I admit, I follow market data to get a signal of what is happening to mortgage rates and I got one. With Putin and Russia invading Ukraine, markets are in turmoil

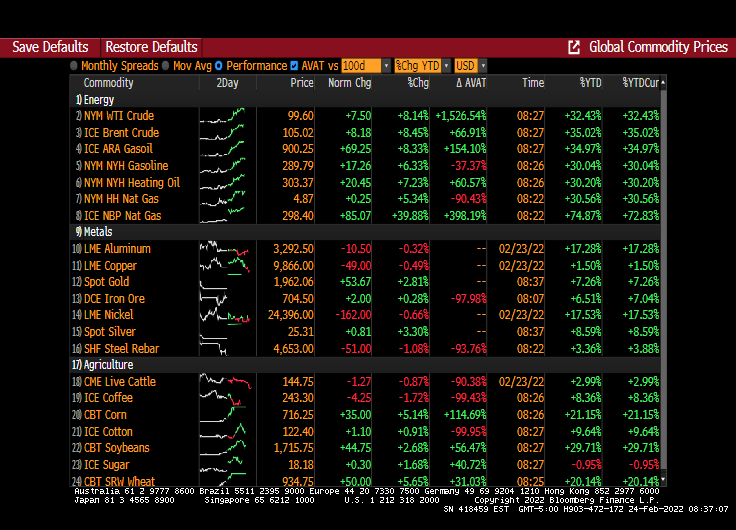

WTI Crude is up 8.14% this morning, Brent Crude is up 8.45% and NBP (UK) Natural gas is up 40%.

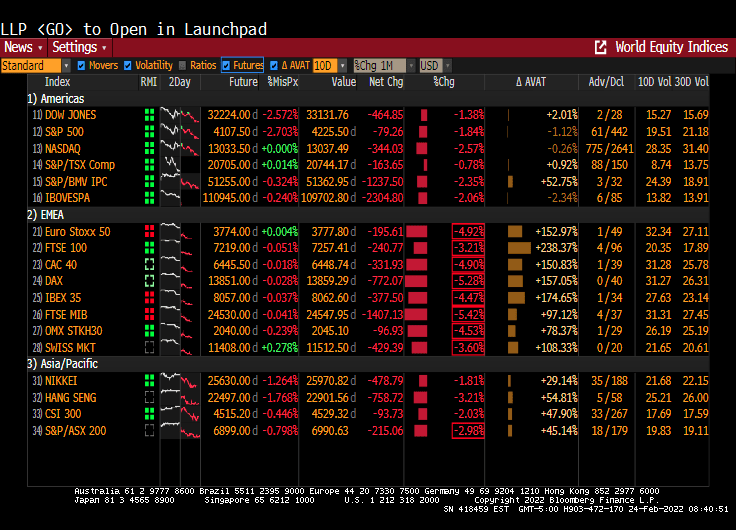

Europe is having a bad day equity market-wise. Eurostoxx 50 was down 4.92%. The US Dow is braced for a 2.5% opening.

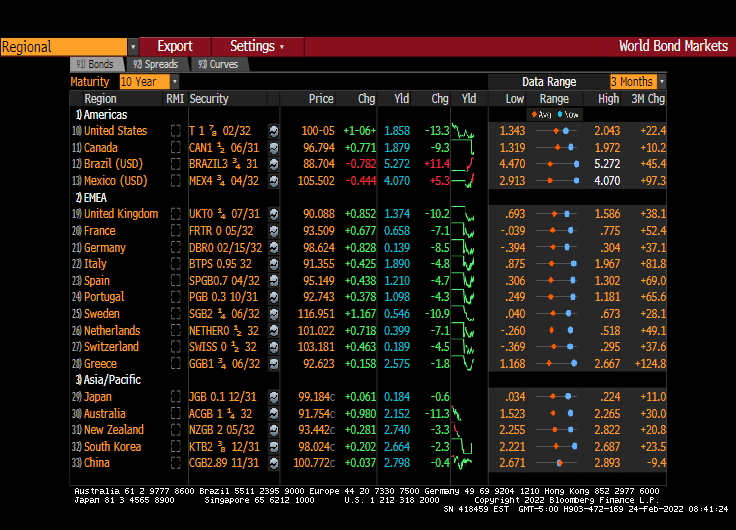

Now to bonds. The 10-year Treasury yield is down 13.3 bps this morning. Sweden and UK are down 10 bps as well.

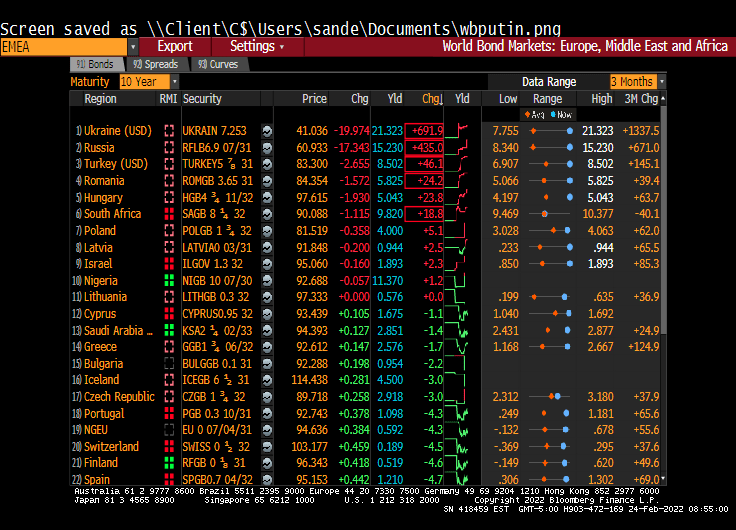

How about the new Russian front? Ukraine’s 10y yield rose 691.0 bps while Russia’s 10Y yield rose 435 bps.

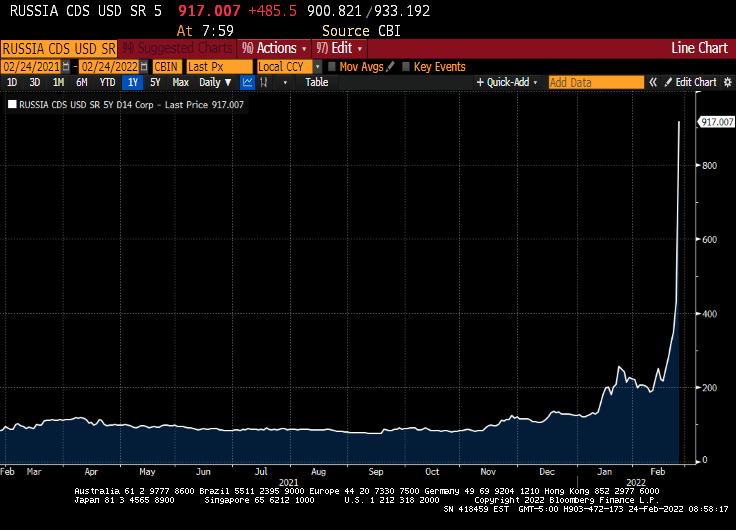

Russian 5Y Credit Default Swaps (CDS) leaped to a Greek-like 917.

