Both The Federal government and Federal Reserve went wild with stimulus surrounding the Covid economic shutdown in 2020. The excessive reaction function is still working its way through the economy and we finally got Q2 Real GDP QoQ of 2.4%! But seriously, is that all we got from an increase in public debt of 39% since January 2020, and M2 Money increased 36%. And, of course, The Federal Reserve double their balance sheet from 2020 to today … and are slow walking its removal. So, with Biden’s insane green spending and Powell’s monetary stimulytpo, all we got was 2.1% Real GDP growth YoY??

And US public debt to GDP is now over 120%, thanks in part to Federal spending and Fed monetary stimulus related to the Covid economic shutdowns.

New home sales in June fell -2.5% from May to June to 697k units sold. But on a year-over-year (YoY) basis, new home sales are up 23.8%. Thanks largely to The Federal Reserve slow walking the shrinking of their massive balance sheet.

Too much monetary stimulus and The Fed’s failure to remove the Covid stimulus is now hitting new home sales.

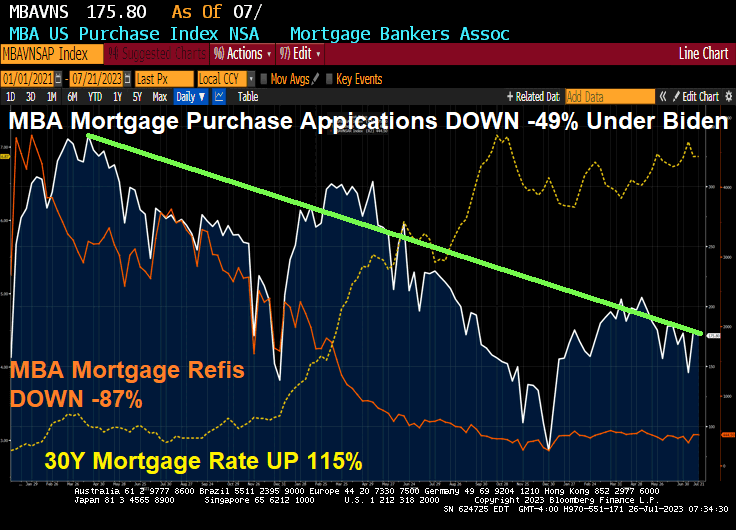

Mortgage applications decreased 1.8 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending July 21, 2023.

The Market Composite Index, a measure of mortgage loan application volume, decreased 1.8 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index 1.5 percent compared with the previous week. The Refinance Index decreased 0.4 percent from the previous week and was 30 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 3 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 23 percent lower than the same week one year ago.

Since April 2021, purchase mortgage demand is down -49%, refi mortgage demand is down -87% as mortgage rates are up 115%.

Biden Press Secretary KARINE JEAN-PIERRE: “The American people are beginning to feel Bidenomics”

Prices are up 16.6% and real wages are down 3% since Biden took office.

Well, at least Jean-Pierre didn’t claim like her boss Joe Biden claimed that he “ended cancer as we know it.”

But getting back to Jean-Pierre’s claim that “The American people are beginning to feel Bidenomics.” She is right (for once). Americans are REALLY feeling Bidenomics. And it hurts SO BAD!!!

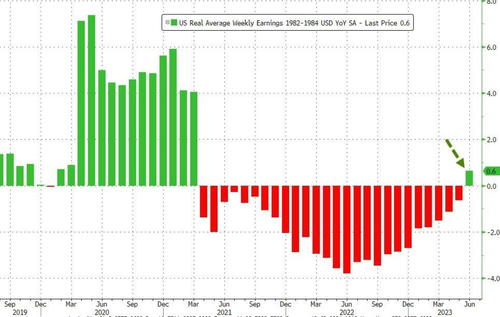

What hurts so bad? Food (CRB Foodstuffs) are up 56% under Bidenomics. Real weekly wage growth is down -90% since Biden assumed office. Regular gas prices are up 52%. And the 30Y mortgage rate is up a staggering 153%. Yes, Karine, this hurts so bad!

While real wages are down -3% under Biden and the real average weekly wage growth is down -90%. That REALLY hurts so good.

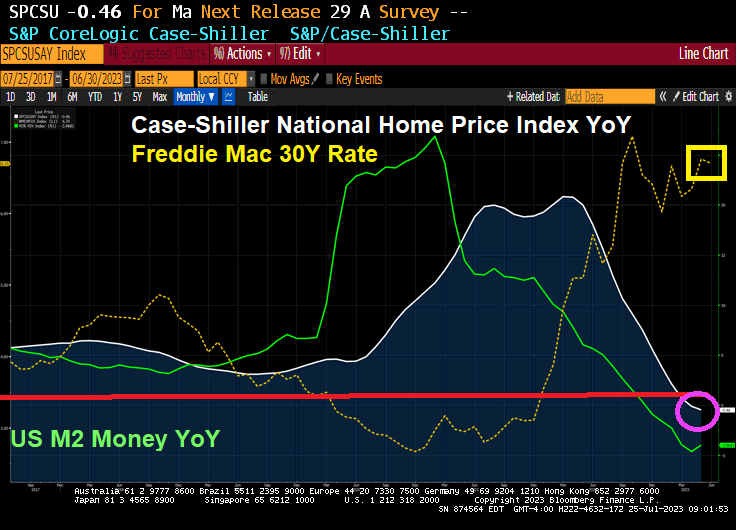

The Case-Shiller home price numbers are out for May. The national home price index is down -0.46% YoY as The Fed slows M2 Money growth into negative growth territory. No doubt Biden (and Karine Jean-Pierre) will take credit for slowing home price growth, although The Federal Reserve slowing monetary stimulus is mostly responsible.

