Heartaches in heartaches. US GDP growth for Q2 has stumbled to 0.446% as The Fed is launching quantitative tightening (QT) to fight the inflation that they caused in the first place.

According to the Atlanta Fed’s GDPNow real-time GDP tracker, US GDP growth has stumbled to a meager 0.446%. Despite the massive stimulus from The Federal Reserve and Washington DC’s massive fiscal stimulus.

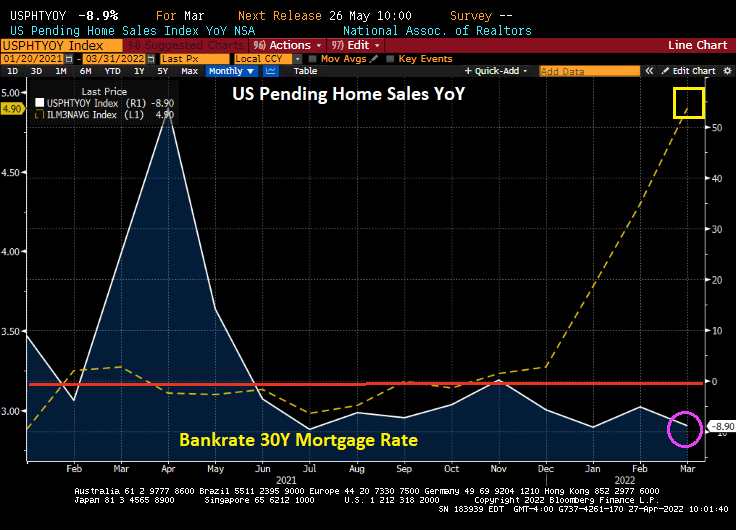

From the MBA: Mortgage Applications Decrease in Latest MBA Weekly Survey. Mortgage applications decreased 8.3 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending April 22, 2022.

The Refinance Index decreased 9 percent from the previous week and was 71 percent lower than the same week one year ago.

The seasonally adjusted Purchase Index decreased 8 percent from one week earlier. The unadjusted Purchase Index decreased 7 percent compared with the previous week and was17 percent lower than the same week one year ago.

The percentage of adjustable-rate mortgages (ARMs) increase 9.4% from previous week.

Yes, the 30-year mortgage rate is rising extremely fast.

“You’re Going Down” by Jerome Powell and The Constitution Avenue band. President Joe Biden conducting.

US existing home sales in March were expected to fall -0.6% from February, but they actually fell -8.6%. This is happening at The Federal Reserve is signaling tightening and mortgage rates are rising rapidly.

Making homes affordable is NOT one of the mottos for The Federal Reserve. But making homes outrageously unaffordable for the masses should be their motto.

