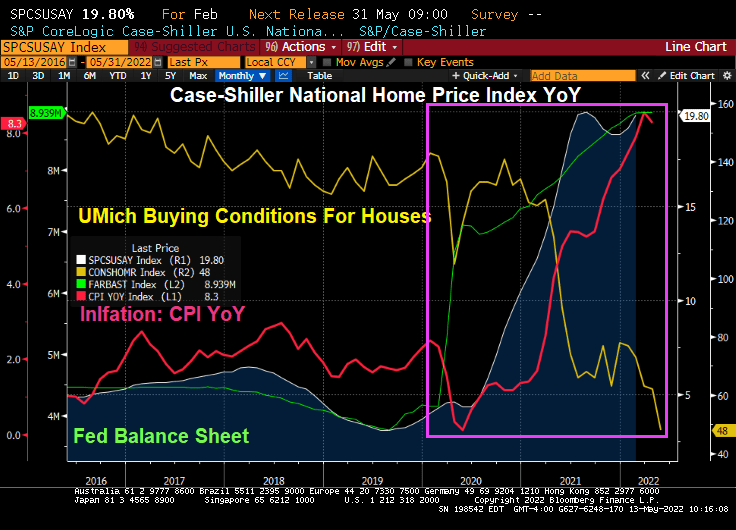

US home prices were growing at a near 20% YoY rate for the latest Case-Shiller National home price index report. But mortgage rates have soaring like a SpaceX missile shot.

Of course, I am moving to one of the metro areas in the USA where closed sales fell only -1.10% YoY in April: Columbus Ohio. I should move to San Diego CA where closed sales fell -21.4% YoY.

Of course, the US still suffers from lack of available inventory for sale.

April new listings are down -5.7% YoY. Columbus Ohio didn’t change from April ’21. San Diego is down -18.4% YoY for new listings.

Rising mortgage rates? Inflation? What a total fiasco.

Mortgage rates have increased dramatically under “Middle Class Joe” as The Federal Reserve attempts to choke-off inflation caused by … The Fed coupled with Biden’s energy policies (hope you are enjoying those high gasoline and diesel prices!) and the Federal government’s staggering spending spree under Pelosi, Schumer and McConnell.

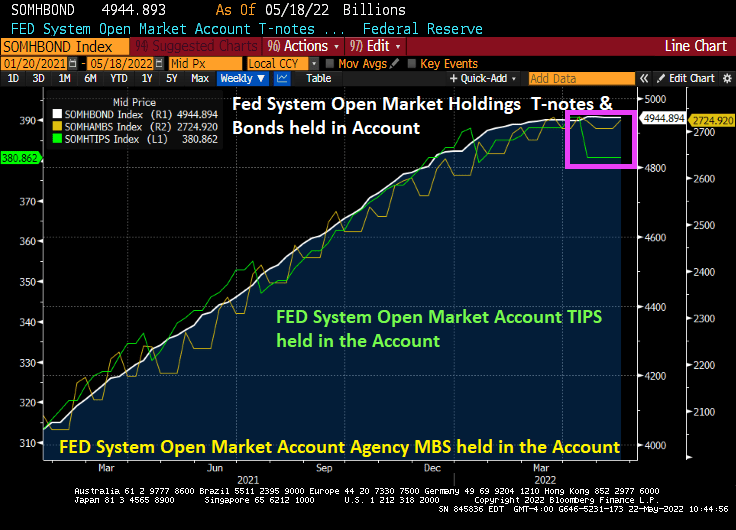

Thus far, The Federal Reserve has leveled-out out their Treasury Note and Bond purchases, increased their Agency Mortgage-backed Securities (AgMBS) holdings, but strangely have reduced their holding of Treasury Inflation-Protected Securities (TIPS) in the face of rising inflation.

