I admit, I follow market data to get a signal of what is happening to mortgage rates and I got one. With Putin and Russia invading Ukraine, markets are in turmoil

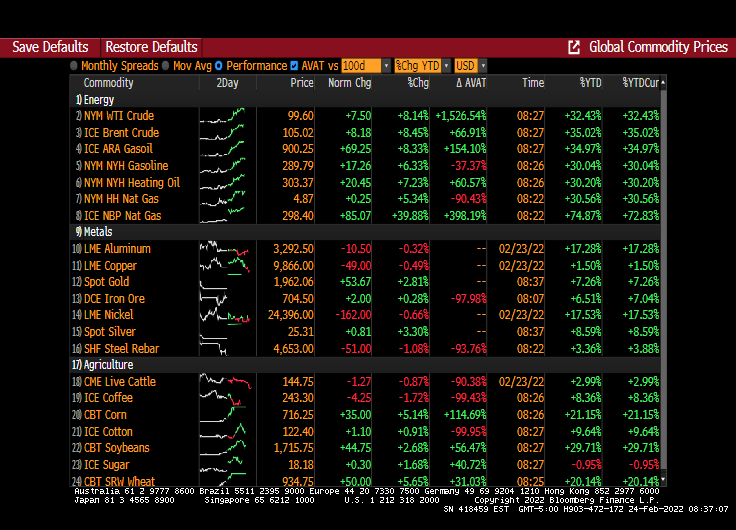

WTI Crude is up 8.14% this morning, Brent Crude is up 8.45% and NBP (UK) Natural gas is up 40%.

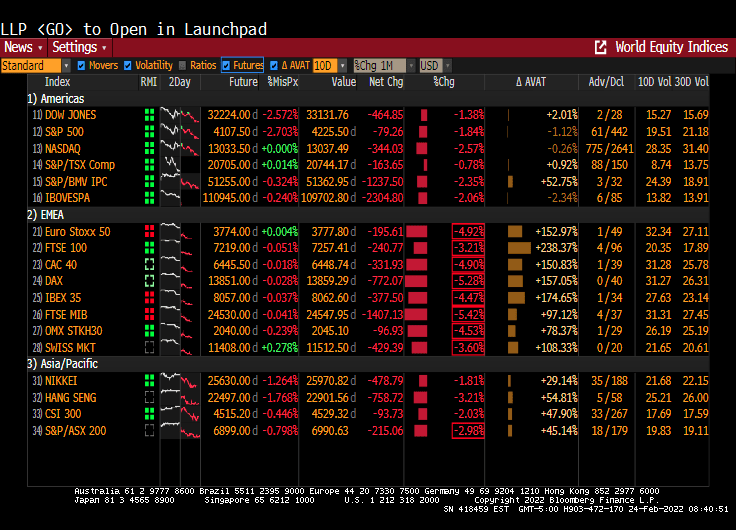

Europe is having a bad day equity market-wise. Eurostoxx 50 was down 4.92%. The US Dow is braced for a 2.5% opening.

