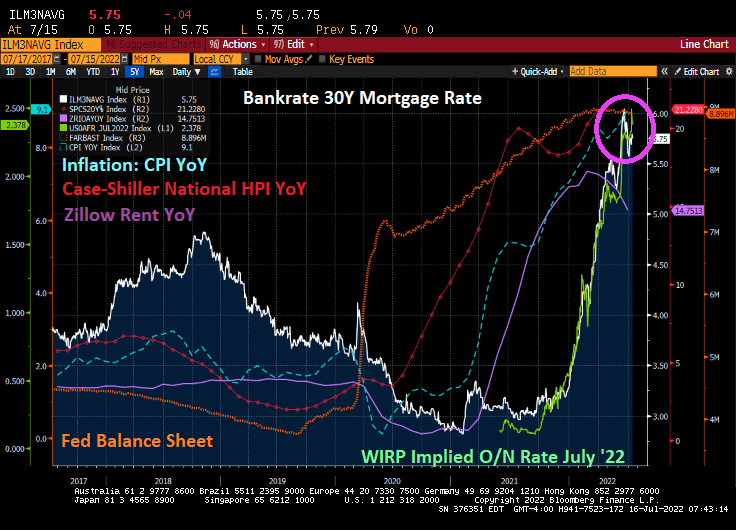

But home price inflation remains high (Case-Shiller National home price index at 21.23% YoY, Zillow’s rent index at 14.75% YoY) while the Consumer Price Index YoY is at 40-year high of 9.1% YoY. In other words, home price inflation is 233% of the stated inflation rate from Uncle Sam.

May’s existing home sales report was … sobering. There is still historically low levels of available inventory and median sales price of existing home sales was 14.64% YoY. Of course, the alternative to ownership is renting which is growing at 14.75% YoY. Simply unaffordable.

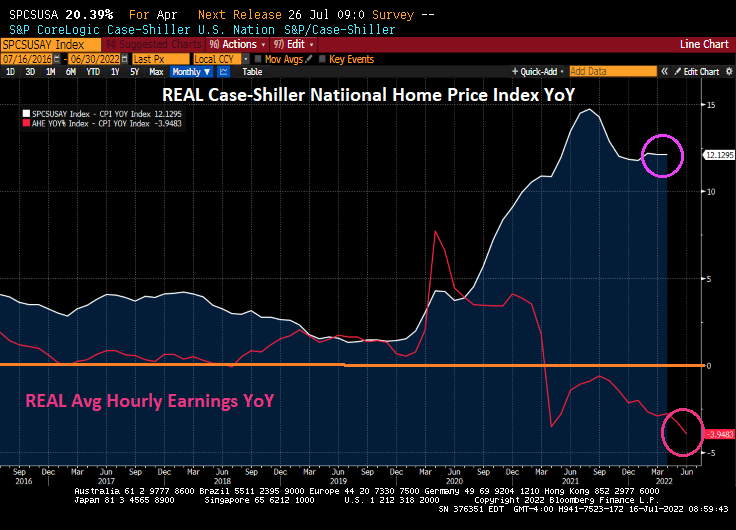

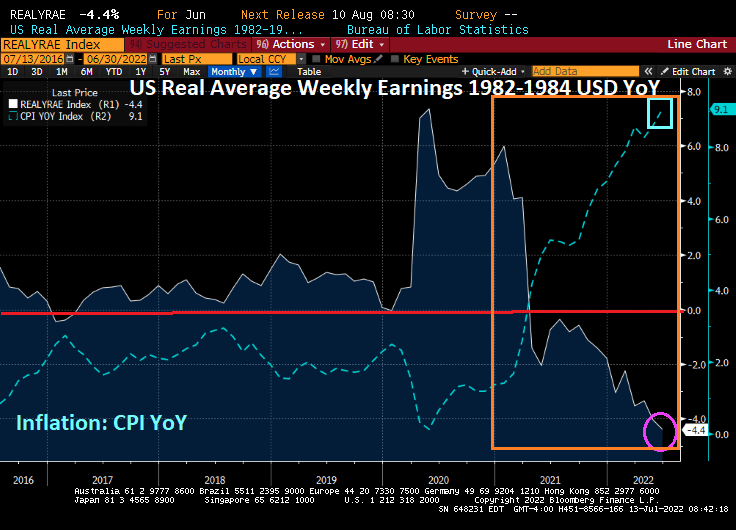

The gap between REAL home price growth (12.13% YoY) and REAL average hourly earnings (-3.95% YoY).

