This isn’t Barbara Tuchman’s class novel about the horrors of World War I, but the ongoing horrors of Bidenomics with its guns pointed at the American middle class.

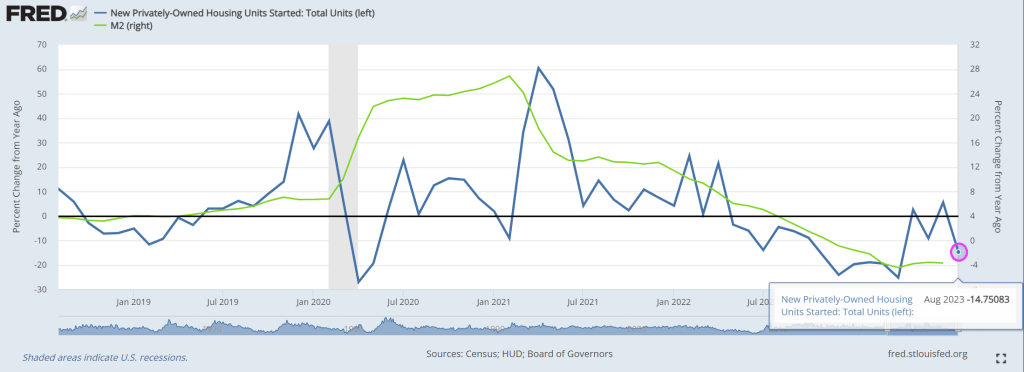

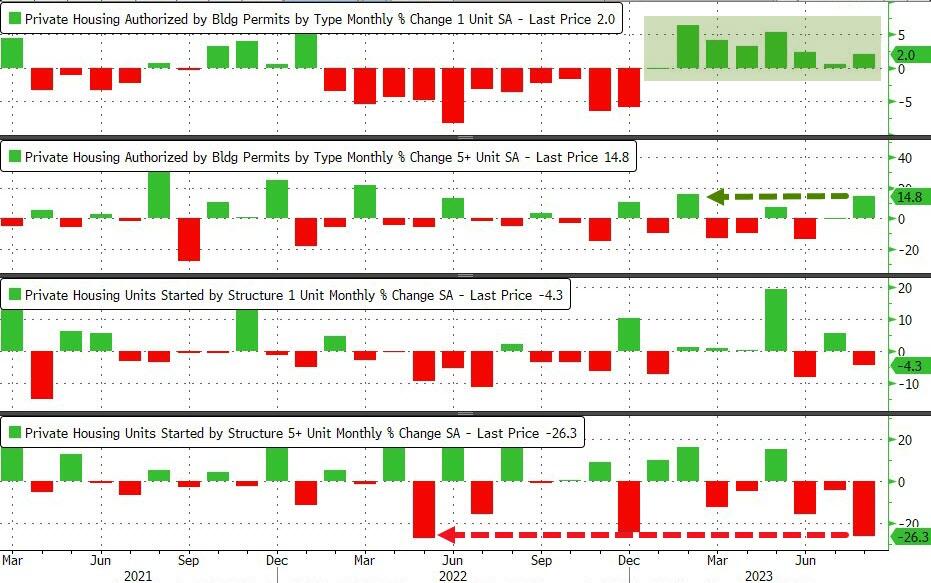

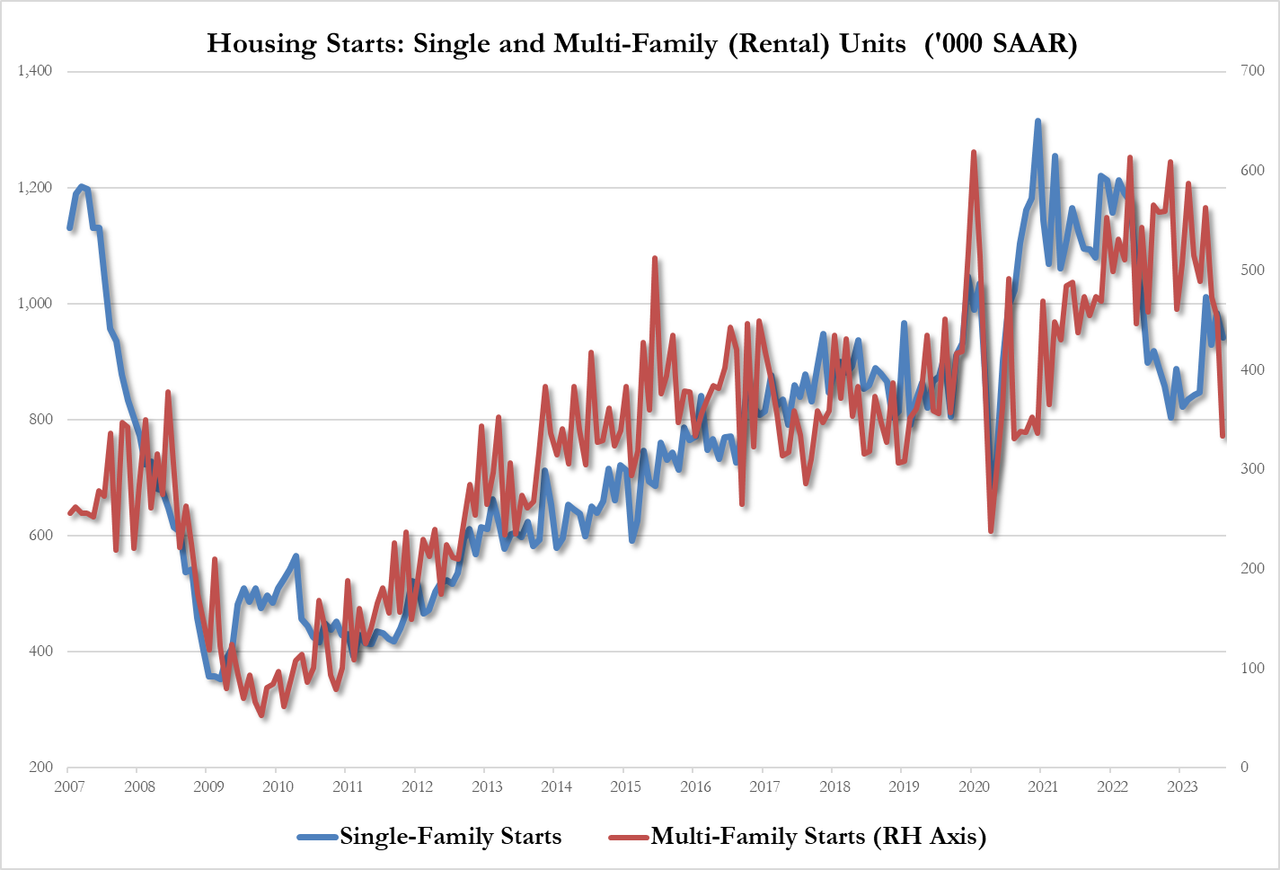

Privately‐owned housing starts in August were at a seasonally adjusted annual rate of 1,283,000. This is 11.3 percent below the revised July estimate of 1,447,000 and is 14.8 percent below the August 2022 rate of 1,505,000.

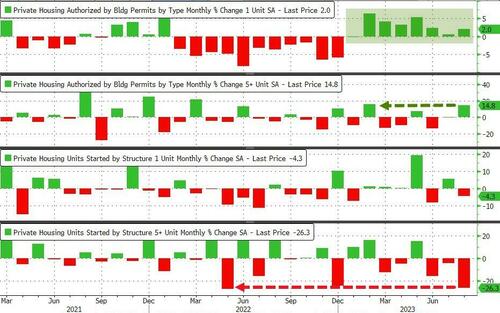

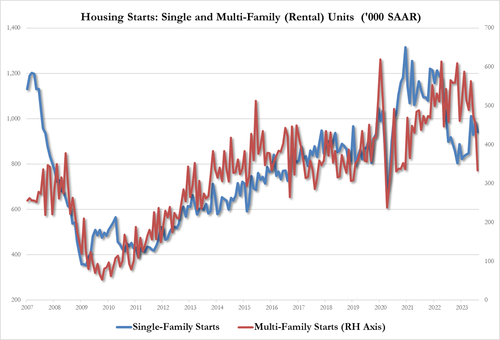

Single‐family housing starts in August were at a rate of 941,000; this is 4.3 percent below the revised July figure of 983,000. The August rate for units in buildings with five units or more was 334,000. This leaves Starts (SAAR) at their lowest since June 2020 and Permits (SAAR) at their highest since Oct 2022…

Source: Bloomberg

Under the hood, multi-family rental starts plunged by the most since June 2020 while single-family permits rose for the 8th straight month…

Source: Bloomberg

For context…

Finally, if sentiment among homebuilders is collapsing again, why are they loading up on permits?

