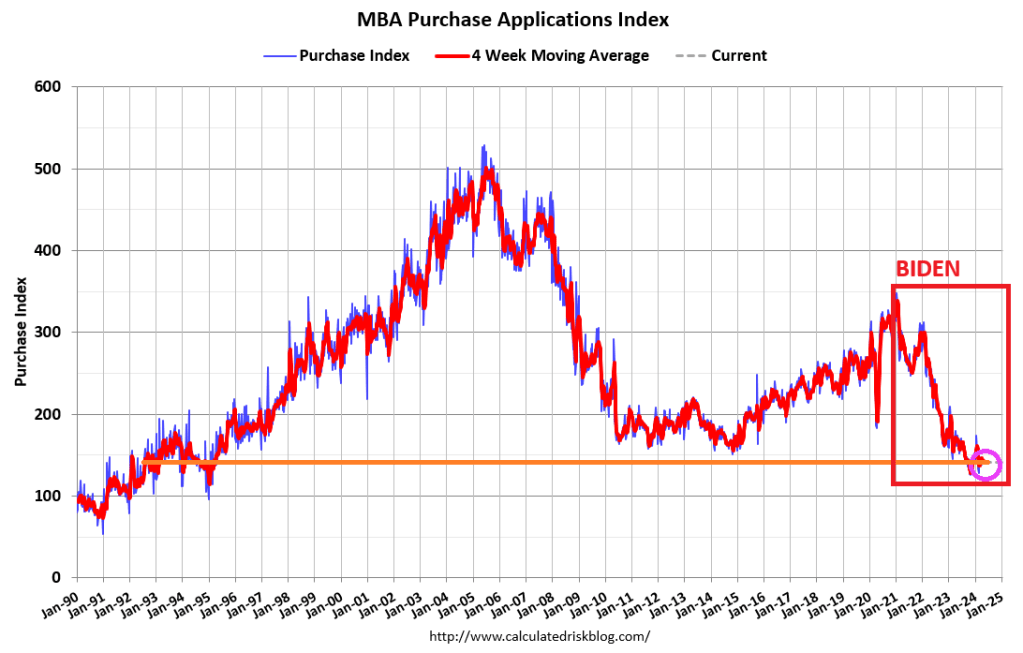

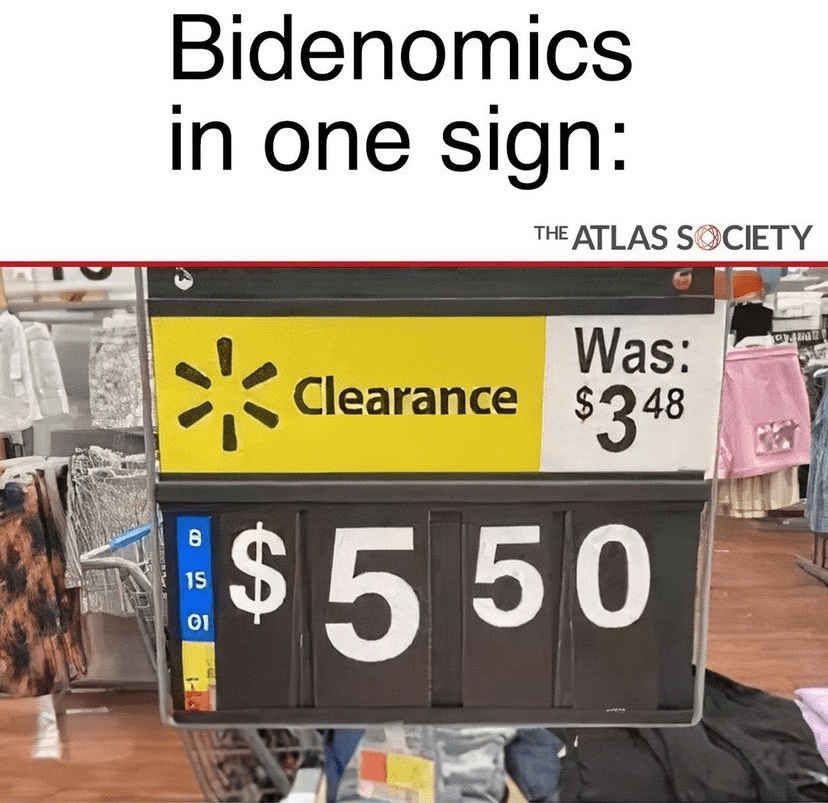

Biden and Bidenomics is disastrous for the middle class and low wage workers. Food and housing prices through the roof, and now we have mortgage purchase demand declining -57% under Biden.

Mortgage applications increased 2.6 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending May 3, 2024.

The Market Composite Index, a measure of mortgage loan application volume, increased 2.6 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 3 percent compared with the previous week. The seasonally adjusted Purchase Index increased 2 percent from one week earlier. The unadjusted Purchase Index increased 2 percent compared with the previous week and was 17 percent lower than the same week one year ago.

In fact, Mortgage Purchase demand (applications) are down -57% under Biden and Bidenomics.

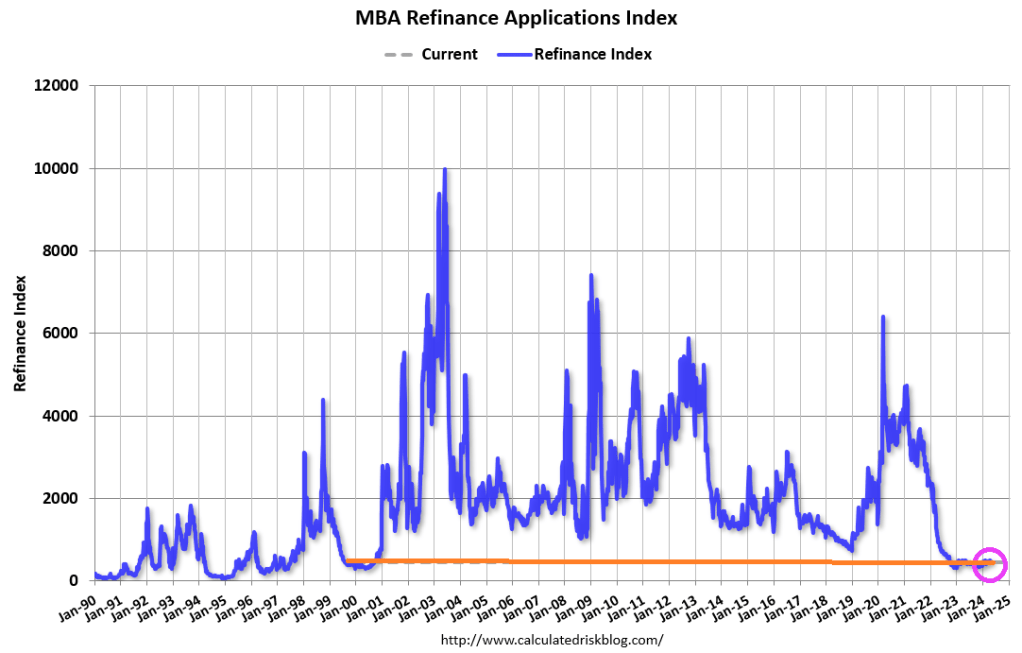

The Refinance Index increased 5 percent from the previous week and was 6 percent lower than the same week one year ago.

One year after regional banks crashed and burned due to the combination of tumbling debt/treasury prices coupled with cratering commercial real estate loans, fears about the current state of Commercial Real Estate – where most offices still see tenants at best 3 to 4 days a week and are literally burning through rents – appear long forgotten. Is that sensible?

For one answer, we turned to the latest report from Goldman’s REIT/CRE expert Chandhi Luthra who has published a visual assessment of the state of CRE in 2024 in terms of loan maturities, 2023 extensions, and property and lender groups. She also looks at the latest transaction and leasing volumes, and shares several key takeaways.

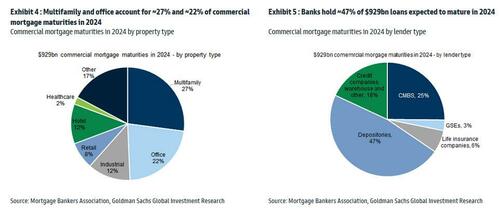

There are ~$4.7tn of outstanding commercial/multifamily mortgages outstanding, according to the Mortgage Bankers Association’s 2023 Commercial Real Estate Survey of Loan Maturity Volumes.

More specifically in 2024, $929bn of CRE mortgages are expected to mature, ~20% of ~$4.7tn total commercial mortgages outstanding. In terms of property type, multifamily and office account for ~27% and ~22% of commercial mortgage maturities in 2024 respectively. In terms of lender type, banks hold ~47% of debt maturing in 2024, followed by CMBS at ~25%.

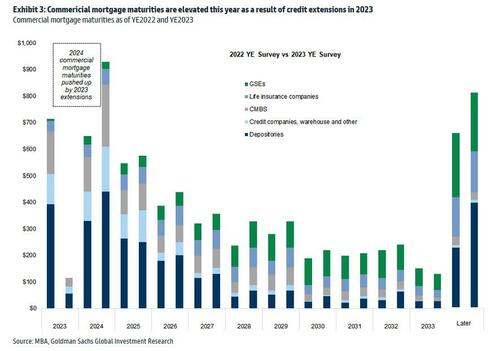

It is worth noting that 2024 commercial mortgage maturities are pushed up by 2023 extensions. As shown in Exhibit 3, among the CRE loans scheduled to mature in 2023, ~$610bn were refinanced, with ~$300bn pushed into 2024 and the remainder into future years. As a result, the total CRE refinancing volume is expected to be ~$929bn in 2024.

Of course, it does not end there, and since there has been no fundamental improvement, it is certain that extension volumes in 2024 will be high as well. However, as interest rates are expected to come down, demand for refinancing in 2024 may outpace that in 2023 according to the Goldman analyst (rates are still far, far higher than where they were when most of the loans were originated several years ago). At the same time, for loans that have already been extended in the past, it is also likely that future extensions could be harder.

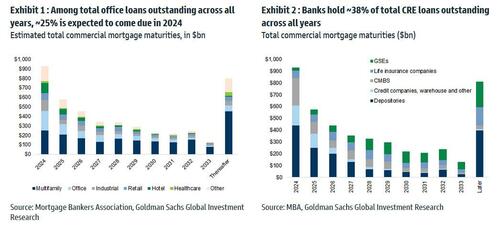

Among the loans backed by office properties overall, ~25% is expected to come due in 2024. In terms of lender type, banks (primarily small, regional banks) hold ~38% of total CRE loan outstanding across all years, followed by the GSEs at 20%.

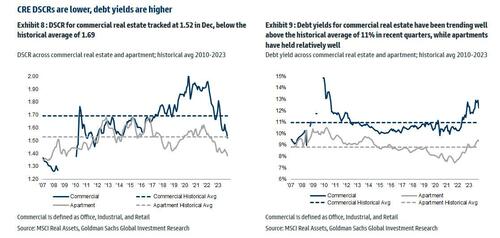

Looking at different debt metrics, DSCR for commercial real estate (office, industrial and retail combined) tracked at 1.52 in Dec, below the historical average of 1.69; debt yields for commercial real estate have been trending well above the historical average of ~11% in recent quarters, while apartments have held relatively well.

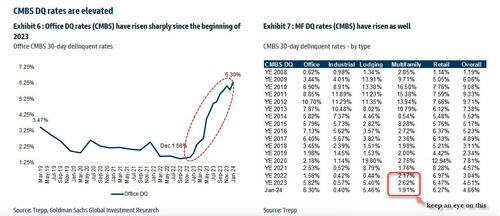

Office CMBS DQs have risen significantly, with Jan tracking at 6.3%, up significantly from 1.58% in Dec 2022. And while everyone knows the Office canary in the coalmine is dead and buried, keep an eye on Multifamily CMBS DQs which tracked at 1.91% vs 2.62% in December, with the sequential decline associated with a large San Francisco apartment loan that was recently disposed. The overall DQ rate tracked at 4.66% in January.

The Goldman strategist concludes with a word about CRE transaction and leasing: U.S. CRE transaction market continues to be muted, primarily driven by elevated interest rates, limited sources of capital, and the pricing gap between buyers and sellers. January volume was down -11% yoy, driven by easier compares in Jan 2023 (down -55%). In terms of leasing, Jan preliminary trends indicate weakness in activities, with office down -25% yoy and industrial down -28% yoy.

Here, Goldman trader Sara Cha chimes in (her report is also available to pro subs) and notes that we can see from the transaction data “why sentiment in CRE brokers is a bit more mixed of late – thought yesterday’s JLL print had mixed reception – while you’ve seen some signs of life in capital markets space broadly to start the year, not seeing that as much on the CRE front (remember those 3Q-4Q greenshoots?).“

Multifamily CRE

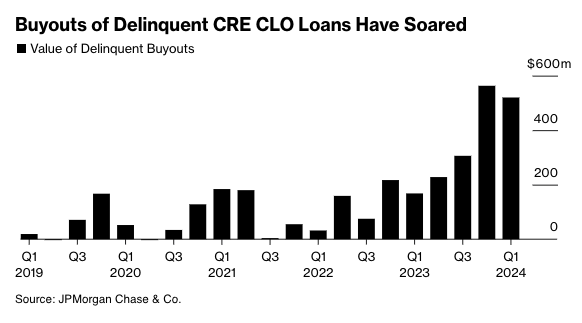

The commercial real estate sector continues to experience elevated stress . The latest crack to emerge is the increasing number of delinquencies on multifamily mortgages.