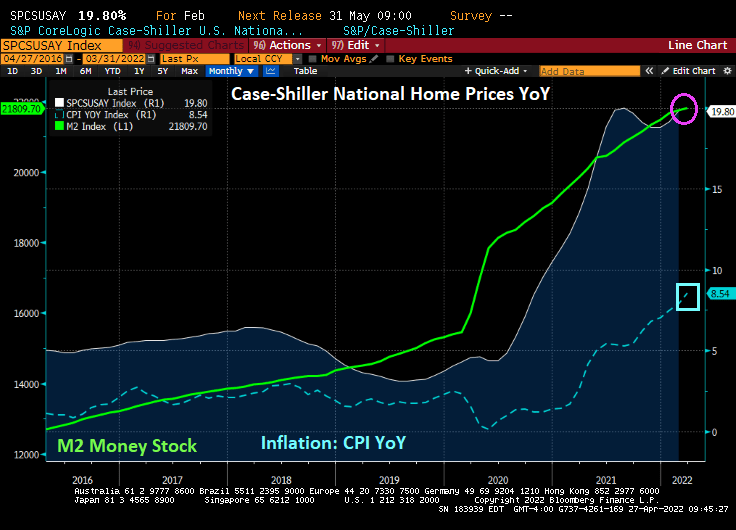

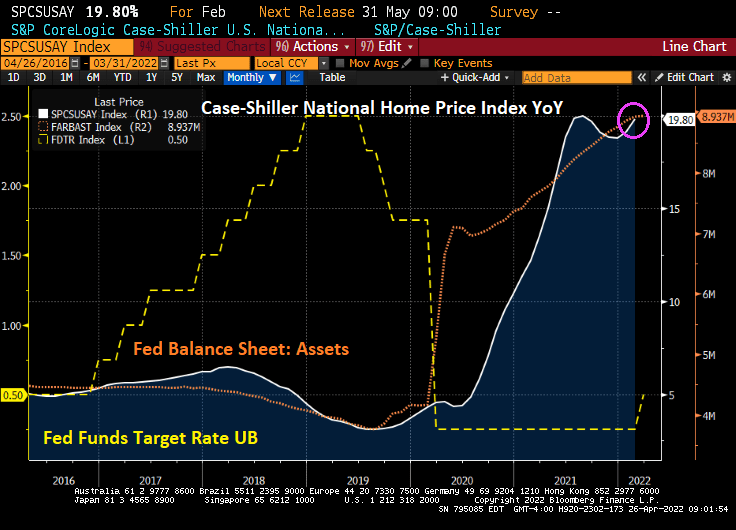

The February Case-Shiller home price indices are out for February and the national home price index rose to 19.80% YoY.

Instead of the limbo rock, The Fed is apparently trying to see “How HIGH can we go?”

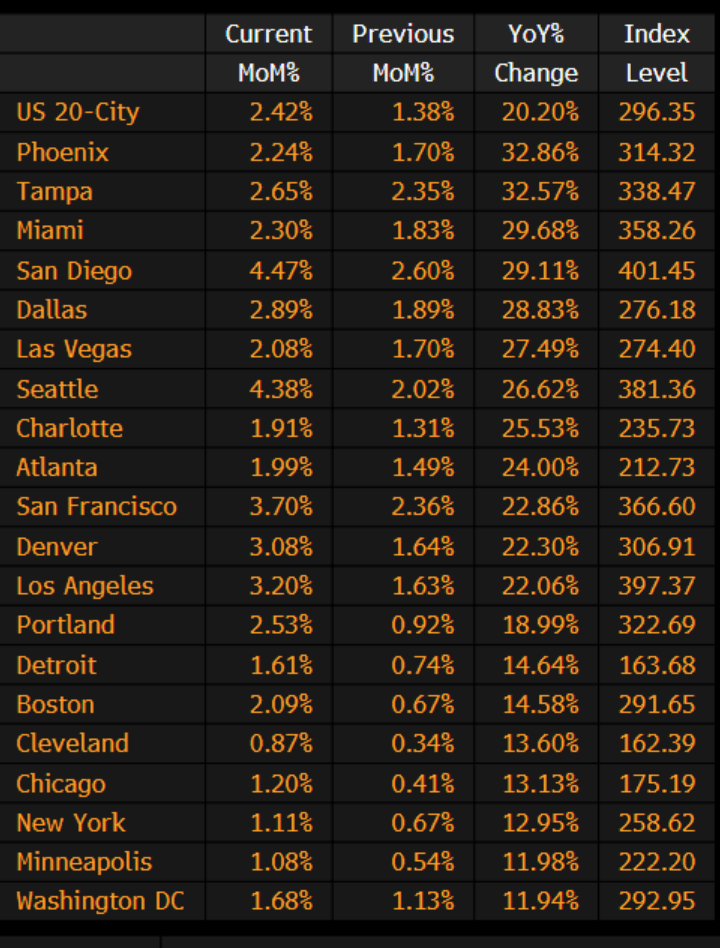

Once again, Phoenix is the fastest growing city in term of home prices at a sizzling 32.86% YoY. The slowest? Washington DC at 11.94% YoY. That’s right! 12 of the top 20 metro areas had price growth of over 20% in February!