Source: Bloomberg

Source: Bloomberg

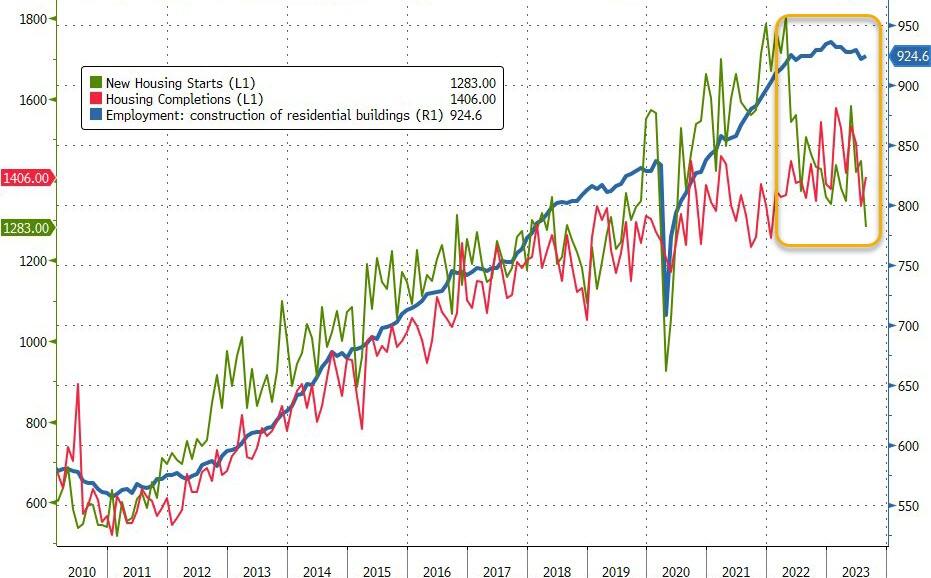

And why is construction employment still holding near its highs…

Source: Bloomberg

Will The Fed see permits soaring as homebuilders betting on their dovishness and step in tomorrow to curb-stop that optimism?

The Guns of August … Bidenomics’ guns pointed at the American middle class.

Call Bidenomics a new name: The Biden Blitzkrieg Bop since the administration launched a blitzkrieg attack on America’s middle class and low wage workers through bad energy policies and soaring inflation.

Clearly, economists were wrong earlier this year when they forecast an economic contraction that has yet to manifest. Could they be wrong now?

To be sure, economic growth, the labor market and consumer spending have proven unexpectedly resilient in the face of rising interest rates and elevated inflation. But there are still plenty of signs a recession might still be on its way.

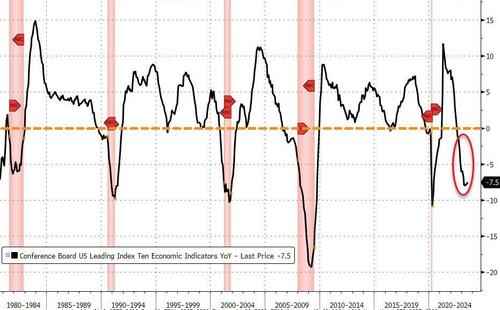

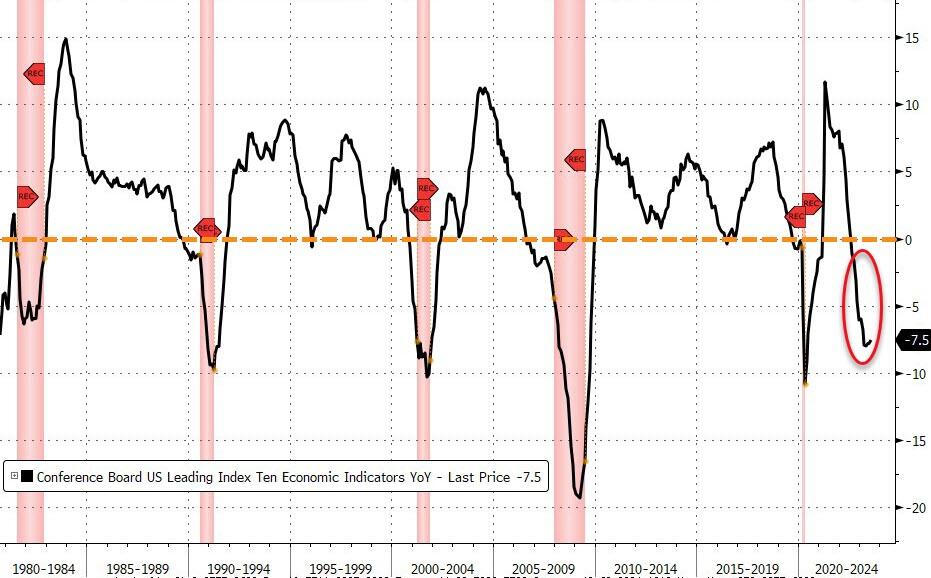

1. An “uncertain outlook” from leading indicators

Many mainstay economic indicators measure the past. So-called leading indicators reflect what likely lies ahead.

“The outlook remains highly uncertain,” said Justyna Zabinska-La Monica, senior manager of business cycle indicators, at The Conference Board.

“The leading index continues to suggest that economic activity is likely to decelerate and descend into mild contraction in the months ahead.”

The index is based on 10 components, ranging from stock prices and interest rates to unemployment claims and consumer expectations for business conditions.

2. Consumer confidence is just a hair above recessionary levels

The Conference Board’s consumer confidence index came in at 80.2 in August, hovering just above 80, the level that often signals the U.S. economy is headed for a recession in the coming year.

It is also a leading indicator used to predict consumer spending, which drives more than two-thirds of U.S. economic activity.

3. Consumers are foregoing big-ticket purchases

Retailers report that their customers have shifted their purchasing habits, spending less on furniture and other big ticket items in favor of necessities. They have also been trading down on grocery items, ditching pricier cuts of beef and buying chicken.

“We saw some switch even to some canned products, like canned chicken and canned tuna and things like that,” Costco’s Chief Financial Officer Richard Galanti told analysts on a May conference call.

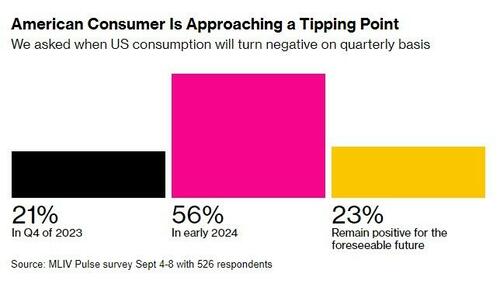

Consumer spending has remained one of the bright spots in the economy, but most investors expect consumer spending to slow by as early as next year, Bloomberg’s latest Markets Live Pulse survey found.

4. Credit cards are getting maxed out

U.S. consumers ran up their credit card debt past the $1 trillion mark for the first time last month, according to a report on household debt from the Federal Reserve Bank of New York.

Total household debt, which includes home and auto loans, has eclipsed $17 trillion.

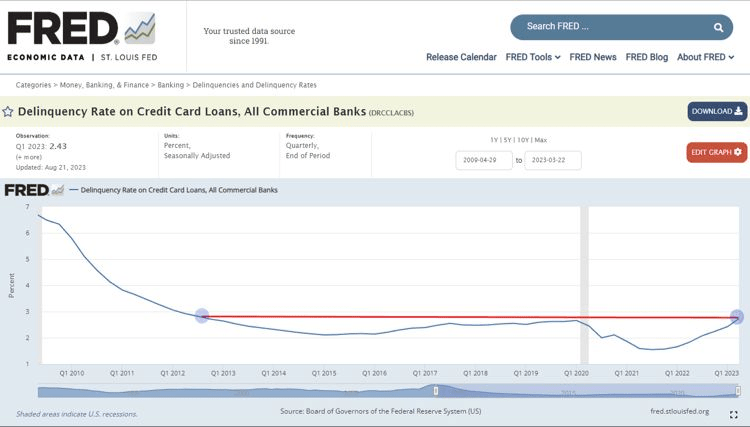

The Federal Reserve Bank of St. Louis reports that credit card delinquencies, which are still low compared to periods such as the Great Financial Crisis, are on the rise.

5. Banks are increasingly reluctant to lend

The latest Senior Loan Officer Opinion Survey by the Federal Reserve reports tightening credit conditions across the board, from business loans to home mortgages and consumer credit.

“Regarding banks’ outlook for the second half of 2023, banks reported expecting to further tighten standards on all loan categories,” the Fed survey concluded.

“Banks most frequently cited a less favorable or more uncertain economic outlook and expected deterioration in collateral values and the credit quality of loans as reasons for expecting to tighten lending standards further.”

When banks pull back on lending, businesses curb their investments and consumers cut spending, and this trend is expected to continue for at least the rest of the year.

6. Corporate bonds are maturing and refinancing them will be costly

Goldman Sachs estimates that $1.8 trillion in corporate debt is coming due over the next two years and it will have to be refinanced at higher interest rates.

The expense will eat up more corporate resources, possibly leading to slower growth and investment.

Recessions occur as debt levels peak and borrowers begin to default.

Moody’s has already reported a surge in corporate defaults this year. In the first half of the year, it counted 55, that’s 53% more than the 36 that defaulted in all of 2022.

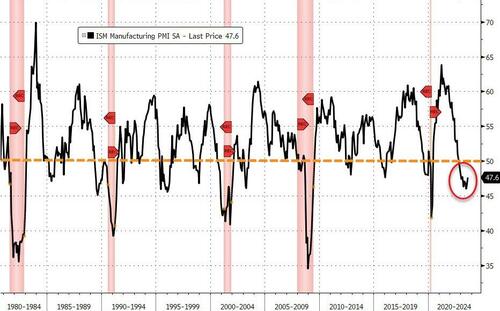

7. Manufacturing remains in a prolonged post-pandemic slump

Respondents to the ISM survey reported weaker customer demand because of higher prices and interest rates.

