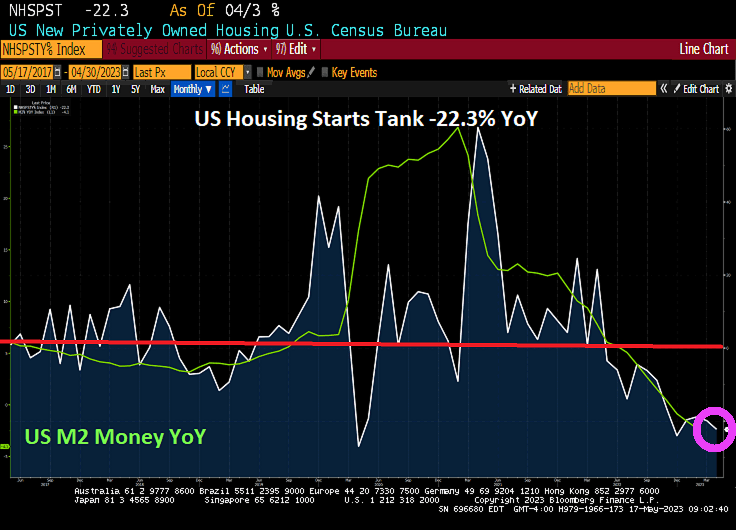

More bad news about the economy and housing sector under Biden/Yellen/Powell’s Reign of Economic Error.

US housing starts are out for April 2023. The bad news? Housing starts tanked -22.3% year-over-year (YoY).

The good news? US housing starts were up 2.19% from March to April. 1-unit detached starts were up 1.56% MoM while 5+ unit starts up 5.24% MoM. Permits for multifamily were down -9.71% from March to April.

The media will no doubt try to ignore the horrifying Durham Report. The report showed that Hillary Clinton and the Obama administration knowingly smeared Presidential candidate Donald Trump with false Russian misinformation and knowingly tried to steal an election. I wonder if Attorney General Merrick Garland will open an investigation into Hillary Clinton’s involvement in election tampering? Oh wait, the IRS was told to stop investigating Hunter Biden’s nefarious dealings. Never mind.

Resident Biden has been an unmitigated disaster for the US middle class, but fantastic for BIG corporate America and the donor class.

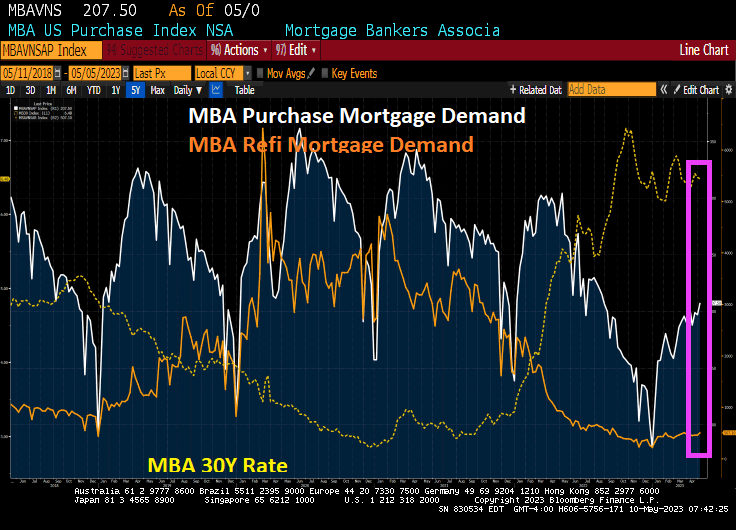

Mortgage applications increased 6.3 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending May 5, 2023.

The Market Composite Index, a measure of mortgage loan application volume, increased 6.3 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 7 percent compared with the previous week. The Refinance Index increased 10 percent from the previous week and was 44 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 5 percent from one week earlier. The unadjusted Purchase Index increased 5.3 percent compared with the previous week and was 32 percent lower than the same week one year ago.

Here is the data.

Middle class Joe as he likes to call himself is actually BIG CORPORATE Joe. A friend of big donor and BIG pharmam, BIG banks, BIG tech, BIG defense contractors, BIG media. No wonder Hunter Biden refers to Joe as “The BIG guy!”