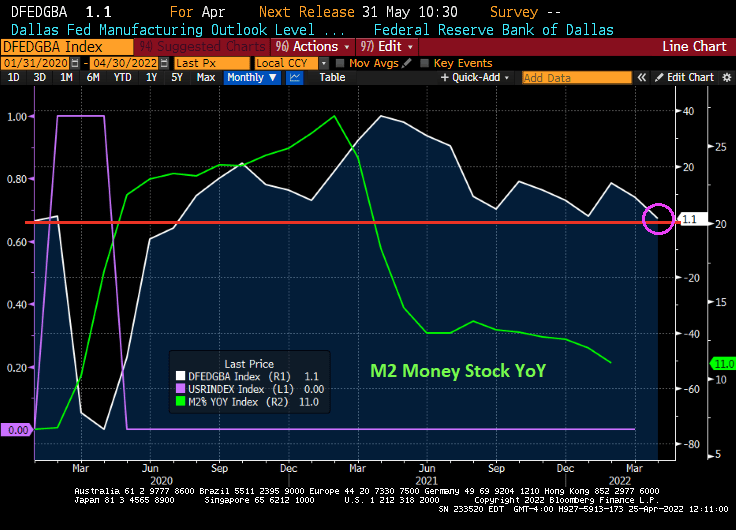

M2 Money stock YoY skyrocketed during the Covid mini-recession, peaking at 21% during February of 2021. The Dallas Fed manufacturing outlook grew to 38.1 in March 2021.

However, as M2 Money growth has slowed 11%, the Dallas Fed manufacturing outlook has plunged to near zero.

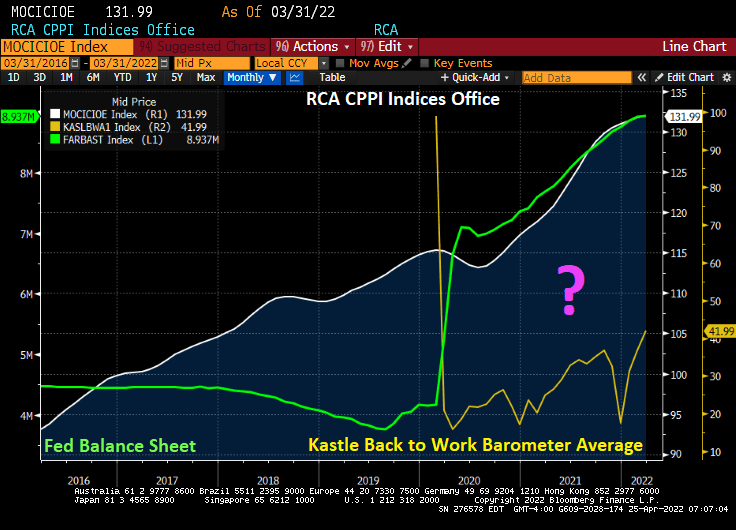

Do you want to see a magic trick? Like how governments shut down the US economy resulting in collapsing office occupancy rates while the price of office buildings rose dramatically (+16.3% since Q2 2020)?

Kastle’s “Back to work barometer” is showing that the 10 city average occupancy rate in the US is now only 42.8% as remote working has caught on. And the fear of yet another Covid mutation is keeping office occupancy below 50%.

Even Washington DC, home of Dr. Anthony Fauci, has only a 37.5% occupancy rate. Of the top 10 cities, Austin TX has the highest office occupancy rate at 62.4%.

So, the magic trick is not why America is so slow to return to the office, but why commercial office prices are rising so fast. Ah, Federal government STIMULYTPO! Aka, The Federal Reserve has been overstimulating the economy since 2008 and particularly since 2020 and Covid.