Well, it looks like the sanctions imposed by Winken (US VP Harris), Blinken (US Secretary of State) and Nod (US President Biden because he always looks half-asleep) apparently didn’t work as intended.

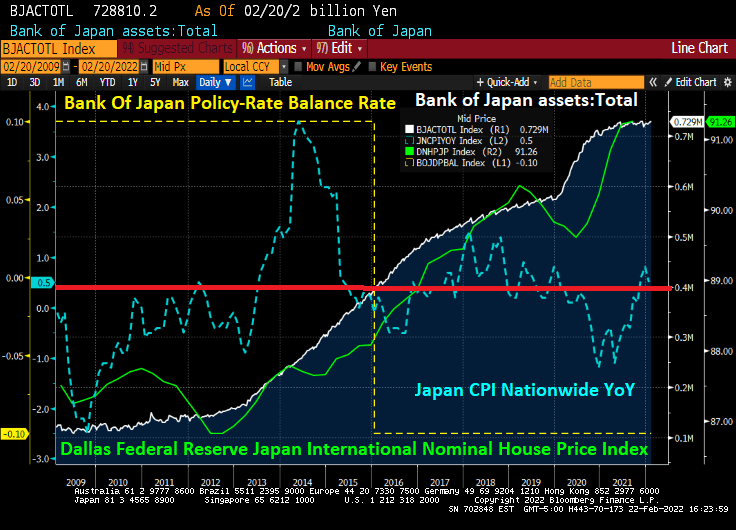

It’s taken nine years and the Bank of Japan supersizing its balance sheet to the $5 trillion mark, but Asia’s second-biggest economy finally has some inflation.

Officials in Tokyo are realizing the hard way, though, that it’s best to be careful what you wish for as bond yields spike.

Granted, the gains in consumer prices Japan is reporting are negligible compared to those in the U.S. and China. And inflation is still a good distance from the BOJ’s 2% target. Still, the 0.5% rise in consumer prices in January year-on-year is already unnerving the bond market. It followed a 0.8% jump in December and marks the fifth straight month of increases.

The worry is that Japan’s inflationis the “bad” kind. Haruhiko Kuroda was hired as BOJ governor in March 2013 to end deflation. Kuroda unleashed tidal waves of liquidity. That drove the yen down 30%, generated record corporate profits and sent Nikkei 225 Average stocks to 31-year highs.

Despite a staggering balance sheet with a -0.10 bps policy rate, Japan has only 0.5% inflation.

And Japan’s yield curve is negative at 3 year tenor and less.

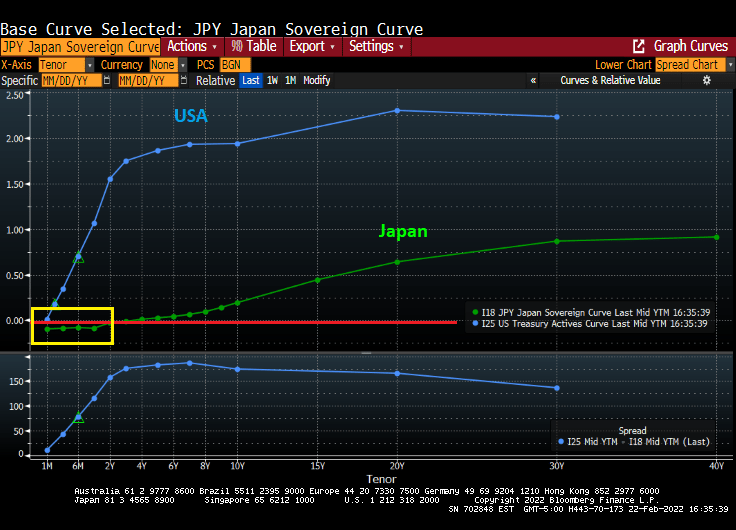

How is it that Japan has virtually no inflation with negative rates but the USA has 7.5% inflation with a 0.25% target rate? Could it be the USA undertook massive fiscal spending related to COVID and reduced energy sources in an effort to go “green” that led to 7.5% inflation??

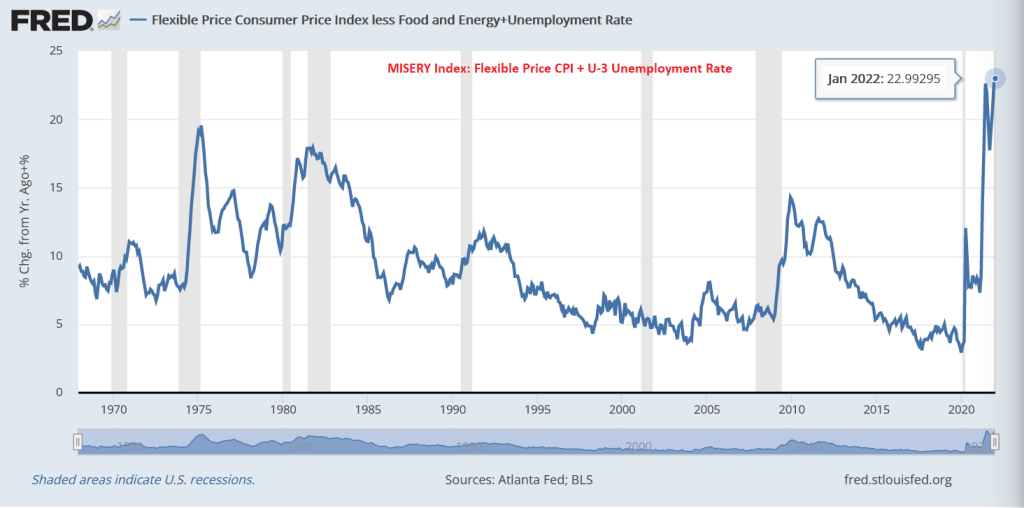

It is truly a miserable time for many Americans as demonstrated by the Misery Index (inflation rate + unemployment rate). But rather than using the CPI YoY measure at 7.5%, I am using the FLEXIBLE CPI YoY to compute the misery index. And is it ever miserable!

In January, the CORE flexible CPI YoY + U-3 unemployment rate hit a modern high at 22.99%. Or at least since 1967.

Like the movie “50 Shades of Gray,” we have 50 shades of inflation. Examples?

How about hardwood? Producer Price Index for hardwood is up 30.8% YoY.

