The US Empire State Manufacturing Survey General Business Conditions, that is. It just crashed and burned (-31.3) in August, the lowest reading since The Great Covid Shutdown and before that The Great Recession.

The inverted US Treasury yield curve (10Y-2Y) is beginning to make sense.

The 2020 Covid outbreak led to a massive (and generally awful) reaction. There were economic shutdowns that caused extensive damage (particularly to small firms), but it was the massive overreaction by The Federal government in terms of Covid relief and The Federal Reserve’s expansion of the money supply that caused considerable damage.

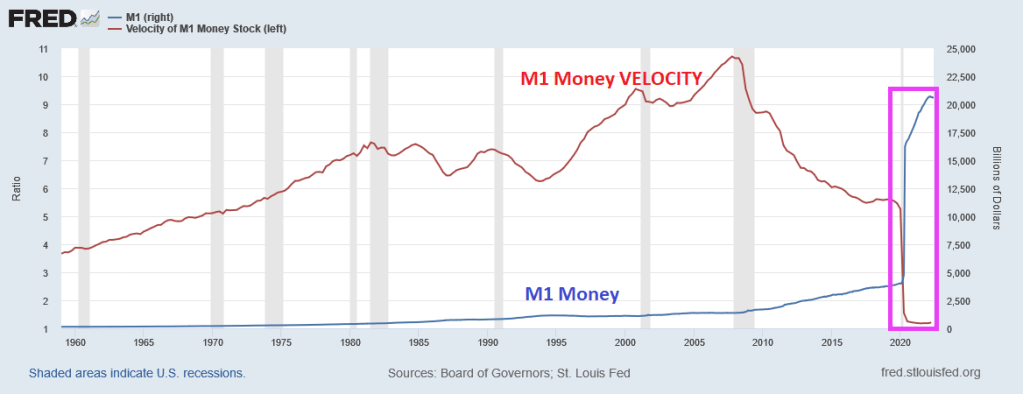

One truly horrific chart is that of M1 Money and M1 Money Velocity (M1/GDP). M1 Money surged with Covid driving M1 Money Velocity down to levels never seem before.

The broader measure of money, M2, isn’t as dramatic, but we also see that M2 Money VELOCITY has plunged to levels never seen before.

What does low money velocity indicate? Simply put, The Fed is printing trillions of dollars, but GDP isn’t moving much. But that won’t stop Congress from spending (and using The Fed to buy its debt).

So, here we sit. This morning, the US Treasury yield curve (10Y-2Y) remains inverted. This AM, the curve inverted another -.591 basis points to -42.725, a sign of impending recession.

Yes, we are living through Jay Powell’s famous chili episode where money velocity is near historic lows and we have an inverted yield curve.

BTW, congratulations to Will Zalatoris (aka, Happy Gilmore’s caddy) for his first PGA Tour victory at the FedEx St. Jude Championship!

Only in today’s Kafkaesque (having a nightmarishly complex, bizarre, or illogical quality) Federal government would Biden, Schumer and Pelosi cheer about passing a bill hilariously called “The Inflation Reduction Act” that not only will NOT reduce inflation, but also raises taxes on most Americans.

