Call this a double whammy! Red-hot rents combined with a slowing economy.

According to CoreLogic, single-family annual rent growth finished 2021 at a new record: 11.7% YoY for high tier rental properties and 10.4% YoY for low tier rental properties.

Of course, southern and southwest rental properties are seeing the fastest rent growth. Particularly Miami at 36% YoY. Phoenix is no slouch at 19% growth in rents.

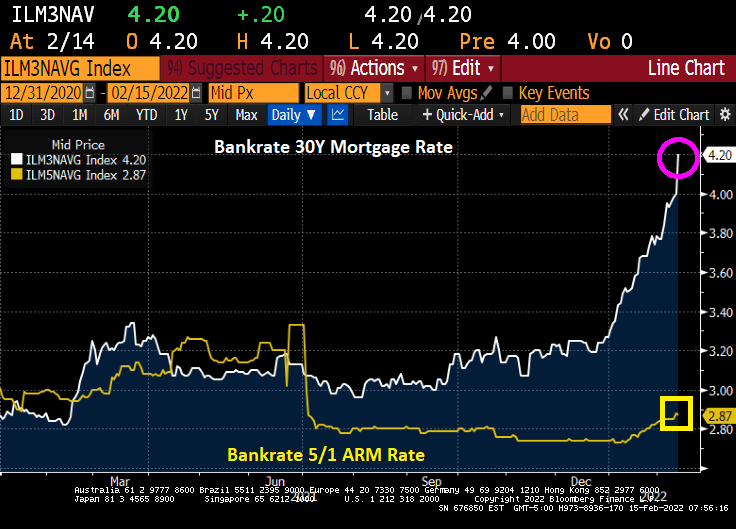

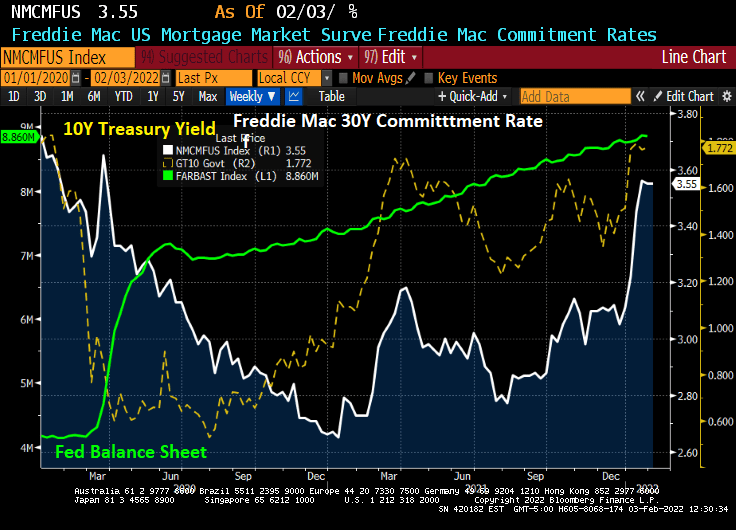

The US 30-year mortgage rate broke through the 4% barrier. According to Bankrate’s mortgage survey, the 30-year mortgage rate is now 4.2%.

Even more interesting is the 5/1 Adjustable Rate Mortgage (ARM) rate falling slightly to 2.87%. That is quite a spread between the 30-year fixed and 5/1 ARM rates! That is 133 basis points.

