The Federal Reserve raised their target rate just once under President Obama until Donald Trump was elected. Then raised their target rate 8 times AFTER Trump was elected. In other words, Bernanke/Yellen kept the target rate near 0% for too long. When you throw the insane level of spending by Biden and Congress on top of the massive Fed stimulus. Now The Fed is trying to remove the excessive monetary stimulus by raising rates which is crushing banks.

Small bank reserces are low.

In any case, rate hikes are causing turmoil at small banks (as witnessed by the failures of SVB, Silvergate, First Republic and Signature Banks. Even worse, small banks hold 70% of commercial real estate loans.

Money managers have stepped up their bearish bets against office landlords, wagering that the US regional banking crisis will slash the availability of credit to property owners that were already suffering from the pandemic and rising interest rates.

Hedge funds are using credit derivatives and equities to bet against the companies and their debt. Almost 40% of shares in the iShares US Real Estate ETF are sold short, the highest proportion since June, according to data from analytics firm S3 Partners.

At Hudson Pacific Properties Inc., short interest reached a record 7.4% earlier this week before dropping to about 5% of shares outstanding, according to data compiled by IHS Markit Ltd. That’s almost double the level a month ago. For Vornado Realty LP, short interest is the highest since January.

Three regional banks have failed in the US, raising concerns about the implications for commercial real estate finance. Many lenders are losing deposits, which might cut into their ability to finance real estate in the future. Regional banks account for about 80% of bank lending to commercial properties, according to economists at Goldman Sachs Group Inc.

“What’s changed in the last few weeks is the credit markets,” said Rich Hill, chief of real estate strategy research at Cohen & Steers Capital Management Inc. “It went from a story of work-from-home and the impact on occupancy and the lack of rent growth to also the compounding of tighter financial conditions given everything happening with banks.”

Fears of tighter credit are adding to risks for offices that have been building for some time, Green Street analysts wrote in a Tuesday report. Hedge fund manager Jim Chanos, Marathon Asset Management and Polpo Capital Management founder Daniel McNamara are among those who have been betting for months that landlords will struggle to lure staff back to workplaces.

“This regional banking crisis is just throwing fuel on the fire,” McNamara said in a telephone interview. “I just don’t see a way out of this without a lot of pain in the office sector.”

Vulnerable Landlords

Real estate was already the most shorted industry across global equities, according to a March 17 report by S&P Global Inc. It was the third most-shorted sector in the US.

That’s in part because interest rates have been climbing for the last year, which pressures real estate owners. Defaults remain low for now. But office assets are the collateral for about $100 billion of the $400 billion of US commercial real estate debt maturing this year, according to MSCI Real Assets.

Workplaces worth nearly $40 billion face a higher probability of distress, more than apartments, hotels, malls or any other type of commercial real estate, MSCI said on Wednesday. Almost $20 billion of office loans that were bundled into commercial mortgage-backed securities and are due to mature by the end of next year are already potentially distressed, Moody’s Investors Service estimates.

Credit availability for commercial real estate was already challenged this year as investors have grown less interested in buying commercial mortgage bonds, JPMorgan Chase & Co. analysts including Chong Sin wrote in a note. Sales of CMBS deals without government backing have fallen more than 80% this year, according to data compiled by Bloomberg News.

Smaller banks potentially retreating may bring a credit crunch to smaller markets, the JPMorgan analysts wrote.

Lenders advanced a record $862 billion to commercial real estate last year, a 15% increase from a year prior, data provider Trepp estimates. Much of that was driven by banks, which originated 50% more loans in the period. The pace of growth has slowed since then, Federal Reserve data show, as the outlook for real estate grows increasingly negative.

The pressure on offices means lending standards are now being tightened, bad news for landlords that have high levels of leverage and putting lenders at a higher risk of defaults.

“Recent developments have increased downside risk to commercial real estate values from expectations of tightening lending standards,” Morgan Stanley analysts including Ronald Kamdem wrote in a note on Monday. Office REITs may have to sell assets to help them successfully refinance, they said.

Shorts soared on office landlords last year as rising interest rates weighed on the industry. They dropped subsequently as investors wagered that borrowing benchmarks would top out at a lower level than initially expected or the Federal Reserve would begin to cut the rates earlier than previously expected.

Cohen & Steers, which oversees about $80 billion, including $48 billion in real estate investments, went under weight on offices during the pandemic and will steer clear until the market shows signs of hitting a floor.

“I actually want to see more signs of weakness,” Hill said. “The more headlines I see that things are really, really bad, the closer I think we are to the end.”