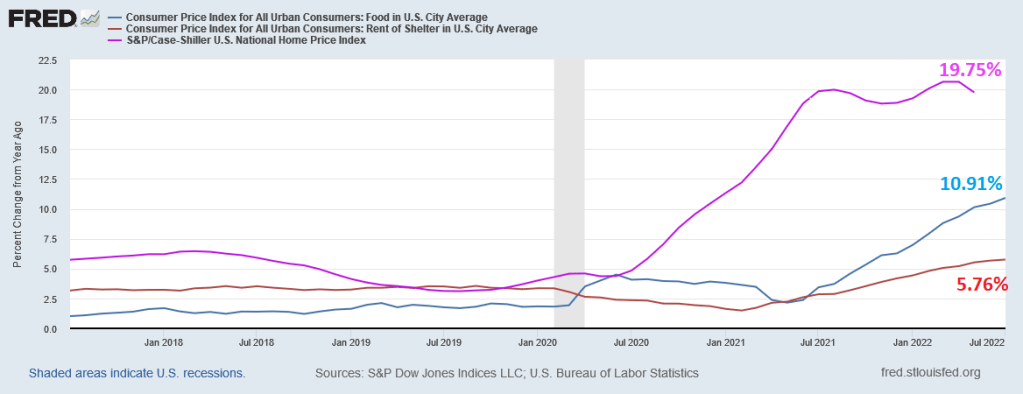

In terms of the inflation tax on the middle class and low-wage workers, we see that FOOD inflation was 10.91% YoY in July and the BLS’s low-ball estimate of “rent” at 5.76% YoY. Odd, since home price growth is 19.75% YoY.

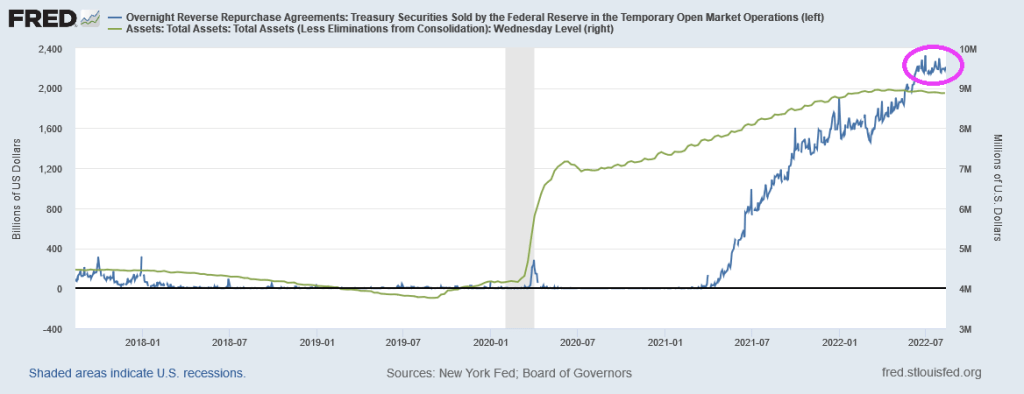

The Fed’s monstrous balance sheet is still near $9 TRILLION (over stimulus) and The Fed’s Overnight Repo Facility remains near $2 TRILLION.

