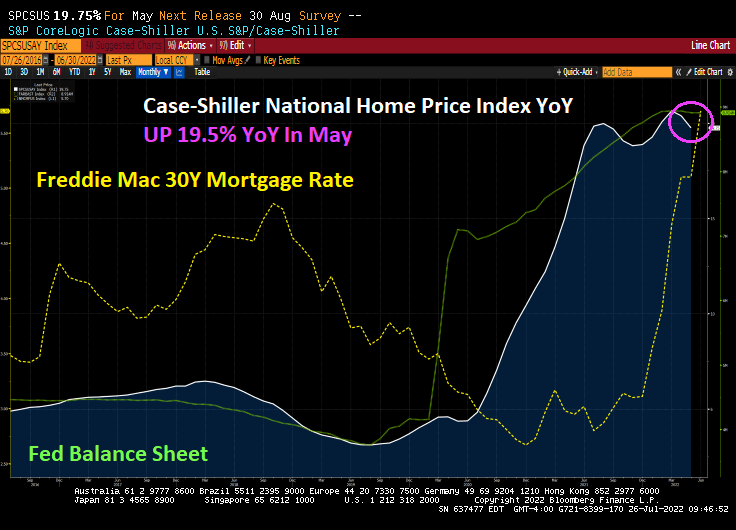

The May Case-Shiller home price indices are out and they’re a doozy. The national home price index rose 19.75% YoY. Why? You can thank The Fed’s “slowhand” approach to withdrawing the Covid-related stimulypto.

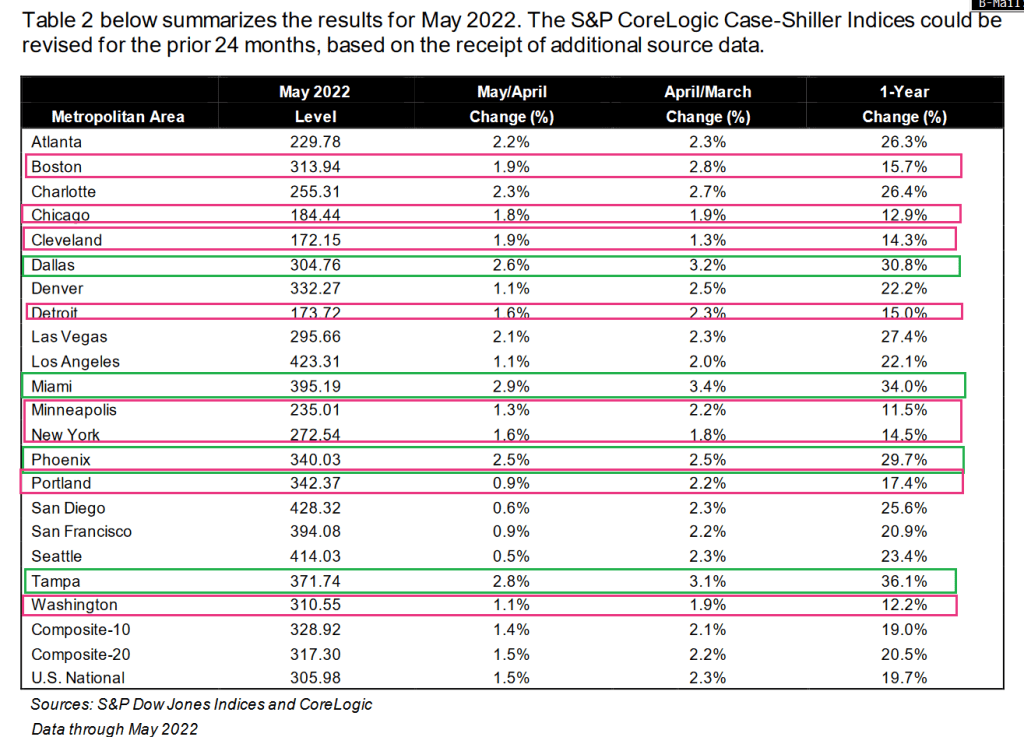

Where are home prices booming? Everywhere.

Miami, Tampa, Dallas and Phoenix (red states) are growing at over 30% YoY. Boston, Chicago, Cleveland, Detroit, Minneapolis, New York, Portland and Washington DC (blue states) are all growing at over 10% YoY. Cleveland is a blue city in a mostly red state while San Diego is a red city in an almost blue state.

Jerome “Slowhand” Powell is not shrinking The Fed’s balance sheet.

Hold on, The Fed is coming! To raise their target rate by 75 basis points at Wednesday’s FOMC meeting. Will this stem the tide of rising inflation?

Under Biden, we have seen regular gasoline prices rise 82% despite recent declines. Diesel fuel is up 121% and foodstuffs are up 46%. And house rents keep rising at a staggering 14.75% YoY. The recent declines is more due to the global economic slowdown and central bank rate increases than anything Washington DC is doing.

