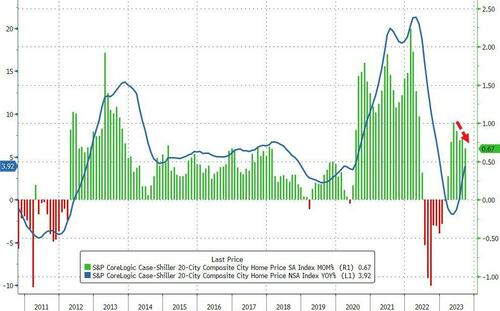

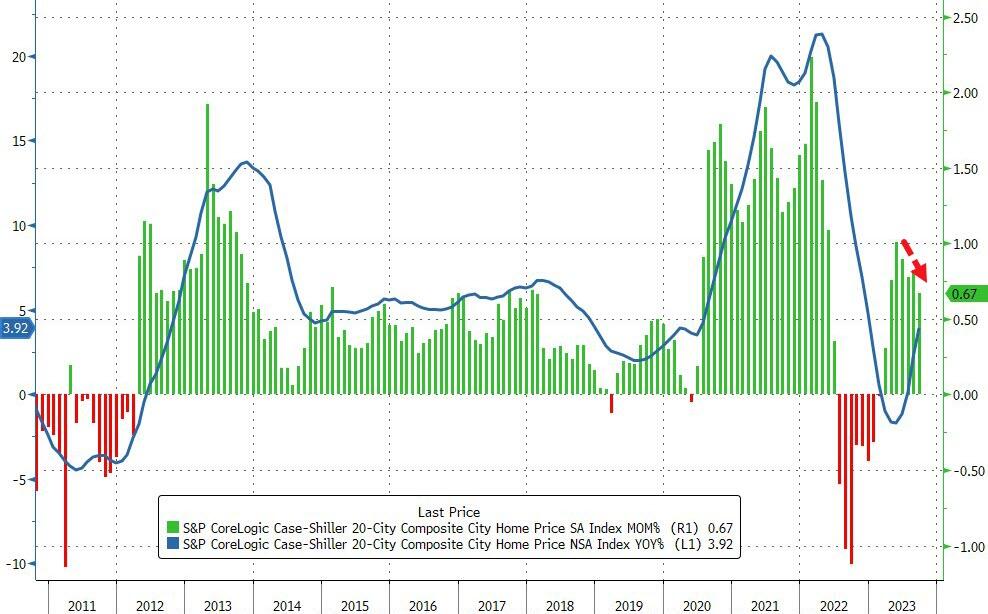

That pushed the YoY rise in prices up 3.92% – the fastest pace since Dec ’22 – but as the chart shows the MoM gains are slowing rapidly.