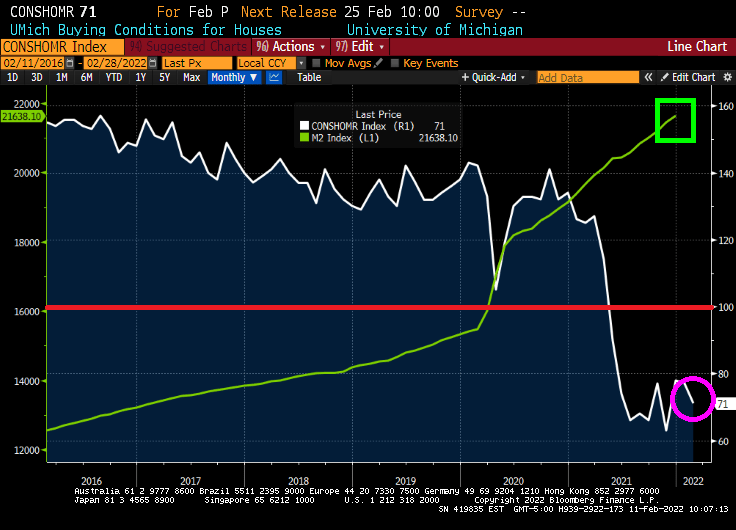

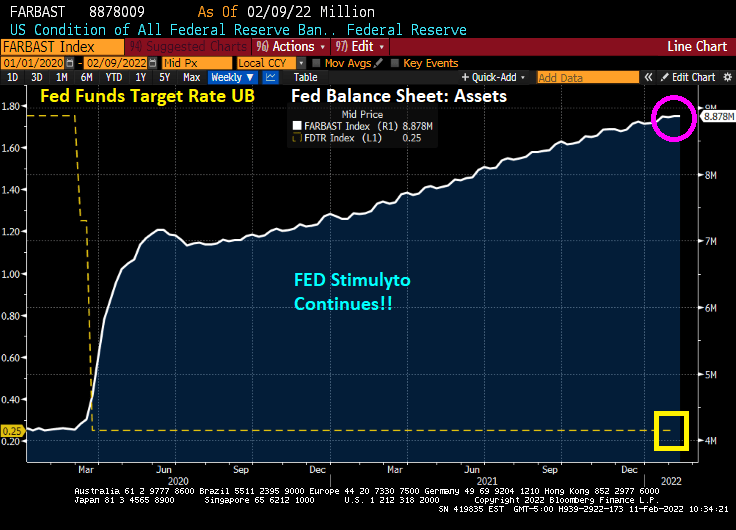

The University of Michigan consumer survey is out for February. And an ugly survey is it! Buying conditions for housing fell to 71 as The Federal Reserve continues it monetary stimulypto!

Despite 7.5% inflation, The Fed continues its “Stimulytpo” monetary policy.

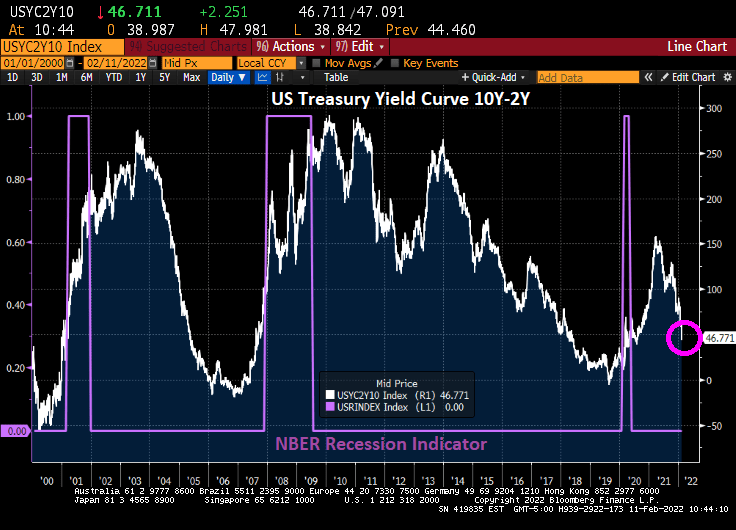

US consumer confidence is the lowest in 10 years as the yield curve crashes.

Here is the POMO schedule just released by The Fed.

I am reminded of my roommate at University of Wyoming who played James Brown over and over and over again. Much like The Fed doing nothing to curb inflation. Until they finally do something with a crashing yield curve.