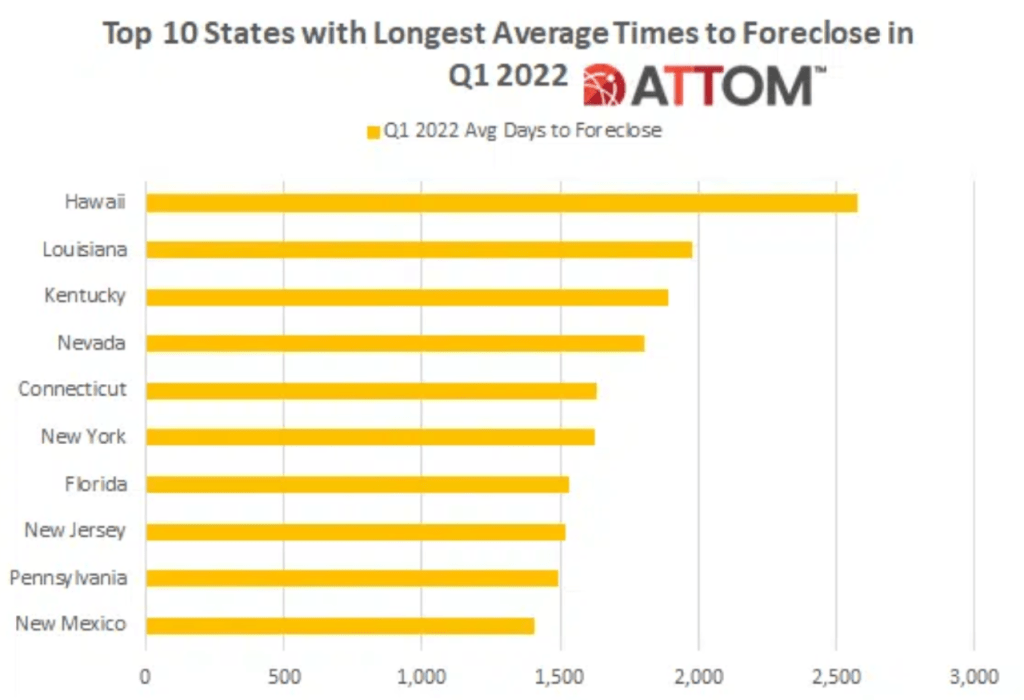

Speaking of a magic trick, here is how government’s make the average time to foreclosure up to over 7 years in Hawaii and 4.4 years in New York. In simple terms, you can buy a home in New York, never make a mortgage payment and live rent free for an average of 4.4 years.

So, the government’s magic trick is to 1) shut down local economies in fear of Covid, 2) provide excessive fiscal and monetary stimulus to combat the shutdown, 3) watch office building prices soar with stimulus as office occupancy remains below 50%.

Do you want to see a magic trick? Watch The Fed try to tighten monetary easing and NOT crash the economy.

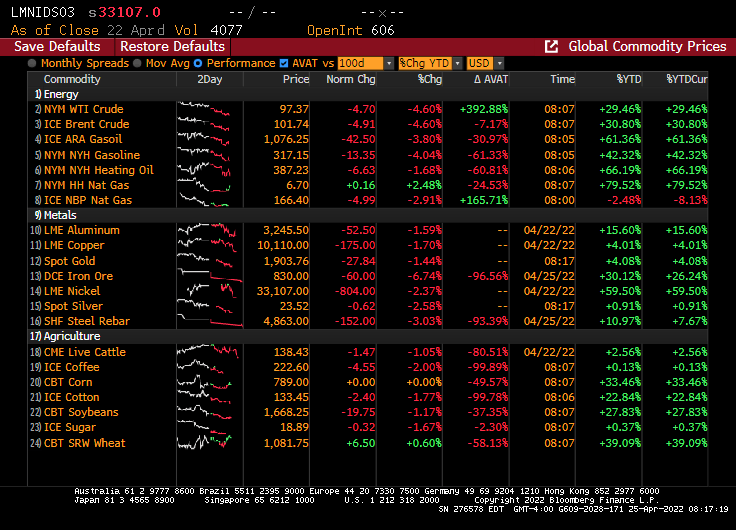

Update for 04/25/2022. 10Y Treasury yields DOWN 8.7 bps.

And commodities are tanking. WTI oil is down 5%, iron ore is down almost 7%.

And the Dow is diving with increased expectations of Fed monetary tightening, but the expectations (green line) have been declining this morning.

