The Federal Reserve is reversing its excessive monetary stimulus policies left over from the financial crisis of 2008 (and Covid) and the mortgage industry and potential home buyers are paying the price.

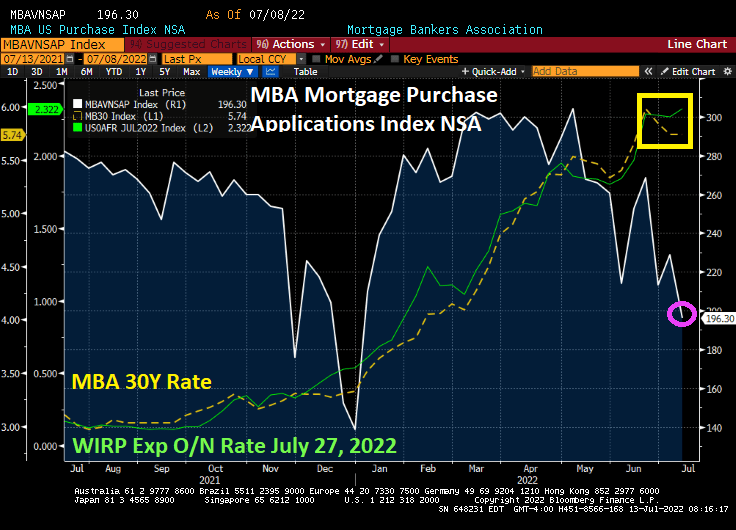

Mortgage applications decreased 1.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending July 8, 2022. This week’s results include an adjustment for the observance of Independence Day.

The seasonally adjusted Purchase Index decreased 4 percent from one week earlier. The unadjusted Purchase Index decreased 14 percent compared with the previous week and was 18 percent lower than the same week one year ago.

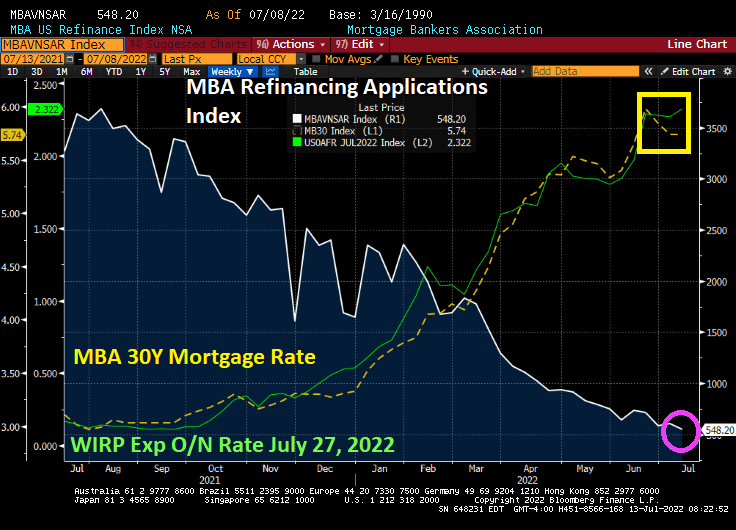

The Refinance Index increased 2 percent from the previous week and was 80 percent lower than the same week one year ago.