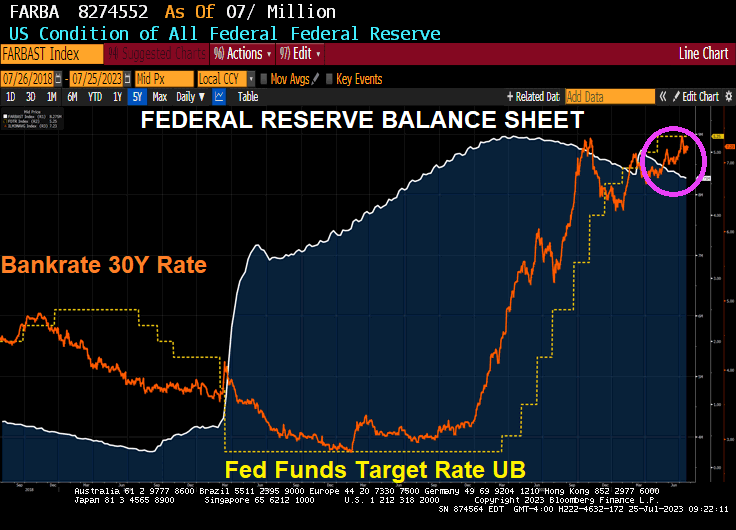

The Fed is still slow walking shrinking its enormous balance sheet. Although The Fed is cranking up their target rate.

The Taylor Rule suggests a 10.42 target rate to cool inflation. They are only half way there!!!

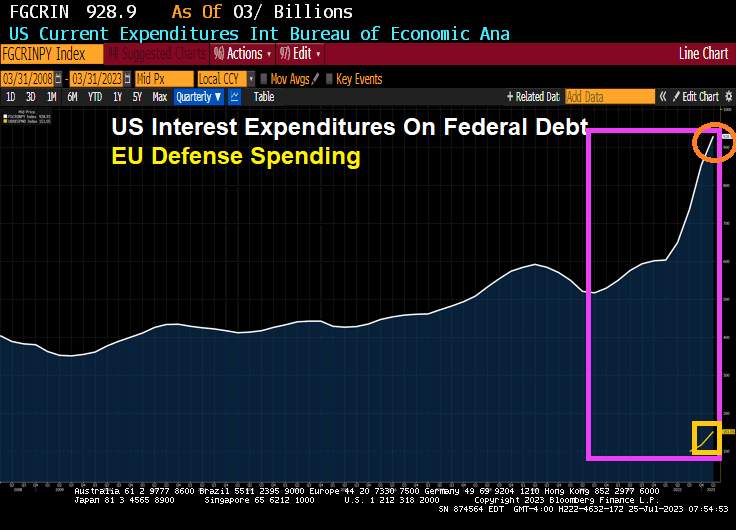

How badly has Bidenomics and generally Federal spending has crippled the US? An example. The interest on US Federal debt is approaching $1 TRILLION (and Biden/Democrats REFUSE to cut any spending, not that Republicans are much better). To show up how messed up this is, the EU’s defense budget (remember Ukraine?) is far smaller that the US interest payments on their debt. That is, US interest payments alone on the massive Federal debt of over $32 trillion is over 6 times larger than the entire defense budget for the European Union!

How this all works, considering the nation’s technically insolvent, is quite miraculous. But it works, nonetheless. Again and again, the Treasury borrows money. And Washington spends it.

Yellen likely knows that full faith and credit is too good to be true. The U.S. government’s gross fiscal mismanagement should call the veracity of its notes into question. But why focus on it when there’s an abundance to be acquired from weekly Treasury bill auctions?

On a recent trip to China, Yellen was spotted by a local food blogger consuming a plate of magic mushrooms. An aide to Yellen later confirmed that she did, indeed, order them. The restaurant’s “staff said she loved [the] mushrooms very much. It was an extremely magical day.”

We don’t know what their acute effects on Yellen were, while she was in Beijing. But the mushrooms appear to be contributing to her chronic hallucinations about the U.S. economy’s current health. This week, for example, while attending the G20 meeting in India, Yellen remarked:

“For the United States, growth has slowed, but our labor market continues to be quite strong. I don’t expect a recession. The most recent inflation data were quite encouraging.”