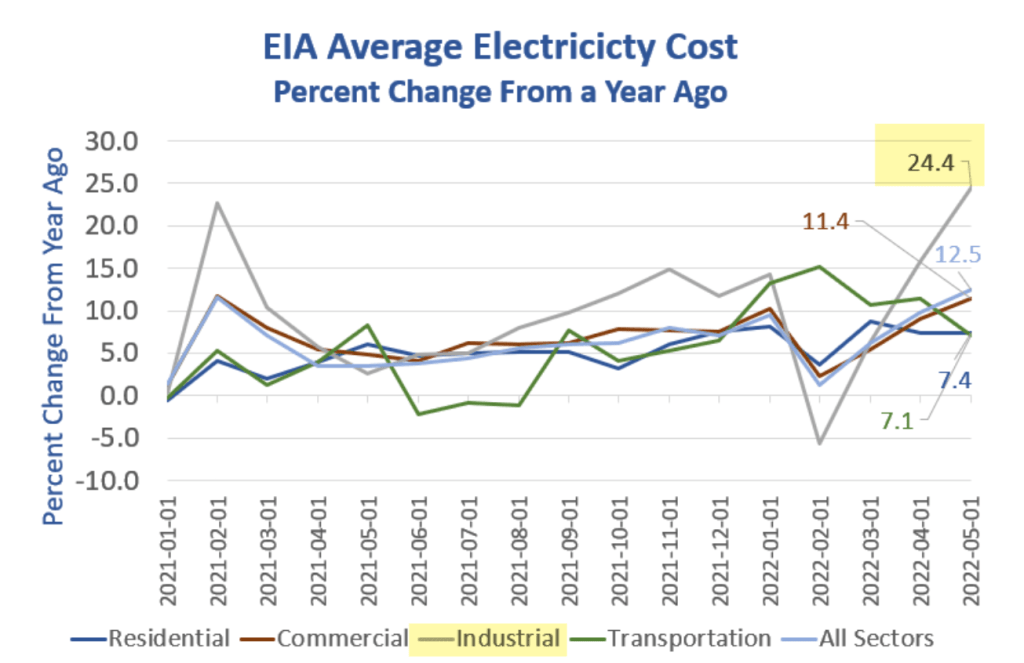

Industrial electricity costs (to be passed on to consumers in the form of higher prices) is up 24.4% YoY. Residential electricity cost is up “only” 7.4% YoY. (Source: Mish GEA)

Politicians like to (falsely) take credit for things, such as Biden bragging about gasoline prices declining. Bear in mind that regular gasoline prices were $2.88 when Biden was inaugurated as President, rose to over $5 a gallon in June and now have declined to $3.98 for which Biden is taking credit. So, regular gasoline prices are still up 34% under Biden. Ouch!

But other rates and prices are dropping too. Bankrate’s 30yr mortgage rate started at , broke the 6% plane on June 21, 2022 only to drop to 5.53% on Friday. CRB’s foodstuffs price index started at 370.58 on Biden’s inauguration as President, rose to 606.71 on May 17, 2022 then retreated to 561.32 on Friday, August 13th. Even headline inflation (CPI YoY) is cooling … slightly.

You can see the recent declines in mortgage rates, gasoline and food prices (pink box) that corresponds to a shrinking of the US M2 Money stock growth. M2 Money is still growing at torrid pace (8.5% YoY) almost back to pre-Covid stimulypto levels of 6.8% YoY. So shrinking M2 Money growth is helping reduce mortgage rates and inflation, food/gasoline prices.

Instead of trying to remove Fed stimulus even more, Biden and Congress passed the “Inflation Reduction Act” which will barely scratch inflation and raises taxes across the board (despite Biden’s promise that no one making under $400,000 will see a cent of increase taxes). And Biden’s preposterous promise ignores the inflation tax which has been severe and still growing at 8.5% YoY. Not 0% as Biden and Harris claimed.

But wait for winter as food, gasoline and heating prices start to soar again.

My favorite dim-witted explanation of inflation belongs to Democrat Representative Pramila Jayapal who recently claimed that “inflation is a theoretical word that economists use.” Like the brilliant Milton Friedman???

