On the commodity side, Spot Silver is up 1.46%. Iron Ore is up 1.60%, but I don’t think my neighbors would appreciate me taking delivery on 10 tons of iron ore on my driveway! Heating oil is up 2.90%.

On the crypto side, bitcoin is up 20.84 (0.08%) with Ethereum up slightly more.

Bitcoin and silver doing well as the US Dollar loses ground since September 2022.

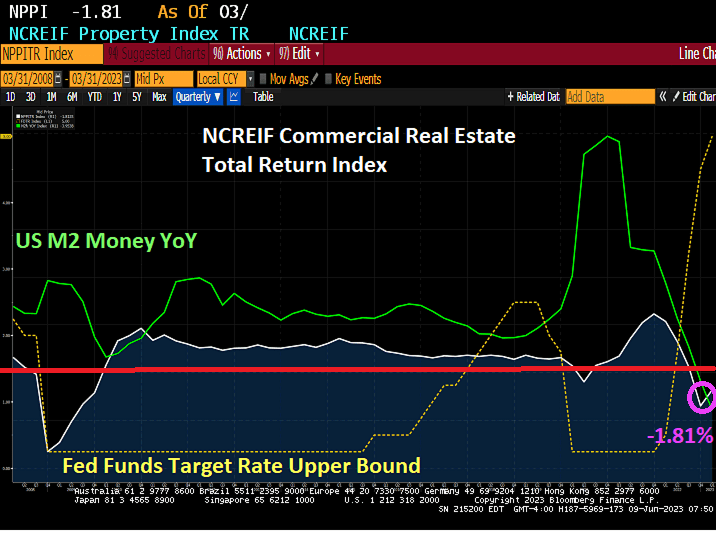

Between work at home, Bidenflation and The Feral Reserve, commercial real estate and regional banks are suffering … and it could get a lot worse. And Joe Biden (aka, Negan) in general. Living in Negan Country!

The work-from-home trend has been taking its toll on office landlords and is now making its way through to banks’ commercial loan portfolios, leading some analysts to predict that more trauma could be on the way for regional banks this year.

And in the current climate of bank failures, short sellers, and nervous depositors, banks with large exposures to commercial real estate (CRE) loans are racing to clean up and sell down their loan portfolios in hopes that they will not fall victim to another round of bank runs.

“There is an estimated $1.5 trillion of commercial property debt that will be due for repayment in about 18 months,” Peter Earle, an economist at the American Institute for Economic Research, told The Epoch Times. “It’s not improbable that even if interest rates have fallen by that time, some of that real estate debt will nevertheless be impaired and have an adverse impact on regional banks.”

In step with a recent trend in the CRE market, tech giant Google announced in May that it was attempting to sublease 1.4 million square feet of vacant office space in its Silicon Valley home base in order to “match the needs of our hybrid workforce.” Despite more employees returning to their offices this year, average office occupancy rates across the United States are still below 50 percent.

According to a report by Bank of America, 68 percent of CRE loans are held by regional banks. Approximately $450 billion in CRE loans will mature in 2023. JPMorgan Chase estimated that CRE loans comprise, on average 28.7 percent of the assets of small and regional banks, and projected that 21 percent of CRE loans will ultimately default, costing banks about $38 billion in losses.

Double Hit (of Biden’s Policies) Commercial mortgages are getting hit on two fronts: first, by the lack of demand for office space, leading to credit concerns regarding landlords, and second, by interest rate hikes that make it significantly more expensive for borrowers to refinance.

According to a June 12 report by Trepp, a CRE analytics firm, CRE loans that were originated a decade ago, when average mortgage rates were 4.58 percent, are now coming due, and in today’s market, fixed-rate CRE loan rates are averaging around 6.5 percent.

Banks that make CRE loans consider factors like debt service coverage ratios (DSCRs), which measure a property’s income relative to cash payments due on loans. Simulating mortgage interest rates from 5.5 percent to 7.5 percent, Trepp projected that between 28 percent and 44 percent, respectively, of currently outstanding CRE loans would fail to meet the 1.25 DSCR ratio today, and thus be ineligible for refinancing.