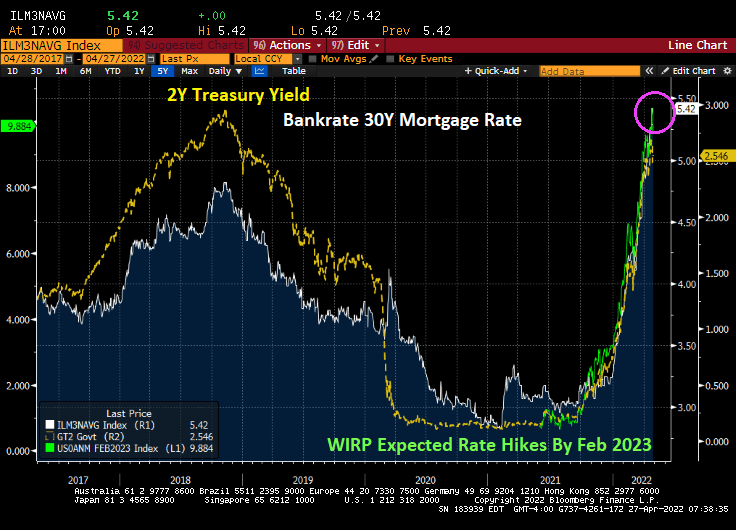

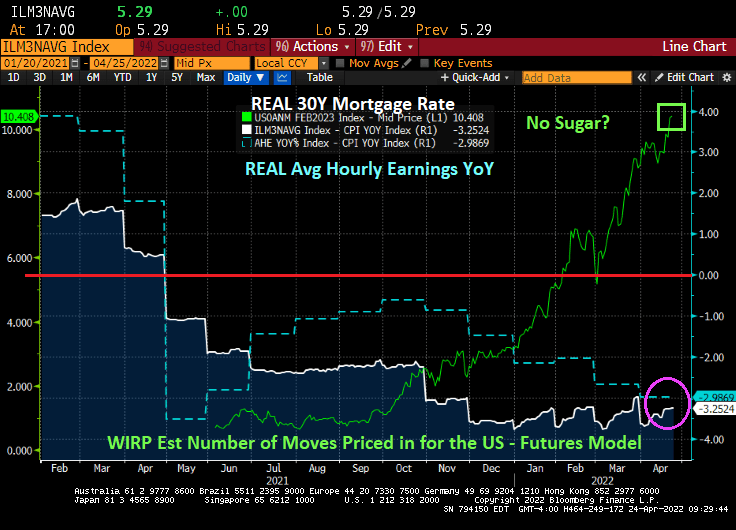

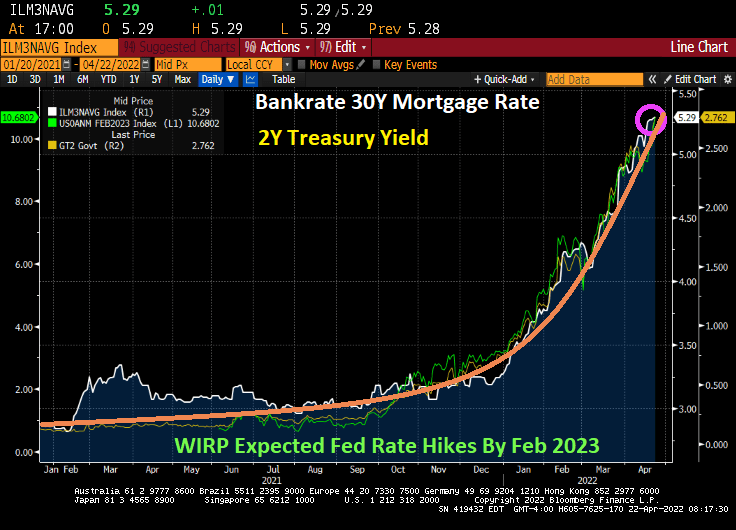

As The Fed sings “No sugar tonight” exemplified by the number of expected Fed rate hikes by February 2023 has grown to 10.4. Mortgage rates are now the highest since 2009, but inflation is the highest in 40 years. The result? The REAL 30-year mortgage rate is -3.25%.