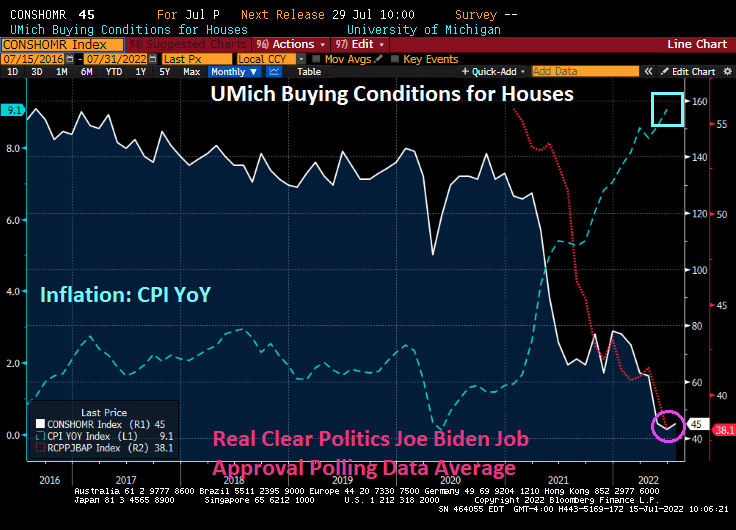

Consumer sentiment for housing is near the lowest level since 1982.

The Fed seems determined to remove the punch bowl in its efforts to crush inflation. But will The Fed’s efforts also crush the housing and mortgage market?

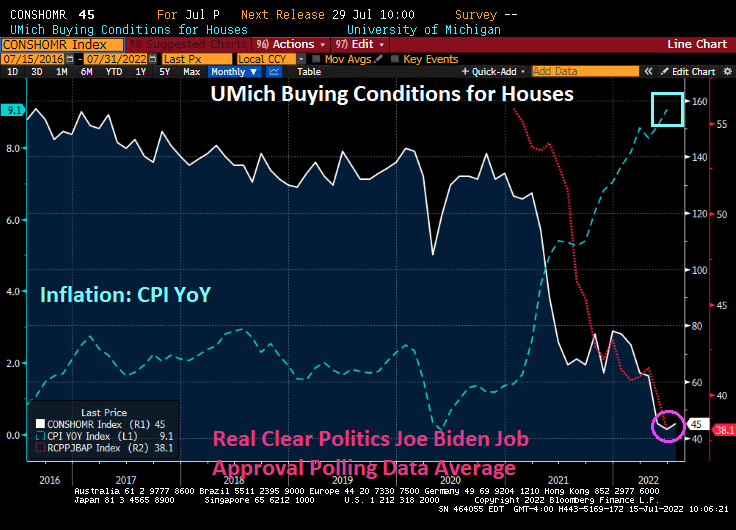

One measure of how bad things are in the US for the middle-class and low-wager workers ix consumer sentiment from University of Michigan. The latest University of Michigan survey of consumers remains depressed at 51.1.

The consumer sentiment index was at 80.7 at the beginning of 2021, but has plunged dramatically with rising gasoline, food and inflation in general. Biden’s popularity has sunk from 55.8 in January 2021 to 38.1 today.

How about housing sentiment? Housing sentiment was 134.0 in January 2021 but has plunged to a depressing 45 with inflation and rising home prices (and rent). And with declining sentiment about housing, Biden’s popularity has plunged.

As Americans are painfully aware, inflation is the highest in 40 years prompting The Federal Reserve to remove the massive punch bowl. In fact, Federal Reserve Governor Christopher “Fats” Waller backed raising rates by 75 basis points this month.

