Federal Reserve Bank of St. Louis President James Bullard said he favors a strategy of “front-loading” big interest-rate hikes, and repeated he wants to end the year at 3.75% to 4% to counter the hottest inflation in four decades.

“We still have some ways to go here to get to restrictive monetary policy,” Bullard said in a CNBC interview Tuesday.

“I’ve argued now with the hotter inflation numbers in the spring, we should get to 3.75% to 4% this year. Exactly whether you want to do that at a particular meeting or some other meeting is a great question. I’ve liked front-loading. I think it enhances our inflation-fighting credentials.”

Federal Reserve presidents including Bullard speaking this week emphasized that inflation at a 40-year high has yet to slow, and pushed back against the perception the central bank was pivoting to a less aggressive phase of tightening monetary policy. Fed Chair Jerome Powell last week cited Federal Open Market Committee forecasts that the Fed would raise rates to 3.4% at the end of the year and 3.8% in 2023.

Bullard wants to raise rates to boost Fed credibility?? When flexible price inflation is at 20.13% and The Fed is awfully slow to shrink their balance sheet??? What credibility is he talking about????

The US economy may need to undergo a deeper and longer recession than investors currently anticipate before inflation can be brought under control, according to Zoltan Pozsar of Credit Suisse Group AG.

Markets expect the surge in consumer prices will soon peak and central banks will become less hawkish, but there’s a high risk that global cost pressures will remain elevated, Pozsar, global head of short-term interest-rate strategy at Credit Suisse in New York, wrote in a client note.

The world is being wracked by an economic war that’s undermining the deflationary relationships that have prevailed in recent decades where Russia and China supplied cheap goods and services to more developed nations such as the US and those in Europe, he said.

“War is inflationary,” Pozsar wrote. “Think of the economic war as a fight between the consumer-driven West, where the level of demand has been maximized, and the production-driven East, where the level of supply has been maximized to serve the needs of the West.” That pattern held “until East-West relations soured, and supply snapped back,” he said.

The result is that inflation is now a structural problem, rather than a cyclical one. Supply disruptions have arisen from the changes in Russia and China, along with tighter labor markets due to immigration restrictions and a reduction in mobility caused by the coronavirus pandemic, Pozsar said.

There’s now a risk the Federal Reserve under Chair Jerome Powell has to raise interest rates to 5% or 6% and keep them there to create a substantial and sustained reduction of aggregate demand to match the tighter supply profile, he said.

‘More Misguided’

Connect the dots on the biggest economic issues.Connect the dots on the biggest economic issues.Connect the dots on the biggest economic issues.

Dive into the risks driving markets, spending and saving with The Everything Risk by Ed Harrison.Dive into the risks driving markets, spending and saving with The Everything Risk by Ed Harrison.Dive into the risks driving markets, spending and saving with The Everything Risk by Ed Harrison.