“Orders are in fact falling faster than factories are cutting output, suggesting firms will need to continue scaling back their production volumes into the near future,” writes Chris Williamson, chief business economist at S&P Global Market Intelligence.

“An increasing sense of gloom about the near-term outlook has meanwhile hit hiring and led to a further major pull-back in purchasing activity.”

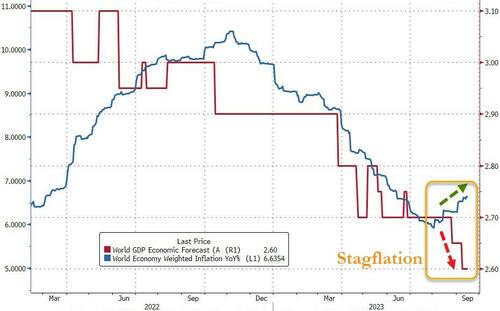

8. ‘Cascading crises’ could tip the balance of a slowing global economy

China, a growth engine for the past 40 years, is still struggling to recover from the pandemic, global economic growth has fallen below long-term average, and the ailing world could pull the U.S. economy down with it.

Like a plane crash, every economic disaster stems from a confluence of mishaps. Along these lines, G20 nations on Saturday put out a dire warning:

“Cascading crises have posed challenges to long-term growth,” the group said.

“With notable tightening in global financial conditions, which could worsen debt vulnerabilities, persistent inflation and geoeconomic tensions, the balance of risks remains tilted to the downside.”

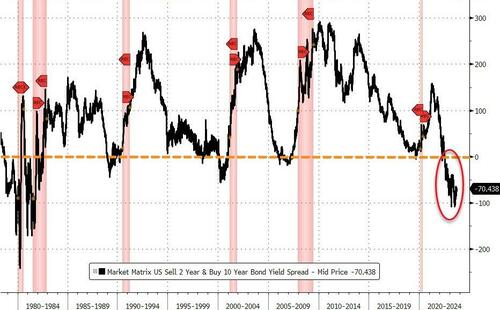

9. The yield curve, a classic recessionary signal, is still inverted

Investors should be paid more for taking a long-term risk than they should for a short-term risk. That’s why the yield on a 10-year Treasury is supposed to pay a higher yield than a 2-year Treasury.

When this is not the case, it’s called an inverted yield curve, and it has long been considered a sign that a recession is due within the next 18 months.

The yield curve for 10-year and the 2-year Treasury has been inverted since July 2022. It’s been inverted for so long that many observers have given up on its reliability — though it still hasn’t been 18 months since it first inverted.

As for history, the yield curve last inverted was in late 2019, just before the pandemic U.S. recession.

10. Inflation is sticky, and the Fed isn’t done

The soft landing scenario that is so widely embraced is based on observations that inflation has dropped precipitously as the economy continues to grow at a healthy pace and the labor market is still holding strong with the unemployment rate at 3.8%.

The Fed, which has raised interest rates 11 times since March 2022 to curb inflation, can now take a bow. The consumer price index, which measures inflation, has come down from a peak of over 9% in June 2022 to 3.2% on its last reading in July.

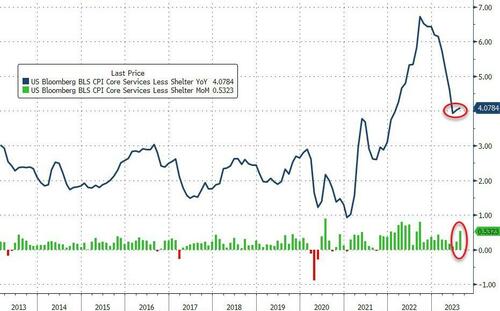

The latest reading on CPI, for August, came out Wednesday, and re-accelerated more than expected, with The Fed’s most-watched ‘Core Services CPI Ex-Shelter’ back above 4.00%…

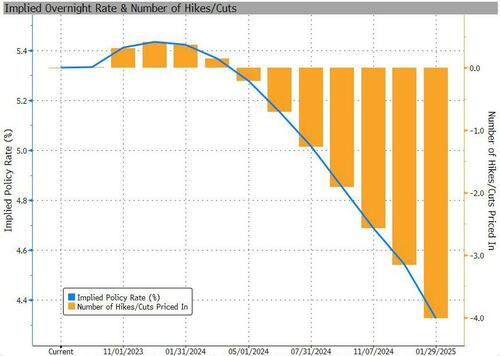

Meanwhile, the Fed, which next meets on Sept. 19-20 to decide on interest rates, is holding fast to its 2% target for inflation and will keep rates higher for longer, or possibly even raise them further to meet that goal.

Wall Street traders are not expecting another increase this month, according to the CME FedWatch tool, which is based on Fed funds futures trading.

Policy makers are still waiting to see what happens next after raising rates to their highest level in 22 years. Perhaps those actions have already sent the economy on a path of contraction. Or perhaps they haven’t done enough to continue slowing inflation.

Sticky inflation presents on ongoing risk of a recession.

“I believe we must proceed gradually,” Dallas Fed President Lorie Logan said last week, “weighing the risk that inflation will be too high against the risk of dampening the economy too much.”

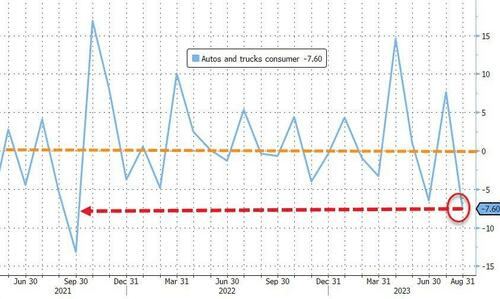

The Big Three auto companies and the UAW are suffering under Bidenomics (code for massive green energy payoffs to large donors). As I pointed out yesterday, the auto industry suffered a large decline of -7.60% in Q2 as a result of rising car prices (going electric is EXPENSIVE) and increasing consumer debt to cope with Bidenomics.

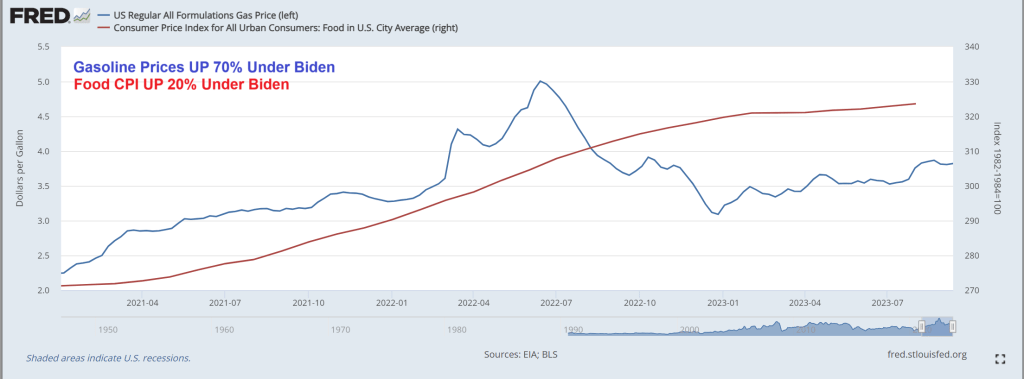

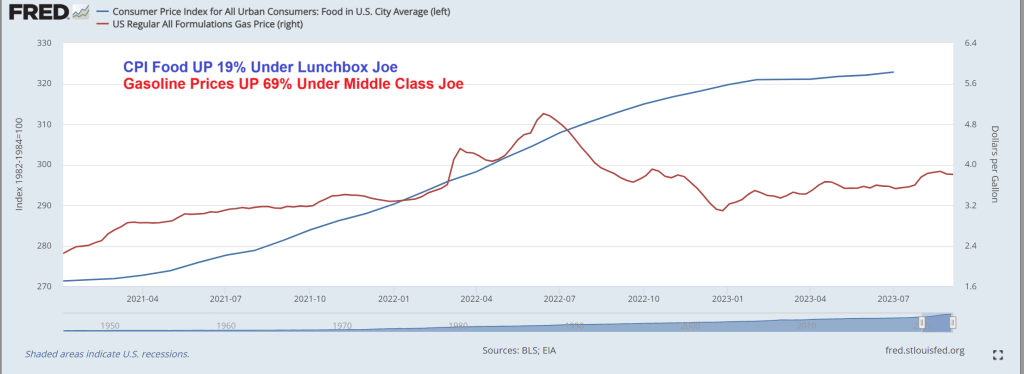

So when we consider the UAW’s demands of $20 an hour hike in pay, you have to consider that under “Union Joe” gasoline prices are up 70%, and food CPI is up 20%. So a 20% pay hike won’t even cover the cost of commuting and will just cover the increased food costs.

The shortened work week to 32 hours? How European of the the UAW.

But perhaps they will have the extra time to travel to Paris France to eat some beef au poivre at Le Bistrot Paul Bert.