In April, about 8.6% of commercial real estate loans bundled into collateralized loan obligations were distressed, reaching the record high set in January, according to Bloomberg, citing new data from analytics firm CRED iQ.

The loans bundled into CRE CLOs were merged with funds from individual investors to acquire multifamily housing during the Covid era. After that, borrowing rates surged, catching many off guard. A significant portion of the deteriorating loans had floating-rate interest rates, putting massive pressure on landlords’ cash flows, diminishing the market worth of the properties, and obliterating equity in a large number of investments.

According to data provider Trepp, $78.5 billion of CRE CLO loans are outstanding. This means many CRE CLO issuers are racing to find ways to prevent a tsunami of bad loans from defaulting or risk losing the fees they collect on the securities.

Recent estimates from JPMorgan show lenders purchased $520 million of delinquent loans in the first quarter of this year. Lenders have been ramping up the number of buyouts over the last four quarters because of mounting bad loans in a period of elevated rates.

Source: Bloomberg

JPMorgan strategist Chong Sin said he’s surprised by lenders’ ability to obtain warehouse lines to purchase bad debt, given tightening credit conditions.

“The reason these managers are engaged in buyouts is to limit delinquencies,” Sin said, adding, “The wild card here is, how long will financing costs remain low enough for them to do that?”

Anuj Jain, an analyst at Barclays Plc, expects buyouts to continue as distress increases across the CRE CLO space.

“If the outlook for the Fed shifts materially to hikes or no rate cuts for a while, that might lead to a sharp increase in delinquencies, which can stifle issuers’ ability to buy out loans,” Jain said.

Bloomberg explains much of the CLO space derives from multifamily bridge loans originated around 2021-2022:

CRE CLO issuance surged to $45 billion in 2021, a 137% increase from two years earlier, when buyers of apartment blocks sought to profit from the wave of workers moving to the Sun Belt from big cities. Three-year loans would give them time to complete upgrades and refinance, the thinking went.

Fast forward to today and the debt underpinning many of the bonds is coming due for repayment at a time when there’s less appetite for real estate lending, insurance costs have skyrocketed and monetary policy remains tight. Hedges against borrowing cost increases are also expiring and cost significantly more to purchase now.

Those blows helped increase multifamily assets classed as distressed to almost $10 billion at the end of March, a 33% rise since the end of September, according to data compiled by MSCI Real Assets.

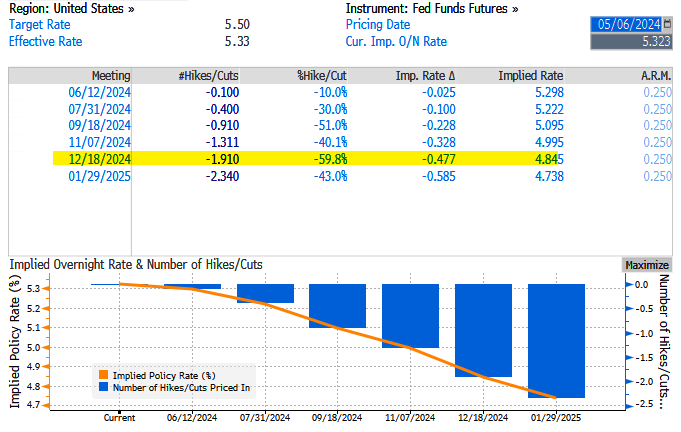

Last Wednesday, the Fed left interest rates unchanged at around 550bps as inflation data reaccelerates and economic growth tilts to the downside, stoking stagflation fears.

Fed swaps are pricing in just under two cuts – this is down from nearly seven earlier this year and about 1.14 before last week’s FOMC.

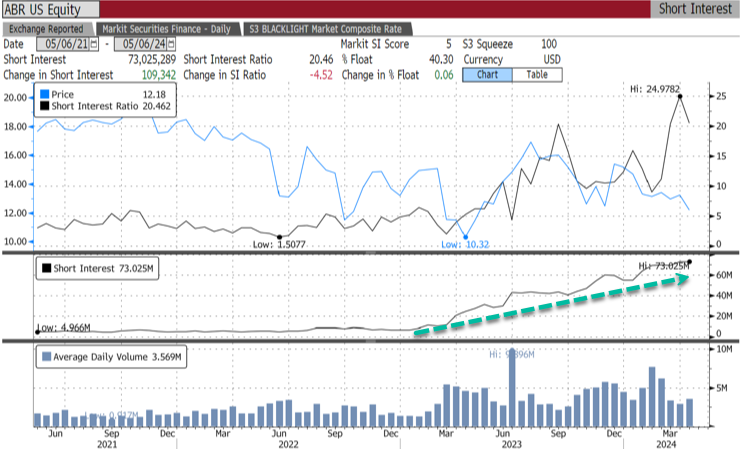

Meanwhile, bears are piling in on CRE CLO issuer Arbor Realty Trust Inc., with 40.3% of the float short, equivalent to 73 million shares short.

“The multifamily CRE CLO market was not prepared for rate volatility,” said Fraser Perring, the founder of Viceroy Research, which has placed bear bets against Arbor, adding, “The result is significant distress.”

The longer the Fed delays rate cuts, the worse the CRE mess will get.

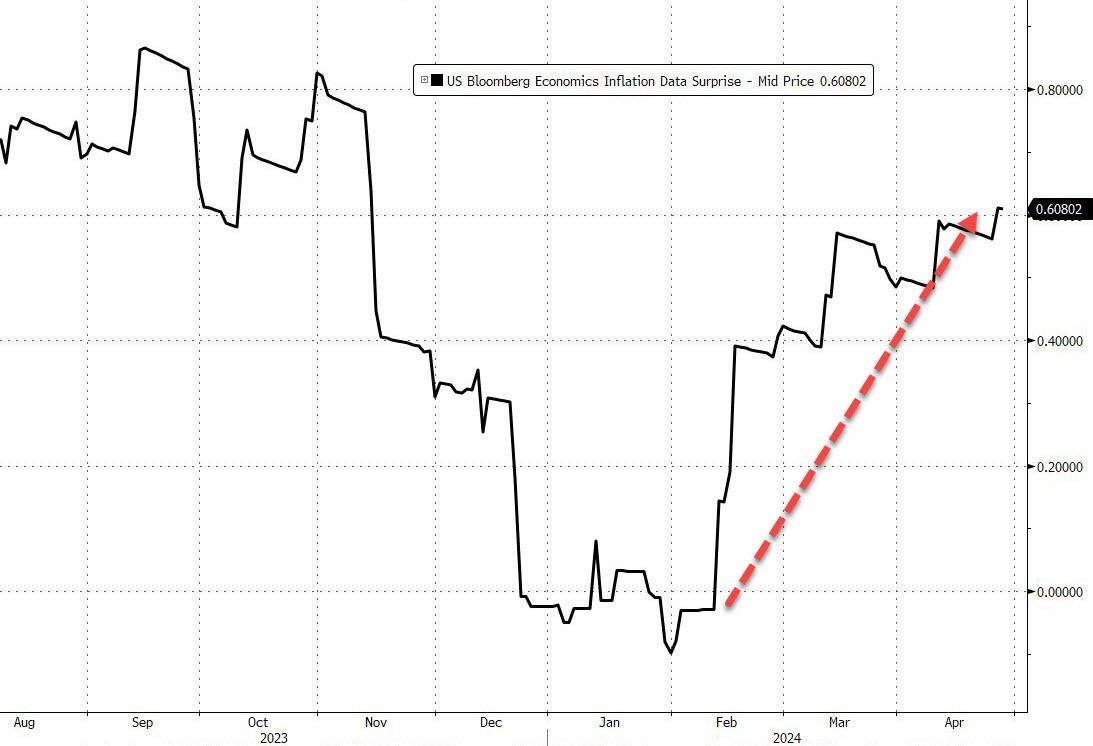

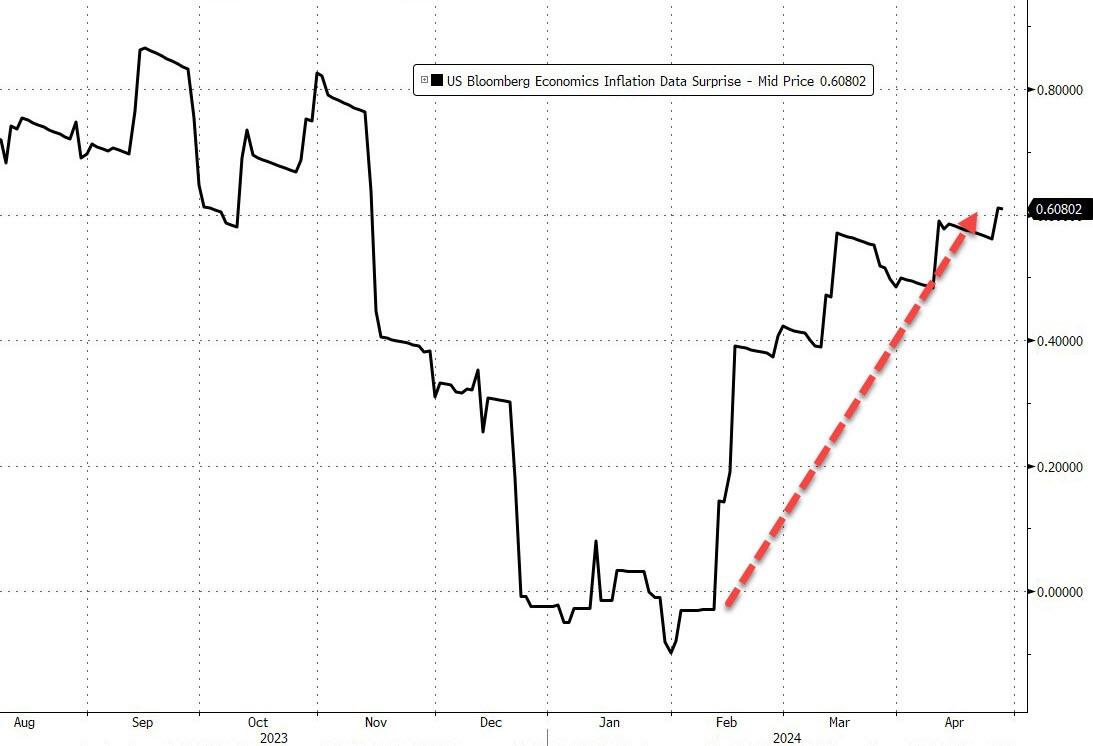

Surprise! Just in time for the November election, this is a negative surprise that Biden doesn’t want to hear.

The Citi Economic Surprise index crashed to -7.30, the lowest since January 2023.

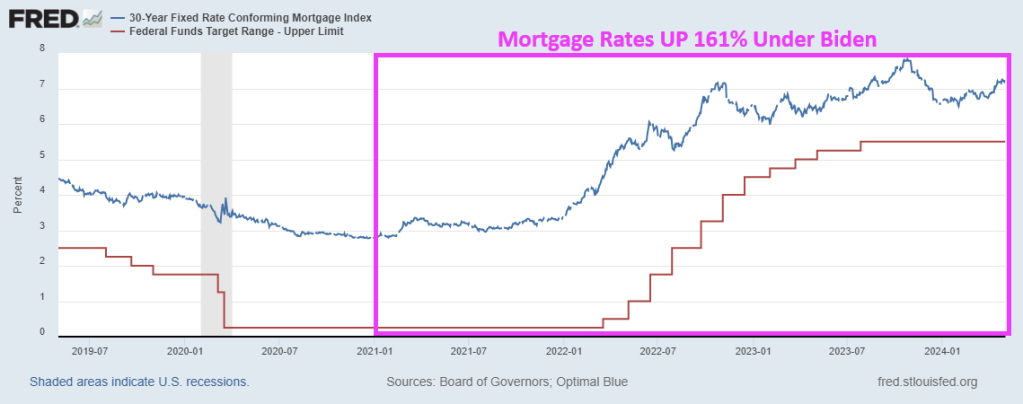

Under Biden’s leadership (hell, he and his family already own several mansions … on a Senator’s pay), home prices are up 32% under Biden and mortgage rates are up a staggering 160%.

Getting young households who rent to buy a home in this environment will require magic.

Yellen: Mortgage rates have been so low for so long that it’s created a lock-in effect where people don’t want to sell their homes to buy new ones for fear of losing their attractive rates.

That’s made it “almost impossible” for first-time homebuyers to enter the housing market, U.S. Treasury Secretary Janet Yellen said during her testimony before the House Ways and Means Committee.