These, no doubt, are the fantasies of a person under the influence of mind-altering chemicals. Either that, or her mind has turned soft over decades of working as a professional economist for the Federal Reserve and the Treasury.

Tempered Perspective

The unemployment rate reported by the Bureau of Labor Statistics (BLS) is, in fact, just 3.6 percent. Yellen can celebrate the data point. But the quality of the jobs being created is not the type that will drive economic growth.

Higher-paying technology and finance jobs are being purged. While leisure, hospitality, and government are the sectors contributing to employment growth. These jobs may be important. Still, they will not create new wealth or help America compete with its global rivals.

Yellen, while under the influence, also remarked that she doesn’t expect a recession. Maybe this is why you should expect one.

Her predictive acumen has missed the target in the past. If you recall, in 2017 she said she did not believe another financial crisis would happen in our lifetime. Since then, we’ve had one financial crisis after another, including the most recent bank failures this spring.

Just this week, Bank of America reported its bond losses in the second quarter increased $7 billion to nearly $106 billion. And Starwood Capital Group just defaulted on a $215.5 million mortgage on an Atlanta office tower. Probably nothing to worry about, right?

In addition, this week Taiwan Semiconductor Manufacturing Company (TSMC), the mega chip maker, reported its first profit drop in 4 years. Revenue slipped 10 percent from a year ago. What’s more, net income fell 23.3 percent. Wasn’t AI supposed to drive silicon wafer production to commanding heights?

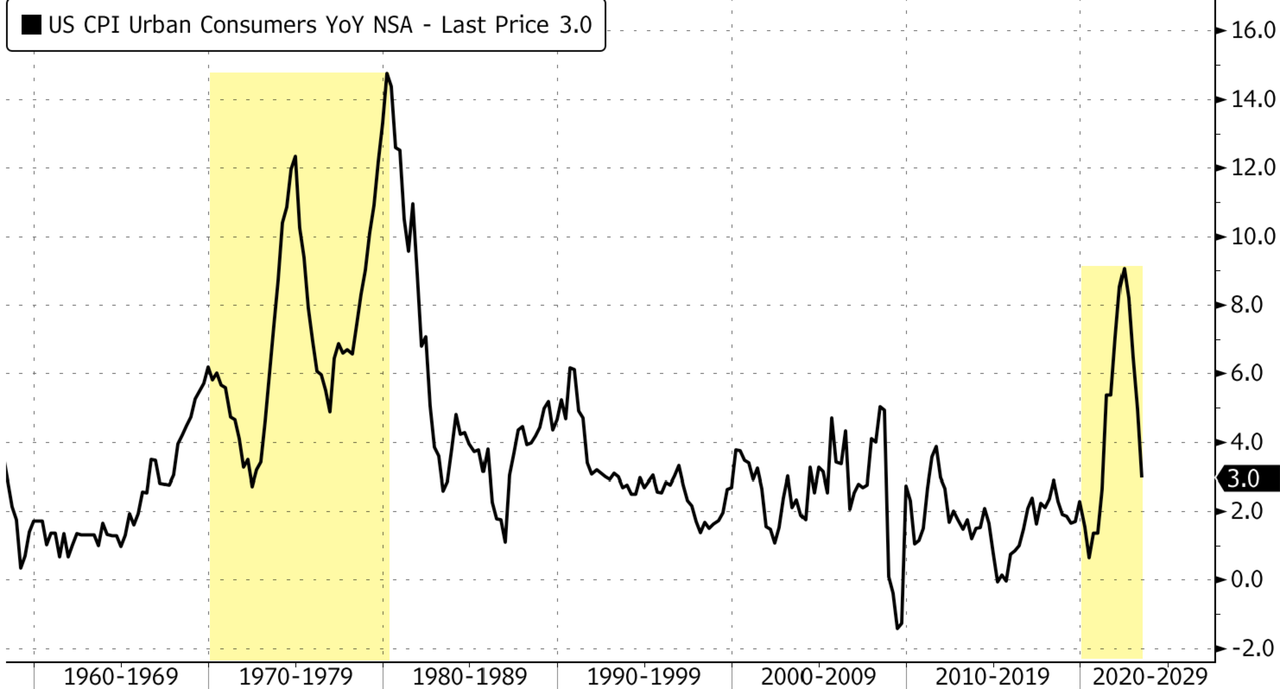

With respect to what Yellen called ‘encouraging inflation data’. While under the influence, she was likely referring to the recent CPI report from the BLS, which showed that in June, consumer prices increased at an annualized rate of 3 percent. This is still 50 percent higher than the Fed’s arbitrary inflation target.

