Fun week ahead. US inflation numbers are out on Tuesday (forecast? CPI YoY = 7.3%, Core CPI YoY = 6.1%) and The Federal Reserve’s Open Market Committee (FOMC) rate decision is on Wendesday.

So, where are we sitting on Monday?

First, the US Treasury 10Y-2Y yield curve has been inverted (a precursor to recession) for 116 straight days). Second, the likelihood of recession in 2023 is 100%. Third, with the forecast of core inflation at a still numbing 6.1%, The Fed seems dead set on raising their target rate by 50 basis points to 4.50% on Wednesday.

dddd

So, as The Fed debates recession versus fighting inflation (partly caused by The Fed), we have Kevin Malone from The Office debating Angela versus double-fudge brownies:

US producer prices rose in November by more than forecast, driven by services and underscoring the stickiness of inflationary pressures that supports Federal Reserve interest-rate increases into 2023.

The producer price index for final demand climbed 0.3% for a third month and was up 7.4% from a year earlier, Labor Department data showed Friday. The monthly gains for October and September were revised higher.

At the same time, the annual increase was the smallest in 18 months, extending a months-long easing and suggesting the central bank still has scope to pause its rate hikes next year as expected. Cooler demand at home and abroad has taken some stress off supply chains.

The data come just days before the release of the closely watched consumer price index, which is forecast to show inflation, while much too high, continues to decelerate.

While PPI is declining, it is still far above The Fed’s inflation rate of 2% (red line).

Watch out for energy prices when the sleeping giant (China) opens up again and demand for energy skyrockets. Meanwhile, Clueless Joe is merrily draining the US Strategic Petroleun Reserve.

Lastly, congratulations to former Cleveland Brown QB Baker Mayfield for winning with the LA Rams against the Las Vegas Raiders with a stunning 99 yard drive for a TD at the end of the game.

During the Covid crisis of 2020 (red box). consumer credit declined and households were saving. But following the end of US Covid economic shutdowns, we saw inflation soaring to 40-year highs as Biden declared war on fossil fuels and a Pelsoi-led Congress went on an epic spending spree. But with soaring inflation, came a decline in personal savings and soaring consumer credit outstanding in an attempt to cope with Bidenflation.

Meanwhile, in the crypto universe, CNBC’s Jim Cramer and ARK’s Cathie Wood are going big for cryptos. With Wood buying Bitcoin and Cramer touting Coinbase.

Hmmm.

But at least Litecoin and the others are up today. Likely because Cramer and Wood are touting cryptos with “buy the dip!” strategy.

And on the Sam Bankman-Fried fiasco front, I am watching the deflection of wrongdoing from SBF to his girlfriend and now the co-CEO of Alameda Research, Sam Trabucco.

Bloomberg: He has a degree from MIT and cut his teeth as a trader at Susquehanna International Group. Yet the former co-head of Alameda Research made it clear that poker and black-jack tables were where he honed the gambler’s instincts he applied to cryptocurrency trading.

“I may or may not be banned from 3 casinos for this,” Sam Trabucco once tweeted about counting cards at black jack tables.

The next Federal Reserve Open Market Committee (FOMC) meeting in on Wednesday, November 2nd. Let’s see what The Fed does with its BIG GREEN BAG … OF MONEY.

As I set here on Sunday morning waiting to see how the Cleveland Browns will lose to cross-state rival Cincinnati Bengals, I see that both the US Treasury 10yr-2yr and 10yr-3mo yield curves are inverted (below zero).

Core inflation (CPI less food and energy) YoY (blue line) was only 1.3% in February 2021 shortly after Biden was sworn-in as President and is now 6.6% in September 2022. That is over a 400% increase in core inflation!

We have this tantalizing headline on Bloomberg:

Goldman Sachs Now Sees Fed Rates Peaking at 5% in March By Simon Kennedy(Bloomberg) —

Goldman Sachs Group Inc. economists said they now expect the US Federal Reserve to raise interest rates to 5%, higher than previously predicted.

The central bank will lift its benchmark rate to a range of 4.75% to 5% in March, 25 basis points more than earlier expected, economists led by Jan Hatzius wrote in an Oct. 29 research report.