Source: Bloomberg

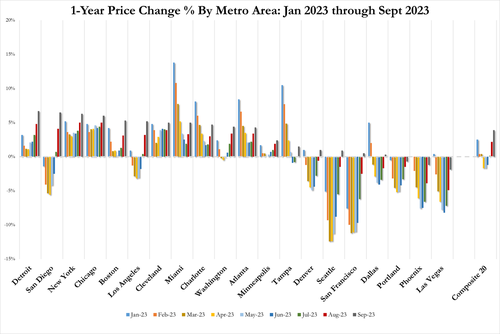

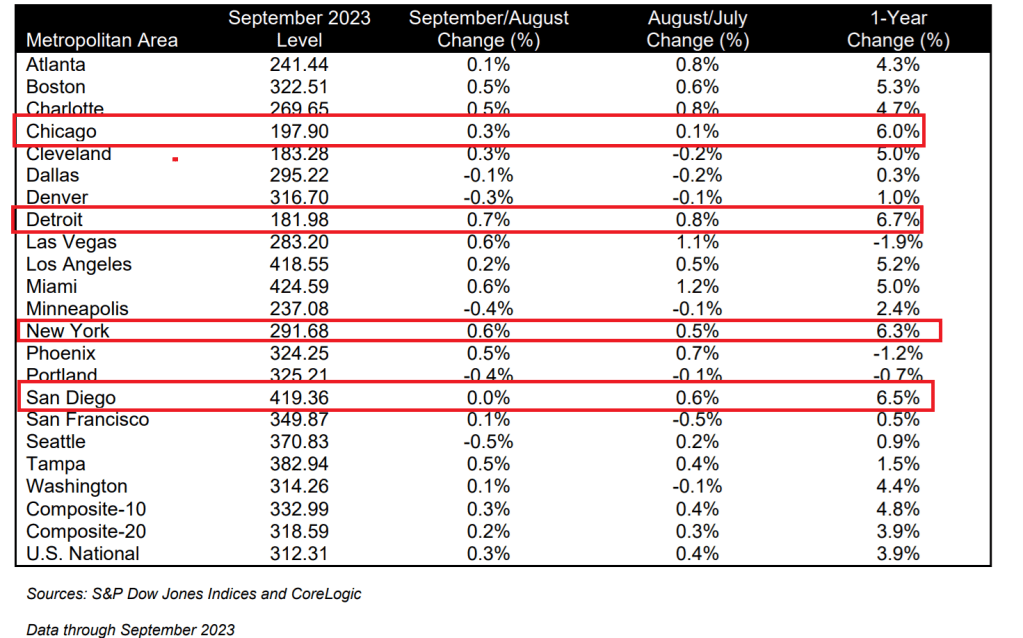

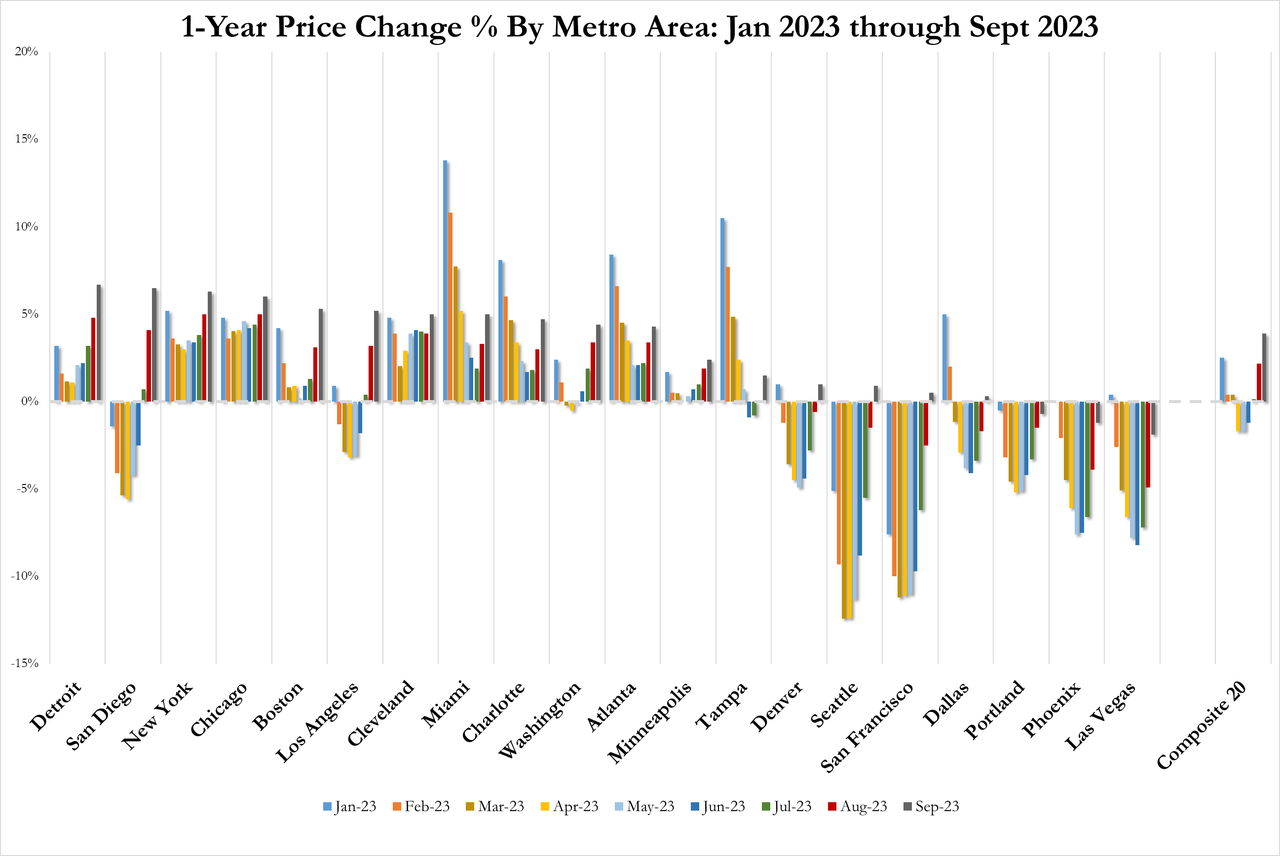

“On a year-over-year basis, the three best-performing metropolitan areas in September were Detroit (+6.7%), San Diego (+6.5%), and New York (+6.3%),” according to Craig J. Lazzara, Managing Director at S&P DJI.

“We’ve commented before on the breadth of the housing market’s strength, which continued to be impressive. On a seasonally adjusted basis, all 20 cities showed price increases in September”

But, judging by the resumption of the rise of mortgage rates since the Case-Shiller data was created, we would expect prices to also resume their decline…

Source: Bloomberg

Inventory is increasing (as homebuilders dump new homes on to the market), but existing home-buyers and -sellers are stuck still (affordability for the former and the mortgage cost gap for the latter), and – despite the market’s hopes – The Fed isn’t cutting rates any time soon (unless the economy utterly collapses). Be careful what you wish for…

Odd that 4 metro areas with 6% or higher home price growth are all cities with larger illegal immigrant migration: Chicago, Detroit, New York and San Diego (all blue cities). This is what is called housing displacement, A surge in immigration leads to rent stock being absorbed and housing prices rising.

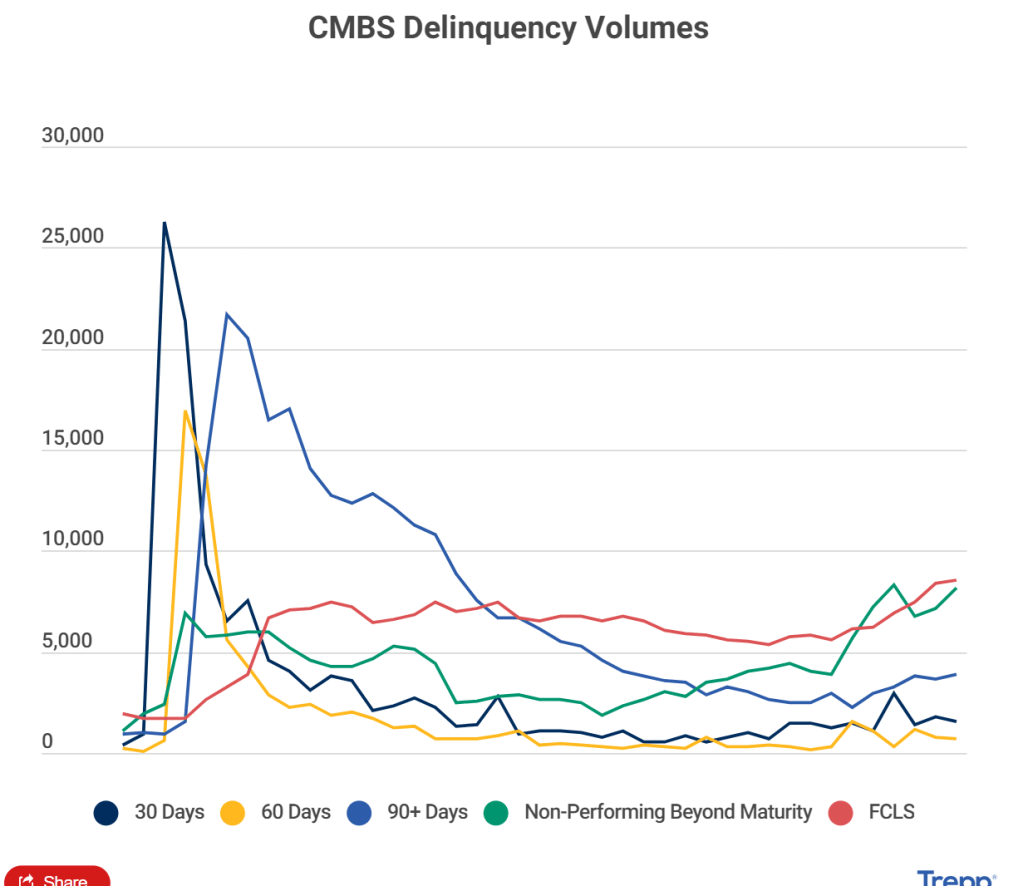

According to Trepp, the volume of CMBS delinquency increased 49.4% during 10 months through October.

Looking for more? This piece has been taken from Trepp and Commercial Real Estate Direct’s Q3 2023 Quarterly Data Review. Access the magazine here.

The volume of CMBS loans that are classified as delinquent increased by 49.4% during the 10 months through October to $27.91 billion. That volume amounts to 5.07% of the $601.98 billion universe tracked by Trepp. In contrast, delinquencies at the end of last year amounted to 3.03% of the $616.15 billion universe then extant.

Office Sector Drives Increase in Delinquency Volumes

The driver of the increase was the office sector, which had a 261% increase in delinquency volumes over the 10-month period through October. A total of 199 loans with a balance of $9.59 billion, or 5.91% of all CMBS office loans were at least 30 days late with their payments, as of the end of October. At the end of last year, 115 loans with a balance of $2.65 billion, or 1.63% of office loans, were delinquent.

The sector’s prospects are unlikely to improve as office occupancy rates have declined in most of the country’s major markets. That’s been driven by a substantial pullback in demand from office-using tenants.