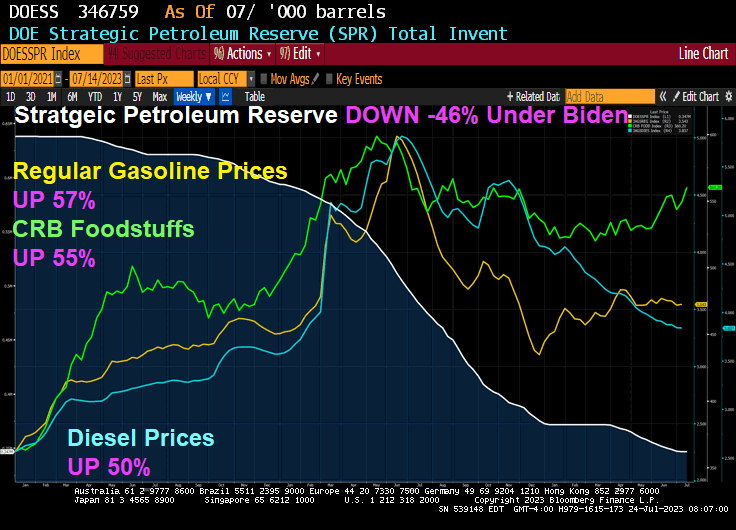

Moreover, the energy commodities component showed a 16.7 percent price decline over the last year. This has coincided with President Biden draining the Strategic Petroleum Reserve to a 40-year low. Without these short-sighted actions, the current inflation data would be much less encouraging.

Structural Crisis

In short, the U.S. economy’s prospects do not quite align with Yellen’s positive outlook. And if you look out further than just the current data reports, you’ll be greeted with a structural crisis of significant consequence.

In fact, simple arithmetic quickly reveals the precarious predicament the 118th Congress is putting the American people in.

The Treasury Department, the agency Yellen oversees, recently reported that for the first 9 months of the 2023 fiscal year, the federal government ran a budget deficit of nearly $1.4 trillion. That’s a 170 percent increase from the same period last year.

The big surprise, however, was that interest on Treasury debt securities for the first 9 months of FY2023 topped $652 billion. A 25 percent increase for this period a year ago.

Rapid and repeated interest rate hikes by the Fed to contain the raging price inflation of its own making, has blown out the interest owed on Treasury debt. Anyone with half an inkling knew this was coming from miles away.

The growth of federal debt has been out of control for decades. But the rate of debt growth in the 21st century has rapidly accelerated.

The solution that’s commonly offered by the politicians for getting a handle on Washington’s debt problem is for the economy to somehow grow its way out. Countless policies over the years have generally involved borrowing money from the future and spending it today.

Yet economic growth never manages to outpace the debt increases. Instead, the debt piles up higher and higher with each passing year. The simple fact is you can’t grow your way out of debt when the debt’s increasing faster than gross domestic product (GDP).

For example, in 2000 the federal debt was about $5.6 trillion, and U.S. GDP was about $10 trillion. Today, the federal debt is over $32.5 trillion, and GDP is about $26.5 trillion. In just 23 years the federal debt has increased by over 480 percent while GDP has increased just 165 percent.

How Washington Ruined America’s Future

Recently, the Peter G. Peterson Foundation attempted to characterize the $32 trillion federal debt. The number is so large it is difficult to comprehend. Here is some of what the foundation came up with:

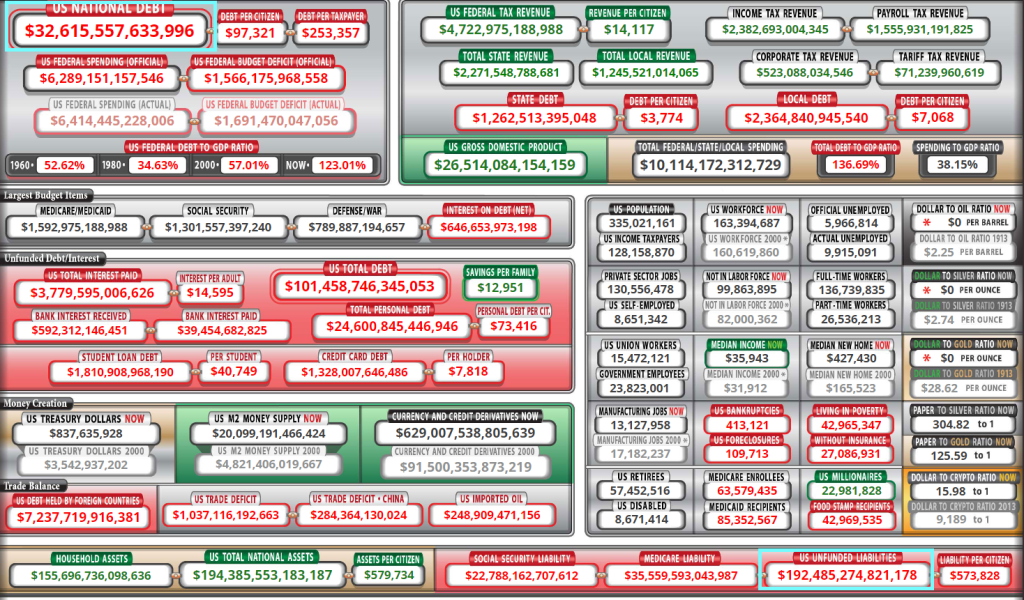

The $32 trillion debt is more than the combined values of the economies of China, Japan, Germany, and the United Kingdom. It represents $244,000 per household or $96,000 per person in America. And if every household contributed $1,000 per month towards paying down the national debt it would take over 20 years.