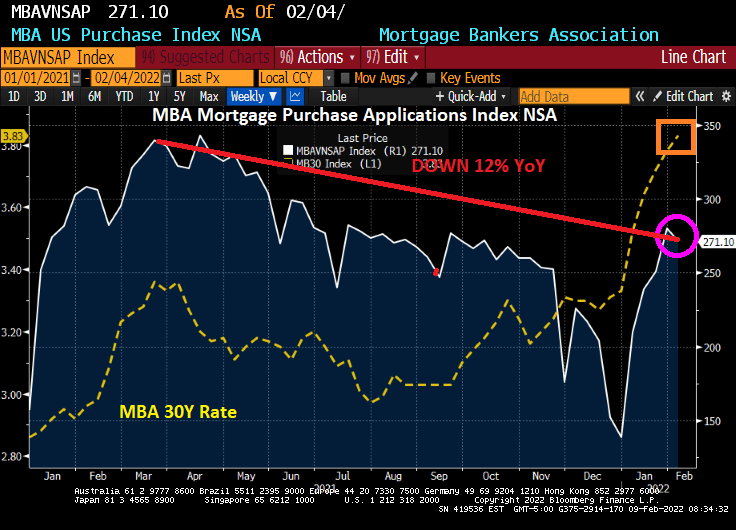

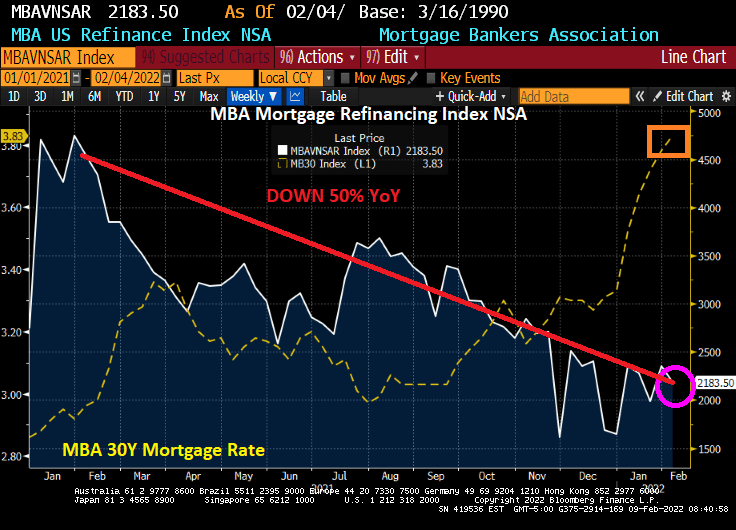

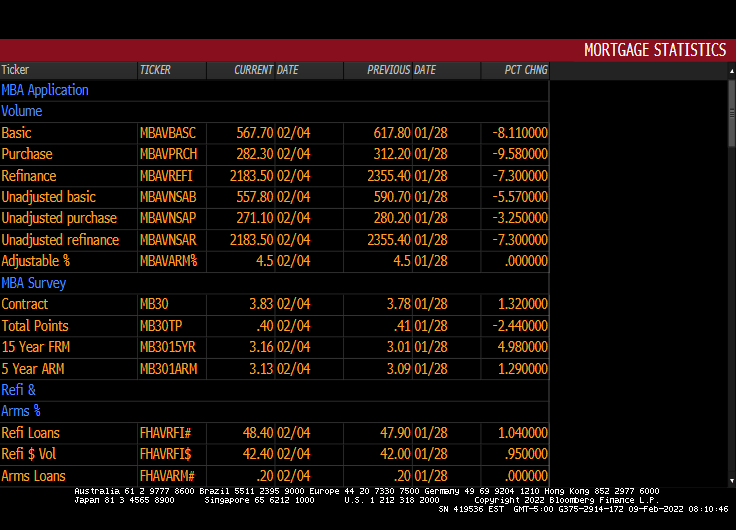

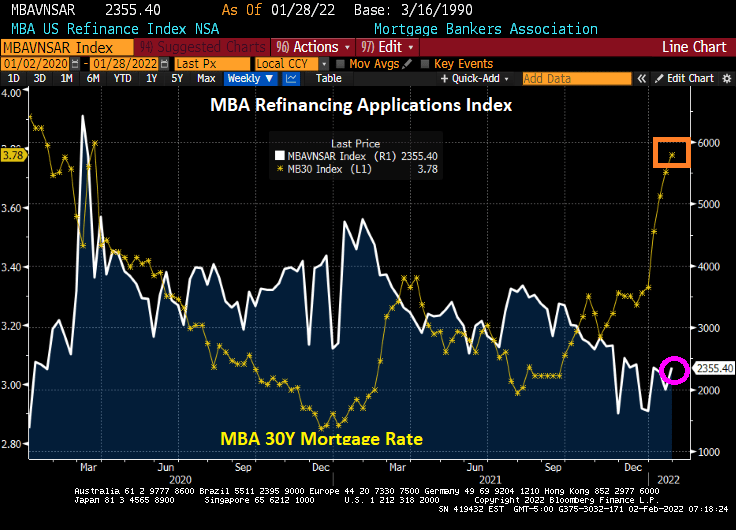

The Mortgage Bankers Association (MBA) released their weekly mortgage application survey this morning. Mortgage applications decreased 8.1 percent from one week earlier, for the week ending February 4, 2022.

The Refinance Index decreased 7 percent from the previous week and was 52 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 10 percent from one week earlier. The unadjusted Purchase Index decreased 3 percent compared with the previous week and was 12 percent lower than the same week one year ago.

And mortgage refinancing applications are down 50% since the same week last week.