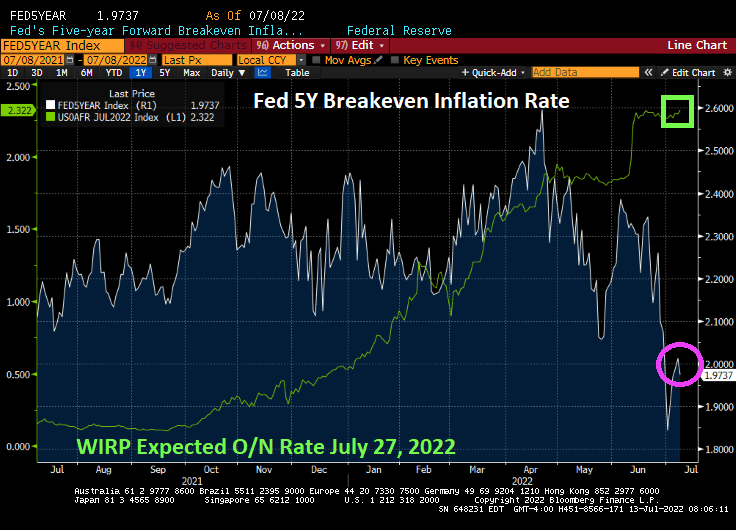

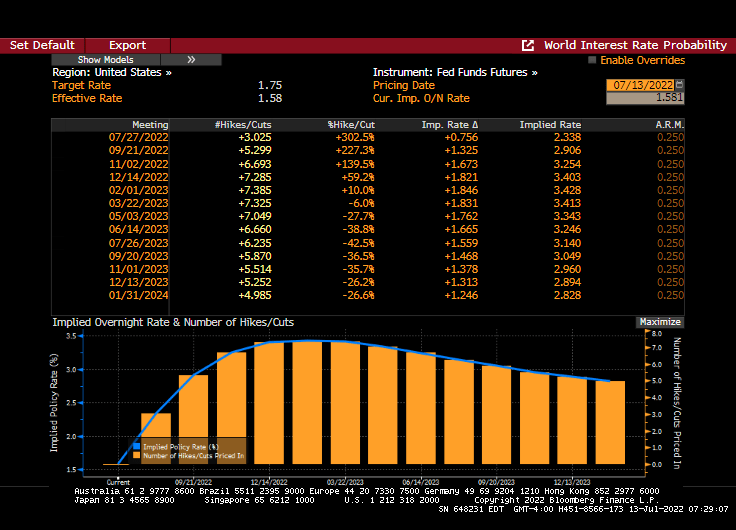

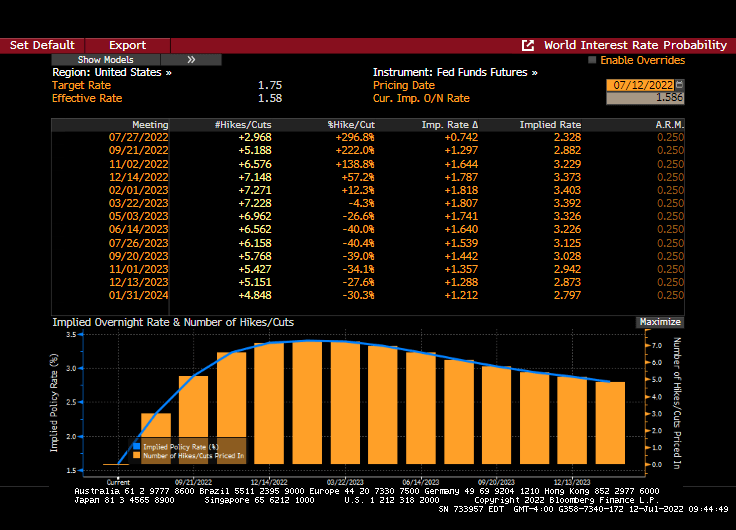

Here we go loop de loop! Traders are pricing in a 75 basis point rate increase at the July FOMC meeting despite collapsing Fed 5-year inflation breakeven rates.

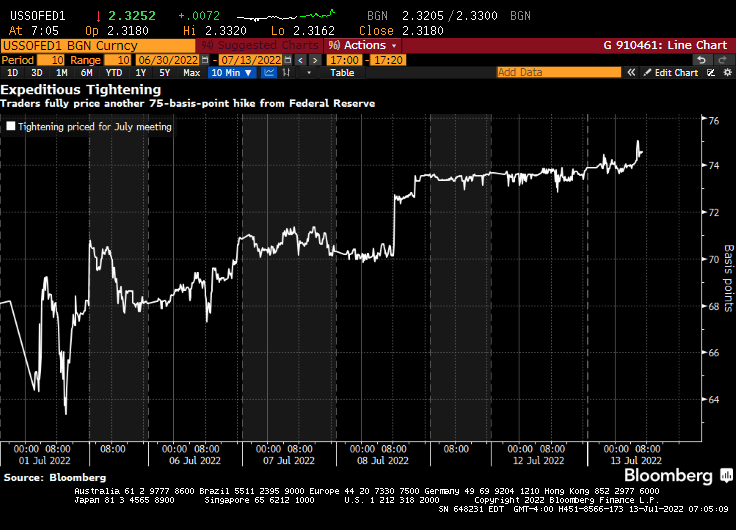

Money markets are betting on a three quarter-percentage point hike by Federal Reserve officials later this month, wagering the US will need to ramp up the pace of monetary tightening to tame inflation.