Without question, Washington has run up an impossible tab. Yet, what does it have to show for all this recklessness?

America’s cities are decaying from the inside out. The infrastructure is crumbling. The country has been involved in one overseas quagmire after another. And the populace is struggling with gender identification pronouns.

The political will to stop this massive debt pileup has been nonexistent. Democrats and Republicans have both spent like drunken sailors. There’s been no tradeoffs or compromises to cut spending. There’s been zero effort to balance the budget. And now it’s too late.

As mentioned above, interest on Treasury debt securities for the first 9 months of FY2023 topped $652 billion – a 25 percent increase from a year ago. But this is just the beginning.

As interest rates continue to rise, the annual interest on Treasury debt will soon pass $1 trillion. That would put this line item at par with outlays for Social Security, the U.S. government’s largest expenditure.

This would also put spending on interest payments above the combined spending of research and development, infrastructure, and education.

Consequently, by repeatedly borrowing and spending money, piling up massive debt, and then being forced to jack up interest rates, Washington has ruined America’s future.

Yippee! Look Ma, no hands! The face of America decline: Former Fed Chair Janet “Too Low For Too Long” Yellen who is now our woefully inept Treasury Secretary. You know, the Treasury Secretary who bowed three times to a Chinese Communist Party leader.

A reminder of the pickle that our politicians have put us in. US Federal debt is at $32.62 TRILLION … and UNFUNDED LIABILITIES (Social Security, Medicare, Medicaid, etc) are at $192.5 TRILLION!!! Yes, the US economy is broken beyond hope of repair, yet dunce voters keep reelecting imbeciles like Joe Biden, Chuck Schumer, John McConnell, etc.

Starwood Capital Group’s Barry Sternlicht recently told Bloomberg’s David Rubenstein about the ongoing crisis in the commercial real estate sector, equating it to a severe “Category 5 hurricane“. He cautioned, “It’s sort of a blackout hovering over the entire industry until we get some relief or some understanding of what the Fed’s going to do over the longer term.”

Currently, the biggest problem in the CRE space is sliding office and retail demand in downtown areas. Couple that with high-interest rates, and there’s a disaster lurking for building owners. According to Morgan Stanley, the elephant in the room is a massive debt maturity wall of CRE loans that totals $500 billion in 2024 and $2.5 trillion over the next five years.

Senior markets editor for Bloomberg, Michael Regan, chatted with John Fish, who is head of the construction firm Suffolk, chair of the Real Estate Roundtable think tank and former chairman of the board of the Federal Reserve Bank of Boston, in the What Goes Up podcast to discuss the biggest problems in the CRE market.

Fish warned that “capital markets nationally have frozen” and “nobody understands value.” He said, “We can’t evaluate price discovery because very few assets have traded during this period of time. Nobody understands where the bottom is.”

For a sense of recent price discovery trends, we were the first to point out to readers of a wicked firesale of office towers in the downtown area of Baltimore City:

As for the overall CRE industry, Goldman Sachs chief credit strategist Lotfi Karoui recently told clients, “The most accurate portrayal of current market conditions with Green Street indicating a 25% year-over-year drop in office property values.”

Sooooo, Powell and The Fed will likely raise rates this week. And maybe a few more times over the next few months. And The Fed remains defiant about taking away the Covid monetary stimulus.

Jared Bernstein was VP Joe Biden’s former Chief Economist and is now chair of the United States Council of Economic Advisers. Pretty impressive! Except that Bernstein is not really an economist. He has a PhD in social welfare from Columbia University. In other words, Bernstein is a Progressive Marxist cheerleader, not a real economist. Perfect for The Biden Adminstration where they installed a small town Mayor with no experience (Buttigieg) as Transportation Secretary.

BERNSTEIN: “Yes, it depends on what your benchmark is.”

Bernstein’s answer reminds me of the infamous reply of President Clinton about having sex in the Oval Office with Monica Lewinsky: “It depends on what the definition of sex is.”

Well, Jared, here is the data.

Since January 2021, regular gasoline prices are up 57% under Biden’s and Bernstein’s Reigns of Error. CRB Foodstuffs are up 55% under Clueless Joe and Diesel prices 50% under Bully Biden. Meanwhile, the Strategic Petroleum Reserves is DOWN -46% under Hidin’ Biden.