The route to the new peak includes increases of 75 basis points this week, 50 basis points in December and 25 basis points in February and March, they said.

The economists cited three reasons for expecting the Fed to hike beyond February: “uncomfortably high” inflation, the need to cool the economy as fiscal tightening ends and price-adjusted incomes climb, and to avoid a premature easing of financial conditions.

Well, not exactly earth-shattering. Fed Funds Futures data point to a peak of near 5% (4.905%) for the May 2023 FOMC meeting, so Goldman Sachs is calling for an earliest peak at the March 2023 FOMC meeting,

Regardless of what Goldman Sachs thinks, Fed officials are expecting a peak in 2023 followed by a decline to 2.5%.

Brainard and Bostic are the only “doves.” Which is silly because Chicago’s Evans is a perma-dove. Let’s see how the Dots Plot changes at the November 2nd meeting.

America’s distressed debt pile is biggest since September 2020.

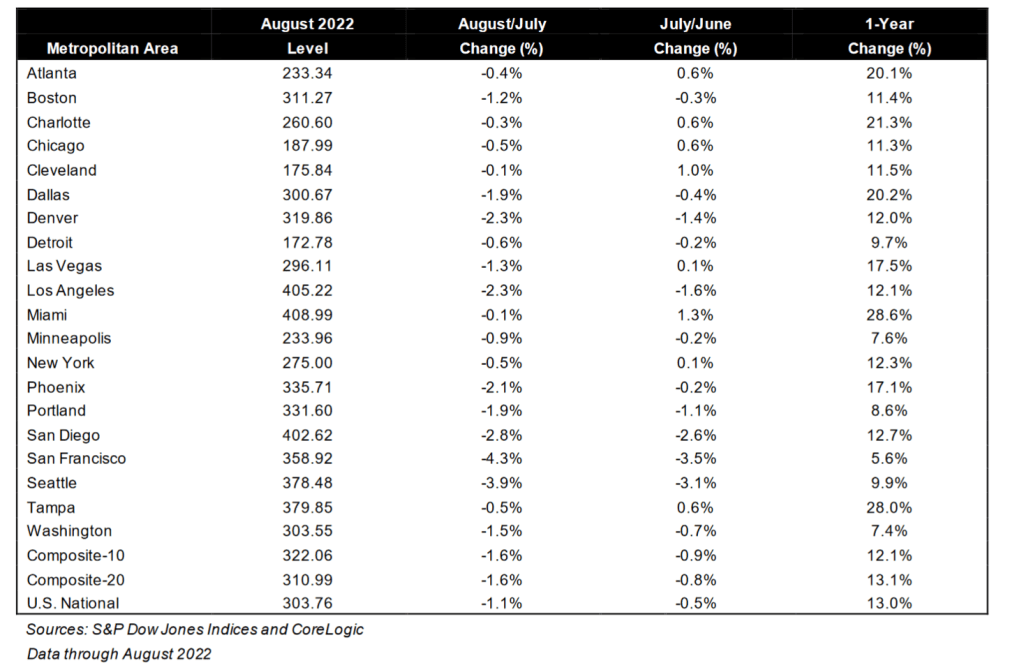

Alarm! US home prices are decelerating as inflation rages and The Fed tightens.

Home price growth in the US slowed the most on record as a doubling of borrowing costs (thanks to the US Federal Reserve) has sapped demand.

A national measure of prices increased 13% in August from a year earlier, but is down from 20.79% in March, the S&P CoreLogic Case-Shiller index showed Tuesday. That’s the biggest deceleration in the index’s history.

The housing market has started to slump as the Federal Reserve hikes interest rates to curb the hottest inflation in decades. Even with the deceleration, prices remain high compared to last year. Coupled with mortgage rates that are edging closer to 7%, many would-be buyers have been shut out, while some sellers have retreated.

While 13% growth sounds good, it is not good for renters looking to buy a home.