Shape of things in the US economy. But a better tune to descible what is happening is over, under, sideways down.

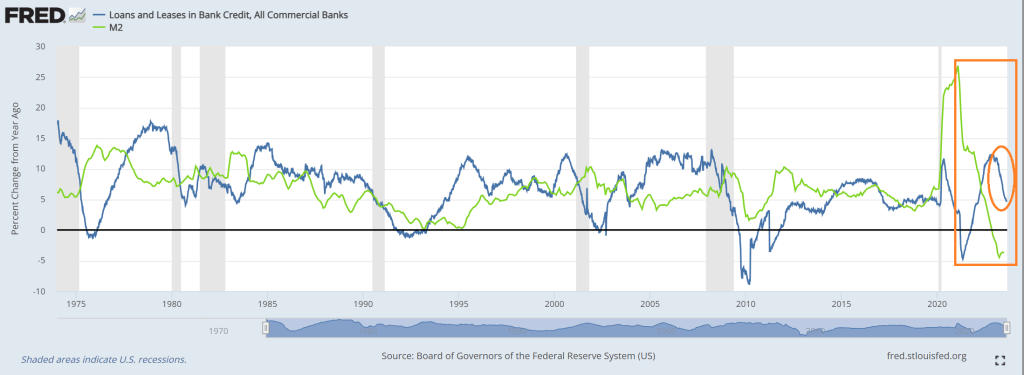

For example, look at this chart of loans and leases at commercial banks, since last year (YoY). The growth rate is plunging rapidly. Of course, M2 Money growth has already crashed.

Loan delinquenices? The trend in delinquencies is rising as consumers struggle with inflation.

When asked about future Fed policies, Powell angrily replied “I’m a man.” Just kidding, but that is almost as nonsensical as his other answers.

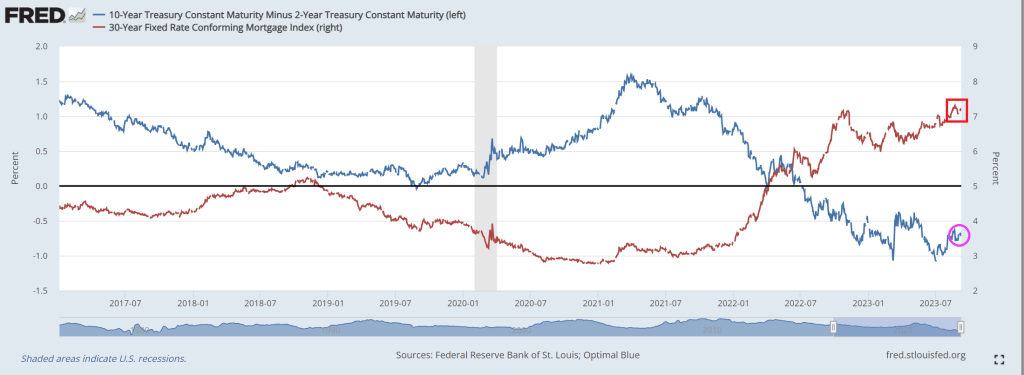

But back in the USA (while Biden does his humiliate the US tour of Vietnam, India, etc, and ignores the tragedy of the 9/11 attacks), we see mortgage rates still up above 7% as the US Treasrury 10Y-2Y yield curve

CPI food prices are up 19% under “Lunchbox Joe” and up 69% under “Green Joe”. True, the American middle class is far worse off under Bidenomics, but it is all about marketing Bidenomics at this point.

Of course, being a true RINO (Republican in name only), he won’t follow Biden around criticising him. Just critcising Trump. He is part of the Globalist Romney RINO Party (GRR).

Bidenomics is terrible! Just a huge payoff to be big donors (the donor class) for green energy, Big Pharma and Big Defense. Now Biden is considering using ankle monitors to prevent illegal immigrants from leaving Texas and traveling to welfare-friendly blue states like California and New York rather than just enforcing the border. The middle class is truly wasting away with Bidenomics.

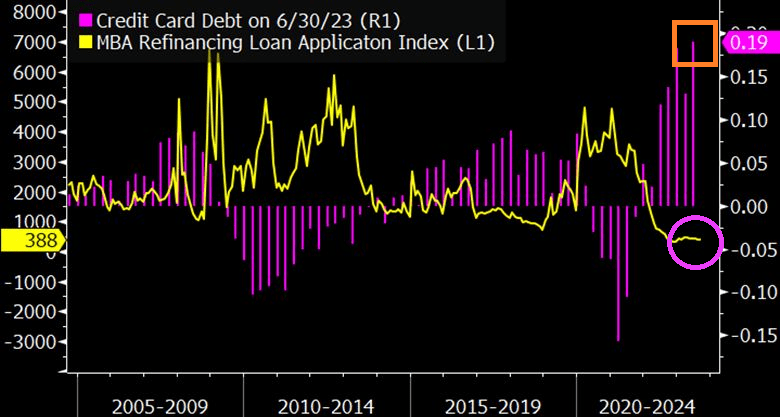

Let’s start with crashing mortgage refi demand as consumers load up on credit cards to afford rising prices thanks to Bidenomics.

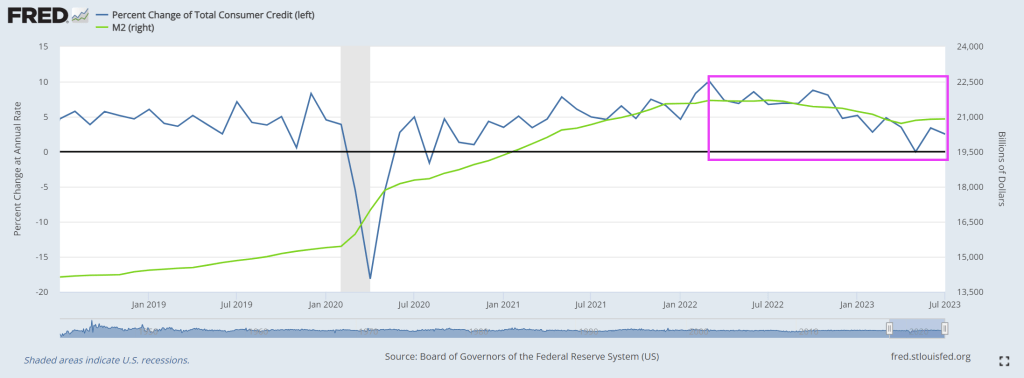

The Fed reports dramatically weakening consumer credit with negative revisions too.

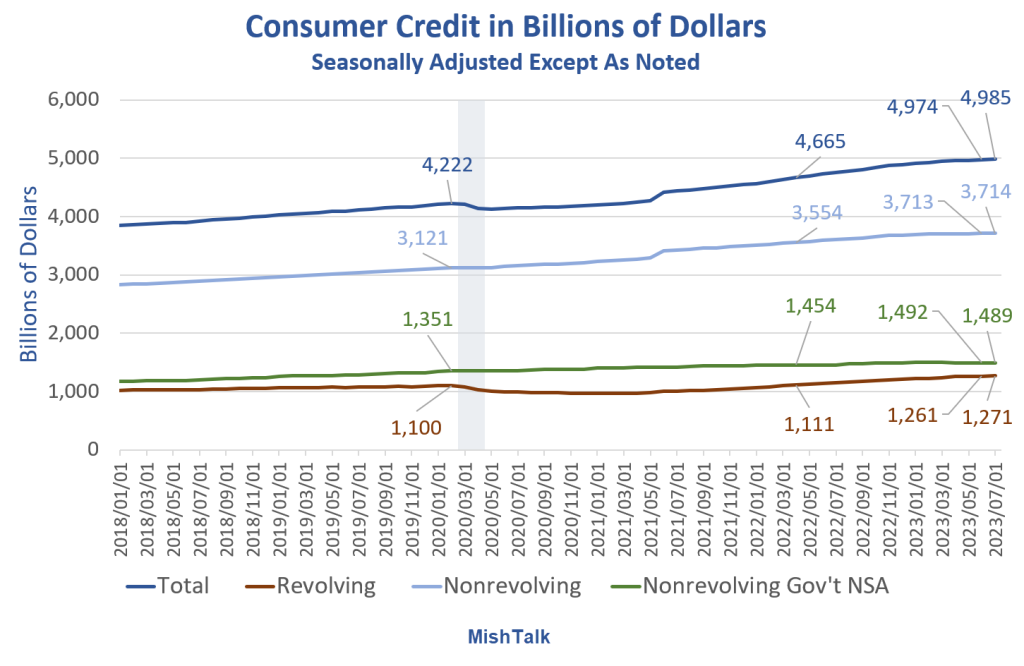

Consumer Credit data from the Fed, the last two months labeled are May and July, chart by Mish

Consumer Credit Report Revisions

Consumer Credit data from the Fed, chart by Mish

Revision Key Points

Most of the revisions are in nonrevolving, but that impacts the totals.