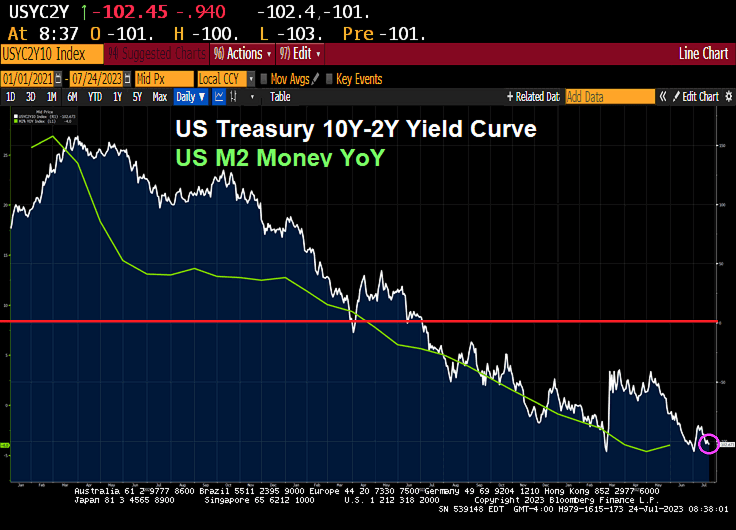

Meanwhile, the US Treasury 10Y-2Y yield curve has inverted to -102.45 as it does prior to a recession. I would love to hear “economist” Jared Bernstein explain that!

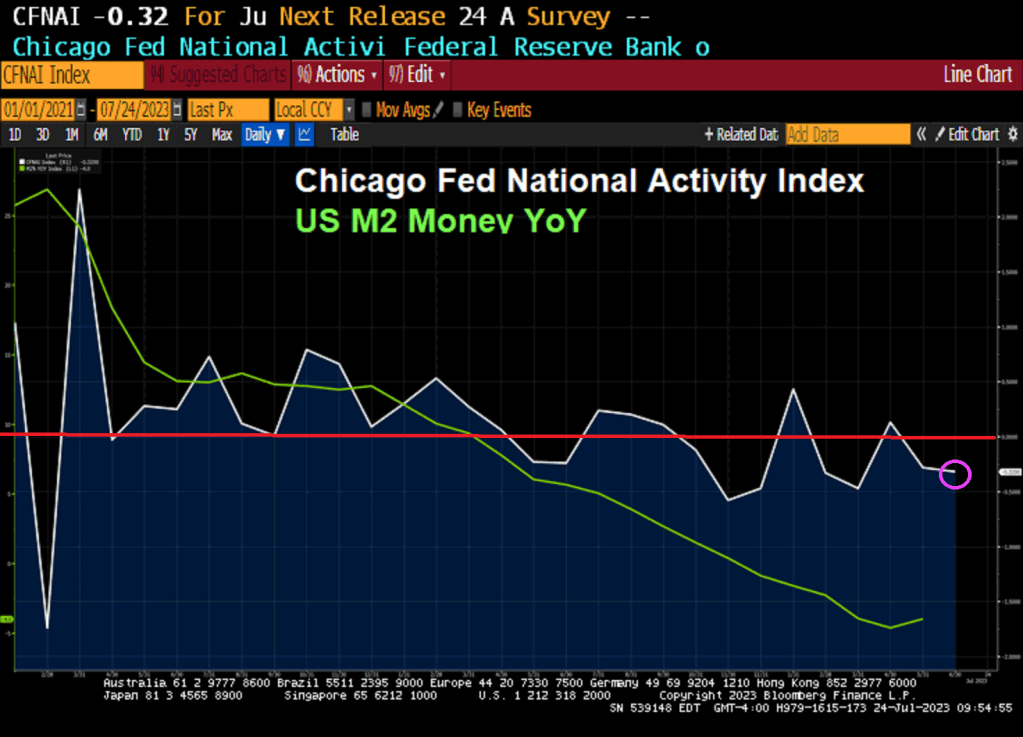

The Chicago Fed’s National Activity index fell to -0.32 in June. That is negative readings for 6 of the last 8 months.

The Fed still hasn’t removed its monetary stimulypto from the market.

