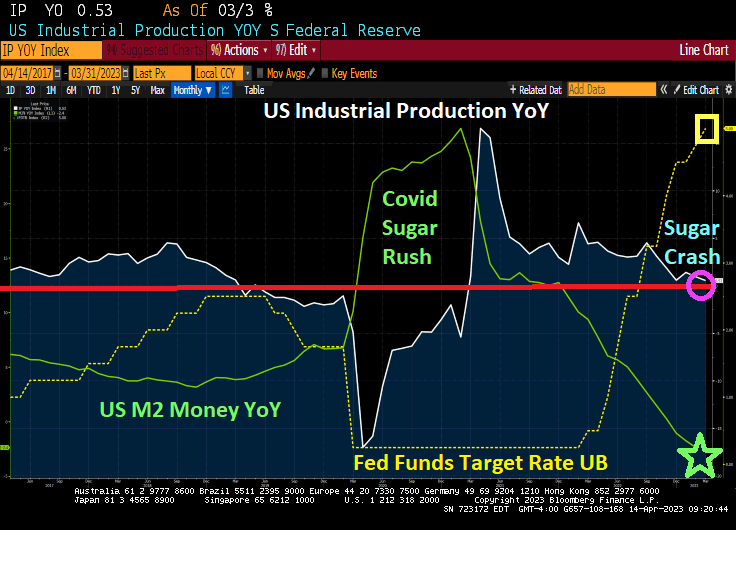

The US economy is barely chooglin along at a dismal 0.53% YoY (but 0.4% MoM in March). As the Covid “sugar rush” that caused a surge in Industrial Production in April 2021 of 16.56% has led to a “sugar crash” as M2 Money growth crashed and The Fed hiked rates to combat inflation. Known as a “sugar crash.”

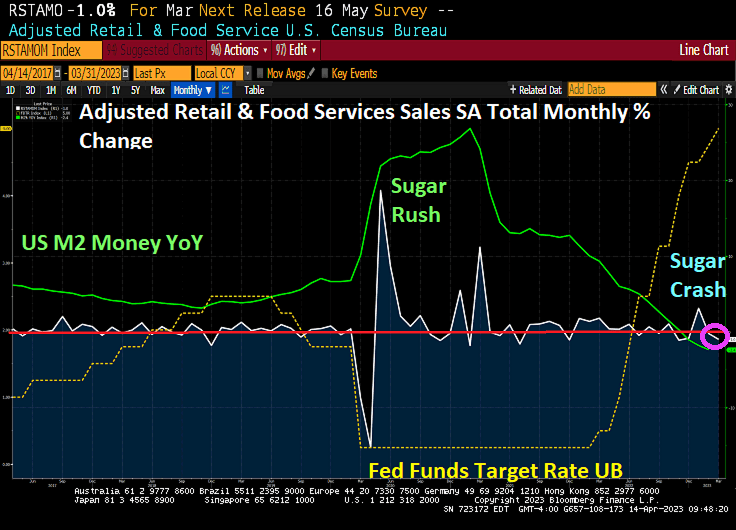

Also in today’s economic news is more Sugar Crash news. Advance retail sales dropped -1% in March. That is -155% lower than a year ago when it was +1.8%.