These calculations were done assuming current cash flows from properties stay the same and that loans are interest-only, but with vacancies rising, many landlords may have substantially less cash flow available. In addition, whereas interest-only CRE loans were 88 percent of the market in 2021, lenders are now switching to amortizing mortgages to reduce risk, which significantly increases debt service payments.

Refinancing Issues Fitch, a rating agency, projected that approximately one-third of commercial mortgages coming due between April and December of this year will be unable to refinance, given current interest rates and rental income.

“It’s a very different world now from the one in which the majority of these loans were made,” Earle said. “In a zero-interest-rate environment, before the COVID lockdowns saw many businesses shift to a remote work basis, many of these loan portfolios full of office properties looked great. Now, a substantial portion of them look quite vulnerable.”

The Trepp report highlighted several regional markets, such as San Francisco, where office sublease offers jumped 140 percent since 2020, and Los Angeles, where office vacancies hit a historic high of 22 percent. Available office space in Washington D.C. increased to 21.7 percent in the first quarter of 2023.

New York has been hit hard, as well. Office occupancy rates in New York City plummeted from 90 percent to 10 percent in 2020 during the COVID pandemic, but only recovered to 48 percent this year. Revenue from office leases fell by 18.5 percent between December 2019 and December 2022.

Vacancy Rates at 30-Year High Overall, according to a report by analysts at New York University and Columbia Business School, office vacancy rates are at a 30-year high in many American cities.

The report found that “remote work led to large drops in lease revenues, occupancy, lease renewal rates, and market rents in the commercial office sector.”

The authors predict that, even if office occupancy returns to pre-pandemic levels, “we revalue New York City office buildings, taking into account both the cash flow and discount rate implications of these shocks, and find a 44% decline in long run value. For the U.S., we find a $506.3 billion value destruction.”