The repricing comes ahead of a key inflation report due Wednesday. The headline figure for June is set to accelerate to 8.8% year over year, the highest since 1981.

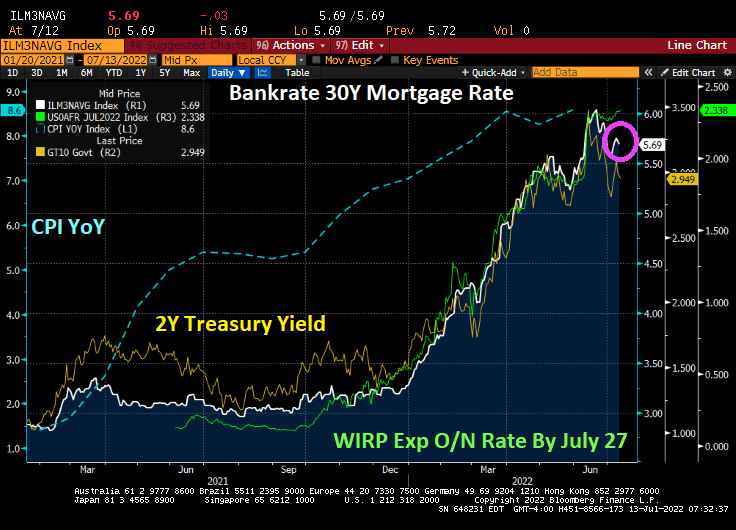

Bankrate’s 30Y mortgage rate fell slightly ahead of today’s inflation report with the expectation of The Fed hiking their target rate by 75 basis points to 2.338% at the July 27th Fed Open Market Committee meeting.

Trader expectations from Fed Funds Futures data:

Last night I watched “The Shallows” on Peacock TV. I thought from the title that it was going to be a biography of The Federal Reserve, but it was a film about a surfer being attacked by a shark.

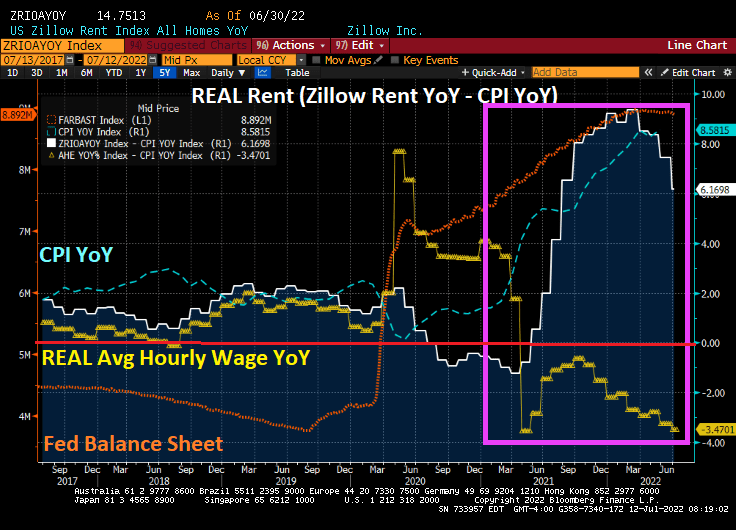

We are all aware that inflation is soaring, since the Covid outbreak in 2020 and the massive overaction by The Federal Reserve and Federal government in terms of stimulus spending and economic lockdowns.

Things were “normal” before Covid in that REAL housing rent (white line) and REAL average hourly earnings YoY (yellow line) moved together. But after Covid shutdowns and Federal stimulus “relief” (orange line), we see that inflation (blue line) took off along with the growth in housing rent. The problem, of course, is that REAL average hourly earnings YoY has been declining. I call this “The Great Divide in housing affordability”.

