Nobody but Biden could so handicap an economy with horrible fiscal policies, massive debt, inflation and open borders. And then go to the Virgin Islands for yet another taxpayer paid vacation. Biden has spent 40% of his Presidency on vacations.

Bidenomics is a disaster for the US middle class. And Bidenomics with its inflation has led The Fed to counterattack and raises interest rates, leading to losses for The Federal Reserve (which is paid for by US Treasury) of over $130 billion.

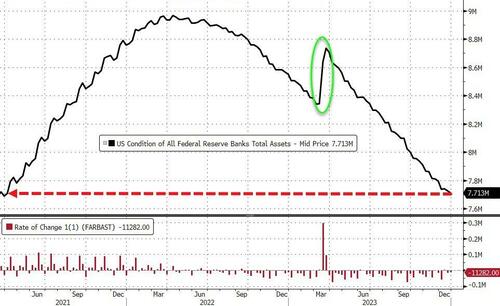

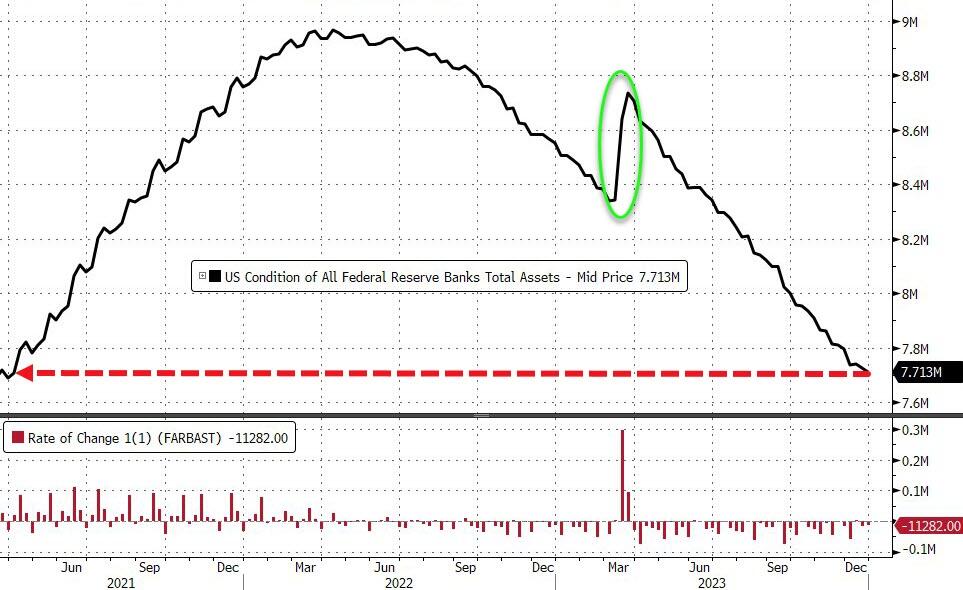

The Fed’s balance sheet shrank by $11.3BN last week to its lowest level since March 2021, but still remains elevated.

Source: Bloomberg

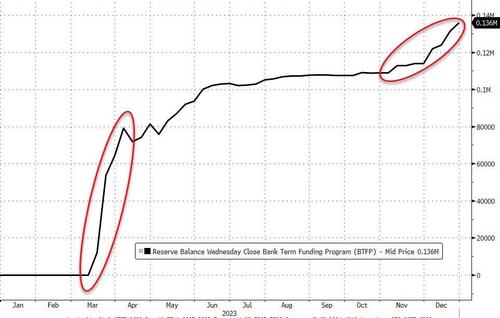

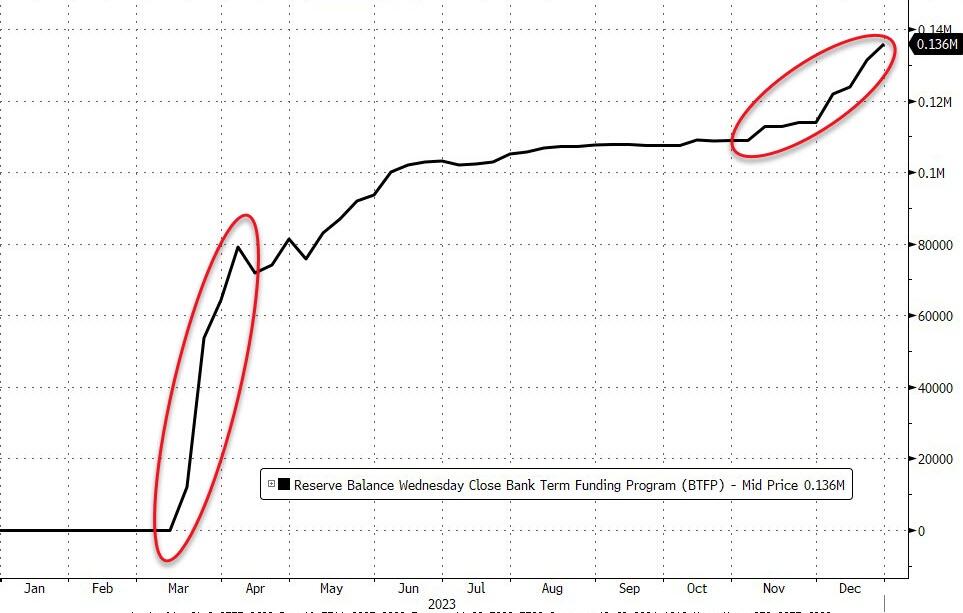

Usage of The Fed’s bank bailout facility rose by another $4.5BN last week to a new record high of $136BN…

