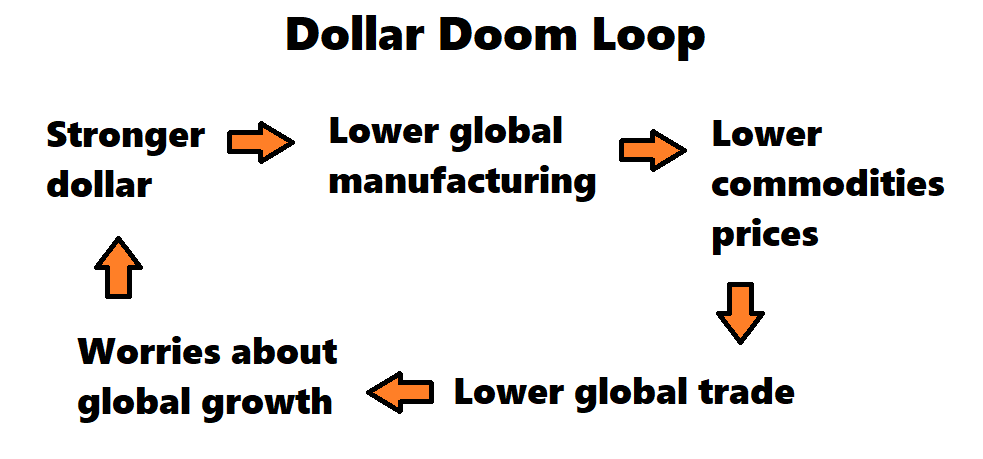

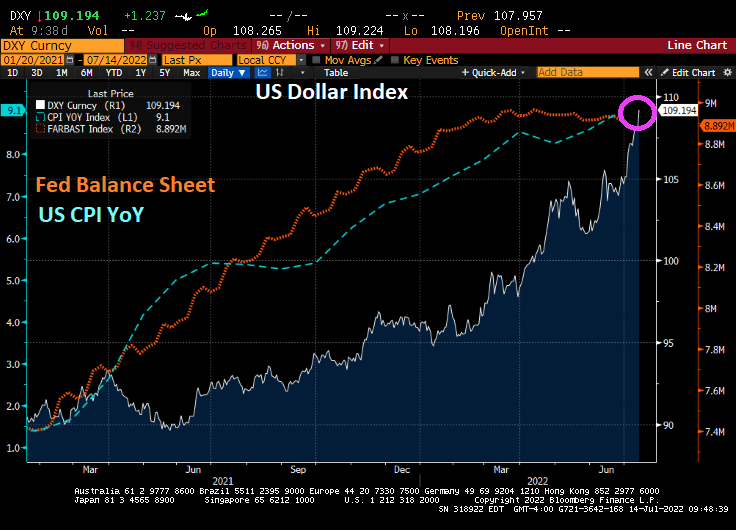

The dollar’s gain is the world’s pain — and based on its current trajectory, the world may be in for a whole lot more discomfort.

Concerns over global growth have recently sent the US Dollar Index to the strongest level on record, with the greenback hitting multi-decade highs against currencies like the euro and the yen.

But the move risks becoming a self-reinforcing feedback loop given that the vast majority of cross-border trade is still denominated in dollars, and a stronger US currency has historically translated into a broad hit to the world economy.

Against the backdrop of higher-than-expected inflation and still-elevated commodities prices, the concern is that we’re in for a dollar ‘doom loop’ like never before, according to Jon Turek, the founder of JST Advisors and author of the Cheap Convexity blog.

With the Federal Reserve hiking interest rates at the fastest pace in decades, he says, it’s much less clear what could break the feedback loop in the next few months.