The question, of course, is whether The Federal Reserve will continue their “war on inflation” with a 75 basis point rate increase.

Inflation is at its fastest pace in 40 years, and is expected to increase even higher in tomorrow’s inflation report.

Gasoline prices have been dropping recently, but remain above $4.50 per gallon (regular gas price was $2.40 per gallon on Biden’s inauguration day. And no, it wasn’t the Biden Administration selling nearly 1 million barrels of crude oil from the strategic petroleum reserve to the Chinese government-owned Sinopec that Biden’s son Hunter is an investor (so, The Big Guy aka Joe Biden gets a 10% piece of the action). It is a slowing global economy that is helping to lower gasoline prices.

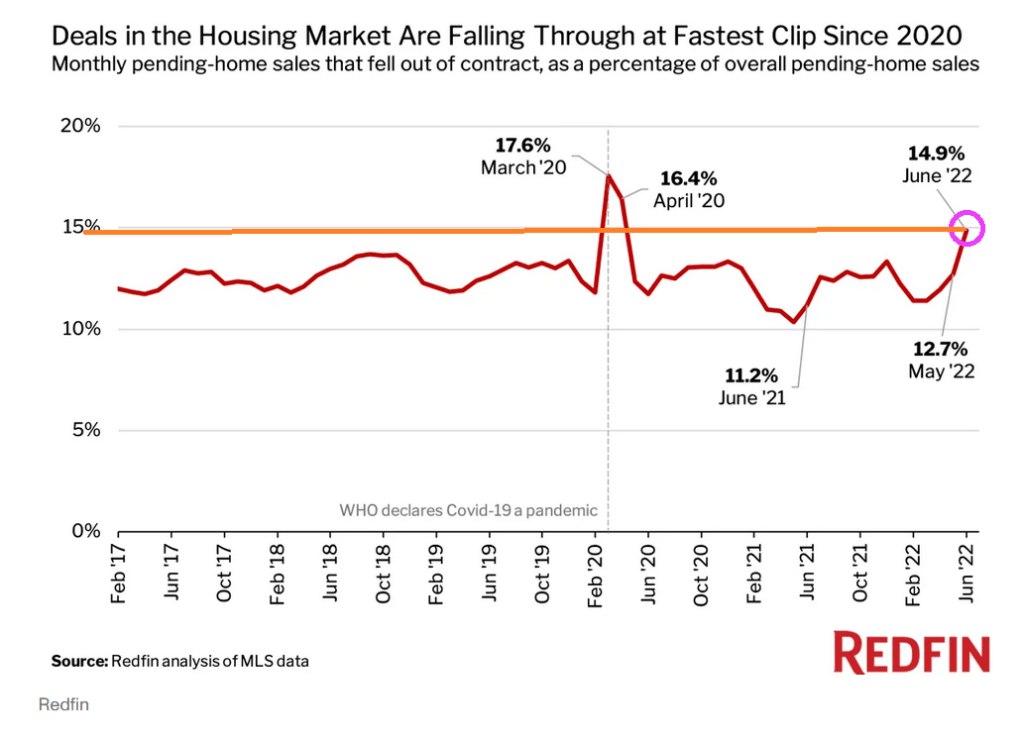

With rising mortgage rates, we are seeing a surge in pending home sales cancellations.

Atlanta Fed’s Raphael Bostic thinks that the US economy is so strong that it can easily handle a 75 basis point increase at the next FOMC meeting. Fortunately, he is not a voting member.

The US economy is slowing as inflation ravages consumers. US Regular Gasoline prices, for example, are up 104% under President Biden which helps to slow the economy.

US personal consumption expenditures fell to +0.2% MoM in May as “inflation” or real personal consumption expenditures PRICES rose +6.3% YoY as The Fed’s balance sheet (aka, Master Blaster!) remains.

As I mentioned above, US regular gasoline prices are UP 103% under President Biden, diesel prices (the cost of shipping goods to markets like … food is up 119% under Biden while CRB foodstuffs is up 55% under China Joe.