Source: Bloomberg

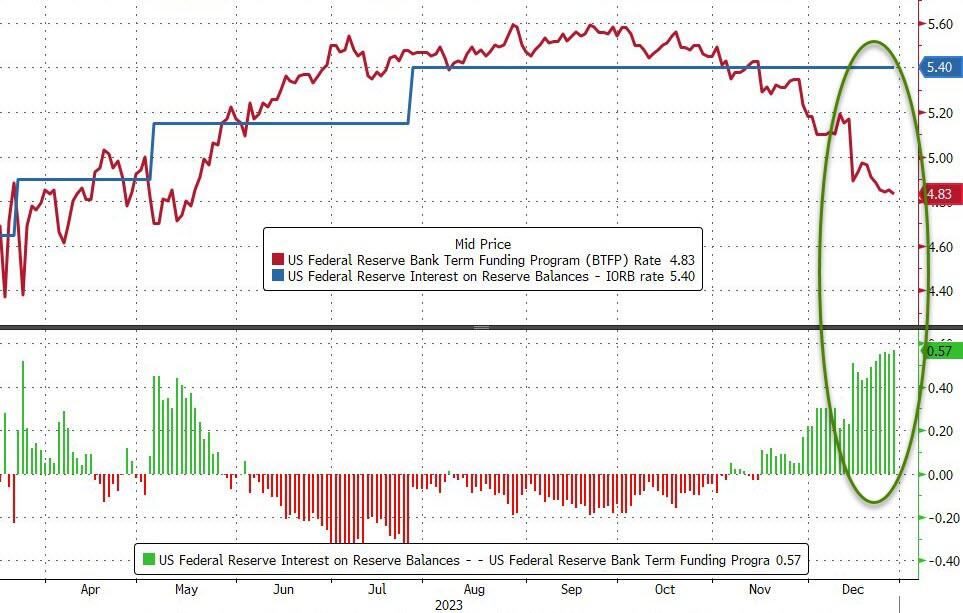

The BTFP-Fed Arb continues to offer ‘free-money’ (and usage of the BTFP has risen by $26.7BN since the arb existed):

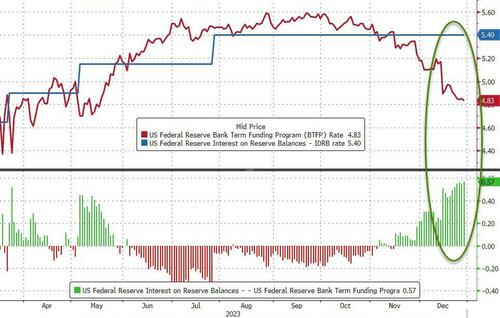

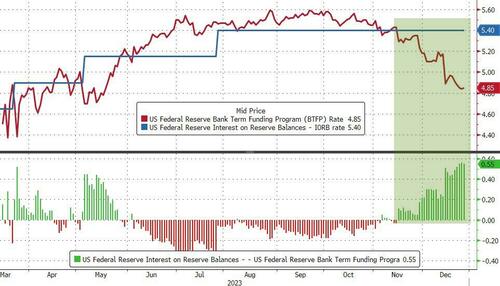

The rate on the Fed’s Bank Term Funding Program – which allows banks and credit unions to borrow funds for up to one year, pledging US Treasuries and agency debt as collateral valued at par – is the one-year overnight index swap rate plus 10 basis points.

That figure is currently 4.83%, down from 5.59% in September.

For institutions that have an account at the Fed, they can borrow from the BTFP at 4.83% and park that at the central bank to earn 5.40% – the interest on reserve balances.

Source: Bloomberg

The 57bp spread is the widest level since the Fed introduced the facility to support a struggling banking system after the collapse of California’s Silicon Valley Bank and Signature Bank in New York.

After witnessing three of the four largest bank failures in U.S. history in 2023, the attention of the media and the markets has turned elsewhere. Banking crisis? It is as though it never happened. Having fallen by some 40 percent in March, the NASDAQ Bank Index has recovered to within 15 percent of its high from February. In the last few months, nearly all markets have gone on a bull run, including bank stocks.

Yet, and despite the relative quiet, the banking sector is not in great shape. Here are some of the reasons why.

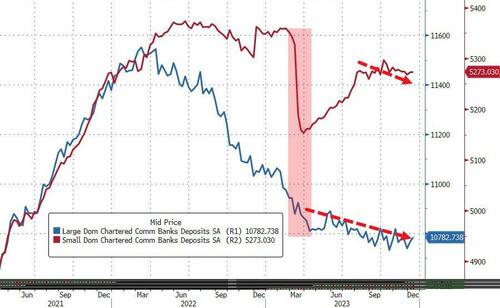

Banks continue to lose deposits. According to data from the Federal Deposit Insurance. Corp. (FDIC), U.S. banks have now lost deposits for six consecutive quarters. While the pace has slowed from the first quarter of 2023, in which nearly $500 billion of deposits were removed from the banking system, approximately $190 billion of deposits have been withdrawn in the last two quarters. Indeed, U.S. banks have lost a net $1.1 trillion of deposits since the beginning of 2022 when interest rates began to rise.

With customer deposits growing scarce, U.S. banks are instead relying on emergency funding lines from the Federal Reserve Banks and the Federal Home Loan Bank (FHLB) system. FHLB bond capital raising, of which the proceeds are used to fund the banks, is up 89 percent year over year through November and looks set to reach $1.1 trillion for 2023. Use of the Bank Term Funding Program, the emergency line put in place by the Fed in March 2023, reached an all-time high last week at $131.3 billion.

This does not reflect normal market operations.

This is a sign that the bank funding markets aren’t operating properly, and that the regulators are stepping in to help prop up the system.

The growing gap between the rate on the Federal Reserve’s nascent funding facility and what the central bank pays institutions parking reserves suggests officials will let the program expire in March, according to Wrightson ICAP.

“In justifying the generous terms of the original program, the Fed cited the ‘unusual and exigent’ market conditions facing the banking industry following last spring’s deposit runs,” Wrightson ICAP economist Lou Crandall wrote in a note to clients.

“It would be difficult to defend a renewal in today’s more normal environment.”