Now hold on a minute, Janet. YOU were the one that kept rates too low for too long as Federal Reserve Chair.

What was her record on mortgage rates? Yellen kept the Fed target rate (upper bound) at 25 basis points under Obama/Biden until December 2015, so only one rate hike under Obama/Biden. Then came the election of Donald Trump in November 2016. Then Yellen raised The Fed target rate 4 times after Trump was elected.

Mortgage rates fell to 3.78% by November 2017, so Yellen helped keep mortgage rates low. But mortgage rates soared after Trump’s election to 4.22% by the end of her term.

There are other reasons why first-time homeownership is so difficult, like local NIMBY (not in my back yard) policies and the absolutely lousy labor market.

She added that Biden’s massive tax increase won’t hit middle class households (other than the massive INFLATION tax that was levied by Biden). That is a plain lie. the Tax Foundation says that someone who’s married, two kids, making $85,000 would pay $1,700 more in taxes. A married couple with two children making $165,000 annually would pay $2,450.50 more than in the previous year, while a family with three kids pulling in $200,000 per year will shell out almost $7,500 more per year.

So much for Biden’s “No one making under $400,000 will pay and additional penny of tax.”

Housing in the US is simply unaffordable, particularly after HUD levied new regulation rising the cost of new housing up to $31,000. Wait for this to kick into the data for mortgage demand!

Mortgage applications decreased 2.3 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending April 26, 2024.

The Market Composite Index, a measure of mortgage loan application volume, decreased 2.3 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 1.4 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 2 percent from one week earlier. The unadjusted Purchase Index decreased 1 percent compared with the previous week and was14 percent lower than the same week one year ago.

The Refinance Index decreased 3 percent from the previous week and was 1 percent lower than the same week one year ago.

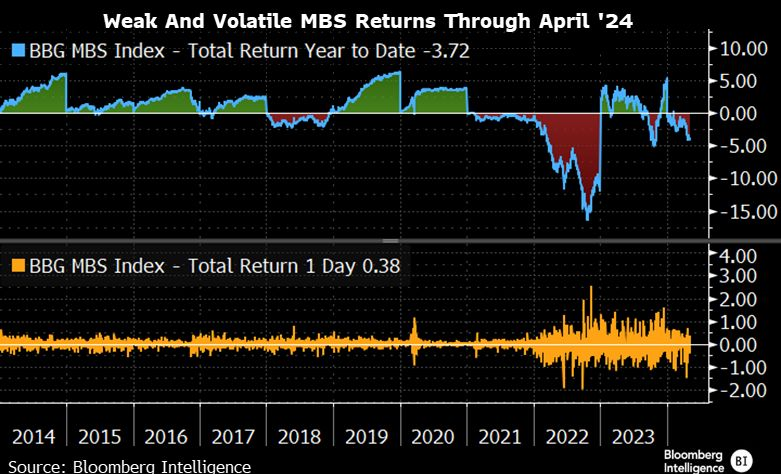

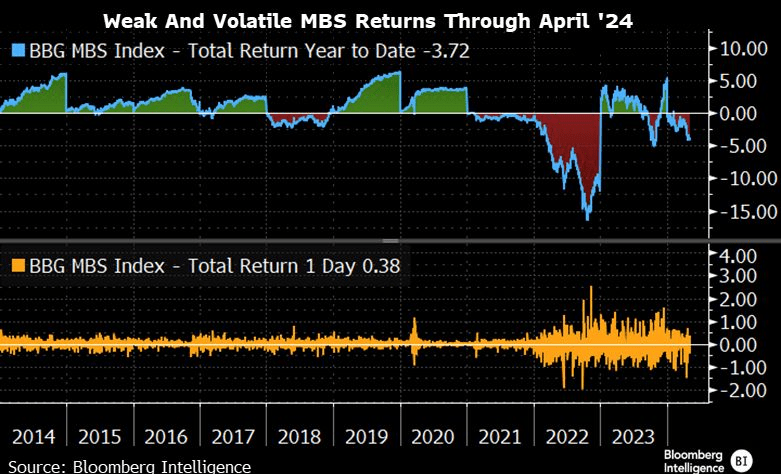

MBS returns are weak and volatile.

How is the Biden Regime making homeownership more affordable? They aren’t. The are using regulations, to drive the cost of new housing way up. New HUD energy rules will raise the cost of home construction by imposing stricter building codes. The National Association of Home Builders says the energy rules can add as much as $31,000 to the price of a new home. Payback time is 90 years (how long it will take the recoup the initial investment).

Under Biden’s “leadership” we are all addicted to gov. But at least Ukraine and Zelenskyy will be getting a guaranteed 10 years of financial support from the US … while E Palestine Ohio and Maui remain destroyed.

Janet Yellen, world class propagandist (US version of Baghdad Bob) and US Treasury Secretary under Biden, was so wrong about inflation. Instead of being “transitory”, turns out to be seemingly permanent.

Today’s Case-Shiller home price report was released for February. The National Home Price index was up 6.4% year-over-year. But look at the explosion of M2 Money and home prices. Hmm.

If we look at home prices and M2 Money on a year-over-year (YoY) basis, we can see the surge in money printing with COVID and the corresponding surge in home prices. As M2 Money growth slowed, the Case-Shiller National HPI slowed as well … until The Fed slowed the declined in M2 Money growth resulting in rising home price growth again.

So, The Fed will likely have to keep on printing. You can see Janet Yellen dancing to the thought of printing more money.

Then the numbers spiraled out of control. Yet Biden/Congress keep shoveling money to Ukraine and leave our borders unsecured.

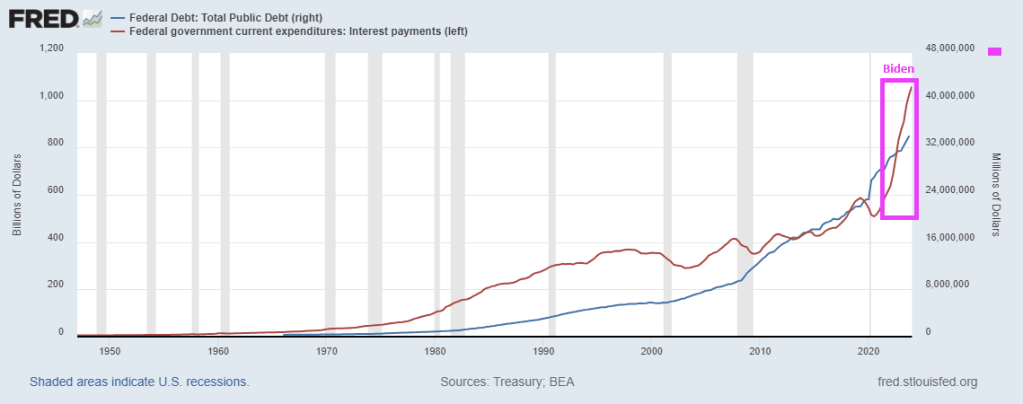

Washington’s fiscal situation has drastically changed since then; total debt has surpassed $34 trillion, the annual budget shortfall exceeds $1 trillion, and interest costs have topped $1 trillion.

David Walker, the former comptroller general of the United States and a Main Street Economics advisory board member, is unsurprised.

Seventeen years ago, Mr. Walker rang fiscal alarm bells. Like Ross Perot before him, he took his case to the American people and delivered the cold, hard truth: The government’s books are unsustainable, and interest charges on the mounting debt will swallow a significant portion of federal revenues.

During this time, the former head of the Government Accountability Office (GAO) appeared on a widely viewed episode of “60 Minutes,” toured the country to spotlight worrisome trends in the U.S. government’s budget (he did this again in 2012), and attempted to convince lawmakers of the unsustainable fiscal path.

He also penned a 2009 book titled “Comeback America: Turning the Country Around and Restoring Fiscal Responsibility.”

Given the treasure trove of budgetary numbers coming out of the nation’s capital almost daily, such as nearly half of income tax revenues being dedicated to interest payments, Mr. Walker’s warnings have not been heeded nearly two decades later.

According to the Congressional Budget Office’s long-term outlooks, the national debt will eye $50 trillion by 2034, fueled by around $17 trillion in cumulative deficits. As a percentage of GDP, debt held by the public and the deficit will reach 166 percent and 8.5 percent by 2054, respectively, the CBO forecasts.

“Washington has become addicted to spending, deficits, and debt, and they’re charging the credit card and planning to send the bill to younger and future generations of Americans,” Mr. Walker told The Epoch Times.

“That’s irresponsible. It’s unethical, and it’s immoral, and it needs to stop.”

Is the United States past the point of no return?

“Only God knows when the tipping point is going to occur, and God’s not telling us,” he said.

He combs through various metrics to gauge the situation.

One of these is the debt-to-GDP ratio, which is presently at about 122 percent. Outside of the coronavirus pandemic, this is a record high.

Mandatory spending as a percentage of the federal budget is another metric. It currently stands at around 73 percent.

Another one is interest as a percentage of the budget, which is close to 15 percent.

For Mr. Walker, it is not only raw numbers but what the trends are displaying, which requires a deep dive into demographics.

“We have an aging society with longer lifespans, relatively fewer workers, supporting more retirees, and a skills gap,” he noted.

Last year, two notable developments happened: a majority of Baby Boomers were at least 65, and the birth rate tumbled to the lowest in a century.

This will metastasize into a costly burden for the federal government, particularly Social Security.

The Peter G. Peterson Foundation estimates that the current worker-to-beneficiary ratio is 2.8-to-1, down from 5.1-to-1 in 1960. By 2035, the Social Security Administration projects the ratio will further slide to 2.3-to-1.

Republicans and Democrats

President Joe Biden has claimed that he has acted fiscally responsibly, telling a crowd at a North America’s Building Trades Unions event on April 24 that he cut the national debt. (Insert a TV laugh track here). President Biden has repeatedly touted this claim over the last 18 months, although he has added close to $7 trillion to the national debt since taking office in 2021.

While Republicans have griped over the current administration’s spending endeavors, experts assert that the GOP has also contributed trillions of dollars to the debt pile. One of the GOP-led expansionist initiatives was Medicare Part D under former President George W. Bush.

This program, which was designed to utilize private health care plans to offer drug coverage to Medicare beneficiaries, added $8 trillion in new unfunded obligations. Mr. Walker accepted that “the politicians were totally out of touch with fiscal reality,” considering that Medicare was already underfunded by $19 trillion.

Put simply, both parties have been fiscally irresponsible, and now the bills are coming due.

Mr. Walker purported that politicians suffer from myopia as they are too focused on the next election and, as a result, fearful of making tough decisions. They also experience tunnel vision, he says, meaning they only concentrate on one issue at a time “without understanding the interdependency” and “the collateral effect.”

Self-interest is another malady infecting both sides of the aisle as they aim to keep their jobs and ensure their party stays in power.

“We’ve lost our sense of stewardship,” he said.

“Stewardship is not just generating results today, not just leaving things better off when you leave them when you came, but better positioned for the future,” Mr. Walker explained. “We’ve lost that sense. We need to regain it if we want our future to be better than our past.”

He identified Rep. Jody Arrington (R-Texas), who chairs the House Budget Committee, as one of the few lawmakers to realize the fiscal issues by committing to the Fiscal Commission Act and supporting a constitutional amendment that would limit government growth and stabilize the debt-to-GDP ratio.

“There are others, but there’s not enough,” Mr. Walker said.

Earlier this year, the House Budget Committee advanced the Fiscal Commission Act of 2024 out of committee with bipartisan support.

The bill would establish a 16-member panel featuring six Republicans, six Democrats, and four outside experts without voting power. The group would explore strategies to balance the budget as soon as possible and assess mechanisms to enhance the long-term solvency of various entitlement programs, especially Social Security and Medicare.

Despite some consternation from several Democrats, the bipartisan push received applause, including from the Committee for a Responsible Federal Budget.

“The federal debt is on an unsustainable course, and lawmakers have been unable or unwilling to correct it,” the organization stated. “A fiscal commission would bring Members of both parties and chambers together to facilitate a conversation over how to solve these problems, without pre-prescribing any particular solution (or a solution at all).”

Hope and Change

Whether the United States can improve its fiscal trajectories remains to be seen.

Mr. Walker is hopeful about some of the legislative efforts coming out of the nation’s capital. The country is beginning to face the consequences of years of fiscal mismanagement, making it harder to sell its debt to the rest of the world.

In recent months, many Treasury auctions have led to lackluster demand among domestic and foreign investors. Market watchers have warned that global financial markets might share Fitch and Moody’s concerns about America’s fiscal deterioration.

But when discussing trillions of dollars, percentages, GDP, and servicing costs, how can the average person, worried about paying his mortgage or replacing a broken-down refrigerator, grasp or even be concerned with these trends?

According to Mr. Walker, you tap into their “head and heart.”

“You have to help them understand that we’re already seeing some of the implications of fiscal irresponsibility,” he said, adding that the causes of the Roman Empire’s demise are familiar to what is transpiring in the United States today: fiscal irresponsibility, a decline in moral values, an overextended military, and an inability to control its borders.