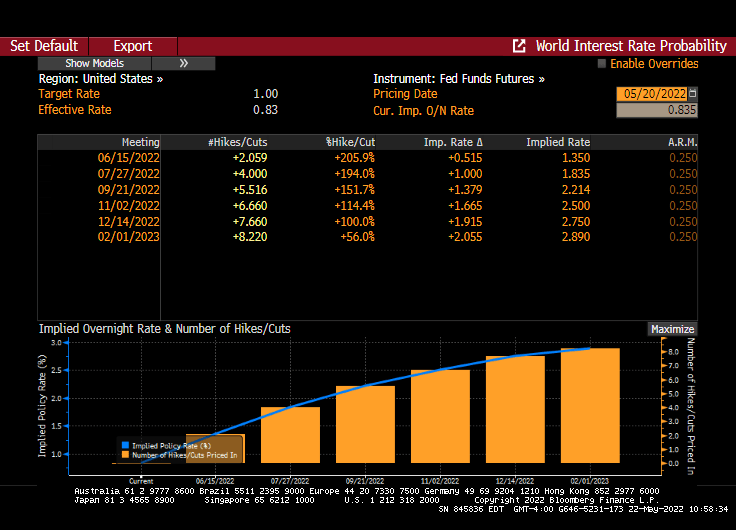

And while The Fed Funds Target rate is a lowly 1%, it is projected to rise to 2.890% by the February 1, 2023 FOMC meeting. That should send mortgage rates up.

As if mortgage rates haven’t skyrocketed already, thanks to The Fed’s jawboning about having to raise rates and extinguish inflation.

With sizzling mortgage rates (cooling a bit as the global economy slows), home mortgage payments have risen +43.4% YoY.

Now we have President Biden trying to scare us about the Monkey Pox, yet leaves the southern border wide open. One would think that Biden would shut the borders (as if the surge in Fentanyl, sex trafficking and other diseases aren’t reason enough. But I do predict another massive spending bill from Biden/Congress to combat Monkey Pox and the resurgence of Covid variants.

Meanwhile The Fed jawbones fighting inflation with monetary tightening in the future, even if they jawboning causes mortgage rates to soar and mortgage payments to spiral.

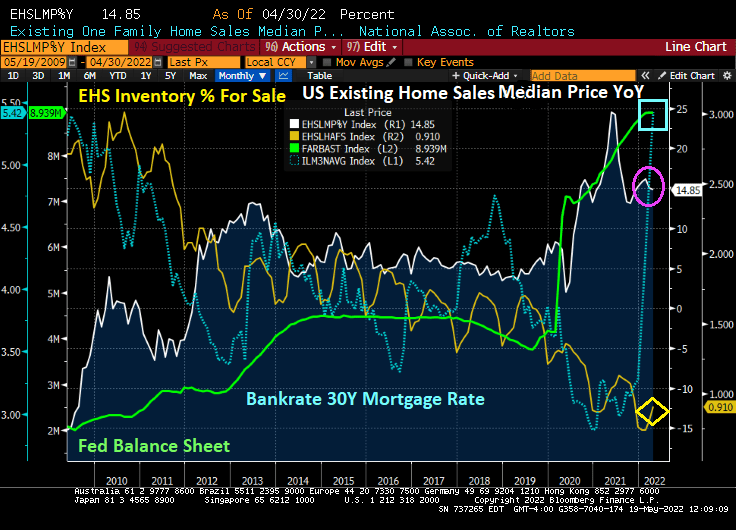

US Existing Home Sales were 5.61M SAAR in April, down -2.4% from March’s -3.0% MoM reading. But median prices YoY for existing home sales printed at 14.85%, still hot, hot, hot.

With 3 consecutive declines in MoM existing home sales, how can prices still be raging at 14.85%? First, inventory for sale in April remains low compared to 2010 (yellow line). Second, The Federal Reserve’s Stimulypto (excessive monetary easing) is still out there in force despite Jerome “Slowhand” Powell signaling rate increases (green line). 30Y mortgage rates are still rising.

Where do we go from here? 30 year mortgage rates have been climbing as The Fed signals its intents to tighten monetary policy. But with global economic slowing, Treasury yields have been coming down (like today’s -5.2 BPS drop (Germany’s 10Y Bund Yield dropped -8 BPS on slowing global economic growth).

But remember, the Existing Home Sales numbers are for April.

Nothing has been the same since Covid and The Federal Reserve’s massive overreaction to the government shutdowns of the economy.