According to S&P/CoreLogic/Case-Shiller, Southern (red) cities Atlanta, Charlotte, Dallas, Miami and Tampa all still grew at over 20% YoY. Other cities like blue cities Detroit, Minneapolis, Portland, San Francisco, Seattle and Washington DC are grew at UNDER 10% YoY.

On related news, I always said in my classes that +/- 10 basis point in the US Treasury yield is a big deal. This morning, the US Treasury 10-year yield is DOWN -16.1 bps. In fact, the 10-year yields are down across the board globally.

25 days later. A real-life horror created by The Federal government.

Yes, according to the US Department of Energy, the US has only 25 days of diesel supply left.

The diesel crunch comes just weeks ahead of the midterm elections and has the potential to drive up prices for consumers who already view inflation and the economy as a top voting issue. Retail prices have been steadily climbing for more than two weeks. At $5.324 a gallon, they’re 50% higher than this time last year, according to AAA data.

Notably, National Economic Council Director Brian Deese recently commented on the emerging crisis. Deese said diesel inventories are “unacceptably low” and added that “all options are on the table.”

Yesh, diesel fuels prices are surging again as diesel inventory is shockingly low.

At least the US gets to live out a horror story created by The Federal government because failed Presidential candidate Al “The Snore” Gore and a teenage Swedish girl (Greta Thunberg) told Biden and Democrats to hate fossil fuels.

How dare you … drive inflation through the roof because of your green energy lunacy.

Like virtually everything in Biden’s economy, the price of turkey (often the main staple for Thanksgiving dinner) is way up in price. Turkey prices are UP 73% since last year. The price per pound of an 8- to 16-pound turkey has risen to $1.99, a 73% increase from $1.15 last year, according to USDA data.

Speaking of turkeys, in recent speeches, President Joe Biden has been misleadingly taking credit for cutting federal deficits by historic amounts, though most of the reduction in deficits is the result of expiring emergency pandemic spending. Deficits fell between fiscal year 2020 and 2021 far less than initially projected after Biden added to them with more emergency pandemic and infrastructure spending.

And apparently Biden (or Jill) haven’t looked at the data recently. While there was a momentary budget surplus in April 2022, the Federal budget deficit has increased dramatically in September 2022 to the worst deficit since March 2021 shortly after Biden took office.

The only thing that is strong under Biden is the labor market. But even the accomplishment is grossly misleading. Under Trump, the U-3 unemployment rate was 3.5% in February 2020 just before Covid-13 struck and the Fauci-ites shut down the economy causing unemployment to rise to 14.7% in April 2020. Most of the reduction in the unemployment rate was the result of the economy slowly opening back up under Trump. When Biden took over, the unemployment rate was 6.4% and it is finally back to Trump’s 3.5% in September 2022. At least Biden didn’t screw that up, as Obama has said. Perhaps that should be his new midterm campaign slogan!

But Biden DID screw up the labor market with Bidenflation. REAL average hourly earnings growth (yellow line) is NEGATIVE..

And yes, the US is rapidly approaching recession which will result in a spike in unemployment. So much for Biden’s “Strong as hell!” economy.

Today’s existing home sales were … gruesome. While EHS month-over-month were down only -1.5%, on a year-over-year basis EHS was down a staggering -23.79%.

If you look at the declining growth rate of M2 Money (green line) and rising mortgage rates (yellow line), we can see why the housing market is struggling.

How about median price? That dropped to 8.07% YoY as inventory for sale remains lower than before Covid and Covid stimulypto.

To begin with, headline inflation remains high at 8.2% YoY while CORE inflation (headline less food and energy) rose to 6.6% YoY.

Meanwhile, REAL average weekly earnings growth YoY further declined to -3.8% YoY.

On the bond front, the Bank of America ICE bond volatility index rose to Great Recession/banking crisis levels (also achieved during the Covid government shutdowns).