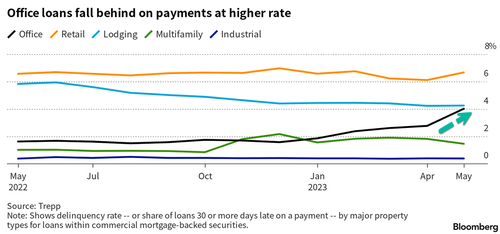

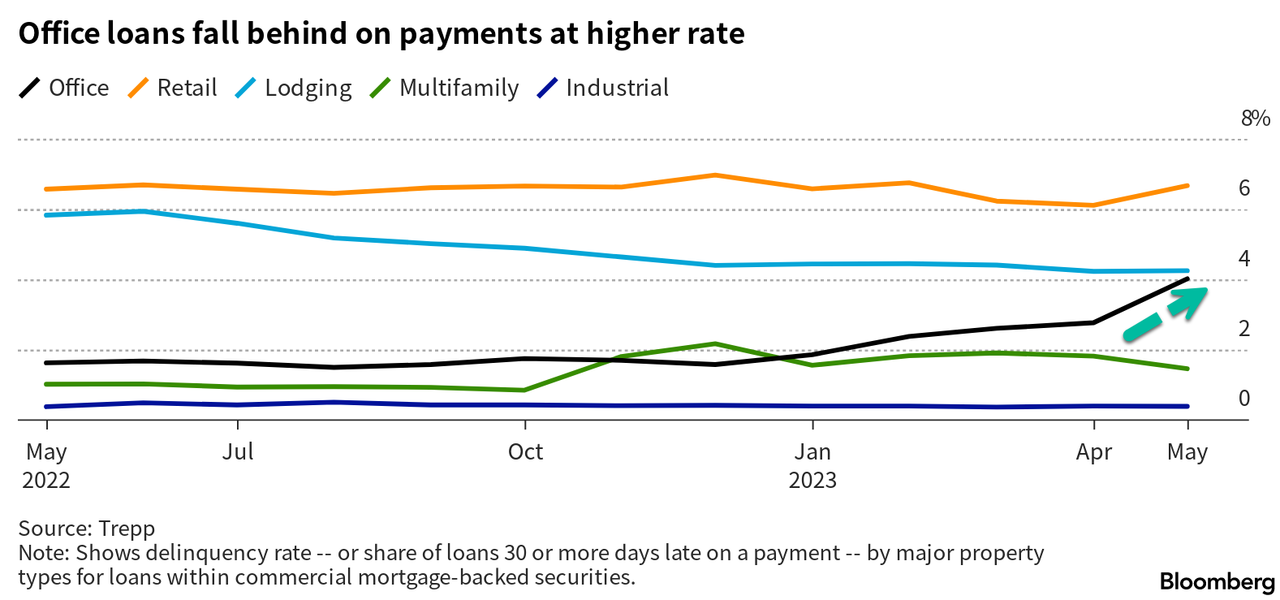

As predicted, delinquencies in commercial mortgage loans are now creeping up. Missed payments in commercial mortgage-backed securities (CMBS) increased half a percent in May over the prior month to 3.62 percent, Trepp reports. The worst component of the CMBS market, which includes multi-unit rental buildings, medical facilities, malls, warehouses, and hotels, was offices, where delinquencies increased 125 basis points to more than 4 percent.

To put this in perspective, however, CMBS delinquencies exceeded 10 percent in 2012 and 2020. And analysts say that lending criteria for CRE have been more conservative than they were before the mortgage crisis of 2008, leaving more cushion on ratios relative to a decade ago.

All the same, the credit crunch at regional banks has created a vicious circle, where banks race to pare down their CRE portfolios, and the dearth of financing leaves more landlords facing default as outstanding loans mature. To make matters worse, commercial property values, which provide collateral for the loans, appear to be taking a hit as well.

In an effort to rapidly clean up their CRE loan portfolios and avoid the fate of failed banks like Silicon Valley Bank, Signature Bank, and First Republic Bank, banks are now attempting to sell off the loans, often taking a loss in the process.

In May, PacWest, a regional bank, sold $2.6 billion of construction loans at a loss. Citizens Bank reportedly has put $1.8 billion of its CRE loans up for sale during the first quarter of this year. Customers Bancorp reduced its CRE lending by $25 million and put $16 million of its existing portfolio up for sale.

Wells Fargo, one of the top four largest U.S. banks, is also downsizing its CRE portfolio, and in announcing the move CEO Charlie Scharf stated, “we will see losses, no question about it.”

“Between the Fed’s 500+ basis point hikes over the past 16 months and the failure of Silicon Valley Bank, and others, earlier this year, a credit tightening is already underway,” Earle said. “That has put a lot of pressure on regional lenders.”