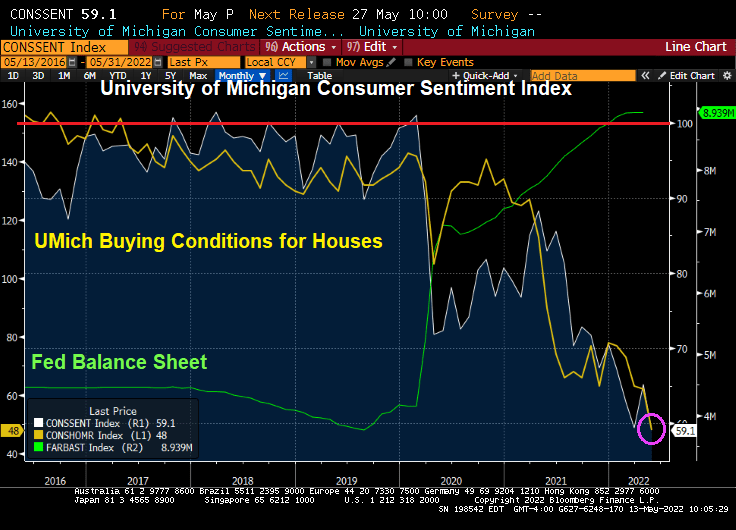

Notice how the University of Michigan Consumer Sentiment Index (white line) has plunged since Covid and the ensuing rise in inflation. University of Michigan’s Buying Conditions for Houses has also plunged to new depths.

Rising inflation (highest in 40 years) and hottest home price bubble (even hotter than the infamous housing bubble of 2005-2007) AND rising mortgage rates have placed a damper on home buying sentiment.

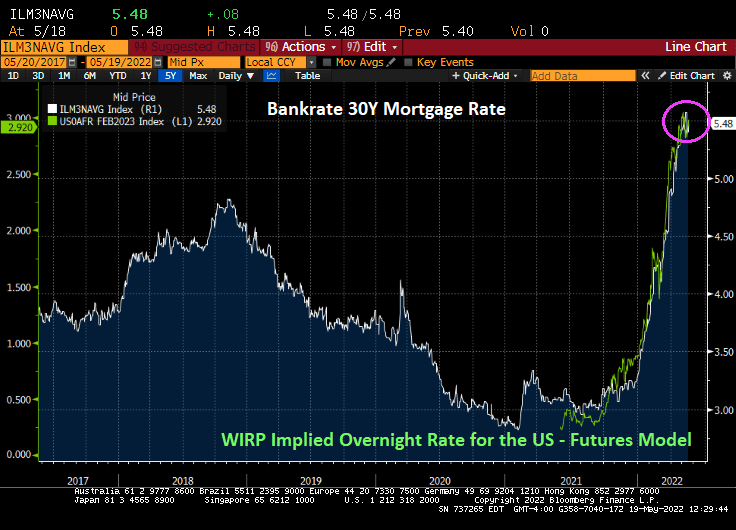

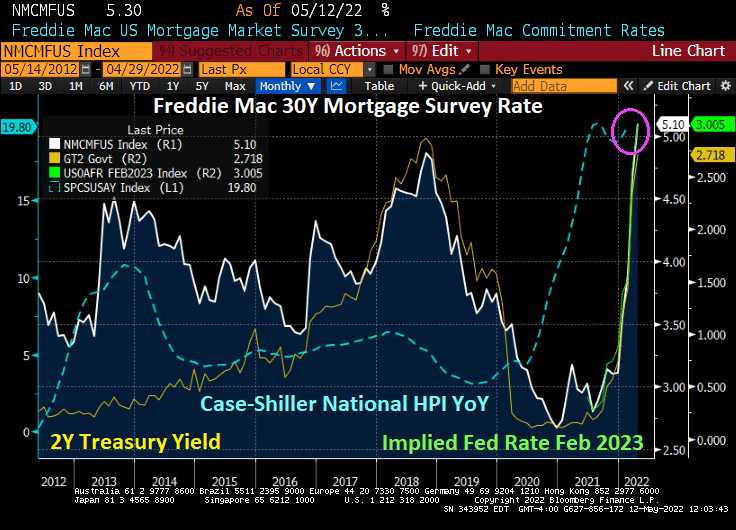

The Freddie Mac 30-year mortgage rate is rising faster than a SpaceX moonshot!

