US Treasury Secretary Janet Yellen changed the drop dead date on a US default from June 1 to June 5, daring Speaker McCarthy to step over the line. The debt ceiting is so urgent that Biden went on vacation to Delware for Memorial Day weekend. In fact, Biden and Yellen expect McCarthy to dance.

White House and Republican negotiators tentatively narrowed differences but were still clashing Friday on key issues as the Treasury Department signaled extra time was available before a potential US default.

Treasury Secretary Janet Yellen announced the department expects to be able to make payments on US debts up until June 5 if lawmakers fail to act on the US debt ceiling. That set a more pointed date for a potential default but is also four days later than her previous comments eyeing trouble as soon as June 1.

The new so-called X-date buys negotiators for House Speaker Kevin McCarthy and President Joe Biden more time to strike a deal. The negotiating teams haven’t met in person since Wednesday but spoke late into the night Thursday and were in regular communication throughout the day Friday.

Yes, there isn’t really a crisis folks. Treasury collects tax dollars continuously so Treasury can prioritze debt payments and other disbursements. The only crisis is in the minds of the media.

Deputy Treasury Secretary Wally Adeyemo warned Friday that payments to Social Security beneficiaries, veterans and others would be delayed if there’s a default. But he said he’s gaining some confidence an agreement will be reached.

We’re making progress and our goal is to make sure that we get a deal because default is unacceptable,” Adeyemo said in an interview on CNN. “The president has committed to making sure that we have good-faith negotiations with the Republicans to reach a deal because the alternative is catastrophic for all Americans.”

The accord would also include a measure to upgrade the nation’s electric grid to accommodate sham renewable energy, a key climate goal, while speeding permits for pipelines and other fossil fuel projects that the GOP favors, people familiar with the deal said.

The deal would cut $10 billion from an $80 billion budget increase for the Internal Revenue Service that Biden won as part of his Inflation Reduction Act (big whoop). Republicans have warned of a wave of agents and audits while Democrats said the increase would pay for itself through less tax cheating.

What is taking shape would be far more limited than the opening offer from Republicans, who called for raising the debt ceiling through next March in exchange for 10 years of spending caps. House conservatives were already balking Thursday at the notion of a small deal, with the House Freedom Caucus sending a letter to McCarthy demanding he hold firm.

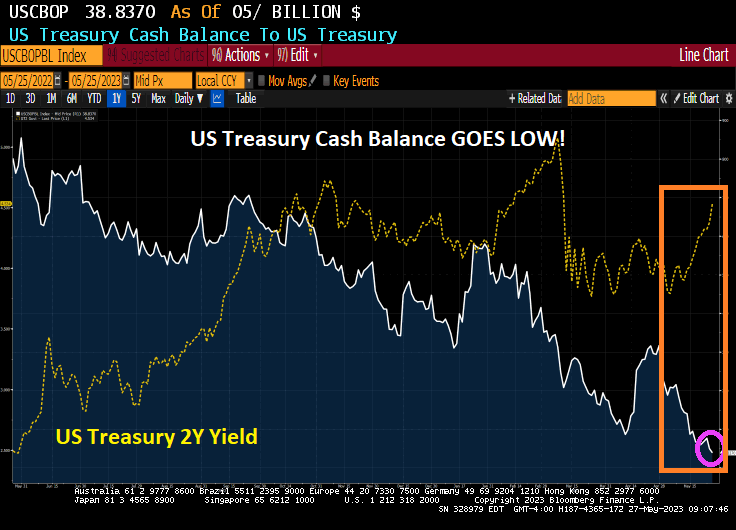

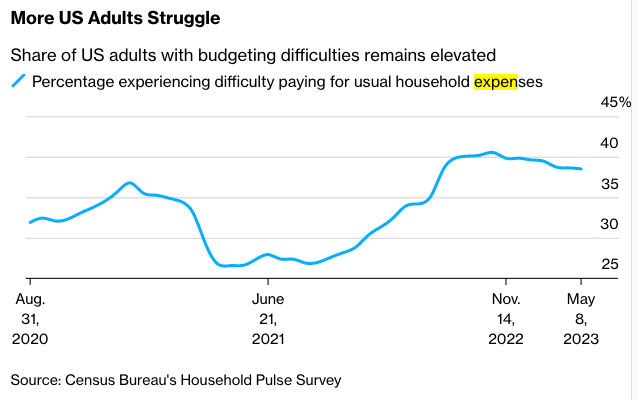

Treasury’s cash balance is at a low point and The Administration threatens Social Security recipients and veterans of delayed payments … while Biden goes on vacation for Memorial Day weekend to honor veterans??