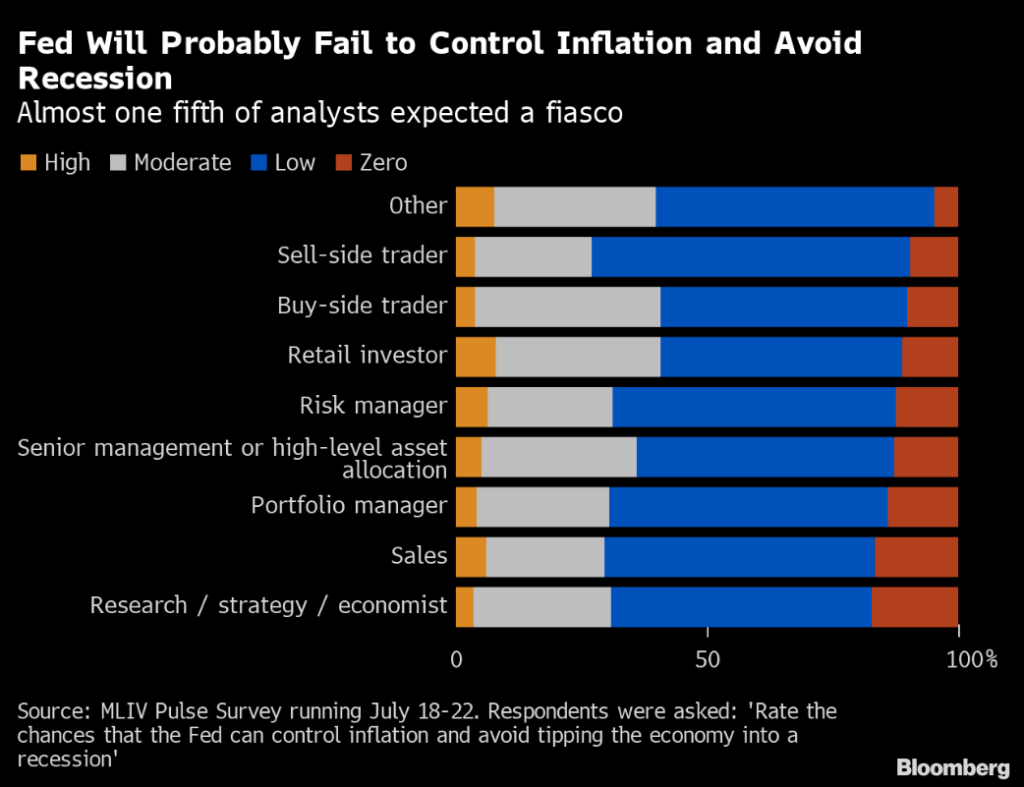

(Bloomberg) Investors are skeptical that the Federal Reserve can tame the worst inflation in four decades without driving the economy into a recession.

That’s bad news for Americans, who face the prospect of a downturn as their bills for food, rent and fuel swell. But to bond investors hit by deep losses this year, it may mean any further pain will be short-lived, as a recession will spark the US central bank to cut rates next year. That’s according to the results of the latest MLIV Pulse survey.

Over 60% of 1,343 respondents in the survey said there’s a low or zero probability that the US central bank can rein in consumer-price pressures without causing an economic contraction. The survey was conducted July 18-22 and included retail and professional investors.

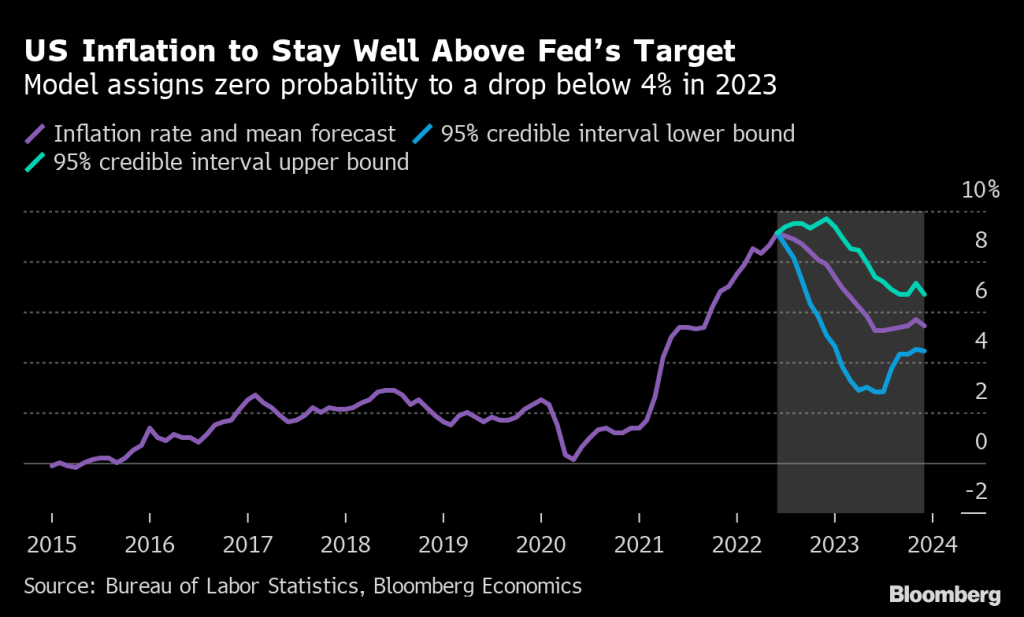

US inflation may be close to a peak, but it’s very likely to stay above 8% through year-end. Bloomberg Economics’ model assigns zero probability to a drop below 4% in 2023. Taken together with increasing recession risks, the Fed faces a tough balancing act as it attempts to bring stubborn price pressures under control without tipping the economy into contraction.

