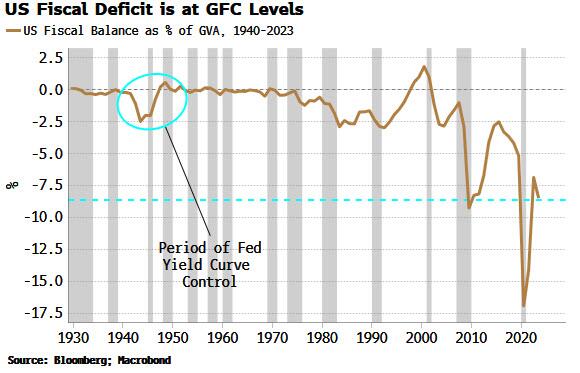

First, the deficit. It’s close to historical wides, bigger than it’s ever been outside of a recession, and almost as wide as it was in the depths of the GFC. It’s the largest in the world in GDP terms, and it is currently heading in the wrong direction. This heaps more pressure on the government debt-to-GDP level, already uncomfortably high at 112%.

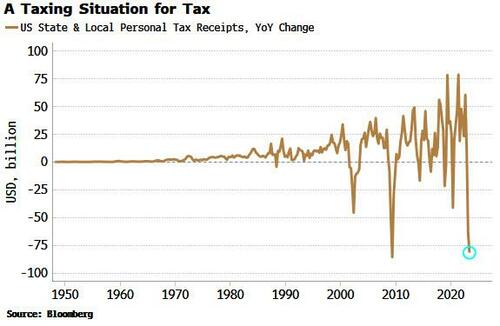

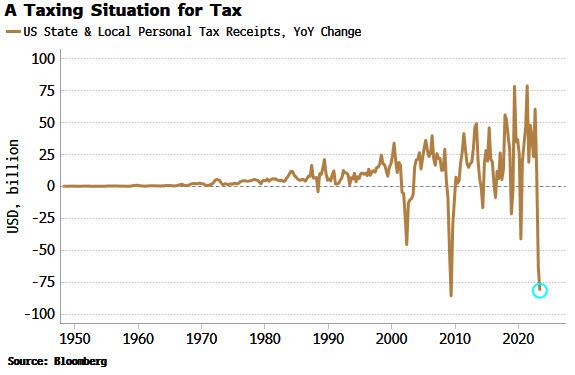

Second, tax revenues. These have seen almost their largest annual fall ever, in an economy that’s supposed to be growing at 2.4%.

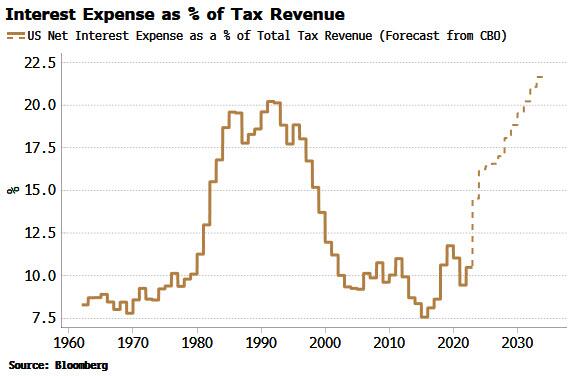

And then there’s rising interest-rate costs. The total interest expense as a percentage of tax revenue is expected to rise sharply in the next year or two, and make new highs by the end of the decade. However, these CBO forecasts should be taken with a grain of salt as they are based on a 10-year yield of only 3.8% (the ten-year average has been higher than that in every decade bar the 2010s and 2020s).

My former student at University of Chicago’s MBA program, Kevin Smith of Crescat Capital, has this charming chart of state and local income tax receipts collapsing.

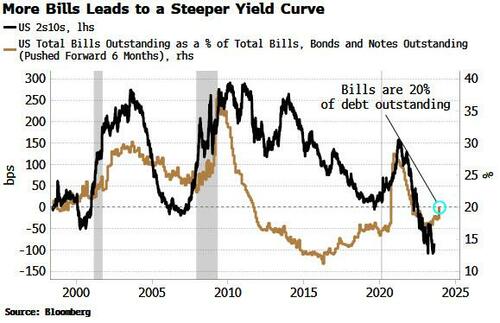

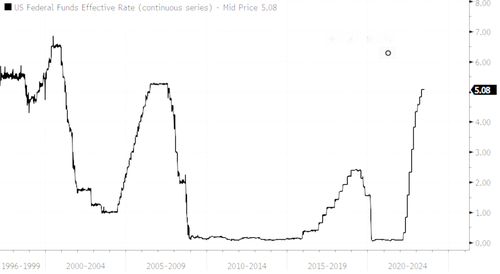

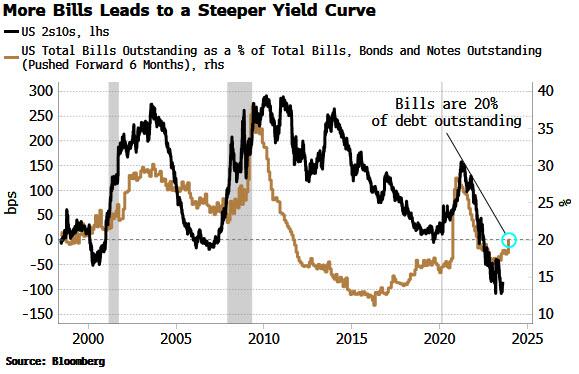

There is a view the Treasury is already implementing YCC, based on the fact it has been skewing its issuance towards bills and away from coupons. But issuing more bills is simply the easiest and fastest way for the Treasury to replenish its account at the Fed (the TGA). It was run down to almost zero in the lead-up to the debt-ceiling limit, and has now risen to over $500 billion.

