Despite the open borders where millions of low wage workers and parasites pour across into the US, we still see 1-unit housing starts plunged -7.4% YoY in June as The Fed continues tightening.

Multifamily starts actually fell worse than 1 unit starts. 5+ unit starts were down -11.56% MoM. Multfamily permits were down -13.52%.

And it just isn’t little girls that Biden is creepy about (like the family member we all keep our kids away from), Biden is creepy towards adult women too! These guys, like most normal people, aren’t digging Old Joe’s creepiness.

The Federal Reserve, an organization that even George Orwell would find outrageous, is a Minsky Moment Machine!

A Minsky Moment refers to the onset of a market collapse brought on by the reckless speculative activity that defines an unsustainable bullish period. Minsky Moment crises generally occur because investors, engaging in excessively aggressive speculation, take on additional credit risk during bull markets.

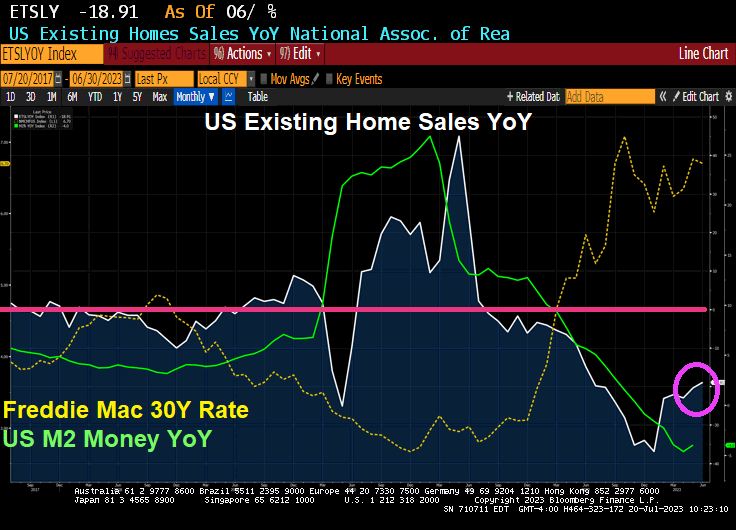

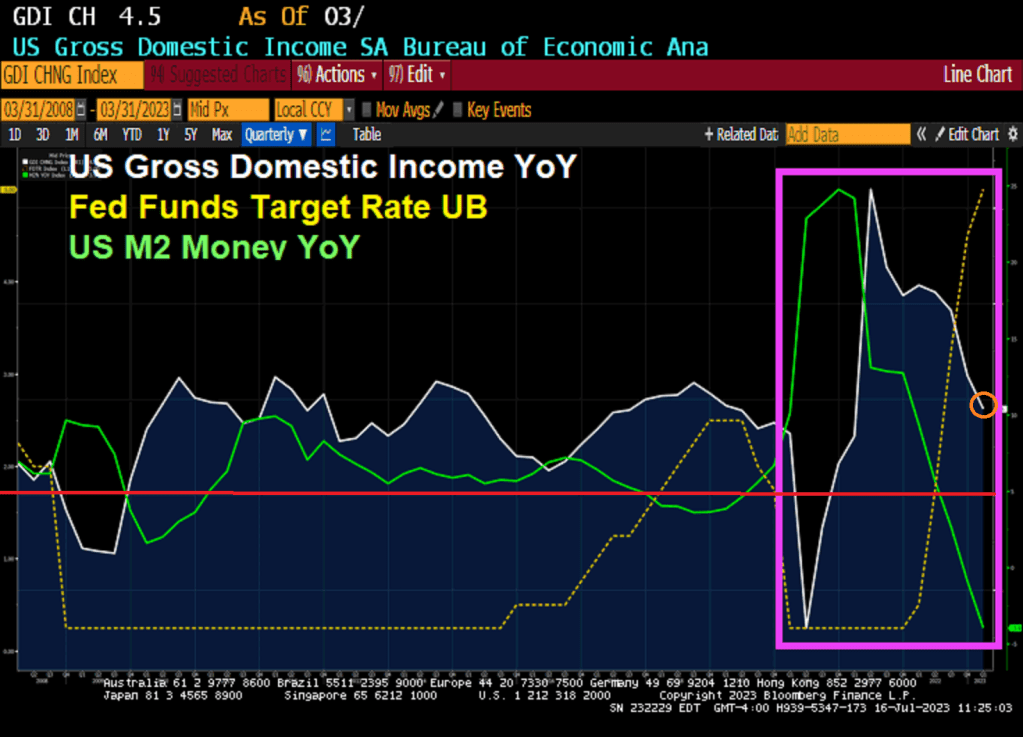

And since Covid and the Great Monetary Expansion to fight it helped creates massive inflation and helps the 1% get wealthier and wealthier. BUT as M2 Money growth slows, the 1% are losing their position as top dogs in the economy. Not by much (see pink circle), but a little.