Here are the stats. Pretty much down across the board.

How bad is inflation in the USA? Try 18%, based on the Flexible Consumer Price Index.

The Flexible Price Consumer Price Index (CPI) is calculated from a subset of goods and services included in the CPI that change price relatively frequently. Because flexible prices are quick to change, it assumes that when these prices are set, they incorporate less of an expectation about future inflation.

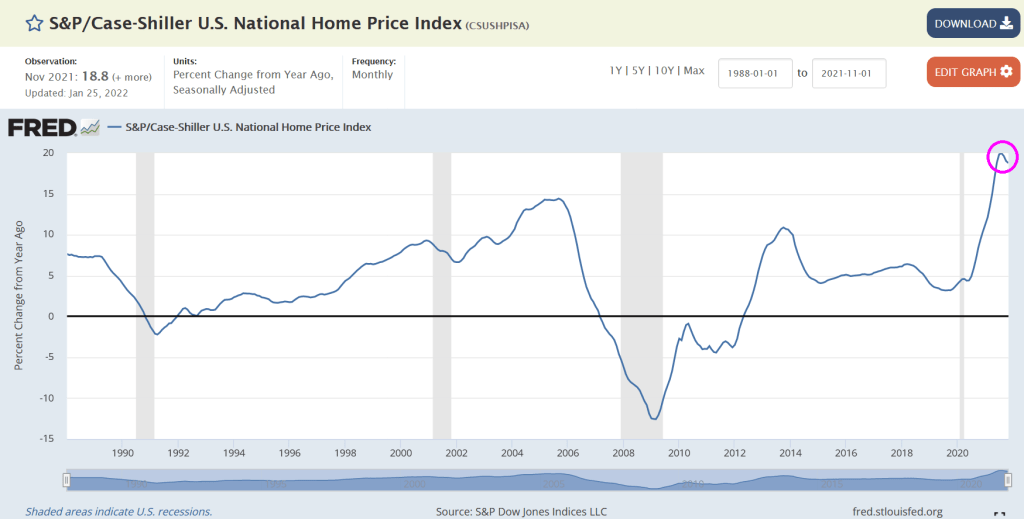

Again, remember that Federal inflation numbers woefully undercount housing and rent inflation. For example, the Case-Shiller National Home Price index (as of November 2021) was growing at 18.8%.

