The CPI news on Friday was so awful that it changed the bond market’s view of Fed trajectory, and the weakest sector broke. In bond jargon, MBS went “no-bid.”No buyers for MBS. Then a few posted prices beyond borrower demand, not wanting to buy except at penalty prices. (Courtesy of Cherry Creek Mortgage)

Despite what Treasury Secretary Janet Yellen has said, Friday’s inflation report demonstrated that inflation is no longer transitory. And with that realization, there was a dearth of bidders for Agency Mortgage-backed Securities (Agency MBS) on Friday.

As a result, agency MBS 2.5% dropped to under $90 as markets expect The Fed to keep raising rates to combat inflation.

Duration of the FNCL 2.5% agency MBS has been extending with growing inflation. Duration was under 1 on August 2, 2021 but is now 7 times greater at almost 7.

Note to Yellen: inflation seems be permanent, not transitory. Or at least inflation will remain high for the foreseeable future, crushing the life out of Agency MBS.

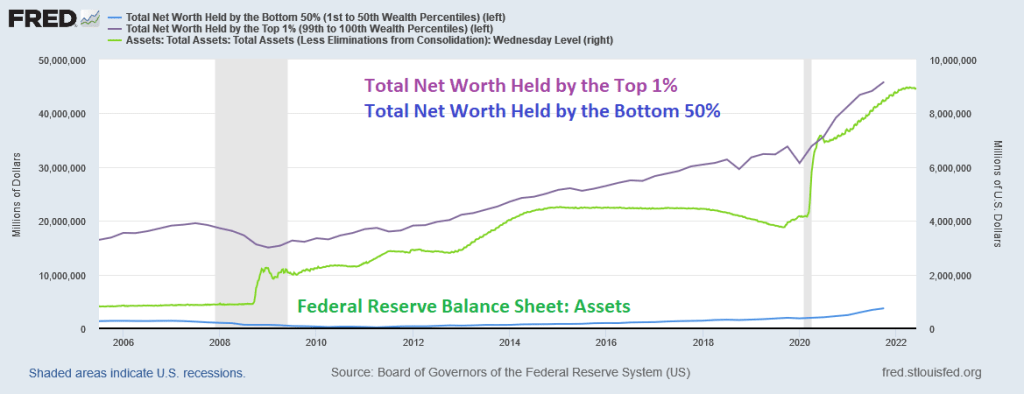

Pennies from Heaven. That is what the bottom 50% received from The Federal Reserve’s massive doses of monetary stimulus (or stimulypto).

There was one big dose of monetary stimulus in late 2008 surrounding the financial crisis and housing bubble burst, another doses (aka, QE 2 and QE3) then the biggest dose of all with the outbreak of Covid in early 2020.

President Biden should have mentioned on Jimmy Dimmel last night that The Federal Reserve has helped the bottom 50% with its endless monetary stimulus.

But if you were fortunate enough to own a home (the top 1% are likely homeowners), then you benefited from The Fed’s monetary stimulypto.

And I noticed that Biden didn’t mention plunging REAL average weekly earnings YoY.

The Federal Reserve’s monetary “policies” have benefited the top 1% and homeowners relative to the bottom 50% (who often rent and got clobbered with 20% growth in rents).

Great job, Fed! Making housing more unaffordable for rents (combine rising rents and declining REAL wages and we have a real affordability problem).

Home affordability for first time homebuyers?

And what is with Biden’s ear lobes? As inflation is rising, his ear lobes are shrinking.

The inflation numbers are out tomorrow. I noticed that Biden and Jimmy Dimmel only discussed gun control, not the sad state of the economy under Biden.

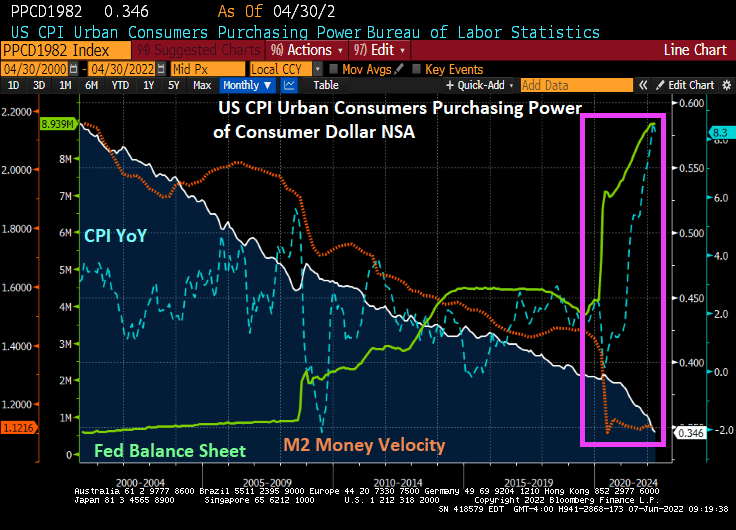

Here is my version of their chart since 2000 where you can seen the seismic shift in the balance sheet (toxic green slime line), particularly with The Fed’s response to Covid. The Fed is signaling a tightening in monetary policy to help reduce inflation (blue line).