However, while it is vital to translate these gigantic numbers into terms the layman can understand, experts also need to “hit their heart.”

“Do they love their country? Do they love their kids, and do they love their grandkids?” he said. “We’re mortgaging their future at record rates.”

Ever worse, politicians have promised $215 TRILLION in unfunded entitlements to the bottom 99%. When this all explodes, who will be left standing to make good on these promises??

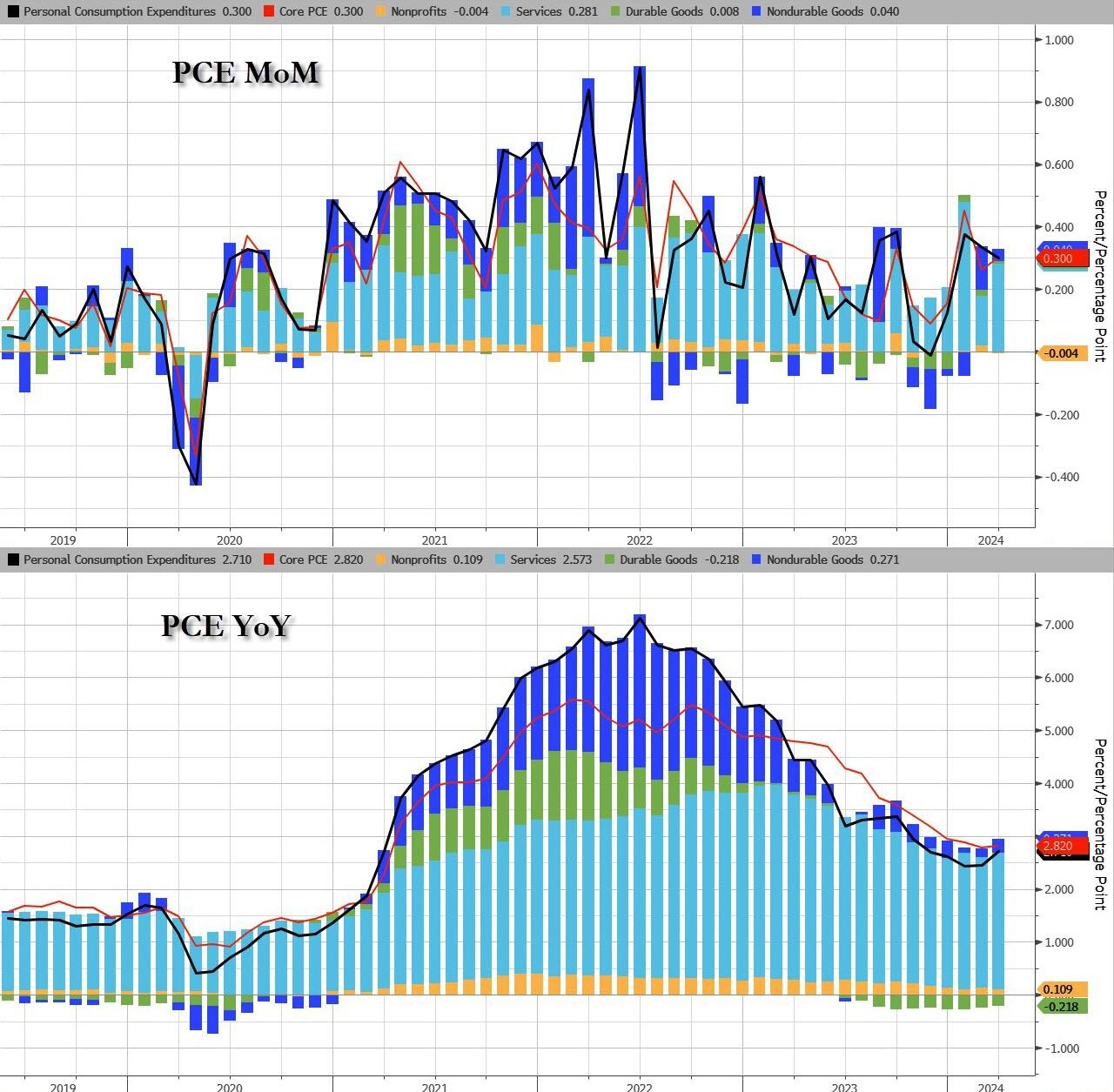

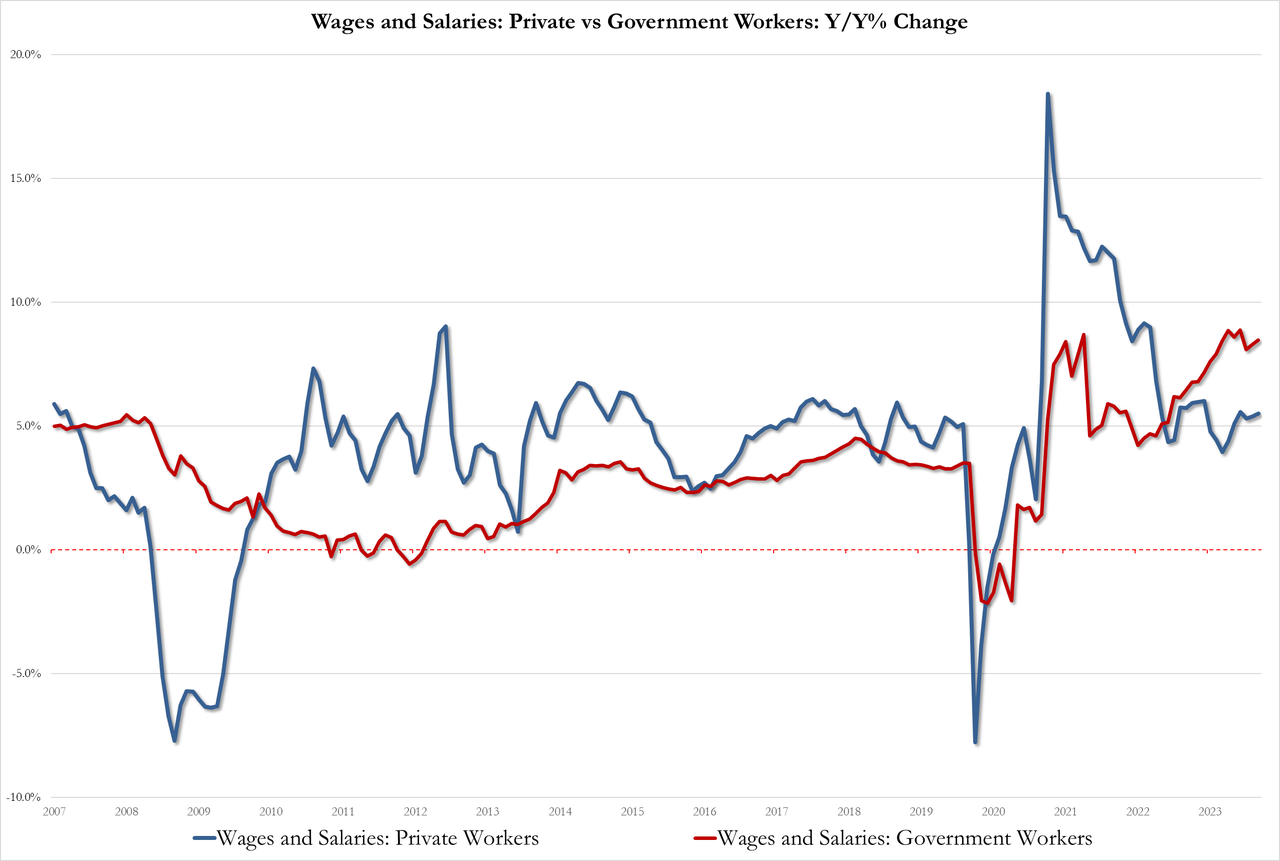

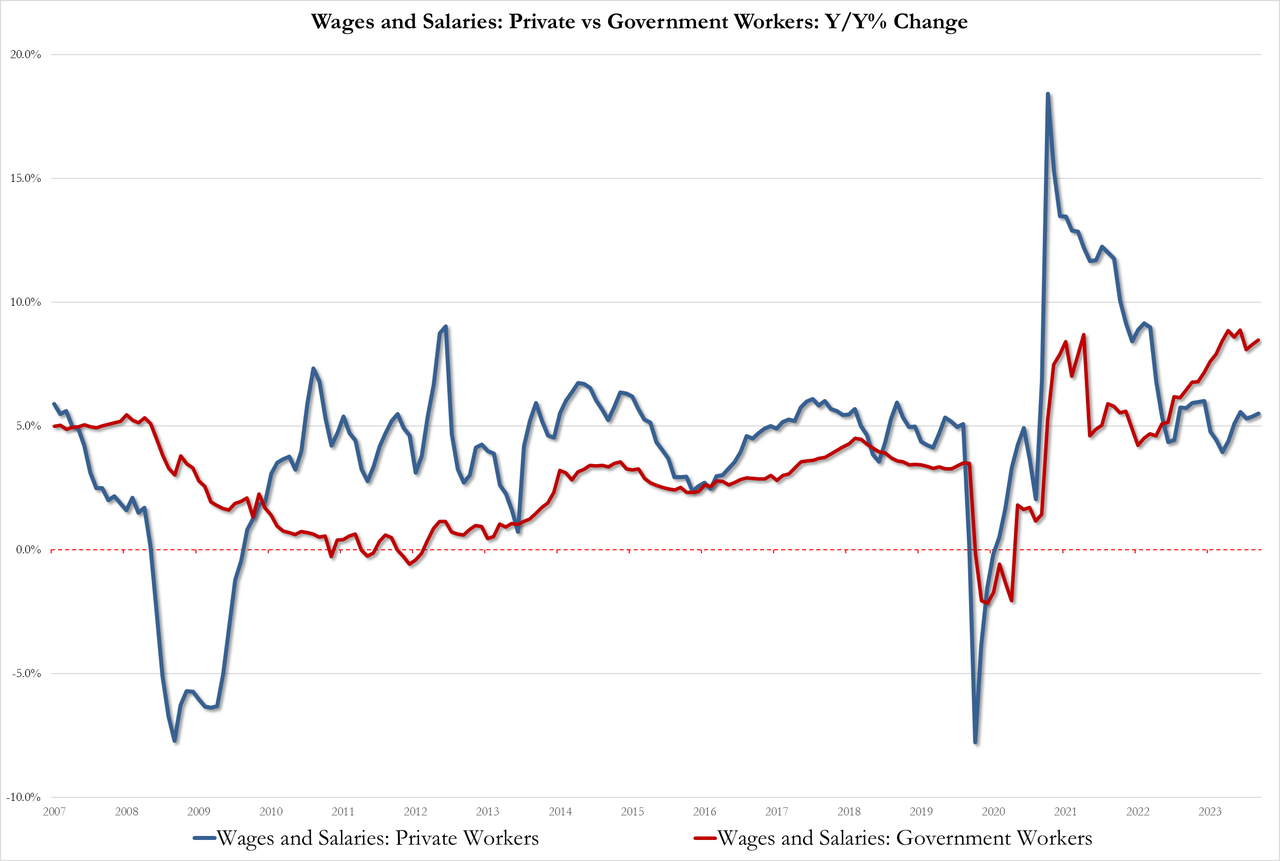

Today’s economic news highlights “Government Power.” Unproductive government jobs saw wages rise 8.5% YoY while productive private sector jobs saw wages rise by only 5.5% YoY. This is Bidenomics!!!