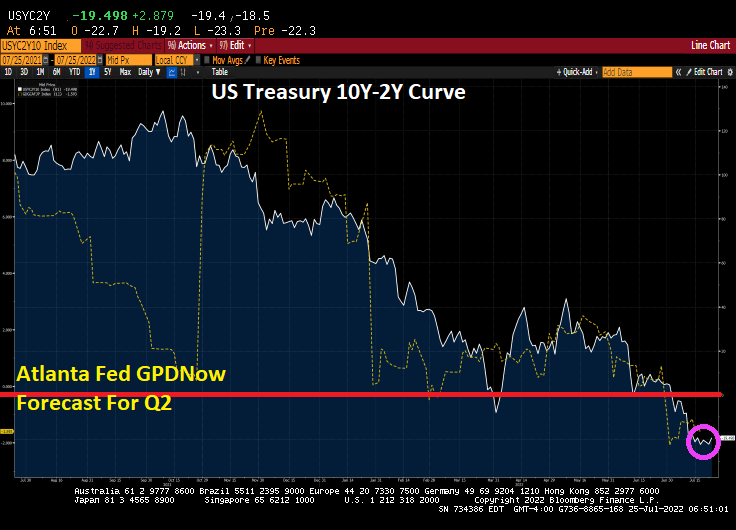

Of course, The Federal Reserve doesn’t really consider energy or food inflation, which are typically higher than core inflation. But going into Wednesday’s meeting, we see the US Treasury 10Y-2Y curve remains inverted (a signal of impending recession) and the Atlanta Fed GDPNow Q2 tracker at -1.6% after a negative Q1 reading.

Will raising the target rate (or ACTUALLY shrinking their balance sheet) reduce inflation? We shall see, but it has got to be better than Lawrence Summer’s suggestion to reduce inflation: raise taxes. Wait a minute, Larry. Inflation was caused by 1) overstimulus by The Fed combined with 2) massive Covid spending by Biden, Pelosi, Schumer and 3) Biden’s anti-fossil fuel policies. So instead of suggesting a decrease in Federal spending, Summer’s wants to give MORE of your money to Biden and Congress to spend. What an unbelievable nitwit.

Here is a picture of Larry Summers, Jay Powell and Janet Yellen attending the FOMC meeting in Washington DC.

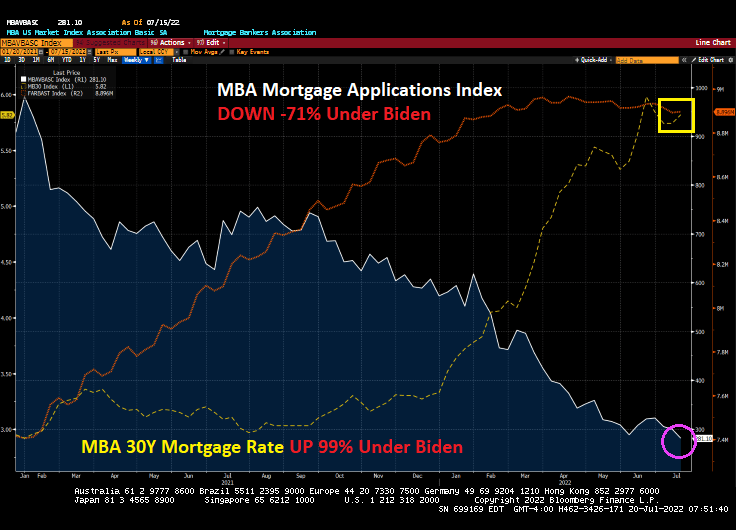

Mortgage applications declined for the third week in a row, reaching the lowest level since 2000.

Mortgage applications decreased 6.3 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending July 15, 2022.

The Refinance Index decreased 4 percent from the previous week and was 80 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 7 percent from one week earlier. The unadjusted Purchase Index increased 16 percent compared with the previous week and was 19 percent lower than the same week one year ago.

Heartache #1: Mortgage rates have risen 99% under Biden.

Heartache #2: Mortgage application have fallen -71% under Biden.

As The Federal Reserve continues to fight inflation caused by 1) excessive stimulus by The Federal Reserve and Federal government surrounding Covid and 2) Biden’s energy policies, we are seeing the mortgage market as collateral damage.

The US is short on supply of housing for a myriad of reasons (high costs, Not-in-my-backyard (NIMBY) local zoning laws, etc), but The Fed’s cranking up interest rates isn’t helping.

US housing starts, a measure of supply, declined -6.3% YoY in June as The Fed cranked up rates.