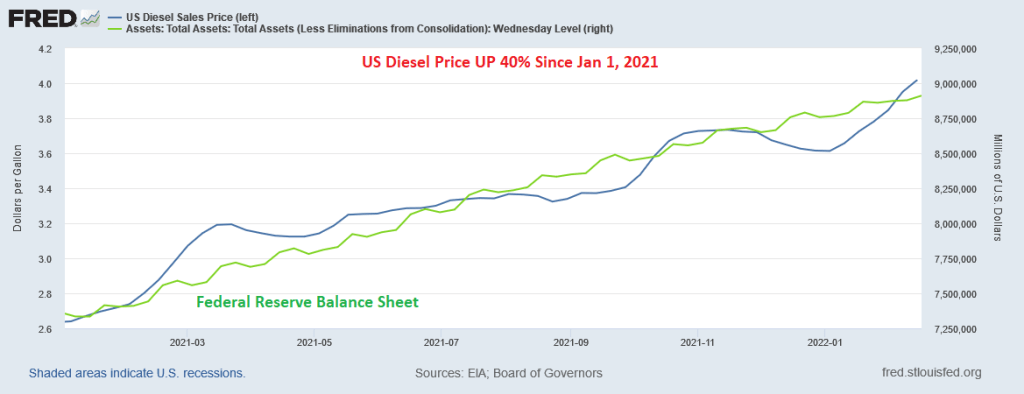

How about diesel fuel prices? They are UP 40% since January 1, 2021.

How about housing? UP 20% YoY according to Zillow’s home value index.

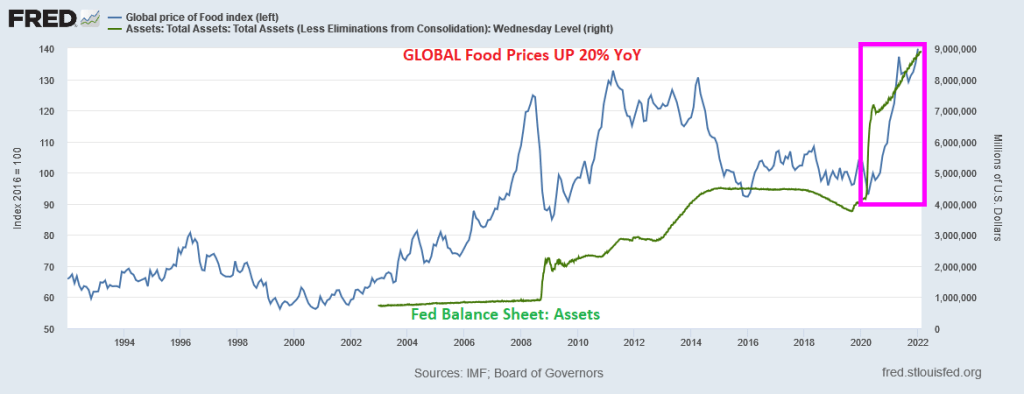

Global food prices? UP 20% YoY.

I could go on and on, but you get the picture. Rising energy, food and construction materials are soaring making many Americans miserable.

But Powell and The Fed have promised to whip inflation. Whip it good … with interest rate increases.

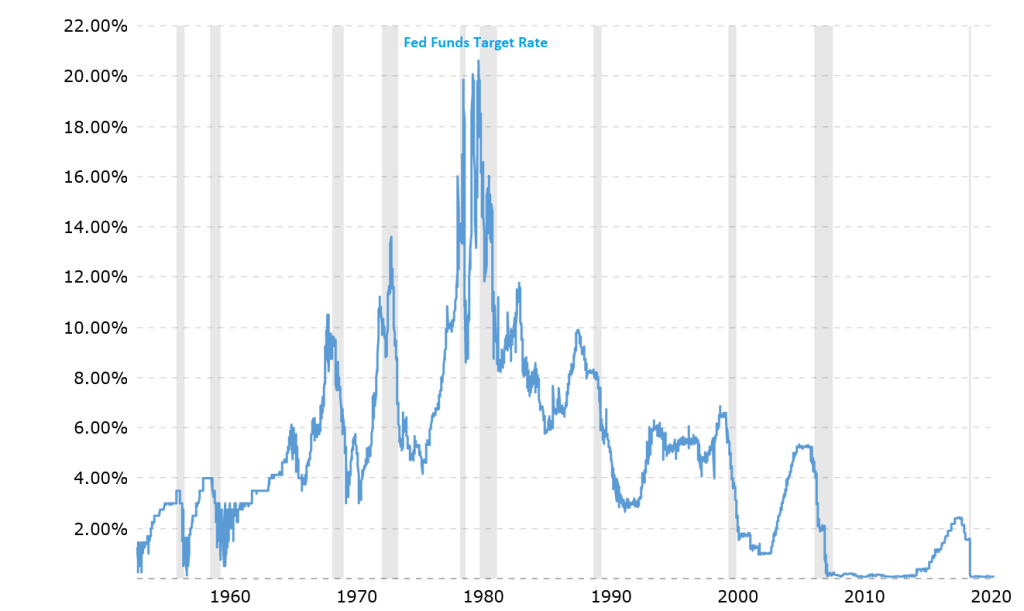

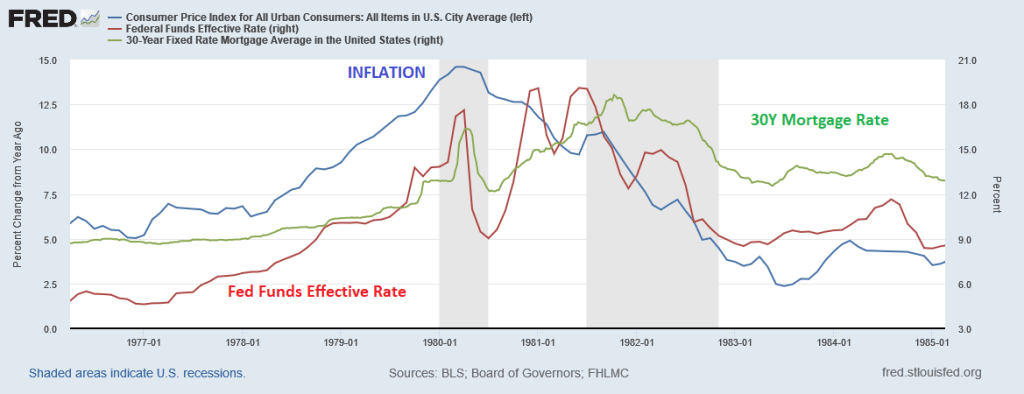

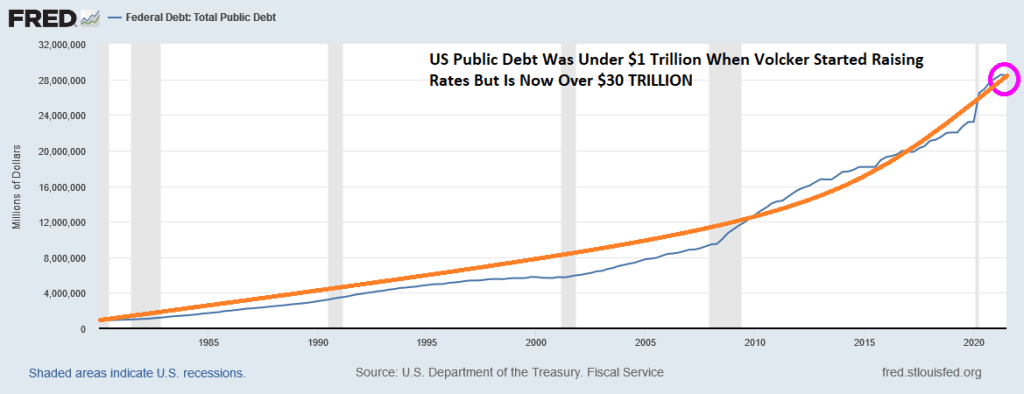

In August 1979, when Paul Volcker became chairman of the Federal Reserve Board, the annual average inflation rate in the United States was 11%. Inflation peaked in 1980 at 14.6%. Volcker raised the federal funds rate from 11.2% in 1979 to 20% in June of 1981.