Biden loves to brag about the greatest economy in history! Sure Joe. Life during Biden.

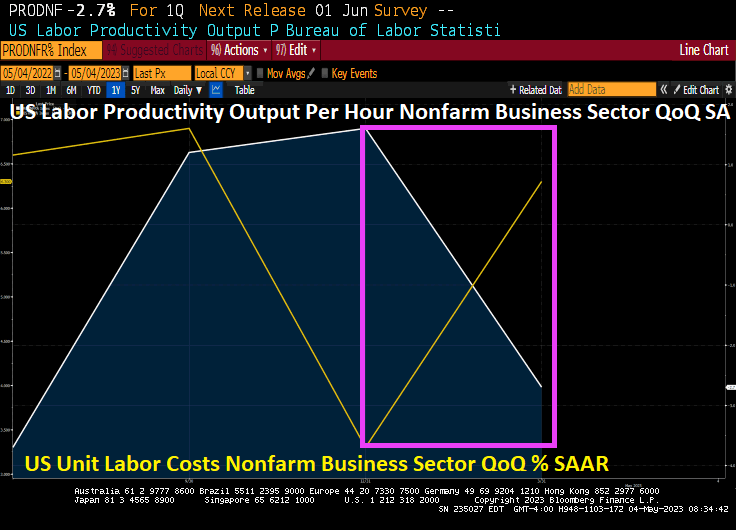

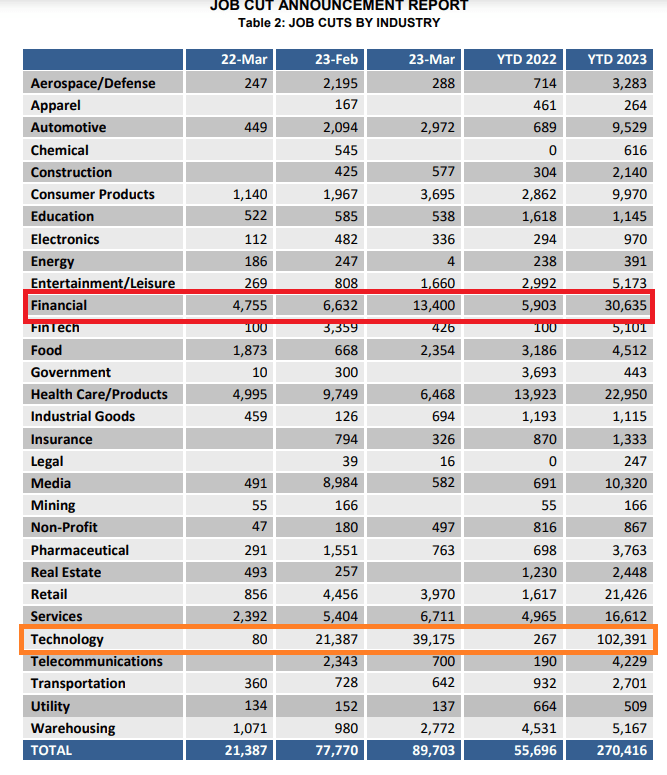

Challenger jobs cuts in April were 176% year-over-year. Non farm productivity in Q1 fell -2.7% QoQ. And unit labor costs in Q1 almost doubled to 6.3% QoQ, almost doubled from the Q4 2022 figure of 3.2%.

At least The Fed is going to pause it manic rate hikes. Then begin dropping them again.

This is life under Joe Biden. Record sovereign risk, record high debt, near 40-year highs in inflation, a hot war in Ukraine with Russia, failure of DOJ/FBI to do anything about the content of Hunter Biden’s laptop, repression of free speech, soaring crime, out of control borders. Should I keep going? It is a disastrous mess created by Obama/Biden and their creepy allies.