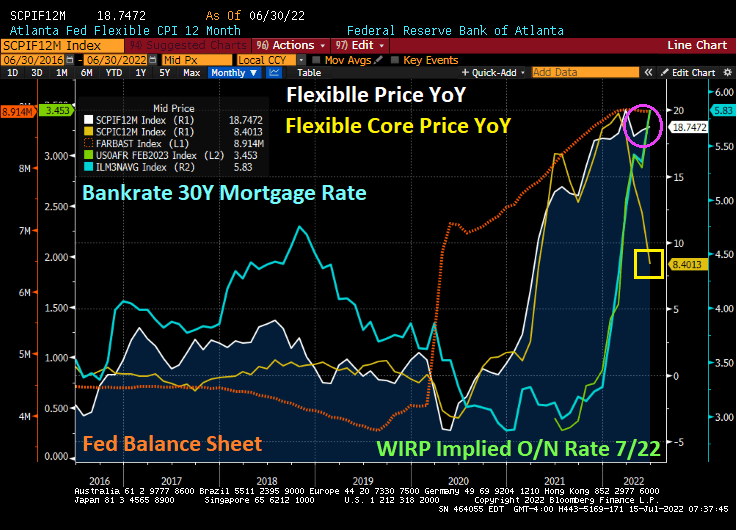

How hot was the recent inflation report? The Atlanta Fed’s flexible price index rose to 18.74% YoY. On the other hand, the CORE flexible price index (less energy and food) plunged to 8.46% YoY. The 30-year mortgage rate from Bankrate rose slightly to 5.83% as the implied overnight rate for the July FOMC meeting rose to 3.45%.

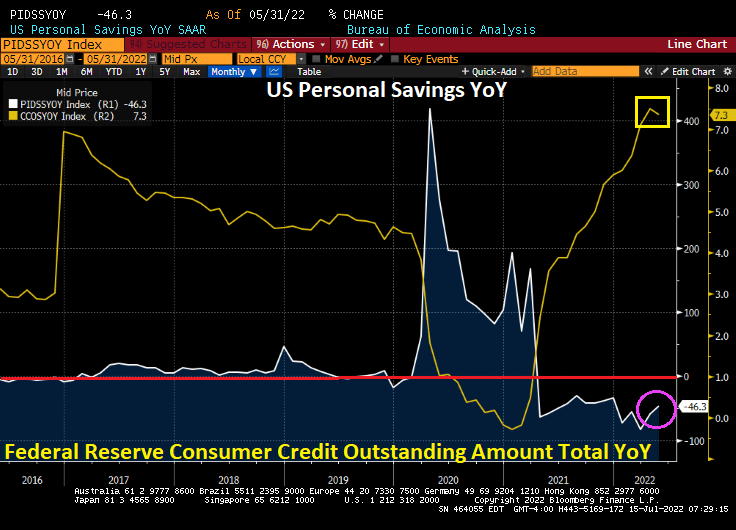

Inflation is ravaging consumers with the savings rate falling by -46.3% YoY while consumer credit rose 7.3% YoY. Yes, thanks to high inflation, consumers are saving less and borrowing more.

When even CORE flexible price inflation is 8.40% YoY, you know that The Fed and Federal government have made serious policy errors.

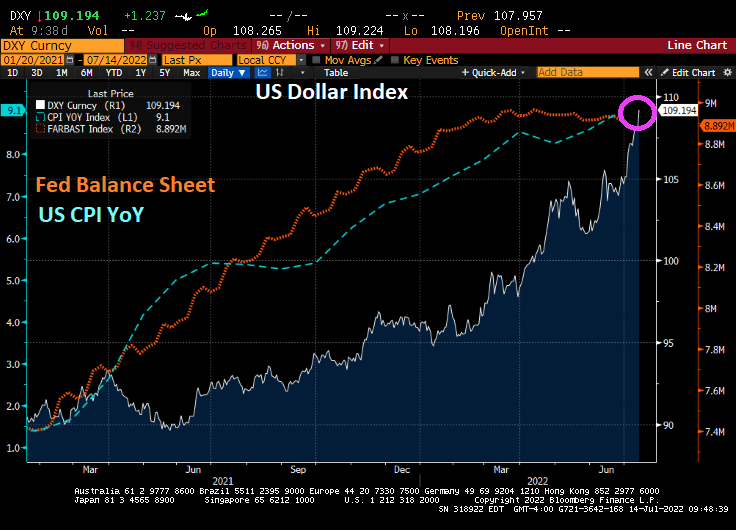

Bear in mind that a strong dollar is a two-edged sword. The US Dollar Index has risen 16% year-over-year, presenting a big hurdle for US firms with business overseas.

That strength of the greenback will rise until the Fed makes a dovish policy pivot.

And that pivot is forecast to occur at the Feb ’23 FOMC meeting.

Face it. The Biden Administration has little interest in trying to increase the supply fossil fuel energy which would anger his “green” base (like building more refineries or allowing for more crude oil and natural gas exploration). So, the burden of “inflation fighting” falls on the frail shoulders of The Federal Reserve.