Hit especially hard have been loans with floating coupons that are maturing and need interest-rate cap agreements in place before they qualify for term extensions. Those rate caps have skyrocketed in price in lockstep with interest rates.

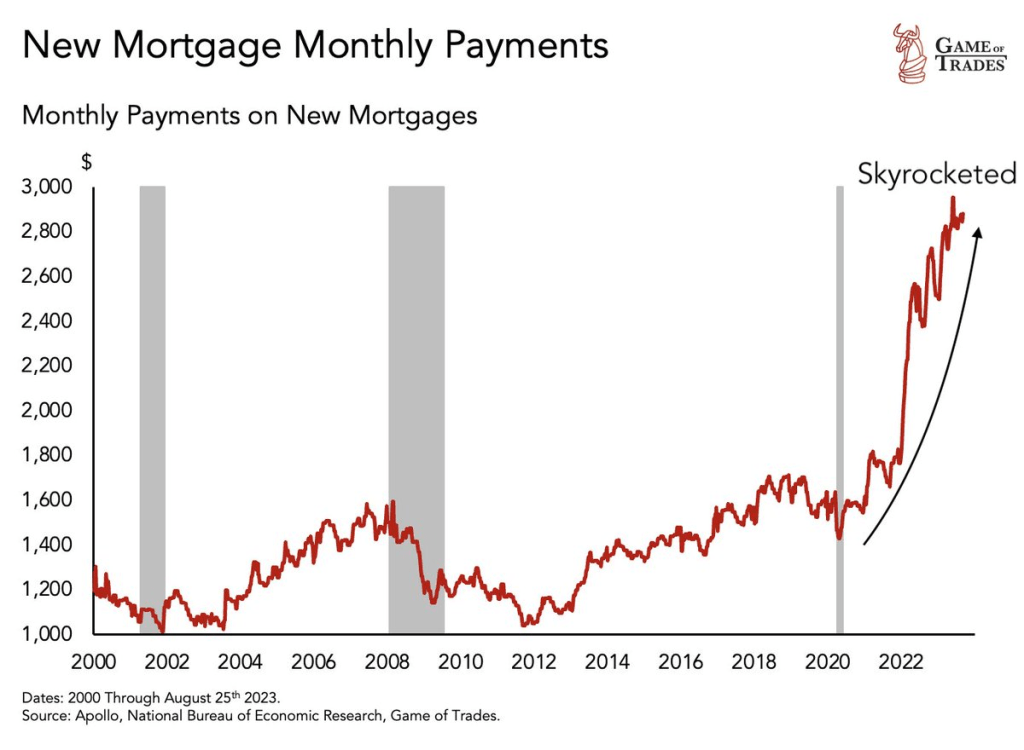

On the residential side, The Fed is helping drive mortgage payments through the roof!

The Federal Reserve reminds me of The Stones’ song “Tumbling Dice.” Why? The Fed can’t tell if inflation is cooling or re-accelerating. Hence, they are just rolling dice.

Let’s start with mortgage rates, a critical component of the housing and CRE markets. Mortgage rates remain up 163% since 2021, not great for housing affordability. Despite recent small declines in the mortgage rate. The 10Y-2Y Treasury curve is also going deeper into reversion … again.

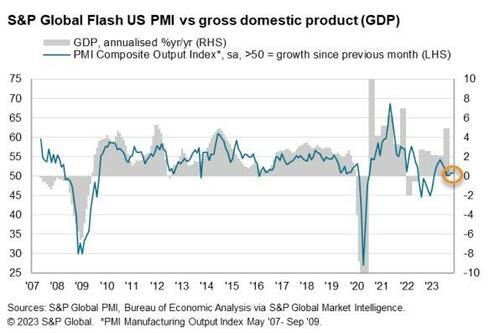

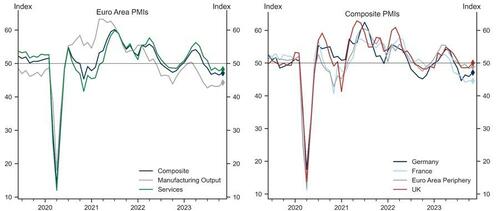

However, the data was more mixed with US Manufacturing falling more than expected to 49.4 – back into contraction – (vs 49.9 exp) from 50.0 in October. However, US Services unexpectedly rose from 50.6 to 50.8 (exp 50.3).

“The US private sector remained in expansionary territory in November, as firms signalled another marginal rise in business activity. Moreover, demand conditions – largely driven by the service sector – improved as new orders returned to growth for the first time in four months.

The upturn was historically subdued, however, amid challenges securing orders as customers remained concerned about global economic uncertainty, muted demand and high interest rates.

Businesses cut employment for the first time in almost three-and-a-half years in response to concerns about the outlook. Job shedding has spread beyond the manufacturing sector, as services firms signalled a renewed drop in staff in November as cost savings were sought.

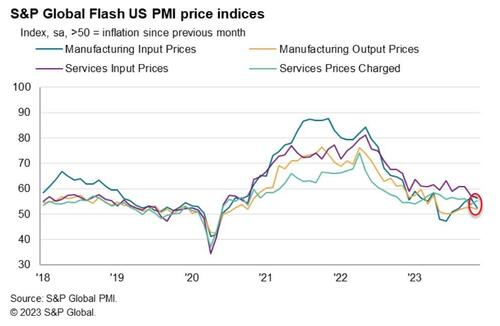

“On a more positive note, input price inflation softened again, with cost burdens rising at the slowest rate in over three years. The impact of hikes in oil prices appear to be dissipating in the manufacturing sector, where the rate of cost inflation slowed notably.

Although ticking up slightly, selling price inflation remained subdued relative to the average over the last three years and was consistent with a rate of increase close to the Fed’s 2% target.”

The US data comes after yesterday’s Euro area composite flash PMI increased by 0.6pt to 47.1, above consensus expectations, driven by a meaningful acceleration in Germany and the periphery, partially offset by a marginal decline in France. In the UK, the composite flash PMI improved meaningfully and entered expansionary territory at 50.1, above consensus expectations, on the back of a pickup in both sectors, with the services sector index entering positive territory at 50.5.

Goldman sees three main takeaways from today’s data.

First, we see a potential turning point in Euro area activity, with forward-looking indicators all improving in November, potentially setting a positive stage for the remainder of the year and the beginning of 2024. While the improvement seems to be broad-based, the upside surprises in the manufacturing sector in Germany and the Euro area as a whole may point to early signs of the sector’s revival.

Second, inflationary pressures, after moderating for some time, show signs of renewed intensification in the Euro area, as reflected by the output and input price components ticking up in November.

Third, UK growth momentum was meaningfully better than last month, and is picking up across the board, with the headline and services indices coming in above 50. This, however, is now accompanied by an increase in cost pressures, with both the input and output price indices edging up in November.

Finally, back to the US, S&P Global found that US business uncertainty was also heightened among US firms, as expectations regarding the year-ahead outlook slipped to the weakest since July.