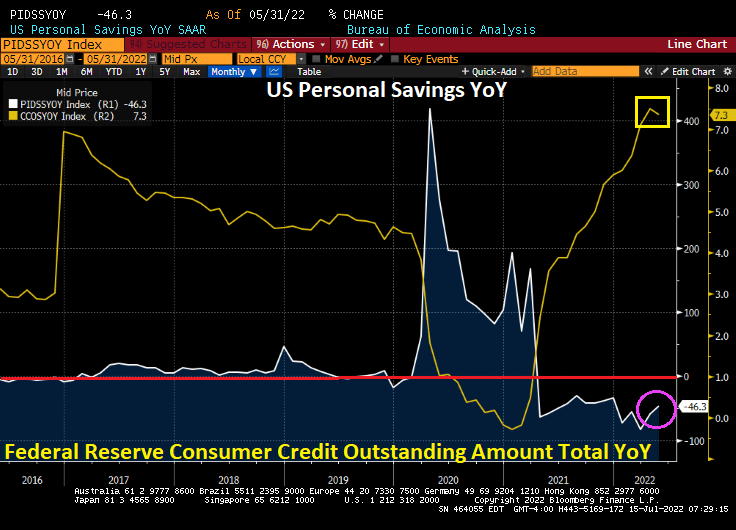

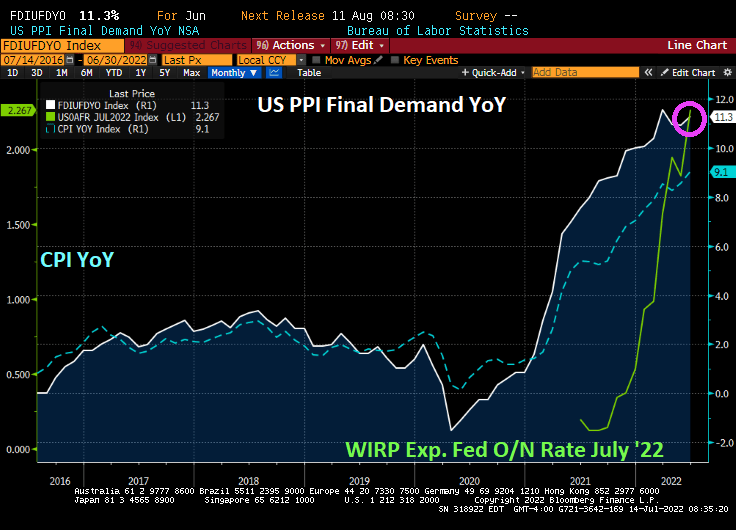

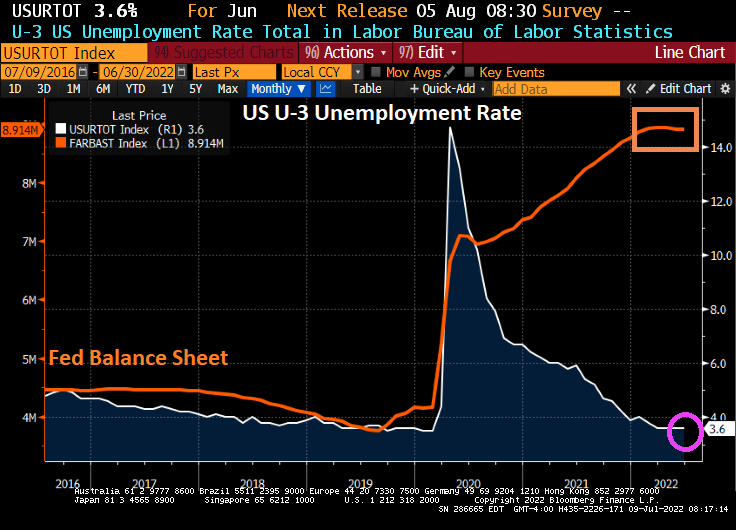

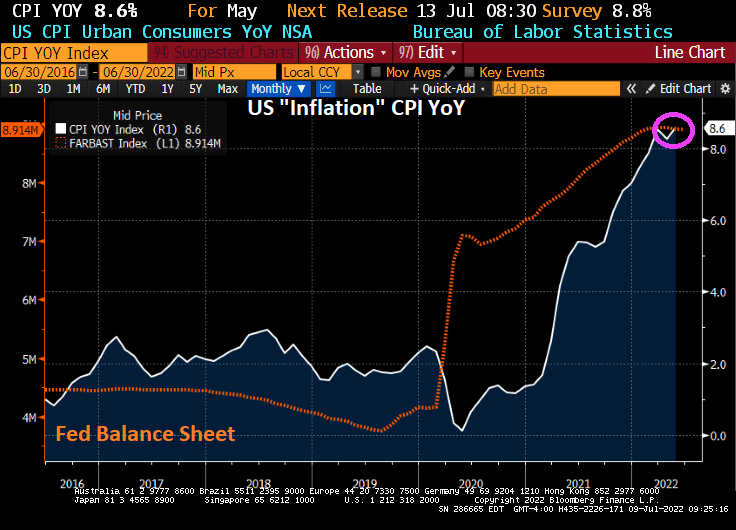

The Dollar Doom Loop with US inflation causing The Fed to tighten

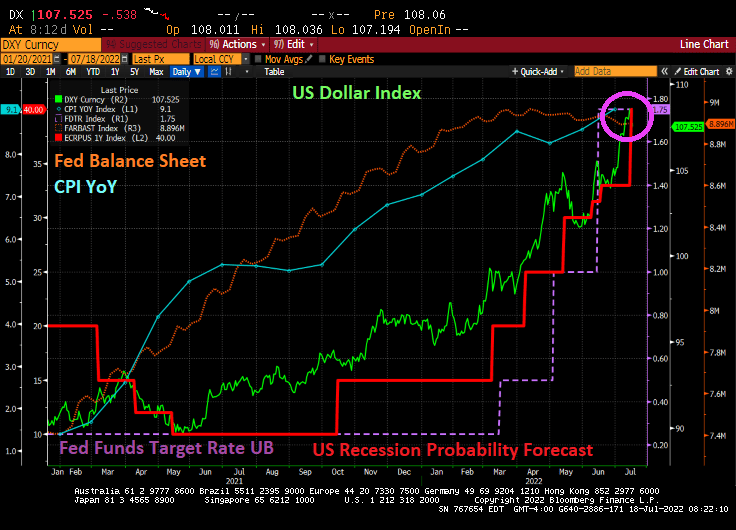