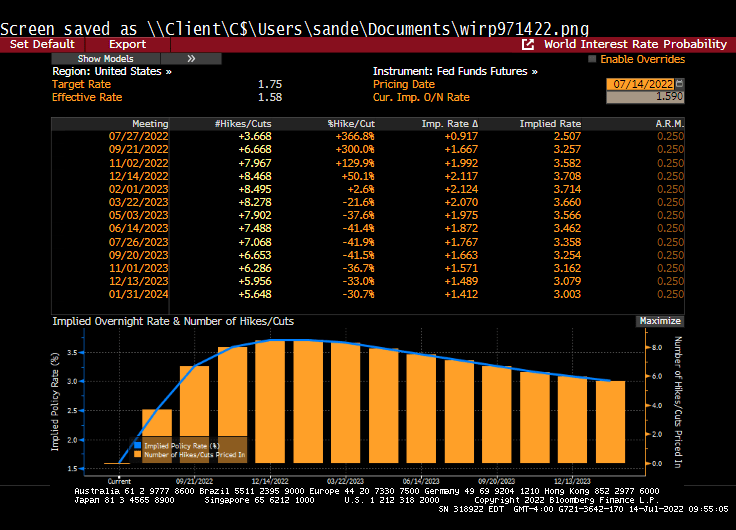

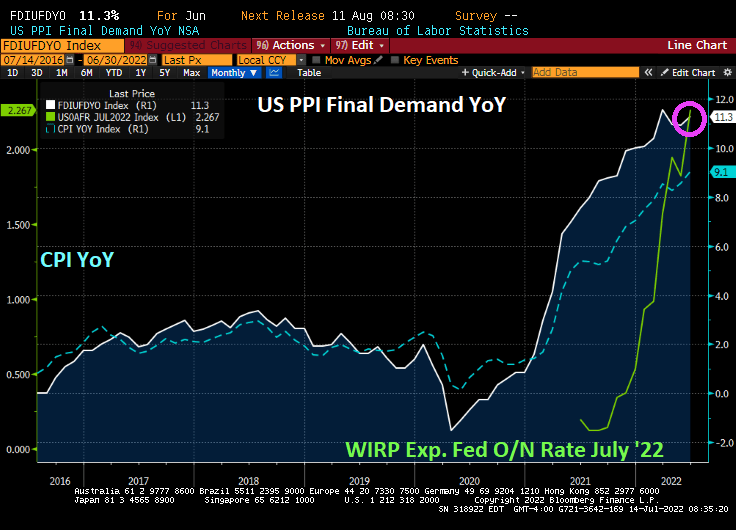

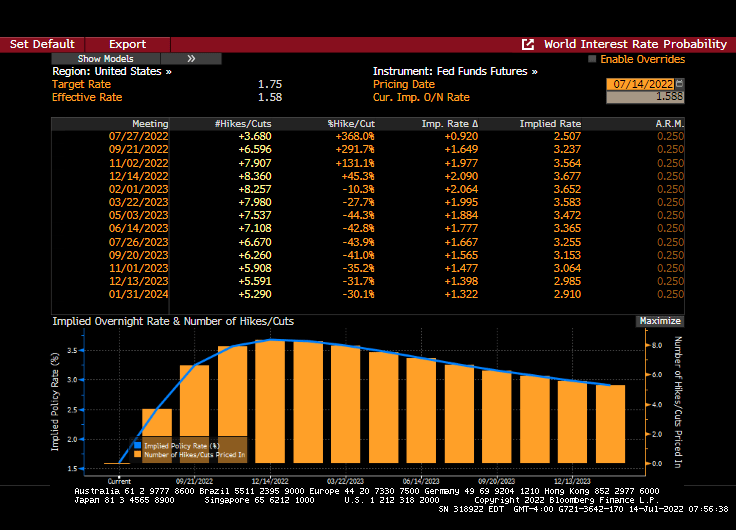

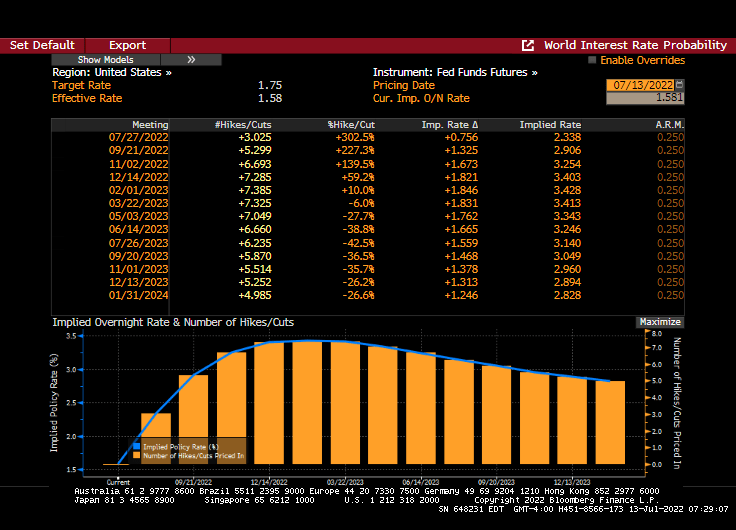

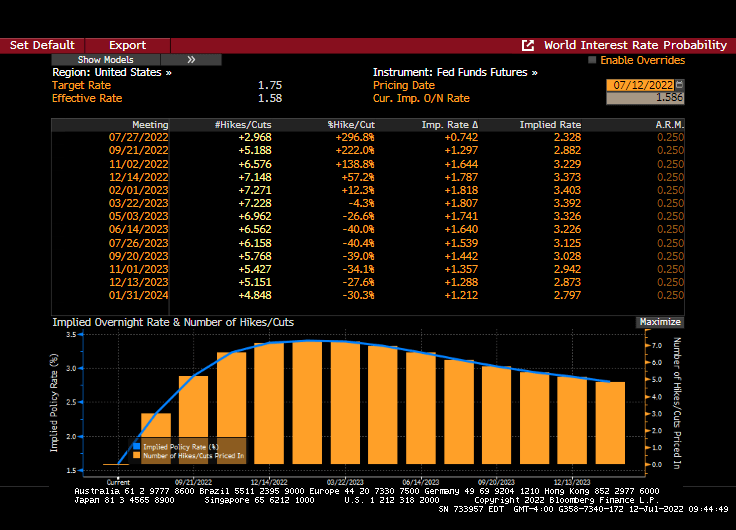

Given today’s US Producer Price Index Final Demand prices rising +11.3% YoY in June, it seems that The Fed has not been able to extinguish the “Tower of Inflation.” But, Fed Funds Futures are pointing to a near 100 basis point (or 1%) increase in The Fed Funds target rate at the July 27th Fed Open Market Committee (FOMC) meeting.

The Fed Funds Futures Data points to a +0.920 (almost 1%) increase at the July 27th FOMC meeting. Followed by rate cuts.

And with the fear of a near 100 basis point increase, today’s stock markets are a sea of red.

It is up to Fed Chair Jerome Powell and policy error brigade to extinguish price increases caused by 1) bad Biden energy policies and 2) too much spending by Biden and Congress. It is like trying to wave-down the Super Chief train with a cigarette lighter.

Yet, the Frail Fed will try to waive down The Super Chief inflation engine with Fed Fireballs. Aka, rate increases of 100 basis points.