Inflation (defined as CPI YoY) declined from over 14.6% in 1980 to 3.6% by 1985. But 30-year mortgage rates resumed their upward trajectory and peaking in October 1981 at 18.63 before beginning a gradual decline as inflation was tamed.

But will Powell enact another Volcker moment by raising the target rate abruptly?

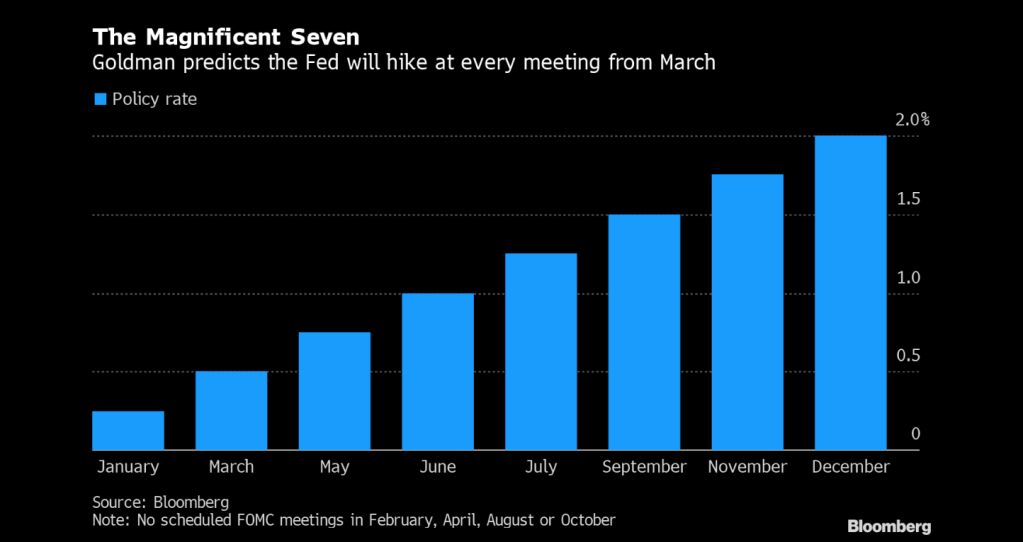

The bank is joining others on Wall Street in ramping up bets for faster policy tightening, after U.S. consumer prices posted the biggest jump since 1982 in January. Goldman Sachs Group Inc. is forecasting seven hikes this year, up from its earlier prediction of five.

“We now look for the Fed to hike 25bp at each of the next nine meetings, with the policy rate approaching a neutral stance by early next year,” the JPMorgan team, led by chief economist Bruce Kasman, said in a research note.

January U.S. inflation readings “surprised materially to the upside,” the economists wrote. “We now no longer see deceleration from last quarter’s near-record pace.”

On inflation, the economists said a “feedback loop” may be taking hold between strong growth, cost pressures, and private sector behavior that will continue even as the intensity of current price pressures in the energy sector eventually fade.

Strong growth? 1.3% is strong growth??

Be that as it may, the US economy is at a different place today than under President Jimmy Carter. When Volcker started raising The Fed Funds Target rate, US public debt was still under $1 trillion. It has ballooned to over $30 trillion today.