A record 130.7 million people are expected to shop in stores and online in the U.S. on Black Friday this year, the National Retail Federation (NRF) estimates. The event is known for crowds lining up at big-box stores at dawn to scoop up discounted TVs and home appliances.

But at 6 a.m. on Friday at a Walmart in New Milford, Connecticut, the parking lot was only half full.

“It’s a lot quieter this year, a lot quieter,” said shopper Theresa Forsberg, who visits the same five stores with her family at dawn every Black Friday. She was at a nearby Kohl’s (KSS.N) store at 5 a.m.

Fifth Avenue, one of the world’s top shopping streets, is dead quiet on Black Friday — at least by New York’s boisterous standards.

The strip of high-end shops from brands like Louis Vuitton and Cartier has largely recovered since its pandemic lull, where vacancies had once reached nearly 30% in Midtown East. Some vestiges of that struggle remain, with a few empty storefronts covered up or filled with little art installations. Yet the street has managed to keep its title as the most expensive retail area on the planet by rent per square foot, according to Cushman & Wakefield.

Mortgage rates up 163% since 2021, manufacturing PMI in contraction and Black Friday shopping muted. Not good. The Fed is rolling the dice on what to do next.

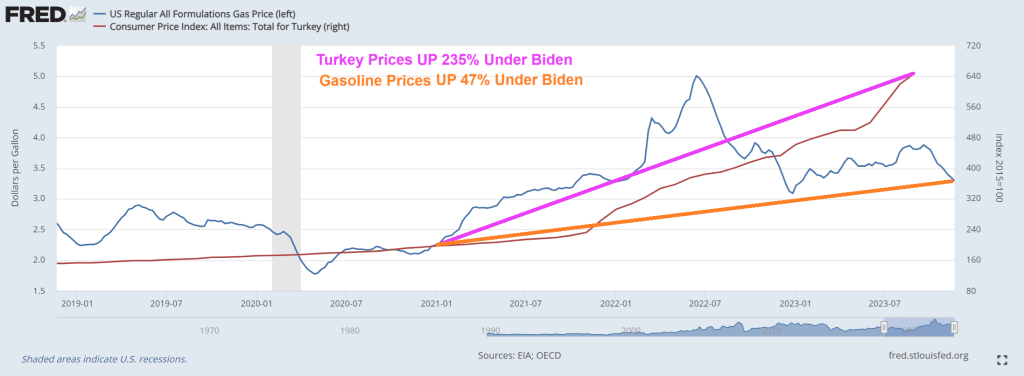

Yes, prices of turkey (that we eat) and gasoline (used to drive to family/friends) have declined a little recently. BUT turkey prices are still up by 235% since Biden was sworn in as President. And gasoline prices are still up 47%. One of Biden’s “economists” came out and said gasoline is now lower than it was in 2020. WRONG! Look at the chart below from The Federal Reserve of St. Louis.

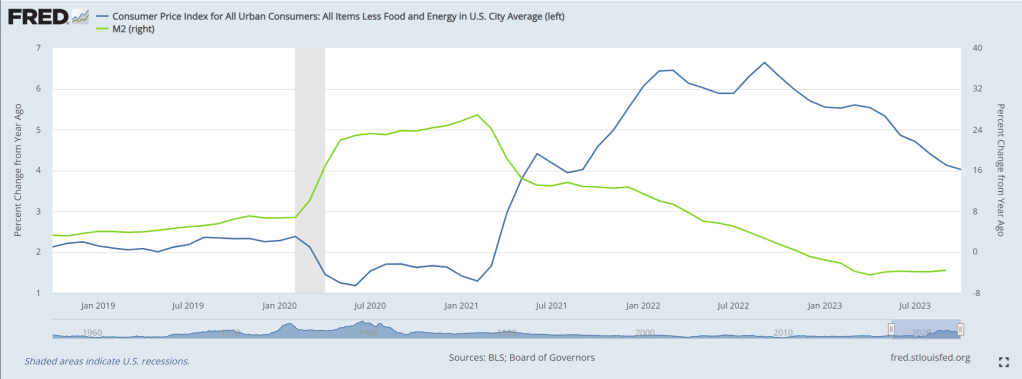

Being politicians, The Biden Administration take credit for RECENTLY declining prices, but failing to mention that declining prices have more to do with declining M2 Money growth (now -3.6% YoY) after the enormous burst in Federal spending with Covid.

With turkey prices up 235% under Biden, I will be eating turkey SPAM tonight. And a small portion at that!