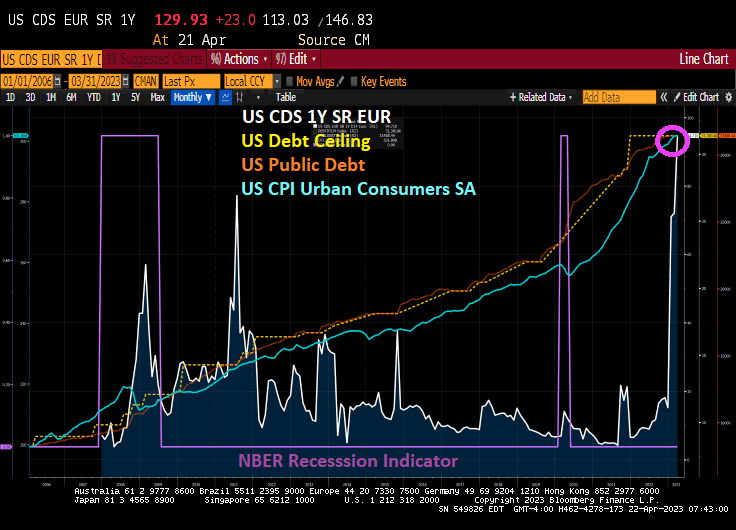

US sovereign risk just hit 130, the highest since CDS was recorded. This alligns with Biden/Congress massive borrow and spend policies where Federal debt has soared to it highest level in history. Inflation, while cooling, remains high.

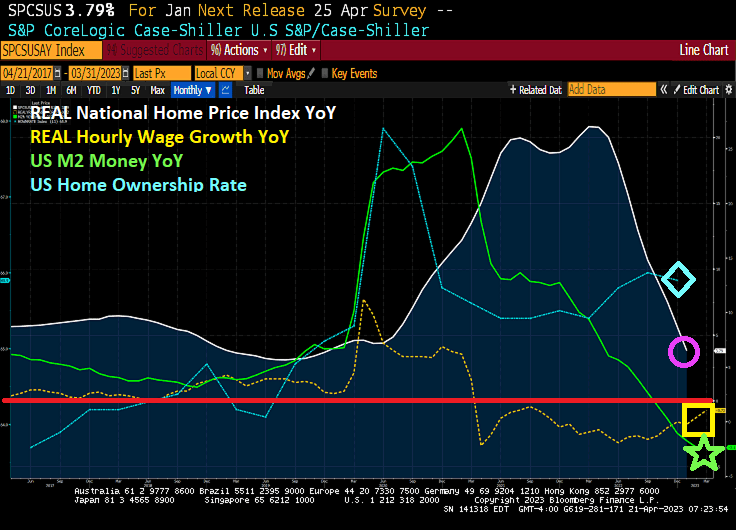

On the housing front, REAL national home price growth is negative which makes sense since REAL average hourly wage growth has been negative for the last 24 months.