But notice that M2 Money Velocity (GDP/M2) is now near the all-time low along with consumer purchasing power.

How BIG is The Fed’s balance sheet? Try more that a third of size of US GDP.

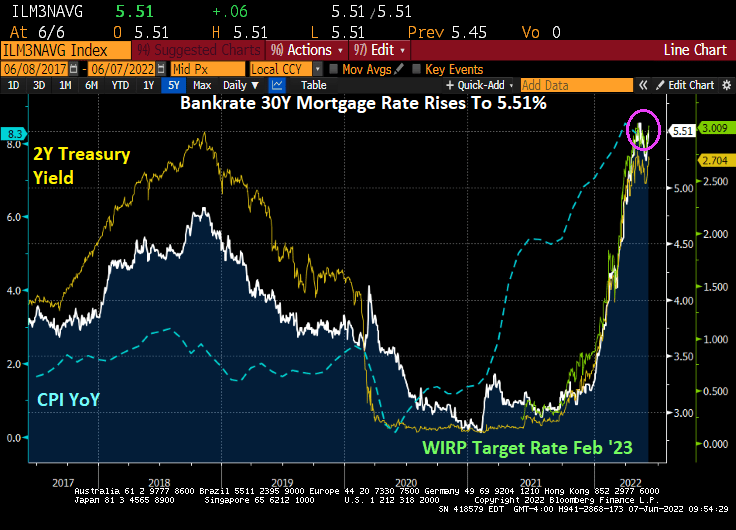

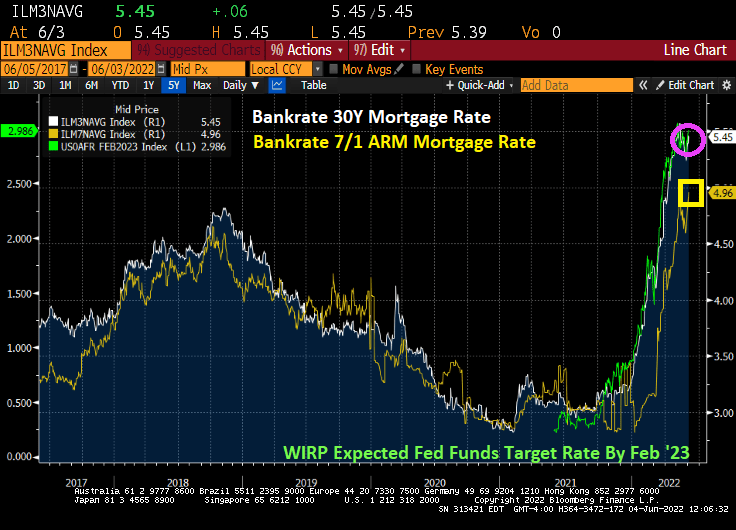

And as The Fed signals its inflation-fighting intentions, mortgage rates have shot up to 5.51%, the highest mortgage rate since June 2009.

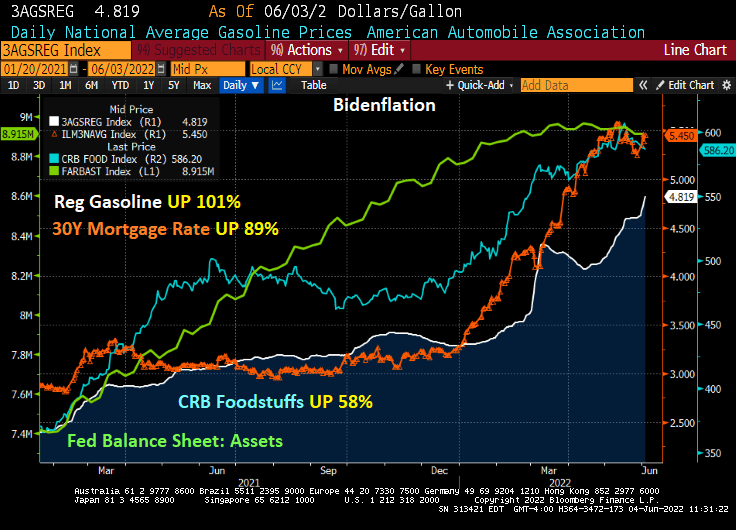

This is not the legacy that will endear President Biden to voters. Regular gasoline prices have risen 101% under Biden.