And The Federal Reserve helps create the monetary expansion through low rate policies, fueling credit and asset bubble expansion. Greenspan, Bernanke and Yellen were the masters at creating a Minsky Moment (named after Hymen Minsky, the late Washington University of St Louis economist).

Then we have the latest bit of bad news. US Industrial Production year-over-year of -0.43% as M2 Money growth evaporates.

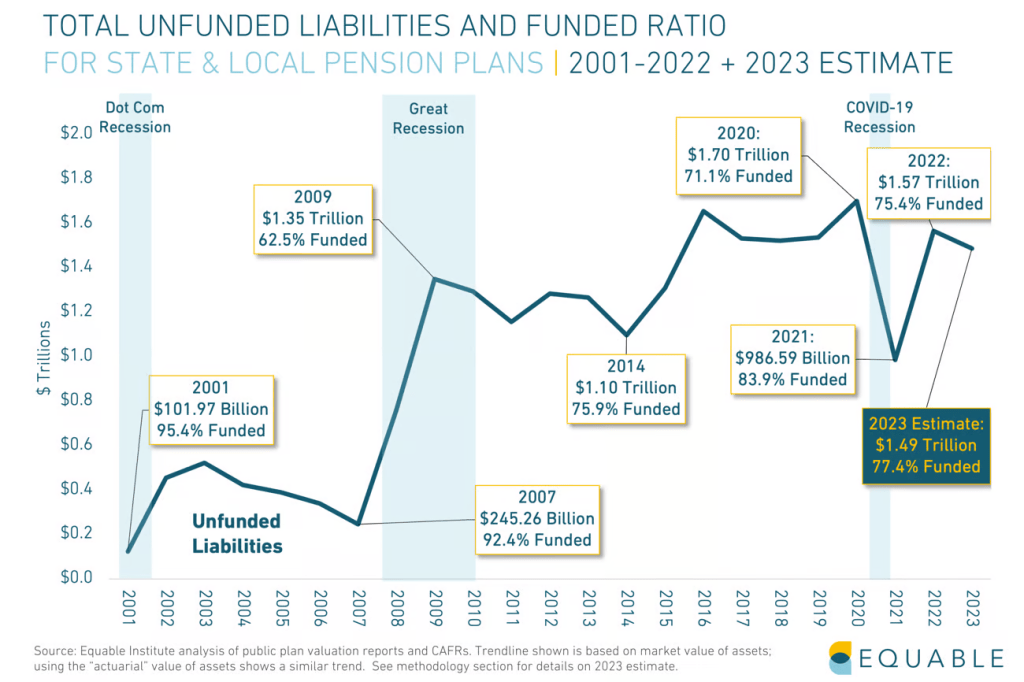

After The Fed’s insertion of massive monetary in 2008, continued stimulus until the second massive stimulus burst in 2020, unfunded liabilities of pension funds have worsened. Another possible Minsky Moment created by the Kafkaesque Fed. Kafedesque??

The Fed’s Powell: Let’s play a game … and make the 1% even wealthier!!!

The Fed. The beauty of failure. When the economy starts failing, The Fed goes wild.

Yes, one of the cornerstones of Bidenomics is the massive expansion of (impractical) electric vehicles (or EVs). You know, those mondo expensive cars that run out of power after a couple of hundred miles requiring a lengthy recharge (kind of makes long distance trips the domain of Internal Combustion Engine (ICE) cars.