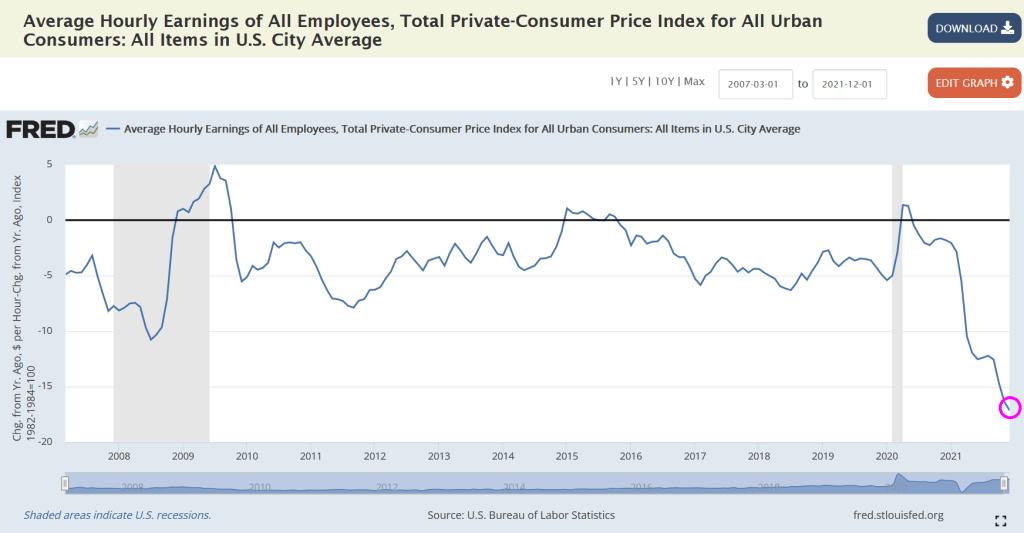

The sad part is that inflation-adjusted average hourly earnings growth of all employees is crashing thanks to inflation.

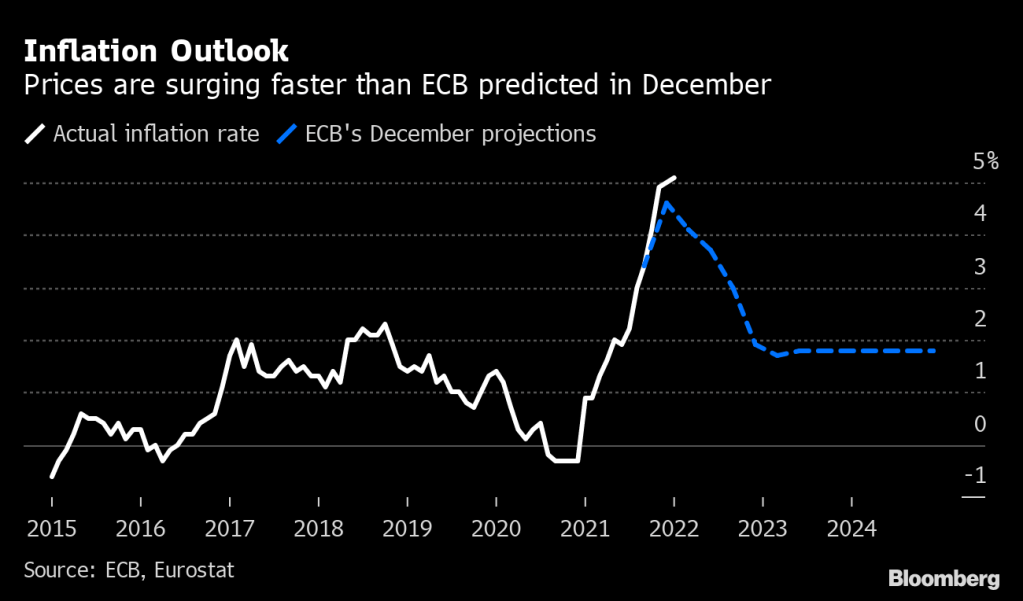

(Bloomberg) — European Central Bank President Christine Lagarde is no longer ruling out an interest-rate hike this year, a pivot toward the tightening stance of global peers that officials privately see materializing with a shift in policy guidance as soon as next month.

Investors brought forward bets on ECB action as the monetary chief delivered surprisingly hawkish comments citing unexpected record inflation data, contrasting with an earlier statement on Thursday that kept intact its formal view that price increases will ease.

She spoke after policy makers agreed that it’s sensible no longer to exclude a rate move in 2022, and that bond buying could end in the third quarter, according to officials familiar with their thinking who asked not to be identified because such discussions are confidential. An ECB spokesman declined to comment.

The result of Lagarde’s jaw boning?

US mortgage rates are rising in anticipation of the US following Largarde’s lead. Powell and the Gang continue to lag.