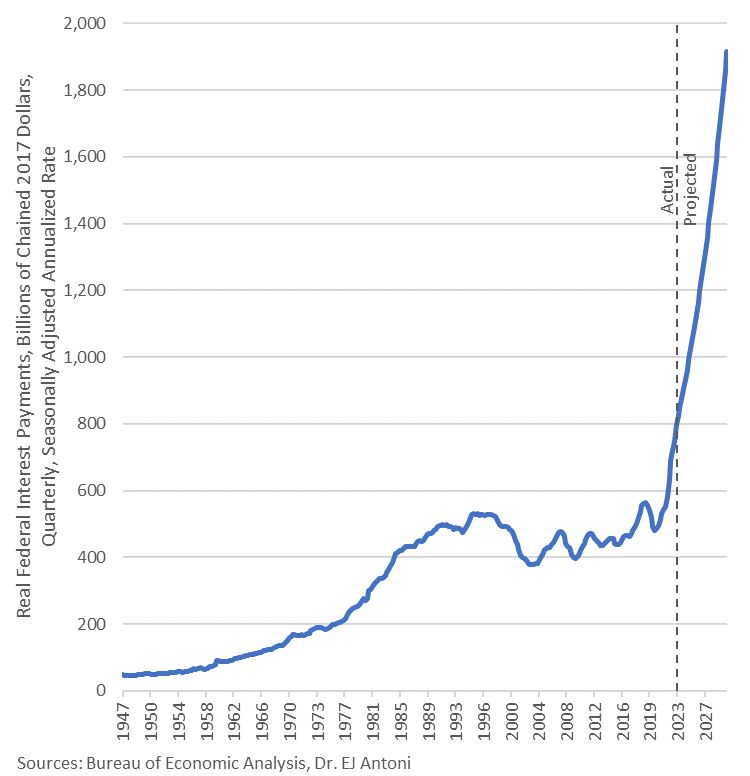

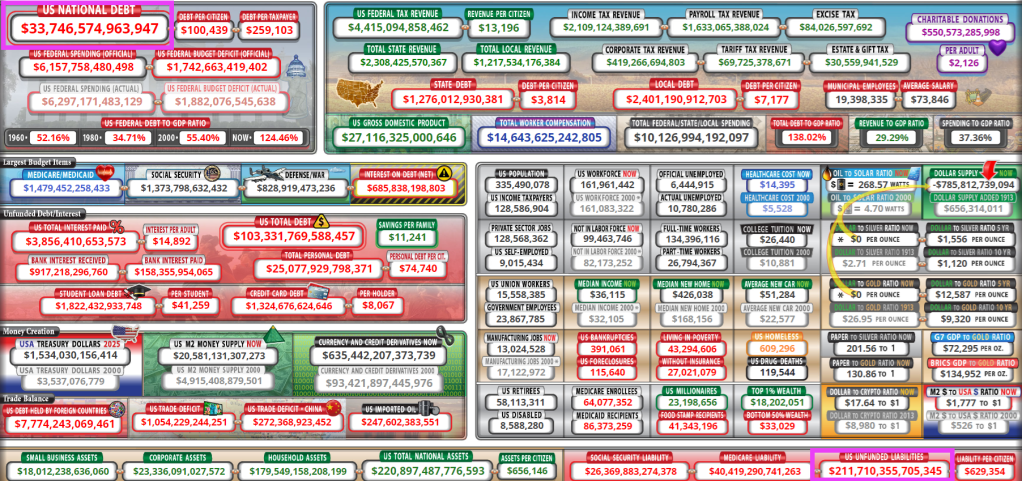

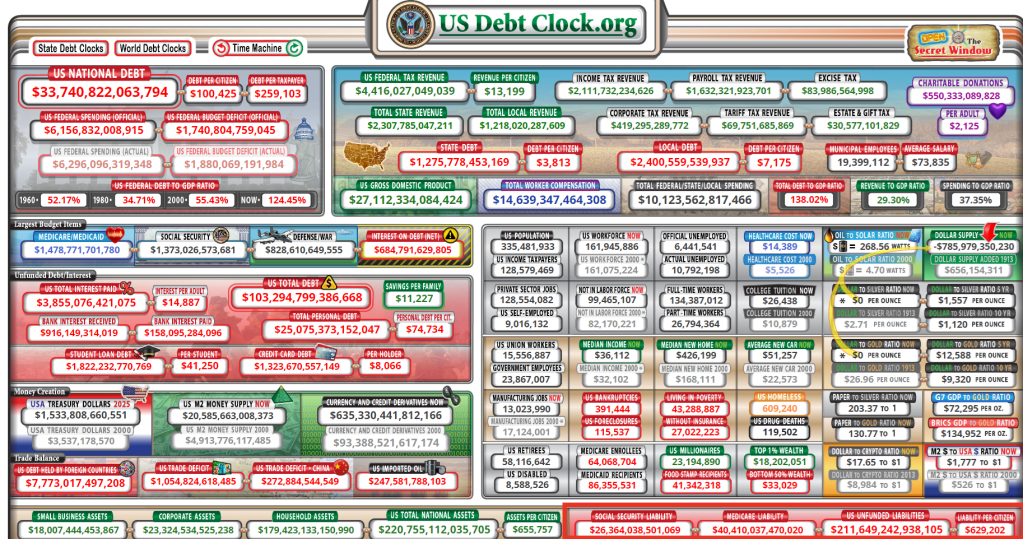

The US is experiencing a fiscal inferno thanks to out of control Federal spending and debt issurace.

The US government collects about $2.5 trillion per year in personal income taxes. Of that about $1 trillion per year (40%) is being consumed by interest on the national debt. REAL Federal interest payments of the debt is skyrocketing!

Interest on the debt is growing as old cheap debt matures and gets refinanced at the new higher rates. Plus new debt added every year.

Within a few more years, at this pace, 100% of personal income taxes will be going to pay interest on the US nationaldebt.

Yes, US national debt is at $33.75 trillion and growing awfully fast. Of course, that is small potatoes compared to the $211.7 TRILLION in unfunded Federal promises (entitlements). That means that unfunded promises are 6.27 times the current national debt. There isn’t enough taxable income from individuals to pay for the promised entitlements.

NY Senator Chuckles Schumer: “We did it Joe! We broke the back of the US economy!”

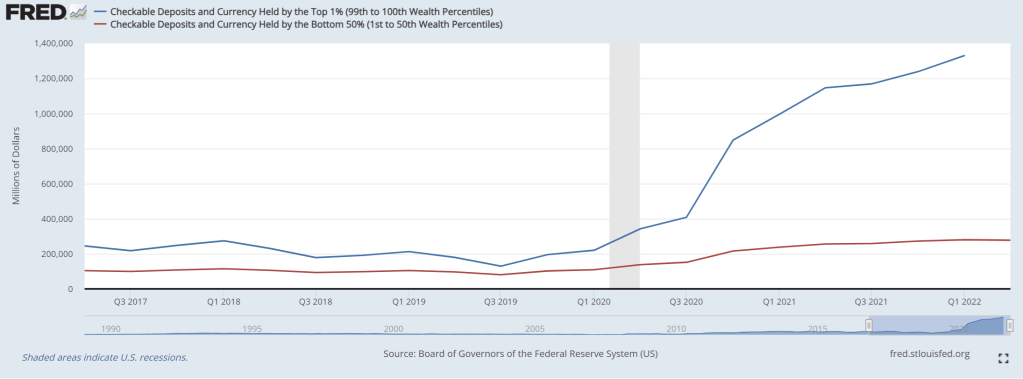

As of June, the bottom 80% of households by income, when adjusted for inflation, had lower bank deposits and other liquid assets compared to their status in March 2020. The decline marks a significant shift from the initial phases of the pandemic, where various factors, including government financial support and restricted spending opportunities during lockdowns, led to an accumulation of excess savings.

In other words, the vast majority of all Americans have been getting poorer.

The Federal Reserve, along with Bloomberg calculations, identified a rapid drawdown of these excess savings, particularly stark among the lower-income groups. While all income groups have experienced a decrease in real-term cash balances from the peak in 2021, the disparity is noteworthy. The wealthiest one-fifth of households still have cash savings approximately 8% above their pre-COVID levels. In stark contrast, the poorest two-fifths have witnessed an 8% decrease, and the next 40% — broadly representing the middle class — have seen their cash savings fall below pre-pandemic levels.

Even checkable deposits and currency held by the top 1% (call it the Kerry Class after multi-millionaire and Statist parasite John Kerry, Biden’s climate “envoy”) are soaring while the bottom 50% are seeing only a tepid rise.

Meanwhile, UMich inflation expectations rose even further intra-month, jumping from 4.4% to 4.5% final (for 1Y inflation outlook) and from 3.1 to 3.2% final (for 5-10Y outlook).

Let’s see if Treasury Secretary Janet Yellen tries to explain once again that Americans just don’t understand how great Bidenomics is.