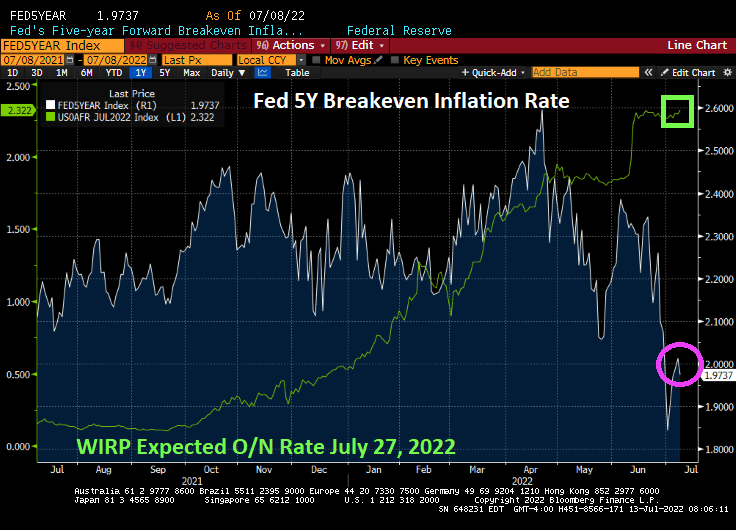

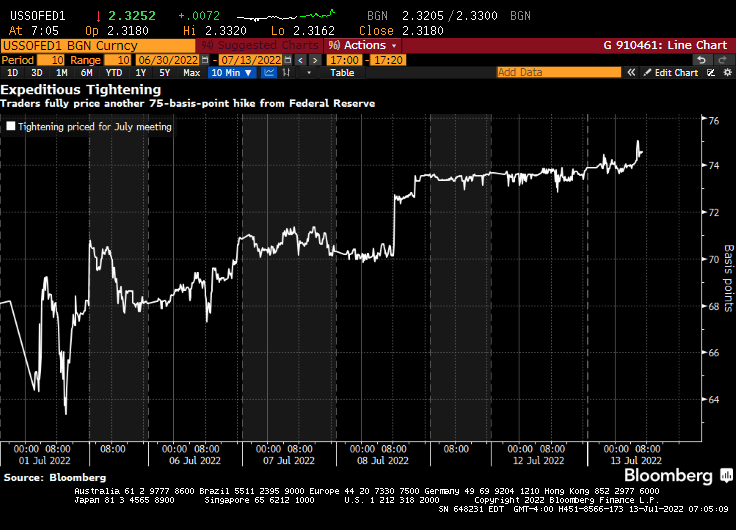

Here we go loop de loop! Traders are pricing in a 75 basis point rate increase at the July FOMC meeting despite collapsing Fed 5-year inflation breakeven rates.

Money markets are betting on a three quarter-percentage point hike by Federal Reserve officials later this month, wagering the US will need to ramp up the pace of monetary tightening to tame inflation.

The repricing comes ahead of a key inflation report due Wednesday. The headline figure for June is set to accelerate to 8.8% year over year, the highest since 1981.

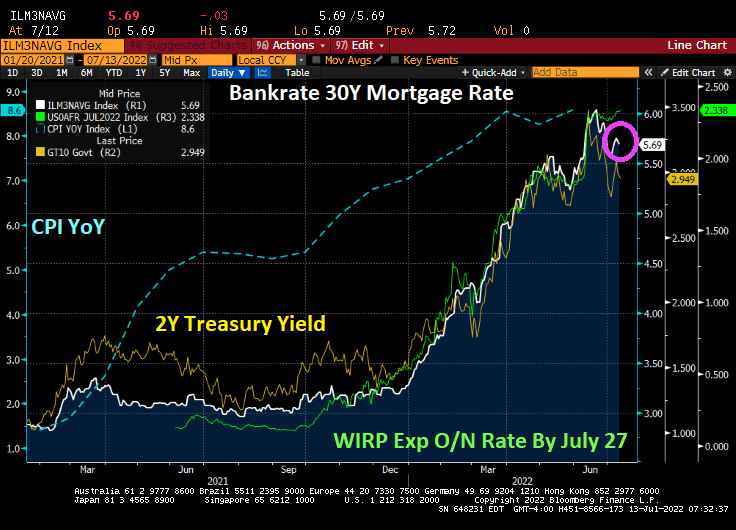

Bankrate’s 30Y mortgage rate fell slightly ahead of today’s inflation report with the expectation of The Fed hiking their target rate by 75 basis points to 2.338% at the July 27th Fed Open Market Committee meeting.

Trader expectations from Fed Funds Futures data:

Last night I watched “The Shallows” on Peacock TV. I thought from the title that it was going to be a biography of The Federal Reserve, but it was a film about a surfer being attacked by a shark.

We are all aware that inflation is soaring, since the Covid outbreak in 2020 and the massive overaction by The Federal Reserve and Federal government in terms of stimulus spending and economic lockdowns.