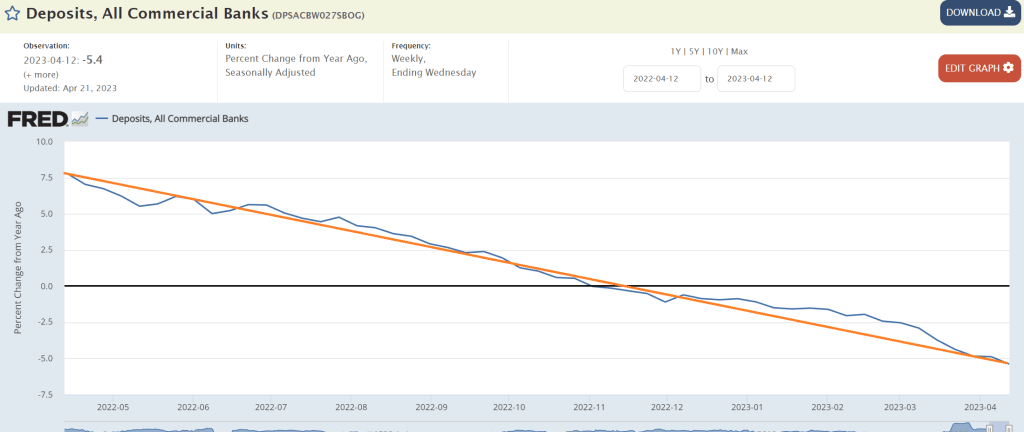

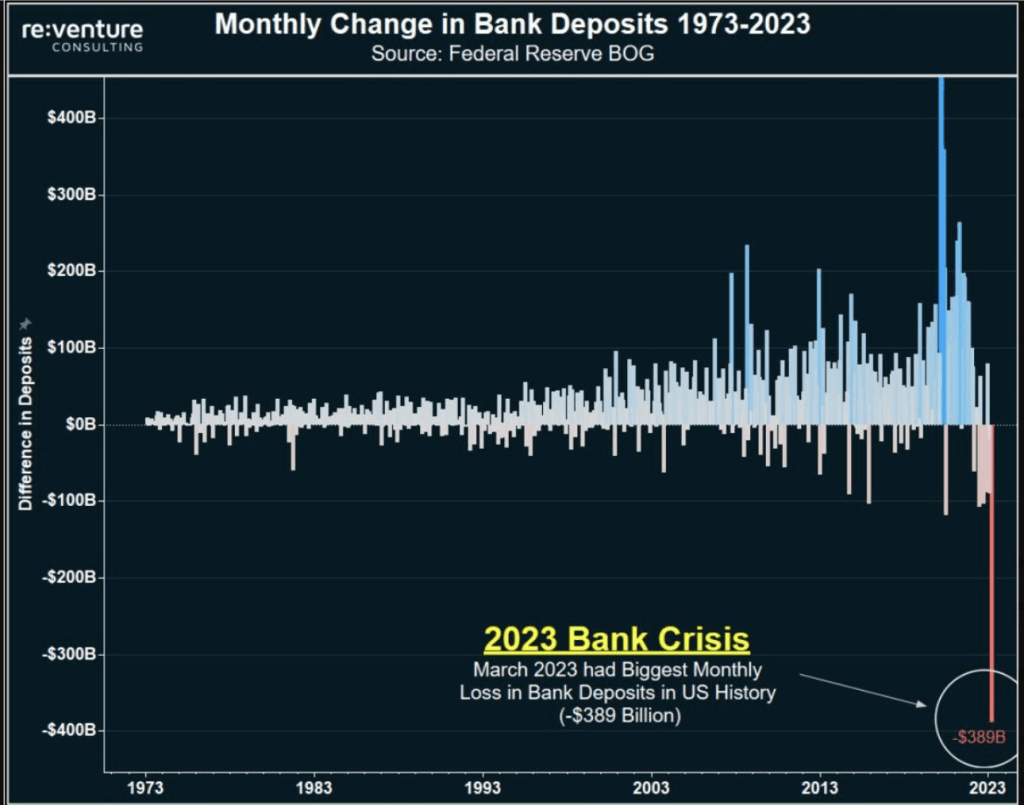

And just over the past year, commericial bank deposits are falling like a paralyzed falcon.

Biden and Obama’s chief hack in the White House, Susan Rice, are burning down the house.