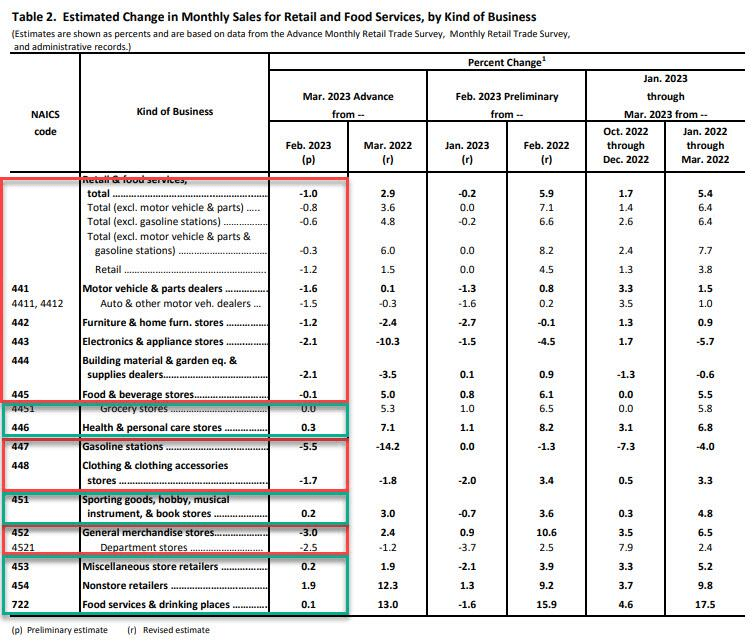

Here is the breakdown.

The Federal Reserve put a spell on us when Bernanke/Yellen kept rates too low for too long (TLFTL) and The Fed is now playing catch up. It is now creating havoc.

And on the Philly Fed’s Christopher “Fats” Waller saying that he favored more monetary policy tightening to reduce persistently high inflation, although he said he was prepared to adjust his stance if needed if credit tightens more than expected, we see that US Treasury 2-year yield jumping 13.5 basis points to 4.103%.

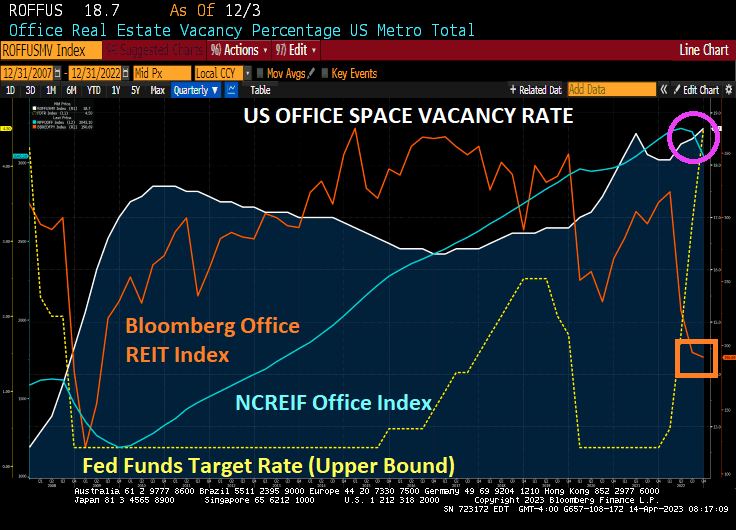

Office vacancy rate in the US has climbed to 20.2% in 2023

Financing for residential building is tepid despite demand

The Covid economic shutdowns have a disastrous effect on small businesses as we know. But office space is really getting crushed in terms of vacancy rates. In fact, it is so bad the investor Kyle Bass is suggesting that office space be torn down across the US much in the same way that FDR’s Agriculture Secretary Henry Wallace ordered the mass execution of hogs in order to drive up prices in a deflationary economy.

(Bloomberg) Kyle Bass has some advice for real estate investors: Tear it down.

The founder of Dallas-based Hayman Capital Management says office buildings in cities need to be demolished because demand isn’t returning and it’s impractical to turn most towers into apartments.

“It’s one asset class that just has to get redone, and redone meaning demolished,” said Bass.

The Dallas-based investor shot to fame more than a decade ago betting against subprime mortgages before the US housing collapse. He’s since pushed a series of contrarian investments that have occasionally burned investors such as predicting the collapse of Japanese government debt and Hong Kong’s dollar.

NCREIF’s office index is starting to decline, but Bloomberg’s Office REIT index (orange line) is really showing the pain being felt in the office market. But just wait to see what happens IF the market takes Bass’ advice and starts removing supply to help increase values. Unfortunately, my chart is only up through December 2022 and office vacancies have worsened in 2023 to a mind-boggling 20.2%.