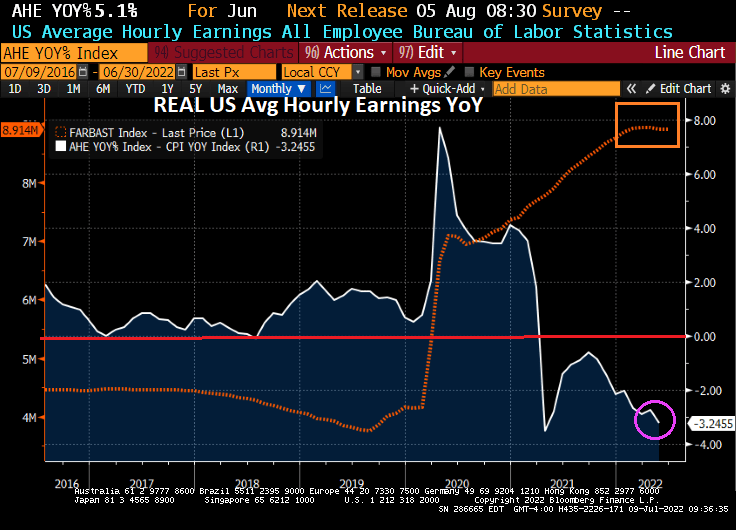

Under Biden’s policies, inflation hit a 40-year high (blue line), and the US Dollar (green line) is strengthening. Then we have The Fed raising the target rate (purple line) and the probability of recession rising with Fed tightening.