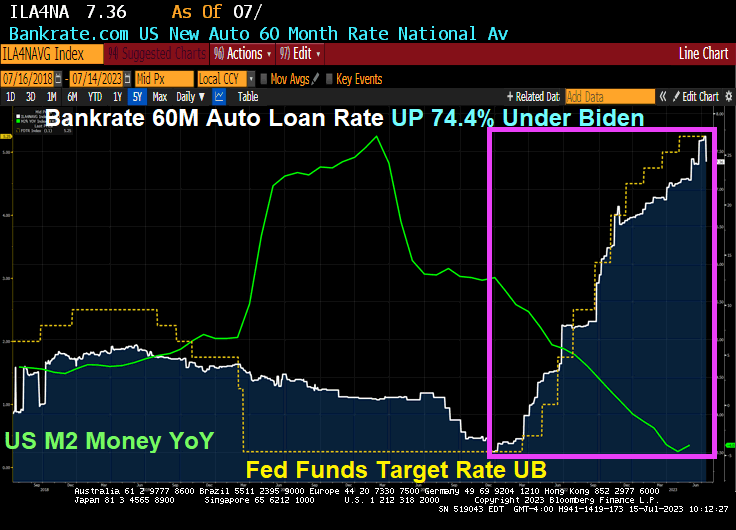

But as Biden/Congress spent trillions on green energy (massive subsidies for anything green), we noticed that 1) inflation hit 40 year highs and 2) The Fed intervened to raise rates. So, now we see that 60-month auto loan rates are now around 7.36%, up 74.4% under “Middle Class Joe.”

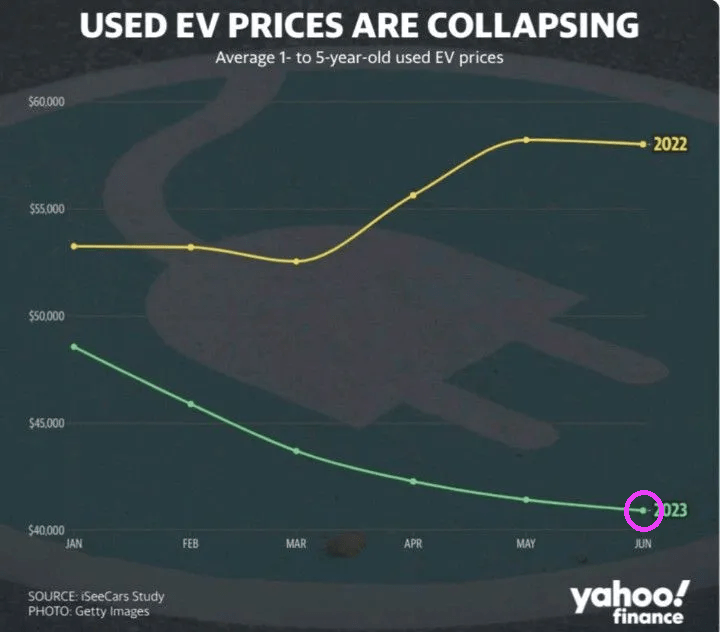

And we see used EV prices collapsing like a week-old soufflé.

Speaking of green energy fraud, here is the leader of the green energy fraud movement, John F’ing Kerry. Aka, Heinz Planes Grifter.

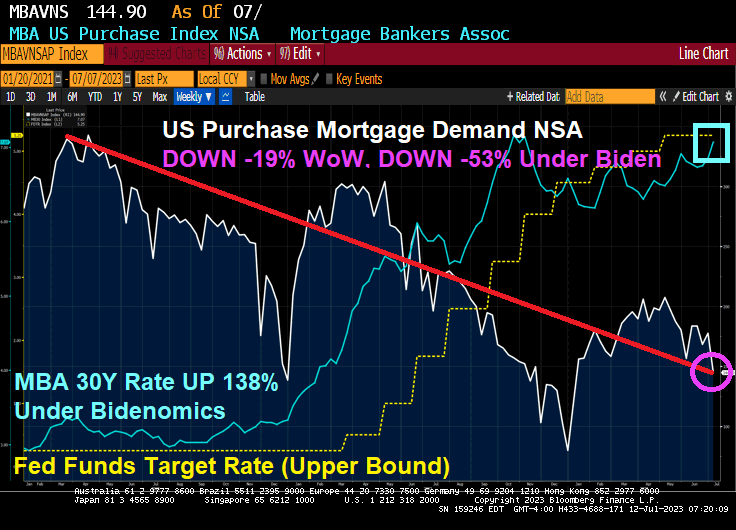

As Bidenomics (why Biden would brag about massive inflation in energy, food and shelter is beyond me), lurches forward, we have another shred of lousy economic news: US mortgage purchase demand fell -19% from the previous week and is how down -53% under Bidenomics).