In a classic Bill Lumbergh move (he was the office manager of Initech in Dallas Texas), JPMorgan now requires managing directors return to office 5 days a week and ‘be visible on the floor’ or else face ‘corrective action’.

An additional non-Bill Lumbergh issue is the rising crime in American cities causing companies like Whole Foods to leave their San Francisco (tenderloin district) location because 1) workers feel unsafe and 2) shop lifting is out of control. Even Washington DC where a large number of office building are leased by The Federal government is experiencing a boom in crime (particularly carjackings). And don’t get me started on Chicago (see Hey Jackass! for a Chicago crime map).

The face of micro-managing office managers, Bill Lumbergh. Or is this now JPMC’s CEO Jaime Dimon?

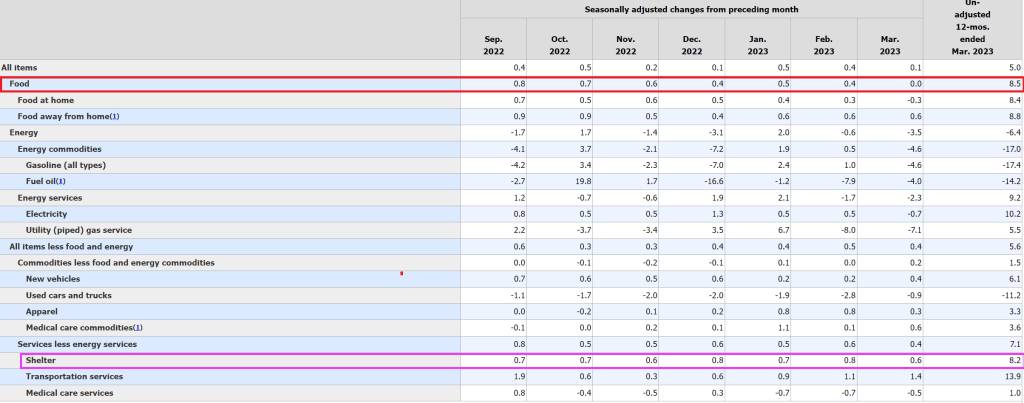

US Producer Price Index (PPI) final demand YoY fell to 2.7% in March as The Fed withdraws its massive monetary stimulus.

Final demand MoM fell -0.5% in March. But the interest number is CORE PPI ex food and energy actually down but at 3.6%. So, CORE PPI final demand growth is higher than the aggregate.

Do I detect a trend in US continuing jobless claims?

At least Biden is in Belfast Ireland making his usual gaffes, telling outrageous lies and looking totally lost. As usual. He can do less damage to the US by being in Ireland.

US Core inflation keeps rising despite The Federal Reserve slowing M2 Money growth and raising The Fed Funds Targget rate as The Fed plays catch up from Janet Yellen’s “Too Low For Too Long” monetary policies under Obama. And she was … negligent.

US Core Inflation (Core CPI YoY) rose to 5.6% in March despite The Fed cranking up their target rate and rapidly withdrawing M2 Money.