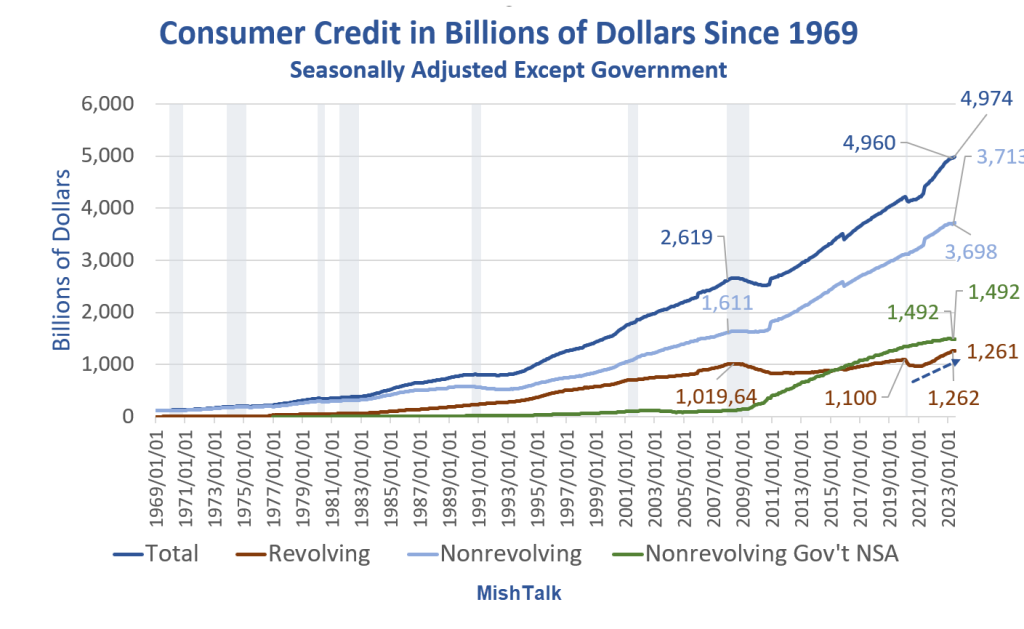

Nonrevolving credit rose $1 billion in July, from a negative $22 billion adjustment in June. The Fed revised a reported $3.735 trillion down to $3.713 trillion.

In turn, nonrevolving impacted the totals.

Total credit rose $11 billion in July, from a negative $23 billion adjustment in June. The Fed revised a reported $4.997 trillion in June down to $4.974 trillion.

Nonrevolving Consumer Credit in Billions of Dollars

Nonrevolving consumer credit data from the Fed, chart by Mish

Nonrevolving Credit Implications

Assuming the data is accurate (unlikely) or at least the revision direction is accurate (likely), mortgage and existing home sales data is suspect.

Real (inflation adjusted) nonrevolving credit peaked in June of 2021.

Consumer Credit in Billions of Dollars Since 1969

Consumer Credit data from the Fed, chart by Mish

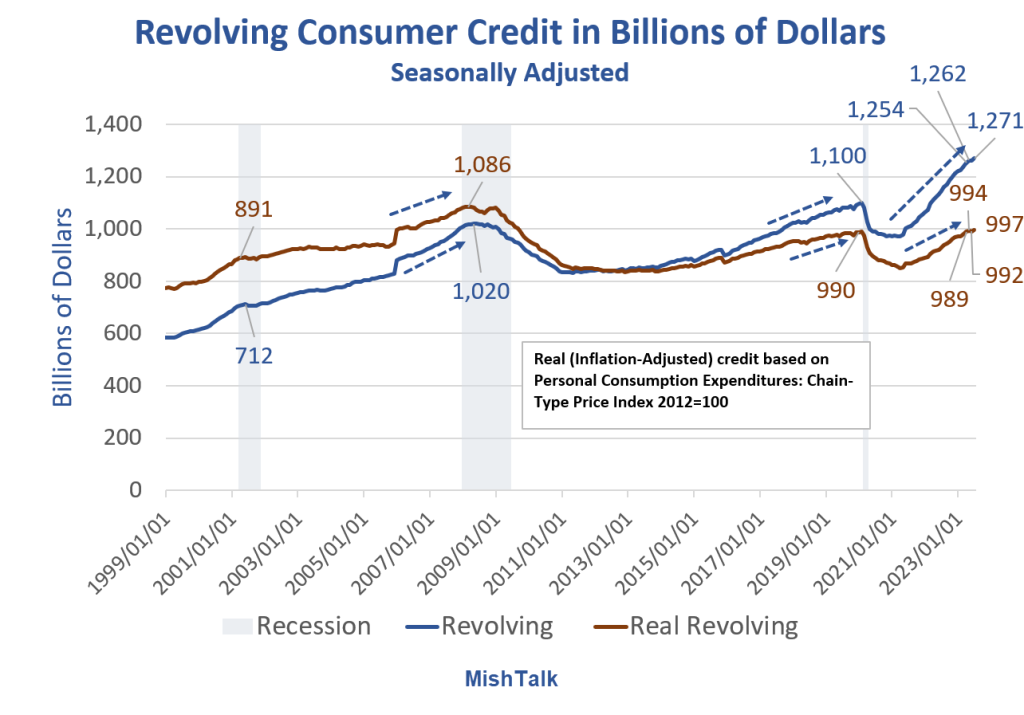

Consumers have generally done a pretty good job of avoiding credit card debt thanks to three rounds of fiscal stimulus.

However, inflation kicked in and the stimulus money has been spent. The result is the steep rise in credit card debt as noted by the blue arrow. Let’s hone in on that.

Revolving Consumer Credit in Billions of Dollars

Consumer Credit data from the Fed, Real (inflation adjusted calculation) and chart by Mish

Stunning Steepness in Credit Card Debt Accruals

The speed at which consumers are going into credit card debt is stunning.

It’s hard to maintain lifestyles with rising inflation unless wages keep up.

The BLS and Fed believe the rate of increase in inflation is falling. Assuming the data is correct, consumers are struggling anyway.

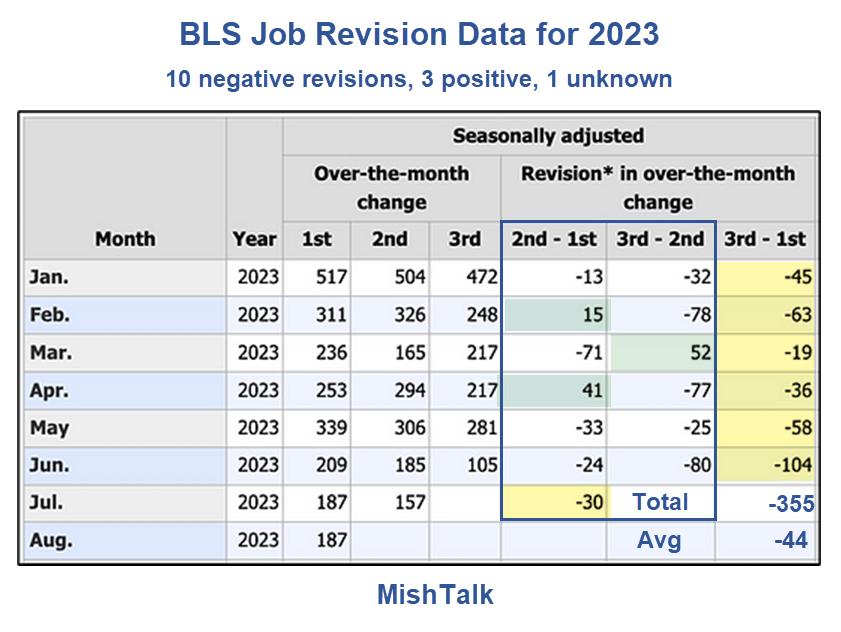

What Happens if Jobs Take a Dive?

That’s actually the wrong question. Job revisions (there’s that word again) have been steeply negative.

BLS Job Revision Data from the Philadelphia Fed

Jobs are still positive, assuming (there’s that word again) you believe the numbers and more negative revisions (there’s that word again) are not in the works.

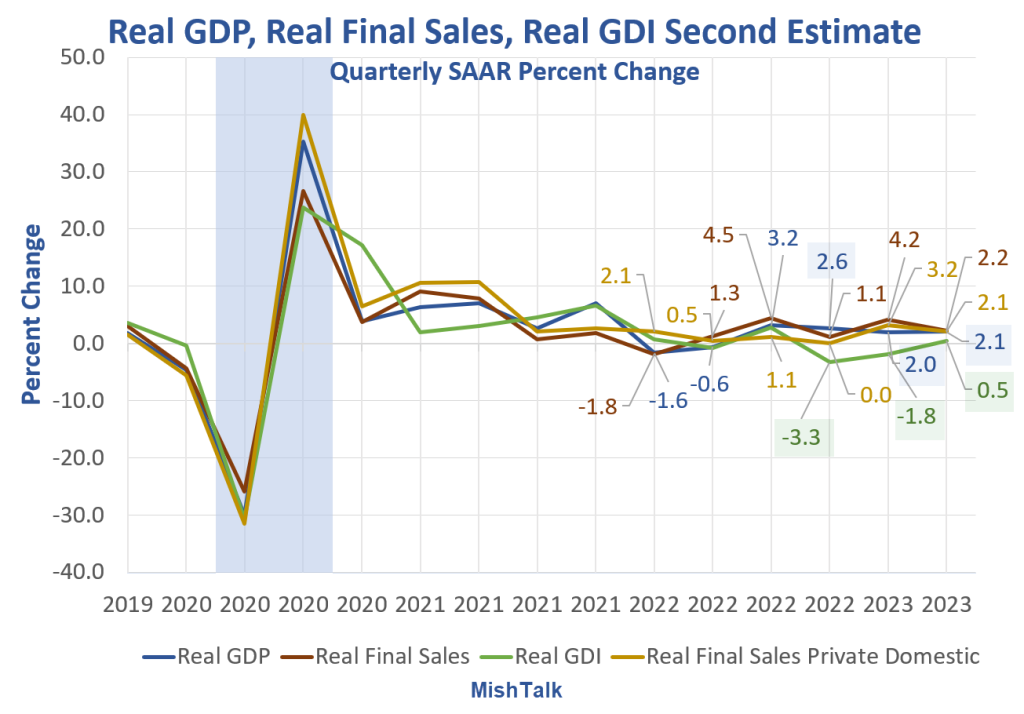

As long as you are making assumptions, if you are rah-rah on the strength of the Biden economy, you may as well assume GDP numbers are correct as well.