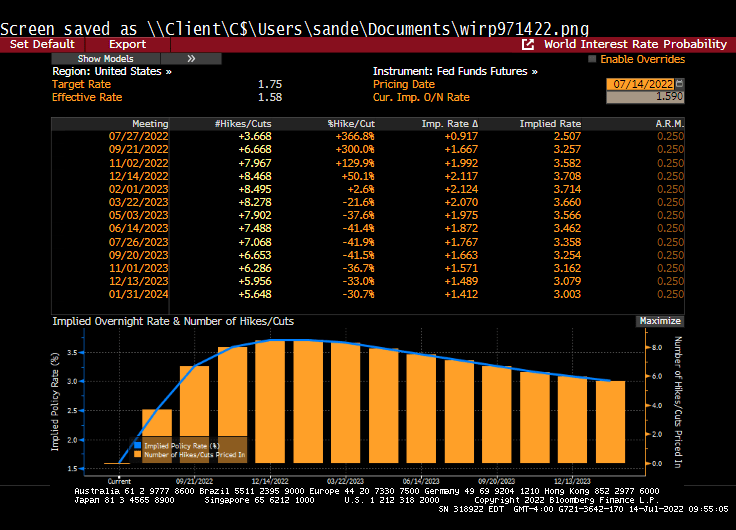

Is a US recession coming? The US Treasury 10Y-2Y yield curve is inverted at almost -20 basis points.

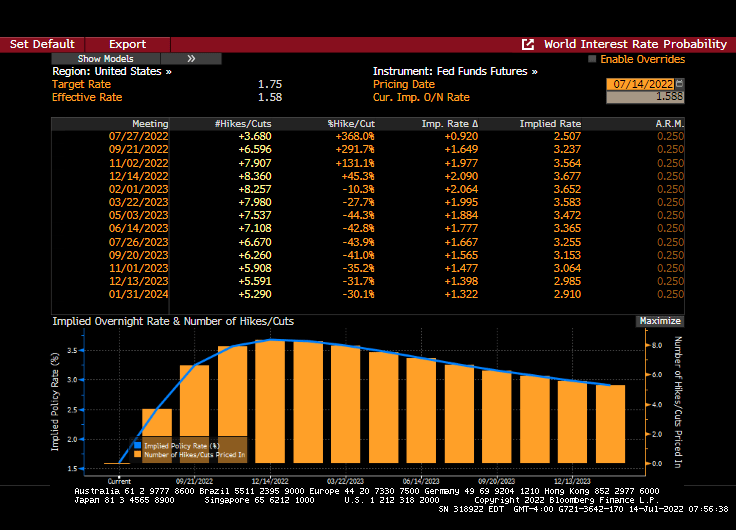

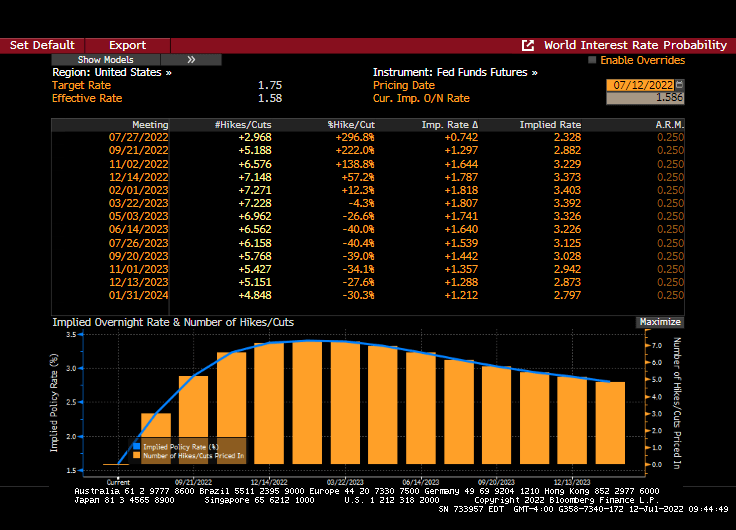

There is a Fed open market committee meeting in one week and they are expected to raise their target rate by 75 basis points according to Fed Fund Futures data. Inflation keeps rising as does the probability of a US recession. So, The Fed will keep on tightening.

You must be logged in to post a comment.