The Philly Fed non-manufacturing sentiment index just tanked to -12.8 as The Federal Reserve removes its Covid-related stimulus.

The banking fiasco (SVB, Signature, etc.) has caused The Fed’s balance sheet to expand … again.

And Fed Funds Futures are pricing in a meager 20 basis points increase at tomorrow’s FOMC meeting (some betting on no change, some betting on 25 basis points). Then another rate hike at the May FOMC meeting, then all downhill from there.

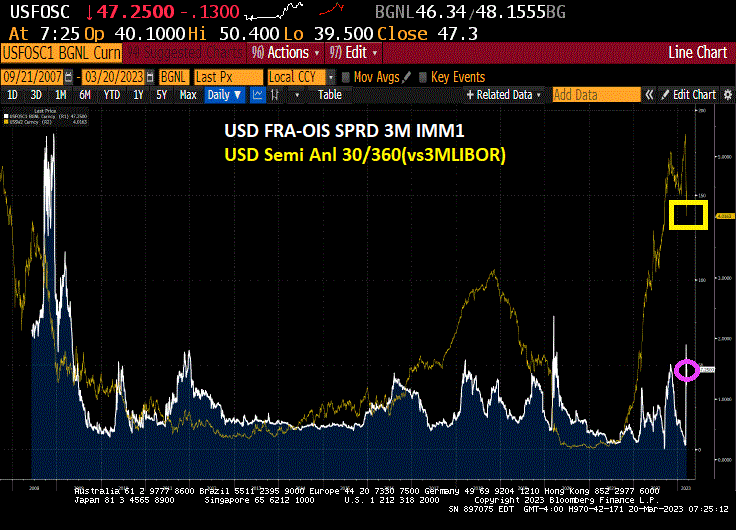

Its the start of a new week after the closure of several US banks (SVP, Signature) and the failure of Credit Suisse. But swaps spreads have calmed down a bit and are no where near the credit crisis highs of late 2008. Or the plain vanilla swap between fixed and variable contracts (white line) has simmered down a bit. BUT was never as high as it was during the financial crisis. Panic by The Fed and FDIC much?

And the 2-year Treasury yield dropped -10 basis points … again.

The Bank of Canada, the Bank of England, the Bank of Japan, the European Central Bank, the Federal Reserve, and the Swiss National Bank are today announcing a coordinated action to enhance the provision of liquidity via the standing U.S. dollar liquidity swap line arrangements.

To improve the swap lines’ effectiveness in providing U.S. dollar funding, the central banks currently offering U.S. dollar operations have agreed to increase the frequency of 7-day maturity operations from weekly to daily. These daily operations will commence on Monday, March 20, 2023, and will continue at least through the end of April.