1-unit (aka, single family detached) starts dropped -8.05% MoM in June while 5+ unit (aka, multifamily) starts rose 15% MoM.

1-unit permits dropped -8% MoM in June while 5+ unit starts were up 13% MoM.

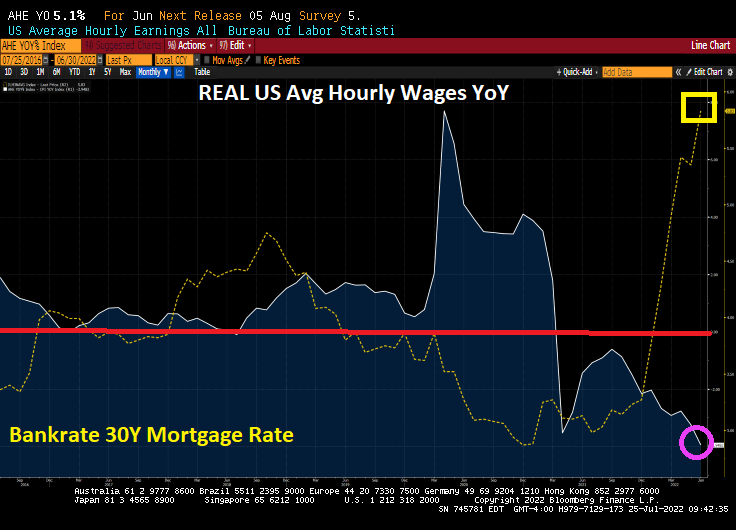

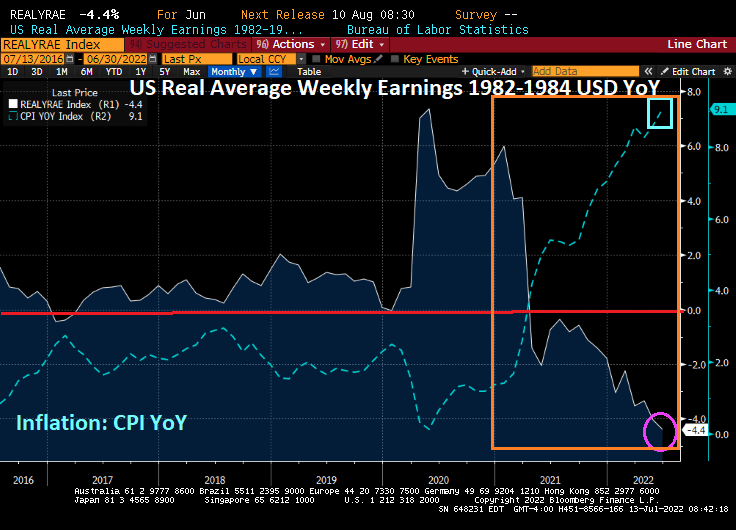

The reason? REAL weekly earnings growth declined -4.4% YoY in June thanks to Bidenflation.

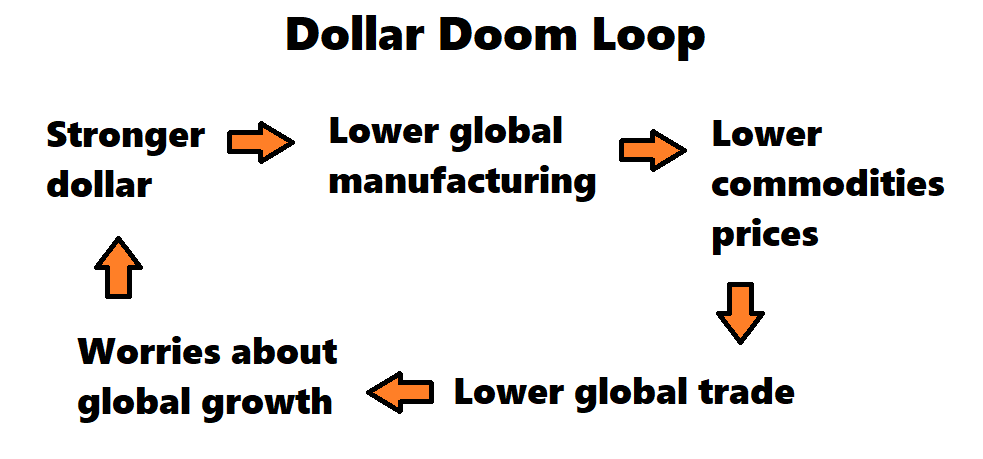

The dollar’s gain is the world’s pain — and based on its current trajectory, the world may be in for a whole lot more discomfort.

Concerns over global growth have recently sent the US Dollar Index to the strongest level on record, with the greenback hitting multi-decade highs against currencies like the euro and the yen.

But the move risks becoming a self-reinforcing feedback loop given that the vast majority of cross-border trade is still denominated in dollars, and a stronger US currency has historically translated into a broad hit to the world economy.

Against the backdrop of higher-than-expected inflation and still-elevated commodities prices, the concern is that we’re in for a dollar ‘doom loop’ like never before, according to Jon Turek, the founder of JST Advisors and author of the Cheap Convexity blog.