REAL average hourly earnings are now a terrible -2.99% YoY thanks to the worst inflation in 40 years. REAL home prices are growing at 11.8% YoY.

Traders are betting that even with the Fed boosting its target for the federal funds rate by 2.5 percentage points this year to 3% won’t be enough to get the inflation rate back down to 2% over the next decade from around 8.5% currently.

In nominal terms, mortgage rates are seemingly trying to rise to 2007 levels (6.5%). But the gap between the 30-year mortgage rate and Fed Funds target rates is back to 2009 levels.

Talk about Fed and Fed government OVER stimulypto! Even REAL US home prices grew at 12% YoY pace while the REAL Fed Funds Target rate is -8.04%.

Its Saturday and I am dreading markets opening on Monday. But here is where we sit today.

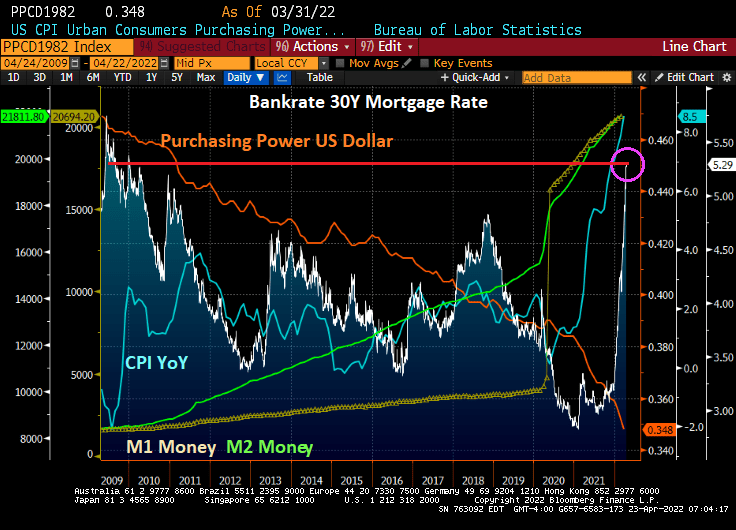

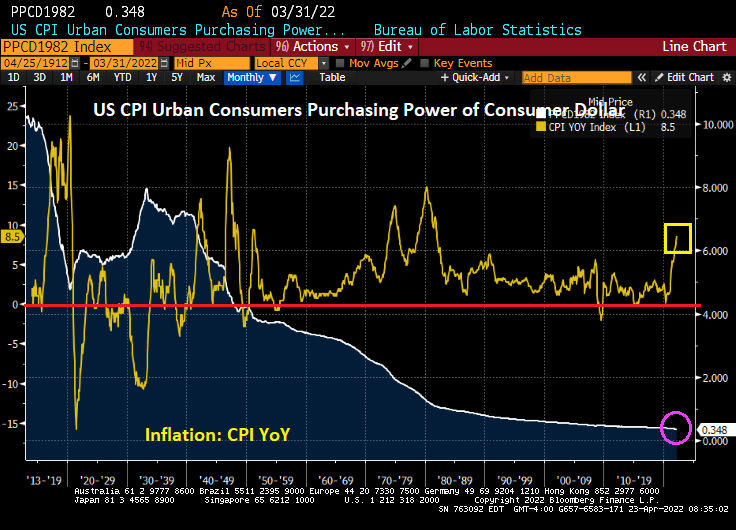

The 30-year mortgage rate has soared to 5.29%, the highest level since 2009 at the beginning of Obama’s Presidency. Since 2009, we have seen the purchasing power of the US Dollar decline further (orange line) while inflation (blue line) has soared. M1 (yellow) and M2 (green) has been growing since the financial crisis, but really took-off with the Covid outbreak in 2020 and The Fed’s massive overreaction coupled with Federal government stimulus.

Since the creation of The Federal Reserve System under President Woodrow Wilson, the purchasing power of the US Dollar has collapsed so much that $10 in 1913 in worth 34.8 cents today. But notice that since 1949, the CPI YoY has rarely been negative meaning that prices are pretty much only going up.