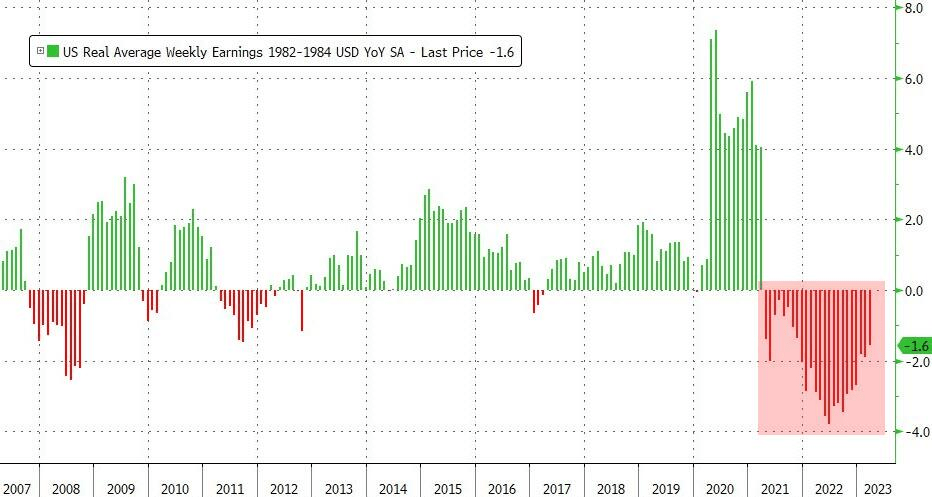

How about REAL wages? Real average weekly earnings growth has now been negative for 24 straight months.

One reason that core inflation is still rising is that The Fed still has not raised rates sufficiently. According to the Taylor Rule, the Fed Funds Target rate should be 11.77% based on core inflation of 5.6%. Hey, The Fed isn’t even half way there. It is like the Doolittle Raiders in World War II dropping their bombs 100 miles off the Japanese coast well short of their target.

Fed Funds Futures are pricing in one more rate hike (and a small one at that) before they resume cutting rates again.

Between inflation under Biden and The Fed’s counterattack to get inflation to 2%, I call this the Biden Blitz.

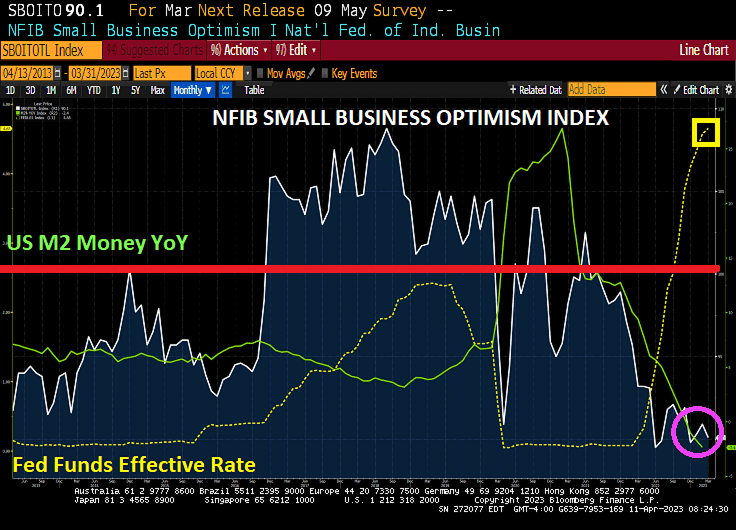

Unlike what the elites in Washington DC think, small business are the cornerstone of the US economy. Unfortunately, small business optimism is getting crushed and just fell in March to a level lower than that found during the Covid economic shutdowns of 2020. HOW is it possible for small businesses to be even less optimistic than it was in April 2002, the nadir of the Covid economic shutdown?

Small business optimism soared in November 2016 after the election of Donald Trump and remained high (above 100) until Covid struck in March 2020. Small business optimism rose above 100 again with the massive money printing by The Fed (green line) and Federal spending spree. But as M2 Money growth slowed, small business optimism hasn’t been above 100 since August 2021. It has been all downhill since then as The Fed started to raise The Fed Funds Target Rate quite rapidly.