This level of bill issuance is not unusual. The Treasury has an implicit target of about 20% for the amount of bills outstanding as a percentage of total debt. As we can see from the chart below, bills have often been more than 20% of debt outstanding over the last 30 years. Moreover, the Treasury announced this week it was raising its coupon-issuance amounts.

According to the stealth YCC thesis, less longer-dated Treasury issuance implicitly caps longer-term yields, but this has not historically been the case. As the chart above shows, the yield curve typically steepens – not flattens – when there is greater bill issuance – the opposite of what is desired by YCC.

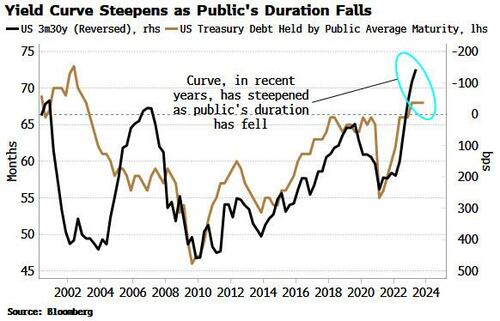

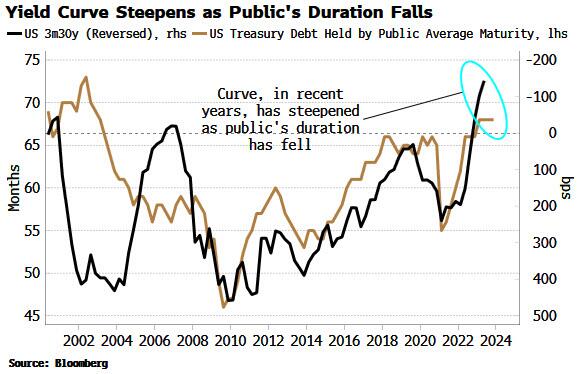

We see the same relationship if we look the duration of US government debt outstanding. When the average duration falls – as it would if issuance is skewed toward bills – the yield curve tends to steepen. The current average duration held by the public is consistent with a steeper, not a flatter, yield curve.

This sounds counter-intuitive. If issuance drives yields, then more issuance at the front-end of the curve versus the longer end – equating to a fall in duration – implies the yield curve should flatten.

But the fact the relationship is the other way implies it’s likely that demand is the more dominant driver of yields in the medium term. There is ready-made demand for bills, from MMFs, etc, so when supply increases, demand rises to meet it, suppressing the yield-curve impact.

It’s thus hard to argue the Treasury is engaging in yield curve control. But that does not detract from the rising possibility it will need to be implemented in some shape or form eventually.

Banks and the Fed are reducing their Treasury holdings, while foreigners now collectively own about $5 trillion less USTs – about 10% – than they did in 2021. At the same time the “Treasury put” means large fiscal deficits are likely to become a feature, not a bug. That means inflation is likely to become embedded.

Fiscal profligacy and elevated price growth are a combustible mix and a road to prohibitively high yields via rising term premium. Yield capping thus starts to look like the endgame.

How it’s done is another matter, whether it’s the Fed co-opted to cap yields as it was in WWII, Treasury buybacks, or financial repression, whereby domestic institutions are forced to hold more government debt. Whatever way, at some point yield curve control in the US is becoming increasingly likely – by stealth or otherwise.

But never fear! Janet “Too Low For Too Long Creating Asset Bubbles” Yellen is still US Treasury Secretary.

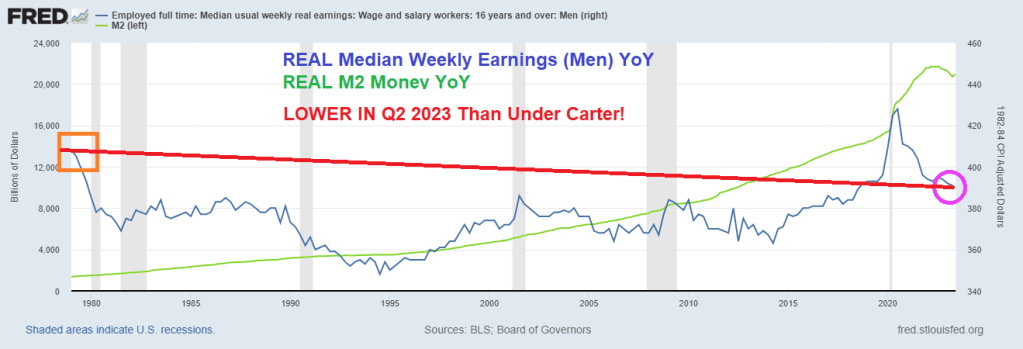

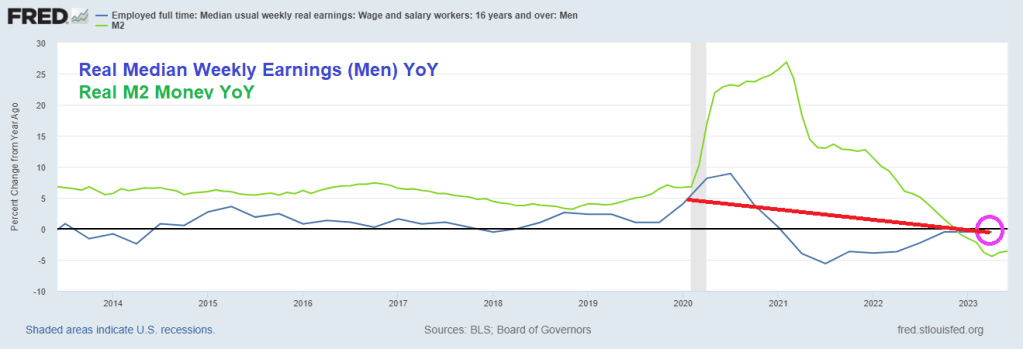

President Jimmy Carter is usually the bar for terrible Presidents. Under Carter, the US experienced economic stagnation and soaring inflation. At least it led to the election of Ronald Regan!