My assumption is GDP is flat out wrong and Gross Domestic Income (GDI) numbers are far more likely to be correct than GDP numbers. GDP and GDI are supposed to be the same but aren’t.

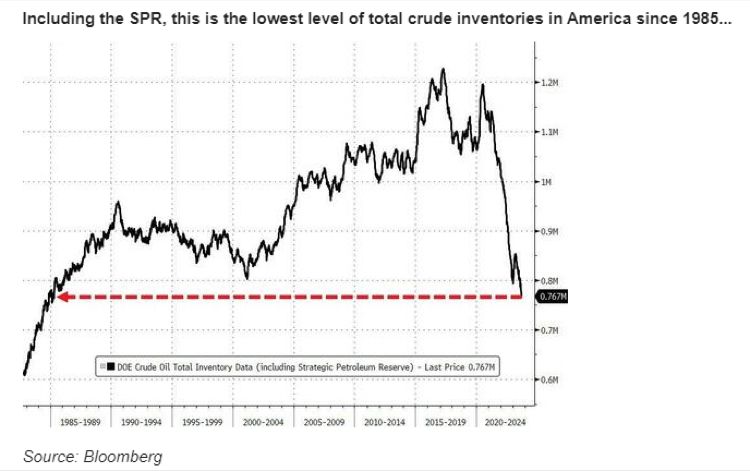

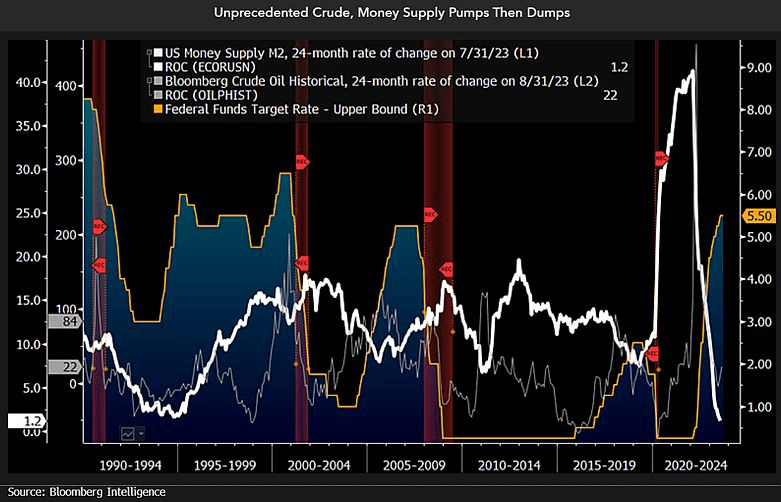

Its hard to watch Biden and The Progressive Greens destroy the enegy security of this great nation. Biden is draining the Strategic Petroleum Reserve, probably in a misguided attempt at ensuring we never go back to abundent petroleum again. Crude oil inventories are now the lowest since 1985.

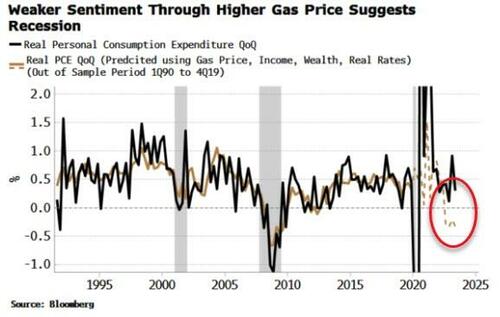

Household spending has kept the US economy afloat, but as growth slows a continued rise in oil and gas prices is poised to push personal consumption expenditure (PCE) lower and thus trigger a near-term recession – with stocks and bonds unpriced for such an outcome.

Once again it has been the redoubtable consumer that has thus far kept a recession at bay. However, Bloomberg Economics (BBE) pointed out in a recent article that negative household sentiment – in confluence with other drivers of household spending – suggests that we should already be in a recession.

A regression model (using income, wealth and real rates) pins PCE growth roughly where it is. But if we add in the University of Michigan’s Consumer Sentiment index, it indicates much weaker PCE growth and thus an economy that would likely be already be in the midst of a slump.

I recreated BBE’s model and got something similar. I then substituted in the Conference Board’s Consumer Index instead of the Michigan survey. This also improves the fit of the original model, but does not paint as negative a picture for PCE. The reason is that the Conference Board’s measure has not deteriorated as much as the Michigan survey.

Why? The divergence between the two likely comes from the Michigan’s greater emphasis on frequent expenditures and business conditions, while the Conference Board’s index is more focused on the jobs market. As an employee, the jobs market has looked pretty good, boosting the Conference Board’s index, while the Michigan survey is more influenced by rising prices and conditions for small-business holders, which have been less rosy.

The Michigan survey is in fact very sensitive to gas prices. In the model, I added the average gas price to the model’s original inputs (i.e. ex Michigan). Doing so also improves the model’s fit, and as the chart below shows, implies notably weaker, and negative, PCE growth – and therefore an economy that would likely already be in a recession.

This highlights that the US economy is potentially on thin ice, with that ice represented by hitherto positive consumer sentiment, driven in no small part by gas prices (and sentiment on how high they are perceived to be) that remain comparatively cheap to the levels they reached last year.

But oil has been rising, driven by excess liquidity, falling inventories and supply cuts.

Tailwinds remain for oil, and therefore the nascent recent rise in gas prices is poised to continue as well. That could be the final straw which unseats the US consumer and tips the US into a recession.

The US warhawks seemed focused on Ukraine’s security, but don’t seem to care about US energy security or the personal welfare associated with open borders. Just ask Mayor Adams of New York City.

What a mess Biden and his Progressive backers have made. And we are forced to suffer the consequeinces of his policies. Or follies!

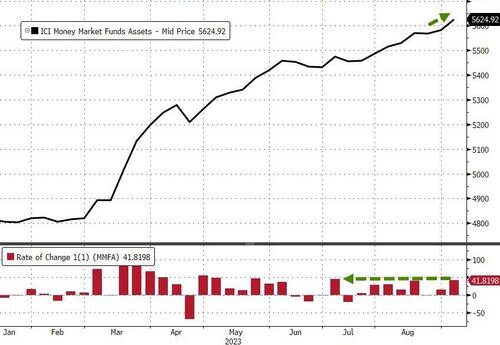

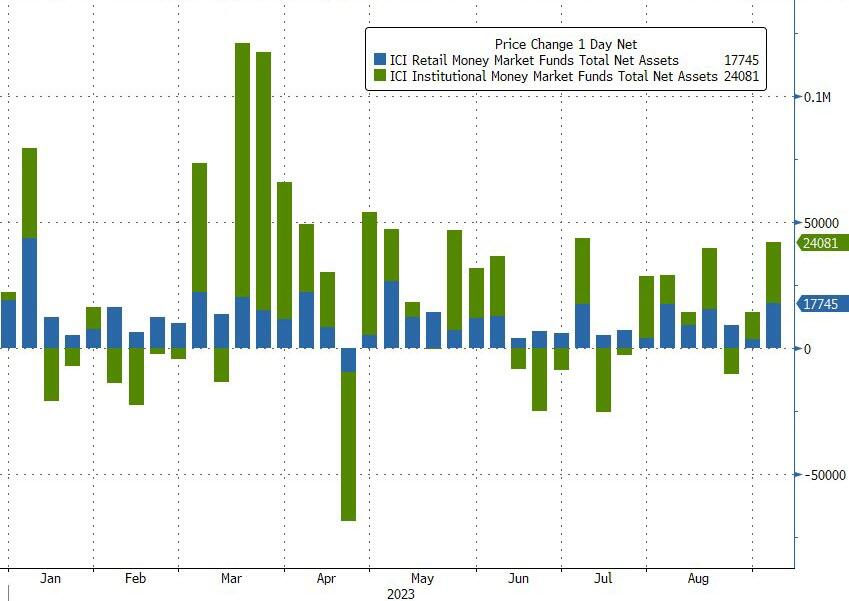

Money-market funds saw inflows for the 7th week of the last 8 with a $42BN jump (the most in 2 months) to a new record high of $5.625TN…

Source: Bloomberg

The inflow was dominated by a $24BN increase in Institutional fund assets while Retail also saw a sizable $17.7BN increase…