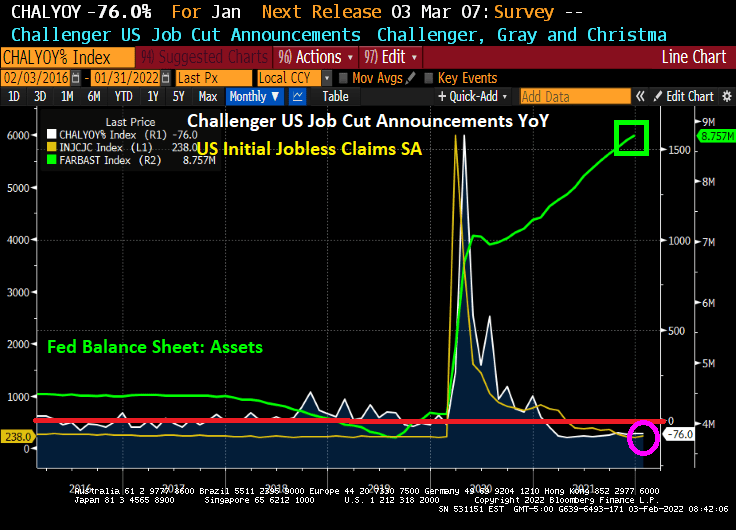

Between the Biden Administration, Anthony Fauci and the media constantly screaming about the devastating effects of Omicron, I would have expected massive job cuts and a large spike in jobless claims. But alas, the numbers and charts tell a different story.

Today, we saw that the Challenger job cuts for January fell further to 76%. Initial jobless claims fell to 236k. And The Federal Reserve is still hyper-stimulating the economy.

After listening to Biden spokesperson Jen Psaki preparing us for an end-of-times job report, I was expecting today’s news dump to be terrible. But alas, it just looks like another day in Stimulyoptoville.

Hey Jen, where’s the beef? Now that I think of it, Jen Psaki looks like Wendy from the burger franchise. Except that the burger Wendy doesn’t terrify people.

Hey, I thought the vaccine mandates and masks were supposed to stop COVID and its mutations in its tracks!

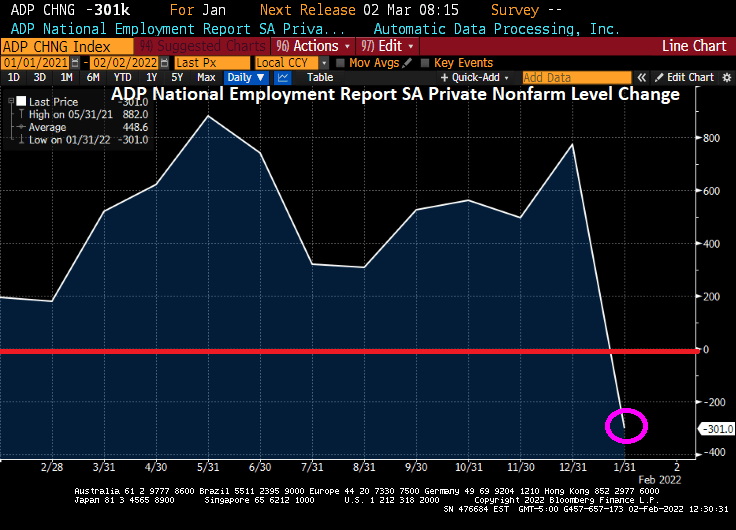

Instead, Omicron has taken a much bigger bite out of the labor market than expected, data from payroll processing firm ADP indicated Wednesday.

The number of workers on private payrolls fell by 301,000 in January, falling far short of expectations for growth of 225,000 jobs.

This was the first decline in payrolls reported by ADP since 2020.

The leisure and hospitality sector shed 154,000 jobs. Trade, transportation, and utilities dropped 62,000 workers. Other services saw payrolls decline by 23,000. Health and education jobs fell by 15,000. Information technology jobs fell by 8,000 and financial services sank by 9,000.

Manufacturers cut 21,000 positions. Construction declined by 10,000. Mining and natural resources added 4,000.

All told, the services sector’s payrolls fell by 274,000 and the goods-producing sector’s payrolls dropped by 27,000.