I’m telling your now that The Fed is killing the dreams of millions of Americans by pricing them out of the housing market. Home price growth is lethal as is the increase in mortgage rates.

The Biden Administration and The Federal Reserve together should be called “The Cooler Kings” in that their policies are putting a Big Chill on the mortgage market and equities.

Mortgage rates are skyrocketing thanks to the Federal Reserve.

The 30-year fixed-rate mortgage averaged 5.27% for the week ending May 5, according to data released by Freddie Mac FMCC, -1.62% on Thursday. That’s up 17 basis points from the previous week — one basis point is equal to one hundredth of a percentage point, or 1% of 1%.

House price growth to wage growth is below the all-time high, but remains above housing bubble levels of 2005-2007.

The Refinitiv Venture Capital Index is down 53% since November ’21 as The Fed cranks up interest rates.

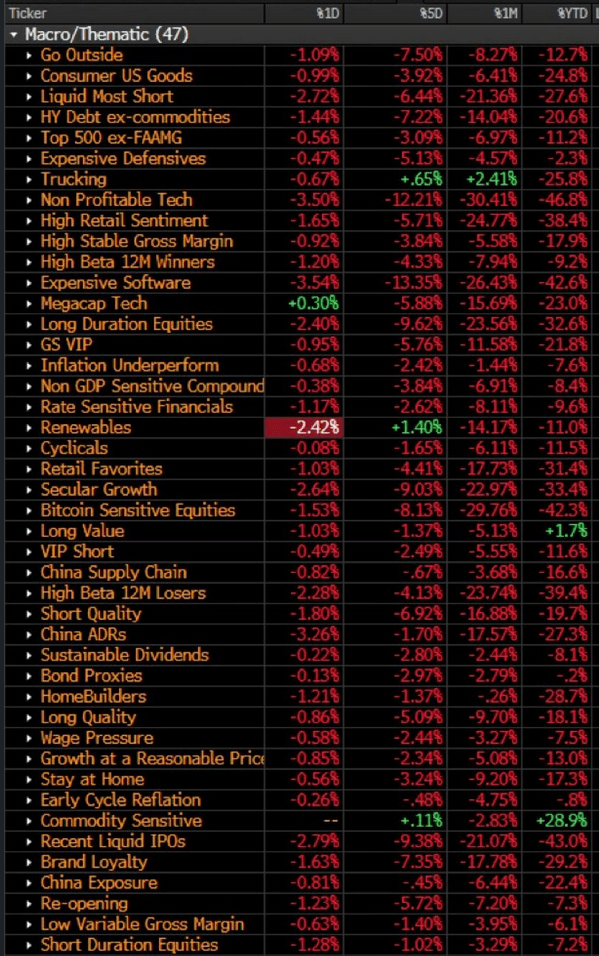

Well, at least commodities are soaring under “The Cooler Kings.” Pretty much everything else is sucking wind.

The question, of course, is whether The Federal Reserve will back off its plans to aggressively raise interest rates in lieu of crashing stock market, venture capital, and possibly home prices.

A measure of U.S. manufacturing activity unexpectedly dropped in April to the lowest level since 2020 as growth in orders, production and employment softened.

The Institute for Supply Management’s gauge of factory activity fell to 55.4 last month from 57.1, according to data released Monday. The Manufacturing Prices index remained elevated.

As the 10-year Treasury yield tries to breech the 3% barrier.