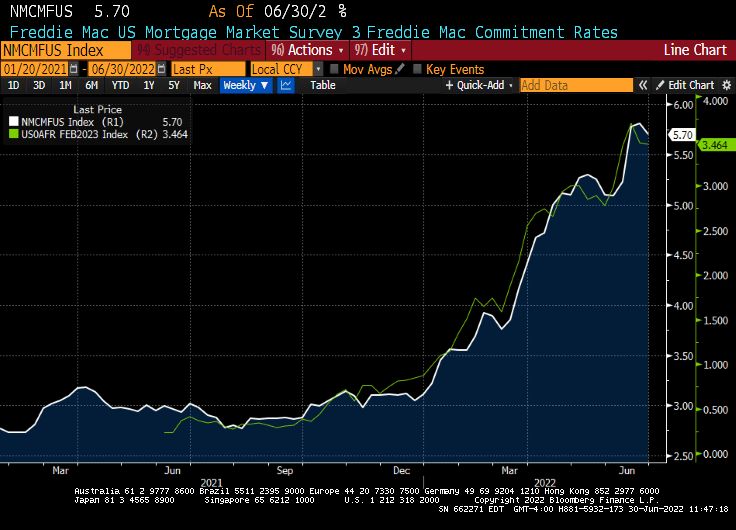

Now we have mortgage rates in the US falling for the first time in four weeks. The average for a 30-year loan was 5.7%, down from 5.81% last week, Freddie Mac said in a statement Thursday.

This year’s Fourth of July celebration is going to cost 18% more than last year’s celebration.

Lastly, the Atlanta Fed GDPNow real time tracker for Q2 is showing … -1% GDP “growth.”

The ECB is planning on a Blitzkrieg Bop, monetary style.

When Lagarde talks about the first line of defense, all I can picture is The Maginot Line in France, a failed defensive line that was easily bypassed by the German Wehrmacht (army).

The European Central Bank will activate the bond-purchasing firepower it’s earmarked as a first line of defense against a possible debt-market crisis on Friday, according to President Christine Lagarde.

Applying “flexibility” to how reinvestments from the ECB’s 1.7 trillion-euro ($1.8 trillion) pandemic bond-buying portfolio are allocated is aimed at curbing unwarranted turmoil in government bonds as interest rates are lifted from record lows to curb unprecedented inflation.

Net buying under a separate asset-purchase program is also set to end on Friday.

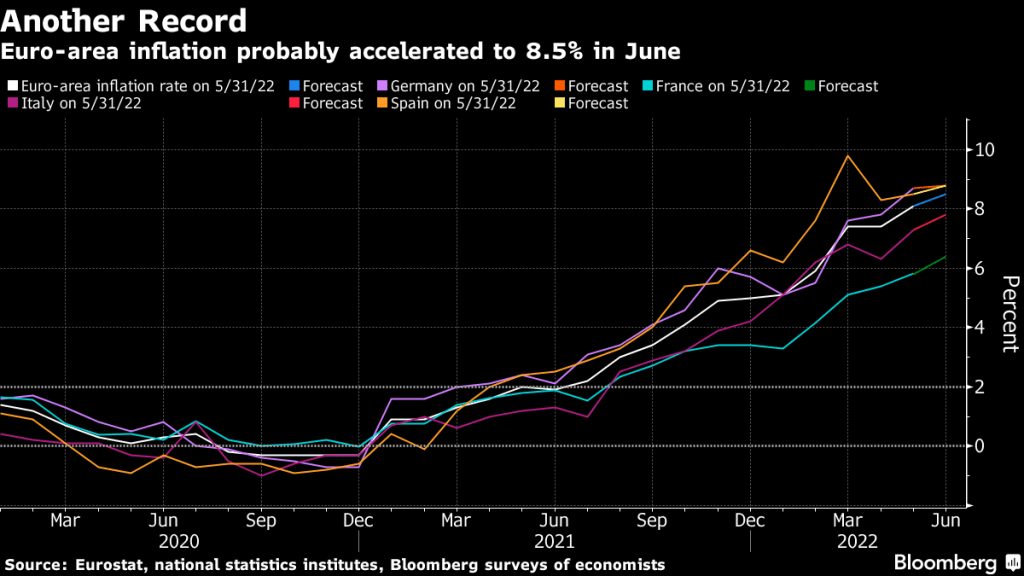

In other words, Euro-area inflation has exploded in 2021, just like the USA.