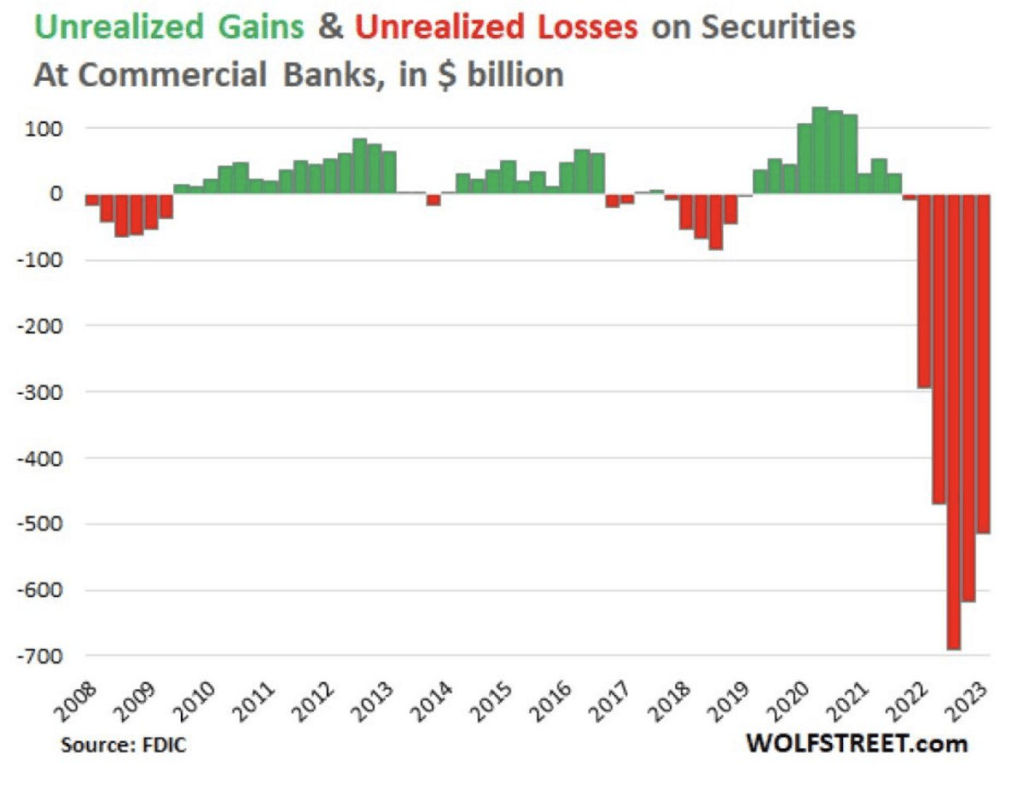

A March academic study titled “Monetary Tightening and U.S. Bank Fragility in 2023” stated that the market value of assets held by U.S. banks is $2.2 trillion lower than what is reported in terms of their book value. This represents an average 10 percent decline in the market value of assets across the U.S. banking industry, and much of this decline came from commercial real estate loans.

Consequently, the authors wrote, “even if only half of uninsured depositors decide to withdraw, almost 190 banks with assets of $300 billion are at a potential risk of impairment, meaning that the mark-to-market value of their remaining assets after these withdrawals will be insufficient to repay all insured deposits.”

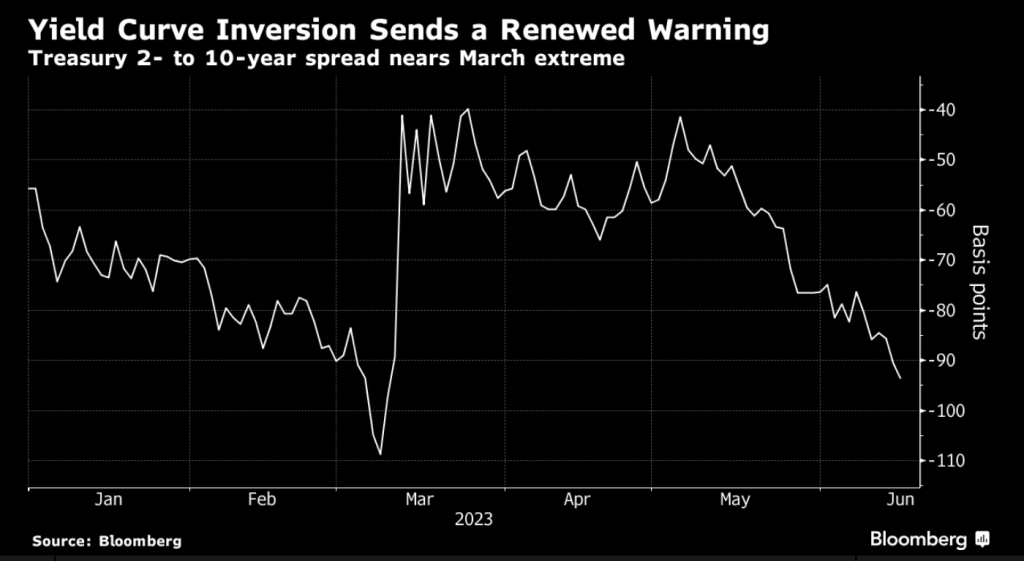

61% of Bloomberg terminal respondents (including me, by the way) see Fed hikes leading to recession.

Bond traders are stepping up wagers that the Federal Reserve will steer the US economy into a recession.