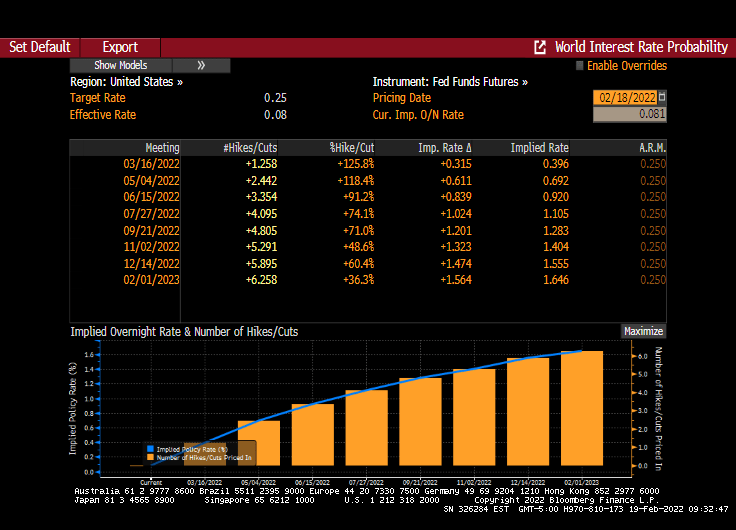

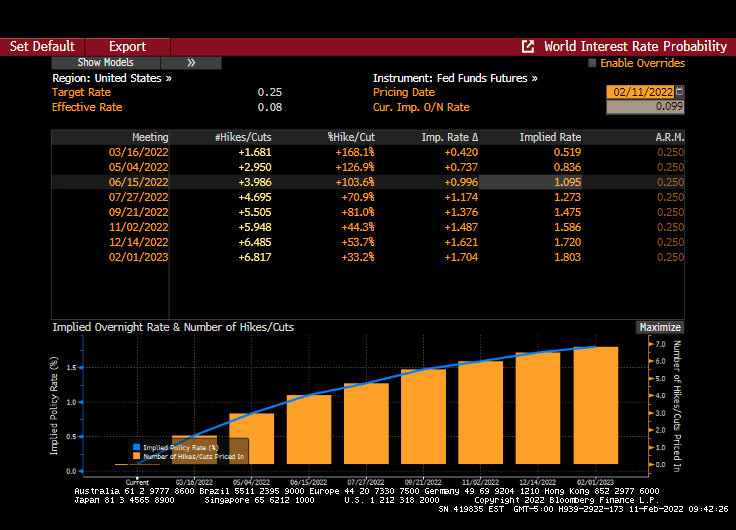

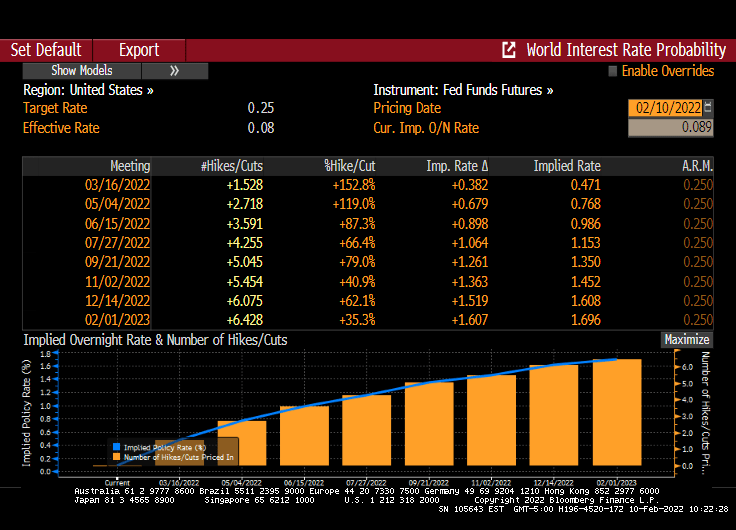

9 rate increases is above what is being priced in The Fed Funds FUTURES market which is 6 rate increases over the coming year.

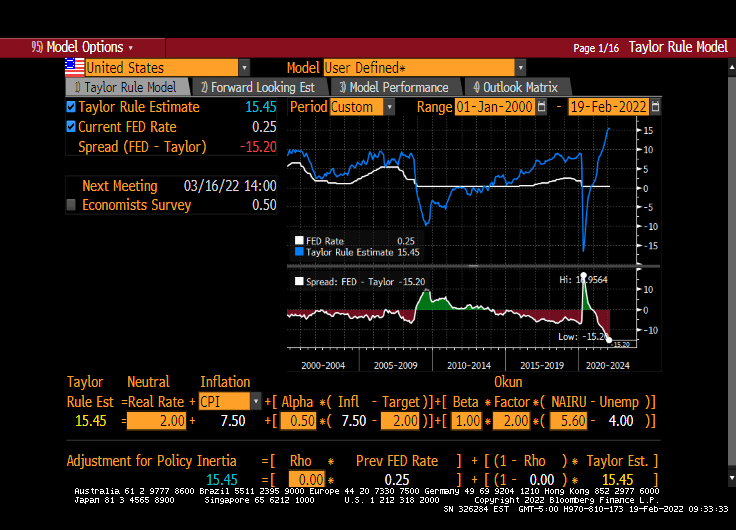

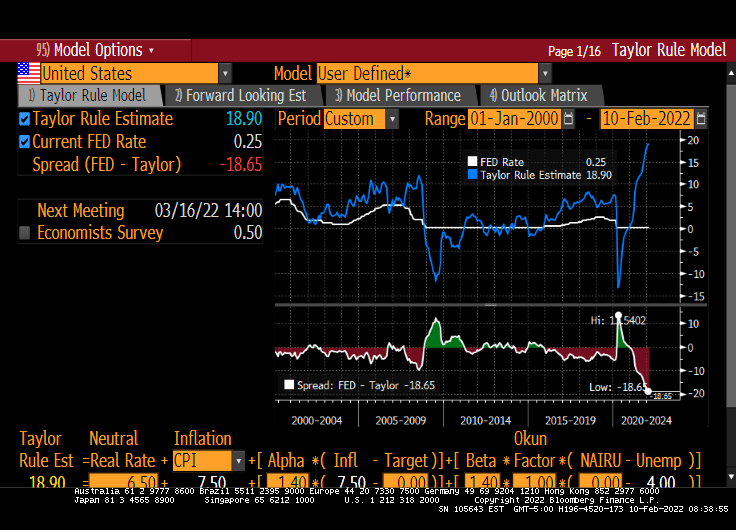

With 7.5% inflation, the Taylor Rule suggests a target rate of 15.45%. Talk about “Shock and Awful!”

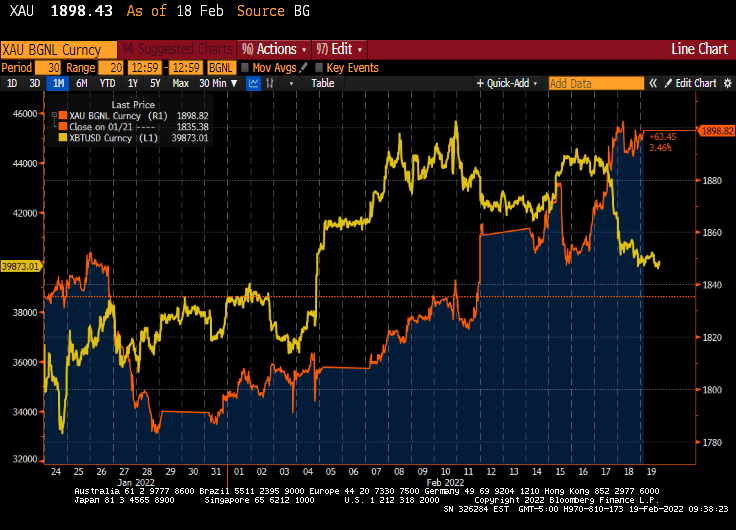

We are starting to see GOLD (gold) surging and Bitcoin (yellow) falling as The Fed prepares “shock and awful” rate hikes and Biden continues to beat the war drums over Russia invading Ukraine.

If The Fed actually raises rates 9 times and dramatically pares back its massive monetary stimulus, it will be “shock and awful.”