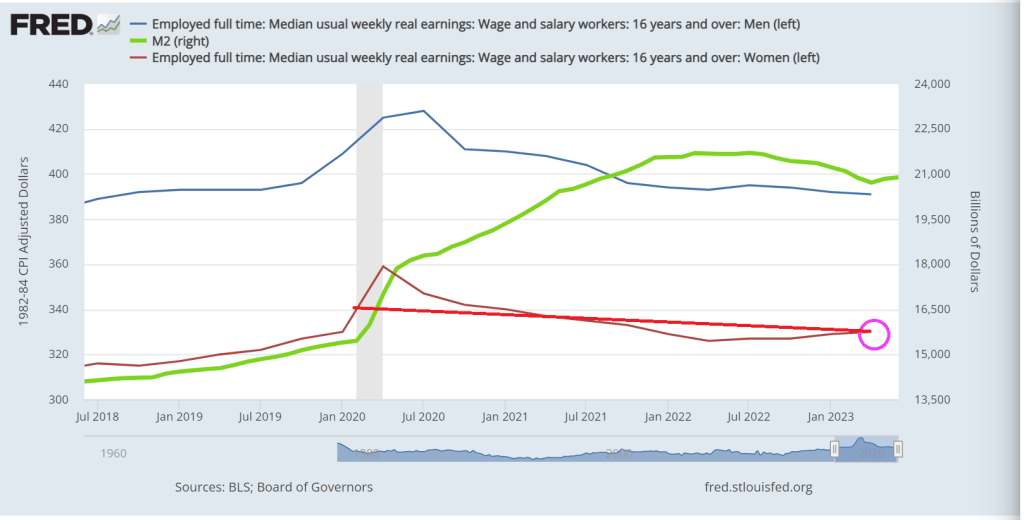

So, Biden’s much mentioned Bidenomics have produced REAL MEDIAN WEEKLY EARNINGS FOR MEN that is currently below 1979 levels under Jimmy Carter.

Even worse for Bidenomics, REAL MEDIAN WEEKLY EARNINGS GROWTH FOR MEN was -4.45% In April 2023, while the last reading prior to Covid under Trump was 6.674% YoY in February 2020. So, Bidenomics isn’t even back to Trump levels for men.

I like this chart which I call “Yellenomics” because it illustrates The Fed’s Folly of money printing and its impact on real earnings. After the Trump wage growth boom, real median weekly earnings for men has been steadily declining.

Women, on the other hand, did show a gain since Carter, but still lower than the last month before Covid struck. Women’s real median weekly earnings growth YoY since Q2 2021 are down -5%. So, Bidenomics has been less sucky for women than men.

Reminds me of The Yardbird’s classic “I’m A Man.” Worse off under Biden than under Jimmy Carter. Although The Yardbird’s “Over Under Sideways DOWN” is more emblematic of Bidenomics.

Bidenomics should be renamed Corruptionomics given Biden’s habit of selling government influence to anyone willing to waive a few million.

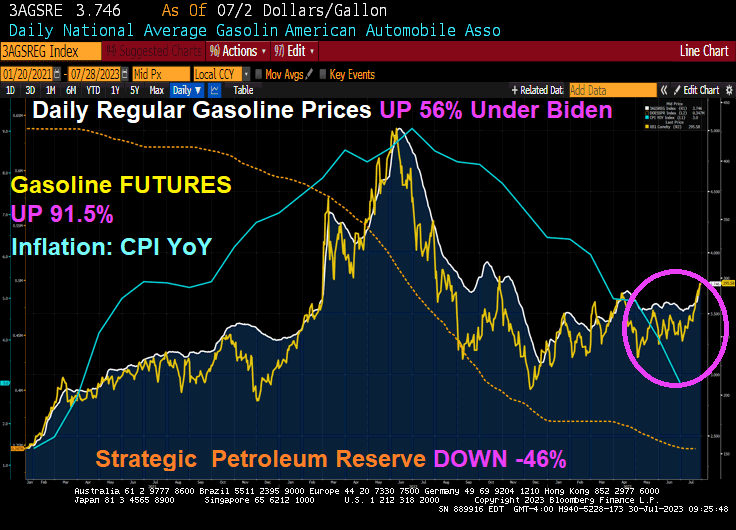

Joe Biden said that Republicans will impeach him in the House of Representatives since inflation is coming down. Huh? No Joe, it is because your are the most corrupt President in history, a compulsive liar and your economic policies are pure World Economic Forum mandates (open borders, Central Bank Digital currency, green energy, etc). Biden started off his Presidency by declaring war on fossil fuels that helped drive prices through the roof. And the middle class are paying the price.

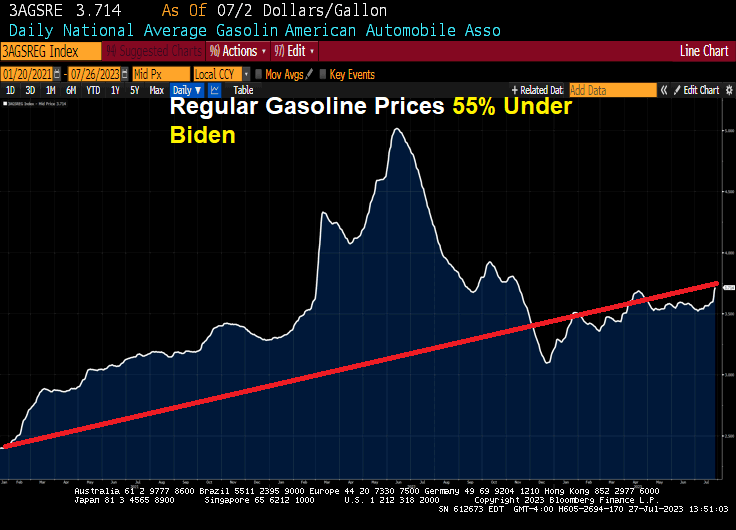

But as inflation cools (blue line) thanks in part to Biden draining the Strategic Petroleum Reserve (orange line), Biden can gloat. But remember, gasoline prices remain 56% higher under Biden’s Reign of Error. Even worse, gasoline FUTURES are up 91.5% under Biden. Yikes!