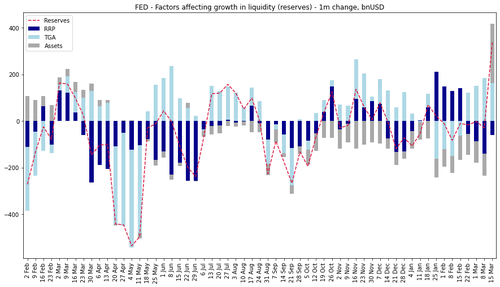

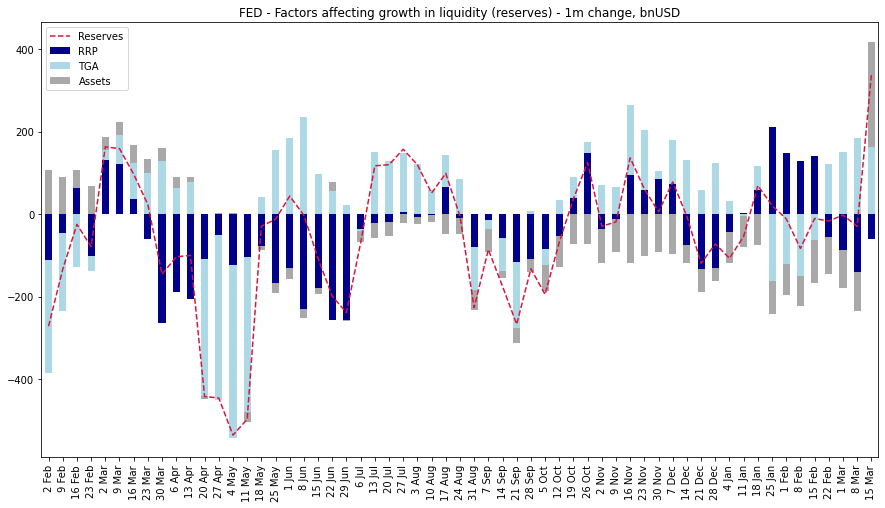

And once the USD swap lines are reopened, the rest of the cavalry follows: rate cuts, QE (the real stuff, not that Discount Window nonsense), etc, etc. In fact, we have already seen a near record surge in reserve injections:

The Fed may as well formalize it now and at least preserve some confidence in the banking sector, even if it means destroying all confidence left in the “inflation fighting” Fed, with all those whose were in charge handing in their resignation for their catastrophic handling of this bank crisis.

So, the Biden Administration made a horrible error by guaranteeing deposits at Silicon Valley Bank for deposits over $250,000. Essentially, Biden bailed out big tech that kept their deposits at SVB.

But what triggered the run on SVB and other banks? Simple. Biden and Congress spent like drunken sailors with Covid and The Federal Reserve went nuts printing money. Viola! We got inflation. But with inflation came The Fed’s attempt to get inflation back to its 2% target (difficult since Biden/Congress refuse to return spending to pre-Covid levels). But as interest rates rise, duration (weighted average life of MBS) rose dramatically meaning that risk increased. But banks like SVP ignored the risk, or didn’t hedge, or were spending time worrying about non-bank related issues.

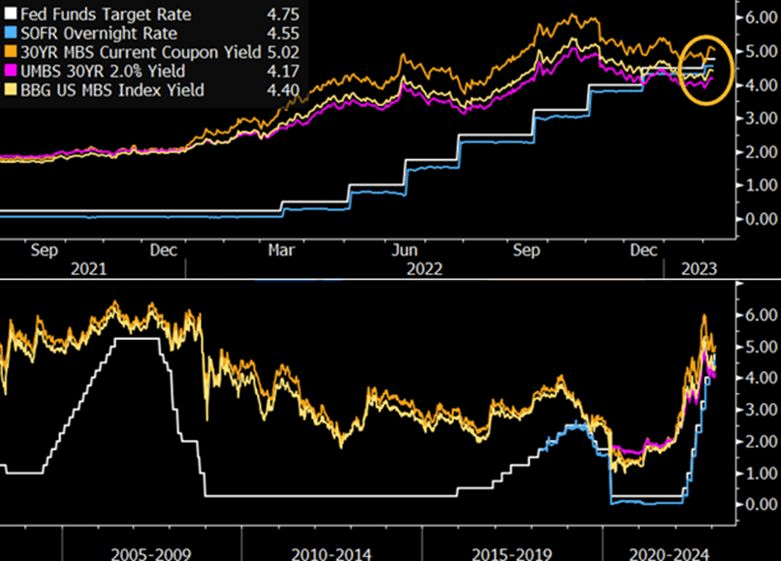

So, what happened? Banks are holding Treasuries and MBS (orange line) that are getting clobbered with rate hikes (yellow line).

Talk about volatility. Today, the 2-year Treasury yield is up over 20 basis points as bond volatility hits levels last seen in 2008, just prior to the subprime credit crisis.

So, Biden’s bailout of SVP depositors stopped the deposit run for the moment. But if The Fed keeps hiking rates, banks are going to be hurting worse and worse. They could rebalance their portfolios and/or hedge. But with Uncle Spam (Biden) at the helm, bailouts are always on the table.