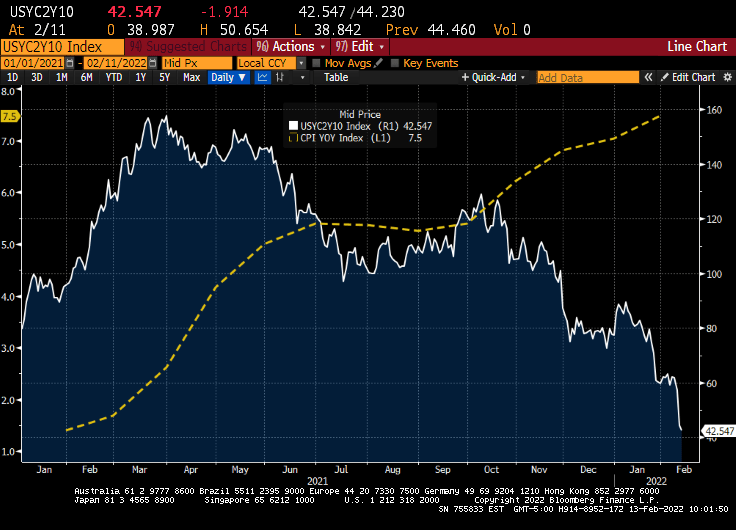

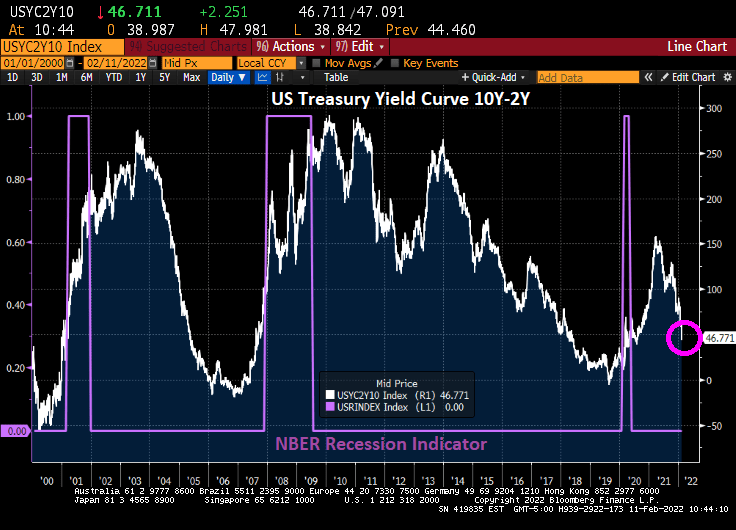

Between raging inflation and the potential wag-the-dog Russian/Ukraine tensions, The Fed has a lot to consider. Particularly if they are watching the 10Y-2Y Treasury yield curve plunging.

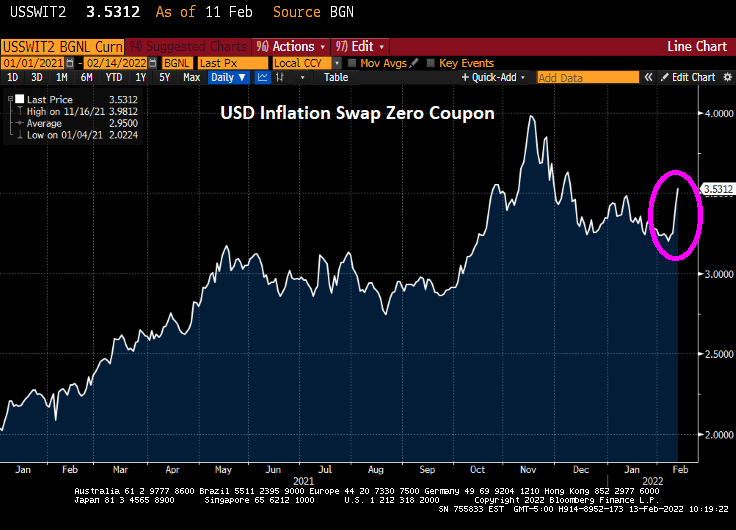

And we have the USD Inflation Swap Zero Coupon rate rising again.

While the Treasury and US Dollar Swaps curve are upward-sloping (not surprising since The Fed has aggressively pushed short-term rates to near zero), we are seeing Treasury Inflation Protected (TIPS) in negative territory until we get to 30 years.

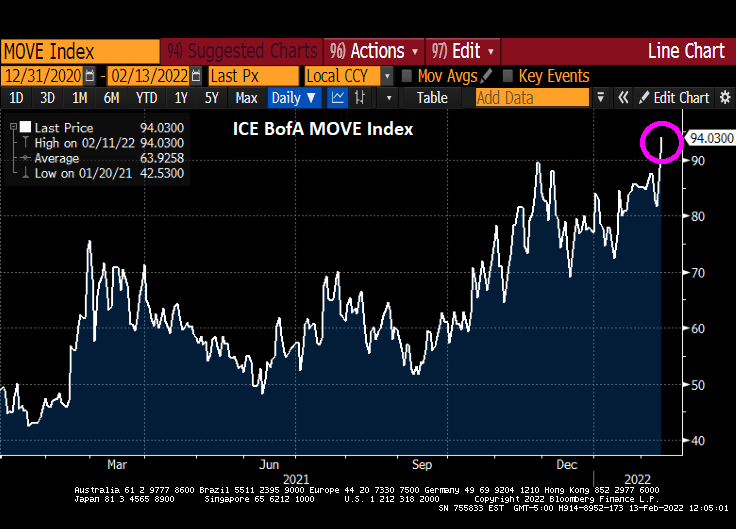

The ICE BofA MOVE volatility index, a yield curve weighted index of the normalized implied volatility on 1-month Treasury options, has more than doubled under Biden.

And with Russian-Ukraine tensions growing, we see WTI crude oil up 96% since Biden took office.

Monday should be an interesting day. The market is now pricing in 6 rate hikes for 2022.

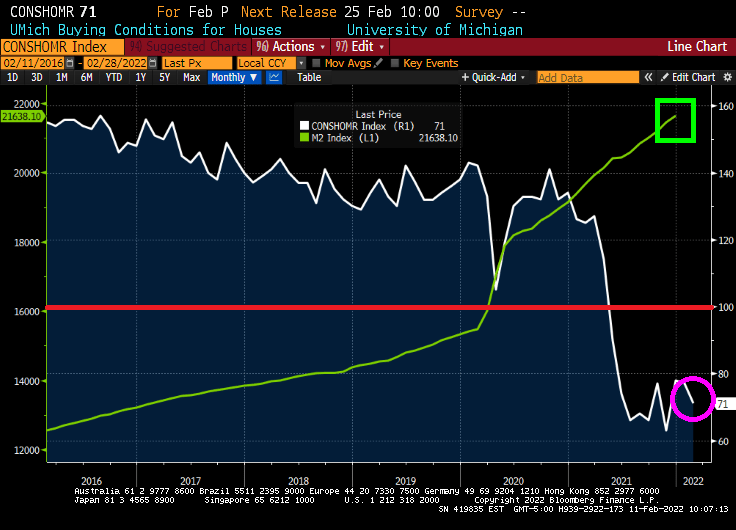

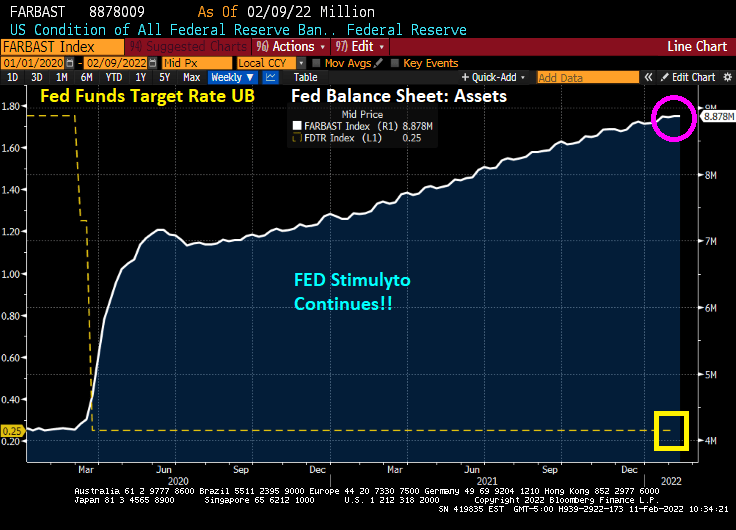

The University of Michigan consumer survey is out for February. And an ugly survey is it! Buying conditions for housing fell to 71 as The Federal Reserve continues it monetary stimulypto!