With the Federal Reserve hiking interest rates at the fastest pace in decades, he says, it’s much less clear what could break the feedback loop in the next few months.

The Dollar Doom Loop with US inflation causing The Fed to tighten

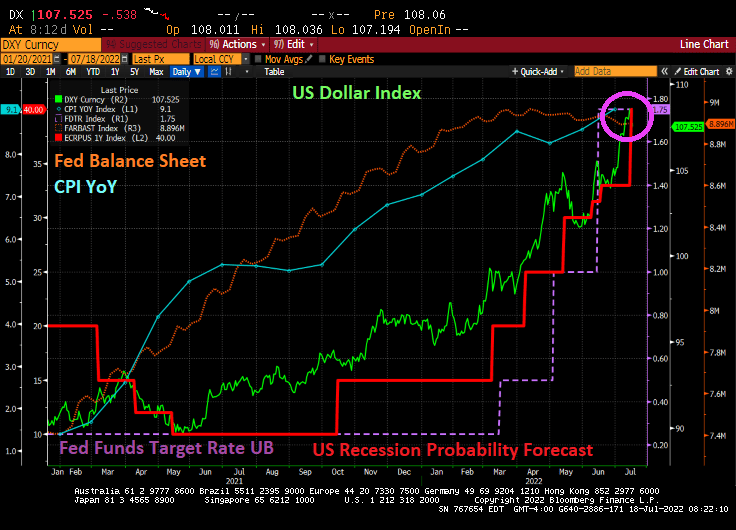

Under Biden’s policies, inflation hit a 40-year high (blue line), and the US Dollar (green line) is strengthening. Then we have The Fed raising the target rate (purple line) and the probability of recession rising with Fed tightening.

Is a US recession coming? The US Treasury 10Y-2Y yield curve is inverted at almost -20 basis points.

There is a Fed open market committee meeting in one week and they are expected to raise their target rate by 75 basis points according to Fed Fund Futures data. Inflation keeps rising as does the probability of a US recession. So, The Fed will keep on tightening.

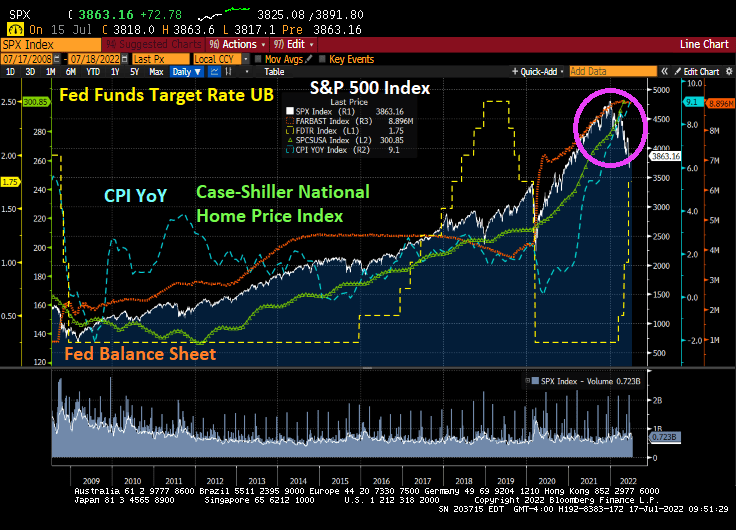

The Federal Reserve has behaved like buckaroos! Why? Since the financial crisis, The Fed has left its enormous monetary stimulus outstanding for too long.

The Fed initiated asset purchases in a series of moves (aka, QE) culminating in Covid QE that has been barley removed. With The Fed’s stimulypto (and Federal spending), we have seen the S&P 500 index soar along with home prices.

Of course, this begs the question as to whether the stock market and housing market can withstand The Fed’s tightening plans.

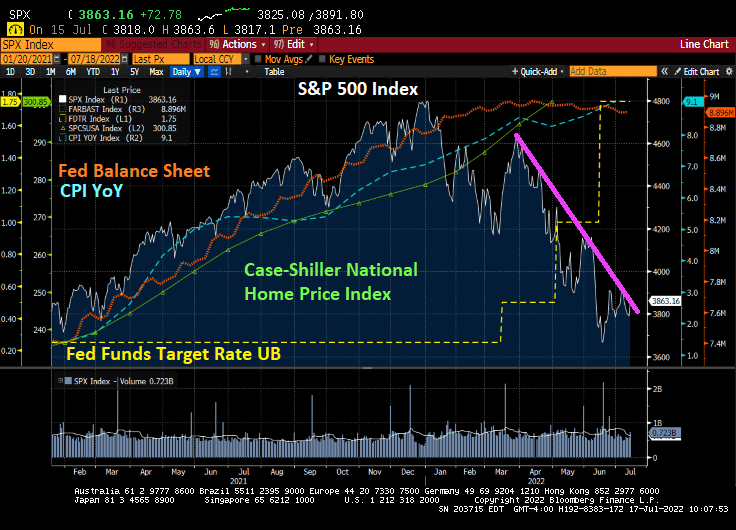

A closer look at the S&P 500 index and the Case-Shiller National home price index under Biden. The S&P 500 has been declining since The Fed started their monetary tightening. But the Case-Shiller National home price index as of April ’22 was still soaring.

