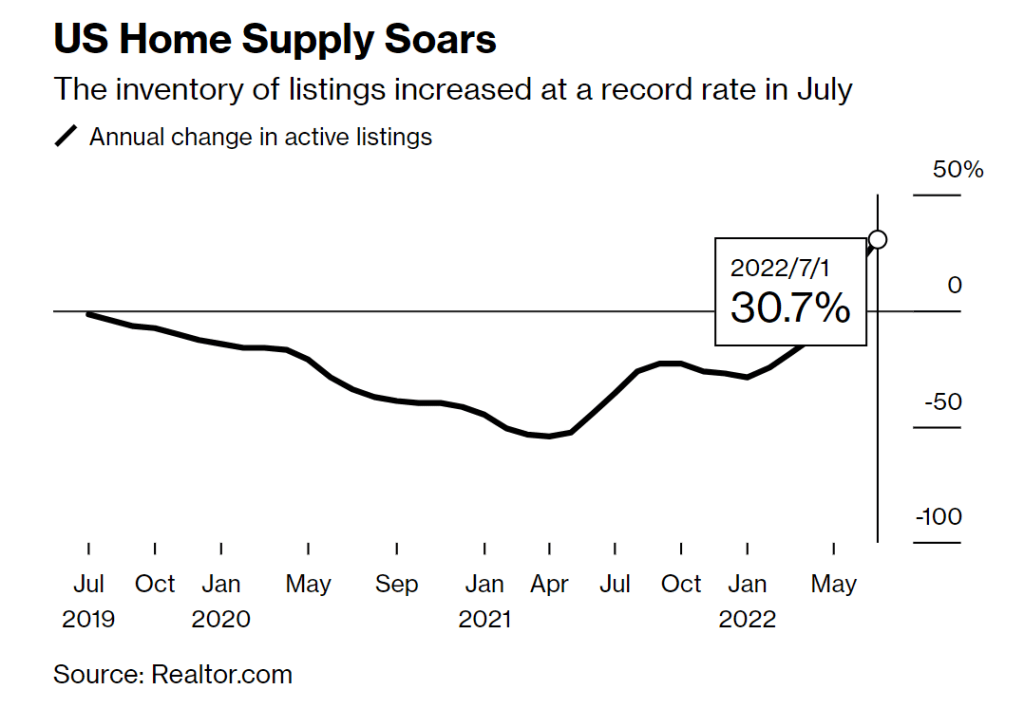

Meet Me At The Bottom … of the housing market?

As The Federal Reserve fights inflation (caused by too much Fed stimulus for too long) and Federal energy policies, we are seeing mortgage rates rising and the housing market decaying.

1-unit (single family detached) housing starts dropped -18.5% YoY in July as mortgage rates rose in 2022. Note the impact of the Covid stimulus (green line) and the resulting surge in housing starts in April 2021, but housing starts have decayed as M2 Money growth slows.

5+ unit (apartment) starts were down -10% MoM in July, but at least permits for apartments rose +2.51% MoM.

Well, we at least know why the NAHB Homebuilder index sucked wind so badly yesterday.

Perhaps the housing market needs a little spoonful of QE.

You must be logged in to post a comment.