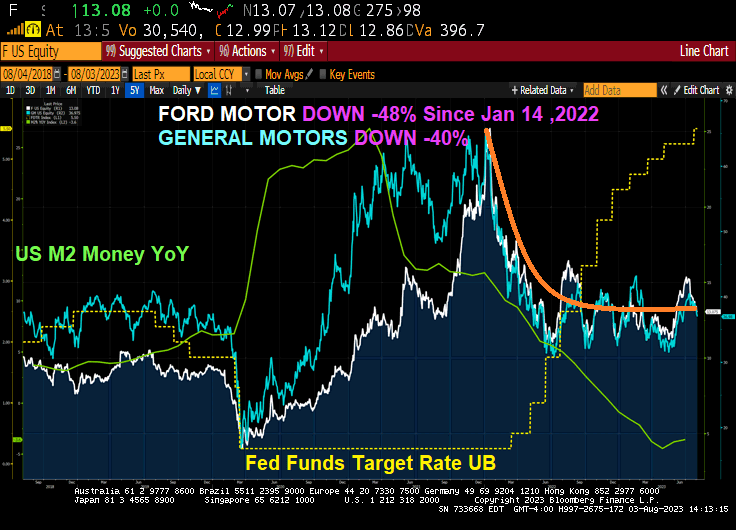

Bidenomics, the term for “Government Gone Wild! in terms of spending and EPA regulations, is a disaster for the US middle class and low wage workers. Even the 1% are now hurting if bought into Biden’s green lunacy. Ford is now down -48% since January 14, 2022 as The Fed started raising rates to fight inflation. GM is down “only” -40%.

So far this year, the division has lost $1.8 billion and this year’s $4.5 billion loss figure blows away last year’s $2.1 billion loss. Ford also announced that its electric F-150 pickup trucks will undergo a price cut, according to Fox.

Ford beat earnings on Thursday and reported adjusted EPS of $0.72, beating expectations of $0.54. It posted revenue of $45 billion and adjusted EBITDA of $3.8 billion, above estimates of $3.15 billion.

The company also raised its guidance, forecasting adjusted EBIT of $11 billion to $12 billion from $9 billion to $11 billion. The company is now guiding for free cash flow of $6.5 billion to $7 billion, from $6 billion.

But reality has sunk in about the company’s comments regarding its EV production schedule and spending plans. Price cuts in the industry, led by Elon Musk and Tesla, have thrown Ford’s production targets into a tailspin and Morgan Stanley noted on Friday morning that “major changes to the EV strategy” could be necessary, according to a wrap up by Bloomberg.

Ford now says it is “throttling back” on plans to ramp up EV production, the wrap up said. It blamed the price war for EVs as part of the cause and told shareholders it would need another year to meet its target of 600,000 EVs produced annually.

Ford CEO Jim Farley said late last week: “The shift to powerful digital experiences and breakthrough EVs is underway and going to be volatile, so being able to guide customers through and adapt to the pace of adoption are big advantages for us. Ford+ is making us more resilient, efficient and profitable, which you can see in Ford Pro’s breakout second-quarter revenue improvement (22%) and EBIT margin (15%).”

CFO John Lawler said yesterday that the company “has ample resources to simultaneously fund disciplined investment in growth and return capital to shareholders – for the latter, targeting 40% to 50% of adjusted free cash flow,” Bloomberg added. He now says Ford is “not providing a date” for producing 2 million EVs per year, which was previously the company’s target for 2026.

Ford’s inability to compete with Tesla was noted earlier this year in a piece titled Tesla ‘Weaponizes’ Price-Cuts To Crush EV Competition.

Is the company pulling an Intel and “kitchen sinking” its guide for the year, or has Elon Musk’s price cuts over at Tesla really put the legacy automaker on the ropes? Ford reports again on October 26, where we’ll get our next glimpse into its continuing operations this year.

Tesla is down -26% since January 14, 2022. And showing a nice turnaround!