But the US also has an inflation problem caused in part by Covid and the government’s reaction to Covid: economic shutdown and massive Federal monetary and fiscal stimulus. The stimulus is still in play.

The bond market is already anticipating an about-face by The Federal Reserve (implied overnight rate peaking at the March 2023 FOMC meeting, then receding.

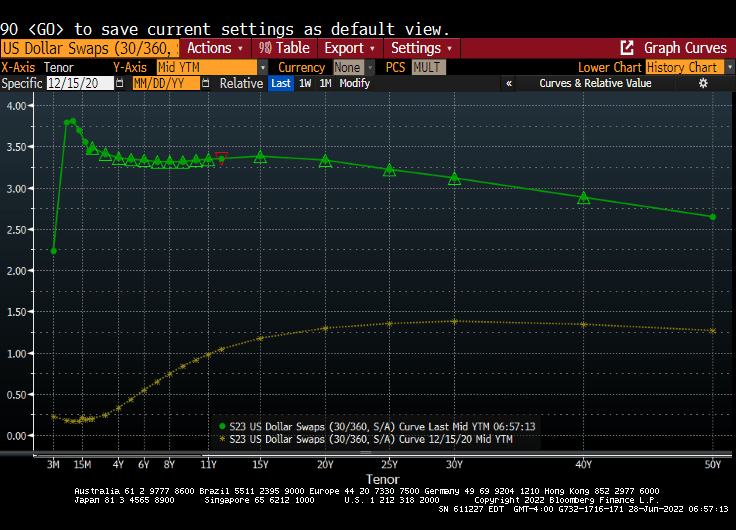

Again, nothing has been the same since the Covid outbreak of 2020 and Fed monetary blitz. Here is the US Dollar Swaps curve before Covid (yellow line) and today’s Fed-enhanced curve (green).

Mortgage rates in the US have climbed to 6% then backed-off slightly. The good ole Back-off Boogaloo as The Fed attempts to unwind its monetary stimulypto.

The French Maginot Line, easily bypassed by German tanks. The Federal Reserve is the US’s Maginot Line. The Yellenot Line??

Sometimes I wonder if The Federal Reserve Board of Governors pays attention to economic news. For example, the Atlanta Fed’s GDPNow forecast for Q2 was released today at -0.002%. So what does The Fed do? They raised their target rate by 75 basis points to 1.75%.

Apparently, The Fed has chosen to fight inflation rather than help the economy.

The CPI news on Friday was so awful that it changed the bond market’s view of Fed trajectory, and the weakest sector broke. In bond jargon, MBS went “no-bid.”No buyers for MBS. Then a few posted prices beyond borrower demand, not wanting to buy except at penalty prices. (Courtesy of Cherry Creek Mortgage)

Despite what Treasury Secretary Janet Yellen has said, Friday’s inflation report demonstrated that inflation is no longer transitory. And with that realization, there was a dearth of bidders for Agency Mortgage-backed Securities (Agency MBS) on Friday.

As a result, agency MBS 2.5% dropped to under $90 as markets expect The Fed to keep raising rates to combat inflation.

Duration of the FNCL 2.5% agency MBS has been extending with growing inflation. Duration was under 1 on August 2, 2021 but is now 7 times greater at almost 7.

Note to Yellen: inflation seems be permanent, not transitory. Or at least inflation will remain high for the foreseeable future, crushing the life out of Agency MBS.