Sign up to this newsletter

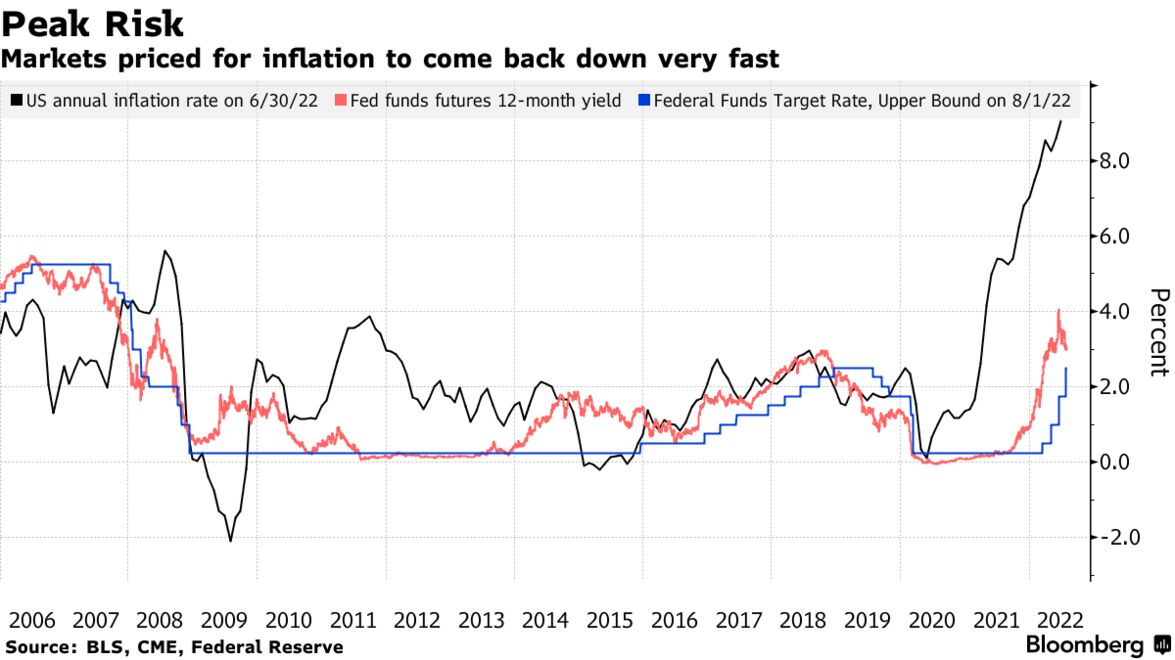

Pozsar’s warning that inflation will stay elevated puts him at odds with the Treasury market, which rallied last month as investors switched their focus to recession risks from inflation concern. While an economic slowdown typically weighs on consumer prices, the latest annual US inflation reading of 9.1% for June remains far above the Fed’s 2% goal, although the price surge is forecast to slow for the first time in three months to 8.8% in July according to a Bloomberg poll of economists.

The bond market is more misguided now than at any other time this year as traders wager the US central bank will start cutting rates in early 2023, Bloomberg Economics’ chief US economist Anna Wong and her colleagues said this week. Money markets are wagering on almost one percentage point of hikes by year-end followed by a quarter-point cut by June.

“Interest rates may be kept high for a while to ensure that rate cuts won’t cause an economic rebound (an ‘L’ and not a ‘V’), which might trigger a renewed bout of inflation,” Pozsar wrote in his note. “The risks are such that Powell will try his very best to curb inflation, even at the cost of a ‘depression’ and not getting reappointed.”

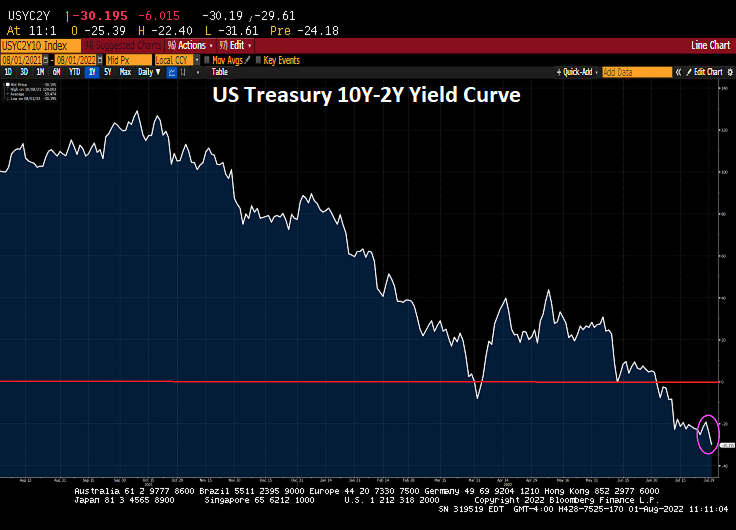

Speaking of “recession,” the US Treasury 10Y-2Y yield curve has inverted even further to -31.69 BPS.

We are seeing a slowing of the US economy. For example, the JOLTs (job openings) numbers are out for June and they are down -5.5% from May. And from April to May, JOLTs declined -3.2% MoM. That is a clear slowing trend.