Mortgage applications increased 0.9 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending July 7, 2023. This week’s results include an adjustment for the observance of Independence Day.

The Market Composite Index, a measure of mortgage loan application volume, increased 0.9 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 19 percent compared with the previous week. The Refinance Index decreased 21 percent from the previous week and was 39 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 2 percent from one week earlier. The unadjusted Purchase Index decreased 19 percent compared with the previous week and was 26 percent lower than the same week one year ago.

Yes, mortgag purchase demand is down a staggering -53% under Bidenomics (another word for the next best thing to Socialism which is Federal control of where the trillions are spent). Economic traffic led by The Keystone Kops.

Here is the rest of the data. Mark Zandi will look at the seasonally adjusted data, I look at the raw or non-seasonally adjusted data.

On a different note, I watch “Sound of Freedom” last night. A tremendous film highlighting the problem of pedophelia and child sex slavery in the US and Latin America. Very, very moving. Biden should be ashamed for cancelling Trump’s anti trafficking program.

The US has passed the 32 trillion mark in national debt, and is going much, much higher. More like 32 tons on the back of taxpayers. When we add unfunded liabilities like Social Security, Medicare and Medicaid, the tab soars to $224.5 TRILLION.

In the first six months of 2023, there were 340 corporate bankruptcies, topping every other comparable span in 13 years, according to S&P Global Market Intelligence. This is up 93 percent from the same time a year ago and higher than in 2020, when there was a spike during the early days of the coronavirus pandemic.

There were 54 recorded corporate bankruptcy filings in June, unchanged from the 54 bankruptcies in May. Last month, some of the most notable companies to submit filings were Lordstown Motors, Rockport Co., Instant Brands Acquisition Holdings, and iMedia Brands.

“Lordstown Motors Corp. filed for bankruptcy June 27, with plans to restructure its business and seek a buyer, according to a company release. The electric vehicle manufacturer’s assets include its Endurance pickup truck and related resources,” S&P noted in the July 6 report.

“Instant Brands Acquisition Holdings Inc. also sought bankruptcy protection June 12. The tightening of credit terms and higher interest rates had impacted the company’s liquidity levels, according to an official release. The company has also already secured $132.5 million from existing lenders and plans to continue discussions with its financial stakeholders.”

Year-to-date through June, 15 companies with more than $1 billion in liabilities filed for bankruptcy, such as Cyxtera Technologies, Diebold Holding, Bed Bath & Beyond, Diamond Sports Group., and Party City.

Epiq Bankruptcy, a U.S. bankruptcy filing data provider, confirmed that 2,973 total commercial Chapter 11 bankruptcies were filed in the first half of 2023, up 68 percent from the same period in 2022.

Higher Interest Rates Impacting Businesses

Banking experts purport that higher interest rates are the leading cause of the increase in corporate bankruptcies. Many businesses either maintain vast debt loans that will require refinancing or need more liquidity to stay afloat.

“The increase in commercial and individual bankruptcy filings during the first half of 2023 underscores the economic challenges faced by businesses and individuals,” said Mr. Gregg Morin, Vice President of Business Development and Revenue at Epiq Bankruptcy, in the report. “Our objective is to provide bankruptcy professionals with timely and accurate data necessary for analyzing stakeholder volumes and trends for making informed business decisions.”

The situation could be exacerbated should the Federal Reserve pull the trigger on two more rate hikes this year. The futures market is penciling in a quarter-point boost to the benchmark fed funds rate at this month’s Federal Open Market Committee (FOMC) policy meeting.

Meanwhile, according to a recent Fitch Ratings report, the corporate default rate is projected to climb to as high as 4.5 percent in 2023, up from the previous forecast low of 2.5 percent. The updated projections reflected “the tighter lending conditions and capital access resulting from stress in the banking sector and inflation uncertainty.”