But it not just gasoline and diesel that are soaring (while the rest of us are sore!), CRB Foodstuffs are up 58% under Biden while the 30-year mortgage rate is up 89% under Biden.

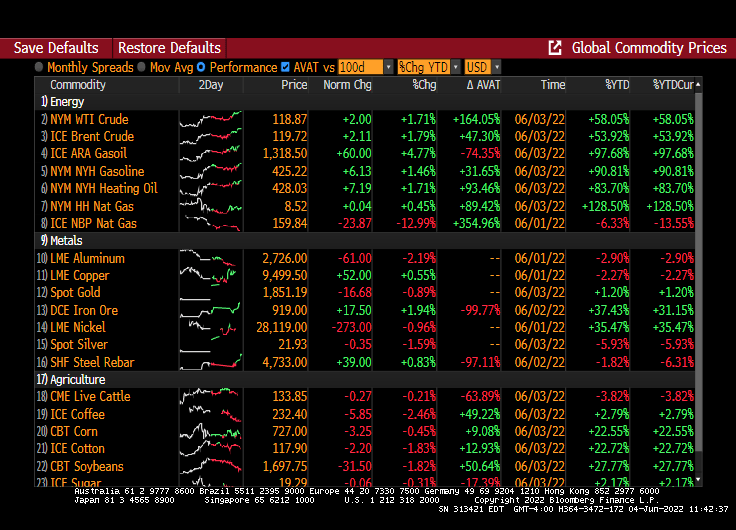

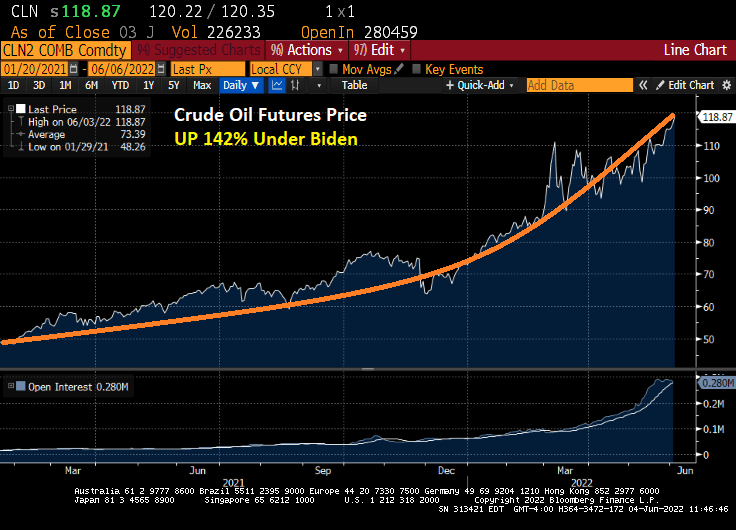

And this morning, WTI crude futures are up +1.71%.

And up 142% under Biden.

Prices are sizzling and clobbering the American middle class and low wage workers. But former Federal Reserve Chair and current US Treasury Secretary Janet Yellen never saw it coming.

Biden’s just killing us. And Powell is making up for Yellen’s keeping monetary stimulus too high for too long. Price? Mortgage rates are soaring.

US Real GDP Annualized QoQ printed at -1.5%. And GDP prices QoQ printed at 8.1%, also higher than expected.

At least Personal Consumption printed higher than expected at 3.1%.

Import prices (goods) led the way at 20.9%. Part of Biden’s brilliant strategy of reducing domestic oil production and import expensive energy from overseas?

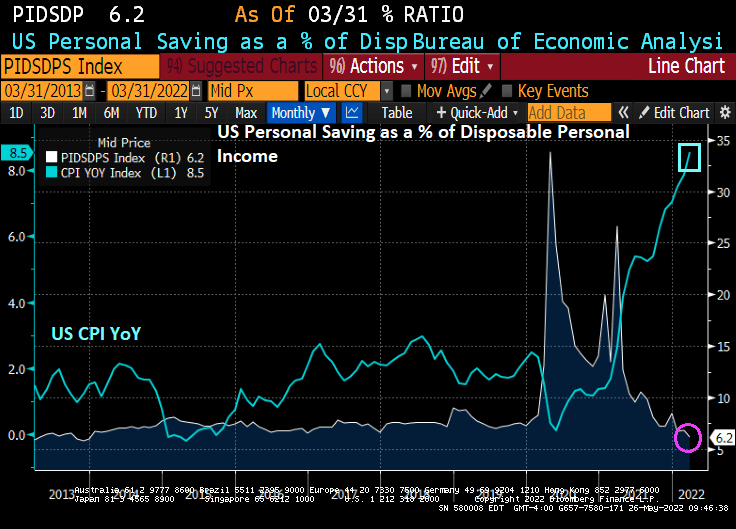

Consumers are spending more, but the personal savings rate is down to the lowest level since 2013 at 6.2% as consumers try to cope with inflation.