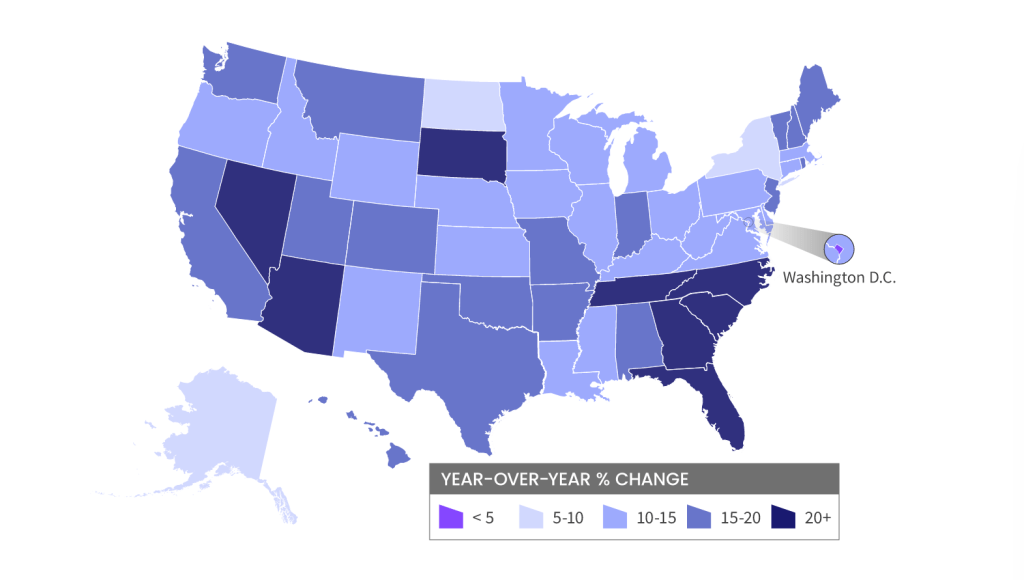

And on the housing front, the CoreLogic HPI Forecast indicates that home prices will increase on a month-over-month basis by 0.6% from June 2022 to July 2022 and on a year-over-year basis by 4.3% from June 2022 to June 2023. But rose +18.3% YoY in June. Also a clear cooling trend.

And its “Escape From Blue States” (perhaps a new Kurt Russell movie), with home prices rising fastest in red states (primarily The South). And contiguous migration from California to Nevada and Arizona.

The Fed Funds Futures market is pricing in rate hikes until the March 2023 FOMC meetings. After all, Prince Imhotep (aka, Minneapolis Fed’s Neel Kashkari) is screaming for more rate hikes to fight inflation … caused by 1) loose monetary policies since late 2008 and 2) insane Federal government spending.

Let’s see if “Mr. Freeze” (aka, Jerome Powell) relents on Fed rate increases before the March 2023 FOMC meeting.