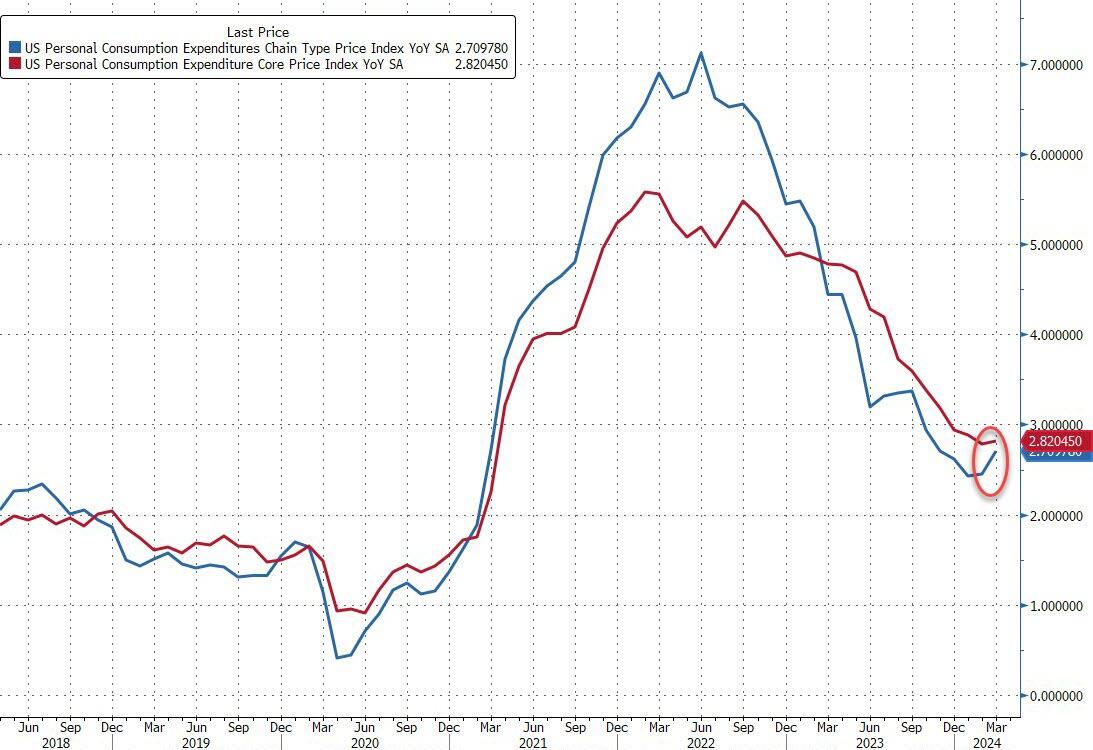

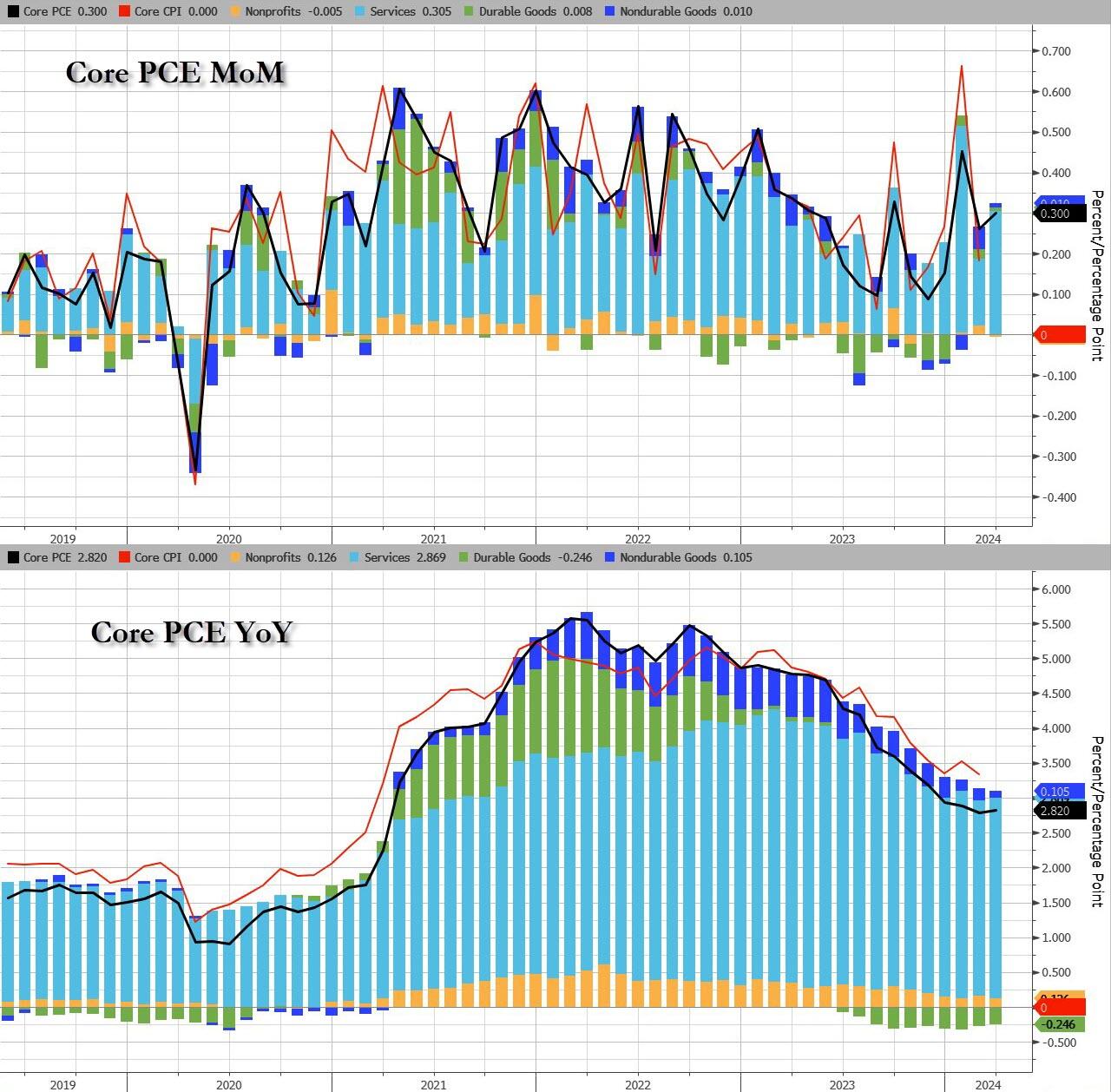

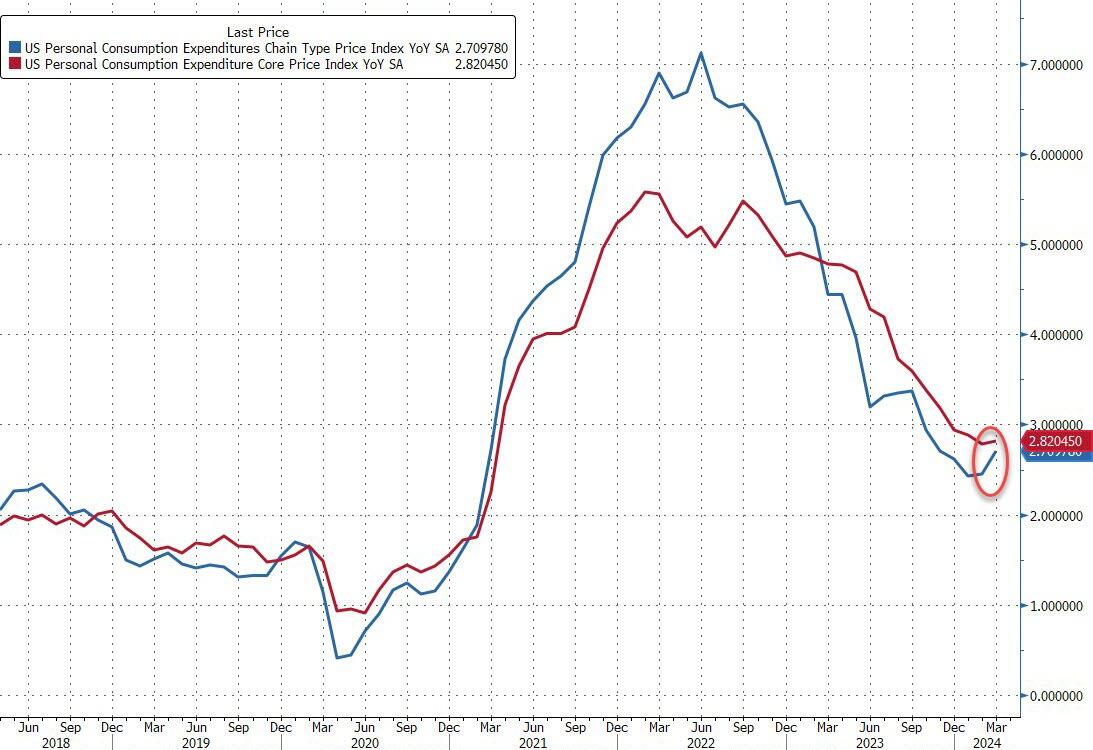

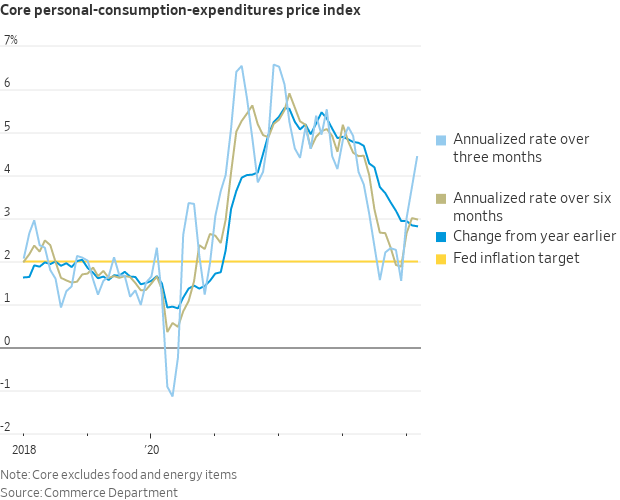

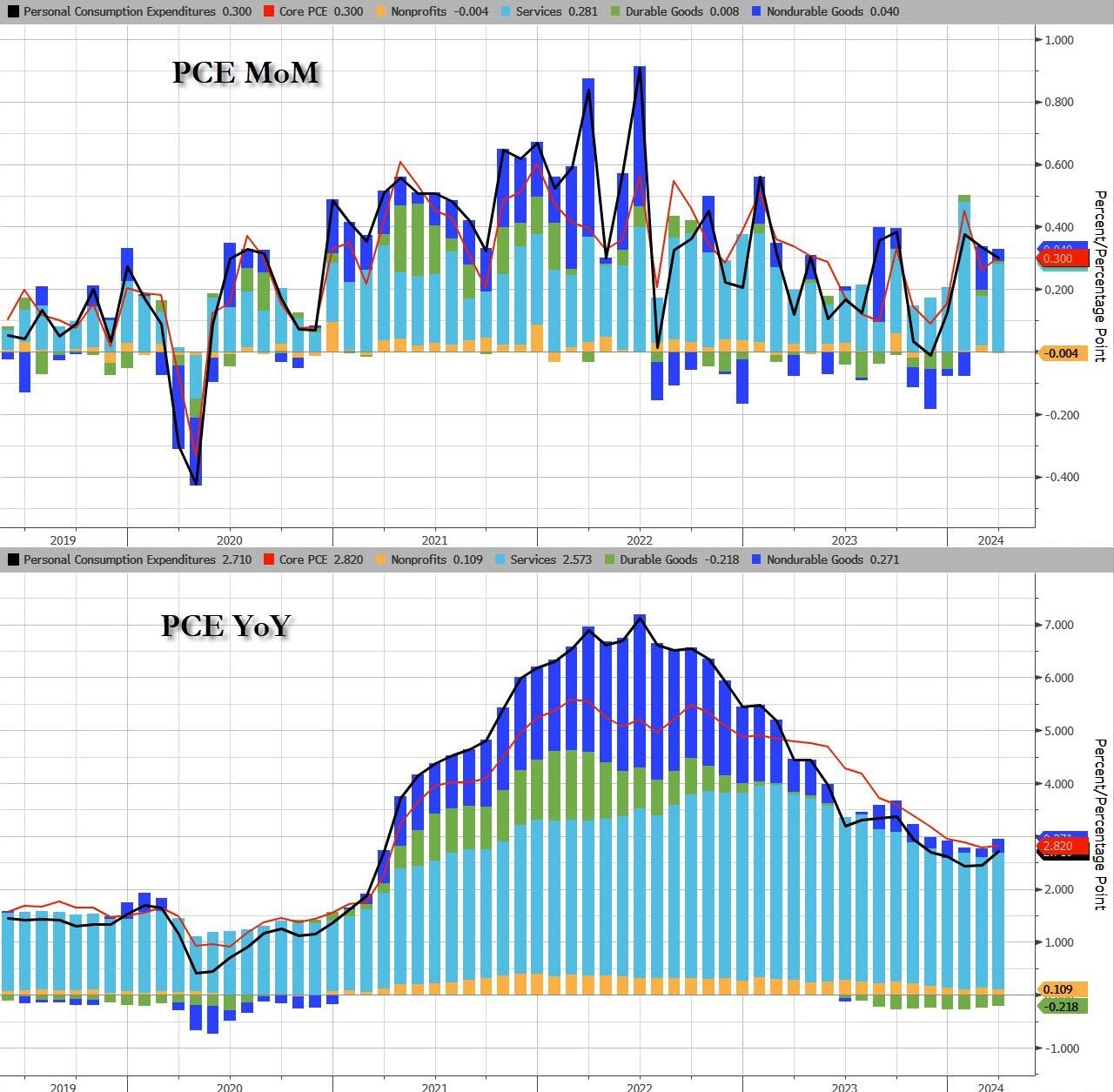

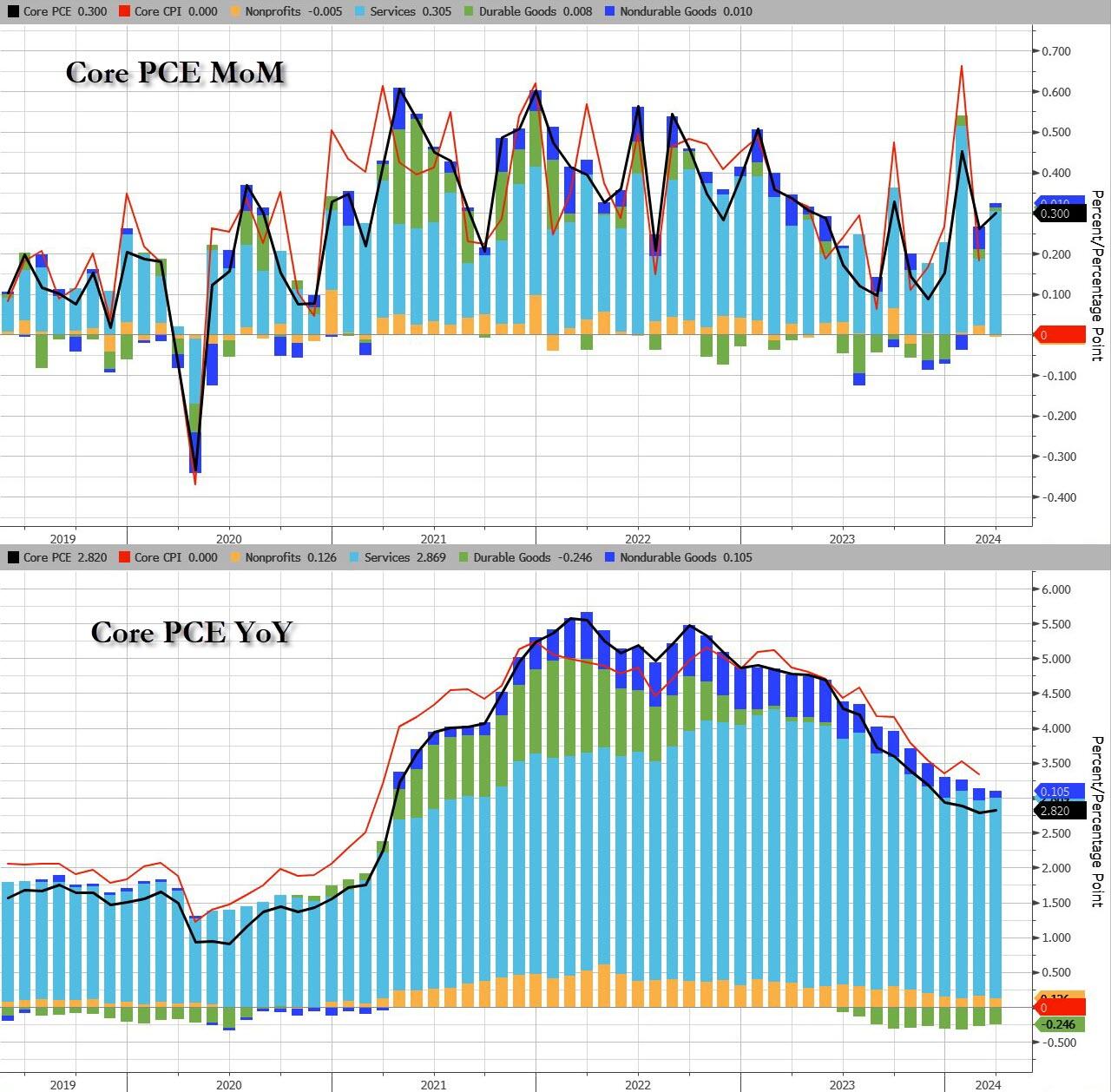

…the doves’ last chance for sooner than later rate-cuts is today’s Core PCE Deflator – often described as The Fed’s favorite inflation signal. Last month saw an uptick in the headline deflator and following yesterday’s core PCE rise for Q1, all eyes are on the March data released this morning.

However, both the headline and core PCE Deflator data printed hotter than expected (+2.7% vs +2.6% exp vs +2.5% prior and +2.8% vs +2.7% exp vs +2.8% prior respectively)…