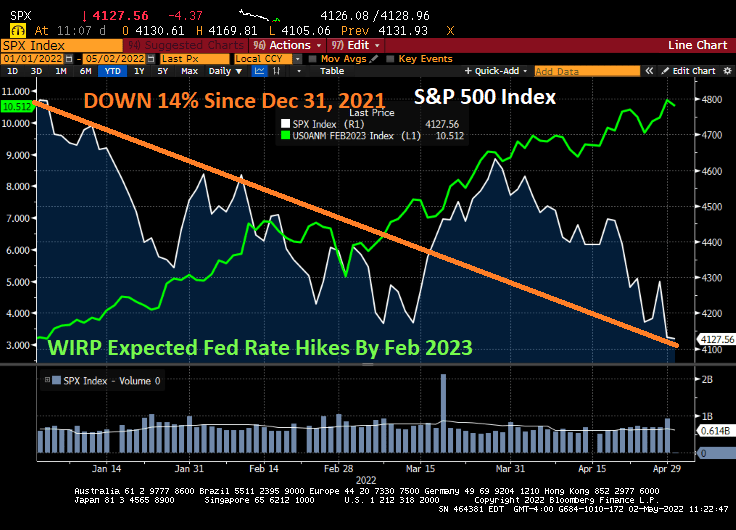

And as The Fed continues to threaten tightening of their monetary follicies, the S&P 500 index is down 14% since Dec 31, 2021.

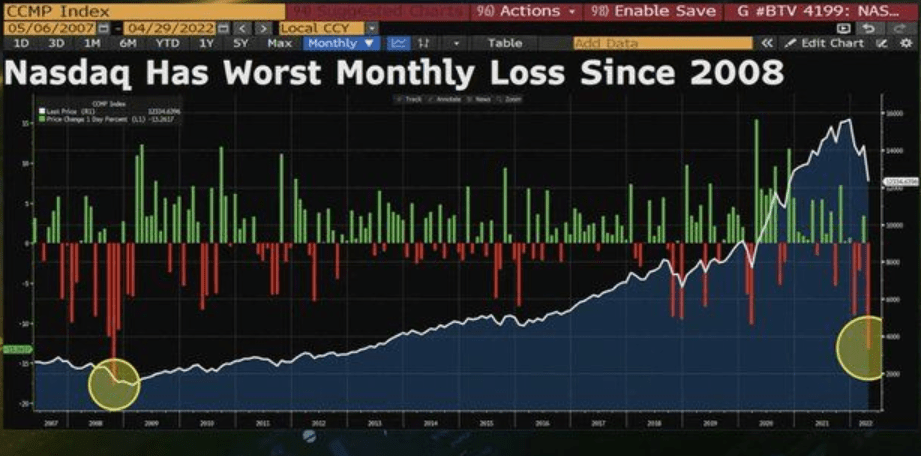

And the NASDAQ had it worst monthly loss since 2008.

We now have the proverbial double whammy happening … soaring home prices AND soaring mortgage rates.

The theory is, of course, that The Federal Reserve will slowly remove its staggering monetary stimulus leftover from 1) the financial crisis of 2008 and 2) the Covid recession of 2020. As you can see, the sheer volume of monetary stimulus remains outstanding and it is the EXPECTATIONS of The Fed tightening that is caused the 30-year mortgage rate to rise.