But look at how gasoline prices and gasoline futures have risen in July (pink circle). The last inflation report showed that inflation has declined to 3% (still higher than The Fed’s 2% target), gasoline prices are up almost 5% since July 19, 2023.

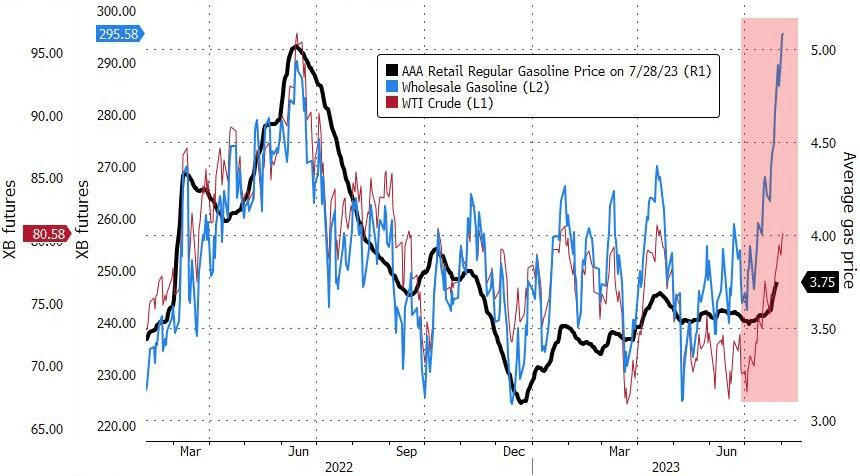

Gasoline, meanwhile, started the year at less than $2.50 per gallon. This week, gasoline topped $2.90 per gallon and may yet reach $3.

WTI Crude Oil futures have broken through the $80 barrier … again. Heating oil futures are up 1.43% today with WTI Crude futures up 0.61%.

So as energy prices keep rising (and Biden’s EPA keeps issuing green energy edicts and fails to recognize that our power grid can’t support all the electric cars and trucks envisioned by the Obama/Biden green dreamers). As such, energy prices will keep rising and with it … inflation.

Commercial real estate (CRE), particularly office space, reminds me of the Arthur Brown tune “Fire!” except that Jerome Powell of The Federal Reserve is the God of Hellfire! While fighting inflation caused by … The Federal Reserve and insane Federal spending (aka, Bidenomics). Call this the Over, Under, Sideways Down economy. The top 1% are doing quite well, while the lower 50% of net worth households are struggling.

The Q1 2023 NCREIF Office property (value) index shows declining office value since Q2 2022 as The Fed began raising its target rate to combat inflation.

From Trepp, we have this shocking table showing the decline the average total value loss over the span of around a decade. The oldest buildings experienced the largest reduction in value of 60%, and the newest experienced the least (but quite substantial) reduction of 52%. Although the newest buildings performed the best relatively, their 52% value reduction is easily the most concerning, and displays truly how much distress is present in the office sector. This group has the highest percentage of Class A buildings, but its reduction value over the past decade is still approximately on par with buildings constructed over half a century prior. With north of $150 billion in securitized maturities beyond 2023, these trends set a gloomy tone for their future and the performance of office properties as a whole.

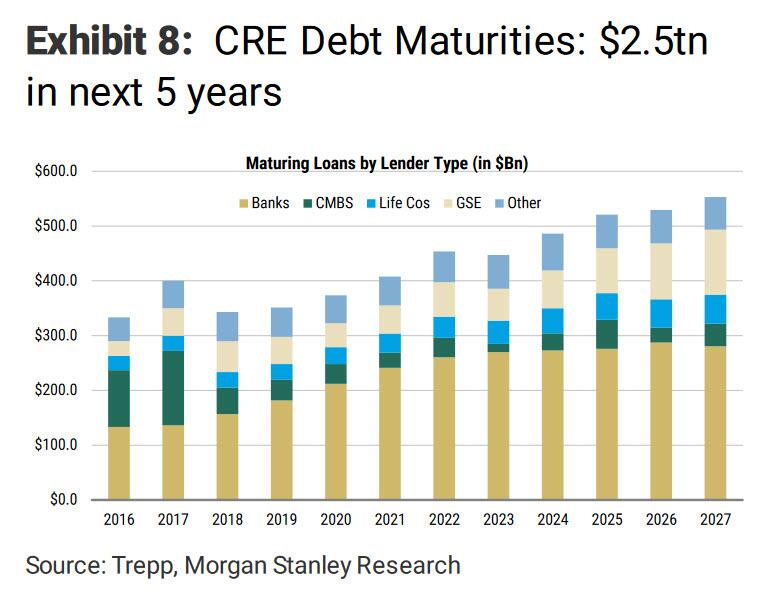

Then we have this alarming headline from Trepp: “Commercial Mortgage Sector Faces Another Wall of Maturities as $2.75 Trillion Rolls by 2027.” An estimated $528.7 billion of commercial mortgages mature this year, according to Trepp data, which projects that next year, maturities will increase to $532.8 billion. The projections are based on data for the first quarter compiled using the Federal Reserve’s flow of funds and made various assumptions regarding loan terms for each of the major lender categories. The data would indicate that the market is facing a wall, if not a mountain of maturities that would make the 2015-2017 wall of maturities look almost inconsequential. During that period, roughly $1.1 trillion of loans were scheduled to come due. But attention was focused on the CMBS market, as more than $335 billion of loans were set to mature during the period.