Source: Bloomberg

The silver lining is that this hot PCE print is ‘dovish’ relative to the GDP-based data we saw yesterday, with whisper numbers of +0.4 to +0.5% MoM (vs the +0.3% print).

But still – it’s not good for the doves.

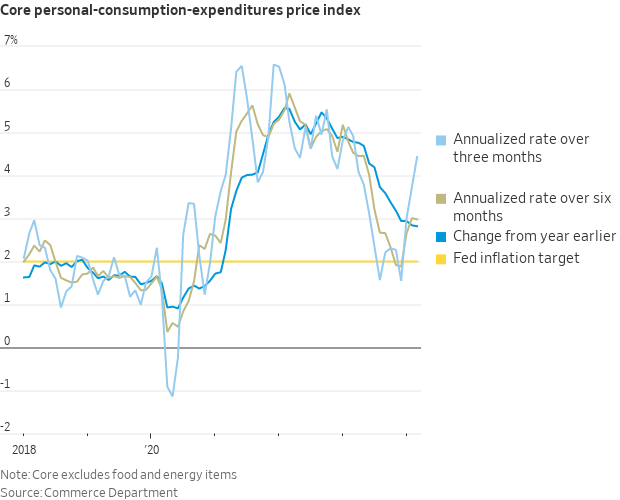

As WSJ Fed Whisperer Nick Timiraos notes, the 3-Month annualized core PCE jumped to 4.4%…

The Service sector led the MoM and YoY acceleration in headline PCE…

Source: Bloomberg

And for Core PCE, it was Services prices too that drove the acceleration…

Source: Bloomberg

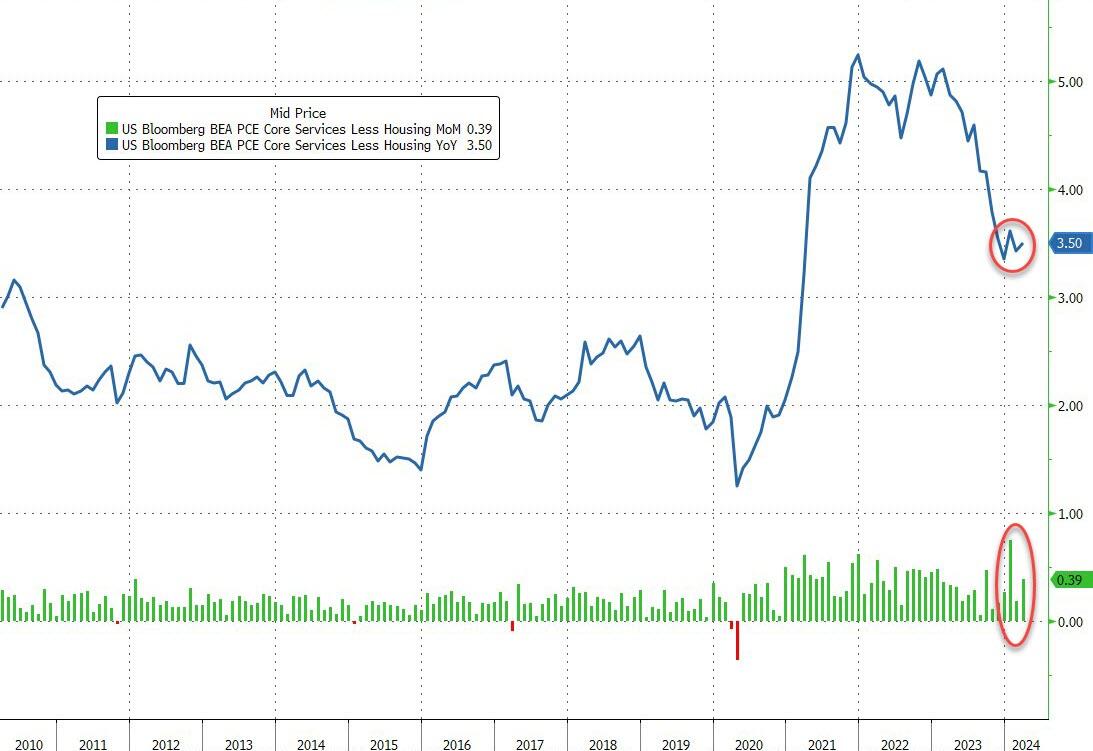

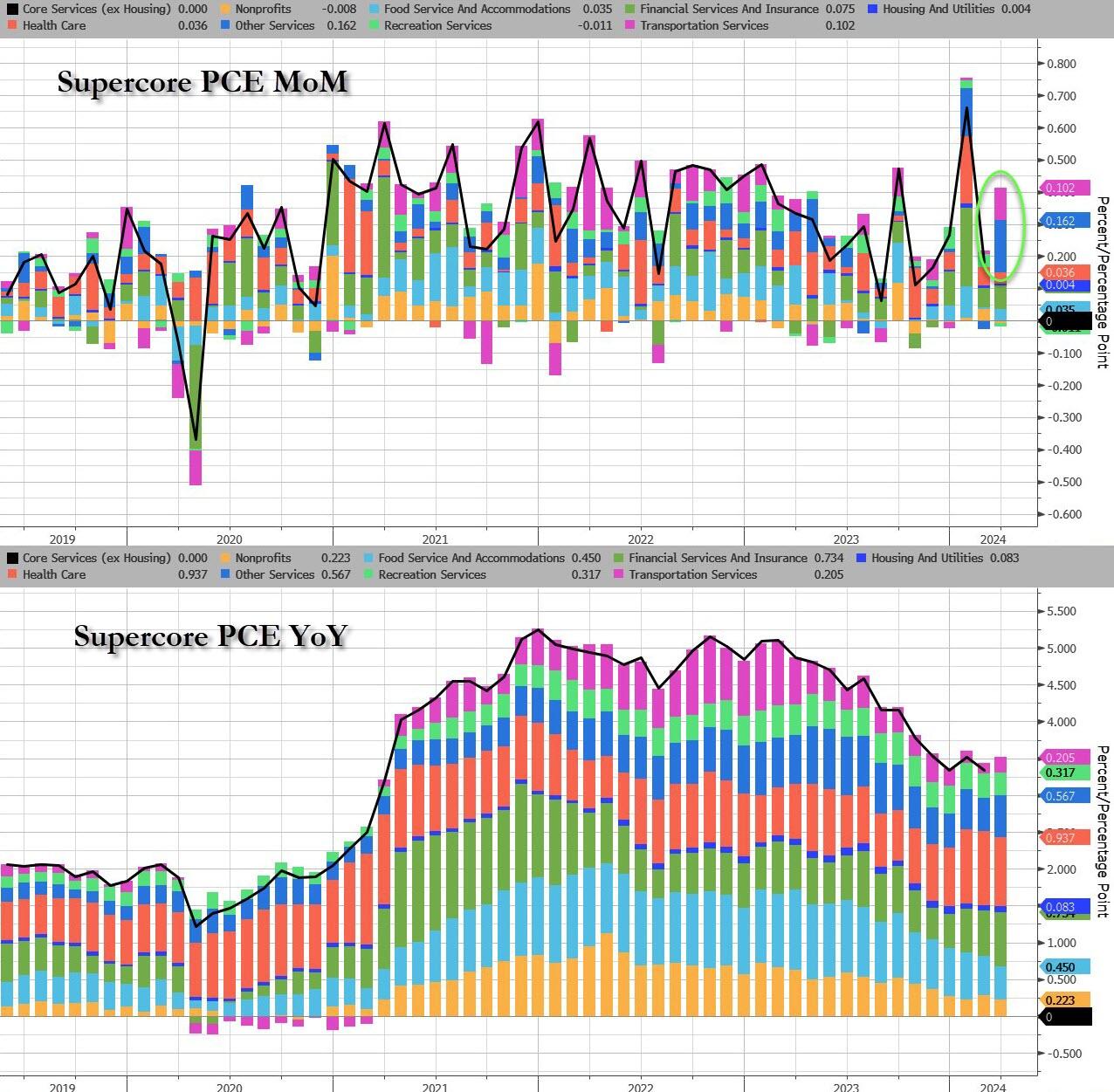

The so-called SuperCore – Services inflation ex-Shelter – rose once again, and was revised higher…