The US Q1 GDP report is due out tomorrow morning. The forecast is for -1.3% decline in GDP.

The Atlanta Fed GDPNow real-time GDP tracker is for 1.806% for Q2. If this holds, then recession fears will diminish.

Even though the US may avoid consecutive negative GDP quarters, M2 Money Velocity (GDP/M2 Money) got crushed by The Fed’s reaction to Covid back in 2020.

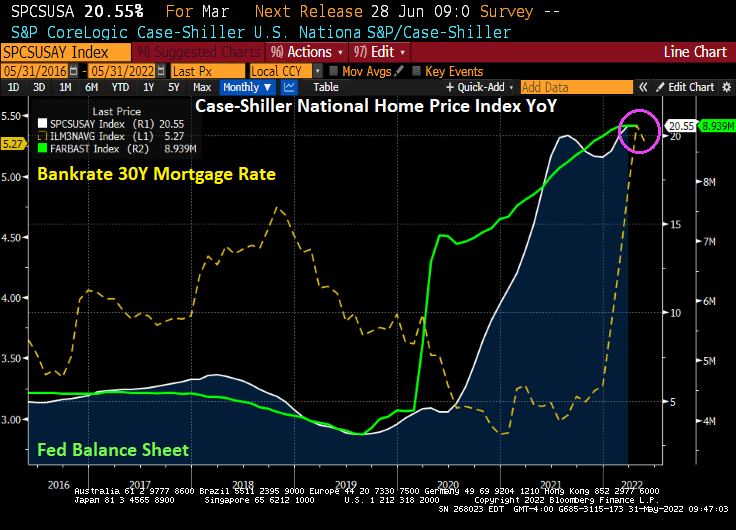

US home prices were growing at a near 20% YoY rate for the latest Case-Shiller National home price index report. But mortgage rates have soaring like a SpaceX missile shot.

Of course, I am moving to one of the metro areas in the USA where closed sales fell only -1.10% YoY in April: Columbus Ohio. I should move to San Diego CA where closed sales fell -21.4% YoY.

Of course, the US still suffers from lack of available inventory for sale.

April new listings are down -5.7% YoY. Columbus Ohio didn’t change from April ’21. San Diego is down -18.4% YoY for new listings.

Rising mortgage rates? Inflation? What a total fiasco.

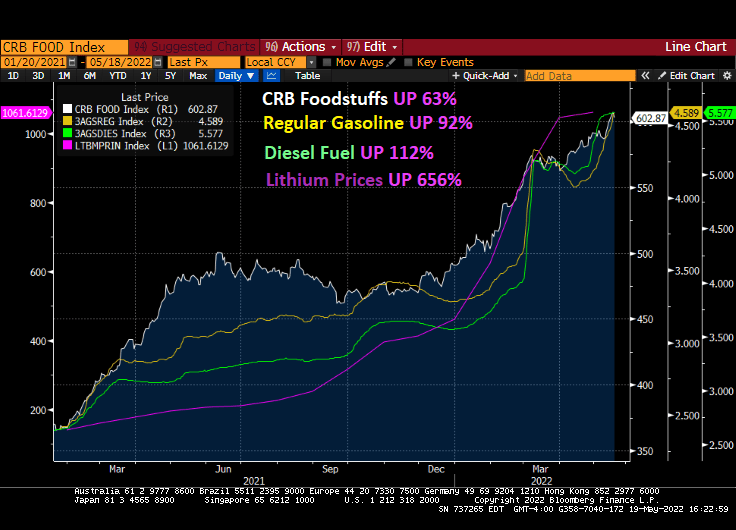

The inflation that is crushing Americans is due to energy and food price increases. That is, the non-core inflation. Under Biden, food is up 63%, gasoline is up 92% and diesel prices are up 112%. But The Fed doesn’t consider food and energy prices, per se.

If we look at the Taylor Rule considering fighting inflation including food and energy, The Fed would have to raise their target rate to … 21.38%.

Now, The Fed can clearly cool-off the housing market by raising rates. In fact, my fear is that they go too far and crash the housing market. The Fed will NEVER get to 20% again like we last saw under Volcker in 1981. 20% rates certainly cooled home prices back then and Fed rate hikes helped crash the housing market in 2008.

So, when The Fed says they want to be the inflation-fightin’ Fed, we must be aware what The Fed can and cannot do. They can’t tame the inflation beast in the form of food and energy prices (unless they crash the economy), but they can crush home prices.

You must be logged in to post a comment.