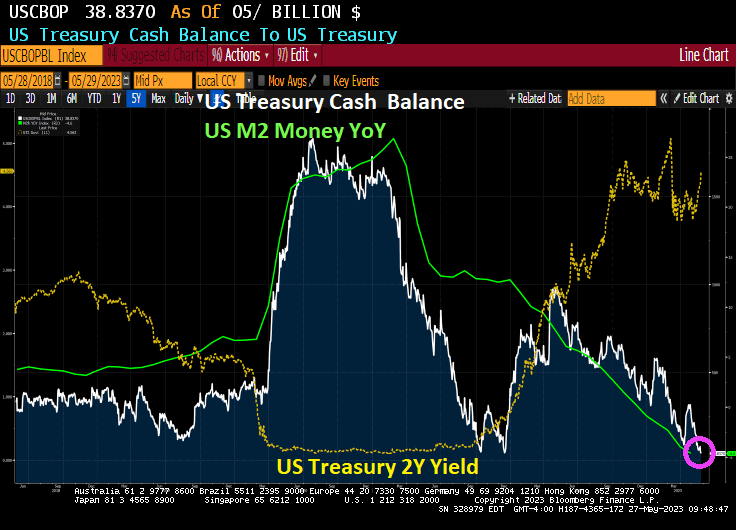

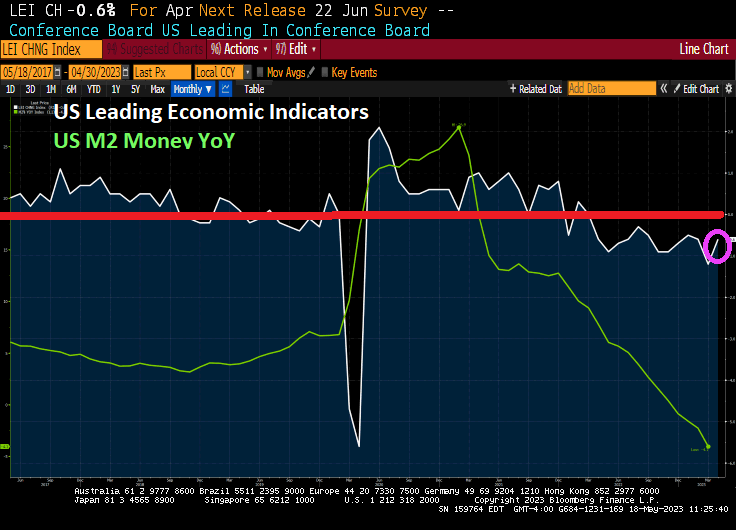

Of course, Yellen know that all The Fed has to do to increase M2 Money growth again.