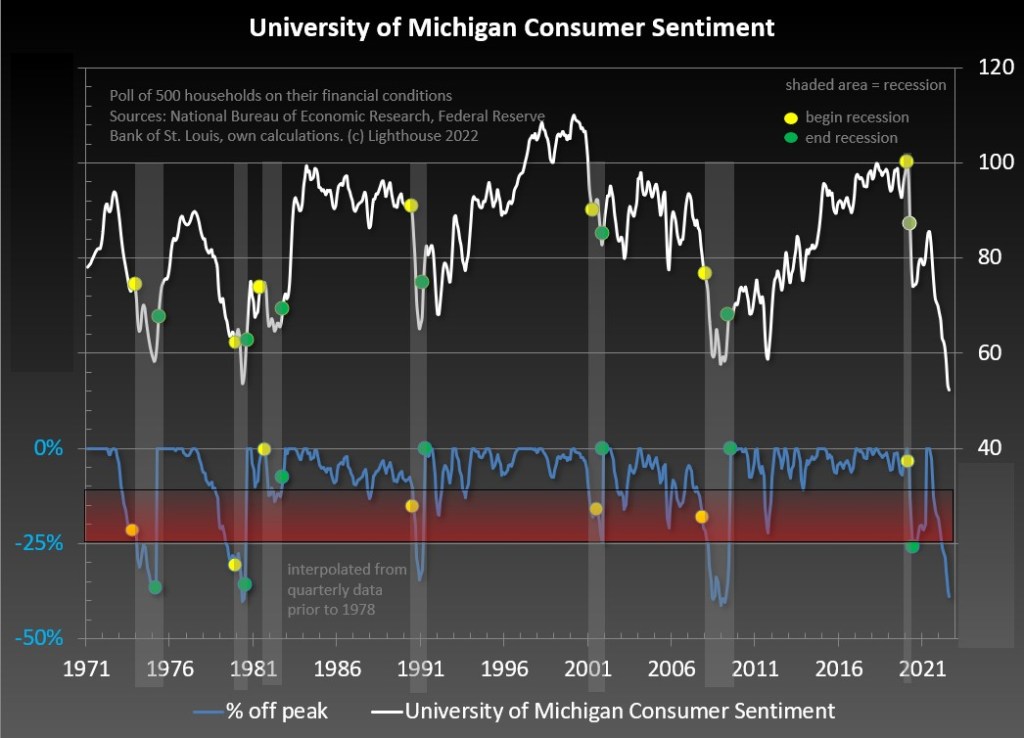

The University of Michigan consumer survey is out for August and the results show improvement … from disastrous to just plain horrible.

The University of Michigan Buying Conditions for Houses remained depressed and didn’t improve.

Bear in mind that today’s consumer sentiment reading in the lowest since 1970, lower than during any recession.

The Conference Board’s leading economic indicator plunged in June despite nearly $8 trillion in Fed stimulus still outstanding.

The good news? President Biden and his son Hunter boarded Air Force One for a carbon-spewing plane trip to South Carolina for a one-week vacation. At least he can do less damage to the US while on vacation.

Agency mortgage-backed securities (MBS) prices started to degrade as The Federal Reserve started to try to combat inflation caused by Biden’s energy policies and rampant Federal spending. That is, under June when the implied Fed O/N rate (red line) cooled and the 30-year mortgage rate (blue line) has come down a little.

In terms of duration risk, the FNCL 3% MBS duration has risen with anticipated Fed tightening.

So, further Fed tightening will result in greater MBS losses AND rising duration risk.

Fannie Mae’s Home Purchase Sentiment index has declined from 81.7 shortly after Biden was sworn-in as President to a meager 62.8 in July 2022.

Of course, mortgage rates have risen quite rapidly and home price growth remains elevated as The Fed still has not trimmed its balance sheet as promised.

While President Biden is technically correct (CPI didn’t increase from June to July), he left out that headline inflation was still painful at 8.5% YoY and core inflation was 5.9% YoY. He also left out that CORE inflation rose 0.3% in July. And he left out that REAL earnings growth was still negative.

The midterm elections are approaching fast and, of course, Biden and his crew have to put the best face of his and the Democrats accomplishments. But seriously Joe, REAL weekly earnings growth is negative meaning that inflation is crushing wage growth. Meanwhile, CPI rent is skyrocketing and was 5.8% YoY in July.

As we know, the CPI measure of rent is terrible and does not reflect the actual rise in rents. Zillow’s Rent index YoY is slowing, but remains at 14.75% YoY, far higher than the CPI rent measure of 5.8%.

So, the Federal Government and Federal Reserve keeps pumping trillions into the economy, so it is not surprising that we have rampant inflation crushing renters.

The US July inflation report remains hot, hot, hot! While mortgage purchase and refinancing applications are not, not, not.

The US consumer price index rose 8.5% in July. And real average weekly growth remains burned by horrid inflation, at -3.6% YoY.

Source of inflation?

Headline inflation above estimates in 14 of last 16 months.

Data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending August 5, 2022 revealed that … the Refinance Index increased 4 percent from the previous week and was 82 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 19 percent lower than the same week one year ago.

You must be logged in to post a comment.