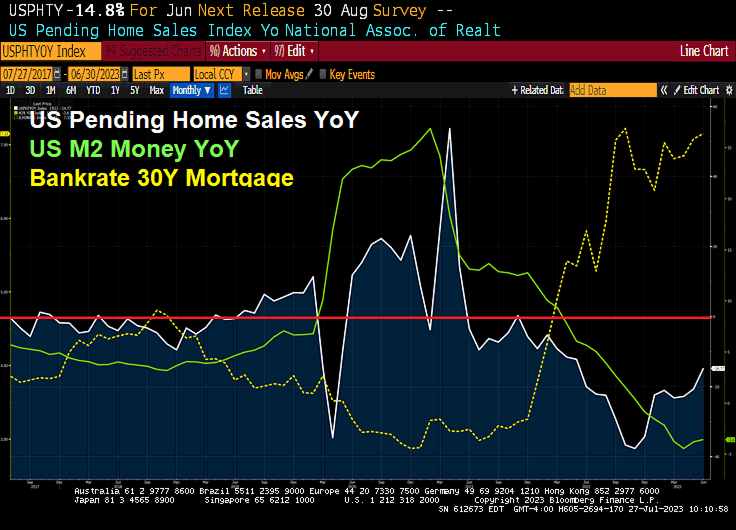

Well, REAL gross domestic income fell -0.8% YoY in Q1 2023 as M2 Money growth crashes. Not a good sign for the US economy or commercial real estate.

Of course, office properties are suffering from almost out-of-control crime in major American cities and the desire of workers to work from home rather than commute to work in cubicles.

But never fear! We have massively corrupt and compulsive liar Joe Biden as President!! He is the President of The 1%! Not the other 99%.

The Biden Administration is gushing about Q2’s Real GDP report of 2.4% QoQ. Wow, after trillions of dollars of stimulus spending and The Fed going wild with monetary stimulus, all we got was 2.4% growth??

Biden Press Secretary KARINE JEAN-PIERRE: “The American people are beginning to feel Bidenomics”

Prices are up 16.6% and real wages are down 3% since Biden took office.

Well, at least Jean-Pierre didn’t claim like her boss Joe Biden claimed that he “ended cancer as we know it.”

But getting back to Jean-Pierre’s claim that “The American people are beginning to feel Bidenomics.” She is right (for once). Americans are REALLY feeling Bidenomics. And it hurts SO BAD!!!

What hurts so bad? Food (CRB Foodstuffs) are up 56% under Bidenomics. Real weekly wage growth is down -90% since Biden assumed office. Regular gas prices are up 52%. And the 30Y mortgage rate is up a staggering 153%. Yes, Karine, this hurts so bad!

While real wages are down -3% under Biden and the real average weekly wage growth is down -90%. That REALLY hurts so good.

Starwood Capital Group’s Barry Sternlicht recently told Bloomberg’s David Rubenstein about the ongoing crisis in the commercial real estate sector, equating it to a severe “Category 5 hurricane“. He cautioned, “It’s sort of a blackout hovering over the entire industry until we get some relief or some understanding of what the Fed’s going to do over the longer term.”

Currently, the biggest problem in the CRE space is sliding office and retail demand in downtown areas. Couple that with high-interest rates, and there’s a disaster lurking for building owners. According to Morgan Stanley, the elephant in the room is a massive debt maturity wall of CRE loans that totals $500 billion in 2024 and $2.5 trillion over the next five years.

Senior markets editor for Bloomberg, Michael Regan, chatted with John Fish, who is head of the construction firm Suffolk, chair of the Real Estate Roundtable think tank and former chairman of the board of the Federal Reserve Bank of Boston, in the What Goes Up podcast to discuss the biggest problems in the CRE market.

Fish warned that “capital markets nationally have frozen” and “nobody understands value.” He said, “We can’t evaluate price discovery because very few assets have traded during this period of time. Nobody understands where the bottom is.”

For a sense of recent price discovery trends, we were the first to point out to readers of a wicked firesale of office towers in the downtown area of Baltimore City:

As for the overall CRE industry, Goldman Sachs chief credit strategist Lotfi Karoui recently told clients, “The most accurate portrayal of current market conditions with Green Street indicating a 25% year-over-year drop in office property values.”