Despite 7.5% inflation, The Fed continues its “Stimulytpo” monetary policy.

US consumer confidence is the lowest in 10 years as the yield curve crashes.

Here is the POMO schedule just released by The Fed.

I am reminded of my roommate at University of Wyoming who played James Brown over and over and over again. Much like The Fed doing nothing to curb inflation. Until they finally do something with a crashing yield curve.

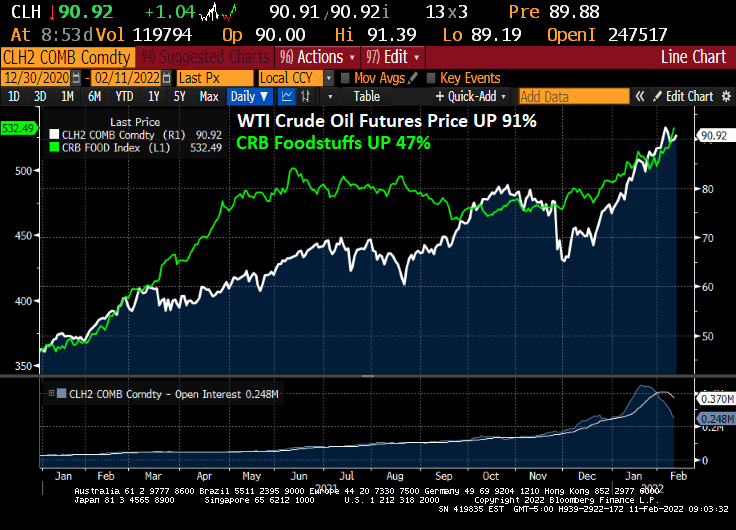

Well, it has been a cringe-worthy year+ under President Biden. West Texas Intermediate Crude futures price is up 91% and the Commodity Research Bureau Foodstuffs index is up 47%. Talk about Biden’s energy folicies being passed through to American households in the form of higher food costs and energy prices!

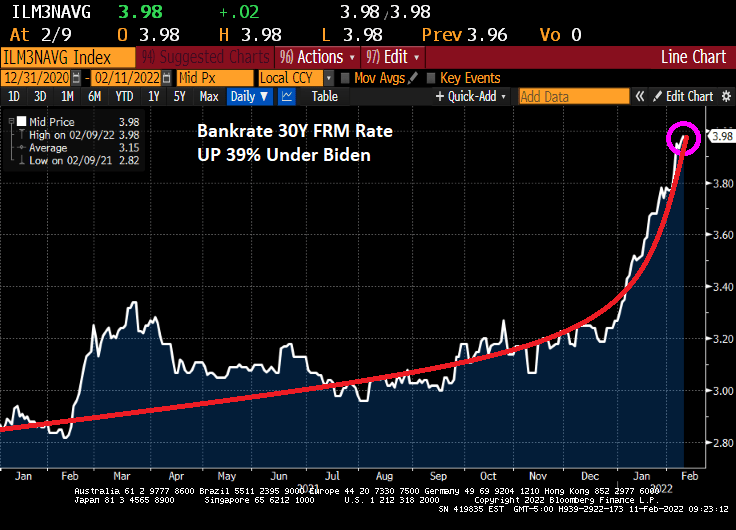

And then we have mortgage rates. Bankrate’s 30Y mortgage rate is up to almost 4%, up 39% since the beginning of 2021.

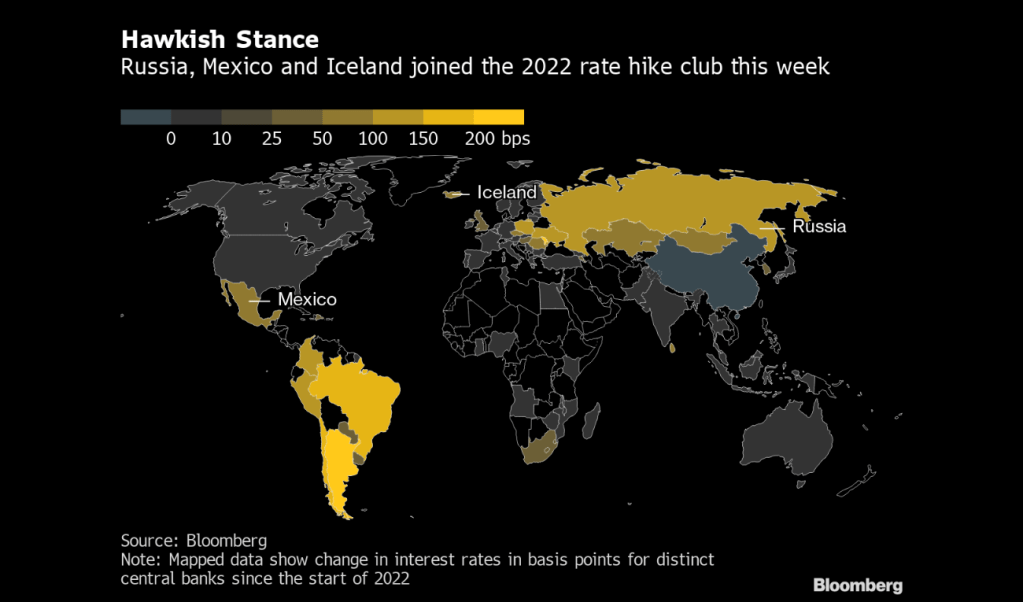

Other central banks are raising rates like banshees on the moor, while The Federal Reserve continues to send conflicting signals about possible March rate hikes.

Goldman Sachs sees 7 rate hikes in 2022, culminating in an eventual 2% rate in December.

Fed Funds Futures are signalling 7 rates increases by the February 1, 2023 meeting.

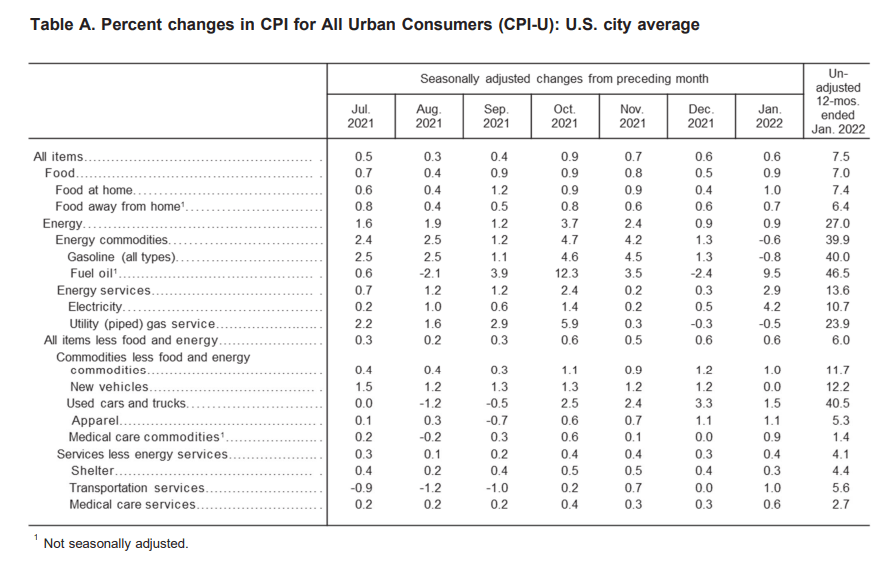

As expected, US inflation surged from 7.0% in December to 7.5% in January.