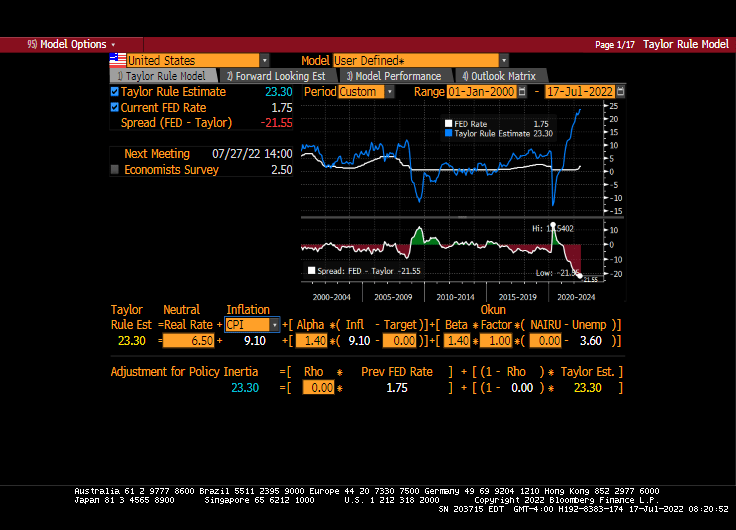

With inflation at a 40-year high, the Taylor Rule suggests a Fed target rate of … 23.30%. It is currently at 1.75%. That is an unrealistic target rate that The Fed will never do. It is, in fact, a Bridge Too Far.

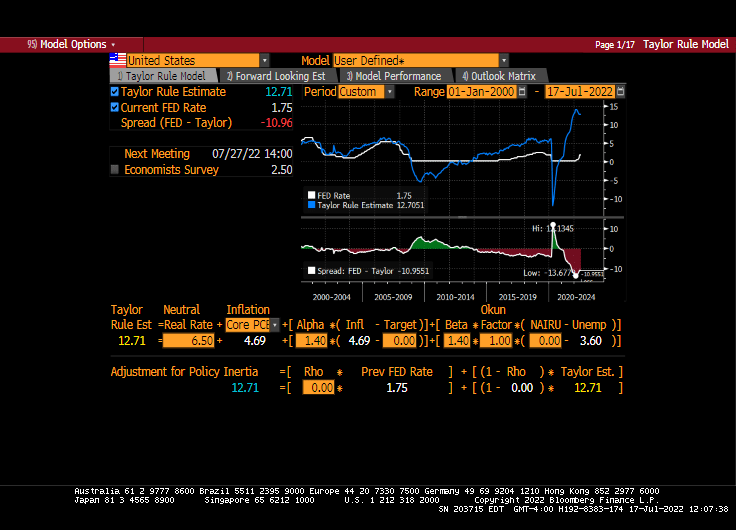

How about the Taylor Rule using Core PCE? It is still 12.71%. Still a bridge too far!

Markets are conditioned to massive Fed stimulypto, so how will markets react to stimulus reduction?

While The Fed is intent on withdrawing SOME of the enormous monetary stimulus, they are still buckaroos. And Biden/Congress still want to distort markets by Federal spending such as the Build Back (Inflation) Better bill that Manchin has blocked … so far.

Housing in the US is simply unaffordable for the middle class and low-wage workers. Combine rising food costs and gasoline/heating costs, and we have an economic disaster on our hands.

US existing home sales for June will be released on Wednesday. But can The Fed kill-off home price inflation?

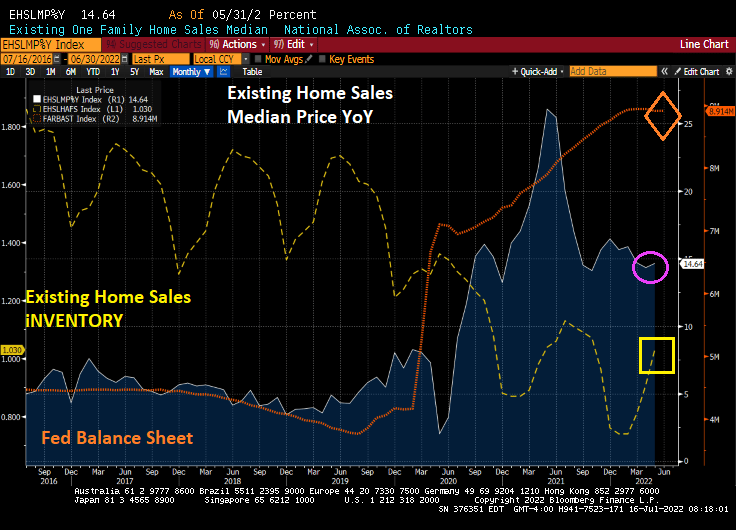

A preliminary analysis of existing home sales for June is for a seasonally adjusted annual rate of 5.1 million, down 5.4% from May and down 14.2% from last June. As The Fed cranks up its target rate (green line) and eventually shrinking its balance sheet, we will see further shrinking of existing home sales this summer.