Chanos Short

Chanos said on CNBC in January that he had been betting against SL Green Realty Corp., short interest in which reached the highest since the financial crisis in recent days. The landlord’s assets include a New York building occupied by Credit Suisse Group AG, the lender taken over by UBS Group AG after government-brokered talks. Short sellers borrow stock and sell it, planning to profit by buying it back at a lower price later.

An SL Green spokesperson directed Bloomberg to company comments at a March 6 investor conference, before the recent bank failures.

The landlord plans to sell $2 billion of properties, cut its debt by $2.5 billion and refinance a $500 million mortgage, Chairman and CEO Marc Holliday said at the Citigroup Inc. conference. Because the securitization market and life insurance financing weren’t receptive to deals, the firm is dependent on banks, which were already an uphill challenge.

“Banks are more likely to say no these days than to execute,” Holliday said. “Knock on wood, hopefully we can get that done.”

Mark Lammas, president of Hudson Pacific, said in an emailed statement that the firm is confident in its business fundamentals and long-term prospects. The company is investment-grade, a majority of its assets are unencumbered, it has $1 billion of liquidity, and no material debt maturities until 2025, Lammas said.

Chanos and representatives of Vornado and Boston Properties didn’t immediately reply to requests for comment.

‘The Widowmaker’

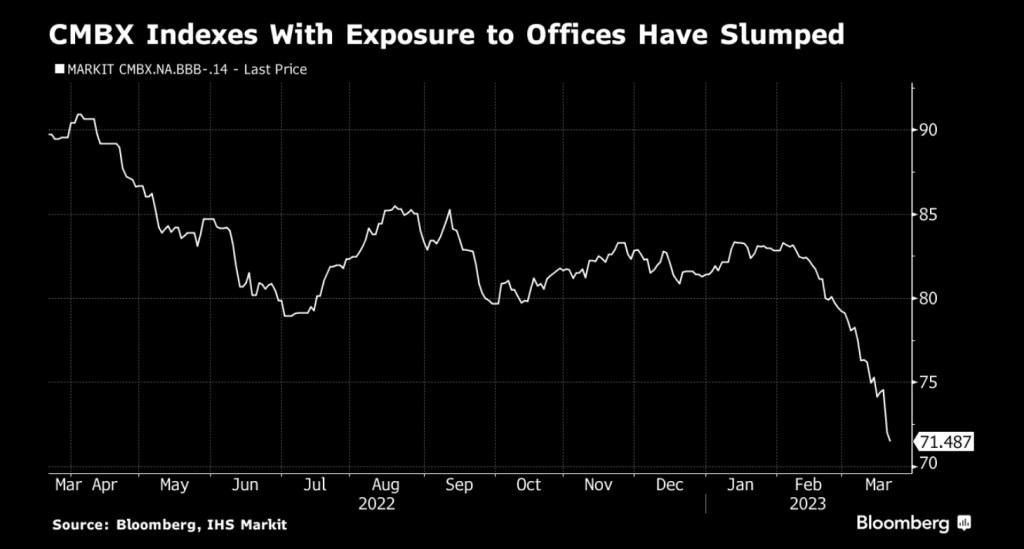

Hedge funds have also been using credit-default swaps indexes known as CMBX to bet against CMBS that are most exposed to offices. The derivatives are tied to portions of bonds backed by commercial mortgages and a number of them reached a record low this week amid fears about a number of regional banks.

Betting against commercial real estate has historically been a hard way to make money, because it can take a long time for losses to emerge, and the range of possible outcomes for even troubled property can be wide. “Shorting CMBX BBB- is regarded as the widowmaker — the undoing of many a young trader’s career,” Morgan Stanley trader Kamil Sadik wrote in a March 6 note.

But the spate of bad news means the BBB- portion of the 14th CMBX index is at the lowest level ever and the same part of the 13th index is at its lowest since the pandemic in 2020. Similar declines are also being seen in share prices of office landlords.

“Our conversation with investors suggests that there has been some capitulation and forced selling as the stocks have continued to underperformed,” Morgan Stanley analysts led by Kamdem wrote.

So far in 2023, there has been 17 downgrades of CMBS deals with no upgrades.

