One of the big problems with Federal goverment and Federal Reserve monetary stimulus is … it wears out. Just look at M2 Money growth.

US existing homes sales fell -7.70% in November to 4.09 million units SAAR. And since the same month last year, existing home sales are down -35.4% YoY.

Existing home sales were the lowest in November since 2010.

The good news? The median price of existing homes fell to 3.21% YoY. The bad news? The ark is really bad pointing to a bad December. Inventory for sale (orange line) remains below pre-Covid shutdown levels.

The mortgage market is behaving like today’s bomb cyclone in terms of the weather. Bomb cyclone in that mortgage rates have dropped 7.16% on October 21, 2022 to 6.34% on December 16, 2022 (a drop of 82 basis points), but mortgage purchase and refinancing applications are not increasing like one would hope.

Mortgage applications increased 0.9 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending December 16, 2022.

The Refinance Index increased 6 percent from the previous week and was 85 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 0.1 percent from one week earlier. The unadjusted Purchase Index decreased 3 percent compared with the previous week and was 36 percent lower than the same week one year ago.

But remember, The Federal Reserve is going to be lowering their target rate after they keep raising it.

US housing starts plunged -16.4% since the same time last year (aka, YoY) as The Federal Reserve continues tightening its monetary policy.

Since October (aka, MoM), housing starts only dropped -.049% in November. 1-unit detached starts were down -4.06%. But multifamily (5+) starts were up 4.85% MoM.

Building permits were down -11.24% from October to November (baby, its cold outside!) and down -22.4% since November 2021 (aka, YoY).

The 12-month-ahead probability of recession spiked in November across all of yield curve models. The deterioration in the outlook was most significant in the one that relies on the 3-month/18-month forward spread — Fed Chair Jerome Powell’s favored model — which now sees a 59% chance of recession next year, compared with almost 0% six months ago. Yield curve models see the strongest signal for recession starting around September 2023.

We assess the probability of recession in the months ahead by looking at a suite of models: three yield curve models — which take as their sole input the spreads between 2-year/10-year, 3-month/10-year, and 3-month/18-month forward US Treasury yields, respectively — as well as a model that takes 13 financial and macroeconomic indicators as inputs.

All three yield curves inverted further in November, indicating higher probability of a downturn next year. Notably, the 3-month/18-month forward curve inverted for the first time this year, and the model based on that indicator suggests a 59% chance of recession in 12 months (vs. 32% for the same reference period in the prior update) — that would be in November 2023.

My favorite yield curve is the 10-year – 2-year curve which has been inverted for 112 straight days.

Rising mortgage rates courtesy of The Federal Reserve’s tightening to fight Bidenflation has led to a Covid-level plunge in the NAHB Homebuilder Market Index.

Everything seems to be going down with a sinking M2 Money growth.

And today, the 10-year US Treasury yield is up over 10 bps. Watch out mortgage rates!

Like the Mel Gibson movie “Apocalypto!”, we are seeing the US middle class and low-wage workers being economically sacrificed by The Federal Reserve, the Biden Administration and Congress.

Despite the rhetoric that Fed stimulus (aka “Stimulypto!”) is being removed, the US remains plagued by NEGATIVE real 10-year Treasury yields, NEGATIVE real Fed Funds Target rate and NEGATIVE real average hourly earnings growth under Inflation Joe.

This chart demonstrates the Stimulytpo problem. Prior to Covid, US wage growth was consistently higher than headline inflation. But starting in March 2021, three months after Biden became President, headline inflation became higher than wage growth.

Even with all these negative REAL rates, the US economy is forecast to have almost no growth in 2023.

To quote Peggy Lee, Is That All There Is? Trillions in Federal spending and Fed monetary stimulus and all we get it 0.50% Real GDP??

One of the great ironies of the Sam Bankman-Fried debacle is that while SBF was a generous donor to Democrats (and a few RINOs) and President Biden, it was Biden’s green energy policies that were part of the nail in SBF’s crypto empire. As inflation exploded upon Biden taking office (and massive overspending by Congress), The Federal Reserve jumped in to cool inflation leading to the downfall of cryptos in terms of price.

M2 Money YoY (green line) shows the massive growth money with the Covid economic shutdowns in 2020. Cryptos skyrocketed after that much money was printed by The Fed. Cryptos fell shortly after peaking in April/May 2021, then peaked again in a horrific display of asset volatility in October/November 2021.

What happened in late 2021 to crush cryptos? Ah, expectations of Fed rate increases (red line) started to soar meaning the punchbowl for cryptos was being taken away. The Fed giveth and The Fed taketh away.

The risk management question is … how did SBF and Alameda Research’s Caroline Ellison didn’t notice the relationshop between crypto prices and changing Federal Reserve monetary policy? Even worse, why didn’t investors ask questions??

Take a gander at Bitcoin relative to US diesel fuel prices (orange line) and The Fed’s inflation counterattack (red line). Sam and Sweet Caroline (who was seen walking free in NYC) must not have been monitoring how rapidly rising diesel prices would permeate the entire economy in terms of price increases. M2 Money YoY (green line) has been declining as the expectations of Fed rate tightening (red line) has increased.