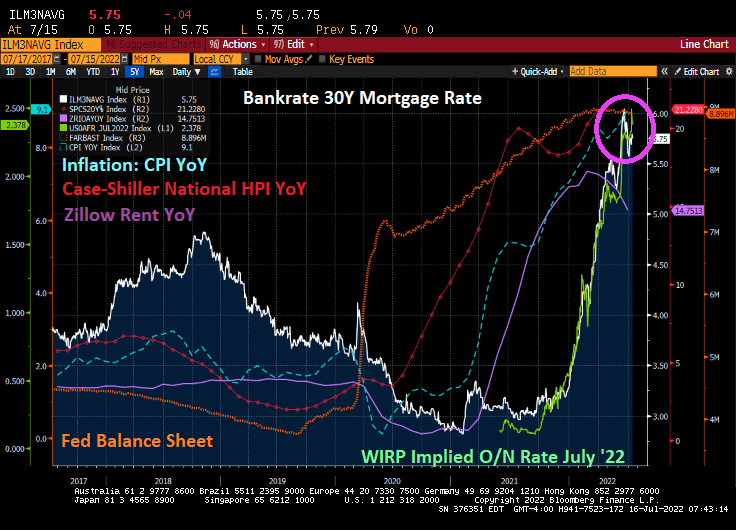

But home price inflation remains high (Case-Shiller National home price index at 21.23% YoY, Zillow’s rent index at 14.75% YoY) while the Consumer Price Index YoY is at 40-year high of 9.1% YoY. In other words, home price inflation is 233% of the stated inflation rate from Uncle Sam.

May’s existing home sales report was … sobering. There is still historically low levels of available inventory and median sales price of existing home sales was 14.64% YoY. Of course, the alternative to ownership is renting which is growing at 14.75% YoY. Simply unaffordable.

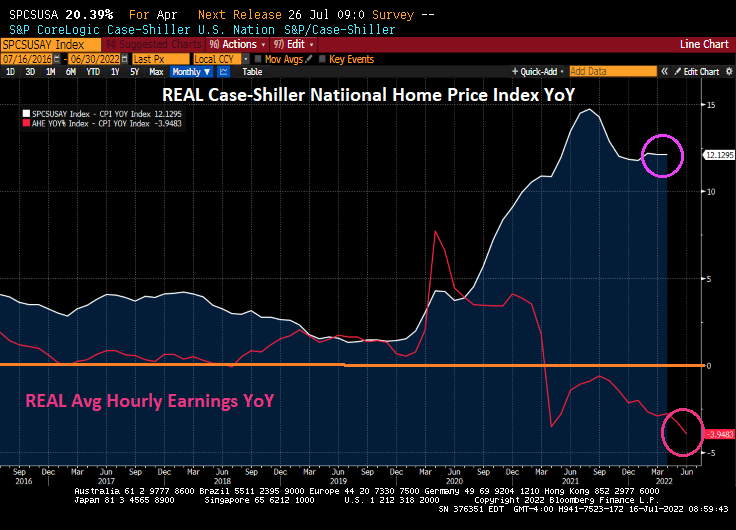

The gap between REAL home price growth (12.13% YoY) and REAL average hourly earnings (-3.95% YoY).

Consumer sentiment for housing is near the lowest level since 1982.

The Fed seems determined to remove the punch bowl in its efforts to crush inflation. But will The Fed’s efforts also crush the housing and mortgage market?