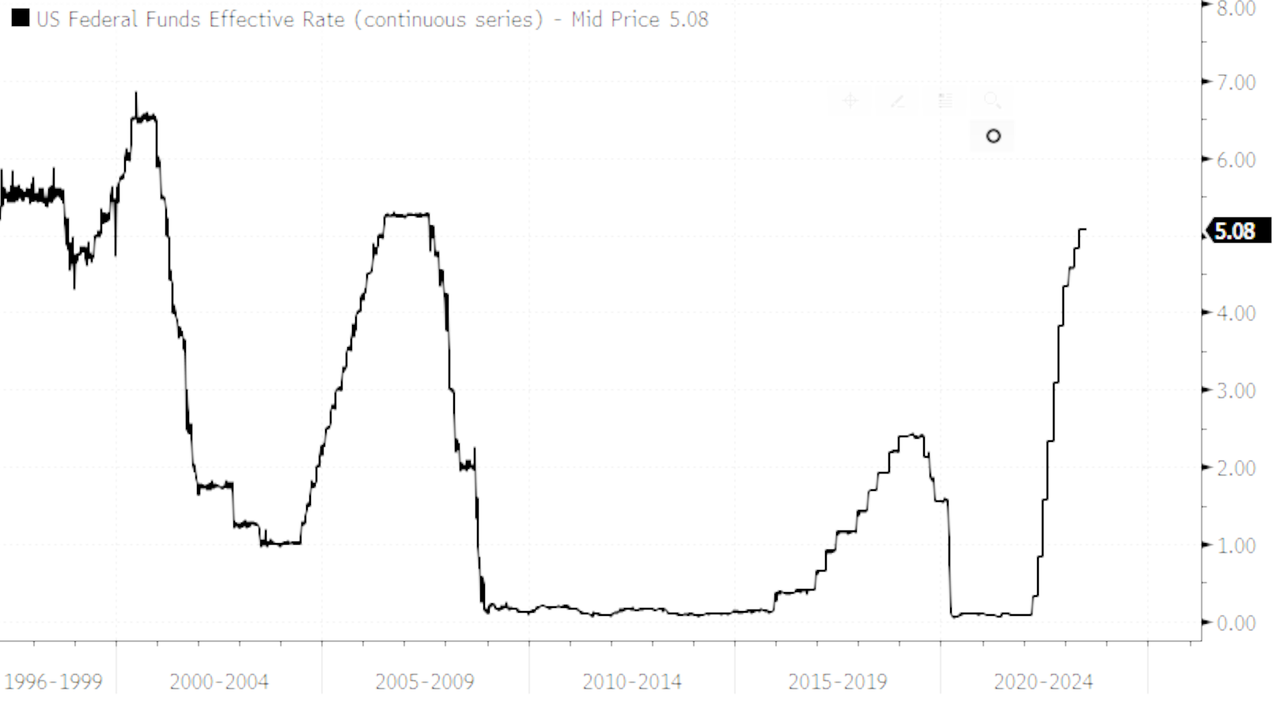

Sooooo, Powell and The Fed will likely raise rates this week. And maybe a few more times over the next few months. And The Fed remains defiant about taking away the Covid monetary stimulus.

US office space vacancies (white line) have soared since 2008 as The Fed’s massive monetary expansion (blue and green line) has not helped. But Fed monetary expansion DID help drive office prices! At least until 2022, when office space values began to fall. Notice that office values are falling as The Fed withdraws monetary stimulus.

During the regional bank failures in March, we directed our readership to focus on the next potential crisis: “CRE Nuke Goes Off With Small Banks Accounting For 70% Of Commercial Real Estate Loans.”By late March, Morgan Stanley warned clients of an upcoming maturity wall in commercial real estate, which amounts to $500 billion of loans in 2024, and a total of $2.5 trillion in debt that comes due over the next five years.

In a recent Bloomberg interview, Barry Sternlicht’s Starwood Capital Group warned that the CRE space is in a “Category 5 hurricane.” He said, “It’s sort of a blackout hovering over the entire industry until we get some relief or some understanding of what the Fed’s going to do over the longer term.”

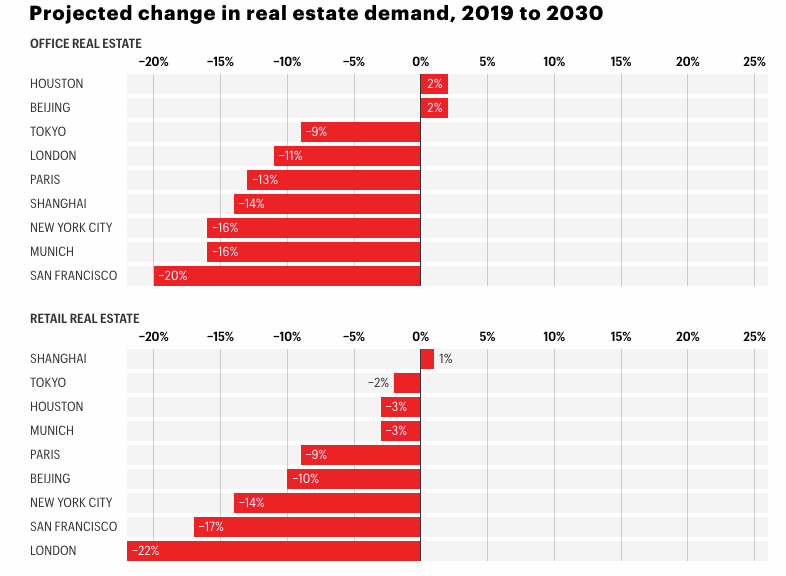

The current downturn in CRE could persist for years, if not through the end of this decade. Jan Mischke, a partner at the McKinsey Global Institute, along with Olivia White, a senior partner at McKinsey, and Aditya Sanghvi, a senior partner and leader of McKinsey’s real estate special initiative, published a note in Fortune, warning “$800 billion of office space in just nine cities could become obsolete by 2030.”

The authors of the report blame the CRE downturn on the “shift to remote and hybrid work prompted two further shifts in people’s behavior”:

First, many residents, untethered from their offices and therefore less fearful of long commutes, moved away from urban cores. New York City’s urban core (that is, the dozen densest counties in the metropolitan area) lost 5% of its population from mid-2020 to mid-2022. San Francisco’s urban core (San Francisco County, Alameda County, and San Mateo County) lost 6%.

Second, consumers began shopping less at brick-and-mortar stores–and far less at stores in urban cores, where people were now less likely either to work or to live. Foot traffic near stores in metropolitan areas remains 10 to 20% below pre-pandemic levels, but the differences between urban and suburban traffic recovery are substantial. For example, in late 2022, foot traffic near New York’s suburban stores was 16% lower than it had been in January 2020, while foot traffic near stores in the urban core was 36% lower.