SBF donated a huge amount to the midterm elections, the party that went along with Biden’s war on fossil fuels. Then inflation ensued as energy and food prices skyrocketed, leading The Federal Reserve to fight inflation by removing the monetary punchbowl. So, in a sense, SBF donations led to his own collapse.

Apparently, SBF, Caroline Ellison and the other FTXers were engaged in orgies and not paying attention to the impact of inflation and Fed policies on cryptos.

Lastly, how did Gary Genslar and the SEC not see any of this? In the same way that Fed Chair Ben Bernanke didn’t see the financial crisis as it was rapidly unfolding: eyes wide shut.

I read that Nicole Kidman underwent psychiatric treatment after filming “Eyes Wide Shut.” I saw it and was bored out of my mind.

The Federal Reserve forecast for the US economy is a dismal 0.50% YoY. Do I detect a trend?

The FOMC forecast for 2023 and 2024. Core PCE YoY (inflation) is forecast to drop to 3.50%, still considerably higher than The Fed’s target rate of inflation of 2%. And unemployment is forecast to be 4.60%.

To cope with Bidenflation, US personal savings rate as of October is -67.9% YoY. The “good” news is that rents YoY are crashing. But food prices under Inflation Joe remain very high. But most everything is slowing down, not due to Biden’s policies, but a global and US economic slowdown.

With a big slowdown coming our way, you can understand why The Fed’s December Dot Plot is showing declining Fed Funds Target rate starts declining in 2024.

Even US mortgage rates are headed down.

Speaking of going down, cryptos are down across the board with Cardano leading the decline at -6.91%.

Years ago, Brent Ambrose, Michael Lacour-Little and I wrote a paper on the US 30-year jumbo mortgage spread over conforming 30-year mortgage rates entitled “The effect of conforming loan status on mortgage yield spreads: a loan level analysis.” But that paper was written before Covid and the dramatic distortion caused in mortgage markets by The Federal Reserve’s massive increase in money.

Here is the spread between Bankrate’s 30-year mortgage rate and their 30-year JUMBO mortgage. Notice that between 2007 and early 2020, the median “jumbo spread” was 49 basis points. But after Covid and The Fed’s counterattack (by printing M2 Money), the median Jumbo spread from 4/1/2020 to today is only 1 basis point.

In the following chart, you can see the jumbo mortgage rate (yellow) against the conforming mortgage rate (white) and there is almost always a spread between the two UNTIL 2020 where we saw M2 Money growth (green line) spike and The Fed increased their purchases of Agency MBS (purple line). Since Covid and The Fed’s massive reaction, the jumbo rate and conforming rate are virtually the same. In fact, the latest jumbo spread is 1 basis point over the conforming rate.

Why is this happening? One explanation is that demand from the investors who ultimately buy jumbo mortgages. The strong demand by investors appears to have driven down the yields on jumbos relative to conventional loans, especially as the use and accessibility to jumbos has grown.

A second explanation is that Loan Level Price Adjustments that were added to conforming loans post-financial crisis never went away (until just recently on selected loans). This makes jumbos and conforming loans very close in yield.

So, when will the mortgage market return to normal and jumbo mortgages go back to the normal 50 basis point spread? We may see normalization if The Fed speeds up its withdrawal from markets. Also, getting rid of Loan Level Price Adjustments would help normalized the mortgage market.

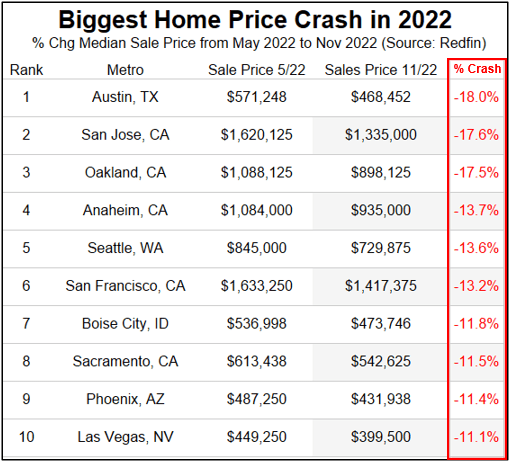

But things are getting stressed in jumboland (California) where home prices are crashing in 5 of the top 8 metro areas.

Harry Houdini couldn’t have created a more tantalizing mystery … and one I wish would go away.

Here is a chart (courtesy of Zero Hedge) showing reported payrolls and REVISED payrolls. Somehow, I don’t think Jean Pierre (Biden’s spokesperson, not the French chef) will be touting “Unlike Trump, our administration barely added any jobs in March, April, May and June 2022.

How will this revelation influence the Fed’s open market committee (FOMC) going forward knowing that the Biden Administrations job creation claims are wildly overstated?

Perhaps it doesn’t matter since Bernanke, Yellen and Powell don’t follow any rules (like the Taylor Rule), but generally with job creation almost nonexistant in March through June of 2022, The Fed should be cutting rates like mad. But wait! Can they with significant inflation?

The good news is that inflation is coming off its peak, but will take a while to get to The Fed’s 2% target. Hence The Fed may raise their target rate since they cannot achieve it will energy price up substantially since Biden became President.

You must be logged in to post a comment.