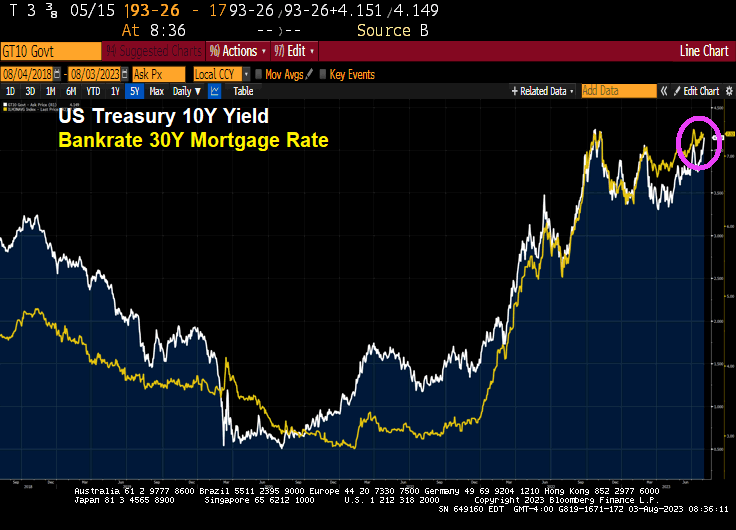

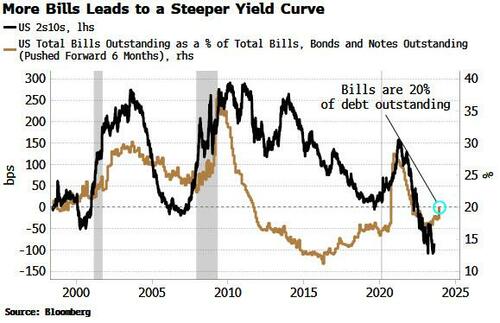

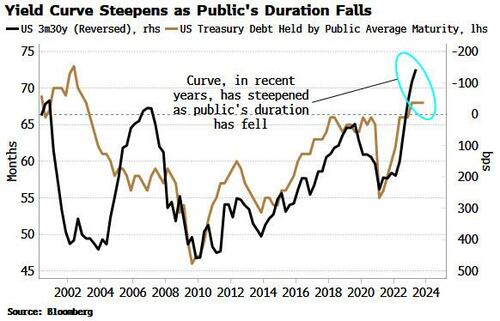

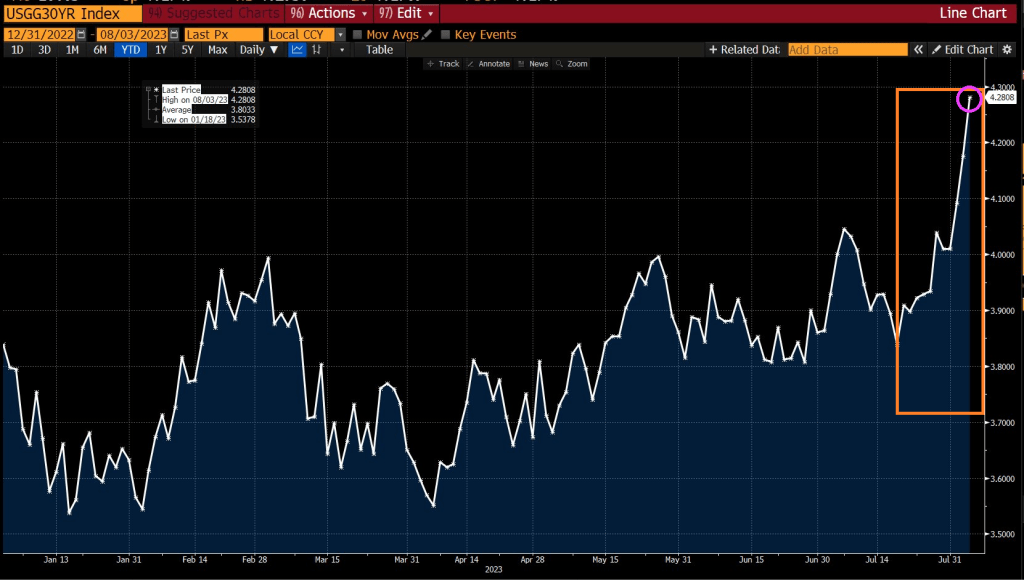

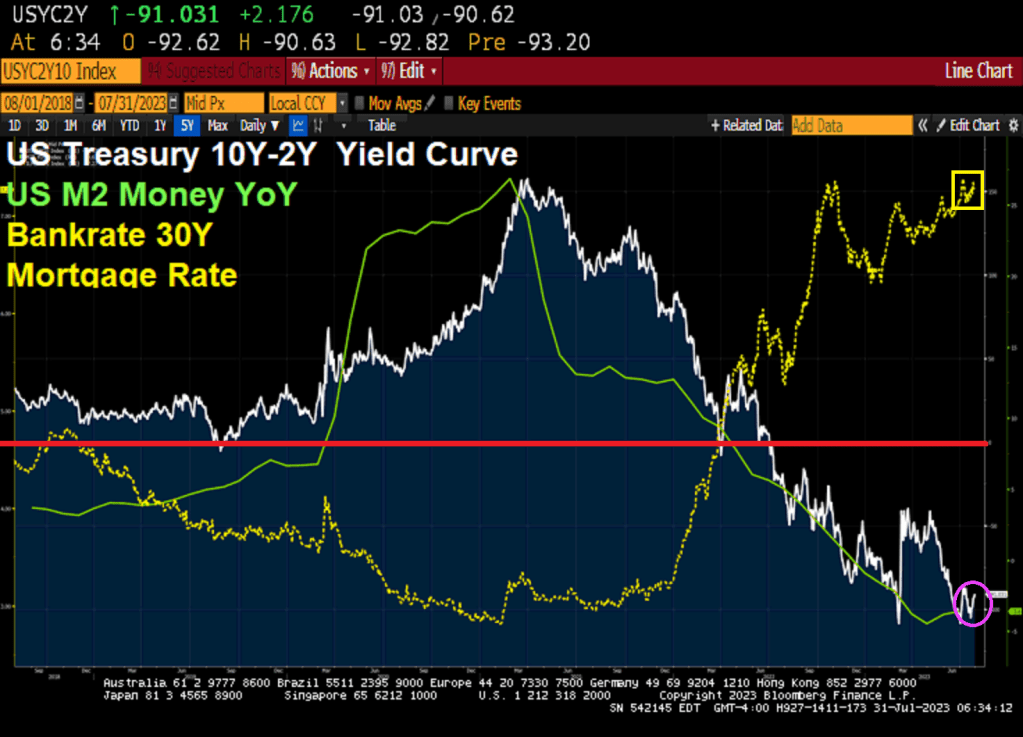