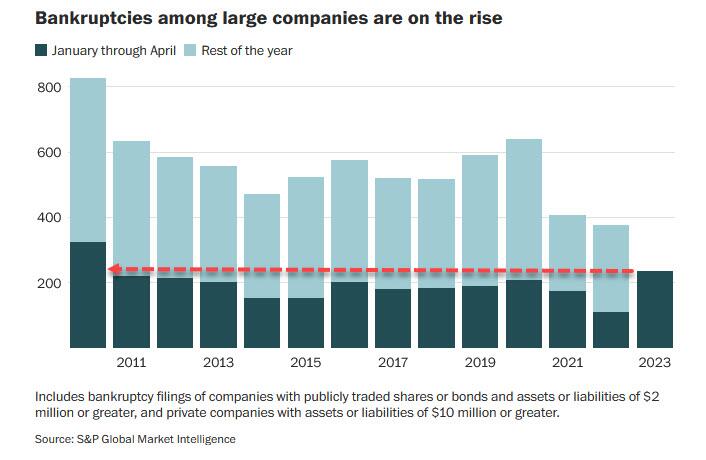

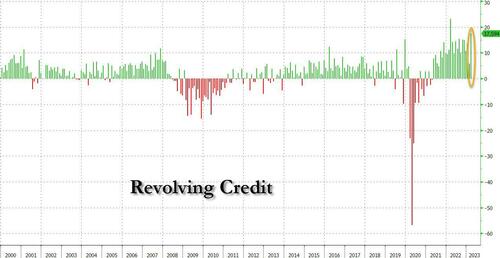

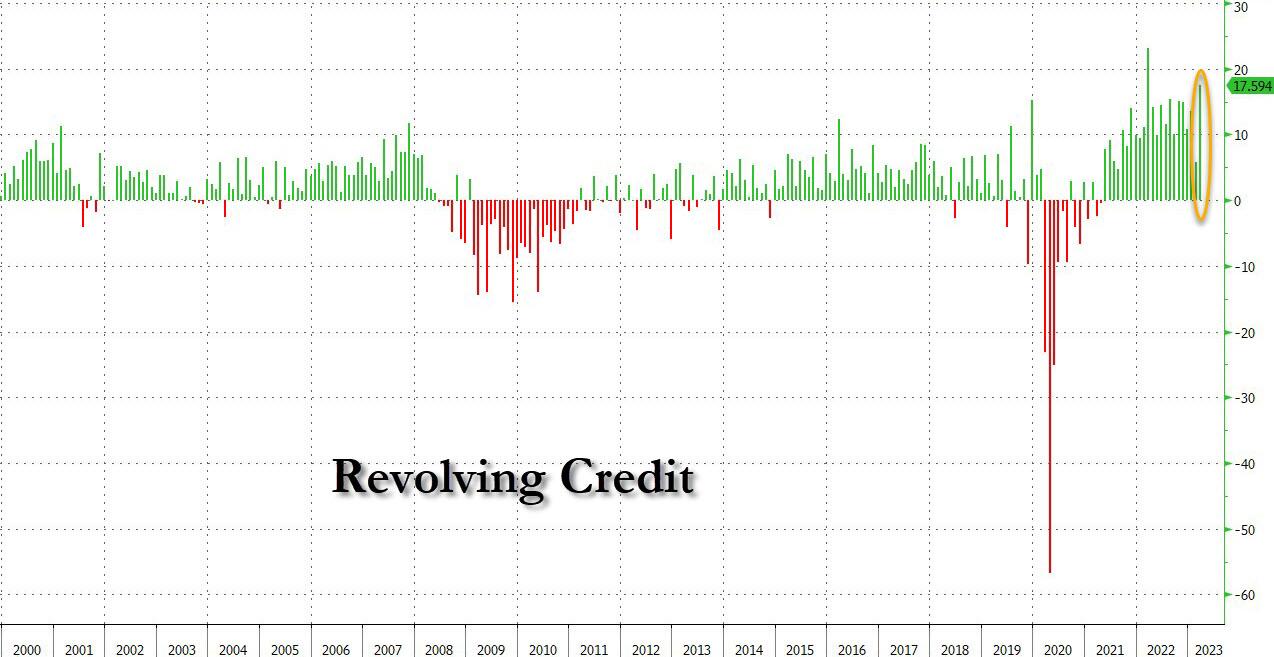

Meanwhile, bankrupties among large companies are highest since 2010.

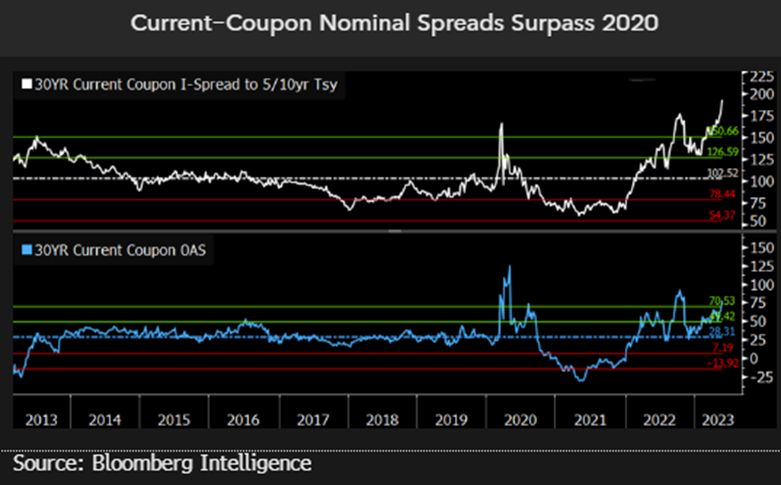

In the mortgage market, current coupon nominal spreads 9Agency MBS 30Y coupon over Treasuries) are soaring.

Meanwhile, to honor US veterans, Biden goes on Memorial Day weekend and threaten veterans with delays in veteran benefits. Sigh.

Is Joe Biden REALLY Reverend Kane from Poltergeist II??

{kind=link}

{kind=link}

You must be logged in to post a comment.