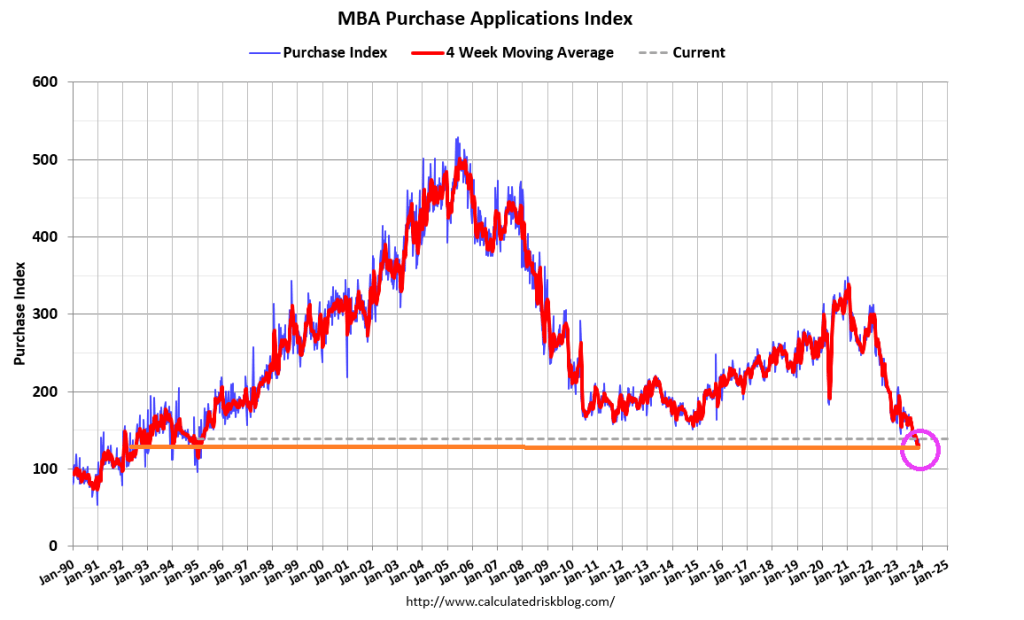

Biden’s economic Dance Macabre! Or Biden’s Mortgage Macabre! Mortgage purchase demand actually fell -1% from the previous week (WoW) and is down -20% from the previous year (YoY).

Mortgage applications increased 3.0 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending November 17, 2023.

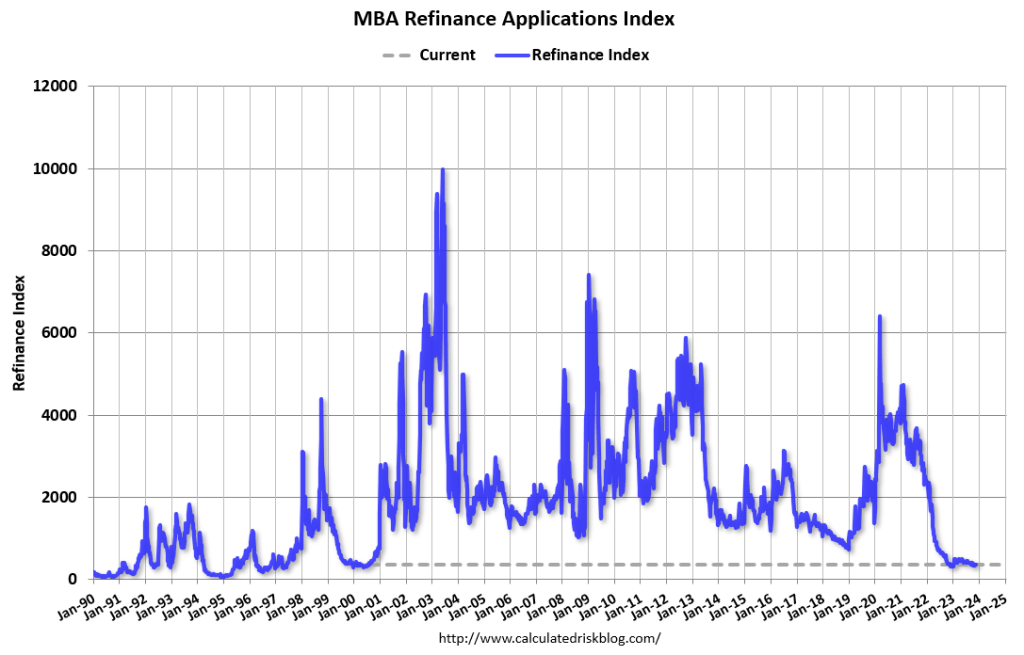

The Market Composite Index, a measure of mortgage loan application volume, increased 3.0 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 0.1 percent compared with the previous week. The Refinance Index increased 2 percent from the previous week and was 4 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 4 percent from one week earlier. The unadjusted Purchase Index decreased 1 percent compared with the previous week and was 20 percent lower than the same week one year ago.

And MBA mortgage refis

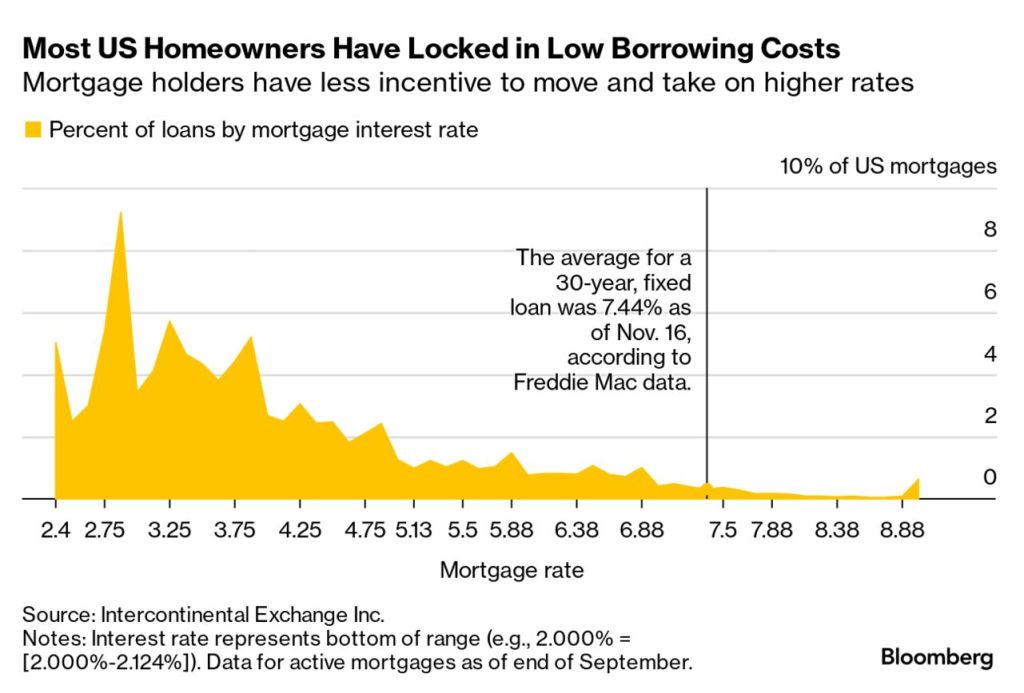

Not surprising since most homeowners have locked in low borrowing costs prior to the Biden/Congress Covid spendathon and the inflation that followed.