Argetina’s inflation rate just hit 102.5% as their M2 Money printing hit 80%

Argentina’s central bank is considering raising its benchmark rate on Thursday for the first time since September after inflation data showed prices increased by more than 100% annually last month, according to two people with direct knowledge.

The monetary authority’s board will consider an increase after leaving the key Leliq rate unchanged at 75% for several months, the people said, asking not to be named discussing internal decisions. The board has not yet decided on the size of the hike in case they opt for such move, they said.

A cautionary tale for Washington DC spendacrats and Fed officials.

Brought to the same country that gave us Statist Juan Peron and his wife Eva.

All together now. The Fed has been printing too much money for too long and Biden restricts fossil fuel production. Ad in rampant Federal spending and we have INFLATION. Inflation led to The Fed to raise rates. And with rate increases and down go the banks.

Of course, The Fed and Biden Administration will overeact (e.g. offering deposit insurance on ALL deposits above $250,000 creating moral hazard risk). As such, we are seeing gold prices soar by 2% this AM.

In adddition to gold rising 2%, natural gas futures are up 6%

The Silicon Valley Bank failure (along with NY’s Signature Bank) are sending shock waves through the global economy. Not because of the incompetence of bank regulators, but because of the reaction function from the FDIC and Fed.

The 10-year Treasury yield is down -26 basis points in the AM. And the Fed Funds Target Rate is expected to drop to 4.7%.

Its not just the US Treasury yield that declined -26 basis points. European sovereign yields are down too (Germany 10-year is down -32.9 basis points).

Look at the 2-year Treasury yield. Its down -54.6 basis points.

On a sad note, Resident Biden is calling for stricter regulations for the banking industry, already one of the most regulated sectors of the economy. How about less politics and just make them do their ^*T^R jobs!

What a mess in Washington DC. While House Republicans are at lagerheads with Senate Democrats and Resident Biden over Federal spending cuts, the price of insuring against a debt default just rose to 76.75.

How bad it that? Put it this way. Millions are fleeing Mexico and Guatemala and coming to the US. But Mexico has a lower cost of insuring against a debt default than the USA. And Guatemala is almost as expensive as the USA.

It will all be over soon, according to CDS prices.

The Federal Reserve is retreating from its Covid-era monetary expansion. And with the retreat, US durable goods NEW ORDERS fell -4.5%% in January. The worst reading since … Covid in 2020.

A breakdown of new orders shows that while NONDEFENSE capital goods orders dropped -5.4% YoY in January, DEFENSE capital goods orders increased by 25.4% YoY.

Mortgage rates increased across all loan types last week, with the 30-year fixed rate jumping 23 basis points to 6.62 percent – the highest rate since November 2022. The jump led to the purchase applications index decreasing 18 percent to its lowest level since 1995.

Mortgage applications decreased 13.3 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending February 17, 2023.

The Market Composite Index, a measure of mortgage loan application volume, decreased 13.3 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 4 percent compared with the previous week. The Refinance Index decreased 2 percent from the previous week and was 72 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 18 percent from one week earlier. The unadjusted Purchase Index decreased 4 percent compared with the previous week and was 41 percent lower than the same week one year ago.

Did Biden appoint “Pothole Pete” Buttigieg to oversee the mortgage market??

The most recent tightening by the Federal Reserve has pushed the federal funds target rate above mortgage-backed securities yields for the first time in history. Though this poses clear challenges of carry for MBS holders, selective investments in specified pool and collateralized mortgage obligations (CMOs) could provide incremental returns.

Inflation started under Biden, but the massive expansion in money supply (M2) begin with Covid in 2020.

Once this latest spending splurge kicks in, we will see rising inflation again. After all, Biden and Congress have gotten the taste for massive spending bills (like vampires) and spending likely won’t slow down.

{kind=link}

You must be logged in to post a comment.