Source: Bloomberg

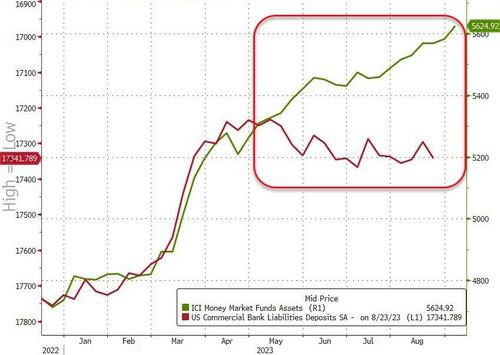

And the divergence between money-market fund assets and bank deposits continues to grow…

Source: Bloomberg

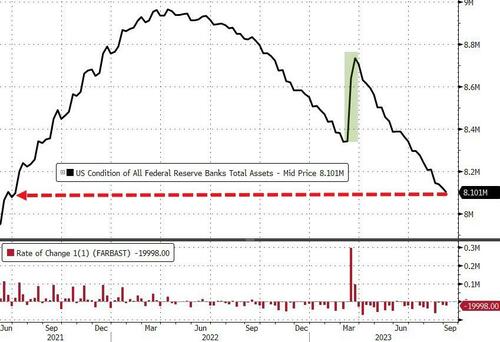

And while we actually saw huge deposit outflows (on a non-seasonally-adjusted basis) – despite The Fed’s seasonally-adjusted deposits increase – The Fed balance sheet shrank by another $20BN last week to its smallest since June 2021…

Source: Bloomberg

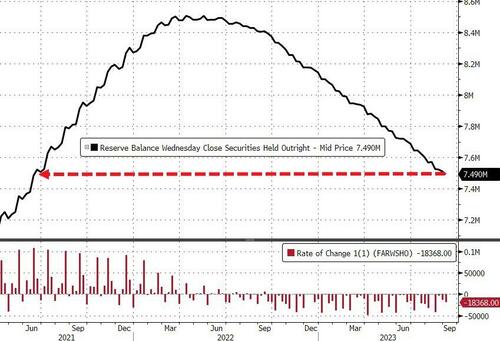

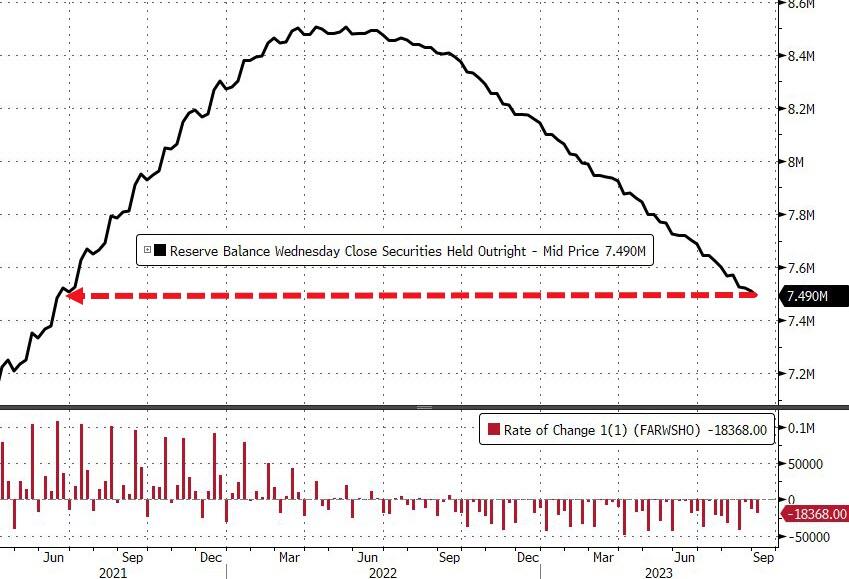

The Fed’s QT program continues apace with$18.4BN sold last week to its smallest since June 2021…

Source: Bloomberg

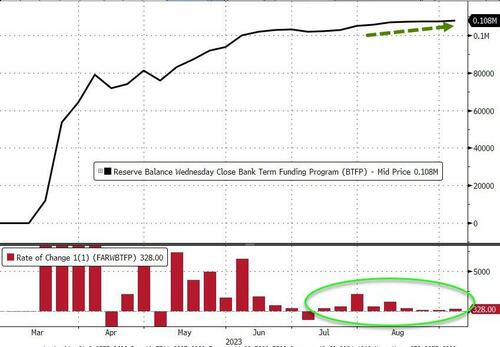

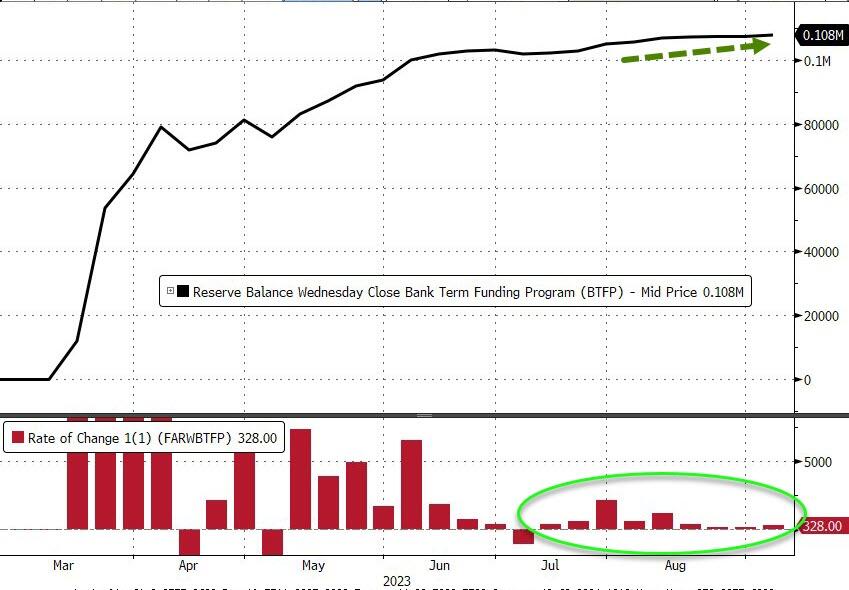

Usage of The Fed’s emergency bank funding facility jumped by $328 Million last week to a new high of $108BN…

Source: Bloomberg

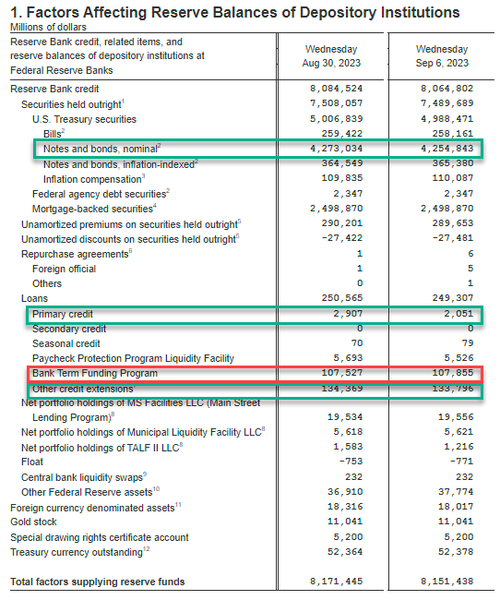

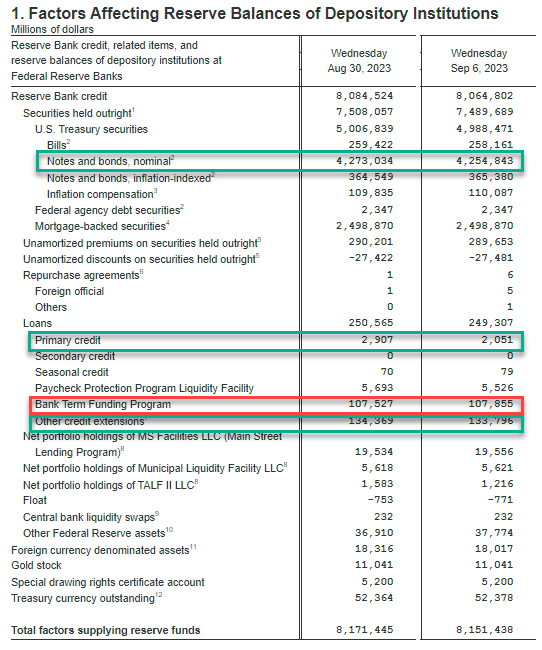

Fed BS weekly change:

Fed balance sheet QT (Notes and bonds decline): $4.255 trillion, down $18,2BN

Discount Window $2.1BN, down $800M from $.29BN

BTFP new record $107.9BN, up $400MM

Other Credit Extensions (FDIC Loans): $133.8BN, down $0.6BN from $134.4BN

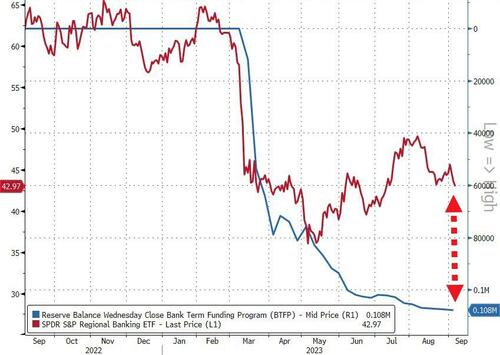

Finally, US equity markets and bank reserves at The Fed have converged a little recently, but the gap remains wide (thanks to the plunge in reverse repo balances)…

Source: Bloomberg

Tick, tock, banks!