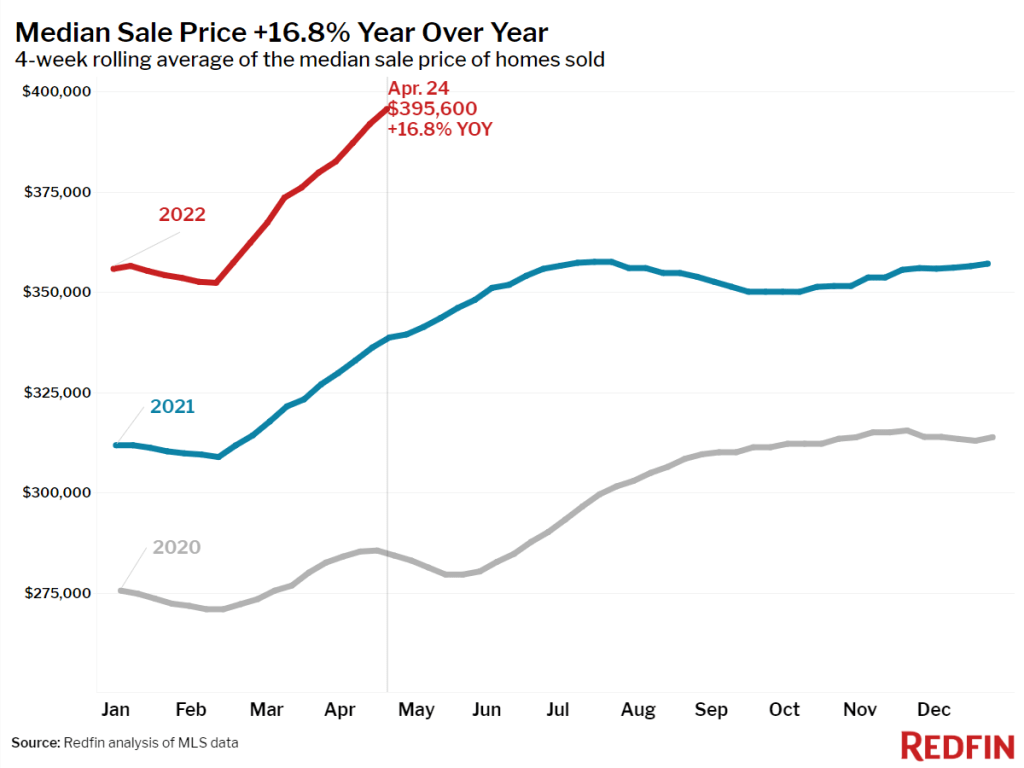

While I used the Case-Shiller National Home Price Index YoY, Redfin shows more contemporaneous home price data with April 24 median home sales price at 16.8%.

Thanks to The Fed, we are seeing homebuyer mortgage payments are up 39.4% YoY.

As inflation continues to damage America’s middle-class and low- wage workers, we may see regulations going into effect from the Consumer Financial Protection Bureau protecting consumers from … themselves.

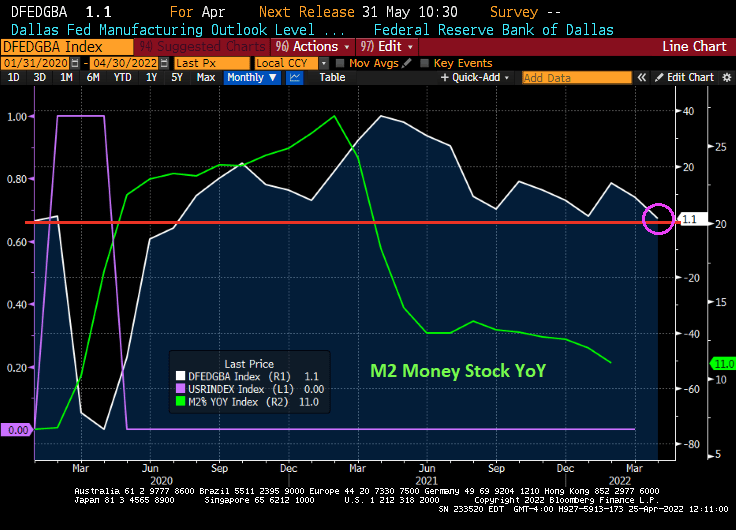

M2 Money stock YoY skyrocketed during the Covid mini-recession, peaking at 21% during February of 2021. The Dallas Fed manufacturing outlook grew to 38.1 in March 2021.

However, as M2 Money growth has slowed 11%, the Dallas Fed manufacturing outlook has plunged to near zero.

Its Saturday and I am dreading markets opening on Monday. But here is where we sit today.