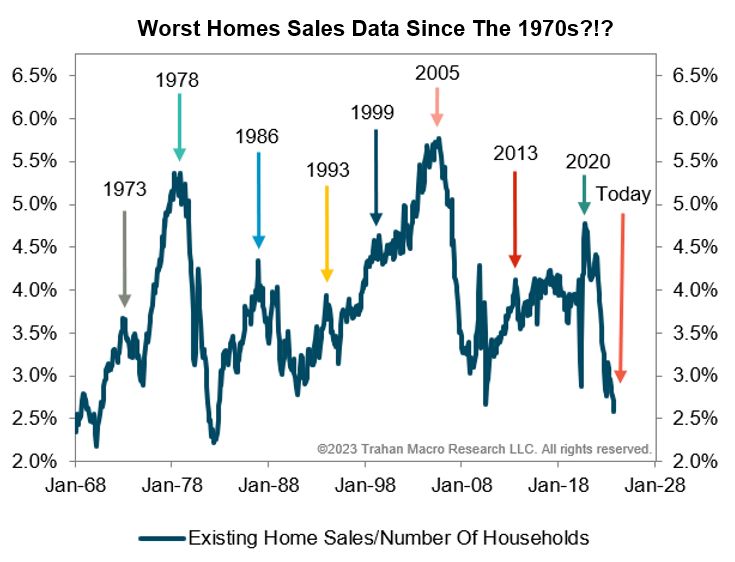

After all, we are seeing the worst home sales data since the 1970s.

Yes, even KJP is finding it difficult to sell Bidenomics to the public (only talking heads like The View and Morning Joe are still trumpeting the greatness of Bidenomics). And now KJP and the Administration are selling Biden’s age of 81 as a treasure trove of experience. Except that Biden’s record in the Senate is an embarrasment. And Biden keeps shuffling and falling and mumbling through his speeches. Watch Biden’s handlers make sure he doesn’t fall again before the election.

Even Biden’s press secretary Karine Jean Pierre admitted that all the slogans and hype about Bidenomics is a losing message. The economy is terrible for the middle class and low-wage workers. But excellent for the 1% donor and political elite class. But housing is very important to the middle class … and housing is simply unaffordable.

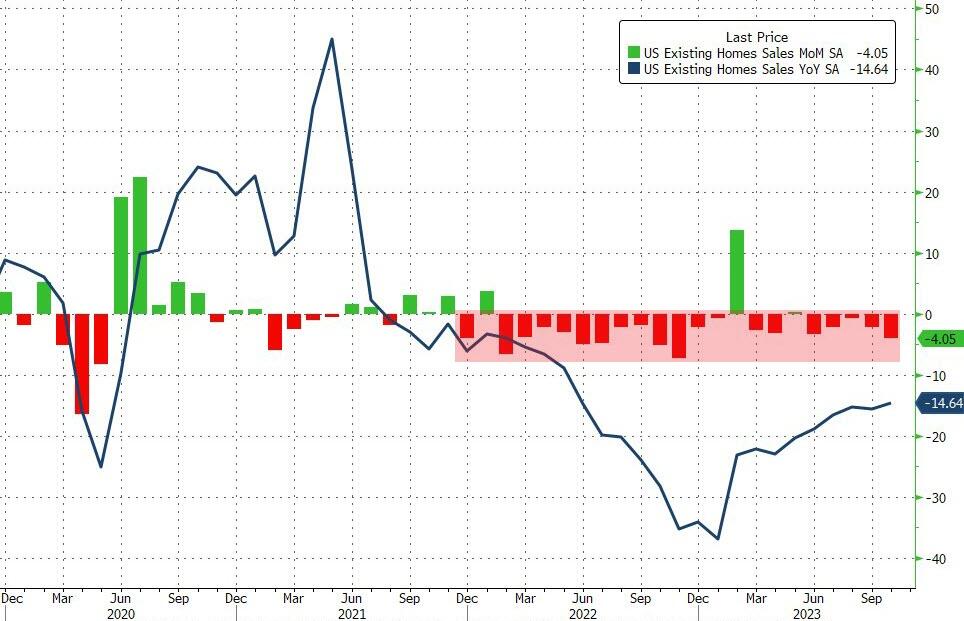

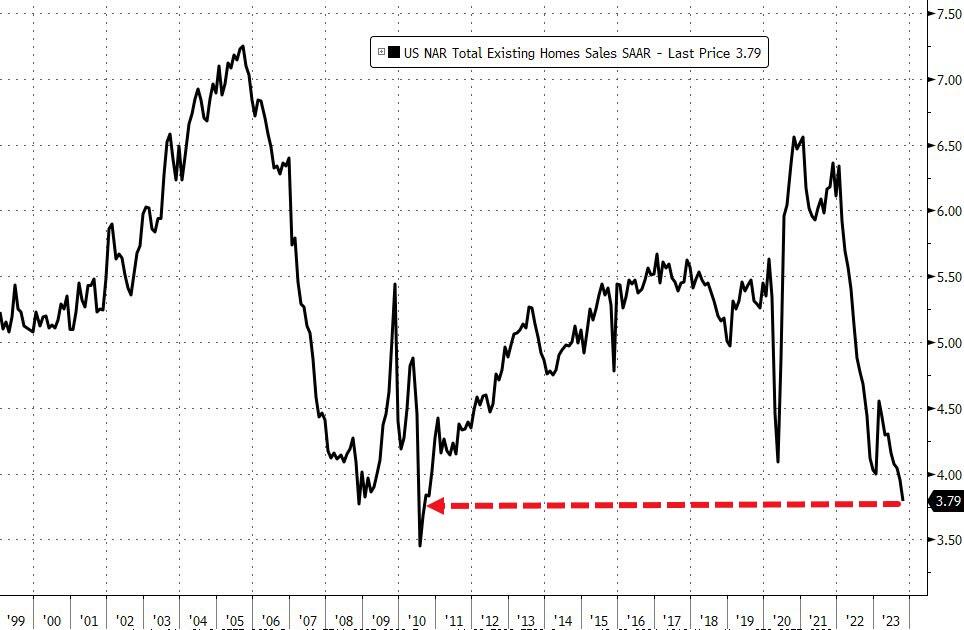

With housing affordability at its lowest since at least the early 1980s, (and homebuilder sentiment slumping as mortgage rates rose), it’s no surprise that analysts expected existing home sales in October to tumble 1.5% MoM.

Sales actually fell 4.1% MoM (far worse than expected and down for the 20th time in the last 23 months) with September’s 2.0% MoM decline revised even lower to -2.2% MoM. That decline left existing home sales down 14.6% YoY.