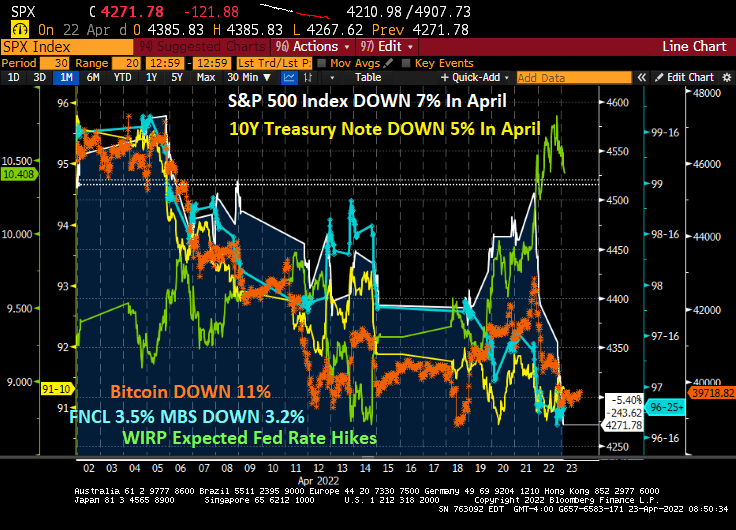

Instead of April showers bring May flowers, it is April expected Fed rate hikes (now 10.408 rate hikes by February 2023) bringing declining assets prices. In April so far, the S&P 500 index is DOWN 7%, the 10-year Treasury Note price is DOWN 5%, Bitcoin is DOWN 11%, the 3.5 coupon agency MBS price is down 3.2%.

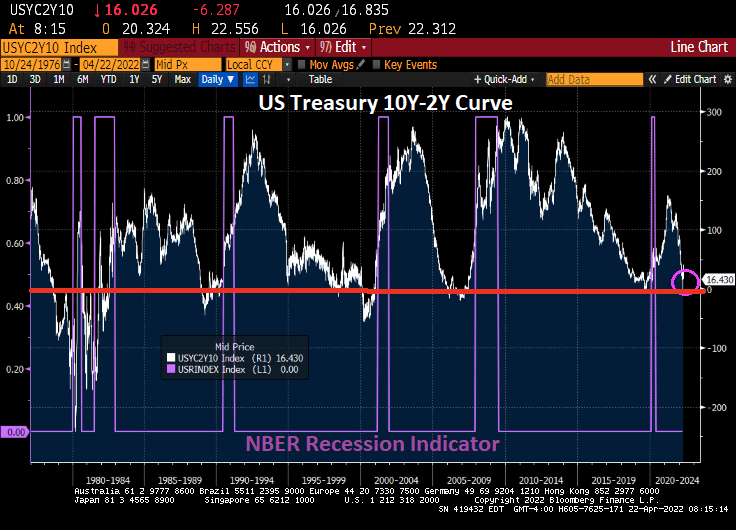

We are seeing increased volatility in both the equity and bond markets.

Well, Powell and The Fed are hurling fireballs at mortgage rates and asset prices in April.

Federal Reserve Chair Jerome Powell said he saw merit in the argument for front-loading interest-rate increases, including a half percentage-point hike next month.“

I would say that 50 basis points will be on the table for the May meeting,” Powell told an IMF-hosted panel on Thursday in Washington that he shared with European Central Bank

President Christine Lagarde and other officials. “We really are committed to using our tools to get 2% inflation back,” he said, referring to the Fed’s target for annual price increases.

Central bankers are grappling with some of the highest inflation rates since the 1980s that are being further pressured as Russia’s invasion of Ukraine boosts food and energy prices and China’s coronavirus lockdowns tangles supply chains anew.