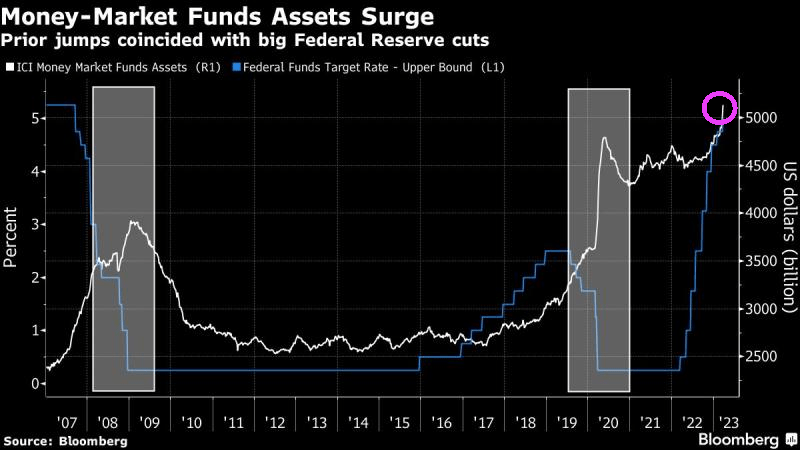

Investors are fleeing to money market funds as The Fed hits the brakes.

Yesterday’s inflation report (in the form on skyrocketing labor costs) helped lead Bankrate’s 30-year mortgage rate to over 7% … again.

Here is yesterday’s horrible unit labor costs YoY chart showing the fastest growth in labor costs since 1982 and Fed Chair Paul Volcker. Jerome Powell, the current Fed Chair is trying to reduce the Bernanke/Yellen/Powell monetary stimulypto (with an extra dose of “sugar” from the Covid outbreak).

The good news is that the 10-year Treasury yield is down -7.3 basis points this morning.

Soft landing for the US economy? It is looking less and less likely. The bond market (10-year Treasury yield) just shed -14.1 basis points. As I always told my investments students, any 10 basis point shift in the 10-year Treasury yield is significant.

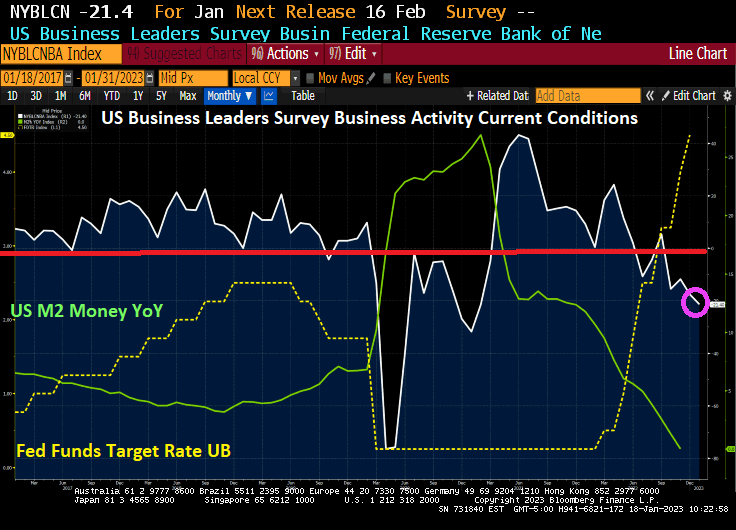

Let’s start wit the US business leaders survey of current conditions. It just crashed to -21.4

Then we have US industrial production, down -0.7% in December. And is up only 1.65% year-over-year as M2 Money growth stalls.

Capacity Utilization plunged more than expected to 78.7% (79.5% exp).

Biden claiming the US economy is strong is pure Fantasy Island.

Today, Jean Pierre annouced that Biden’s economic plans are working.

US existing home sales in November collapsed by -38.6% YoY as M2 Money growth runs out of gas.

The above chart is similar to yesterday’s “Ski Slope” chart of US home prices YoY.

Unfortunately, pending home sales YoY are the worst in recorded history.

What will President Biden do about this dire situation? Our “Vacationer in Chief” is off on yet another vacation to St. Croix in the US Virgin Islands, so probably nothing. Now that Biden is sunbathing, what will his Treasury Secretary Janet Yellen do?

The Federal Reserve forecast for the US economy is a dismal 0.50% YoY. Do I detect a trend?

The FOMC forecast for 2023 and 2024. Core PCE YoY (inflation) is forecast to drop to 3.50%, still considerably higher than The Fed’s target rate of inflation of 2%. And unemployment is forecast to be 4.60%.

To cope with Bidenflation, US personal savings rate as of October is -67.9% YoY. The “good” news is that rents YoY are crashing. But food prices under Inflation Joe remain very high. But most everything is slowing down, not due to Biden’s policies, but a global and US economic slowdown.

With a big slowdown coming our way, you can understand why The Fed’s December Dot Plot is showing declining Fed Funds Target rate starts declining in 2024.

Even US mortgage rates are headed down.

Speaking of going down, cryptos are down across the board with Cardano leading the decline at -6.91%.