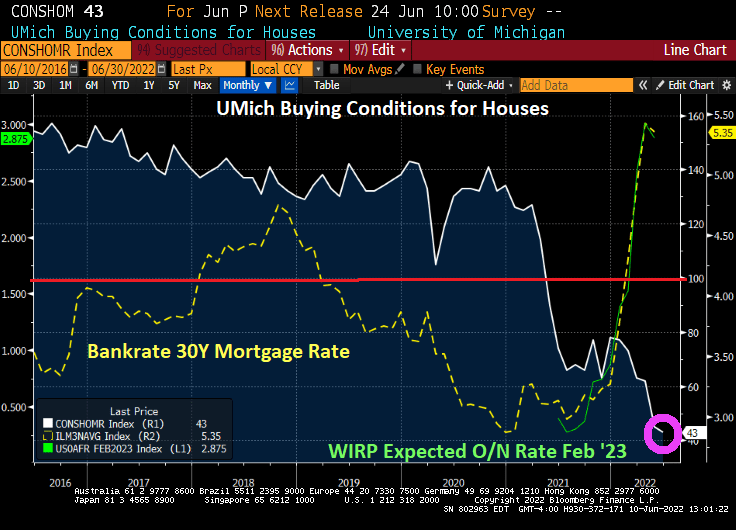

The Fed is expected to raise their target rate to 2.875% by February 2023. With that expectation, mortgage rates (yellow line) are soaring. And with that, University of Michigan’s Buying Conditions for housing has plunged to 43, the lowest levels since 1982 as the US was trying to recover from high inflation.

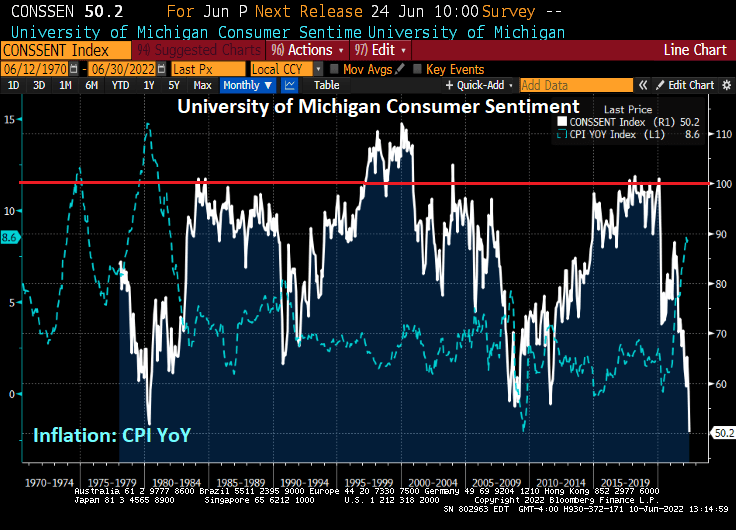

The University of Michigan consumer sentiment index just plunged to the LOWEST LEVEL in history on inflation and Fed’s reaction.

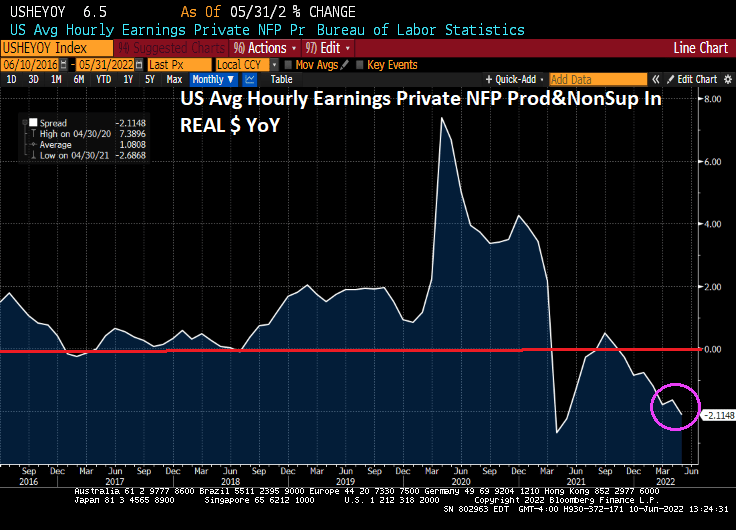

Average REAL wage growth has now declined to -2.11% YoY.