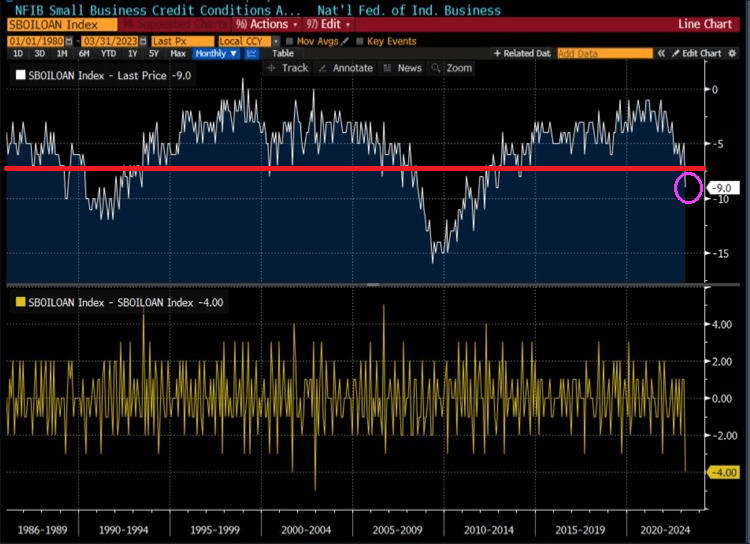

NFIB small business credit conditions are negative at -9.0 and sinking like The Titanic.

Biden is the face of big business (big banks, big pharma, big tech, big defense, big labor unions, big media, etc.). Biden just told Al Roker that he is indeed running for reelection, supported by …. big banks, big pharma, big tech, big defense, big labor unions, big media, etc.

Biden is no longer a President, but an old-time preacher screaming about MAGA Republicans as if they were demons. This is called Blitzkrieg Biden.

I read over the weekend that the Biden Administration was planning to unleash its army of social influencers on us to hype Biden’s economic accomplishments before the Presidential election. I am not one of his preferred social influencers. In fact, the US economy is slippin’ into darkness under Biden.

An example is ISM Manufacturing PMI which has declined to a level typically seen in prior recessions.

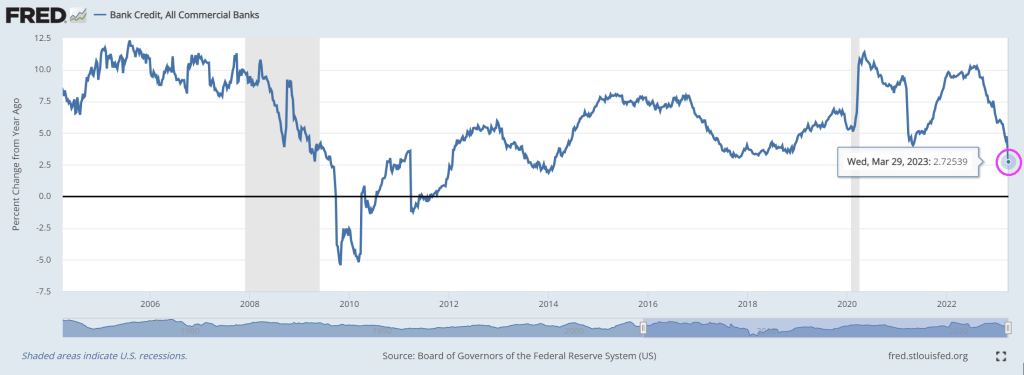

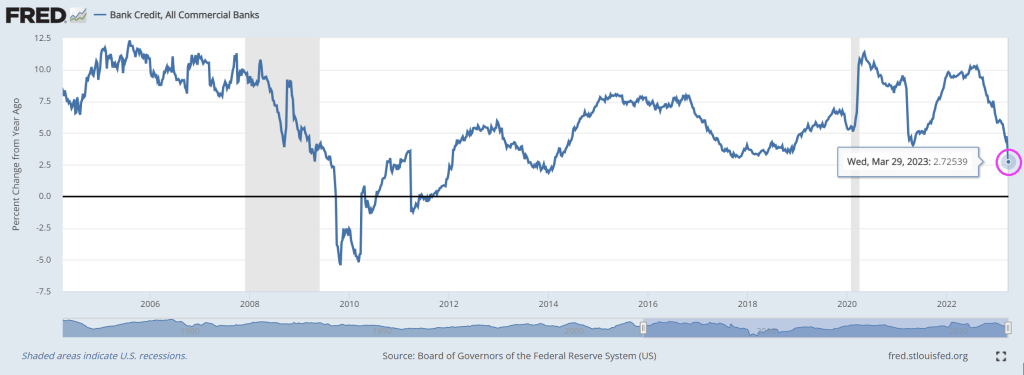

And then we have US bank credit growth which just crashed to the slowest growth rate since 2014.