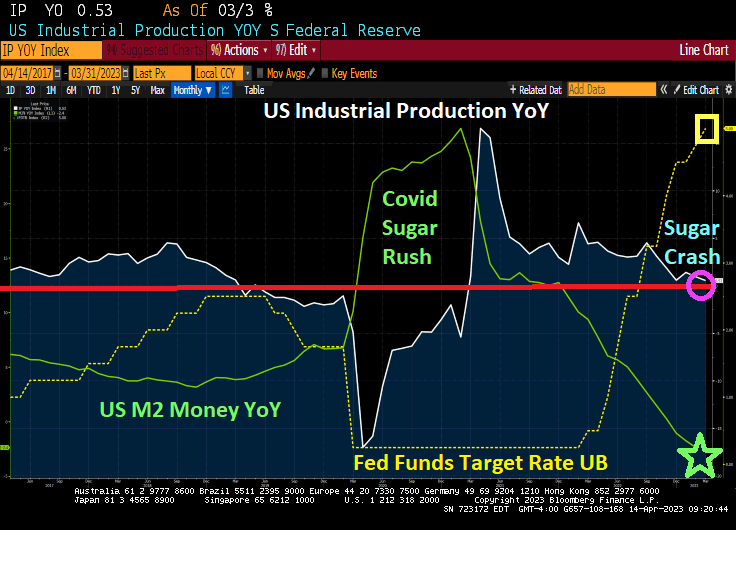

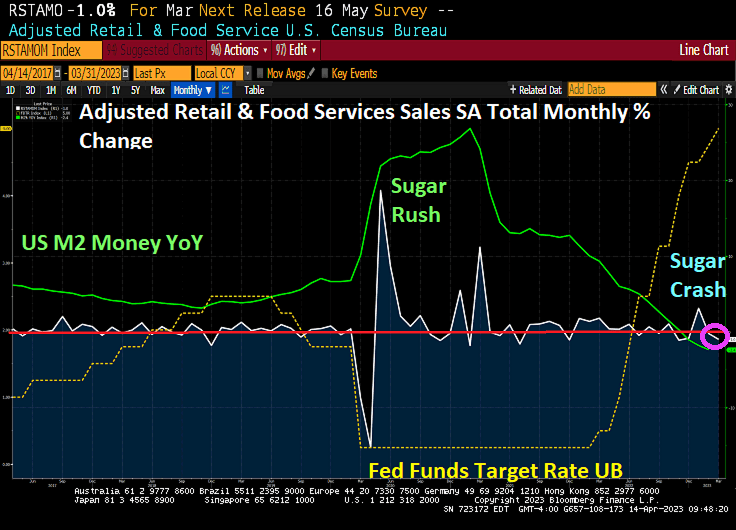

The US economy is barely chooglin along at a dismal 0.53% YoY (but 0.4% MoM in March). As the Covid “sugar rush” that caused a surge in Industrial Production in April 2021 of 16.56% has led to a “sugar crash” as M2 Money growth crashed and The Fed hiked rates to combat inflation. Known as a “sugar crash.”

Also in today’s economic news is more Sugar Crash news. Advance retail sales dropped -1% in March. That is -155% lower than a year ago when it was +1.8%.

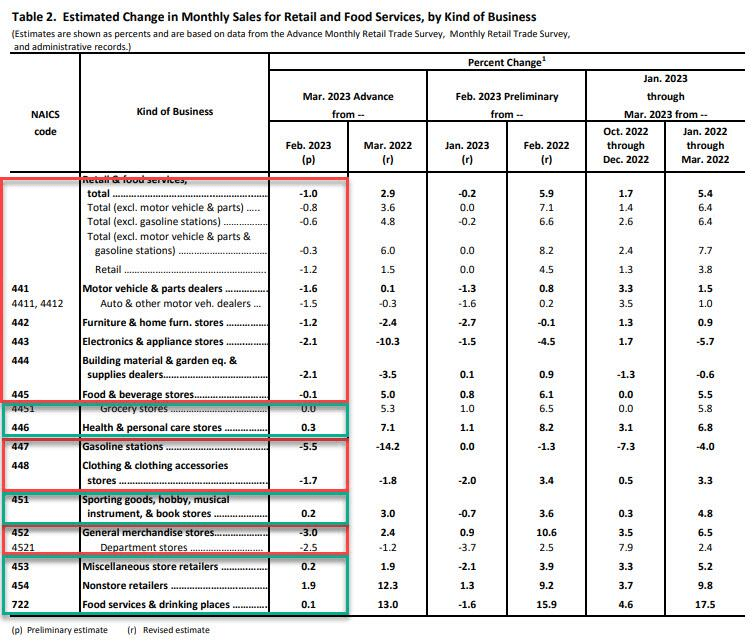

Here is the breakdown.

The Federal Reserve put a spell on us when Bernanke/Yellen kept rates too low for too long (TLFTL) and The Fed is now playing catch up. It is now creating havoc.

And on the Philly Fed’s Christopher “Fats” Waller saying that he favored more monetary policy tightening to reduce persistently high inflation, although he said he was prepared to adjust his stance if needed if credit tightens more than expected, we see that US Treasury 2-year yield jumping 13.5 basis points to 4.103%.