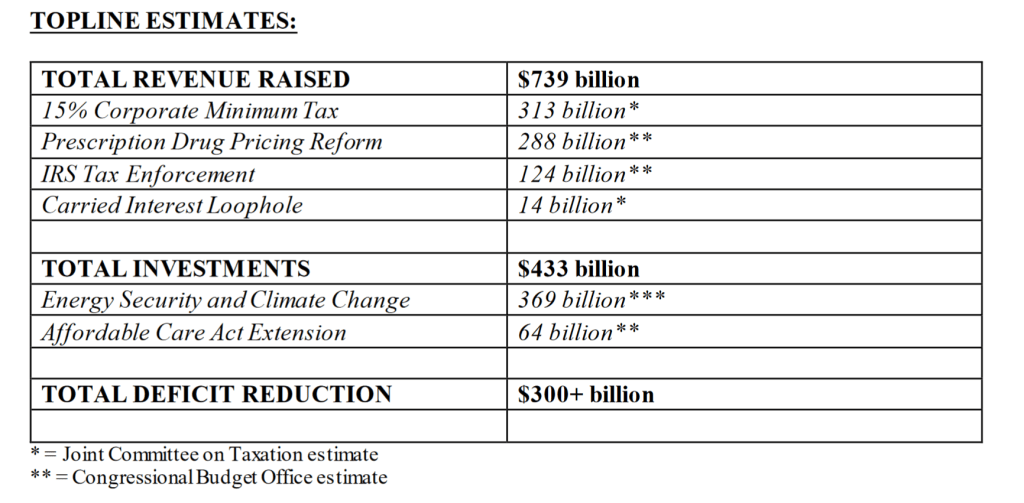

The spendiholics in Washington DC (aka, Biden and Congress) have passed yet another inflationary legislation, this time the sadly misnamed “The Inflation Reduction Act” since it will likely lead to a furthering recession of the US economy. Well, that is one way to reduce inflation: cause a recession and job loss.

An analysis by the National Association of Manufacturers says the tax in 2023 alone will reduce real GDP by $68.5 billion and cut labor income by $17.1 billion. One well-known economic truth is that corporations don’t really pay taxes (they pass on taxes to consumers in the form of higher prices). They are essentially tax collectors, as the corporate tax rate ultimately falls on some combination of workers, shareholders and customers. Raise the corporate tax rate, and you’re cutting wages and salaries for workers.

“Americans are already experiencing the consequences of Democrats’ reckless economic policies. The mislabeled ‘Inflation Reduction Act’ will do nothing to bring the economy out of stagnation and recession, but it will raise billions of dollars in taxes on Americans making less than $400,000,” said Sen. Mike Crapo, an Idaho Republican who sits on the Senate Finance Committee as a ranking member, and who requested the analysis.

“The more this bill is analyzed by impartial experts, the more we can see Democrats are trying to sell the American people a bill of goods,” Crapo added.

According to Schumer and Manchin, “The Inflation Reduction Act of 2022 will make a historic down payment on deficit reduction to fight inflation, invest in domestic (green) energy production and manufacturing, and reduce carbon emissions by roughly 40 percent by 2030. The bill will also finally allow Medicare to negotiate for prescription drug prices and extend the expanded Affordable Care Act program for three years, through 2025.”

No wonder House Speaker Nancy Pelosi took her extensive entourage on a paid vacation to Singapore, Malaysia and perhaps Taiwan. Its called “Getting out of Dodge.” If Pelosi believed in this legislation, she could have “saved the environment” by simply doing a Zoom call. Then again, Biden’s Climate Envoy, John Kerry, still travels the globe trying to sell green energy and carbon reductions in his private carbon-spewing jet. But I forget, Biden, Pelosi, Schumer and Kerry are our elites who deserve platinum treatment, not lowly serfs like 99% of the US population.

So, here we go loop-de-loop. Politicians want to spend money on their friends and donors and then raise taxes on the rest of us.

On the recession front, the 10Y-2Y US Treasury yield curve just flattened another -6.015 basis points to an inverted -30.195 basis points.

After breaking the 6% barrier back in June 2022, Bankrate’s 30-year mortgage rate has backed-off to 5.28% despite Federal Reserve rate hikes.

The reason for the decline in the US Treasury 10-year is, amongst other things, a global economic slowdown (partly due to the US and Europe “going green” and cutting the supply of fossil fuel-based energy). Instead of “The Great Reset,” I call it “The Great Economic Suicide.” The 10-year US Treasury yield and Bankrate’s 30-year mortgage rate are declining with declining global GDP.

US inflation, based on June’s Personal Consumption Expenditures (PCE) deflator, rose to its highest level since 1982. The PCE Deflator YoY rose to 6.8% while the core PCE deflator (less food and energy, the two things more households care about) rose to 4.8% YoY in June.

In order to fight inflation, The Federal Reserve is going to have to raise their target rate to … 17.78% based on 6.80% PCE deflator YoY. We are currently at 2.50%.