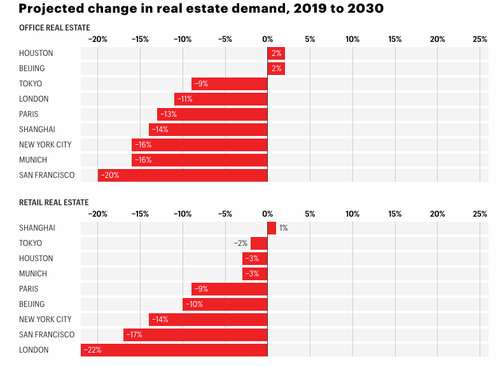

As fewer employees work in the office, demand for office space will fall. By 2030, such demand will be as much as 20% lower, depending on the city–even in a moderate scenario in which office attendance goes up but remains lower than it was before the pandemic.

And as fewer consumers shop at brick-and-mortar stores, demand for retail space will fall as well, according to our model. In the urban core of London, the hardest-hit city, demand for retail space will be 22% lower in 2030 than it was in 2019 in a moderate scenario.

Some of the most significant declines in office and retail space demand through 2030 will be in major US cities such as San Francisco and New York City.

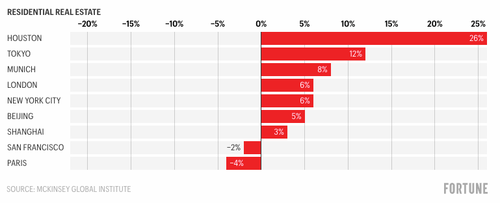

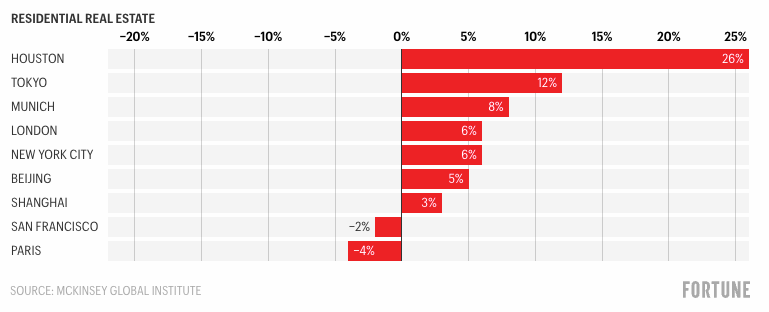

The authors note that the demand for “residential space will suffer less”… Well, according to their forecasting model.

“The reduced demand will have major impacts on urban stakeholders. For example, in just nine cities that we studied especially closely, $800 billion of office space could become obsolete by 2030. And macroeconomic complications could make matters even worse,” the authors continued. Without office workers in downtown areas, economic recoveries in major cities will be a “U” shape or, in some cases, an “L.”

The unraveling of downtowns is already underway. We shared a video this week of scenes of San Francisco’s downtown transformed into a ‘ghost town.’ Building owners in the crime-ridden metro area are already giving up and defaulting as vacancies rise, crime surges, and refinancing is near impossible in today’s climate as the Federal Reserve keeps interest rates sky-high to tame the worst inflation in a generation.

We shift our attention to Baltimore City, where office towers are being dumped in an apparent firesale.

The authors failed to report that the sliding demand for office towers isn’t just because of “remote and hybrid work” but also due to an exodus of companies fleeing crime-ridden progressive cities that fail to enforce law and order.

If McKinsey’s predictions are correct, certain segments of the CRE market are expected to experience prolonged turmoil for years. Some US mayors have proposed an immediate solution to convert office towers into multi-family units. However, this transformation could take years due to the time-consuming processes of obtaining permits and construction.

Yes, the maestros of real estate asset bubbles (Yellen) and eventual deflation (Powell)!

No, this isn’t a John Kerry/Greta Thunberg hysterical warning about climate change. But a storm created by 1) Biden/Congress spending splurge and 2) excessive monetary stimulypto by The Federal (Feral) Reserve. Now that The Fed is withdrawing the excess stimulus, we are seeing a world of pain for commercial real estate. A financial climate change!

“We’re in a Category 5 hurricane,” Sternlicht said in an interview on June 28 taped for a July 25 release in an upcoming episode of Bloomberg Wealth with David Rubenstein.

Sternlicht warned, “It’s sort of a blackout hovering over the entire industry until we get some relief or some understanding of what the Fed’s going to do over the longer term.”

He explained the CRE downturn was sparked by the Federal Reserve’s sixteen months of aggressive interest rate hikes to tame inflation — and unlike past downturns — not due to reckless speculation.

Tighter credit conditions following the regional bank crisis in March have made refinancing existing buildings exceptionally hard for landlords and come as vacancies rise.

Sternlicht recalled that his firm tried to obtain a bank loan for a small property not too long ago. He said his staff reached out to 33 banks, and only two came back with offers.

According to Morgan Stanley, the elephant in the room is a massive debt maturity wall of CRE loans that totals $500 billion in 2024 and $2.5 trillion over the next five years.

As we’ve seen in San Francisco, the inability to refinance as some properties sustain rising vacancies will pressure landlords to sell properties or walk away from them.

Sternlicht said there’s a very real possibility of a “second RTC” event playing out, referring to Resolution Trust Corp., the government entity that led the effort to liquidate assets of the savings and loan associations that failed three decades ago.

“You could see 400 or 500 banks that could fail,” he said. “And they will have to sell. It also will be a great opportunity.”

Sternlicht launched his real estate firm during the era of RTC, purchasing multi-family units and flipping them to billionaire Sam Zell 18 months later for triple the price.