Inflation started with Biden’s misguided war on US energy, then Biden/Congress helped inflation with an epic spending splurge. The Federal Reserve counterattacked with Fed rate hikes.

Over the past year, The Fed Funds Effective rate has risen and US bank credit has crashed to 2.73% year-over-year.

Do I detect a trend?

Since 2005, the crash in US bank credit is looking like 2008/2009 all over again.

Whether Biden is Cap’n Crunch or Jerome Powell or Janet Yellen, they are all crunching the US economy.

US commercial banks deposits (red line) had been slowly declining even before Silicon Valley Bank failed. Along with Signature Bank and First Republic Bank, not to mention Credit Suisse. And The Teutonic Titanic, Deutshe Bank, is on the ropes. But the failure of SVB saw an acceleration of the decline in commercial bank deposits as banks accelerated borrowing.

But never fear! The Fed will raise rates once or twice more, then drop them again.

“The banks will never behave on my watch as US Treasury Secretary, you have my word!” And don’t worry. Biden will bail them all out … again. Call it “The Biden Bailout Shake!”

Joe Biden loves to brag about “his” great economic successes, particulary in jobs added. But the jobs added in March were not in higher-paying factory jobs, but Biden’s building from the bottom-up approach is mostly low-paying leisure and hospitality jobs.

And here is the rub on wages. Average hourly earnings growth fell to 4.2% YoY, too bad inflation is 6% and expected to rise with the summer.

236k jobs added in March, down from a revised 326k jobs added in February. The unemployment rate fell to 3.5% and labor force participation rose slightly to 62.6%.

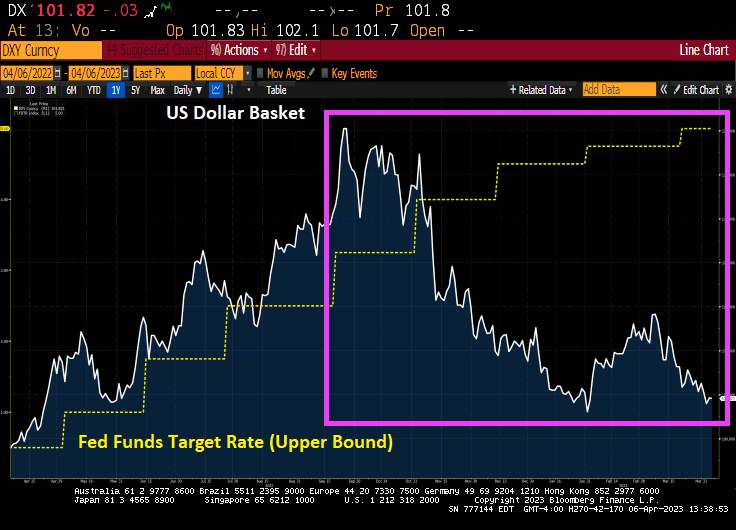

Biden, The Federal Reserve and insane Federal spending are killing King Dollar. Countries that used to use the US Dollar as reserve currency are dumping the dollar like a month old burrito.

What countries are dumping the dollar?

A lengthy list of countries are moving away from using the US dollar, which has long been the reserve currency of the world. The following countries are in the process of reducing their dependency on the dollar.

Russia

China

Iran

Brazil

Argentina

Saudi Arabia

UAE

India

The result?

Biden has vacationed 40% of the days he has been President. In his defense, he has probably needed that time to hunt down the classified documents has left strewn around his his home, vacation home, the Penn-Biden Center and Chinatown in DC.

You must be logged in to post a comment.