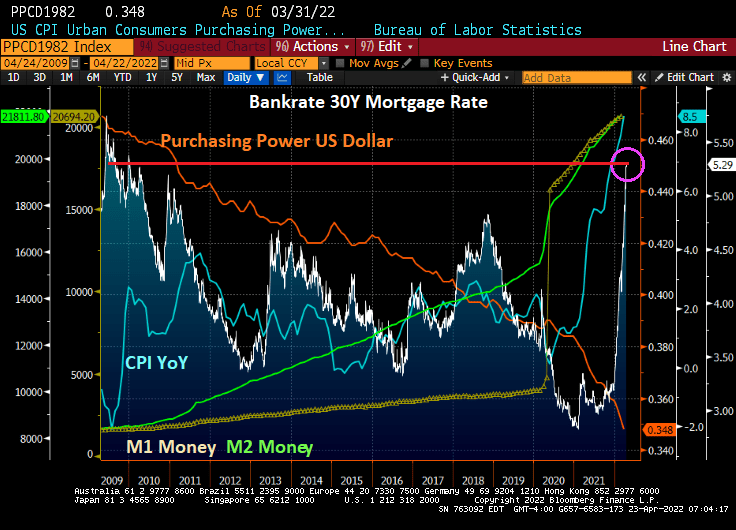

The 30-year mortgage rate has soared to 5.29%, the highest level since 2009 at the beginning of Obama’s Presidency. Since 2009, we have seen the purchasing power of the US Dollar decline further (orange line) while inflation (blue line) has soared. M1 (yellow) and M2 (green) has been growing since the financial crisis, but really took-off with the Covid outbreak in 2020 and The Fed’s massive overreaction coupled with Federal government stimulus.

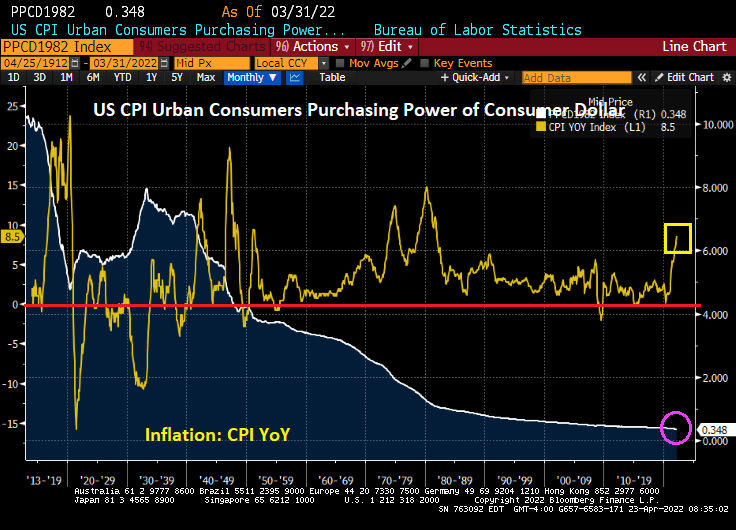

Since the creation of The Federal Reserve System under President Woodrow Wilson, the purchasing power of the US Dollar has collapsed so much that $10 in 1913 in worth 34.8 cents today. But notice that since 1949, the CPI YoY has rarely been negative meaning that prices are pretty much only going up.

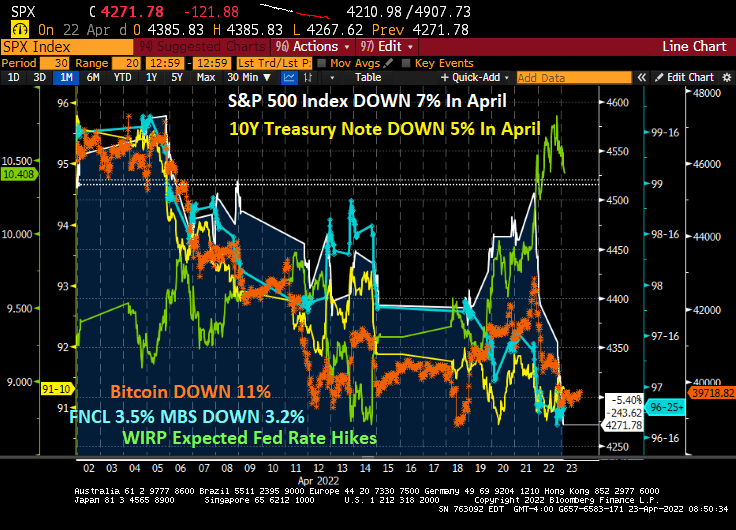

Instead of April showers bring May flowers, it is April expected Fed rate hikes (now 10.408 rate hikes by February 2023) bringing declining assets prices. In April so far, the S&P 500 index is DOWN 7%, the 10-year Treasury Note price is DOWN 5%, Bitcoin is DOWN 11%, the 3.5 coupon agency MBS price is down 3.2%.

We are seeing increased volatility in both the equity and bond markets.

Well, Powell and The Fed are hurling fireballs at mortgage rates and asset prices in April.

You must be logged in to post a comment.