The Department of Labor will report the official count for January jobs on Friday. It is expected to show that jobs grew by around 170,000 but that may be an underestimate of the impact of omicron.

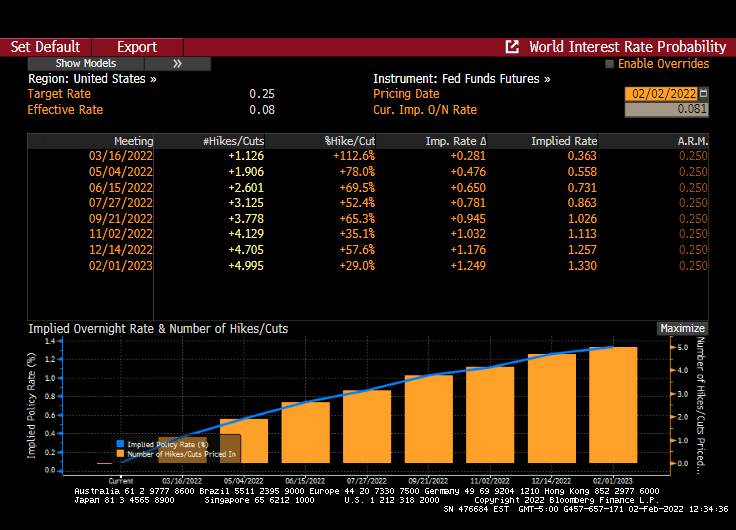

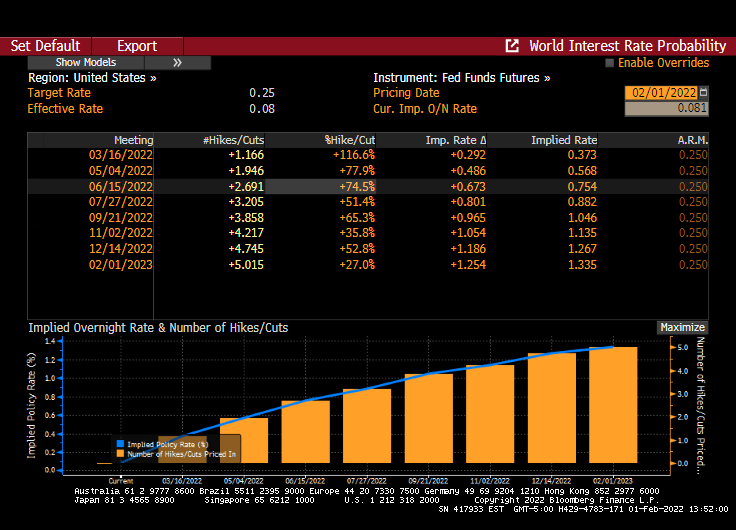

Since Omicron can be readily blamed for ADP report, it doesn’t look like it has affected the implied probability of 5 rate hikes over the next year.

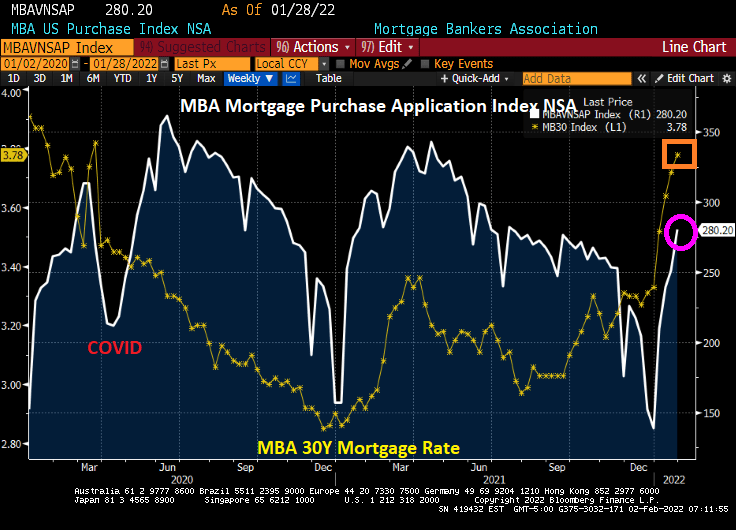

But the housing market is still blistering hot in January 2022. Mortgage Bankers Association (MBA) mortgage purchase applications for the week of 1/21-1/28 were UP 11.63% week-over-week (WoW).