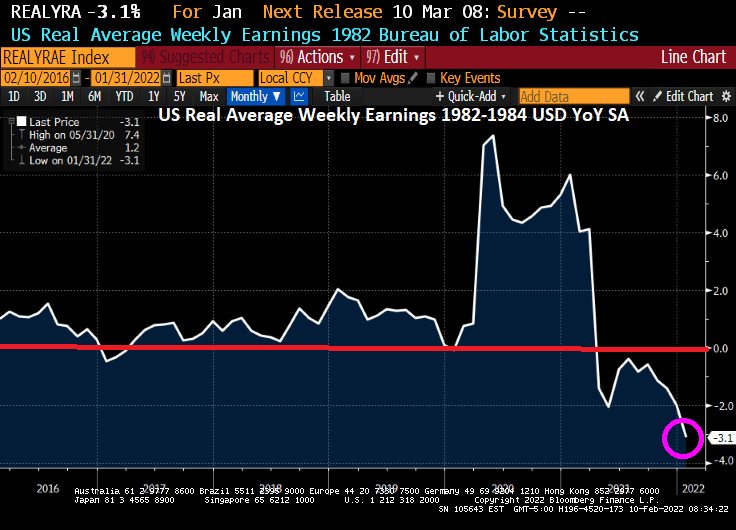

REAL average weekly earnings growth YoY fell to -3.1%.

Energy prices YoY lead the wage (fuel oil UP 46.5% YoY). Used cars and trucks UP 40.5%. At least food is up “only” 7%.

At 7.5% CPI, the Taylor Rule suggests that The Federal Reserve should have their target rate be 18.90%.

At least CORE inflation is “only” 6% YoY.

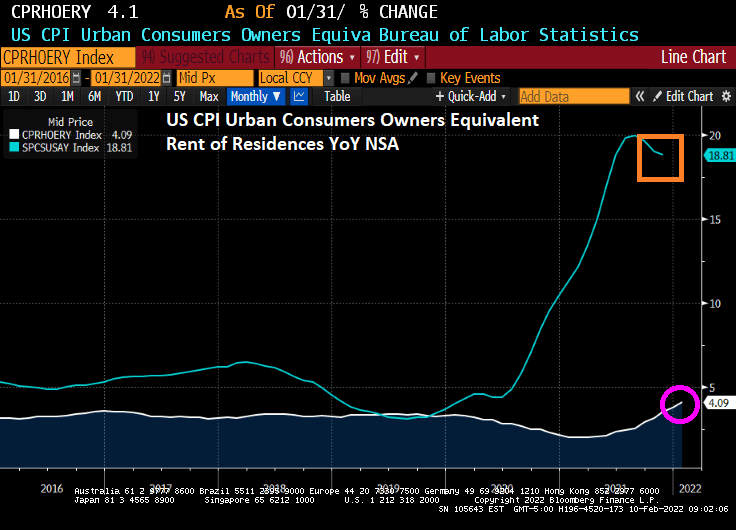

How about rent CPI? The owner’s equivalent rent of residences rose to 4.09% YoY. Seems a little misleading since home prices nationally are growing at 18.81% YoY.

Fed Funds Futures data points to 6-7 rate HIKES over the coming year. BRACE FOR IMPACT!!

Yes, this is Powell’s famous chili recipe if The Fed actually starts to raise rates and pare back the balance sheet stimulus.

Inflation is literally burning a hole though the pockets of Americans. The Flexible Price CPI is raging at 18% YoY. The Dallas Fed has their preferred measure of inflation, the trimmed mean CPI, is growing at only 3.05% YoY. The classic measure of inflation, CPI YoY, is growing at 7.12%.

That is of course if you can find things to buy at the grocery store.

I remember when Fleetwood Mac played at Bill Clinton’s first inauguration party. Perhaps Fleetwood Mac can play at the midterm election party commemorating the rampant inflation under Biden’s “leadership”: Bare Shelves.

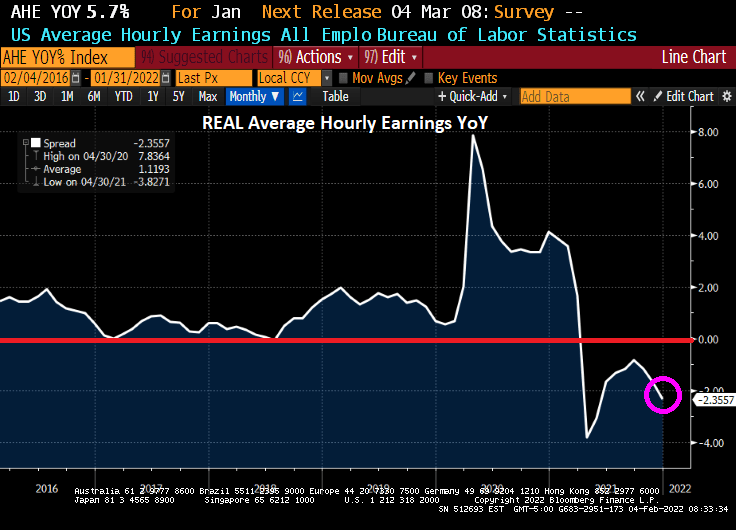

Well, the COVID hysteria from the Biden Administration and the media preparing us for a horrible jobs report was … incorrect. In fact, the January jobs report was “exceptional”. 467,000 jobs were added and average hourly earnings growth ROSE to 5.7% YoY.

The bad news? Thanks to surging inflation, REAL average hourly earnings growth YoY FELL to -2.36%.

Unemployment ROSE to 4.0% from 3.9% as more people dropped out of the labor force in January. On the bright side, labor force participation rate rose to 62.2% from 61.9%.

Leisure and hospitality employment (one of the most vulnerable to inflation) expanded by 151,000 in January, reflecting job gains in food services and drinking places (+108,000) and in the accommodation industry (+23,000).

The reaction in the bond market? US 10-year yields are up 6.9 basis points as Eurozone is up across the board.

Energy prices are up (except natural gas futures).

You must be logged in to post a comment.