Fun week ahead. US inflation numbers are out on Tuesday (forecast? CPI YoY = 7.3%, Core CPI YoY = 6.1%) and The Federal Reserve’s Open Market Committee (FOMC) rate decision is on Wendesday.

So, where are we sitting on Monday?

First, the US Treasury 10Y-2Y yield curve has been inverted (a precursor to recession) for 116 straight days). Second, the likelihood of recession in 2023 is 100%. Third, with the forecast of core inflation at a still numbing 6.1%, The Fed seems dead set on raising their target rate by 50 basis points to 4.50% on Wednesday.

dddd

So, as The Fed debates recession versus fighting inflation (partly caused by The Fed), we have Kevin Malone from The Office debating Angela versus double-fudge brownies:

US mortgage rates fell for a fourth week in a row, the longest such stretch of declines since May 2019.

The contract rate on a 30-year fixed mortgage eased 8 basis points to 6.41% in the week ended Dec. 2, still the lowest since mid-September, according to Mortgage Bankers Association data released Wednesday.

Rates have retreated for the past month as the Federal Reserve has signaled it will soon slow down the pace of interest-rate hikes, likely at next week’s policy meeting.

Even so, MBA’s mortgage purchase index fell 3%, the first drop in five weeks, underscoring how demand remains fickle and driving a decline in the overall measure of mortgage applications. On the other hand, refinancing activity rose last week, but remains near the lowest level in two decades.

Here is a chart of mortgage applications from the Mortgage Bankers Association showing the decline in US mortgage rates, and increases in mortgage purchases and refi applications. The Refinance Index increased 5 percent from the previous week and was 86 percent lower than the same week one year ago. The unadjusted Purchase Index increased 31 percent compared with the previous week and was 40 percent lower than the same week one year ago.

The MBA survey, which has been conducted weekly since 1990, uses responses from mortgage bankers, commercial banks and thrifts. The data cover more than 75% of all retail residential mortgage applications in the US.

Due to high inflation, reduced consumer spending, higher rents and other economic pressures, U.S.-based small business owners’ rent problems just escalated to new heights nationally this month, based on Alignable’s November Rent Poll of 6,326 small business owners taken from 11/19/22 to 11/22/22.

Unfortunately, 41% of U.S.-based small business owners report that they could not pay their rent in full and on time in November, a new record for 2022. Making matters worse, this occurred during a quarter when more money should be coming in and rent delinquency rates should be decreasing. But so far this quarter, the opposite has been true.

Last month, rent delinquency rates increased seven percentage points from 30% in September to 37% in October. And now, in November, that rate is another four percentage points higher, reaching a new high across a variety of industries.

All told in Q4 so far, the rent delinquency rate continues to increase at a significant pace, up 11 percentage points from where it was just two months ago.

Well, this is not good.

And on the mortgage front, not all is quiet.

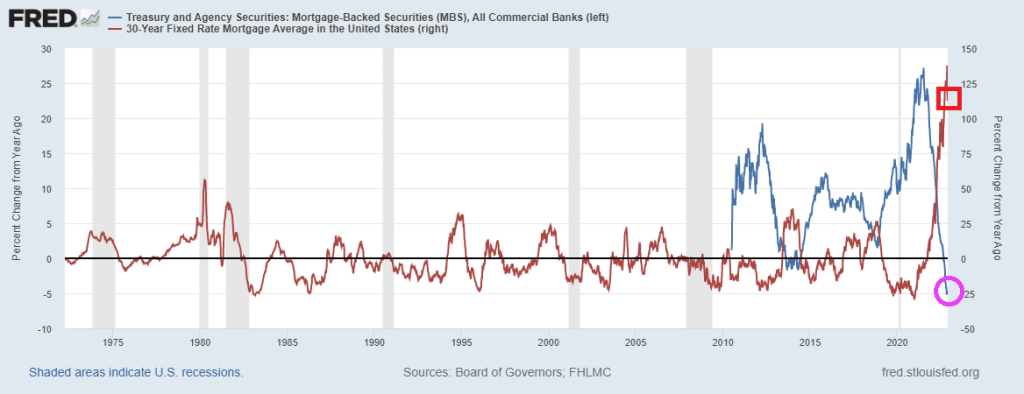

Commercial bank holding of Agency mortgage-backed securities (MBS) has collapsed with Fed tightening and mortgage rate increases.

November’s consumer sentiment survey from University of Michigan is one for the books. It printed at 33.0, the lowest in the history of the survey that goes back to 1977.

This chart shows how The Fed and Federal government threw trillions at the Covid economic shutdowns and the aftermath (green line).

You must be logged in to post a comment.