What happens then?]

So much for the liabilities side. But banks face challenges on the asset side as well.

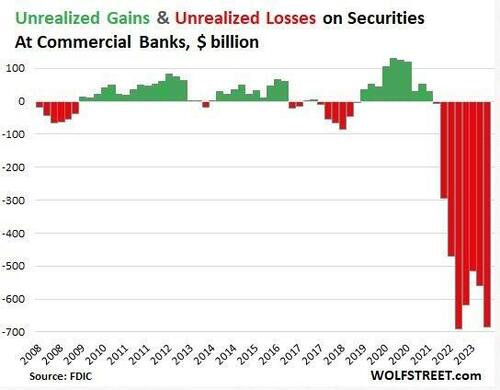

Unrealized losses on investment securities, which is the same problem that got SVB into trouble a year ago, continue to rise. U.S. banks reported unrealized losses of over $684 billion in the third quarter, up 22 percent from the second quarter. Of these unrealized losses on securities, $294 billion are categorized as available for sale (AFS), as opposed to held to maturity (HTM), whereby the bank intends to hold the asset and (hopefully) recapture principle at the end of the term. The high amount of AFS suggests that if interest rates remain “higher for longer,” then a portion of these losses will begin to realize in 2024 as they are sold by the banks. This will pressure profitability and capital levels.

Net income is declining across the banking system generally, but particularly among the smaller community banks. Credit quality is deteriorating, but has not yet reached crisis level. Commercial real estate continues to drive the increase in problem loans.

To grow (or at least slow the decline) of deposits, banks are going to have offer rates that are somewhat competitive with money market funds (considering that bank deposits are insured by the FDIC and thus relatively safe), and that offer positive real (i.e., after inflation) returns. With inflation persisting in the range of 3–4 percent, this means that banks will have to offer 4–5 percent to be relevant. This isn’t going to work for the banks. They won’t be able to maintain profitability. And it won’t work for the U.S. Treasury, which itself is committed to trillion-dollar bond issuances each quarter, which also must offer a positive interest rate above investor perceptions of inflation and the deteriorating fiscal condition of the U.S. government.

If funding costs rise further, or if unrealized losses begin to realize, banks will start taking hits to their capital levels. This will spook the markets, including depositors, and we may find ourselves in round two of deposit runs. To head off these challenges, some banks are looking to merge. There have been 78 bank deals announced in the second half of 2023, mostly among the smaller and community banks. But this won’t work in many situations where the result is the proverbial “two drunks holding each other up.”

Investor optimism is permeating markets going into year-end, with most all asset classes continuing to rise. But we must not lose sight of the banks. They are not out of the woods yet. While there is a “goldilocks” scenario in which the banking sector makes a soft landing, the risk of another set of bank failures in 2024 remains meaningful.

And we have 21 straight weeks of negative growth in bank credit. And The Fed still has a staggering amount of financial stimulus outstanding.

With all hell breaking loose around the world, President Biden has gone on yet another vacation, this time to the Virgin Islands to stay at the home of a big donor. But his handlers run things, not Vacation Joe.

C’mon Joe. The media has always reported bad news. Warm and fuzzy doesn’t anger people, but bad news does! And under Bidenomics, there has been a lot of bad news.

President Biden railed against corporate media before he and several family members headed by helicopter to Camp David, the presidential retreat in the mountains of western Maryland.

Before boarding the presidential helicopter, Biden was asked by one reporter: “What’s your outlook on the economy next year?”

The president responded: “All good,” adding, “Take a look. Start reporting it the right way.”

Sounds like Biden watched the Travola/Jackson flick “Basic” where the infamous line was uttered “Tell the story right.”

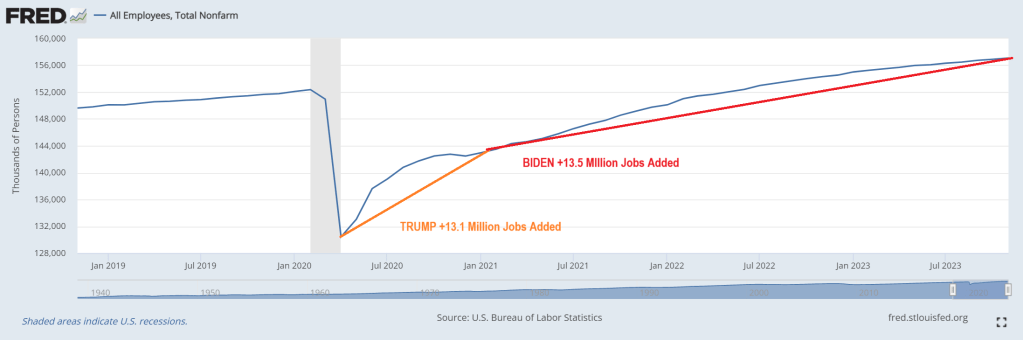

OK Joey, let’s tell the story right. After the horrendous economic shutdowns of local economics and schools in 2020, 15.1 million jobs were added after the shutdowns ended in just 10 months. Wow, that was simple! But under Biden’s Reign of Economic Error, only 15.5 million jobs were added over the next 34 months.