However, some argue that corporate bond market indicators are “less ominous.”

“The interest rate differentials, or spreads, between the 10-year U.S. Treasury note and investment grade (IG) and high yield (HY) corporate bonds continue to hover within their average width over the past 25 years, a bond market signal indicating the likelihood of a less severe recession, with traders pricing in fewer corporate defaults,” wrote John Lynch, the CIO at Comerica Wealth Management, in a research note.

Economists contend that the worst corporate bankruptcies typically occur one or two years into a recession. Today, they are happening before the official start of an economic downturn as the U.S. economy is still expanding.

What’s happening?

“Simple,” says Mr. Pete St. Onge, a Heritage Foundation economist, “banks aren’t lending.”

“Banks are battening down the hatches, hogging their bailout money instead of lending it out,” he said in a recent podcast. “That credit crunch means not only do we get bankruptcies like in any recession, on top of that, we get a lending wall that cuts off even the healthy businesses. Of course, their jobs go down with them.”

Since the Federal Reserve launched the Bank Term Funding Program (BTFP) following the Silicon Valley Bank collapse in March, financial institutions have kept tapping into these emergency lending facilities. After hitting a record high at above $103 billion at the end of June, it remains elevated at $102 billion.

32.5 trillion in debt and $192 trillion in unfunded liabilities which means a total of $224.5 total debt + liabilities.

This is Bidenomics. Spend trillions, borrow trillions, promise entitlements. Rinse, repeat.

Bidenomics, the massive Federal spending spree that helped drive inflation to 40 year highs, is the most top-down Soviet-style command economy model imaginable.

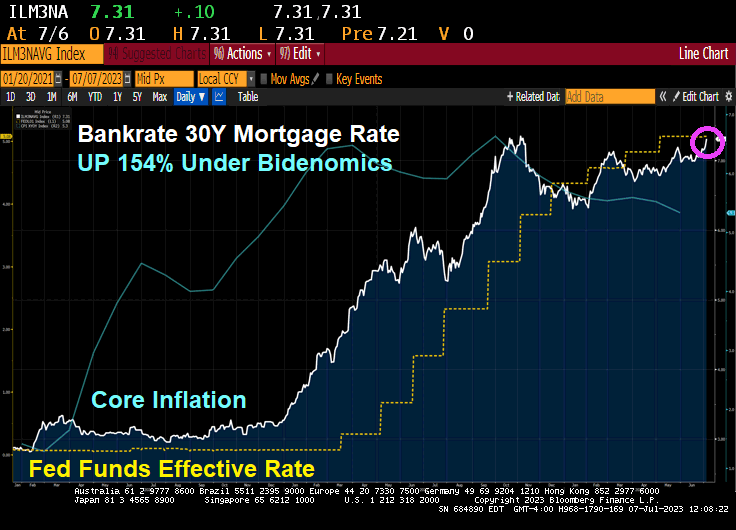

As The Fed battles Bidenflation, the 30-year mortgage rate has now risen to 7.31%, a far cry from 2.88% when Biden was installed as President. That is a 154% increase in the 30-year mortgage rate under Bidenomics.

What is Bidenomics? It isn’t what Press Secretary Karine Jean Pierre thinks. She said Biden hates “trick down economics”. Instead, Biden prefers a Soviet-style command economy where The Federal Government spends trillions of dollars and directs where the money goes. We also have the Socialist Federal Reserve that relies on rate manipulation to achieve policy results.