Today, the 10-year Treasury yield is up 11 basis points.

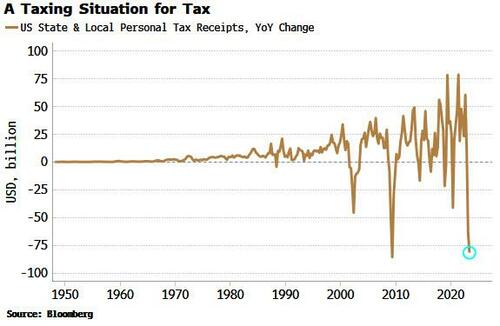

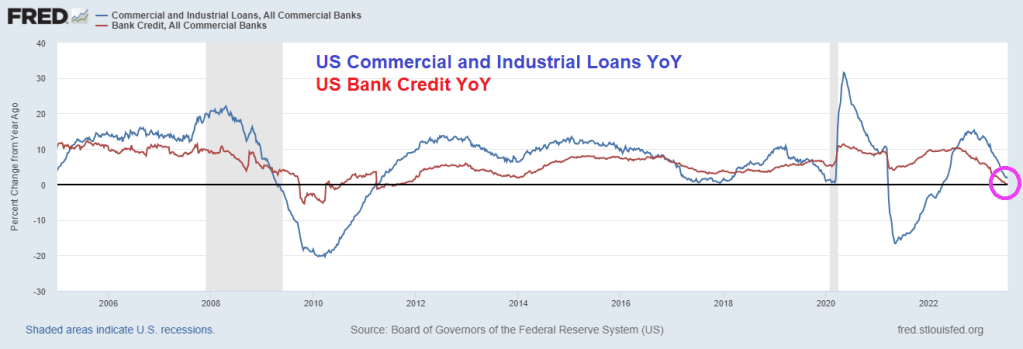

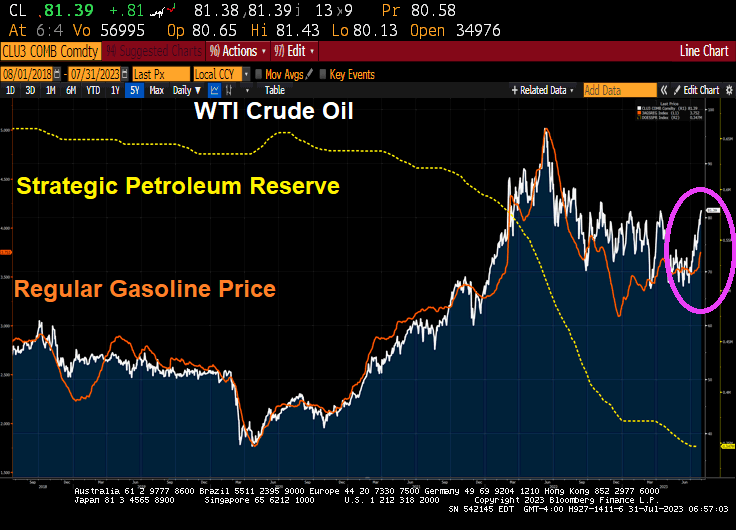

Government Gone Wild!

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.