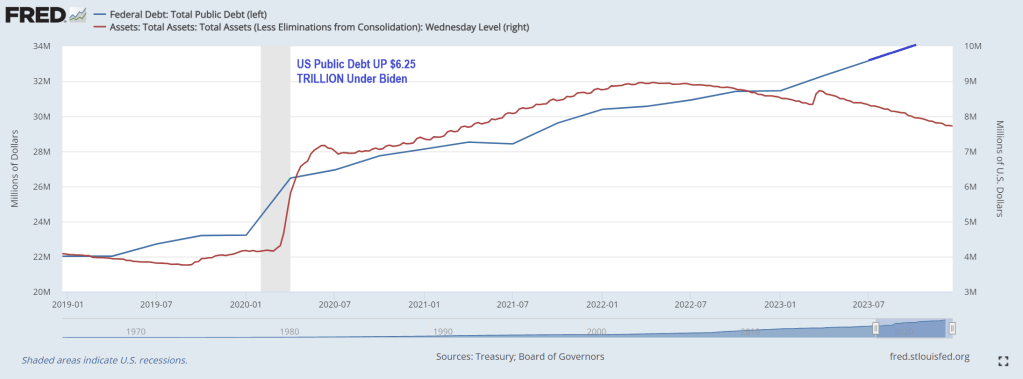

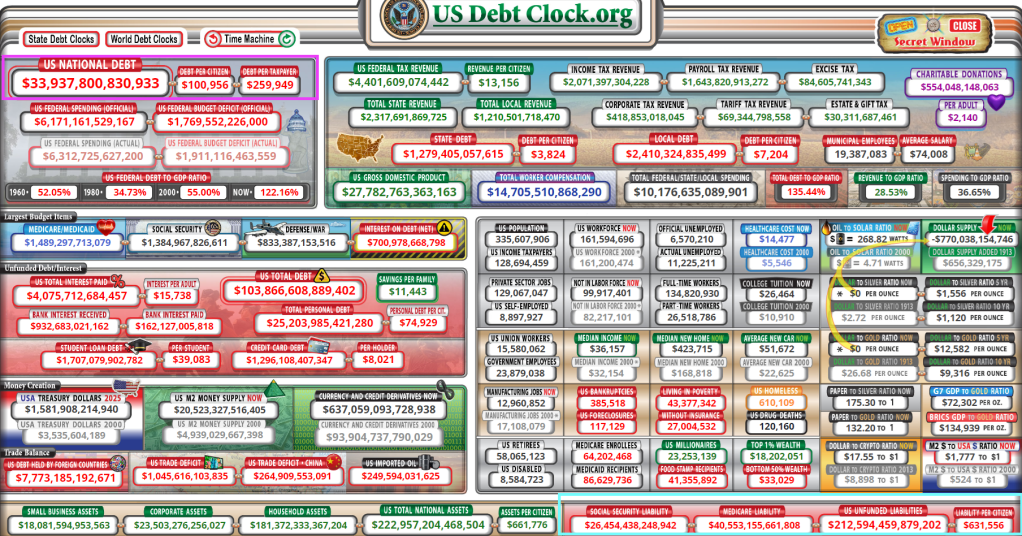

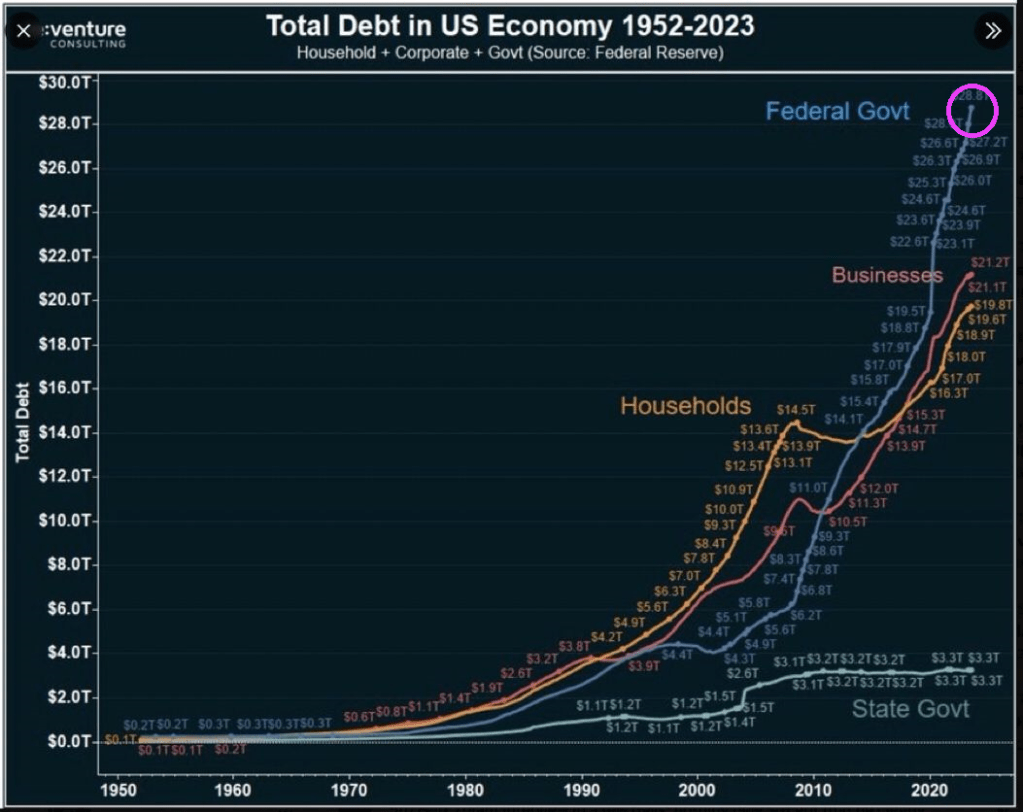

But Biden’s record on jobs comes at the expense of an additional $6.25 TRILLION IN PUBLIC DEBT.

With $34 trillion and rapdily growing debt and budget deficits, it is hard to find good news about Bidenomics.