Sternlicht said the Federal Deposit Insurance Corp would likely begin offloading CRE loans on Signature Bank’s books, which failed in March. He said, “The government’s going to prop up the value of that portfolio by providing very cheap financing to it.”

* * *

Transcript of the interview:

David Rubenstein:

Sometimes people are saying that the best investment opportunity now is distressed real estate debt — that you can buy the debt from banks at a discount. But do you think it’s too early for that?

Barry Sternlicht:

You know, we were gonna give back an office building. And they said, “Well, not so fast. If you want to, we’ll restructure the loan. And we’ll cut the loan in half. And you put the money in here. And we’ll take this as a junior note.” Because the banks don’t want the assets back. They’re not set up to carry these assets. It’s not their business.

So you’re beginning to see stuff. We’re going to see this big trade of the [Signature] Bank portfolio. That’s going to be a benchmark for market.

David Rubenstein:

A lot of fortunes were made in the real estate world in’ 07-’08 when people bought distressed real estate. The late ’80s too, when the RTC was here. Do you see funds being formed to buy these assets? But you think they won’t be available for a year or two?

Barry Sternlicht:

Right now you have an unusual situation in the real estate markets because everyone’s sort of looking at the yield curve. And it says rates will be lower later. Everyone says, “You know, survive till ’25. Hold onto your assets.” So transaction volumes have plummeted.

Unless you have to sell something today, nobody wants to sell anything today. They think tomorrow will be rosier. So for the most part, everybody’s pushing any sales back. But what you’re seeing is when a loan is maturing and a borrower can’t cover the current debt service. Something’s gotta give. Unfortunately, we’re also a lender.

David Rubenstein:

Are we going to change the way office buildings are really valued in the future because tenants aren’t going to need as much space? Or do you think eventually the tenants will come back and the employees will come back?

Barry Sternlicht:

The work-from-home phenomenon is a US phenomenon. If you go to England or Germany, rents are up, and vacancy rates in the top German property markets — Berlin, Frankfort, Munich, Hamburg — are less than 5%. People are back in the office. You and I go to the Middle East, they’re full. We have offices in Asia, they’re full. So this is a US situation.

In the US you have two markets. The nice buildings will stay rented and my guess is at pretty good rates. And the B and C stuff is going to be — maybe fields of grain or something. It’ll be very pretty. We’ll have all these little mid-block parks in New York City because there won’t be anything else to do with those buildings.

The other thing about office is AI. AI is going to hit a couple of these industries that have been big users of office space. So that’s sort of a big question mark in the investment equation.

David Rubenstein:

Let’s suppose I’m an average person. Where should I put my money as an investor in real estate?

Barry Sternlicht:

High interest rates are depressing the number of single-family home units that have been built so now you’re having an ever-increasing scarcity of residential. Given the cost of construction, the whole residential complex — including single-families for rent, multi-family, the housing market, even residential land — I think they make interesting investment opportunities today.

David Rubenstein:

Is it a good thing for people to now invest in a real REIT?

Barry Sternlicht:

I think real estate has a nice place in the balance sheet of any individual. In the pandemic, we raised a special-situations fund and bought 15 names in the REIT business, and we were up, like 70% at one point. We’re going to do that again. And if you take a long-term view, some of these are good companies with the wrong interest-rate environment. I wouldn’t even say they have the wrong balance sheet, but they are so out of favor. There are some really good buys out there. So if you’re clever, you could buy some public REITs.

David Rubenstein:

What kind of return should an average REIT investor expect?

Barry Sternlicht:

In the mortgage REIT, Starwood Property Trust, we’re paying a 10% dividend. So you get that and any appreciation in the stock, and the stock’s currently trading below book value. It usually trades above book value. It used to trade at 1.23 times and now it’s trading at .9. So if it reverts, you’ll get a 15% return. We’ve averaged 11.3% over 10 years.

David Rubenstein:

Why should somebody want a career in real estate? Why is that a good business to be in?

Barry Sternlicht:

You’ve got to find niches, and there are a lot of niches in real estate. And it’s very micro, block by block. If I didn’t have my firm today, could I buy — even in a city like New York — and redo apartments and housing. I could make money doing that. I have a friend of a friend who’s bought 300 homes. He turned living rooms into bedrooms, put them all on Airbnb. He’s earning a fortune and using Airbnb as his distribution set. It’s a giant industry. There’s always something to do.

David Rubenstein:

You were based in the northeast part of the US for much of your career. You grew up in Connecticut, you were born in Long Island. But you picked up and moved to Miami. Why did you do that a few years ago? And any regrets about moving to Miami?

Barry Sternlicht:

Well, my mom’s down there. And I got divorced. That was one reason. Change your life, start over. There was obviously a tax benefit to doing so. And I had sold an interest in my firm at the time. I was based in Connecticut. I was based in Greenwich, our headquarters was there. I looked at my travel calendar in a normal year and I was only home for about a third of it. So I didn’t think it’d be that hard to move and make that my base of operations. It turned I caught the wave perfectly.

I was an early settler into Miami. And, you know, the home prices probably tripled there. I should have bought everything with my house. I would have had the best-performing real estate fund in the world.

David Rubenstein:

If your mother came to you and said, “I have $100,000. I need to invest it somewhere. Where should I invest it?” You would say where, real estate?

Barry Sternlicht:

Today if you look at my portfolio, I have a significant amount of cash that I never had before because I’m getting 5% for the cash. Pretty soon I’m going to just start deploying that capital when I can see the sun coming through the clouds of the Fed’s movement. When the Fed basically tells you they’re done, I think real estate will catch a very firm bid.

Greta Kerry? John Thunberg?? They are the same repeater, and non thinker.

Here the real (financial) climate terrorists!! Yellen and Powell.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.