Policy-sensitive front-end Treasuries led a selloff Thursday, while longer-date bonds lagged, a day after Fed officials indicated that they’re prepared to raise interest rates by another half-point this year following the first pause in the central bank’s 15-month hiking campaign. That sent the yield-curve inversion, as measured by the gap between two- and 10-year securities, to 95 basis points — a level last sustained in March — and approaching this cycle’s 109-basis-point extreme.

The price action suggests bond traders are skeptical that policymakers can avoid a so-called hard landing as they continue to press the case for higher borrowing costs in an effort to get a handle on inflation that remains more than double their 2% target.

“The Fed runs the risk of solving one policy error of being too easy for too long with another policy error as they ignore the growing credit contraction and persistent losses from higher rates,” said George Goncalves, head of US macro strategy at MUFG. “The catch-22 is that for them to ease, something now has to break or the economy has to crack.”

It’s not just bond traders who are growing concerned.

Sixty-one percent of respondents in a Bloomberg poll of terminal users conducted in the hours after the Federal Open Market Committee decision said tighter monetary policy will ultimately cause a recession at some point in the next year.

“The Fed was clearly trying to send a hawkish message that they are not quite done yet and don’t think they have made enough progress on inflation,” said Michael Cudzil, portfolio manager at Pacific Investment Management Co. “You see curve flattening and rates not pricing in the full extent of hikes, so the thinking is that these hikes may bite and the Fed is closer to the end.”

Officials left their target range for the federal funds rate unchanged at 5% to 5.25% Wednesday, but projected the key rate will rise to 5.6% by the end of this year, implying two more quarter-point increases, up from 5.1% in March. They also revised higher estimates of core inflation for year-end to 3.9%, from 3.6%, owing to what Chair Jerome Powell called surprisingly persistent price pressures.

Still, markets aren’t convinced borrowing costs will rise as high as central bankers project.

The highest rate on swap contracts for future meetings by early Thursday was around 5.32% for both September and November, with July at 5.27%, compared to a current Fed effective rate of 5.08.

The Fed’s aggressive outlook for rate hikes through year-end may be an effort to dash bond-market expectations for cuts in the months ahead, according to Michael de Pass, global head of linear rates at Citadel Securities.

While The Fed paused at their recent FOMC meeting, they are expected to raise their target rate at the July meeting …. then stop. Despite being only a little over 50% of where they should be (10.12%) to cool inflation.

Okay, Joe Biden was generally regarded as the dumbest member of the US Senate and mean-spirited (I won’t repeat podcaster Joe Rogan’s opinion of Biden). Now we realize how brazenly corrupt Biden is (taking bribes from China and Ukraine to influence American poliicies). Not only is Biden an attrocious human being, but his policies have damaged the US middle class terribly thanks to inflation.

Some structural factors, such as remote work and hybrid work, have doomed the office space segment. This has left empty office buildings scattered across major US cities as the number of landlords falling behind on repayments due to the difficulty of refinancing and high vacancies has hit a five-year high.

According to real estate data firm Trepp, more than 4% of office loans packed into commercial mortgage-backed securities were delinquent in the last 30 days as of May, the highest level since 2018.

Dan McNamara, the founder of Polpo Capital Management, told Bloomberg about impending CRE turmoil:

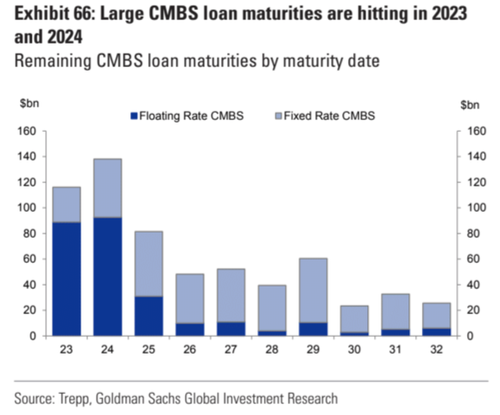

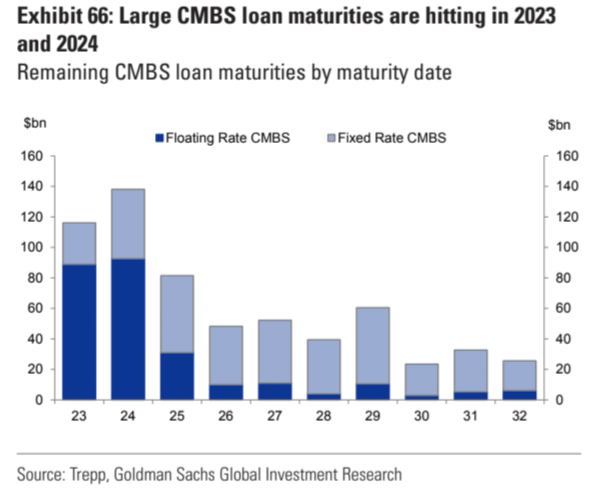

“This is just the tip of the iceberg for office delinquencies as $35 billion in CMBS office loans are scheduled to mature this year and the refinancing market is effectively shut to this asset class.”

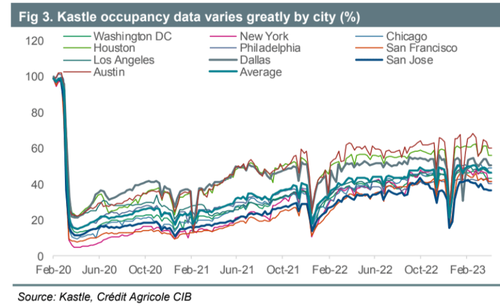

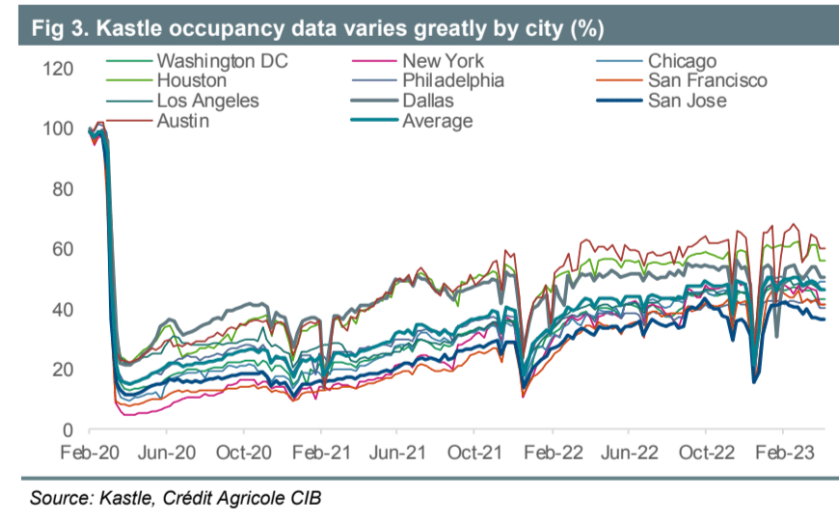

The rise in delinquencies comes as security card swipe data from Kastle shows many workers have yet to return to their desks in major US cities, resulting in high office space vacancies nationwide.

As Goldman pointed out to clients days ago, one major issue is a steep maturity wall of floating and fixed-rate CMBS loans due this year and next. The inability to refinance in these challenging market conditions will likely unleash a tidal wave of defaults in the second half of this year.

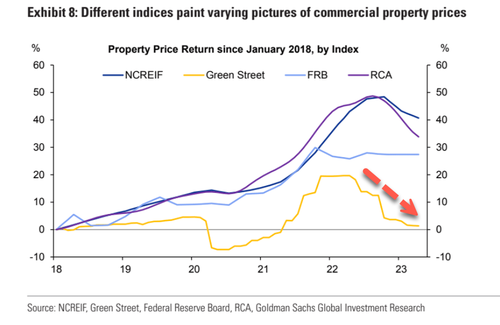

Goldman Sachs chief credit strategist Lotfi Karoui told clients last month, “the most accurate portrayal of current market conditions” is data via the Green Street Commercial Property Price Index, which suggests trouble ahead.

Just how much danger? Karoui believes “Green Street indicates a 25% year-over-year drop in office property values and a 21% drop in apartment property values.”