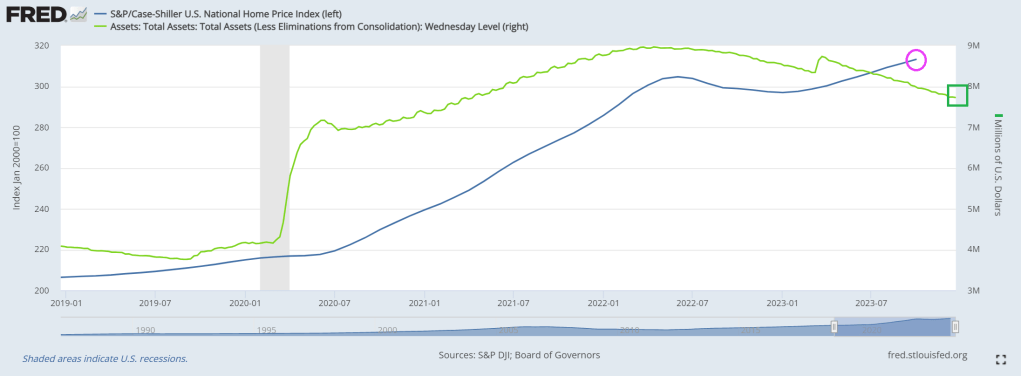

So much for “The Fed killed inflation” narrative. Inflation is still alive and well in housing prices. Particularly in cities like Miami and Detroit? Maybe the Lions winning their division for the first time in 30 years helped!

The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, reported a 4.8% annual change in October, up from a 4% change in the previous month. The 10-City Composite showed an increase of 5.7%, up from a 4.8% increase in the previous month. The 20-City Composite posted a year-over-year increase of 4.9%, up from a 3.9% increase in the previous month. Detroit reported the highest year-over-year gain among the 20 cities with an 8.1% increase in October, followed again by San Diego with a 7.2% increase. Portland fell 0.6% and remained the only city reporting lower prices in October versus a year ago.

The Case-Shiller National Home Price index was up 4.8% in October as The Federal Reserve keeps its monstrous foot on the balance sheet pedal.

Home prices in America’s 20 largest cities rose for the 9th straight month in October (the latest data released by S&P Global Case-Shiller today), up 0.64% MoM (slightly better than the +0.60% MoM expected).

That pushed the YoY rise in prices up 4.87% – the fastest pace since Dec ’22…

Source: Bloomberg

…but as the chart shows the MoM gains are slowing rapidly.

“U.S. home prices accelerated at their fastest annual rate of the year in October”, says Brian D. Luke, Head of Commodities, Real & Digital assets at S&P DJI.

“We are experiencing broad based home price appreciation across the country, with steady gains seen in nineteen of twenty cities.”

Miami and Detroit saw the biggest MoM gains while the West Coast dominated the MoM price declines with San Francisco, Portland, and Seattle worst.

But, judging by the resumption of the rise of mortgage rates since the Case-Shiller data was created, we would expect prices to also resume their decline…

Source: Bloomberg

So prices are up, mortgage rates are actually falling again now (lagged)… so The Fed is re-blowing the same bubble?

Well, at least Detroit is near the top! Playing in Rocket Mortgage stadium.

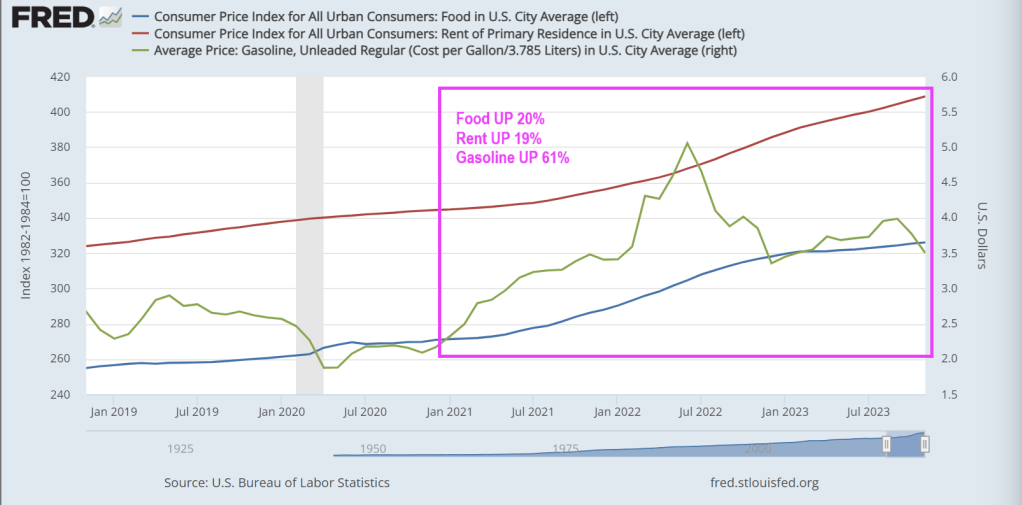

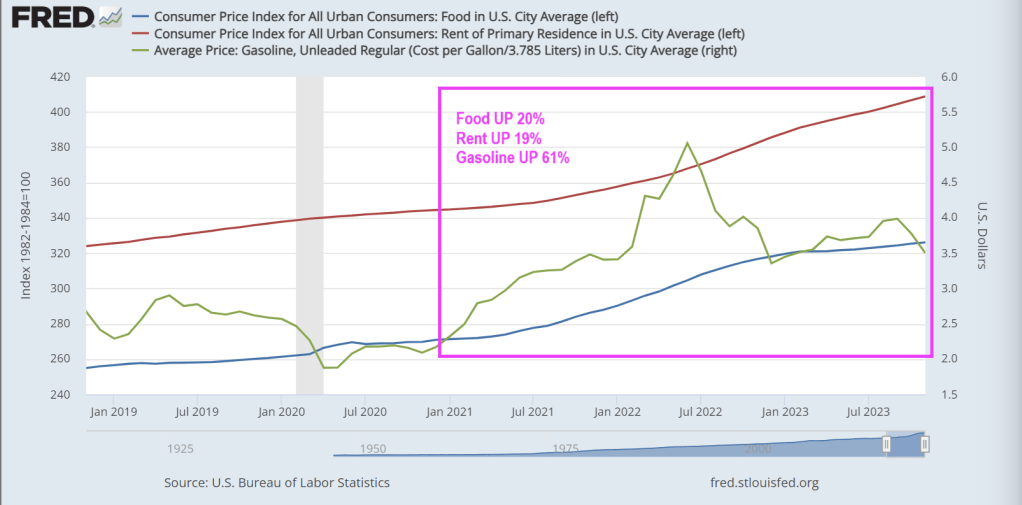

The ‘Misery Index’ is near its lowest level since pre-COVID, but Misery Index masks the true horrors of Bidennomics: 20% higher food prices, 19% higher rents and 61% higher gasoline prices under Bidenomics.