Source: Bloomberg

The total existing home sales SAAR plunged to 3.79mm – the lowest since the tax credit expired in Aug 2010…

Source: Bloomberg

Sales fell in three of four regions, while they were unchanged in the Midwest. They hit a record low in the West and matched an all-time low in the Northeast

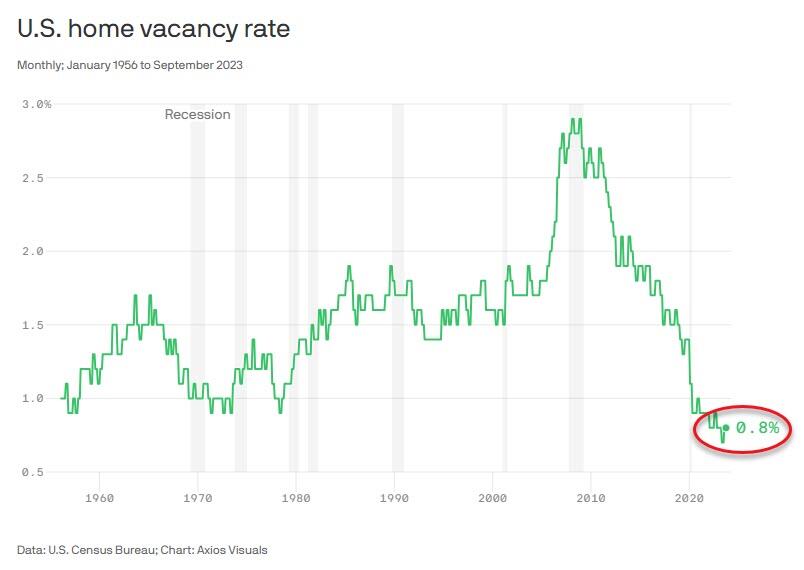

Finally, the percentage of homes that are vacant fell to the lowest level on record in August, and ticked up only slightly in September…

Ever the optimistic,Lawrence Yun, NAR’s chief economist, suggested that:

“Fortunately, mortgage rates have fallen for the third straight week, stirring up buying interest,” adding “though limited now, expect housing inventory to improve after this winter and heading into the spring.”

Good luck with that idea Larry!

Yun added that nearly a third of homes sold above their list price, indicating that multiple offers are still occurring with the median selling price climbed 3.4% from a year earlier to $391,800, the highest for any October in data back to 1999.

Even though the number of homes for sale ticked up from a month earlier to 1.15 million, it’s still the lowest for any October in the series.

Finally, first-time buyers made up a historically low 28% of purchases in October.

After all, the US economy and housing markets are addicted to goverment. (Addicted To Gov!)

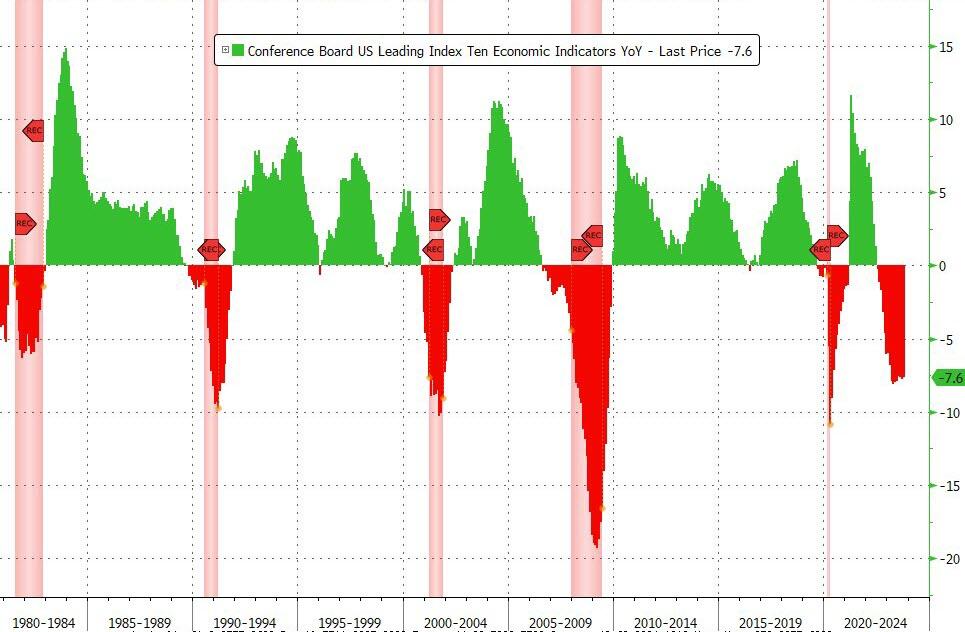

Bidenomics is the economy’s Highway to Hell! Massive, staggering misallocation of scare resources to fund endless wars, green energy fraud, and massive wealth transfers to immigrants while disabled veterans suffer. Now we see that the US leading economic indicators is down -7.6%, definitely smelling like a recession.

On a year-over-year (YoY) basis, the Leading Economic Indicators is down 7.6% (down YoY for 16 straight months) – close to its biggest YoY drop since 2008 (Lehman) outside of the COVID lockdown-enforced collapse.

On a monthly basis (MoM), leading economics indicators are down -0.8%. It has been going down for 16 straight months. Here are the components.

Most of the components are in red and need to be back in black for economic growth.

Treasury Secretary Janet Yellen, a mega pro-China elitist, acknowledges that Bidenomics isn’t popular but she attributes that to people not understanding how good Bidenomics is! It is good for the 1% elitist, donor class. But not for the US middle class.

At least Argentina elected AC/DC guitarist Angus Young as President!

Rubino says, “If the U.S. government is running crisis level deficits, which it is right now, borrowing money and paying interest on it means we are in a financial death spiral…”

“The debt goes up, the interest on the debt goes up and that raises the debt even further, and you just spiral out of control.

We are there right now. The official U.S. debt is $33.5 trillion. It’s growing by $1.7 trillion a year, and $1 trillion of that is interest costs.

Interest costs are rising as the overall debt goes up. Then throw in this incredibly reckless military spending in the guise of foreign aid, and you get a society that has completely lost control.

That’s where we are now.

We are in the blowoff stage of a 70-year credit super-cycle.

Those things do not end with a whimper, and they certainly do not end with a soft landing. They end with a bang, and the bang is going to be centered on the currency.

People are going to look at this and say, ‘Do I really want to hold the currency or bonds of a country that is destroying its finances at this trajectory and this scale?’ The answer will be ‘No.’

At that point, it is game over for a deeply indebted economy. We are headed that way fast, and these wars are taking us that way even faster.”

If the Fed keeps raising interest rates, the economy tanks, but you protect the dollar. If you cut interest rates, you spike inflation even more, and the U.S. dollar tanks.

Rubino says in the end, we get a “massive reset,” and the everything bubble explodes.

Rubino says the dollar is going to decline and, at some point, it starts to go into freefall in terms of buying power. Rubino explains,

“If a currency starts to decline in a disorderly way, then you have a massive financial crisis on your hands.

That is definitely where Japan is right now. The U.S. is headed that way fast.

So, once we reach that point, there is no fix.

Then it is only a matter of time that everybody realizes that there is no fix, and they just bail on the whole experiment, and that’s where we are headed.”

Rubino talks about plunging home prices, more trouble coming in the commercial real estate market and why you need gold and silver as core assets during a currency reset.

Riots, already happening in American cities (not to mention looting in New York City, Chicago, San Francisco and Los Angeles), will accelerate if Congress attempts to curtail entitlements (now at $211.65 TRILLION).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.