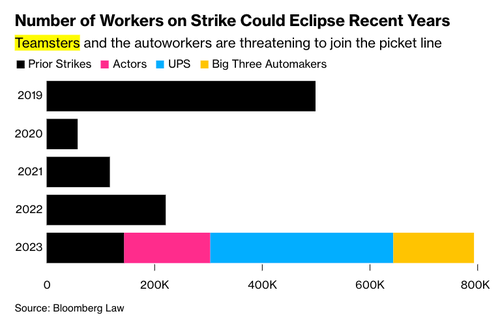

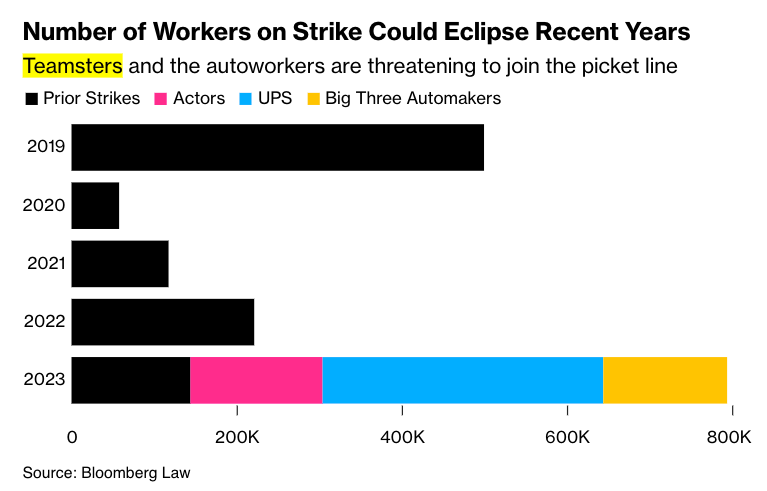

Joe Biden loves to tout “Bidenomics” which is a top-down command economy model with massive Federal spending directed primarily at green energy. But remember that a pillar of Bidenomics is support for labor unions. But “Union Joe” will be remembered as “Inflation Joe” as inflation remains hot. But now the labor unions are threatening to stall the recent rise in real weekly earnings (finally above 0%!).

So why is 2023 shaping up to be one of the biggest years of strikes in the US since the 1970s? Well, it didn’t happen overnight. Two years of negative real wage growth has crushed the working poor as they drained their savings and maxed out credit cards to make ends meet.

Unionized workers have taken advantage of upcoming contract expirations with companies to bargain for better wages and benefits. Many unions say companies can boost wages because profits have been off the charts.

This summer might go down in history as the “Summer of Strikes” because 650,000 American workers are threatening to walk off the job imminently (some have already hit the picket lines):

Unions for United Parcel Service Inc. and Detroit’s Big Three automakers are poised to join them in coming weeks if contract negotiations fall through.

A Bank of America analyst warned a United Auto Workers strike is at 90% odds of happening as union contracts with automakers Ford, General Motors, and Stellantis expire in September. Some logistics experts believe Teamsters will reach a deal with UPS, but that deadline (July 31) is quickly approaching.

Labor historian Nelson Lichtenstein, who leads the University of California, Santa Barbara’s Center for the Study of Work, Labor, and Democracy, said this summer could “be the biggest moment of striking, really, since the 1970s.”

What’s shaping up to be a summer of strikes comes as inflation spiked to levels not seen since the 1970s. The good news is that it has cooled in recent quarters.

Still, two years of negative real wage growth crushed the working poor — many are in rough financial shape.

So far, strikes have not had a broad economic impact, but that could change overnight. Increasing labor actions are happening across the Western world, also in Europe, for the same reason in the US, due to a cost-of-living crisis sparked by high inflation.

Under O’Biden (the combined reign of economic errors of Presidents Obama and Biden), we won’t see any strike breaking for the good of the economy. Rather, the Biden Administration will be missing in action (or sending in Kamala Harris or Transportation Secretary Pete Buttigieg to do … nothing.

US office space vacancies (white line) have soared since 2008 as The Fed’s massive monetary expansion (blue and green line) has not helped. But Fed monetary expansion DID help drive office prices! At least until 2022, when office space values began to fall. Notice that office values are falling as The Fed withdraws monetary stimulus.

During the regional bank failures in March, we directed our readership to focus on the next potential crisis: “CRE Nuke Goes Off With Small Banks Accounting For 70% Of Commercial Real Estate Loans.”By late March, Morgan Stanley warned clients of an upcoming maturity wall in commercial real estate, which amounts to $500 billion of loans in 2024, and a total of $2.5 trillion in debt that comes due over the next five years.

In a recent Bloomberg interview, Barry Sternlicht’s Starwood Capital Group warned that the CRE space is in a “Category 5 hurricane.” He said, “It’s sort of a blackout hovering over the entire industry until we get some relief or some understanding of what the Fed’s going to do over the longer term.”