Joe Biden loves to brag about “his” great economic successes, particulary in jobs added. But the jobs added in March were not in higher-paying factory jobs, but Biden’s building from the bottom-up approach is mostly low-paying leisure and hospitality jobs.

And here is the rub on wages. Average hourly earnings growth fell to 4.2% YoY, too bad inflation is 6% and expected to rise with the summer.

236k jobs added in March, down from a revised 326k jobs added in February. The unemployment rate fell to 3.5% and labor force participation rose slightly to 62.6%.

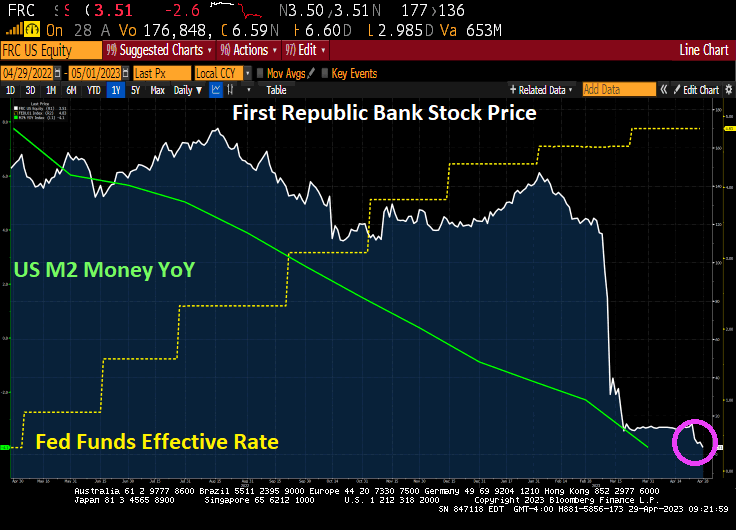

Thanks to Yellen’s catestrophic Too-Low-For-Too-Long (TLFTL) and insane Federal spending, we are seeing the aftermath of The Fed trying to fight inflation. A fire sale of failed bank assets!!

With interest rates still rising, prices retreating and credit evaporating—and a stressed-out banking system moving to shore up balance sheets—expect more fire sales of older CMBS loans and an acceleration of plunging CRE values in markets across the US.

Last month, a fire sale of CMBS loans was lit as $72B in assets from the failed Silicon Valley Bank (SVB) were sold. The SVB assets—including about $13B in real estate exposure and at least $2.6B worth of CRE loans—were sold at a discount of $16.5B, which translates into about 77 cents on the dollar, according to a report in MarketWatch.

The Federal Deposit Insurance Corp. has lit a fuse on an even larger fire sale of assets—a bonfire in terms of CRE loans—for NYC-based Signature Bank, which like SVB was a regional bank that collapsed and was taken over by regulators last month.

FDIC last week tapped Newmark to sell $60B in assets held by Signature, according to the Wall Street Journal, including nearly $36B in CMBS loans backed primarily by multifamily properties, the lion’s share of them in New York City. Since 2020, Signature initiated more than $13.4B in loans backed by NYC buildings, the most of any lender.

Experts who specialize in pricing CRE loans believe a discounted sale as large as the disposal of Signature’s assets will speed a markdown of valuations by banks who until recently have been reluctant to set off a downward spiral. The 77 cents on the dollar benchmark established by the SVB sale likely will be the top end of where prices are heading, the experts say.

“The SVB trade created a baseline for the market. To me, that’s the top end, not the bottom end, for CRE loans,” David Blatt, CEO of CapStack Partners, told MarketWatch. CapStack is a credit fund that buys CMBS loans from banks and originates short-term bridge loans and mezzanine debt.

“What everybody has been operating under is this hold-to-maturity veneer,” Blatt said, referring to banks that have continued to value loans at 100 cents on the dollar, known as par.

In the wake of the SVB asset sale, “there’s just no way these things get resolved at par,” Blatt said, adding “the write-down is kind of implied.”