So the combination of high vacancies, sliding prices, and tightening lending standards is a perfect storm that could ignite an eruption of delinquencies in office loans in the coming quarters.

Biden has a line on you! And it isn’t good. More like we are fish being caught and eaten by Washington DC bureaucrats.

Another example of Biden’s dismal economy. US pending home sales plunged -22.6% YoY in April. Even worse, REAL weekly wage growth has been negative for 23 straight months!

I have gotten a flood of emails and text messages asking about what happens if Biden defaults on the US debt. In short, Biden has made a career out of spending money, as has Speaker McCarthy. They both have an incentive to raise the debt ceiling, but whether it is cuts to Biden’s insane budget (higher than Covid-era spending) and wants to raise taxes on the middle class to pay for it. McCarthy wants a trimmed budget (aka, back to pre-Covid spending levels) and NOT raises taxes. They will eventually agree somewhere in the middle (US Congress member Pramila Jayapal will be outraged, but then again, she is ALWAYS outraged like Senator Elizabeth Warren) and AOC.

The Federal Reserve has taken a brief respite from fighting inflation that they helped cause. But with $188 TRILLION in unfunded entitlements promised by politicians, The Fed will undoubtedly start buying assets again (aka, QEInfinity) and the debt ceiling will keep being raised. In essence, the DC merry-go-round is broken and politicians will keep pushing it around until it collapses.

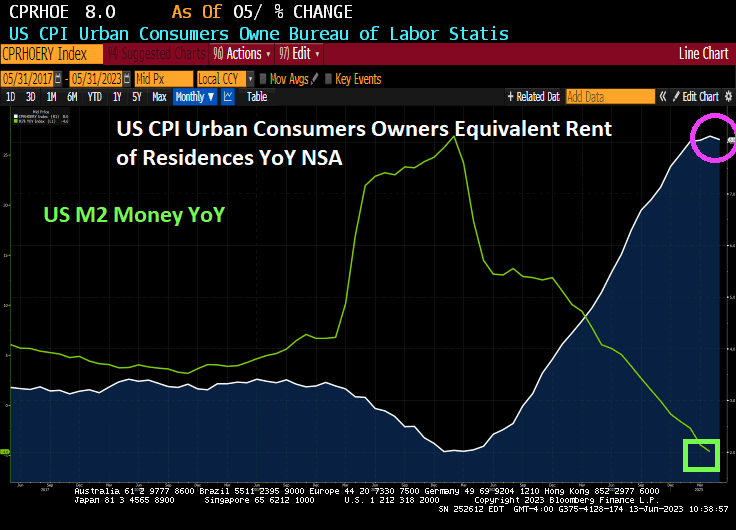

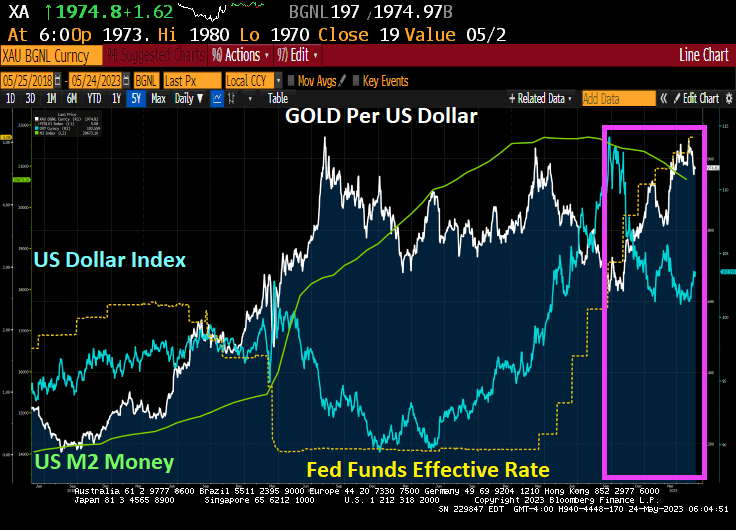

For the moment, The Federal Reserve is reducing M2 Money (green line). With it, the US Dollar (blue line) has declined. Gold (white line fever) is on the rise along with The Fed’s effective funds rate.