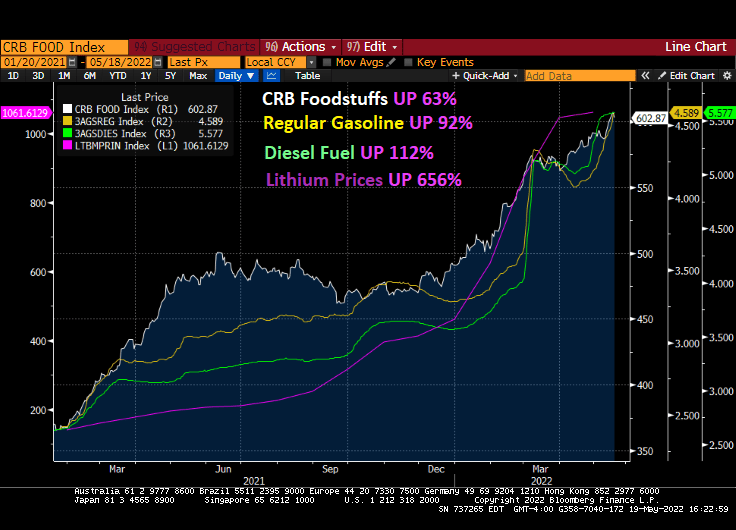

The inflation that is crushing Americans is due to energy and food price increases. That is, the non-core inflation. Under Biden, food is up 63%, gasoline is up 92% and diesel prices are up 112%. But The Fed doesn’t consider food and energy prices, per se.

If we look at the Taylor Rule considering fighting inflation including food and energy, The Fed would have to raise their target rate to … 21.38%.

Now, The Fed can clearly cool-off the housing market by raising rates. In fact, my fear is that they go too far and crash the housing market. The Fed will NEVER get to 20% again like we last saw under Volcker in 1981. 20% rates certainly cooled home prices back then and Fed rate hikes helped crash the housing market in 2008.

So, when The Fed says they want to be the inflation-fightin’ Fed, we must be aware what The Fed can and cannot do. They can’t tame the inflation beast in the form of food and energy prices (unless they crash the economy), but they can crush home prices.

Well, the Fed’s talking heads have been saying a 50 basis point hike was coming in May … and it appeared!

And it looks like 9 rate hikes are a comin’ by February 2023.

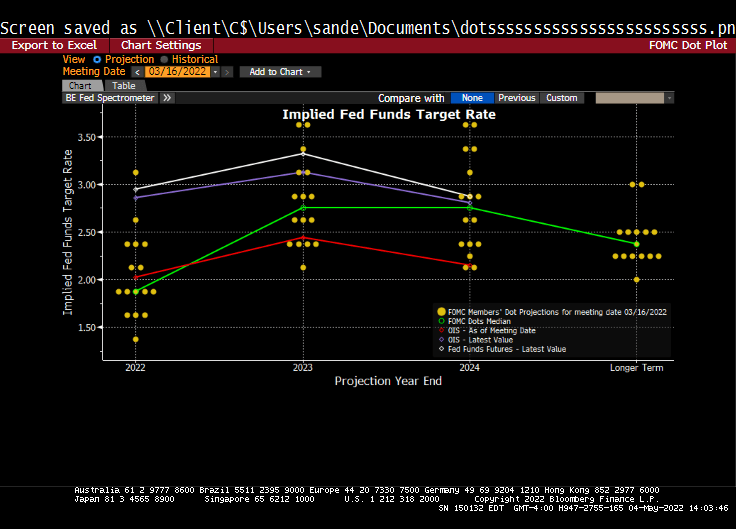

The Fed’s Dot Plots shows a cooling of Fed rate hikes by 2024 and beyond.

Here is the path of Balance Sheet peel-off.

The US Treasury actives curve is up by 14 bps at the 10-year tenor and up 17 bps at the 2-year tenor.

The plan will see $30 billion of Treasuries and $17.5 billion on mortgage-backed securities roll off. After three months, the cap for Treasuries will increase to $60 billion and $35 billion for mortgages.

I could read the Fed’s speech on their decision, but since The Fed has been so highly politicized, I don’t really care what they say. Only what they do.

You must be logged in to post a comment.