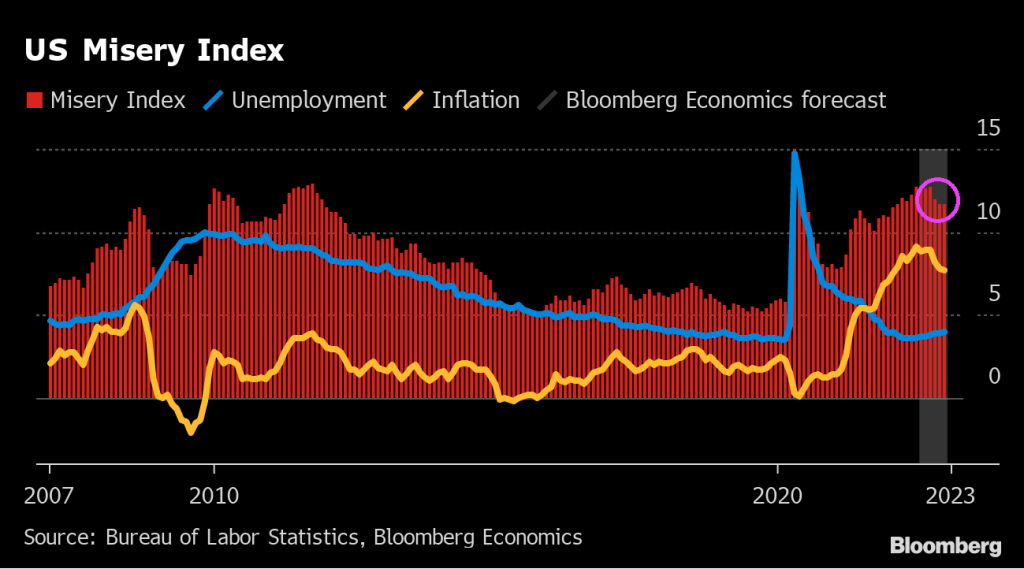

The US Misery Index remains elevated.

Based on the PCE Deflator YoY and U-3 unemployment, the misery index remains elevated compared to before Covid and The Fed’s/Federal government hyper-stimulypto to counter the Covid economic shutdowns. We never fully recovered.

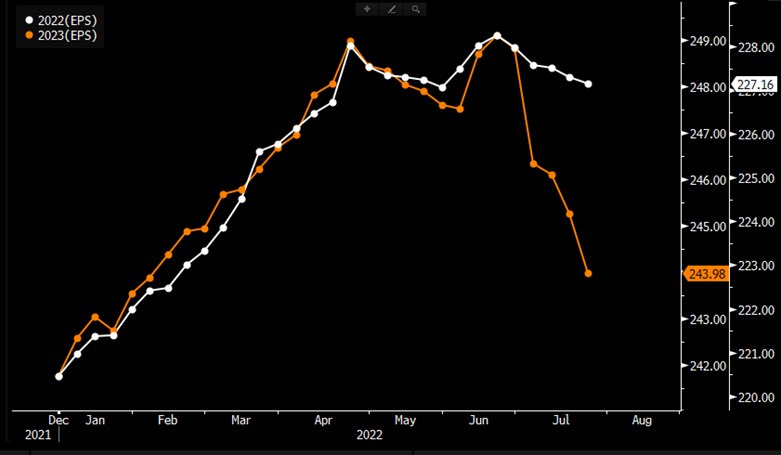

S&P 500 2023 EPS expectations falling off a cliff (orange line).

My former colleague at Deutsche Bank, Joe Carson, said recently that the US economy is not in a recession, but corporate profits are in a recession. While I cling to the traditional definition of recession (two consecutive quarters of negative real GDP growth), there is another component of the US economy that is in recession: consumer sentiment.

The University of Michigan Consumer Sentiment Index rose slightly in the latest release, but remains depressed at 51.5. University of Michigan Buying Conditions for House also rose to 47.0, also a depressed reading.

While unemployment remains low, the price of gasoline is crushing the wallets of American households helping to cause a recession in consumer sentiment.

Biden feebly attempts to explain why 2 consecutive quarters of negative real GDP growth (better known as contraction) is NOT a recession.

You must be logged in to post a comment.