Source: Bloomberg

You have six months to figure out how to clean up the $108 Billion hole in your balance sheet that you’re currently paying The Fed’s exorbitant rates to fill.

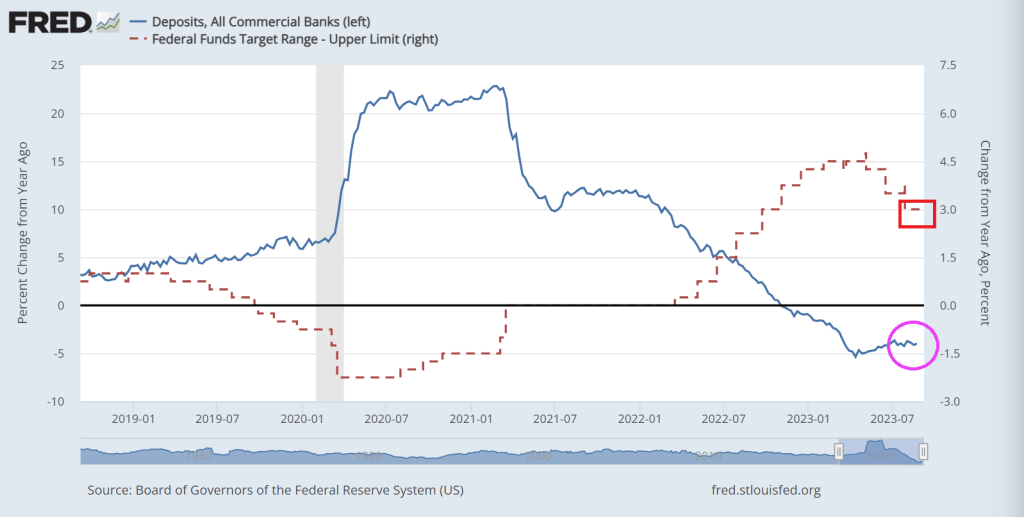

Bank deposit growth remains negative as The Fed tightens its overly accomodative monetary policy.

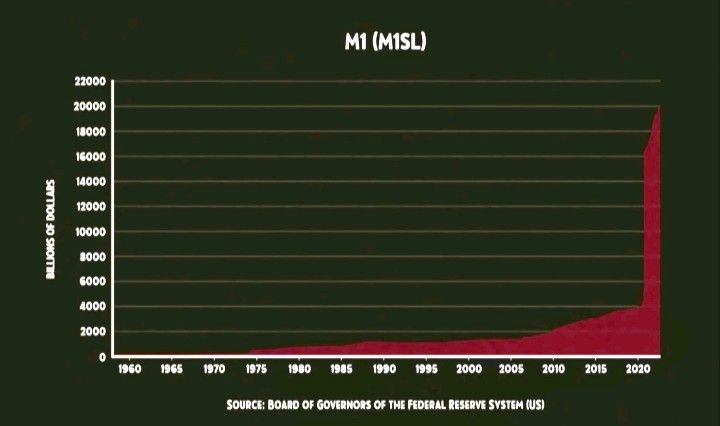

And then we have this chart showing plinging M2 Money (white line fever).

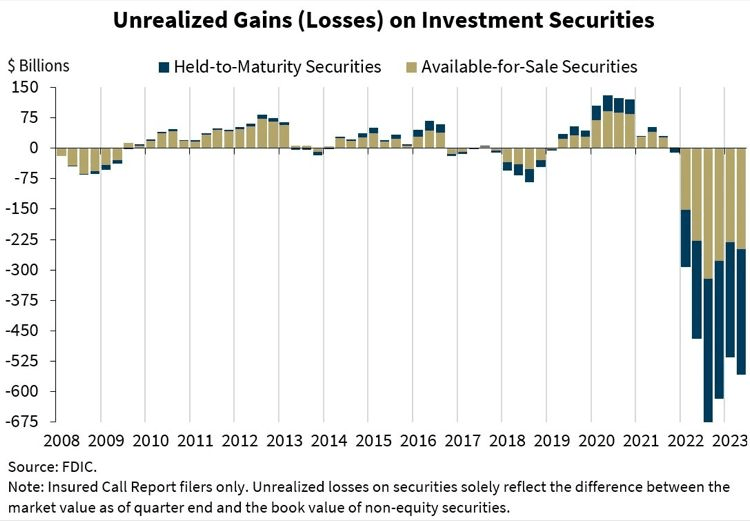

And the horrific unrealized losses on bank’s books.

Bidenomics is failing America. Primarily because Biden was one of the stupidest members of the US Senate. Not to mention nasty. Great President, America! /sarc

As Bidenomics fails to do anything other than make big donors wealthier (green energy companies, big tech and union bosses, etc), we are seeing the impacts of Fed monetary tightening to combat inflation caused by Biden/Pelosi/Schumer’s spending spree.

First, the 10-year REAL Treasury yield is close to breaching 2%.

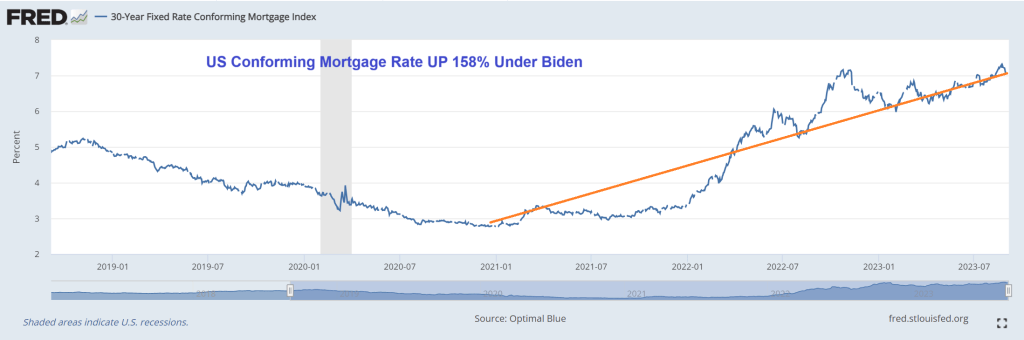

Second, 30-year mortgage rates are now 7.62%, up over 150% under Bidenomics.

Third, mortgage purchase applications crashed to the lowest level since 1995.

Fourth, the 2-year Treasury yield just breached 5%.

Fifth, the 10Y-2Y yield curve remains deeply inverted.

Thanks to Bidenomics, code for massive Federal spending on green energy initiatives and payoffs fo large donors, we have agonizing inflation and consumers are borrowing more and more to cope with inflation. And with the increased use of debt comes …. drumroll … delinquenices!

The US conforming mortgage rate is UP 158% under Bidenomics.

Let’s move on to some forms of consumer loans, where the story is a little more daunting.

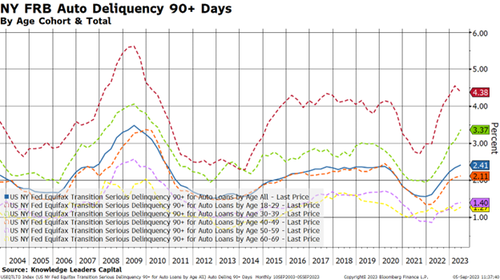

Auto loans are definitely the epicenter of the credit cycle. While the overall average is a still somewhat tame 2.41%, younger borrowers are not keeping up. Younger borrowers have delinquency rates that are 1-2% higher than the average while the inverse is true for older borrowers. Eighteen-to-thirty-nine year-old borrowers have the highest delinquency rate in 13 years.

Somehow, I sense that used car lots are going to start filling up again as these vehicles get repossessed. This should put downward pressure on used car prices, bringing that element of inflation down. This is one of the channels through which monetary policy works.

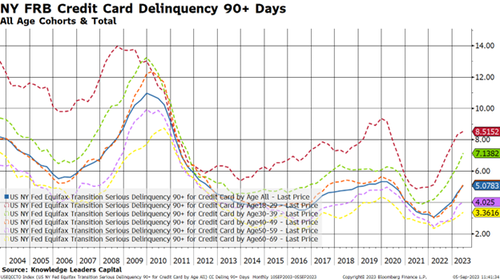

Lastly, I’ll take a look at credit card delinquencies.

Here is where we can really see the stresses building.

First, the overall delinquency rate has about doubled from 2.5% to 5% over the last couple years.

Second, older borrowers have seen a tick up in delinquency rates, a feature we don’t really see in other credit products.

Third, one in 12 younger 18-29 year-old borrowers are 90+ days late making their credit card payments.

Credit Card Delinquency Rate across all commercial banks hit 2.77% in the 2nd quarter, the highest level in more than a decade.

In conclusion, we are in the early days of a consumer credit cycle. Younger borrowers are the weakest link in this analysis, and this makes me wonder where rates go when student debt payments turn back on at the end of the month.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.