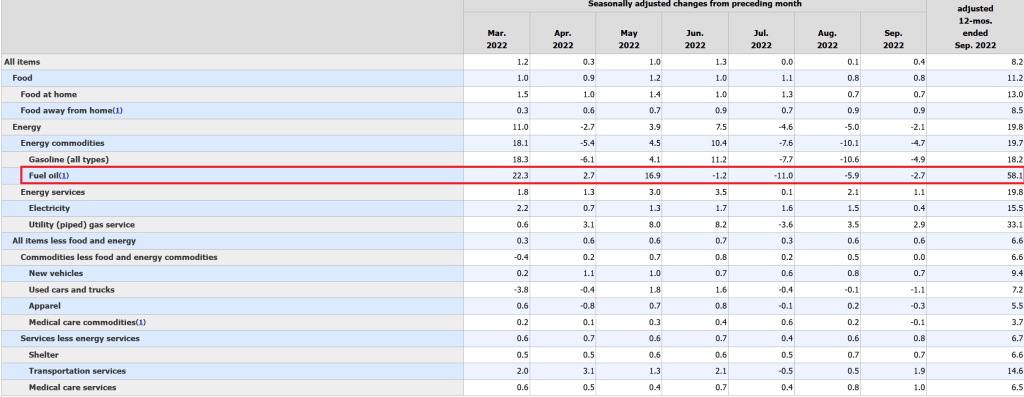

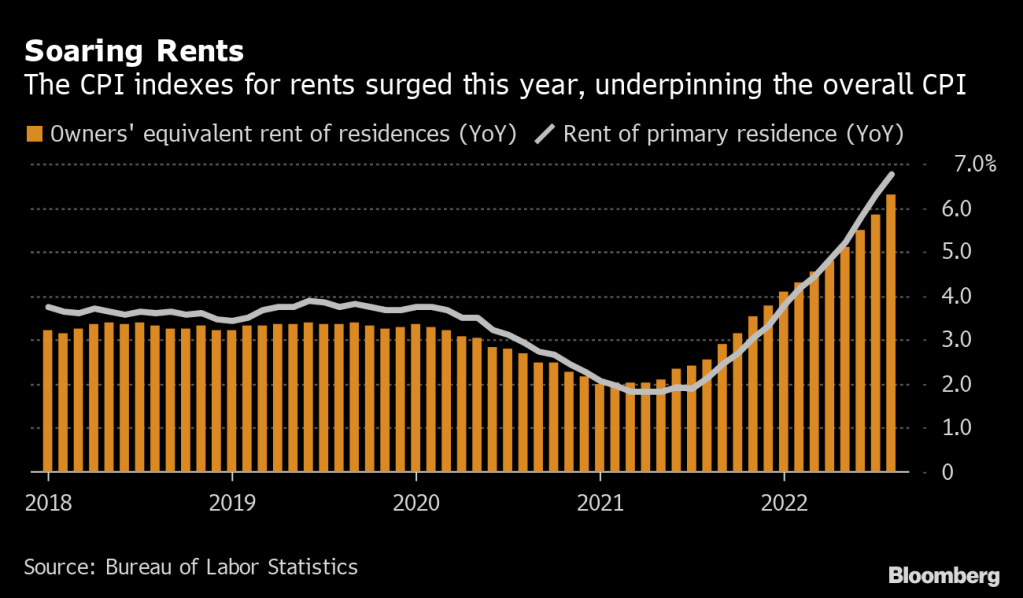

But back to the low-ball BLS inflation data. The biggest gain in price is … fuel oil at 33.1% YoY. Food at home rose 13.0% while gasoline rose 18.2%. Rent, according to the BLS, rose 6.6%.

Biden has probably been told by Ron Klain and Susan Rice that this is a good report.

The US Producer Price Index (Final Demand) printed at a higher than expected 8.5% YoY, throwing cold water on the notion that inflation is “transitory.”

A key US inflation measure due Thursday is set to return to a four-decade high, underscoring broad and elevated price pressures that are pushing the Federal Reserve toward yet another large interest-rate hike next month.

The so-called core consumer price index that excludes food and energy is projected to rise 0.4% in September from the prior month and 6.5% from a year earlier, matching the rate seen in March that was the highest since 1982.

The overall CPI, however, is expected to decelerate to a still-rapid 8.1% annual pace, restrained by a decline in gasoline prices, based on the median estimate.

You must be logged in to post a comment.