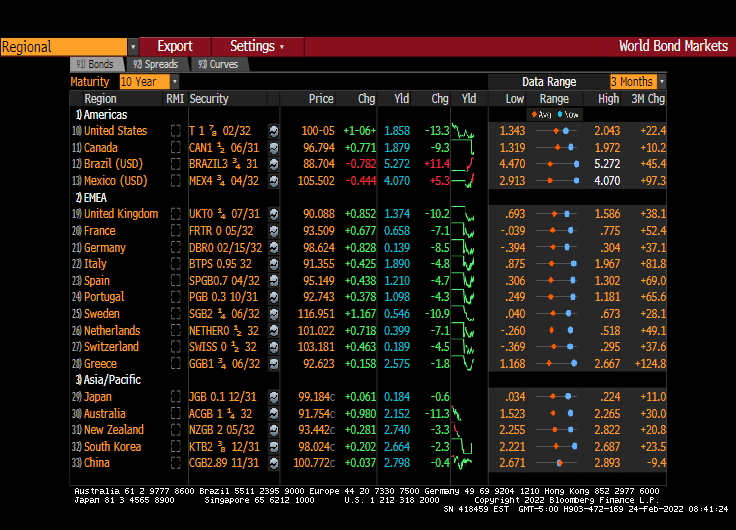

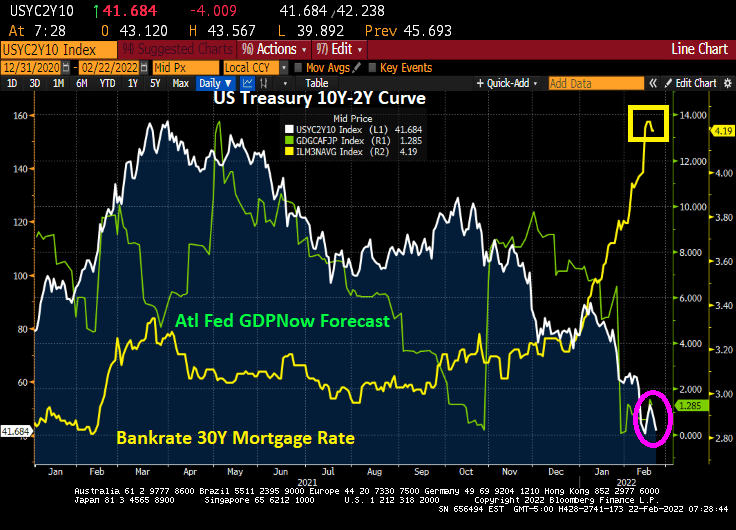

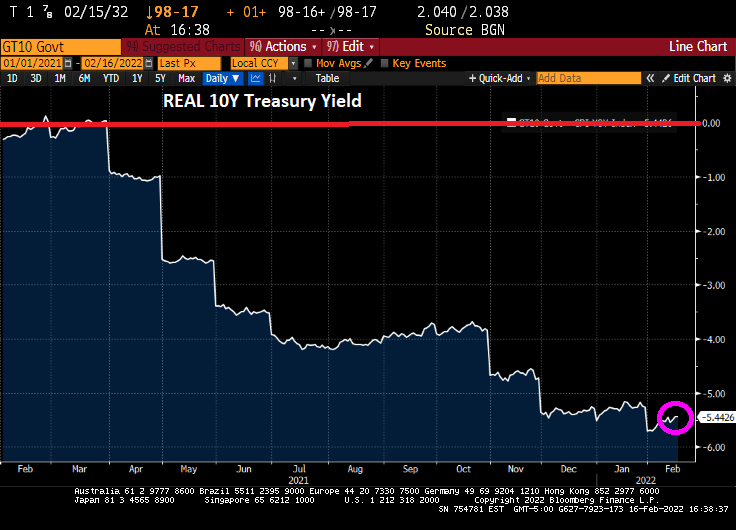

Now to bonds. The 10-year Treasury yield is down 13.3 bps this morning. Sweden and UK are down 10 bps as well.

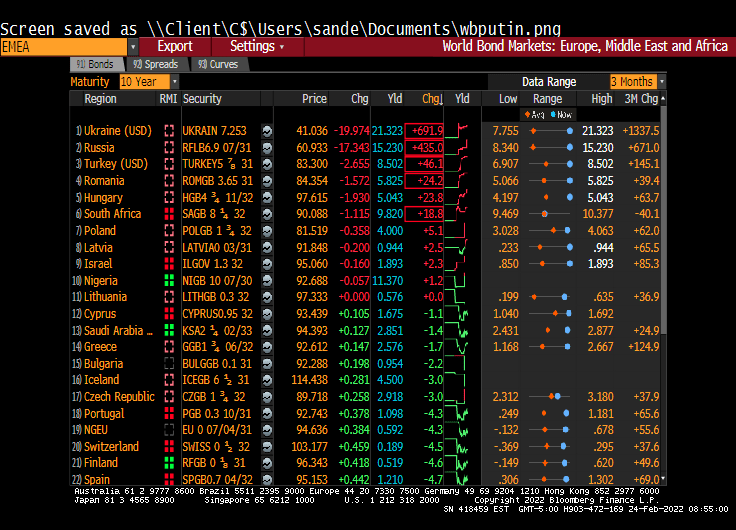

How about the new Russian front? Ukraine’s 10y yield rose 691.0 bps while Russia’s 10Y yield rose 435 bps.

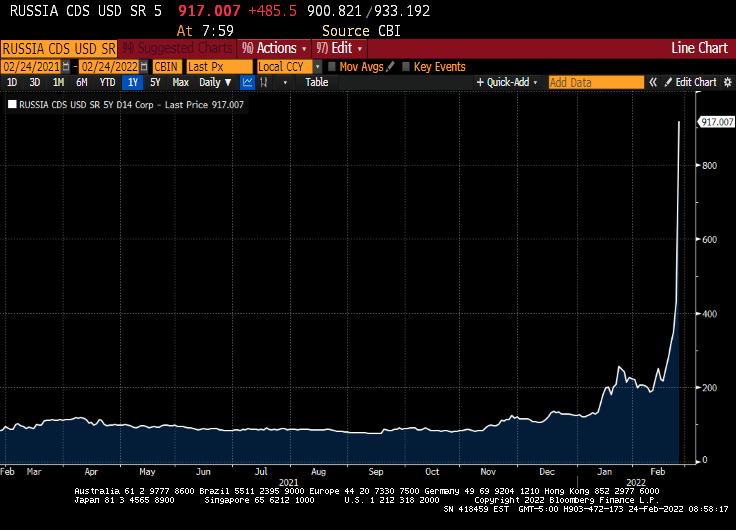

Russian 5Y Credit Default Swaps (CDS) leaped to a Greek-like 917.

Well, it looks like the sanctions imposed by Winken (US VP Harris), Blinken (US Secretary of State) and Nod (US President Biden because he always looks half-asleep) apparently didn’t work as intended.

Putin finally made up his mind.

You must be logged in to post a comment.