The sum of U.S. unemployment and inflation – known as the “misery index” – fell to 6.8% in November from 7.5% the previous month. That’s the lowest since the summer and fast approaching pre-Covid levels.

The misery index is calculated by adding up the current unemployment rate (3.7%) and the inflation rate (3.1%). The formula provides a simple way to gauge whether the well-being of Americans is improving or not.

Misery peaked in April 2020 when the index spiked to 15%, the highest since 1982. Conditions have improved since the early onset of Covid, but it hasn’t been smooth sailing.

After falling back to 7.7% in January 2021, the index re-accelerated over the next two years as inflation surged. The misery index was 12.5% in June 2022—the same month that annual inflation hit 9.1%.

The unemployment component of the index has been faring well since Covid emergency measures were lifted back in 2021. The unemployment rate has remained below 4% for nearly two years—even as the economy begins to slow.

But economists warn that the misery index doesn’t offer a complete picture of how the average American is doing.

You can tell just by asking them how they feel about the economy and personal finances.

How do Americans really feel?

Economist Greg Ip, who heads economic commentary at The Wall Street Journal, compared the misery index to the University of Michigan’s consumer sentiment index—one of the most closely-watched consumer surveys.

“Based on historic correlations, sentiment has been more depressed this year than you would expect given the level of economic misery,” Ip wrote, arguing that consumers are more pessimistic than the misery index would suggest.

A deeper dive into the sentiment data reveals that Americans are still frustrated about inflation and the impact of high interest rates on their finances. And while the consumer sentiment index rose in December—breaking a four-month skid—some economists attributed it to a temporary holiday boost ahead of Christmas.

“Consumer spirits are perking up for the holiday season which is a sign Christmas is still coming this year,” said Christopher Rupkey, chief economist at FWDBONDS, a New York-based financial research company.

A separate sentiment survey from LSEG/Ipsos paints an even less enthusiastic picture of the average consumer.

The December primary consumer sentiment index—which measures Americans’ attitudes toward jobs, investments, the economy, and personal finances—declined from November and was only up slightly compared to 12 months earlier.

According to the survey, attitudes toward the current situation, investments, and jobs “showed significant declines this month.”

The impact of cumulative inflation

As Creditnews Research reported in a recent study, Americans aren’t celebrating the slowdown in inflation because they’re still reeling from the cumulative price increases of the past three years.

While inflation has fallen to 3.1%, consumer prices have increased by a cumulative 19% since the start of 2020. Food prices are up a whopping 25% over that period.

Americans spent the better part of two years—April 2021 to January 2023—seeing inflation grow faster than their paychecks. That trend reversed in February of this year.

But even with stronger purchasing power this year, the vast majority of Americans (92%) said they reduced their spending in the six months through September, according to a Morning Consult survey for CNBC.

A majority of respondents across all wage brackets said current economic conditions negatively impacted their finances.

So, while the Misery Index indicates that the inflation RATE has slowed, it masks the fact that Americans are far worse off under Bidenomics.

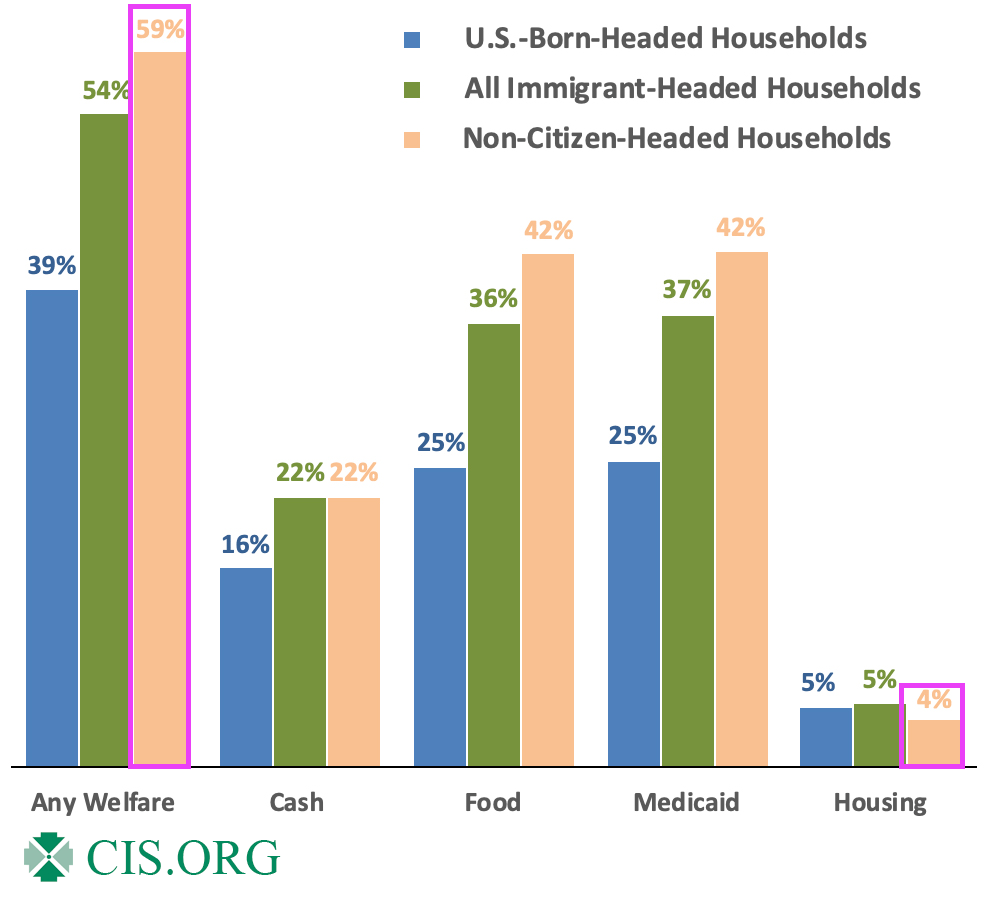

Biden is lucky in that many portray him as a senile, dumb US Senator who happens to be President. Perhaps Biden is actually insidious allowing for open borders in the hopes of crashing the US economy by overloading the welfare system and driving national debt through the roof?