“Everybody is dusting off their old playbook. There just hasn’t been [as] much distress for years,” Jack Mullen, founder of Summer Street Advisors, told Marketwatch. “People are not going to let it carry into next year. On the regulatory side, it’s coming to the front of the line. People are super-mindful about it.”

The rising cost of debt was cutting into the value of older, low-coupon loans before SVB and Signature were shut down. Now, everyone is guessing how low will prices go on CMBS loans in the wake of the fire sales of the fallen lenders’ portfolios.

A recent advisory from Cohen & Steers estimates the decline in values will likely be at least 25%. Loans associated with multifamily properties won’t be immune from the valuation hit; apartment rents declined for the fifth time in six months from January to February.

For office properties, especially in Manhattan, the decline in value will be much steeper. Older NYC office properties are facing a cliff-diving plunge of up to 70%.

CMBX S15 is plummeting like a paralyzed falcon after The Fed started raising rates.

As bank deposits continue to crash and burn.

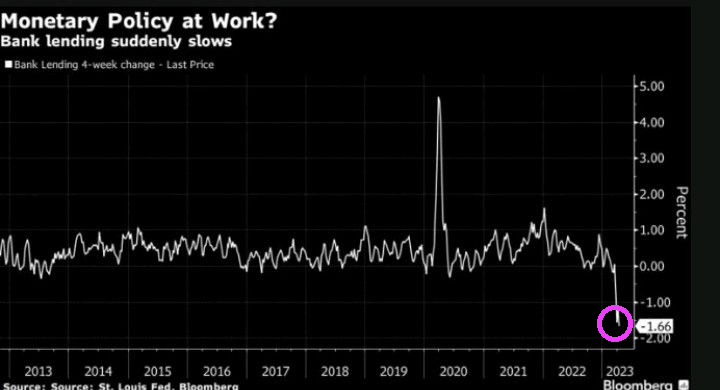

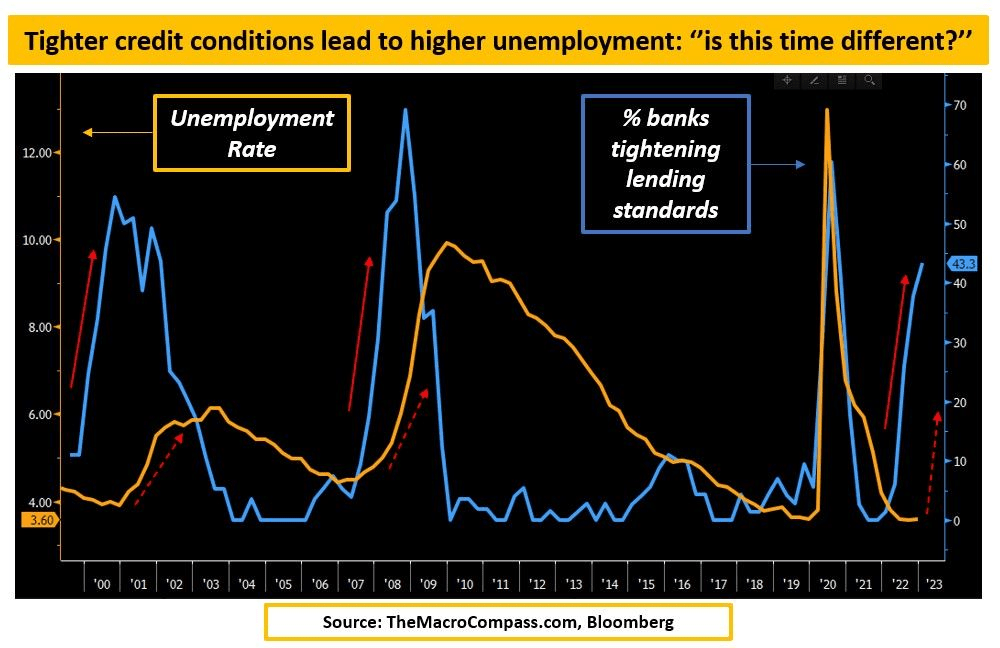

Now we have banks tightening lending standards.

So instead of The Boston Strangler, we have the DC Strangler.

You must be logged in to post a comment.