Refinancing applications were up 18.4% WoW as fear of Fed monetary tightening grips the mortgage market.

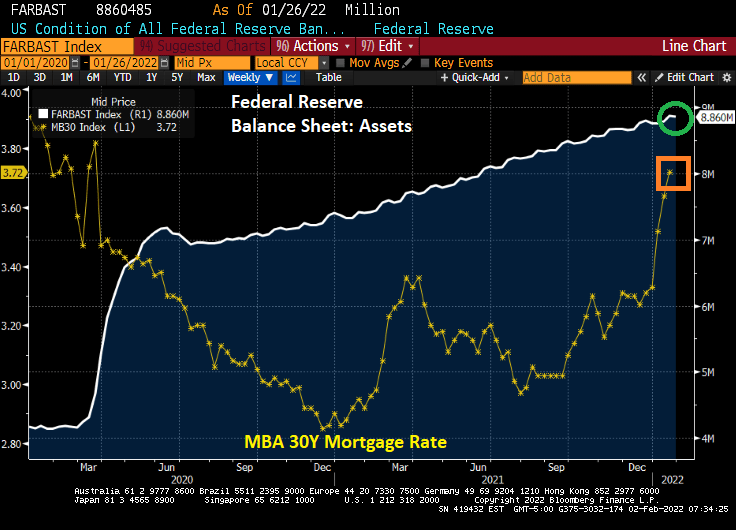

Now, The Fed is expected to raise their target rate 5 times or so over the next year AND slow down asset purchases. Mortgage rates are rising in anticipation of the Fed’s withdrawal of COVID related stimulus.

So, the housing market is expected to slowdown in 2022 as The Fed withdraws its ample monetary stimulus.

(Bloomberg) — The White House is lowering expectations for this week’s U.S. jobs report, saying that brief absences of workers due to omicron could overstate the number of unemployed people for last month.

Several White House officials have teed up Friday’s report with warnings, saying that the week when surveys were taken for the January payroll numbers was the height of illness absences in the aftermath of the holidays.

Brian Deese, the director of President Joe Biden’s National Economic Council, said the numbers could be “confusing” as Covid illnesses are recorded as job losses.

“We expect that that will have an impact on the numbers,” Deese told MSNBC on Tuesday. “We never put too much weight on any individual month; this will particularly be true in this month, because of the likely effect of the short-term absences from omicron.”

Biden has repeatedly touted employment data as an indicator of a robust economic rebound, and highlighted the tumbling jobless rate to blunt criticisms about overheated inflation. Friday’s report may still show historically low unemployment, which is based on a separate survey from the one for payrolls and counts temporary, unpaid sick leave differently.

LaborSecretary Marty Walsh and White House Press Secretary Jen Psaki have also delivered warnings that the official January jobs gain may be poor.

If a worker was out “and did not receive paid leave, they are counted as having lost their job,” Psaki said Monday. Nearly 9 million people missed work due to illness in January, when the data were being collected, she said.

“So we just wanted to kind of prepare, you know, people to understand how the data is taken,” she said. “As a result, the month’s jobs report may show job losses in large part because workers were out sick from omicron.”

Economists expect nonfarm payrolls to rise by 150,000 for January — the weakest reading since the end of 2020. The U.S. unemployment rate is seen remaining unchanged, at 3.9%, according to the median estimate of forecasts compiled by Bloomberg.

So, are Dreese and Psaki saying that US GDP will roar back … from 0.1% … if Omicron fades away? And that all the fiscal and monetary stimulypto are going to cease creating problems??

Despite the fear of Omicron in the upcoming jobs report, there are still 5 rate hikes on the horizon to combat inflation … created by the Biden Administration and Federal Reserve as they combated COVID with massive fiscal and monetary stimulus.

But don’t worry, the Biden Administration ordered rapid test kits from China … and they have arrived!

You must be logged in to post a comment.