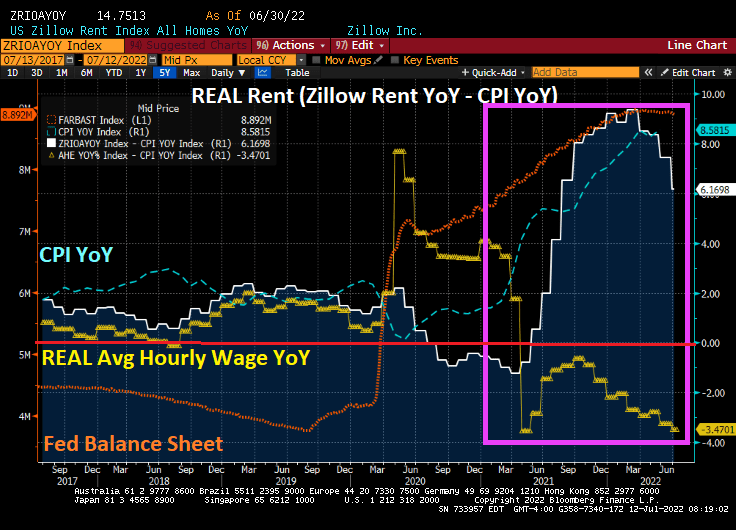

Things were “normal” before Covid in that REAL housing rent (white line) and REAL average hourly earnings YoY (yellow line) moved together. But after Covid shutdowns and Federal stimulus “relief” (orange line), we see that inflation (blue line) took off along with the growth in housing rent. The problem, of course, is that REAL average hourly earnings YoY has been declining. I call this “The Great Divide in housing affordability”.

The question, of course, is whether The Federal Reserve will continue their “war on inflation” with a 75 basis point rate increase.

Inflation is at its fastest pace in 40 years, and is expected to increase even higher in tomorrow’s inflation report.

Gasoline prices have been dropping recently, but remain above $4.50 per gallon (regular gas price was $2.40 per gallon on Biden’s inauguration day. And no, it wasn’t the Biden Administration selling nearly 1 million barrels of crude oil from the strategic petroleum reserve to the Chinese government-owned Sinopec that Biden’s son Hunter is an investor (so, The Big Guy aka Joe Biden gets a 10% piece of the action). It is a slowing global economy that is helping to lower gasoline prices.

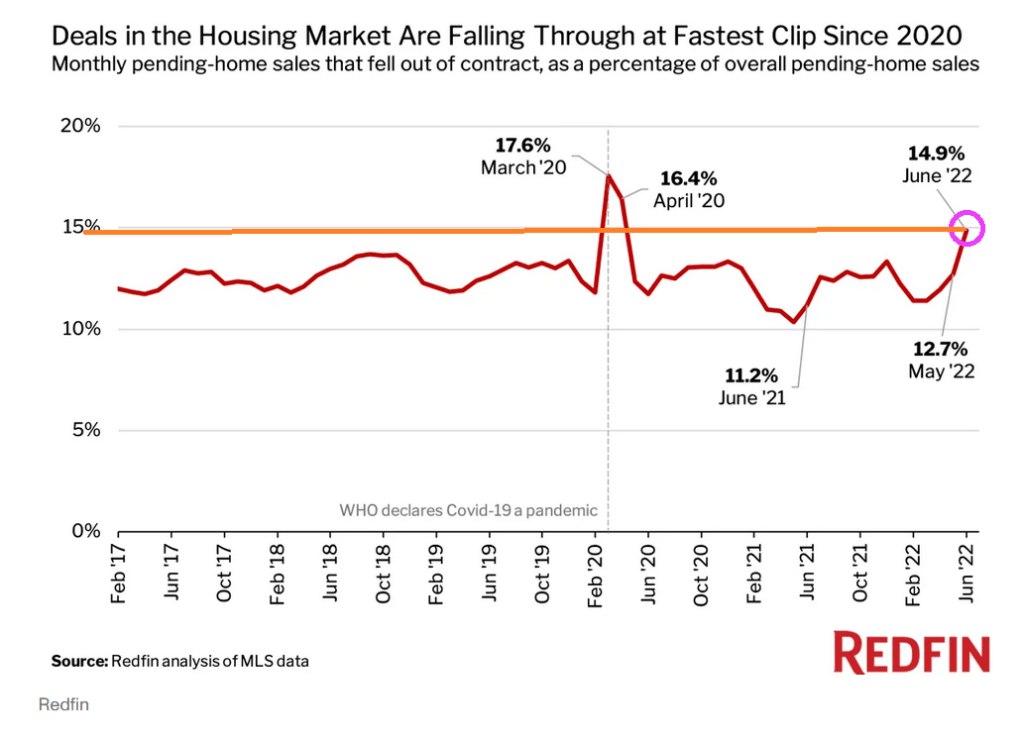

With rising mortgage rates, we are seeing a surge in pending home sales cancellations.

Atlanta Fed’s Raphael Bostic thinks that the US economy is so strong that it can easily handle a 75 basis point increase at the next FOMC meeting. Fortunately, he is not a voting member.

You must be logged in to post a comment.