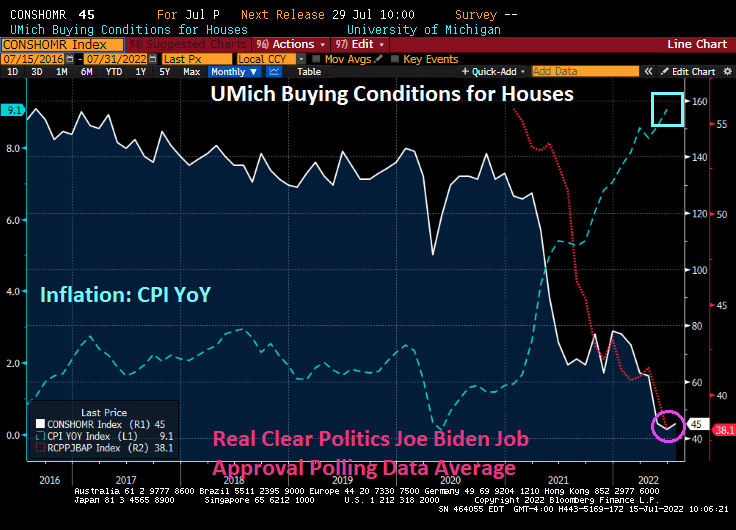

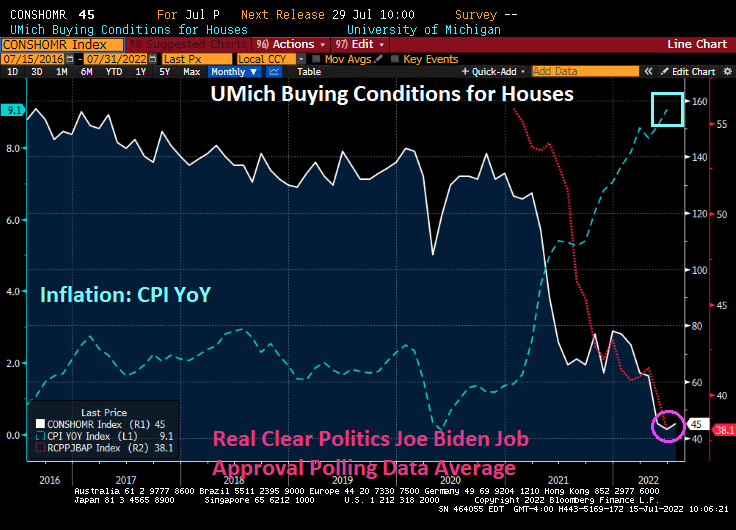

One measure of how bad things are in the US for the middle-class and low-wager workers ix consumer sentiment from University of Michigan. The latest University of Michigan survey of consumers remains depressed at 51.1.

The consumer sentiment index was at 80.7 at the beginning of 2021, but has plunged dramatically with rising gasoline, food and inflation in general. Biden’s popularity has sunk from 55.8 in January 2021 to 38.1 today.

How about housing sentiment? Housing sentiment was 134.0 in January 2021 but has plunged to a depressing 45 with inflation and rising home prices (and rent). And with declining sentiment about housing, Biden’s popularity has plunged.

As Americans are painfully aware, inflation is the highest in 40 years prompting The Federal Reserve to remove the massive punch bowl. In fact, Federal Reserve Governor Christopher “Fats” Waller backed raising rates by 75 basis points this month.

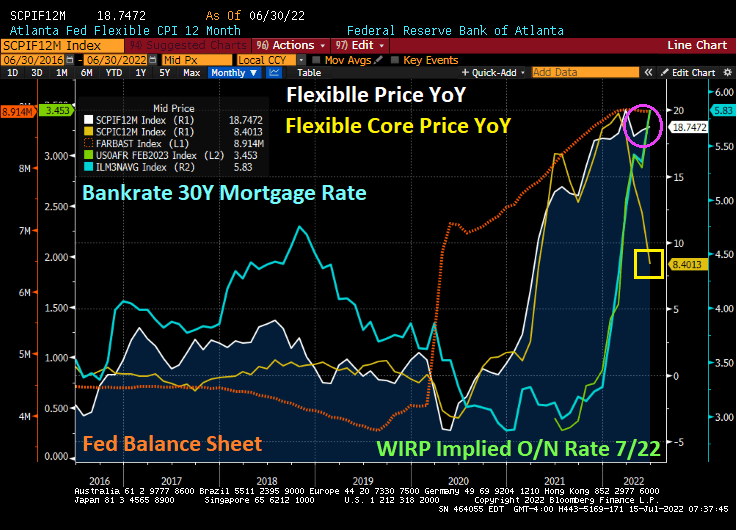

How hot was the recent inflation report? The Atlanta Fed’s flexible price index rose to 18.74% YoY. On the other hand, the CORE flexible price index (less energy and food) plunged to 8.46% YoY. The 30-year mortgage rate from Bankrate rose slightly to 5.83% as the implied overnight rate for the July FOMC meeting rose to 3.45%.

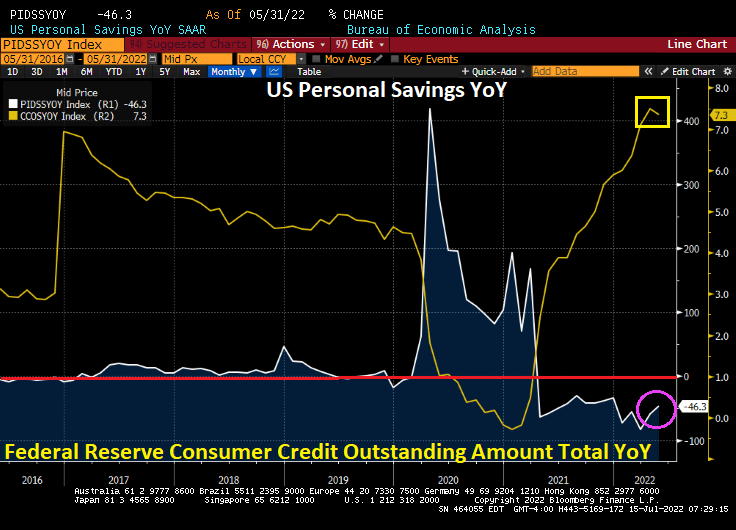

Inflation is ravaging consumers with the savings rate falling by -46.3% YoY while consumer credit rose 7.3% YoY. Yes, thanks to high inflation, consumers are saving less and borrowing more.

When even CORE flexible price inflation is 8.40% YoY, you know that The Fed and Federal government have made serious policy errors.

You must be logged in to post a comment.