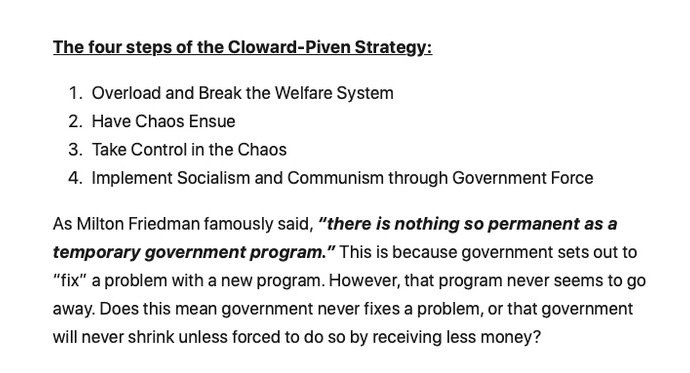

Biden, like Clinton and Obama before him, has been a Cloward-Piven discipile. Who are Cloward and Piven you ask? Two sociologists at Columbia University. (Cloward pass away in 2001, while Piven is still living). Here are Cloward and Piven attending the Voter Registration (aka, Motor Voter Law) Act signing by President “Willie Slick” Clinton.

The Cloward-Piven strategy is to overload the welfare system to the point of chaos, take control and implement Marxism through government force. To that extent, Biden and his incoherent sidekick, Kamala Harris, have been wildly successful. Sociology and Political Science are two of the most worthless college degrees (with Management in the Business School being a close third). Taking advice from Sociologists or Political Science majors or faculty is insane.

Biden should be familiar to Latin American, African and Chinese immigrants who are used to Marxist dictators who try to have their political opponents taken of the ballots and prosecucted.

Yes, the US welfare rolls are overflowing with illegal immigrants and unfunded liabilities are out of control. Perhaps Biden and Harris should be replaced with Cloward and Piven (even though Cloward is dead). But Newsom, Hillary Clinton and Michelle Obama share the idiocy of the Columbia sociology faculty members. Hillary even teaches a course at Columbia!

What about compassion for immigrants? Great! Let’s close the borders and return to LEGAL immigration to halt human trafficking, Fentanyl imports, and cartels controlling the border. But Cloward-Piven’s strategy is best accomplished with open borders and weak-willed politicians.

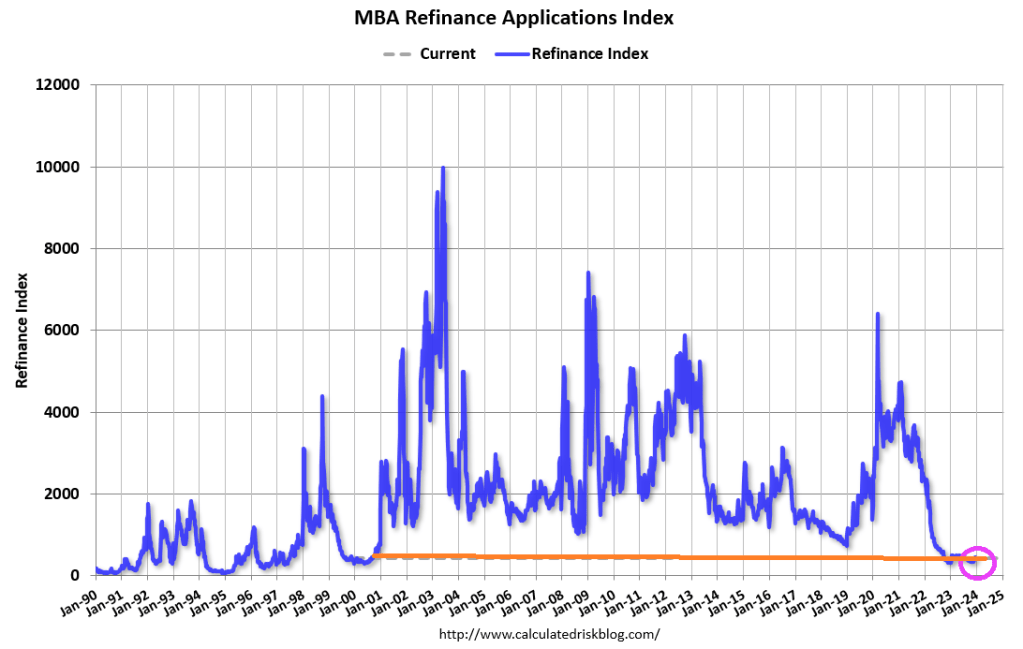

Mortgage applications decreased 1.5 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending December 15, 2023.

The Market Composite Index, a measure of mortgage loan application volume, decreased 1.5 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 3 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index decreased 4 percent compared with the previous week and was 18 percent lower than the same week one year ago.