Source: Bloomberg

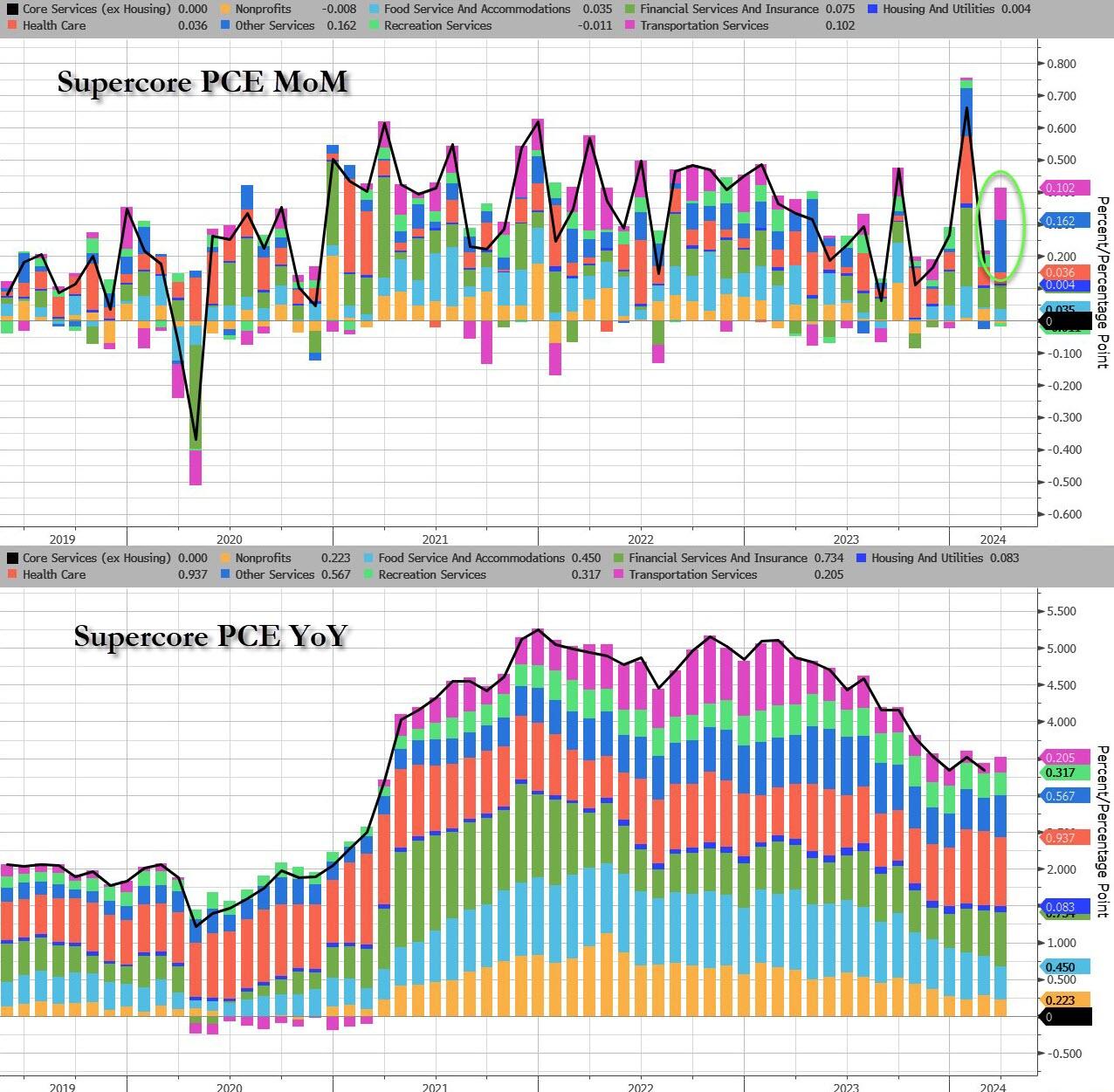

Stripping it back even further, Transportation Services and ‘Other Services’ were the biggest gainers in SuperCore…

Source: Bloomberg

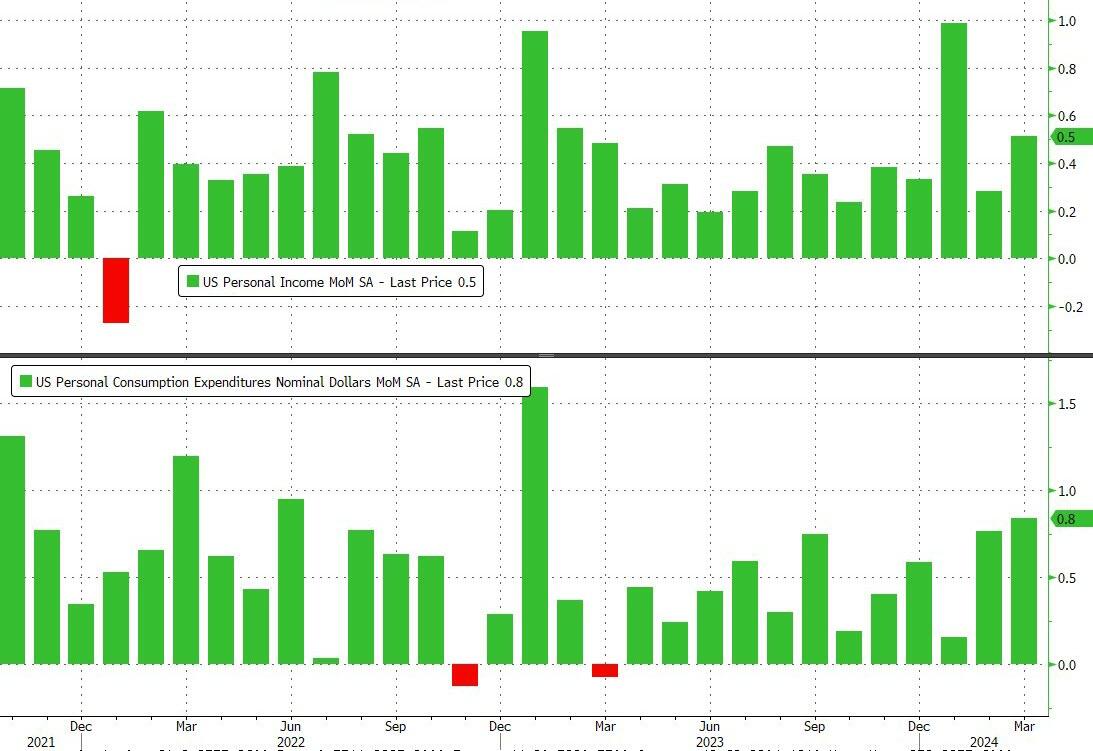

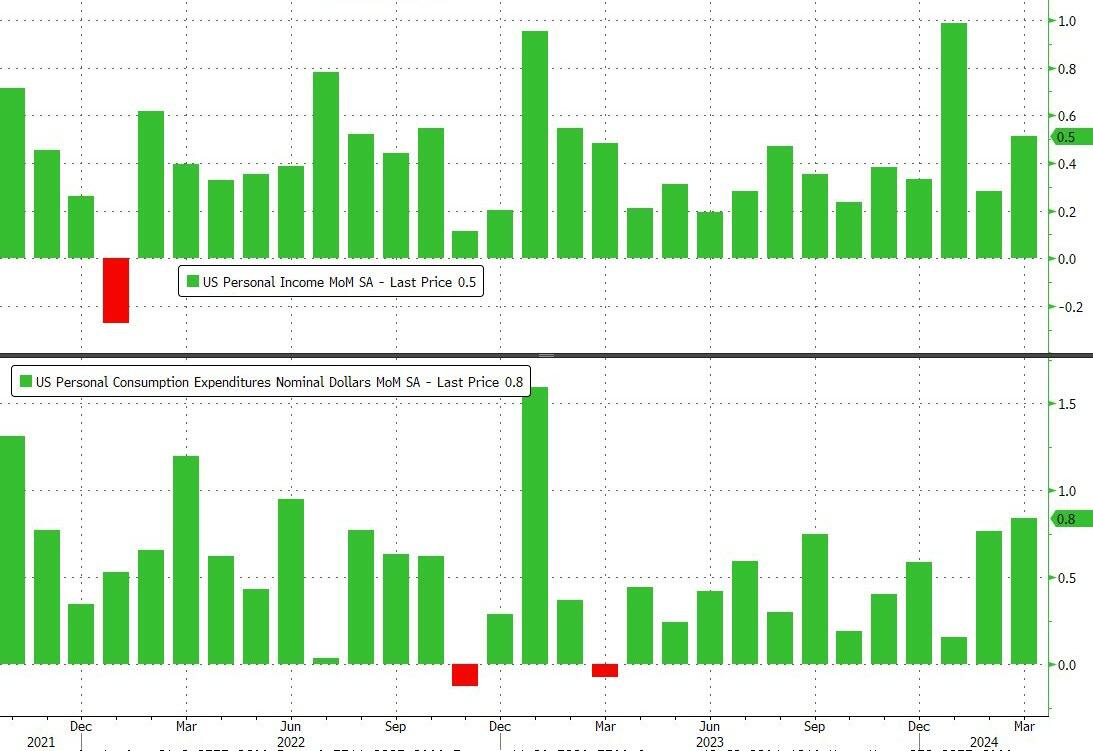

Income and Spending both rose again on a MoM basis with spending outpacing income (again). The 0.8% MoM rise in spending was the highest since Jan 2023…

Source: Bloomberg

Spending is accelerating fast relative to incomes (on a YoY basis) – and remember this is all nominal…

Source: Bloomberg

On the income side, government and private wage growth accelerated:

Govt wages rose to 8.5% YoY, from 8.3%, the highest Dec 22

Private wages rose to 5.5% YoY, from 5.4%, highest since Dec 22 as well

Source: Bloomberg

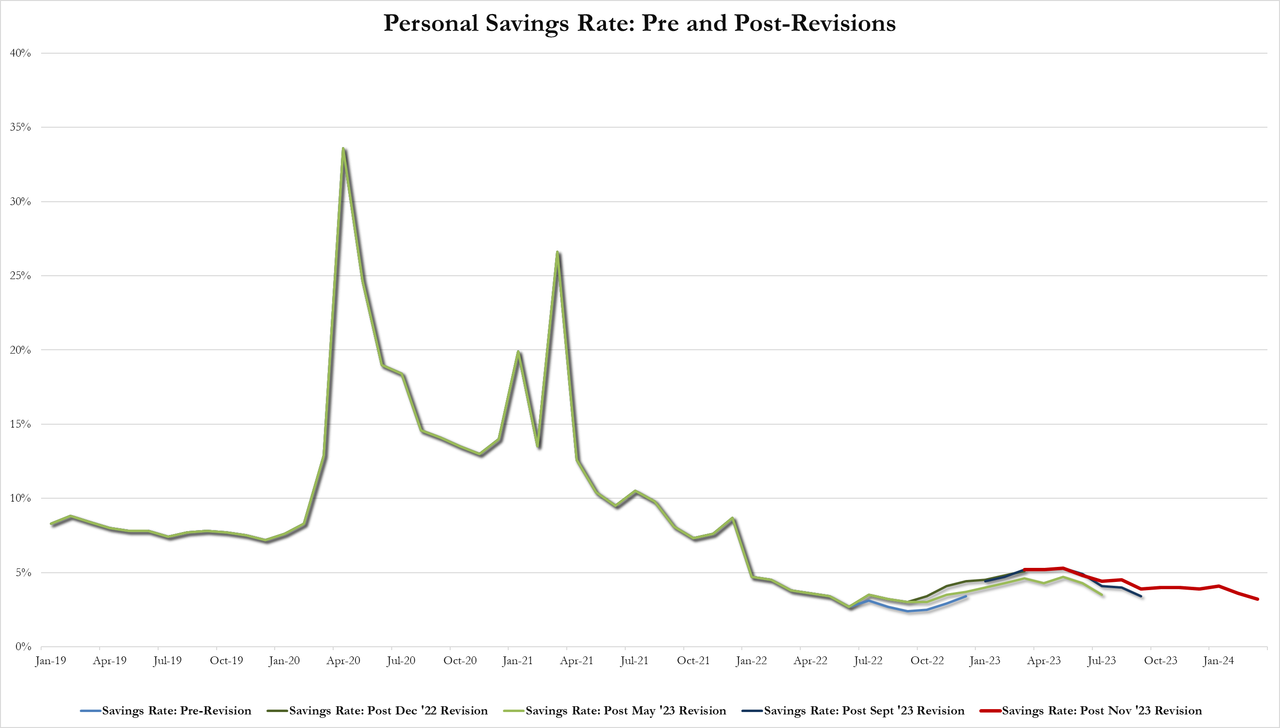

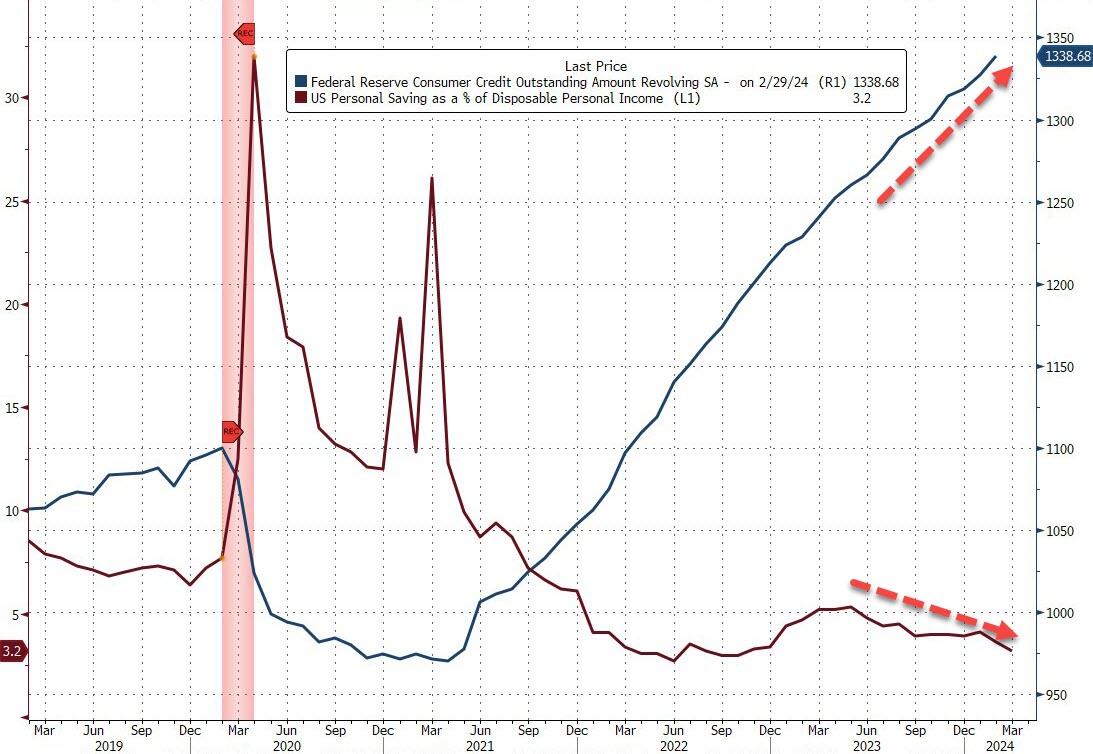

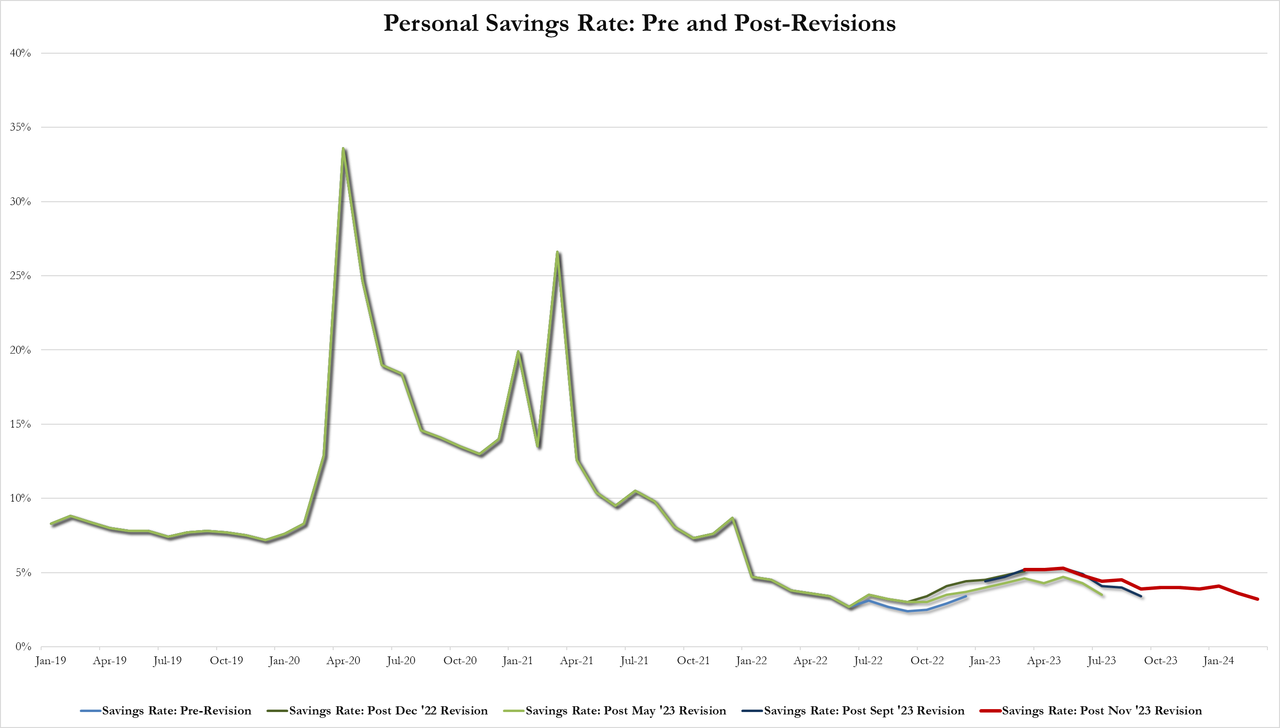

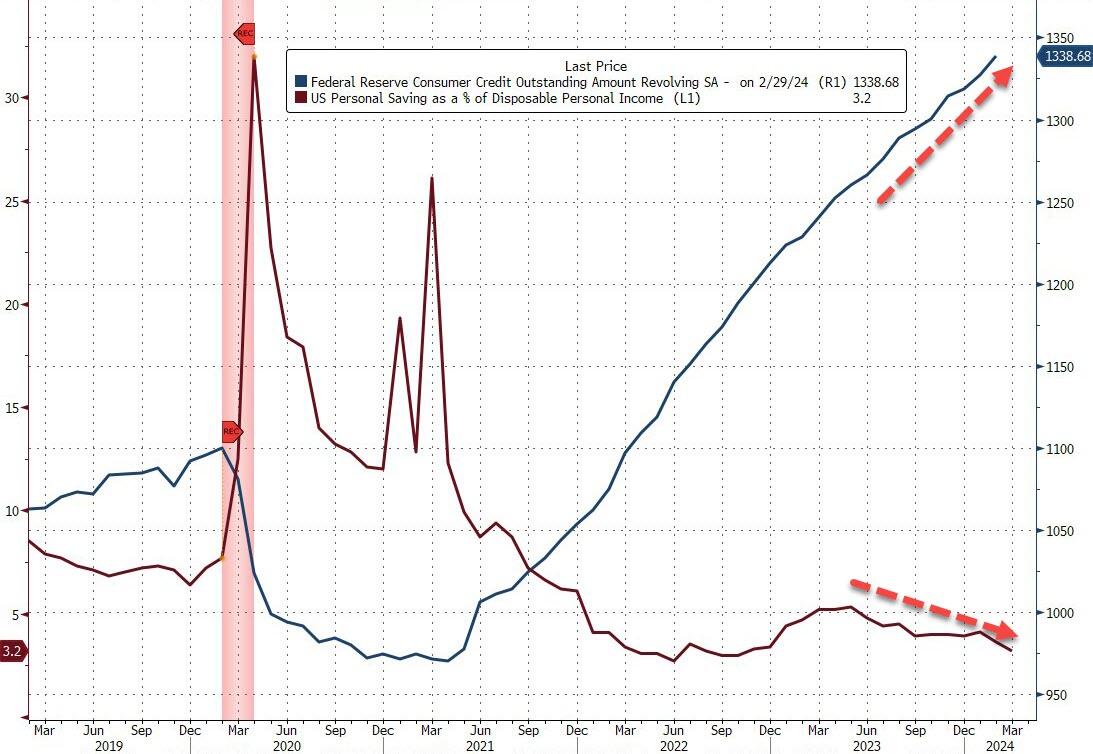

Which meant the personal savings rate plunged to 3.2% from 3.6% – its lowest since Nov 2022…

And the soaring credit card balance explains how people are getting by…

Source: Bloomberg

And all this amid the fourth straight month of government handouts…

Source: Bloomberg

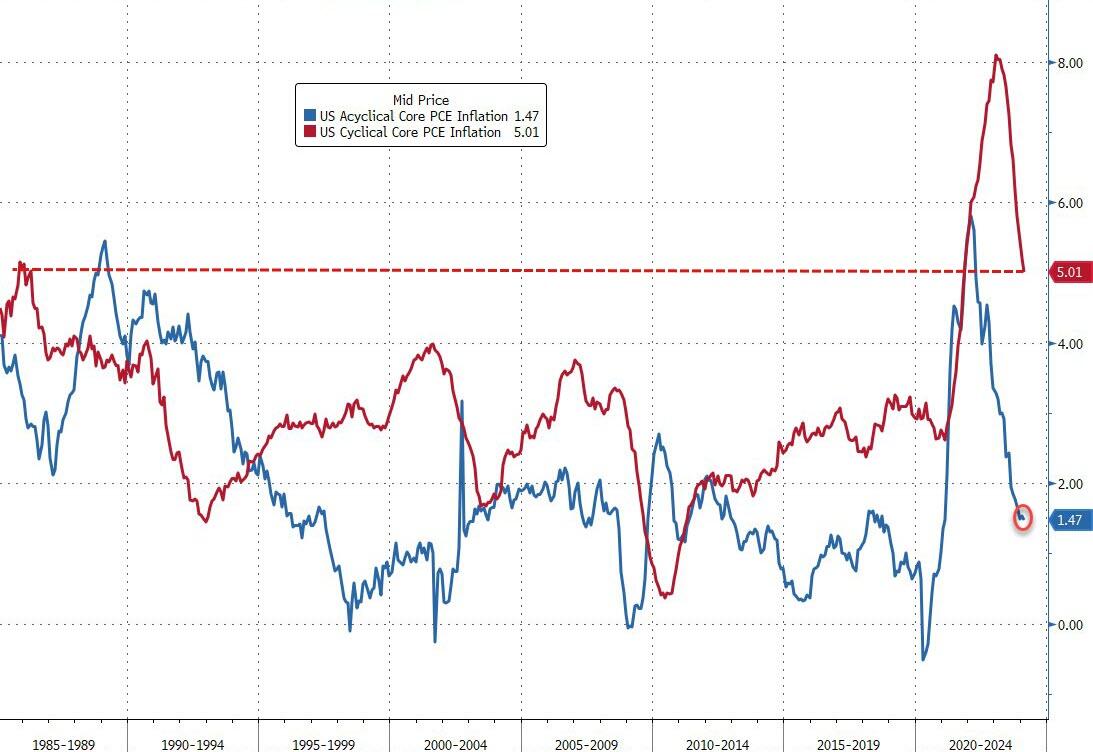

Finally, while the markets are exuberant at the survey-based disinflation, we do note that it’s not all sunshine and unicorns. The vast majority of the reduction in inflation has been ‘cyclical’…

Source: Bloomberg

Acyclical Core PCE inflation remains extremely high, although it has fallen from its highs.

Is The (apolitical) Fed going to be able to cut at all this year like Joe Biden said they would?

The Green Slime! The global movement towards Green Energy (or global Marxist movement) is really The Green Slime! Or maybe it should be renamed “The Red Slime.”

And then we have Hertz dumping its inventory of EVs. A slew of used Teslas have hit the Hertz car sales website after the company announced Thursday it planned to sell off 10,000 more electric vehicles from its fleet than originally planned, bringing the fire sale’s total to 30,000. Perhaps one of the reasons you can get such a good deal on a Tesla at Hertz right now is that the outlook for EV value retention is pretty grim at the moment.

Given the incidents of electric cars catching fire, perhaps saying its a fire sales is a bad choice of words. But what it says is that DESPITE massive incentives to buy EVs, consumer demand stinks. Although Transportation Secretary Pete Buttigieg will claim the market is booming.

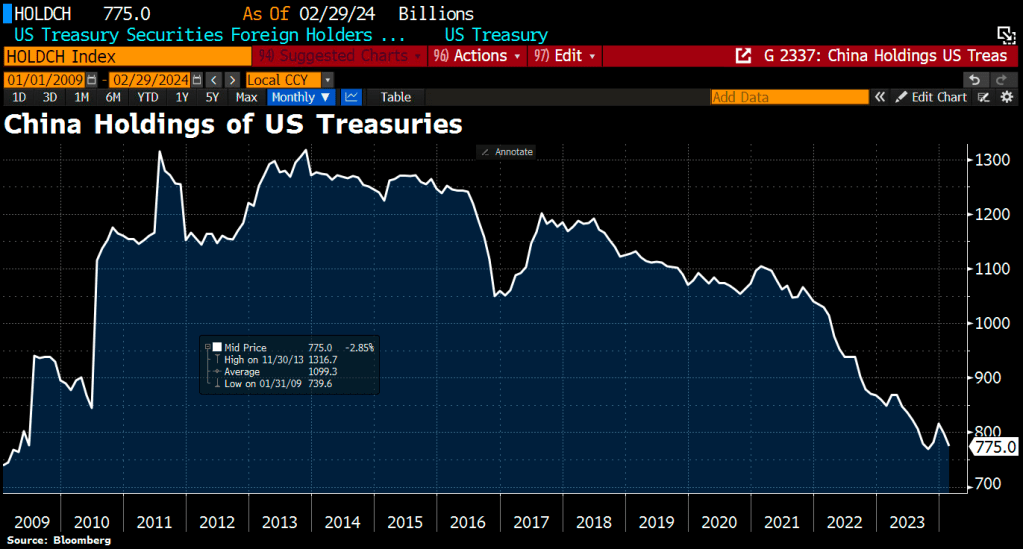

How bad is the trainwreck that is the Biden Regime? China is bailing on US Treasuries.

The Biden Regime is hereafter known as The Green Slime, given their horrible policies. Unfortunately, The Green Slime is here already … and Hertz knows customers don’t want them at least on a temporary basis.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.