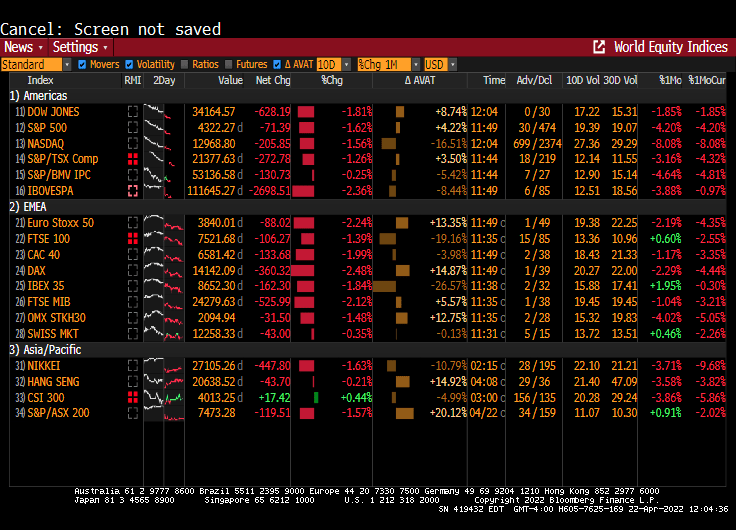

Equity markets in the USA and Europe are getting “Powell’d” and “Lagarde’d” today. As of noon today, the Dow is down 628 points (or -1.81%). Euro Stoxx 50 is down -2.24%.

I remember appearing on Fox Business’ Stuart Varney and Company where he asked me what will happen when The Fed starts to raise rates in a serious fashion. I made a ka-boom gesture at which he laughed. Stuart, I wasn’t joking!

US President Biden went green and signed executive orders on his first day to limit oil and natural gas exploration of Federal lands and offshore (also, killed the Keystone Pipeline), helping to drive up energy prices and food prices. These orders begat inflation (also caused by the massive Covid relief by the Federal government). The highest inflation in 40 years begat The Federal Reserve signalling a tightening of Fed monetary policy … to fight the problem caused by The Fed in the first place … too much monetary stimulus for too long. Fiscal and monetary fanaticism and ignorance is forever busy and needs feeding

There was an interesting article on MarketWatch entitled “Bond rout exposes Social Security’s insanity.” The headline was “Every dollar of yours that’s invested in the Social Security trust fund is invested in low-yielding government bonds.”

Yes, another disastrous consequence of The Fed’s lax monetary policy since 2008, helping to push Treasury yields extremely low. And REAL Treasury yields into negative territory.

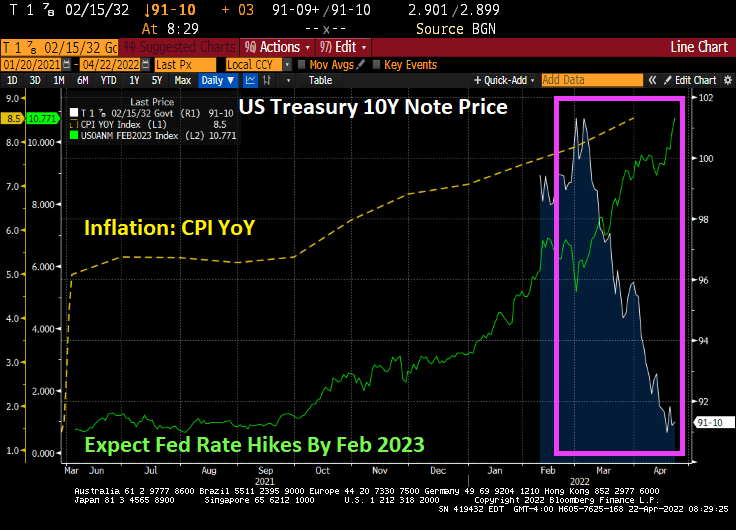

But here we sit today with The Fed threatening to trim their balance sheet and raise rates … to combat the inflation they helped create in the first place. Now we have the 10-year Treasury Note price falling like a paralyzed falcon with expected hate hikes going above rate hikes by February 2023 (based on Fed Funds Futures prices).

Most pension funds also invest heaving in US Treasuries, along with agency Mortgage-backed Securities (AgencyMBS).

You must be logged in to post a comment.