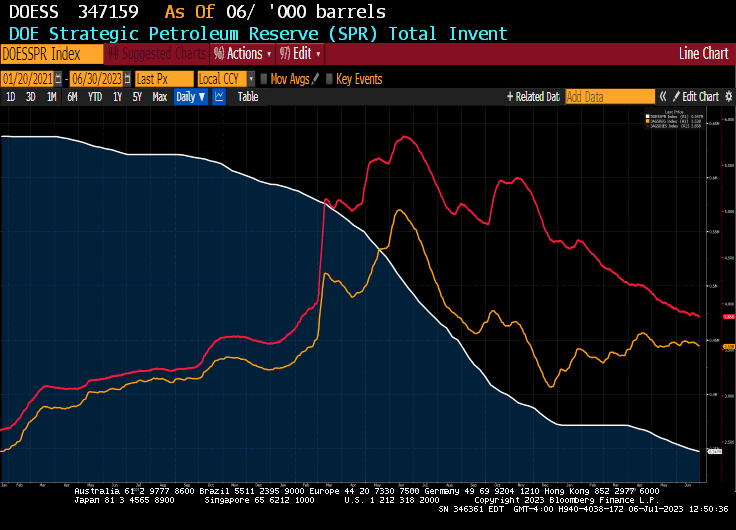

A good example of Biden’s Soviet-style “Bidenomics” is his use of the Strategic Petroleum Reserve (SPR). Biden has now drained almost 50% of the SPR from when he was sworn in as President. And has drained the SPR for 14 straigth weeks to manipulate gasoline and diesel fuel prices in an effort to lower fuel prices ahead of the 2024 Presidential election. Watch Biden suddenly stop caring about fuel prices once he wins reelection!

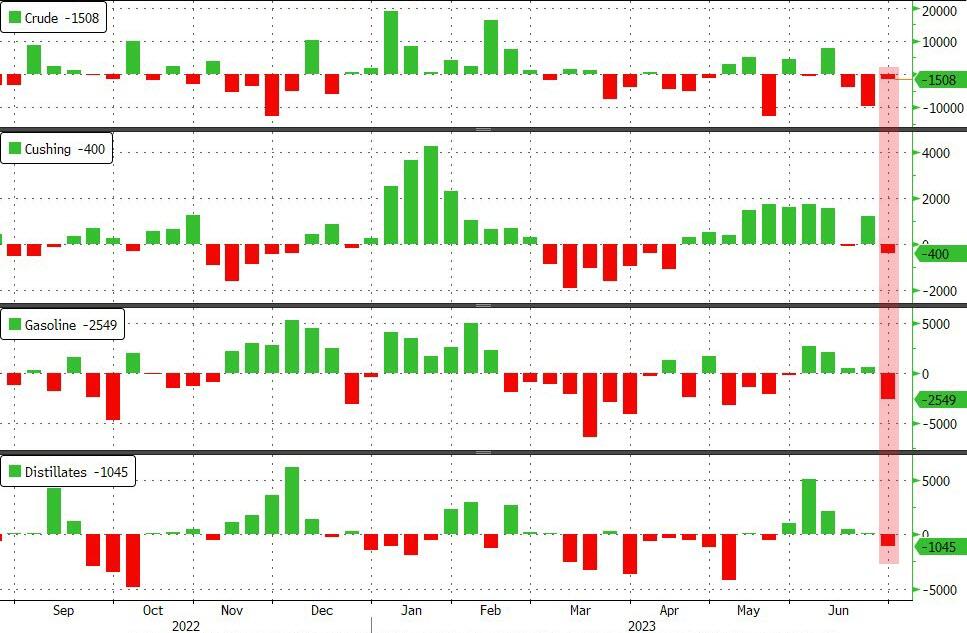

After last week’s huge draw, expectations were for a smaller draw (which API showed last night), but the actual crude draw was smaller – just 1.5mm barrels. Stocks at the Cushing hub fell 400k barrels and products also saw notable draws..

At least we now know who left cocaine in the White House!

The good news (if true)? ADP announced that 497k jobs were added in June.

The bad news? A 497k print on jobs (many seasonal, it is summer!) almost guarantees that The FOMC (Fed Open Market Committe) will raises rates again at at the July meeting.

The 2-year Treasury yield is up over 10 basis points.

The 2-year Treasury yield is up 16.5 basis points.

Bticoin Cash is up 10% today.

I should have bought nickel!

Why is Biden sending Treasury Secretary Janet “The Marxist Midget” Yellen to China? A Treasury Secretary and former Federal Reserve Chair? Likely trying to convince China that our $32 TRILLLION AND GROWING national debt is not a problem, since China is the third largest holder of US Treasury debt (after The Fed and Japan). Note that China has decreased its holdings of US Treasuries by -25.6% since January 2018.

Hopefully, Yellen isn’t acting as a bag man for The Biden Crime Family. 10% for The Big Guy?? How much does Yellen get??

You must be logged in to post a comment.