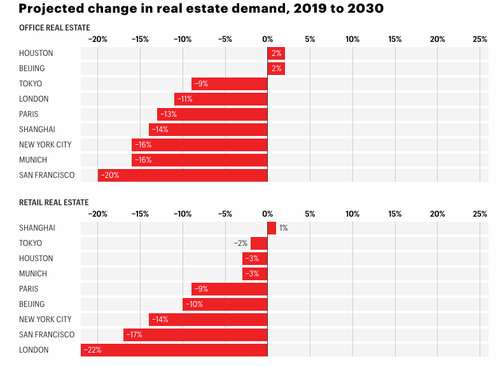

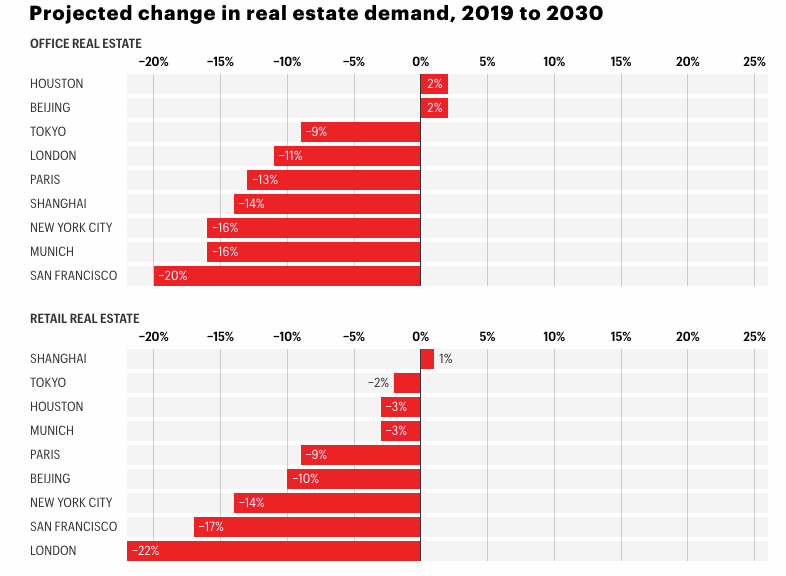

The current downturn in CRE could persist for years, if not through the end of this decade. Jan Mischke, a partner at the McKinsey Global Institute, along with Olivia White, a senior partner at McKinsey, and Aditya Sanghvi, a senior partner and leader of McKinsey’s real estate special initiative, published a note in Fortune, warning “$800 billion of office space in just nine cities could become obsolete by 2030.”

The authors of the report blame the CRE downturn on the “shift to remote and hybrid work prompted two further shifts in people’s behavior”:

First, many residents, untethered from their offices and therefore less fearful of long commutes, moved away from urban cores. New York City’s urban core (that is, the dozen densest counties in the metropolitan area) lost 5% of its population from mid-2020 to mid-2022. San Francisco’s urban core (San Francisco County, Alameda County, and San Mateo County) lost 6%.

Second, consumers began shopping less at brick-and-mortar stores–and far less at stores in urban cores, where people were now less likely either to work or to live. Foot traffic near stores in metropolitan areas remains 10 to 20% below pre-pandemic levels, but the differences between urban and suburban traffic recovery are substantial. For example, in late 2022, foot traffic near New York’s suburban stores was 16% lower than it had been in January 2020, while foot traffic near stores in the urban core was 36% lower.

As fewer employees work in the office, demand for office space will fall. By 2030, such demand will be as much as 20% lower, depending on the city–even in a moderate scenario in which office attendance goes up but remains lower than it was before the pandemic.

And as fewer consumers shop at brick-and-mortar stores, demand for retail space will fall as well, according to our model. In the urban core of London, the hardest-hit city, demand for retail space will be 22% lower in 2030 than it was in 2019 in a moderate scenario.

Some of the most significant declines in office and retail space demand through 2030 will be in major US cities such as San Francisco and New York City.

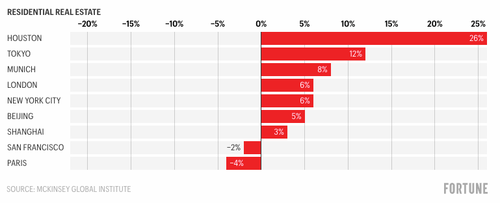

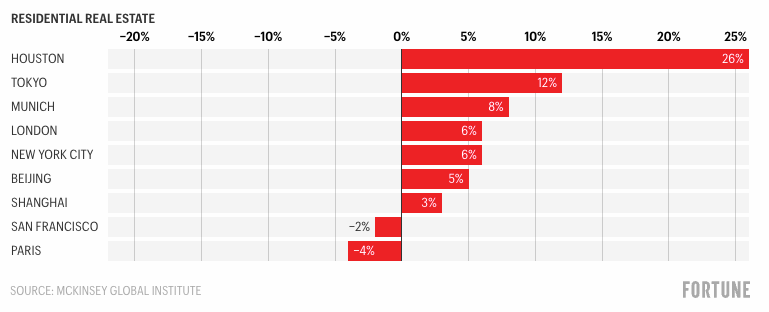

The authors note that the demand for “residential space will suffer less”… Well, according to their forecasting model.

“The reduced demand will have major impacts on urban stakeholders. For example, in just nine cities that we studied especially closely, $800 billion of office space could become obsolete by 2030. And macroeconomic complications could make matters even worse,” the authors continued. Without office workers in downtown areas, economic recoveries in major cities will be a “U” shape or, in some cases, an “L.”

The unraveling of downtowns is already underway. We shared a video this week of scenes of San Francisco’s downtown transformed into a ‘ghost town.’ Building owners in the crime-ridden metro area are already giving up and defaulting as vacancies rise, crime surges, and refinancing is near impossible in today’s climate as the Federal Reserve keeps interest rates sky-high to tame the worst inflation in a generation.

We shift our attention to Baltimore City, where office towers are being dumped in an apparent firesale.

The authors failed to report that the sliding demand for office towers isn’t just because of “remote and hybrid work” but also due to an exodus of companies fleeing crime-ridden progressive cities that fail to enforce law and order.

If McKinsey’s predictions are correct, certain segments of the CRE market are expected to experience prolonged turmoil for years. Some US mayors have proposed an immediate solution to convert office towers into multi-family units. However, this transformation could take years due to the time-consuming processes of obtaining permits and construction.

Yes, the maestros of real estate asset bubbles (Yellen) and eventual deflation (Powell)!

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.