The Refinance Index decreased 2 percent from the previous week and was 18 percent higher than the same week one year ago.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($726,200 or less) decreased to 6.83 percent from 7.07 percent, with points increasing to 0.60 from 0.59 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

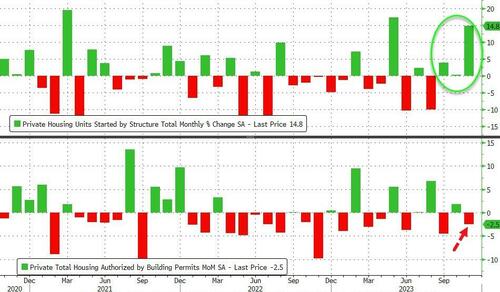

Housing Starts: Privately‐owned housing starts in November were at a seasonally adjusted annual rate of 1,560,000. This is 14.8 percent above the revised October estimate of 1,359,000 and is 9.3 percent above the November 2022 rate of 1,427,000. Single‐family housing starts in November were at a rate of 1,143,000; this is 18.0 percent above the revised October figure of 969,000. The November rate for units in buildings with five units or more was 404,000.

Building Permits: Privately‐owned housing units authorized by building permits in November were at a seasonally adjusted annual rate of 1,460,000. This is 2.5 percent below the revised October rate of 1,498,000, but is 4.1 percent above the November 2022 rate of 1,402,000. Single‐family authorizations in November were at a rate of 976,000; this is 0.7 percent above the revised October figure of 969,000. Authorizations of units in buildings with five units or more were at a rate of 435,000 in November.

Median NEW home prices dropped -20% YoY.

1-unit housing starts exploded, but permits declined.

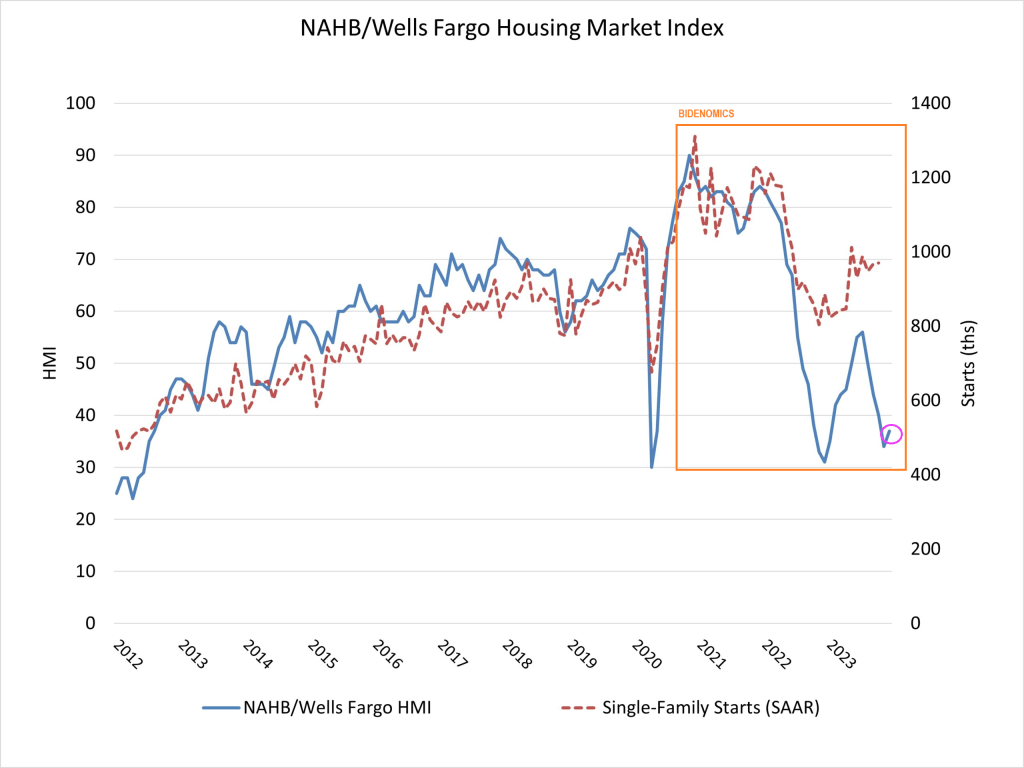

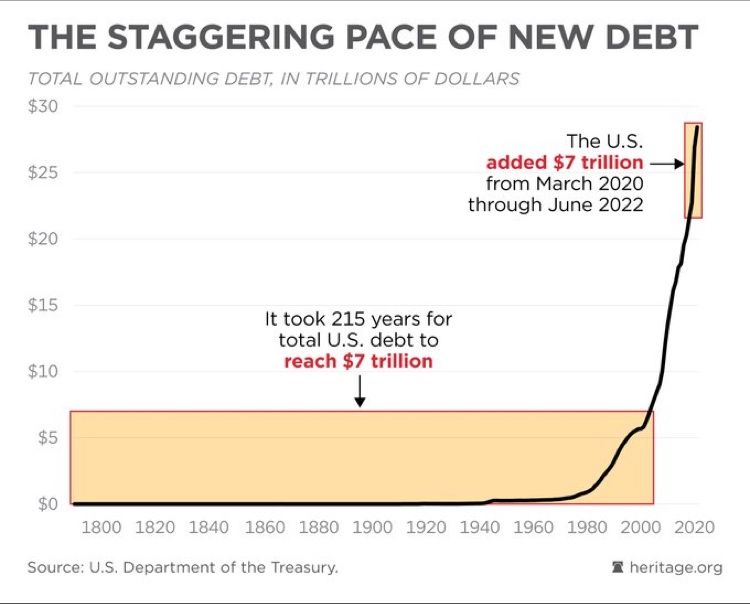

The Federal government added $7 trillion in debt since 2020 while it took 215 years to get to $7 trillion before Covid and Bidenomics.

In what can simply be called fiscal insanity, The Federal government is borrowing like there is no tomorrow (given that Biden is 81 years old, this isn’t far off) displacing businesses and households. Heaven help us if the Federal government has to borrow more money to fight a real war like World War II.

So, the massive Federal debt gorging isn’t helping the housing market.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.