WTI crude is up over 1% this AM. And gold is up 2.29%. Heating oil is up 3.56%.

Face it, I have no confidence in Treasury Secretary Janet Yellen, one of the biggest propronents of MMT (modern monetary theory or borrow and spend without consequences). Yellen is NOT making lose my blues.

Treasury Secretary Janet “The Evil Hobbit” Yellen is a Statist. She can only think of an all powerful central government calling the shots since the private sector and individual liberties are something to be eliminated.

Yellen has mostly declined to spell out what her department would do if Congress fails to raise or suspend the debt limit before the Treasury finds itself unable to cover all the government’s obligations.

Back in Mordor on The Potomac, President Joe Biden and House Speaker Kevin McCarthy postponed a meeting on the debt ceiling set for Friday. People familiar with the talks said the postponement was a sign that staff-level talks were yielding progress.

Biden and congressional Republicans have been locked in disagreement for weeks over raising the US federal government’s $31.4 trillion borrowing limit. GOP leaders have demanded promises of future spending cuts before they approve a higher ceiling. Biden has jinsisted on a “clean” increase, with budget talks kept separate.

Now what no one in our lame pro-government media or Congress or Administration has said is the a US debt default does NOT necessarily mean that the US walks away from its debt. Very likely, China and Japan, our two biggest foreign debt holders, will insist on debt restructuring so that the US pays some fraction of debt owed, like 80%.

But foreign debt holders are a relatively small percentage of US debt holders. The Federal Reserve is the largest single borrower, thanks in part to Yellen who has formally Federal Reserve Chair,

Of course, financial entities like Vanguard, Blackrock and Fidelity are the largest holders of US debt. Since pensions invest heavily with these enetitites, the Federal government would restructure the debt rather than outright default.

US CDS 1Y continues to remain high as Biden/Yellen/Schumer play chicken with the lives of the American middle class while the political donor class is clamoring for endless spending and wealth transfers.

Remember, Biden, Yellen and Schumer all Statists and believe that their job is growing Federal government to wear it is all powerful and their donors get billions in subsidies and wealth transfers. You don’t think green energy subsidies make any common sense, do you? Wind turbines (aka, whale and eagle killing machines) are ineffective. We need nuclear power but Progressives fear nuclear power as much as they have Donald Trump.

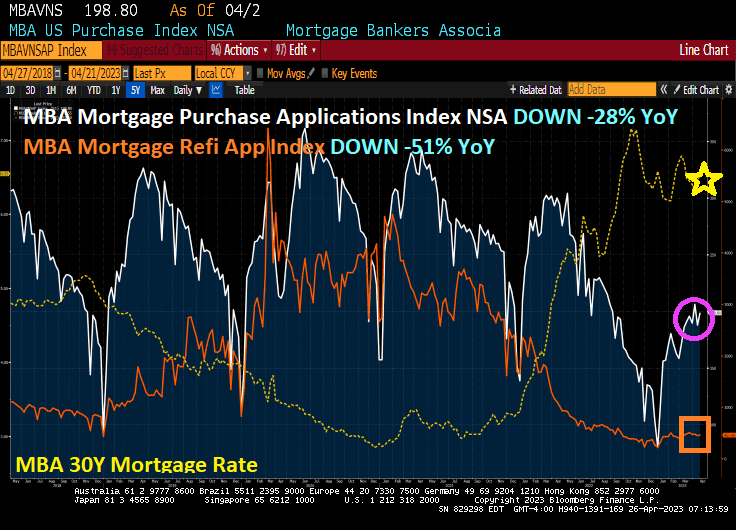

Mortgage applications increased 3.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending April 21, 2023.

The Market Composite Index, a measure of mortgage loan application volume, increased 3.7 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 5 percent compared with the previous week. The Refinance Index increased 2 percent from the previous week and was 51 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 5 percent from one week earlier. The unadjusted Purchase Index increased 6 percent compared with the previous week and was 28 percent lower than the same week one year ago.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.